Embed Size (px)

Citation preview

W W W . R A B E N T R A N S P O R T . P L 1

I N T R O D U C T I O N

• Polish, 46,

• 23 years’ experience in

transport and logistics,

• member of the Raben

Group board for FTL &

intermodal,

• chairman of the board

of Transport i Logistyka

Polska ”TLP”.

• Dutch holding,

• headquarters in

Poland,

• present in 11 European

countries in more than

130 depots,

• 6,500 modern means

of transport,

• 1,100,000 m2 of

diversified warehouse

capacity.

W W W . R A B E N T R A N S P O R T . P L 2

T R A N S P O R T

Basic characteristics of the transport market

• Competitive transport services support trade

exchange between member states.

• Technological progress and customer expectations

make the sector more progressive, environmentally

friendly and safe.

• Carriers compete with others in terms of:

• quality – OTIF: on-Time in-Full, flexibility,

complexity, customer service,

• price – freight, rate per km single/round-trip,

• Image – CSR, Safety Rules.

• Rates are shaped by fixed & variable costs, where

trucks monthly mileage of 9k or 11.5k km can cause

a difference in profitability of 15-20%.

• Cabotage decreases empty mileage and CO2

emissions,

• Drivers are scarce in all European countries.

Because of their high mobility, wages are becoming

equal.

an extremely competitive

industry

dominated by micro-

entrepreneurs

low profitability

W W W . R A B E N T R A N S P O R T . P L

M A R K E T S I T U AT I O N

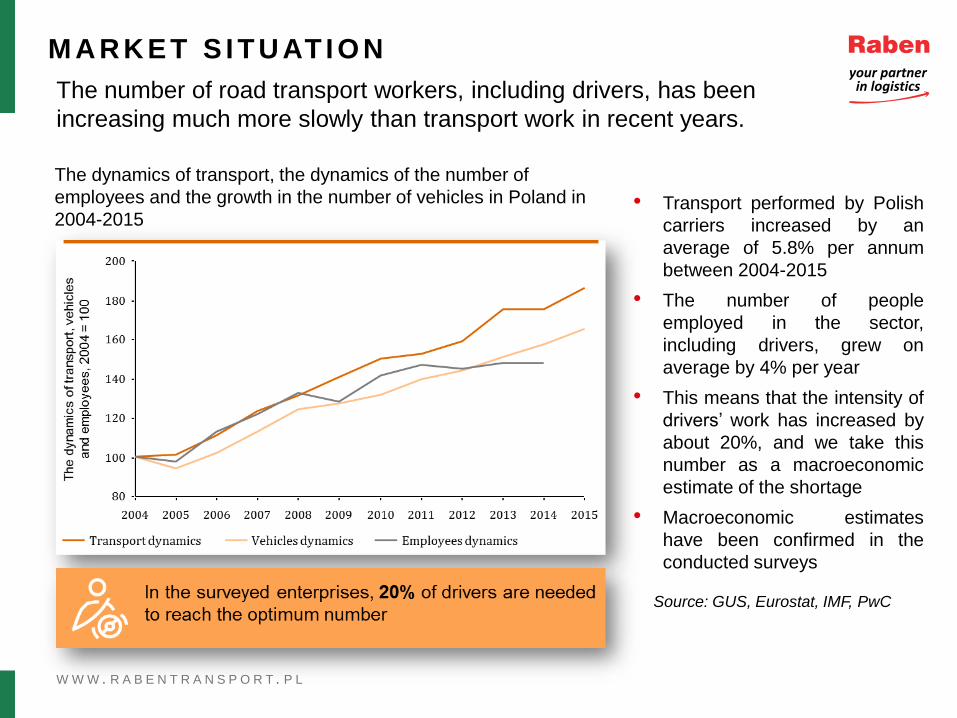

The number of road transport workers, including drivers, has been

increasing much more slowly than transport work in recent years.

• Transport performed by Polish

carriers increased by an

average of 5.8% per annum

between 2004-2015

• The number of people

employed in the sector,

including drivers, grew on

average by 4% per year

• This means that the intensity of

drivers’ work has increased by

about 20%, and we take this

number as a macroeconomic

estimate of the shortage

• Macroeconomic estimates

have been confirmed in the

conducted surveys

The dynamics of transport, the dynamics of the number of

employees and the growth in the number of vehicles in Poland in

2004-2015

Source: GUS, Eurostat, IMF, PwC

W W W . R A B E N T R A N S P O R T . P L

M A R K E T S I T U AT I O N

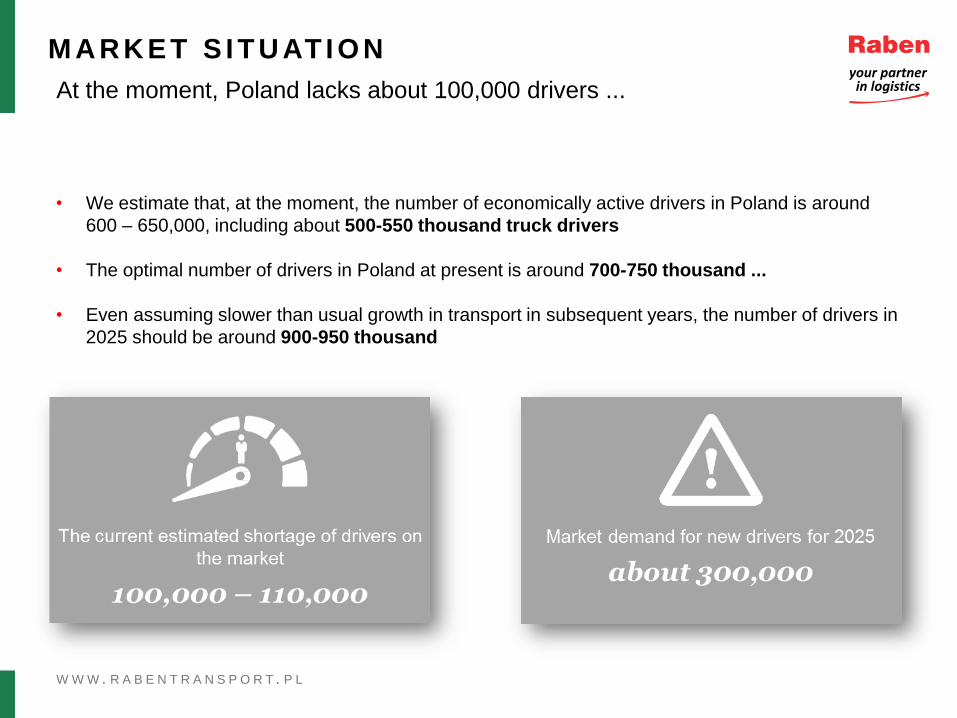

At the moment, Poland lacks about 100,000 drivers ...

• We estimate that, at the moment, the number of economically active drivers in Poland is around

600 – 650,000, including about 500-550 thousand truck drivers

• The optimal number of drivers in Poland at present is around 700-750 thousand ...

• Even assuming slower than usual growth in transport in subsequent years, the number of drivers in

2025 should be around 900-950 thousand

W W W . R A B E N T R A N S P O R T . P L

M A R K E T S I T U AT I O N

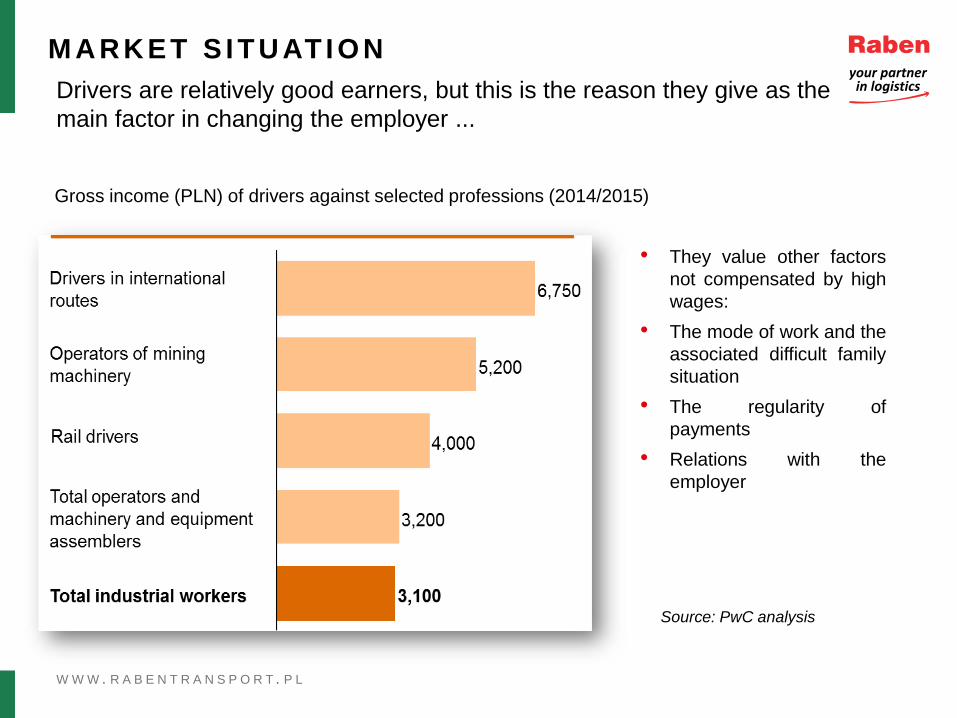

Drivers are relatively good earners, but this is the reason they give as the

main factor in changing the employer ...

• They value other factors

not compensated by high

wages:

• The mode of work and the

associated difficult family

situation

• The regularity of

payments

• Relations with the

employer

Gross income (PLN) of drivers against selected professions (2014/2015)

Source: PwC analysis

W W W . R A B E N T R A N S P O R T . P L 6

T R E N D S I N T R A N S P O R TAT I O N

What direction are we really heading in?

digitalisation

platooning

driverless trucks

Potential future

business

models in

transportation

Future of EU

road transportation

?

W W W . R A B E N T R A N S P O R T . P L 7

M A N A G I N G A T R A N S P O R T C O M PA N Y

many countries

many

regulations

huge

administrative

workload

complex IT

solutions

multilanguage

communication

high penalties permanent

uncertainty

W W W . R A B E N T R A N S P O R T . P L 8

P O S T E D W O R K E R S D I R E C T I V E

Practical questions with no answer

• How to manage labour costs – shorter work in certain

countries?

• How to ensure comparable earnings – rotation of

drivers?

• How to calculate rates to contracts – according to the

lowest or perhaps the highest minimum wage?

• What happens after 24 months, if the driver was in

different countries? In which system should he be

insured? Or perhaps he should be dismissed in the

23rd month? Who will employ a driver with higher

social costs?

• Where should drivers’ rest be organised if there is no

infrastructure? Who thinks that drivers would prefer

to sleep in a motel rather than in the cabin?

W W W . R A B E N T R A N S P O R T . P L 9

H Y P O C R I S Y

• The EU founder states,

from which originated

the primary EU values,

including the free flow

of goods and services

• Mostly states with

direct investments in

CEE: Germany, the

Netherlands, France,

the UK and Austria.

• Minimum wage in

transport: Germany,

France, Austria,

Norway, Italy and the

Netherlands.

• Top EU road freight

markets: Germany,

France, Italy, the UK,

Spain.

• Main carriers in the

EU: Germany, Poland,

Spain, France and

Italy.

W W W . R A B E N T R A N S P O R T . P L 10

O N C E D E M O L I S H E D…

The wall is rising again

W W W . R A B E N T R A N S P O R T . P L

T H A N K Y O U F O R

Y O U R AT T E N T I O N

Paweł Trębicki

Raben Transport

T. +48 61 89 88 594

M.+48 693 794 675

Managing Director