Embed Size (px)

Citation preview

Confidential

April 2008

PRELIMINARY | SUBJECT TO FURTHER REVIEW AND EVALUATIONThese materials may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with Credit Suisse.

Software 2008 Presentation Slides for CS Panel

Confidential

1

$1 $0

$3

$1 $1

$3 $2$1 $1 $1

$7

$5 $5

$3

$5

$9

$5$4

$19 $19

$2 $2 $1

$5

$2$4

$7

$0$0$0

10194

73

153

168

155

115

144

216

120

68

249

202

22 20 21

67

42

55

73

24

3 414

3816

35 3240 40

53

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Val

ue

of

Tra

nsa

ctio

n (

$BN

)

0

50

100

150

200

250

Nu

mb

er o

f Tra

nsa

ctio

ns

Q1’08

6

$0.4

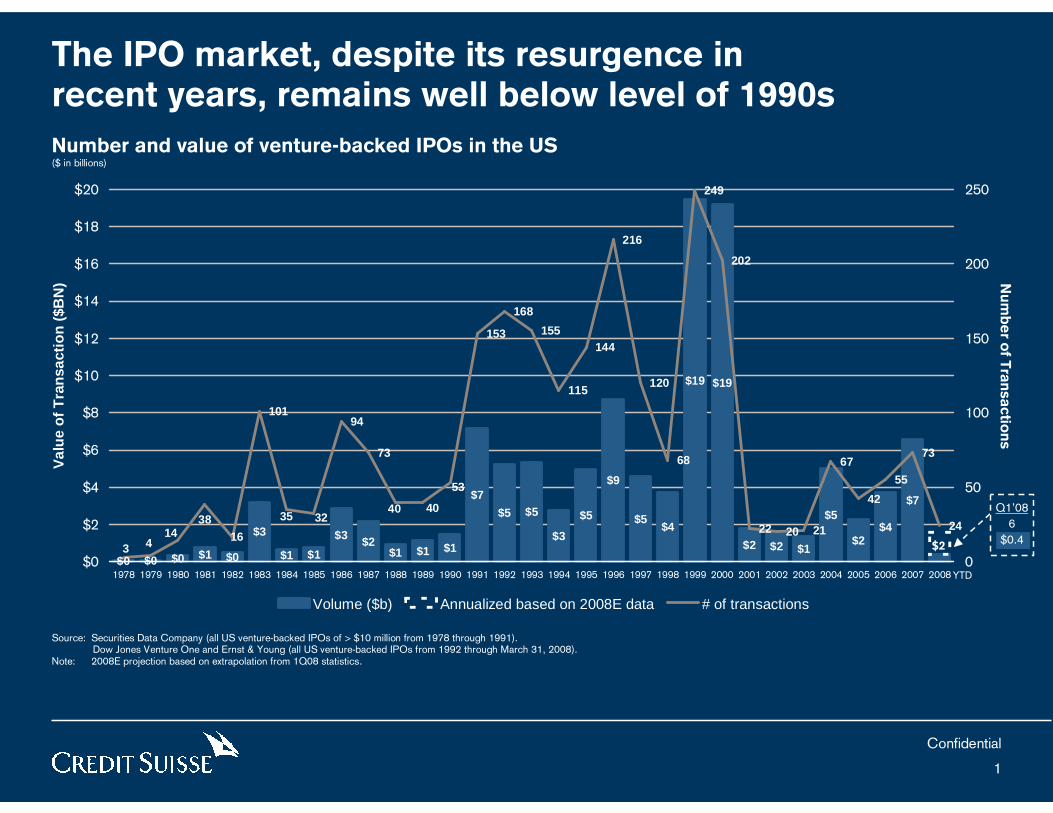

The IPO market, despite its resurgence in recent years, remains well below level of 1990s

Number and value of venture-backed IPOs in the US($ in billions)

Source: Securities Data Company (all US venture-backed IPOs of > $10 million from 1978 through 1991).Dow Jones Venture One and Ernst & Young (all US venture-backed IPOs from 1992 through March 31, 2008).

Note: 2008E projection based on extrapolation from 1Q08 statistics.

Volume ($b) Annualized based on 2008E data # of transactions

$2

YTD

Confidential

2

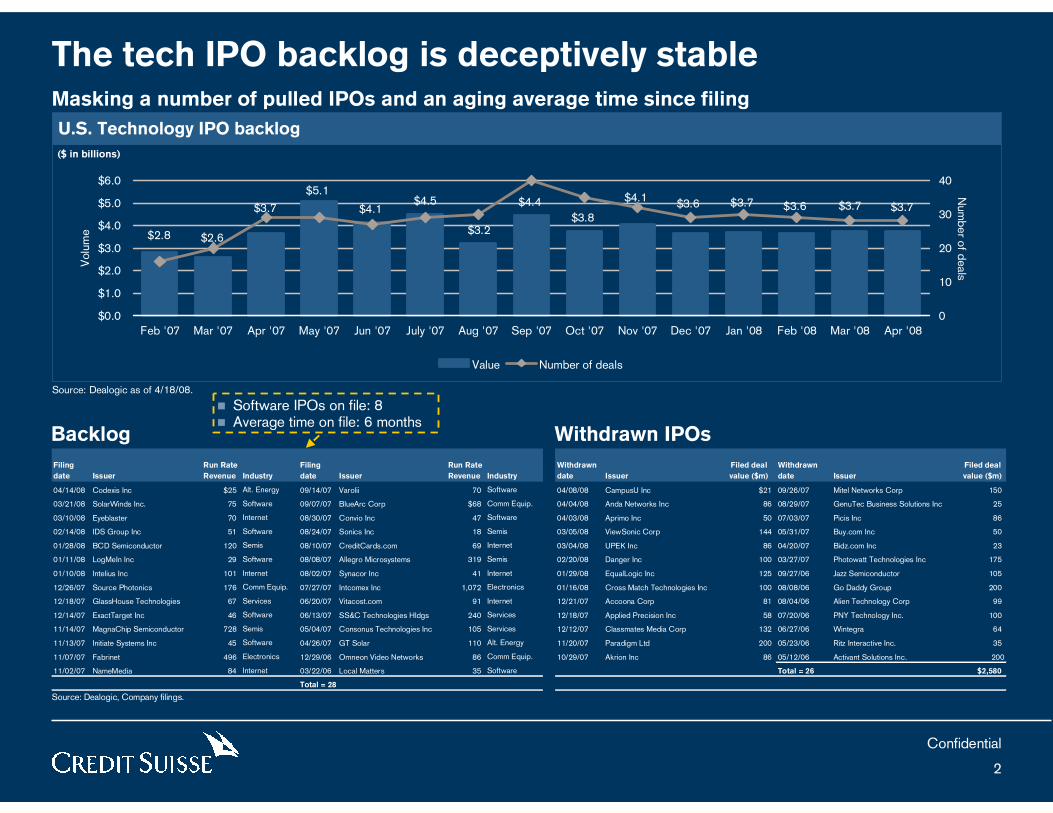

U.S. Technology IPO backlog

The tech IPO backlog is deceptively stable

Source: Dealogic, Company filings.

Masking a number of pulled IPOs and an aging average time since filing

Source: Dealogic as of 4/18/08.

$4.1$4.4

$3.8

$4.1

$3.2

$4.5

$2.6

$3.6 $3.7$3.6$3.7$5.1

$3.7 $3.7

$2.8

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

Feb '07 Mar '07 Apr '07 May '07 Jun '07 July '07 Aug '07 Sep '07 Oct '07 Nov '07 Dec '07 Jan '08 Feb '08 Mar '08 Apr '08

Volu

me

0

10

20

30

40

Num

ber o

f deals

Value Number of deals

($ in billions)

Backlog Withdrawn IPOs

Filing

date Issuer

Run Rate

Revenue Industry

Filing

date Issuer

Run Rate

Revenue Industry

Withdrawn

date Issuer

Filed deal

value ($m)

Withdrawn

date Issuer

Filed deal

value ($m)

04/14/08 Codexis Inc $25 Alt. Energy 09/14/07 Varolii 70 Software 04/08/08 CampusU Inc $21 09/26/07 Mitel Networks Corp 150

03/21/08 SolarWinds Inc. 75 Software 09/07/07 BlueArc Corp $68 Comm Equip. 04/04/08 Anda Networks Inc 86 08/29/07 GenuTec Business Solutions Inc 25

03/10/08 Eyeblaster 70 Internet 08/30/07 Convio Inc 47 Software 04/03/08 Aprimo Inc 50 07/03/07 Picis Inc 86

02/14/08 IDS Group Inc 51 Software 08/24/07 Sonics Inc 18 Semis 03/05/08 ViewSonic Corp 144 05/31/07 Buy.com Inc 50

01/28/08 BCD Semiconductor 120 Semis 08/10/07 CreditCards.com 69 Internet 03/04/08 UPEK Inc 86 04/20/07 Bidz.com Inc 23

01/11/08 LogMeIn Inc 29 Software 08/08/07 Allegro Microsystems 319 Semis 02/20/08 Danger Inc 100 03/27/07 Photowatt Technologies Inc 175

01/10/08 Intelius Inc 101 Internet 08/02/07 Synacor Inc 41 Internet 01/29/08 EqualLogic Inc 125 09/27/06 Jazz Semiconductor 105

12/26/07 Source Photonics 176 Comm Equip. 07/27/07 Intcomex Inc 1,072 Electronics 01/16/08 Cross Match Technologies Inc 100 08/08/06 Go Daddy Group 200

12/18/07 GlassHouse Technologies 67 Services 06/20/07 Vitacost.com 91 Internet 12/21/07 Accoona Corp 81 08/04/06 Alien Technology Corp 99

12/14/07 ExactTarget Inc 46 Software 06/13/07 SS&C Technologies Hldgs 240 Services 12/18/07 Applied Precision Inc 58 07/20/06 PNY Technology Inc. 100

11/14/07 MagnaChip Semiconductor 728 Semis 05/04/07 Consonus Technologies Inc 105 Services 12/12/07 Classmates Media Corp 132 06/27/06 Wintegra 64

11/13/07 Initiate Systems Inc 45 Software 04/26/07 GT Solar 110 Alt. Energy 11/20/07 Paradigm Ltd 200 05/23/06 Ritz Interactive Inc. 35

11/07/07 Fabrinet 496 Electronics 12/29/06 Omneon Video Networks 86 Comm Equip. 10/29/07 Akrion Inc 86 05/12/06 Activant Solutions Inc. 200

11/02/07 NameMedia 84 Internet 03/22/06 Local Matters 35 Software Total = 26 $2,580

Total = 28

� Software IPOs on file: 8� Average time on file: 6 months

Confidential

3

$10 $17 $34

$97$111

$153

$426

$588

$130

$54$77

$91

$144

$236

$281

35

382

228

164120

9565

809

327

196215

278

340

396

521

444

$0

$100

$200

$300

$400

$500

$600

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008YTD

Val

ue

of

Tra

nsa

ctio

ns

($B

N)

0

100

200

300

400

500

600

700

800

900

Nu

mb

er of T

ransactio

ns

Volume ($b) Annualized based on 2008E data # of transactions

$112

Q1’08

$28

111

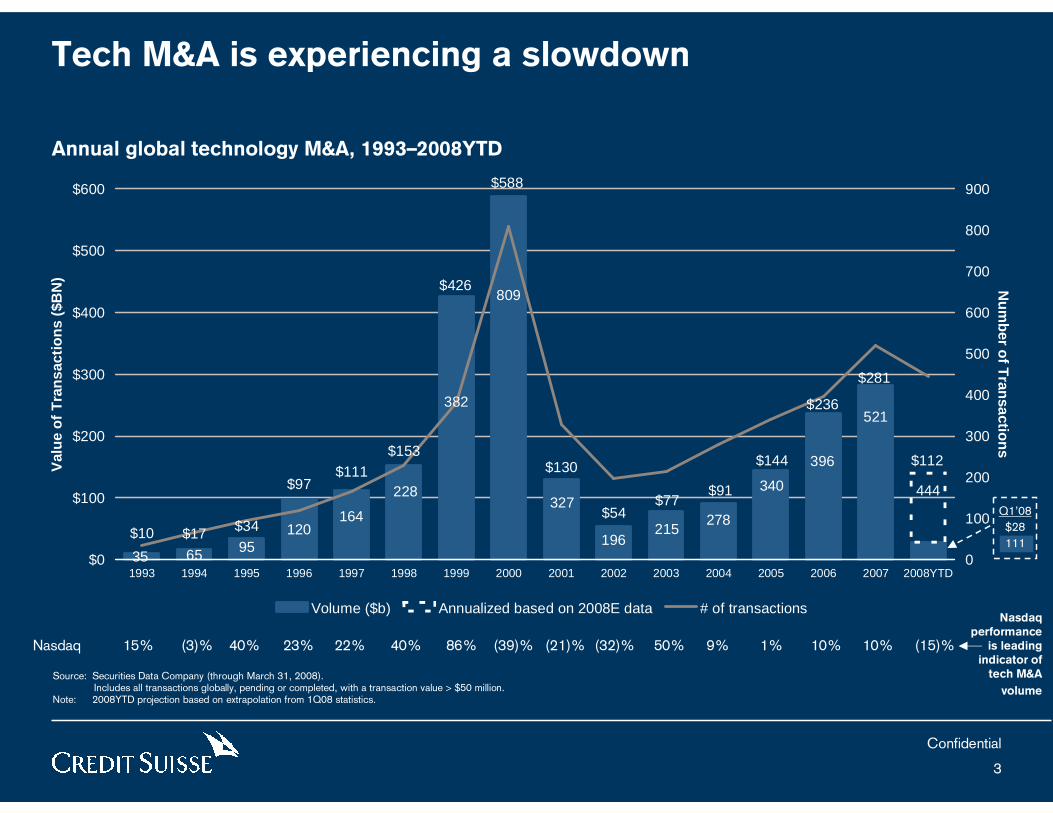

Tech M&A is experiencing a slowdown

Nasdaq 15% (3)% 40% 23% 22% 40% 86% (39)% (21)% (32)% 50% 9% 1% 10% 10% (15)%

Nasdaqperformance

is leadingindicator of

tech M&A

volume

Annual global technology M&A, 1993–2008YTD

Source: Securities Data Company (through March 31, 2008).Includes all transactions globally, pending or completed, with a transaction value > $50 million.

Note: 2008YTD projection based on extrapolation from 1Q08 statistics.

Confidential

4

69

53

77

38

48

25 28 3

4

32

16

24

17

7

22

74 77

77

70

43

71

18

14

10

24

14 19

8 5 17

12

13

16

8

18

13

24

11

27

12

37

25

5 5 4

8

4

9

1

6

2

6

50

20

40

60

80

100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

21

49

49

46 47 52

42

55

69

48

67

62 7

1

53

86

81 84

12

5

11

3

11

6

10

4

10

6

10

4

99

95

88

11

4

89 92

76 8

4

97

83

105

10

8

10

6

10

1

94 98 1

11

99 10

8

10

6

97

81

10

2

93 97 10

6

67

11

813

0

20

40

60

80

100

120

140

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

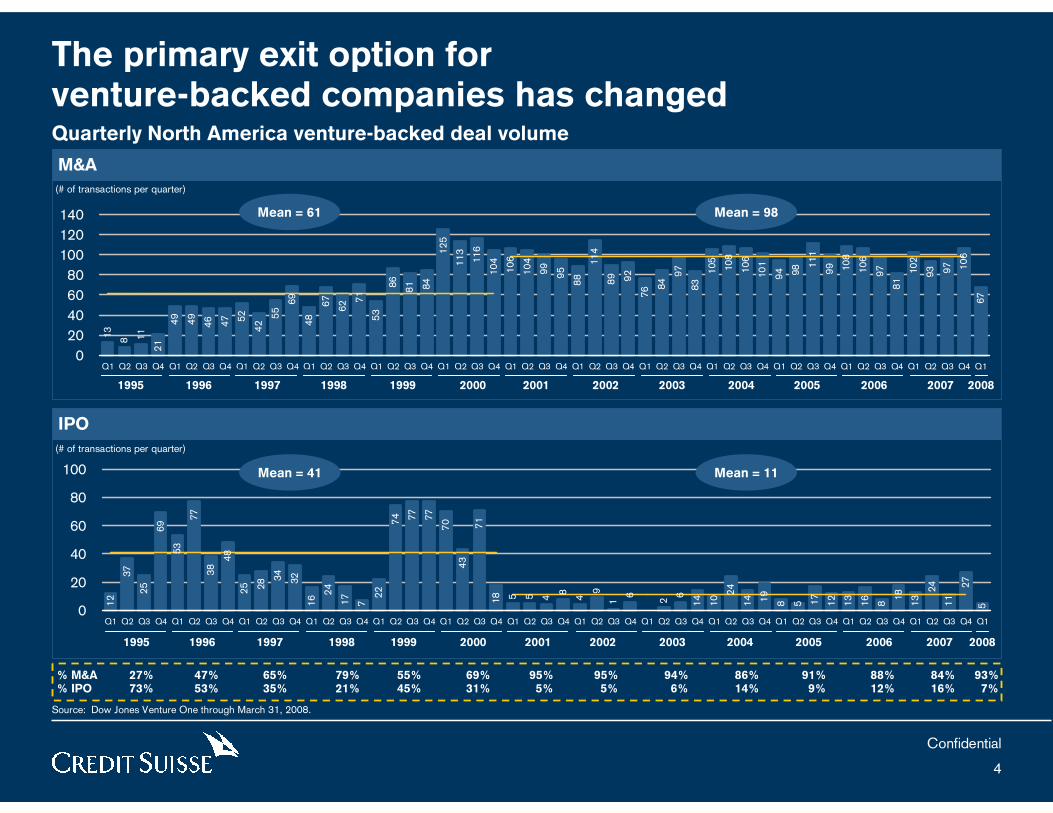

The primary exit option for venture-backed companies has changed

M&A

IPO

Quarterly North America venture-backed deal volume

Source: Dow Jones Venture One through March 31, 2008.

(# of transactions per quarter)

(# of transactions per quarter)

Mean = 61 Mean = 98

Mean = 41 Mean = 11

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

% M&A 27% 47% 65% 79% 55% 69% 95% 95% 94% 86% 91% 88% 84% 93%% IPO 73% 53% 35% 21% 45% 31% 5% 5% 6% 14% 9% 12% 16% 7%

Confidential

5

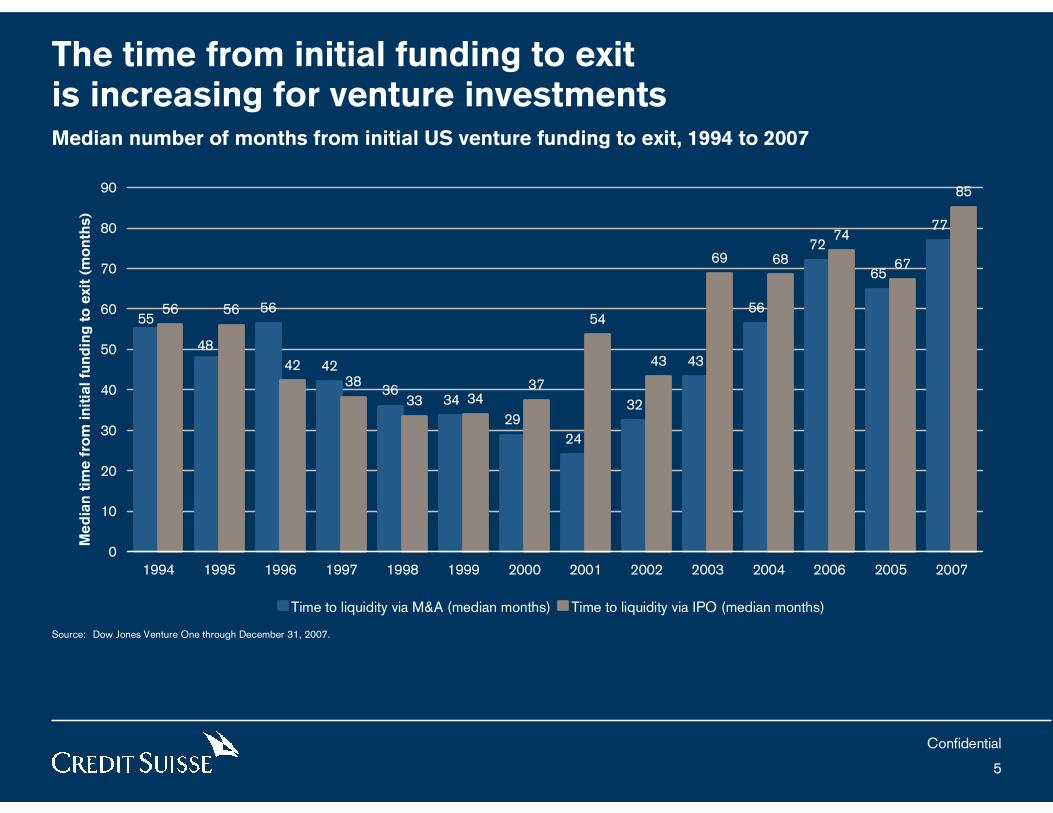

The time from initial funding to exit is increasing for venture investmentsMedian number of months from initial US venture funding to exit, 1994 to 2007

Source: Dow Jones Venture One through December 31, 2007.

56

42

3634

29

24

32

43

56

72

65

77

56 56

4238

33 3437

54

43

69 68

74

67

85

0

10

20

30

40

50

60

70

80

90

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2006 2005 2007

Me

dia

n t

ime

fro

m in

itia

l fu

nd

ing

to

exit

(m

on

ths)

Time to liquidity via M&A (median months) Time to liquidity via IPO (median months)

55

48

Confidential

6

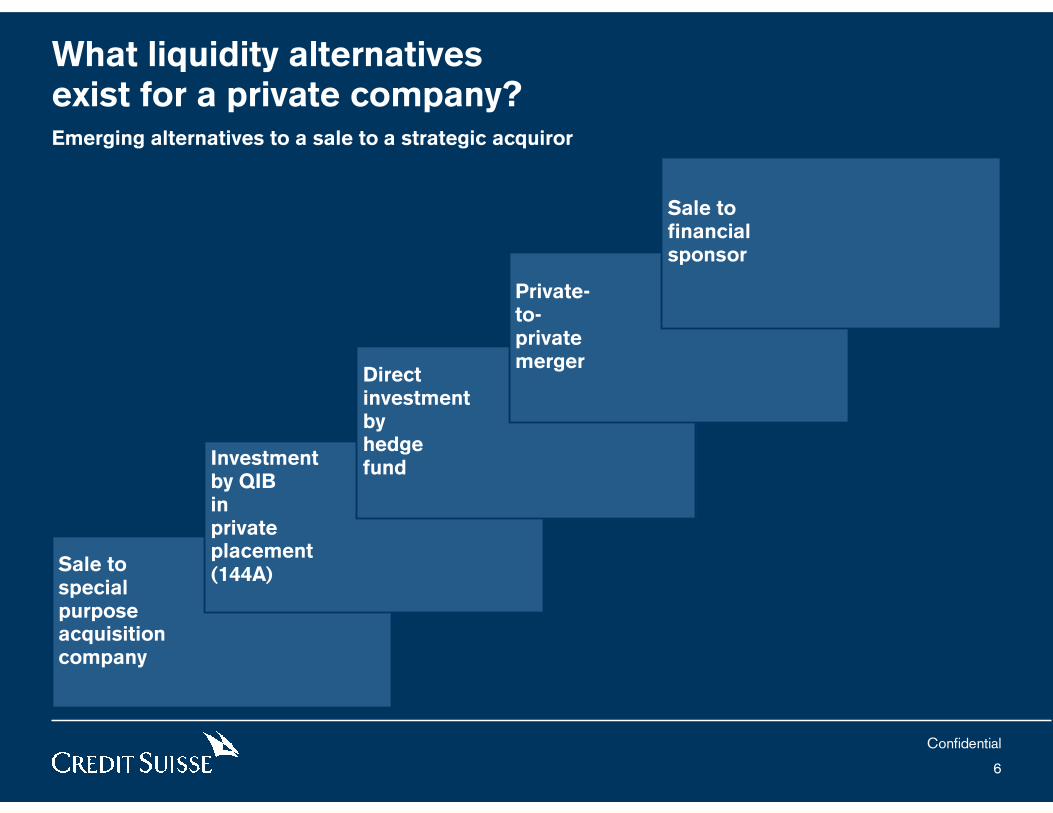

What liquidity alternatives exist for a private company?Emerging alternatives to a sale to a strategic acquiror

Sale tospecialpurposeacquisitioncompany

Investmentby QIBin privateplacement (144A)

Directinvestmentbyhedgefund

Private-to-privatemerger

Sale tofinancialsponsor

Confidential

7

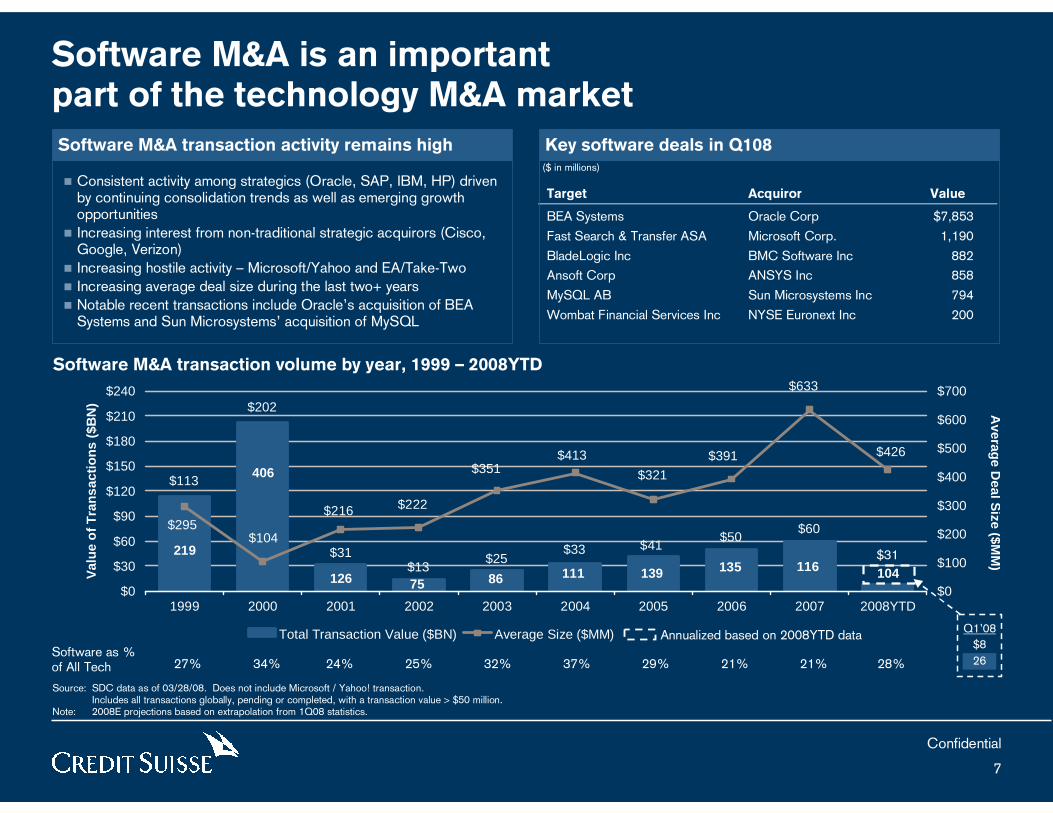

$60$50

$41$33$25

$13$31

$202

$113

$426

$633

$391

$321

$413$351

$222$216

$104$295

$0

$30

$60

$90

$120

$150

$180

$210

$240

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008YTD

Val

ue

of

Tra

nsa

ctio

ns

($B

N)

$0

$100

$200

$300

$400

$500

$600

$700

Total Transaction Value ($BN) Average Size ($MM)

Averag

e Deal S

ize ($MM

)

219

406

126 75 86 111 139 135 116 104

Target Acquiror Value

BEA Systems Oracle Corp $7,853

Fast Search & Transfer ASA Microsoft Corp. 1,190

BladeLogic Inc BMC Software Inc 882

Ansoft Corp ANSYS Inc 858

MySQL AB Sun Microsystems Inc 794

Wombat Financial Services Inc NYSE Euronext Inc 200

Software M&A is an important part of the technology M&A market

� Consistent activity among strategics (Oracle, SAP, IBM, HP) driven by continuing consolidation trends as well as emerging growth opportunities

� Increasing interest from non-traditional strategic acquirors (Cisco, Google, Verizon)

� Increasing hostile activity – Microsoft/Yahoo and EA/Take-Two� Increasing average deal size during the last two+ years� Notable recent transactions include Oracle’s acquisition of BEA

Systems and Sun Microsystems’ acquisition of MySQL

Software M&A transaction volume by year, 1999 – 2008YTD

Annualized based on 2008YTD data

$31

Software M&A transaction activity remains high Key software deals in Q108

Source: SDC data as of 03/28/08. Does not include Microsoft / Yahoo! transaction.Includes all transactions globally, pending or completed, with a transaction value > $50 million.

Note: 2008E projections based on extrapolation from 1Q08 statistics.

27% 34% 24% 25% 32% 37% 29% 21% 21% 28%Software as %of All Tech

Q1’08

$8

26

($ in millions)

Confidential

8

$509

$2,437 $2,429

$582

$3,938$4,254

$1,207

$3,011

$2,494

$1,257

$411

$766

$95

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

Q1 05 Q2 05 Q3 05 Q4 05 Q1 06 Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07 Q4 07 Q108

3 1

7 4

3

10 6

3

4 7

3

14

2% 3%

9%6%

11%

16%

13%15%

0%

5%

10%

15%

20%

2001 2002 2003 2004 2005 2006 2007 2008

YTD

$0 $1 $1

$4$6

$10

$7

$3

$0

$2

$4

$6

$8

$10

$12

2001 2002 2003 2004 2005 2006 2007 2008YTD

Annualized based on 2008YTD data

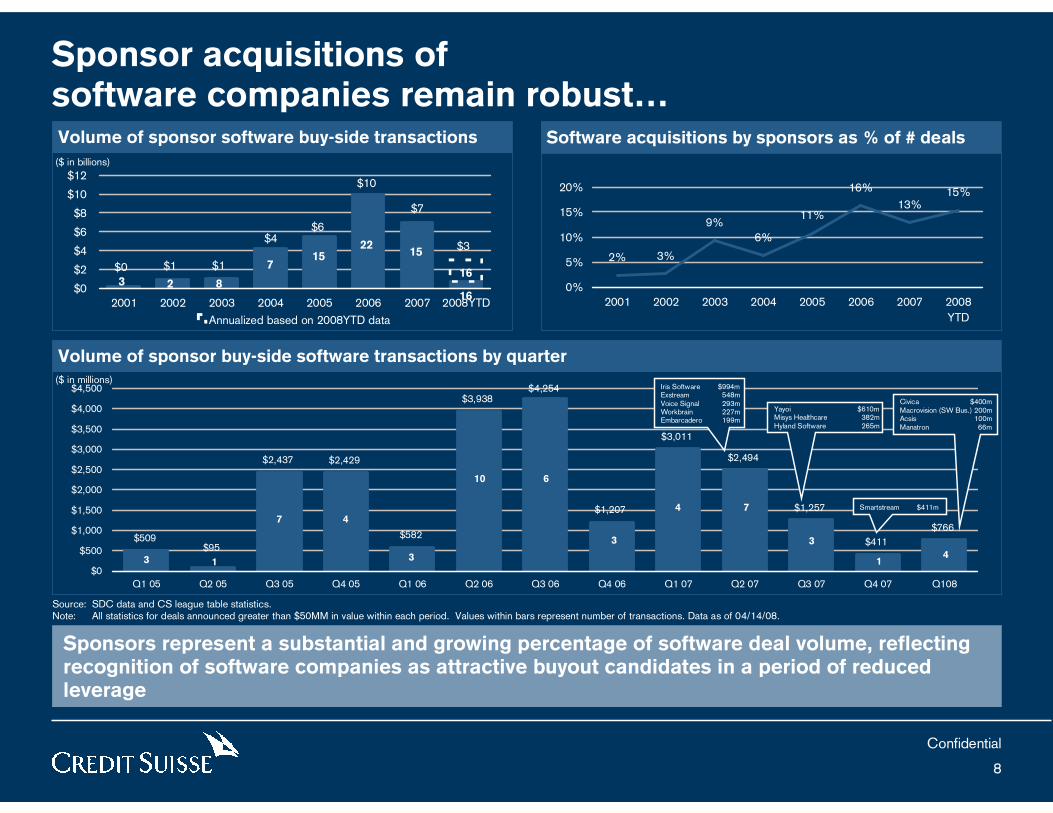

3 2 8

715

2215

16

16

Sponsor acquisitions ofsoftware companies remain robust…Volume of sponsor software buy-side transactions Software acquisitions by sponsors as % of # deals

Volume of sponsor buy-side software transactions by quarter

Sponsors represent a substantial and growing percentage of software deal volume, reflecting recognition of software companies as attractive buyout candidates in a period of reduced leverage

($ in billions)

Source: SDC data and CS league table statistics.Note: All statistics for deals announced greater than $50MM in value within each period. Values within bars represent number of transactions. Data as of 04/14/08.

($ in millions)Iris Software $994m Exstream 548mVoice Signal 293mWorkbrain 227mEmbarcadero 199m

Yayoi $610mMisys Healthcare 382mHyland Software 265m

Smartstream $411m

Civica $400mMacrovision (SW Bus.) 200mAcsis 100mManatron 66m

Confidential

9

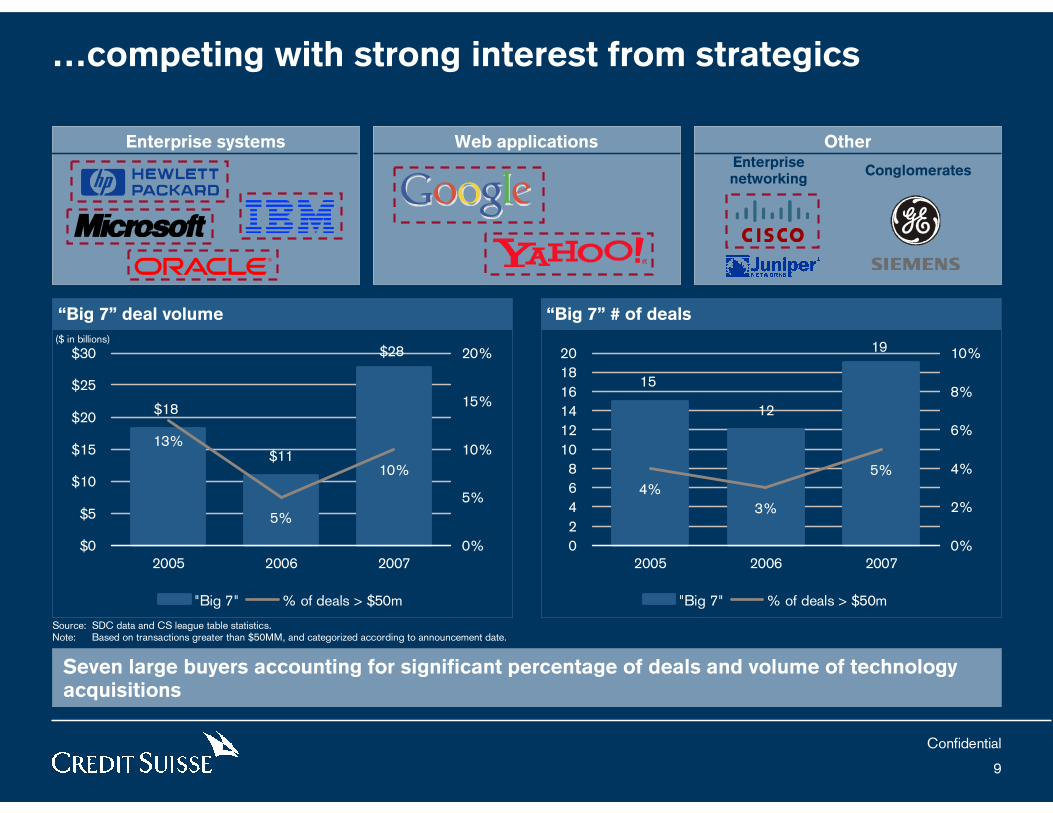

…competing with strong interest from strategics

Enterprise systems Web applications Other

“Big 7” deal volume “Big 7” # of deals

Seven large buyers accounting for significant percentage of deals and volume of technology acquisitions

$28

$18

$11

5%

10%

13%

$0

$5

$10

$15

$20

$25

$30

2005 2006 20070%

5%

10%

15%

20%

"Big 7" % of deals > $50m

($ in billions)19

15

12

3%

5%

4%

0

2

4

6

8

10

12

14

16

18

20

2005 2006 20070%

2%

4%

6%

8%

10%

"Big 7" % of deals > $50m

Source: SDC data and CS league table statistics.Note: Based on transactions greater than $50MM, and categorized according to announcement date.

ConglomeratesEnterprisenetworking

Confidential

10

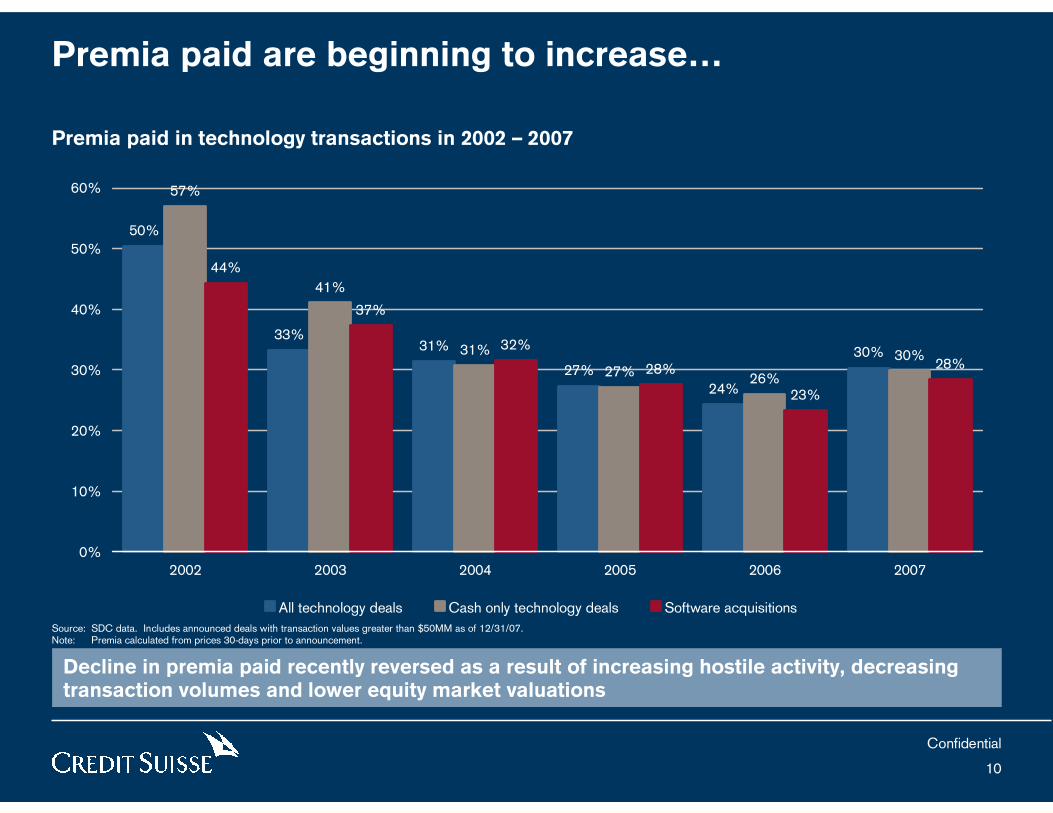

50%

33%31%

27%24%

30%

57%

41%

31%

27% 26%

30%

44%

37%

32%

28%

23%

28%

0%

10%

20%

30%

40%

50%

60%

2002 2003 2004 2005 2006 2007

All technology deals Cash only technology deals Software acquisitions

Premia paid are beginning to increase…

Premia paid in technology transactions in 2002 – 2007

Decline in premia paid recently reversed as a result of increasing hostile activity, decreasing transaction volumes and lower equity market valuations

Source: SDC data. Includes announced deals with transaction values greater than $50MM as of 12/31/07.Note: Premia calculated from prices 30-days prior to announcement.

Confidential

11

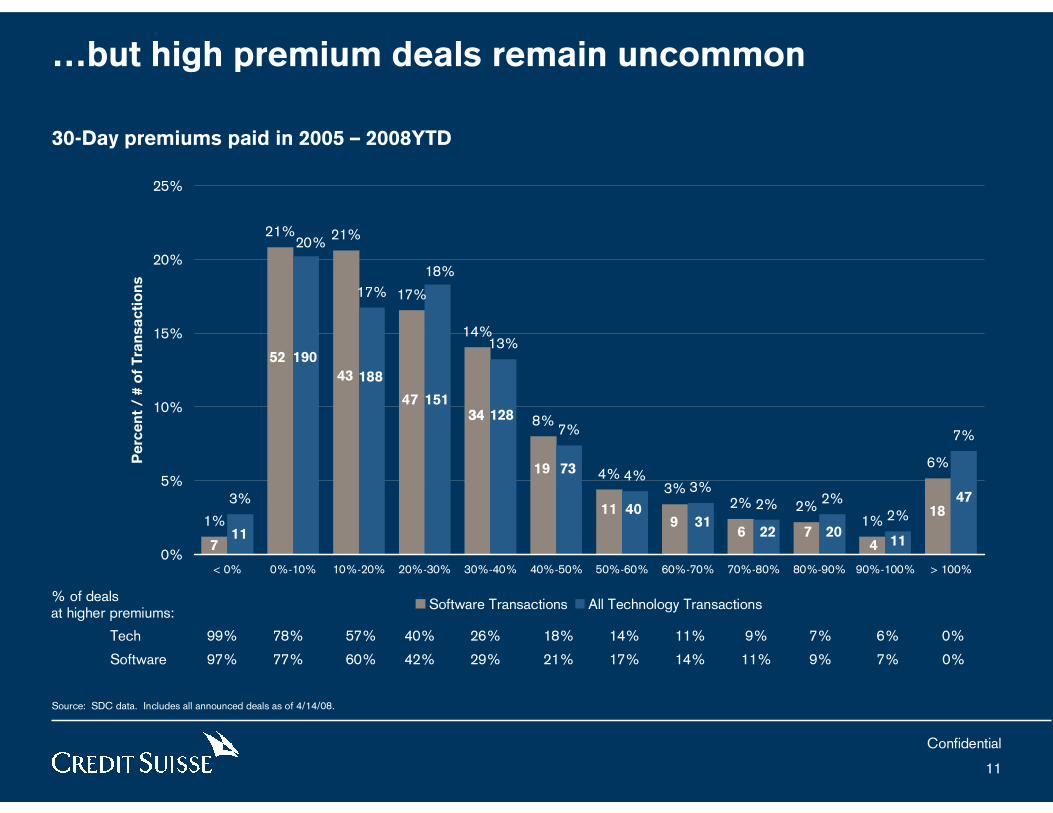

…but high premium deals remain uncommon

30-Day premiums paid in 2005 – 2008YTD

% of dealsat higher premiums:

Source: SDC data. Includes all announced deals as of 4/14/08.

Tech 99% 78% 57% 40% 26% 18% 14% 11% 9% 7% 6% 0%

Software 97% 77% 60% 42% 29% 21% 17% 14% 11% 9% 7% 0%

6%

1%2%2%

3%4%

8%

14%

17%

21%21%

1%

7%

2%2%2%

3%4%

7%

13%

18%

17%

20%

3%

0%

5%

10%

15%

20%

25%

< 0% 0%-10% 10%-20% 20%-30% 30%-40% 40%-50% 50%-60% 60%-70% 70%-80% 80%-90% 90%-100% > 100%

Pe

rce

nt

/ #

of

Tra

nsa

cti

on

s

Software Transactions All Technology Transactions

711

52 190

43 188

47 15134 12834

19 73

11 409 31

6 22 7 204 11

1847

Confidential

12

42%24%

35%20%

53%35%

60% 55%68%

55%69% 69% 77%

68% 73% 77% 77% 77%90% 83%

11%

10%

15%

15%

13%

16%

14% 19%12%

18%11% 17% 10%

14% 9% 10% 12% 14%8%

11%

46%

56%

48%

54%

32%

39%

24% 21%19%

19%18% 10% 9% 14% 15% 7% 7% 6% 7%11% 11% 10% 5% 7% 2% 4% 4% 5% 3% 6%

2%2% 2% 2% 2% 1% 3%3%

0%

20%

40%

60%

80%

100%

T S T S T S T S T S T S T S T S T S T S

Cash Hybrid Stock Other

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008YTD

4%

11%12%

17%15% 15%

10% 11%9% 8%

0%

5%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 (1)

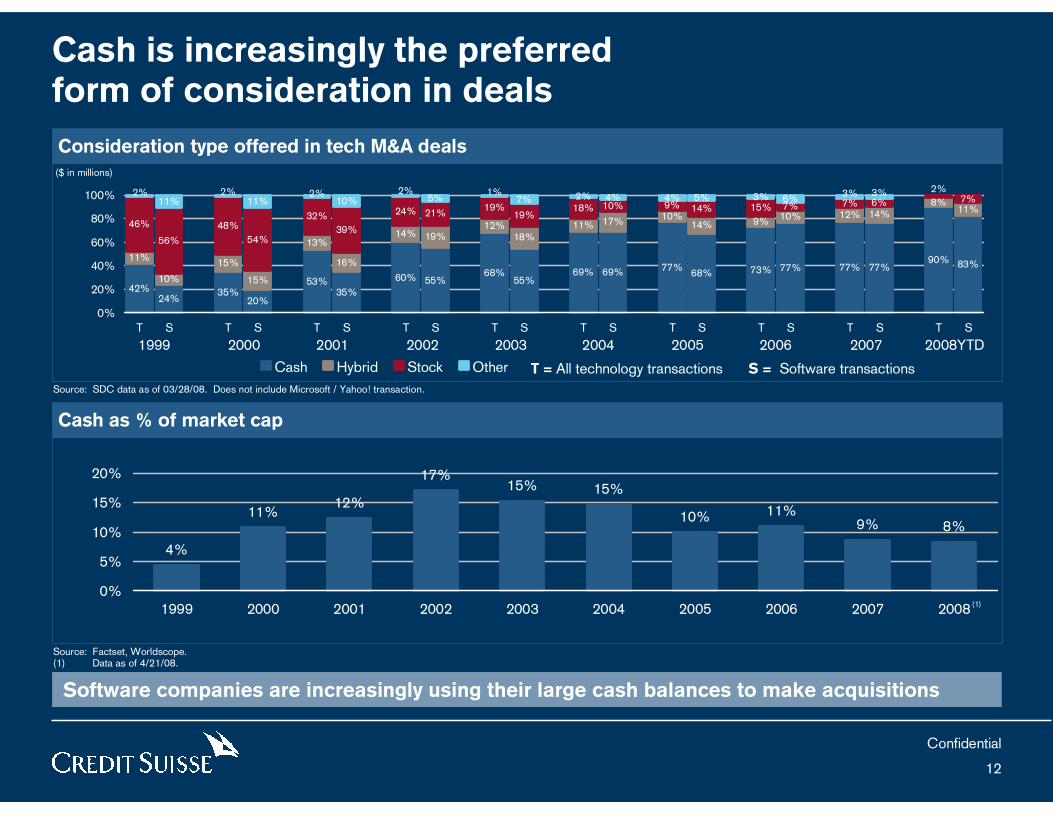

Cash is increasingly the preferredform of consideration in deals

Consideration type offered in tech M&A deals

Source: SDC data as of 03/28/08. Does not include Microsoft / Yahoo! transaction.

Software companies are increasingly using their large cash balances to make acquisitions

Cash as % of market cap

Source: Factset, Worldscope.(1) Data as of 4/21/08.

($ in millions)

T = All technology transactions S = Software transactions

Confidential

13

29%23%

16%

8%

41%

31%

48%

75%

90% 100%

0%

10%

20%

30%

40%

50%

$10MM-$100MM $100MM-$500MM $500MM-$1BN $1BN-$5BN >$5BN

Annual revenue

% m

arg

in

0%

20%

40%

60%

80%

100%

% o

f co

mp

anie

s

Mean NTM EBITDA margin % of companies w/ positive EBITDA ests.

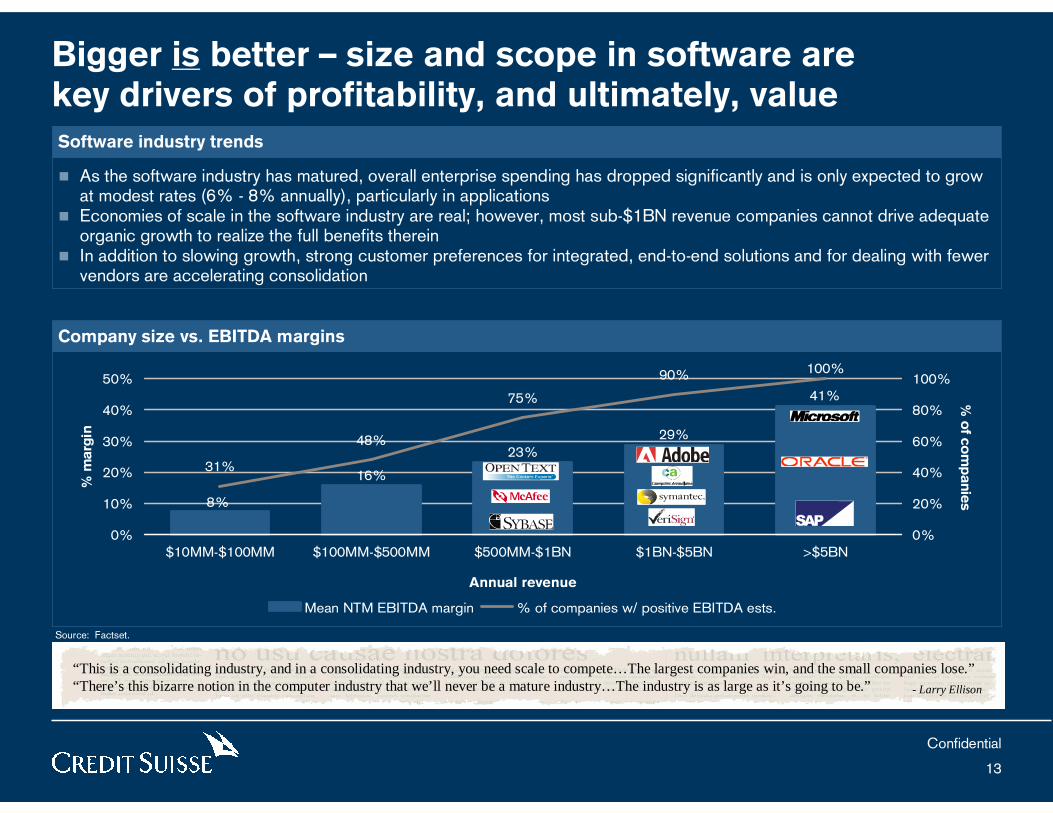

Bigger is better – size and scope in software are key drivers of profitability, and ultimately, valueSoftware industry trends

� As the software industry has matured, overall enterprise spending has dropped significantly and is only expected to grow at modest rates (6% - 8% annually), particularly in applications

� Economies of scale in the software industry are real; however, most sub-$1BN revenue companies cannot drive adequate organic growth to realize the full benefits therein

� In addition to slowing growth, strong customer preferences for integrated, end-to-end solutions and for dealing with fewer vendors are accelerating consolidation

Company size vs. EBITDA margins

- Larry Ellison

“This is a consolidating industry, and in a consolidating industry, you need scale to compete…The largest companies win, and the small companies lose.”“There’s this bizarre notion in the computer industry that we’ll never be a mature industry…The industry is as large as it’s going to be.”

Source: Factset.

Credit Suisse does not provide any tax advice. Any tax statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding any penalties. Any such statement herein was written to support the marketing or promotion of the transaction(s) or matter(s) to which the statement relates. Each taxpayer should seek advice based on the taxpayer's particular circumstances from an independent tax advisor.

These materials have been provided to you by Credit Suisse in connection with an actual or potential mandate or engagement and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with Credit Suisse. In addition, these materials may not be disclosed, in whole or in part, or summarized or otherwise referred to except as agreed in writing by Credit Suisse. The information used in preparing these materials was obtained from or through you or your representatives or from public sources. Credit Suisse assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance (including estimates of potential cost savings and synergies) prepared by or reviewed or discussed with the managements of your company and/or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). These materials were designed for use by specific persons familiar with the business and the affairs of your company and Credit Suisse assumes no obligation to update or otherwise revise these materials. Nothing contained herein should be construed as tax, accounting or legal advice. You (and each of your employees, representatives or other agents) may disclose to any and all persons, without limitation of any kind, the tax treatment and tax structure of the transactions contemplated by these materials and all materials of any kind (including opinions or other tax analyses) that are provided to you relating to such tax treatment and structure. For this purpose, the tax treatment of a transaction is the purported or claimed US federal income tax treatment of the transaction and the tax structure of a transaction is any fact that may be relevant to understanding the purported or claimed US federal income tax treatment of the transaction.

Credit Suisse has adopted policies and guidelines designed to preserve the independence of its research analysts. Credit Suisse’s policies prohibit employees from directly or indirectly offering a favorable research rating or specific price target, or offering to change a research rating or price target, as consideration for or an inducement to obtain business or other compensation. Credit Suisse’s policies prohibit research analysts from being compensated for their involvement in investment banking transactions.

C:\

Docu

men

ts a

nd S

ettin

gs\

dch

orney

\Des

ktop

\Softw

are

Slid

es (

Pro

ject

ed).

pp

t

Confidential

14

Confidential

15

CREDIT SUISSE SECURITIES (USA) LLC

Eleven Madison Avenue

New York, NY 10010-3629

+1 212 325 2000

www.credit-suisse.com

![Software Engineering.ppt [호환 모드] - Konkukdslab.konkuk.ac.kr/Class/2008/08SMA/Presentation/Class B... · 2012. 9. 13. · Title: Microsoft PowerPoint - Software Engineering.ppt](https://img.dokumen.tips/doc/110x75/6121bf52e3836428e4353694/software-eeoe-konkukdslabkonkukackrclass200808smapresentationclass.jpg)

![Software Presentation[1]](https://img.dokumen.tips/doc/110x75/558bb9c2d8b42ab07c8b463e/software-presentation1.jpg)