Embed Size (px)

Citation preview

UNDERST&NDING IS EVERYTHING

Mary Meeker

Internet Trends Report 2016

Prepared by Josh Rammell

Overview

Each year Mary Meeker produces a comprehensive look at the

internet trends that are affecting us now, and for the coming

year. We have looked to condense this for you to take the key

highlights for your organisation. We have also added our own

insight to contextualise the findings as much as possible.

While these trends are important, they are at a top level as well

as focusing mainly on USA and global trends, therefore make

sure to place them within that framework when reviewing.

| 2

Key takeaways

• Need to look at content and approach to succeed in a mobile

first world

• Adblocking is worth noting, but see it as an opportunity rather

than a threat

• Video needs to progress, but key stakeholders making

progressive movements

• Messaging at the core of mobile use, look to the Far East to see

where UK market should progress to

• Voice search and Artificial Intelligence are the next steps in

technological progression, advertising methodology will follow

| 3

Key highlights

| 4

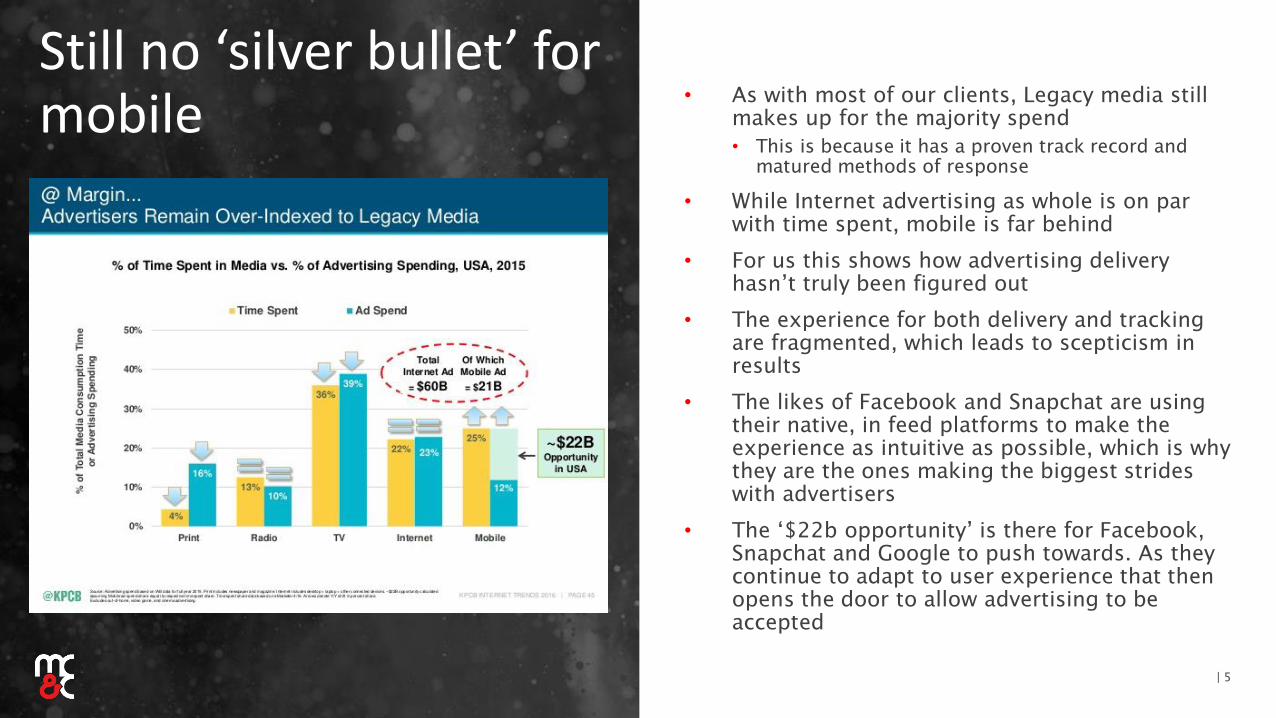

Still no ‘silver bullet’ for mobile

| 5

• As with most of our clients, Legacy media still

makes up for the majority spend

• This is because it has a proven track record and

matured methods of response

• While Internet advertising as whole is on par

with time spent, mobile is far behind

• For us this shows how advertising delivery

hasn’t truly been figured out

• The experience for both delivery and tracking

are fragmented, which leads to scepticism in

results

• The likes of Facebook and Snapchat are using

their native, in feed platforms to make the

experience as intuitive as possible, which is why

they are the ones making the biggest strides

with advertisers

• The ‘$22b opportunity’ is there for Facebook,

Snapchat and Google to push towards. As they

continue to adapt to user experience that then

opens the door to allow advertising to be

accepted

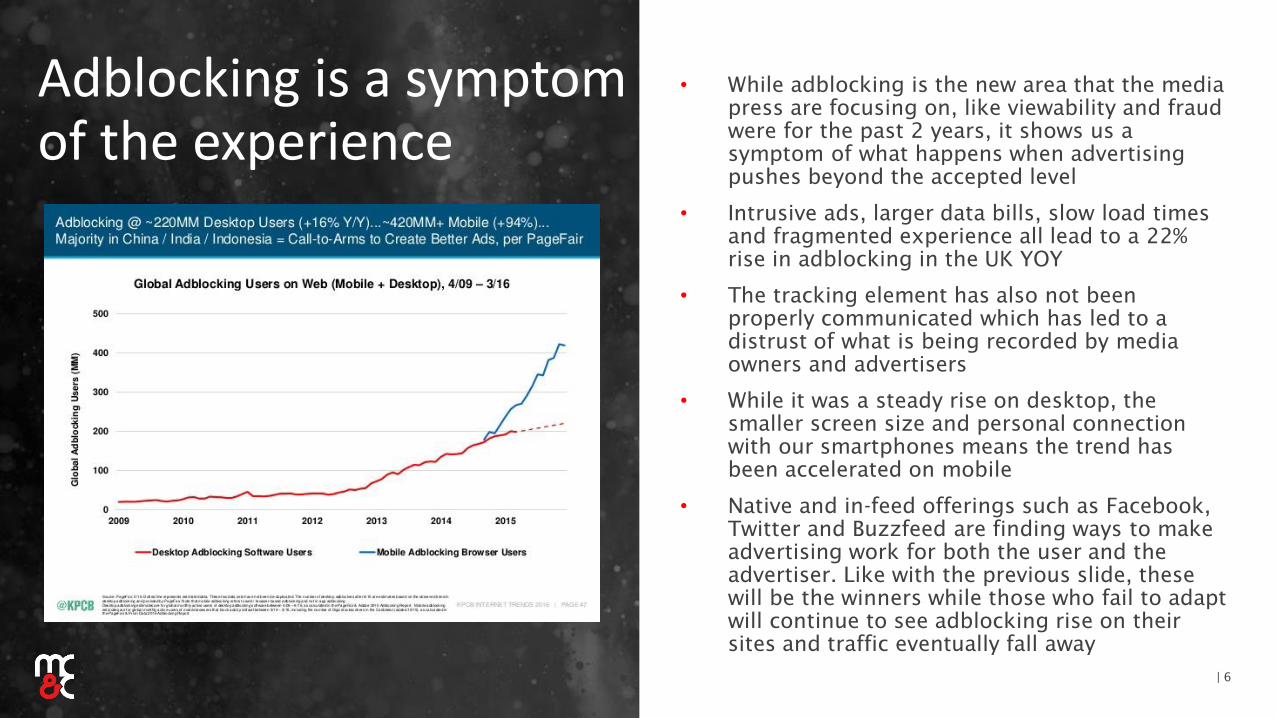

Adblocking is a symptom of the experience

| 6

• While adblocking is the new area that the media

press are focusing on, like viewability and fraud

were for the past 2 years, it shows us a

symptom of what happens when advertising

pushes beyond the accepted level

• Intrusive ads, larger data bills, slow load times

and fragmented experience all lead to a 22%

rise in adblocking in the UK YOY

• The tracking element has also not been

properly communicated which has led to a

distrust of what is being recorded by media

owners and advertisers

• While it was a steady rise on desktop, the

smaller screen size and personal connection

with our smartphones means the trend has

been accelerated on mobile

• Native and in-feed offerings such as Facebook,

Twitter and Buzzfeed are finding ways to make

advertising work for both the user and the

advertiser. Like with the previous slide, these

will be the winners while those who fail to adapt

will continue to see adblocking rise on their

sites and traffic eventually fall away

Video is still in it’s infancy

| 7

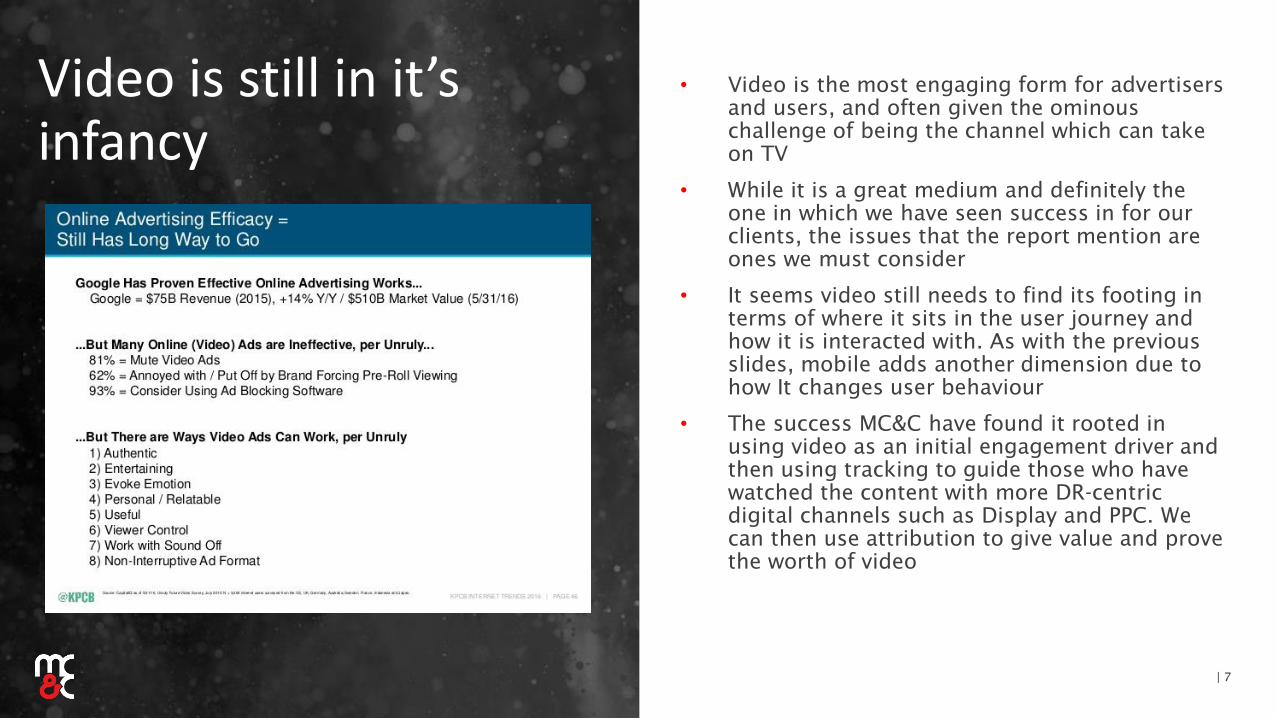

• Video is the most engaging form for advertisers

and users, and often given the ominous

challenge of being the channel which can take

on TV

• While it is a great medium and definitely the

one in which we have seen success in for our

clients, the issues that the report mention are

ones we must consider

• It seems video still needs to find its footing in

terms of where it sits in the user journey and

how it is interacted with. As with the previous

slides, mobile adds another dimension due to

how It changes user behaviour

• The success MC&C have found it rooted in

using video as an initial engagement driver and

then using tracking to guide those who have

watched the content with more DR-centric

digital channels such as Display and PPC. We

can then use attribution to give value and prove

the worth of video

Video evolutions

| 8

• As video is looking for ways to grow, we have

seen the leaders such as YouTube and

Facebook innovate and adapt

• YouTube released a new format called ‘Bumper

Ads’ which are 6 seconds long and non-

skippable. We believe this is their attempt to

align with the amount of advertising time TV

takes up, as can be seen in the table below:

• The format does add creative limitations but

can be built in an engagement journey along

with other digital elements

• Facebook are also changing their algorithm to

promote video higher than images, as well as

suggesting content similar to ads to make it as

assimilated as possible

Average Length of

content (minutes)

Length of advertising

(minutes)

% of

total

60 9 15%

4 0.6 15%

Accelerated channel growth

| 9

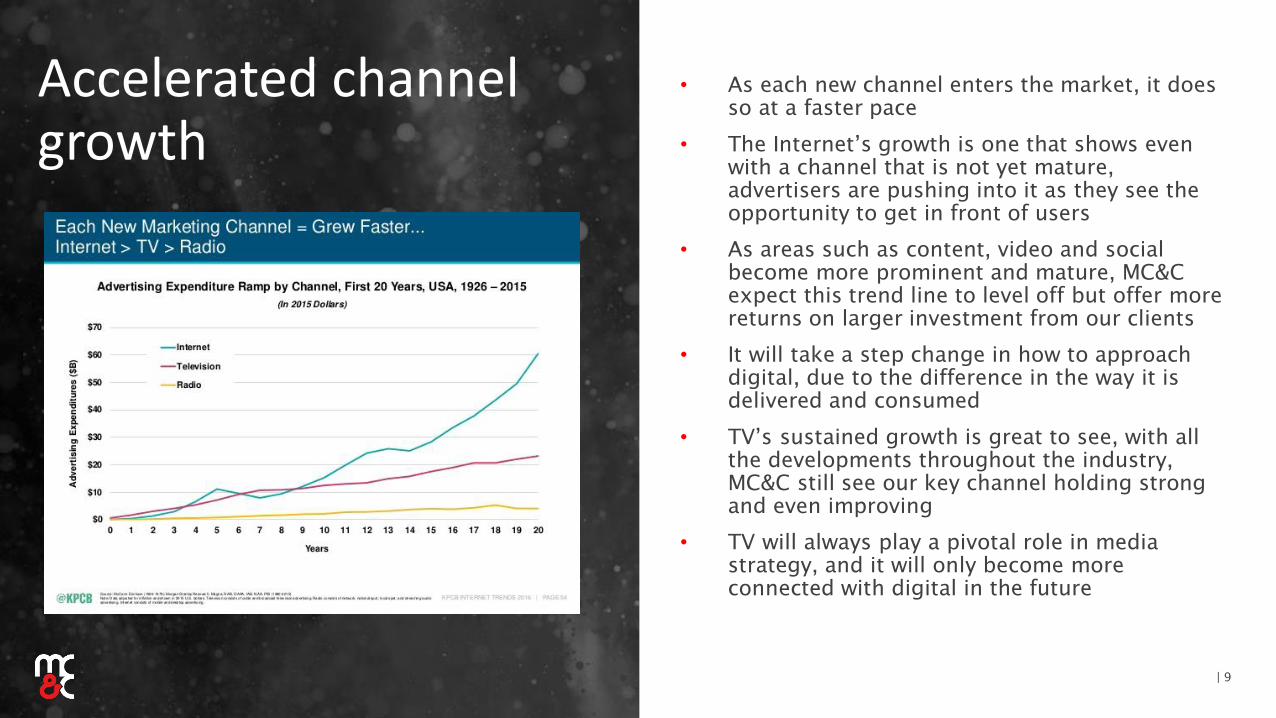

• As each new channel enters the market, it does

so at a faster pace

• The Internet’s growth is one that shows even

with a channel that is not yet mature,

advertisers are pushing into it as they see the

opportunity to get in front of users

• As areas such as content, video and social

become more prominent and mature, MC&C

expect this trend line to level off but offer more

returns on larger investment from our clients

• It will take a step change in how to approach

digital, due to the difference in the way it is

delivered and consumed

• TV’s sustained growth is great to see, with all

the developments throughout the industry,

MC&C still see our key channel holding strong

and even improving

• TV will always play a pivotal role in media

strategy, and it will only become more

connected with digital in the future

Social part of the buying journey

| 10

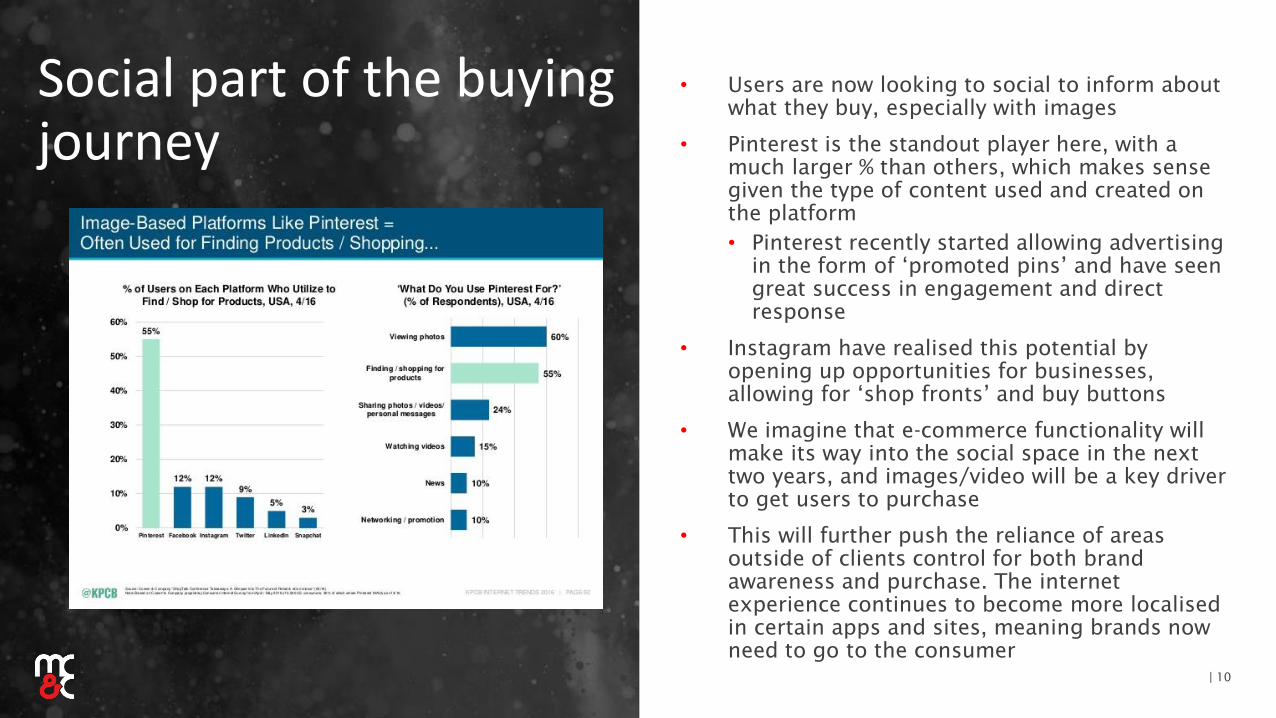

• Users are now looking to social to inform about

what they buy, especially with images

• Pinterest is the standout player here, with a

much larger % than others, which makes sense

given the type of content used and created on

the platform

• Pinterest recently started allowing advertising

in the form of ‘promoted pins’ and have seen

great success in engagement and direct

response

• Instagram have realised this potential by

opening up opportunities for businesses,

allowing for ‘shop fronts’ and buy buttons

• We imagine that e-commerce functionality will

make its way into the social space in the next

two years, and images/video will be a key driver

to get users to purchase

• This will further push the reliance of areas

outside of clients control for both brand

awareness and purchase. The internet

experience continues to become more localised

in certain apps and sites, meaning brands now

need to go to the consumer

Messaging accounts for a large amount of mobile use

| 11

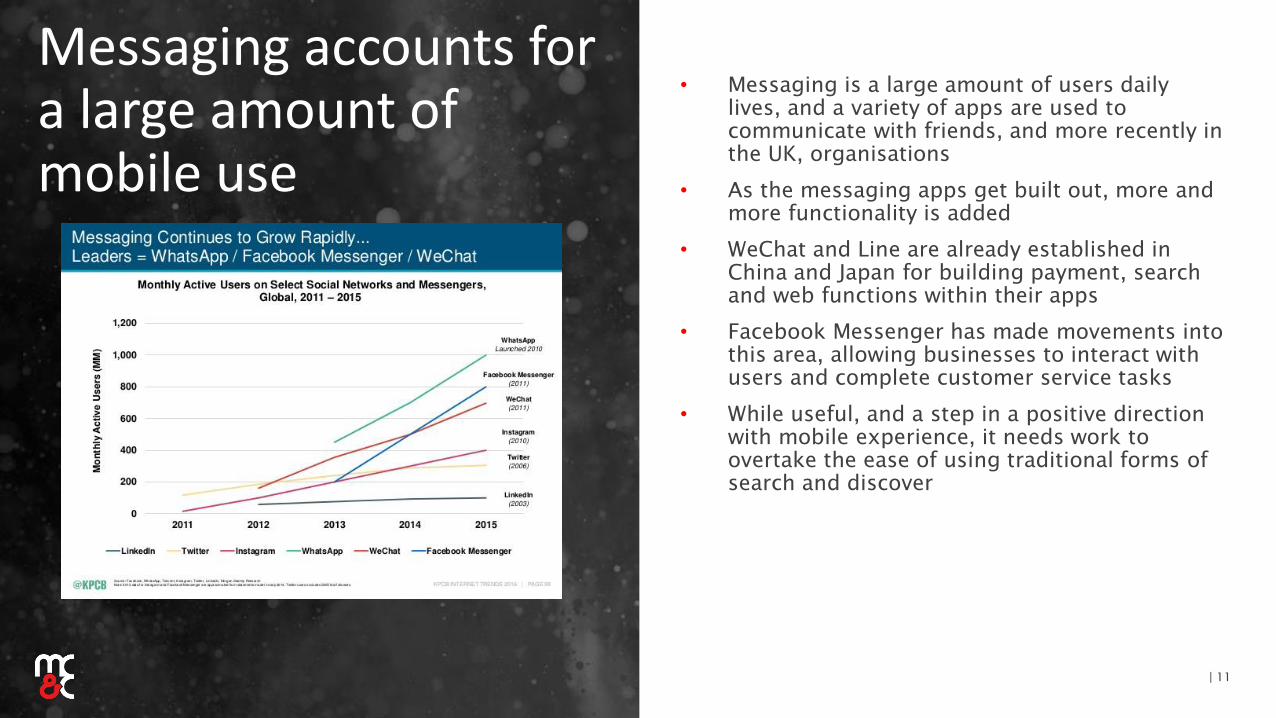

• Messaging is a large amount of users daily

lives, and a variety of apps are used to

communicate with friends, and more recently in

the UK, organisations

• As the messaging apps get built out, more and

more functionality is added

• WeChat and Line are already established in

China and Japan for building payment, search

and web functions within their apps

• Facebook Messenger has made movements into

this area, allowing businesses to interact with

users and complete customer service tasks

• While useful, and a step in a positive direction

with mobile experience, it needs work to

overtake the ease of using traditional forms of

search and discover

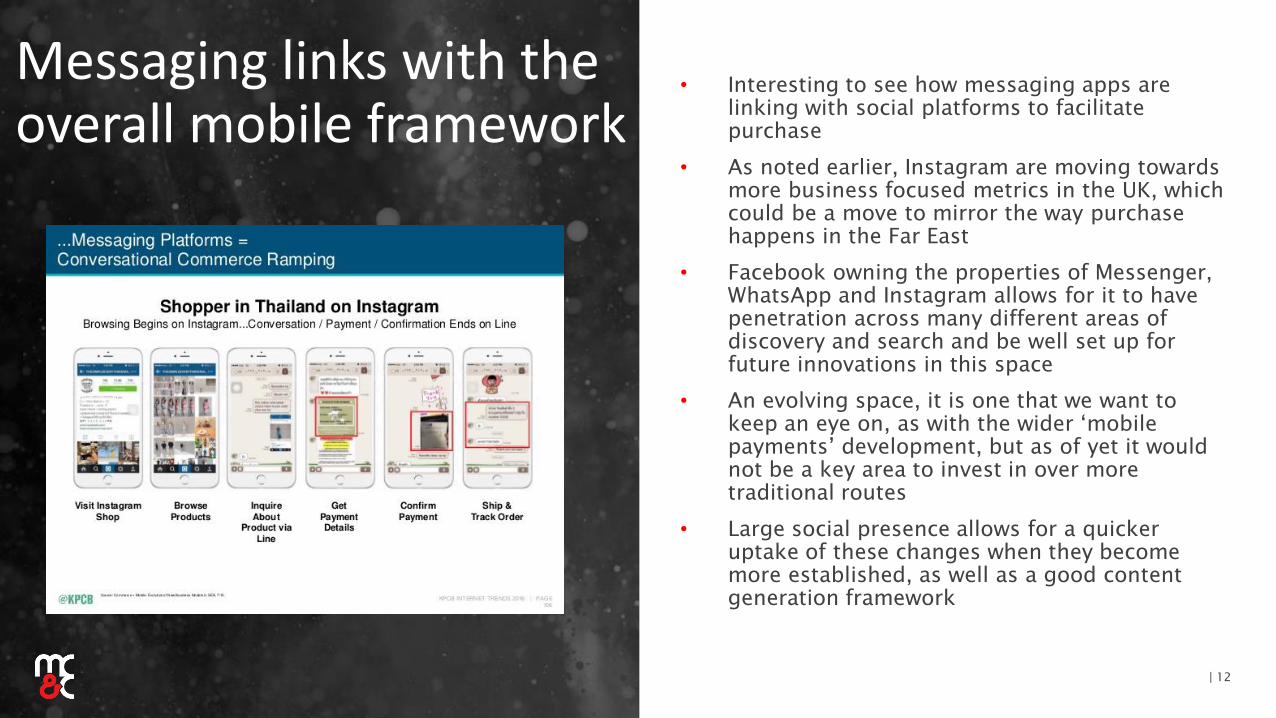

Messaging links with the overall mobile framework

| 12

• Interesting to see how messaging apps are

linking with social platforms to facilitate

purchase

• As noted earlier, Instagram are moving towards

more business focused metrics in the UK, which

could be a move to mirror the way purchase

happens in the Far East

• Facebook owning the properties of Messenger,

WhatsApp and Instagram allows for it to have

penetration across many different areas of

discovery and search and be well set up for

future innovations in this space

• An evolving space, it is one that we want to

keep an eye on, as with the wider ‘mobile

payments’ development, but as of yet it would

not be a key area to invest in over more

traditional routes

• Large social presence allows for a quicker

uptake of these changes when they become

more established, as well as a good content

generation framework

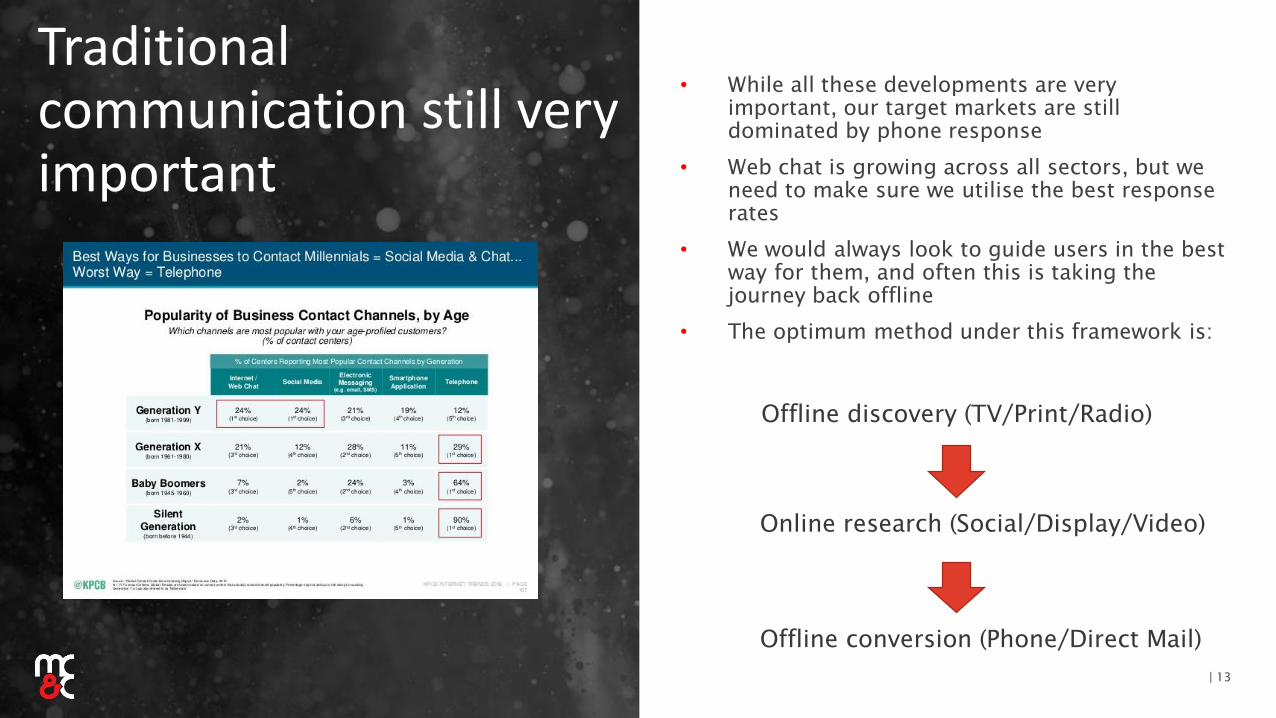

Traditional communication still very important

| 13

• While all these developments are very

important, our target markets are still

dominated by phone response

• Web chat is growing across all sectors, but we

need to make sure we utilise the best response

rates

• We would always look to guide users in the best

way for them, and often this is taking the

journey back offline

• The optimum method under this framework is:

Offline discovery (TV/Print/Radio)

Online research (Social/Display/Video)

Offline conversion (Phone/Direct Mail)

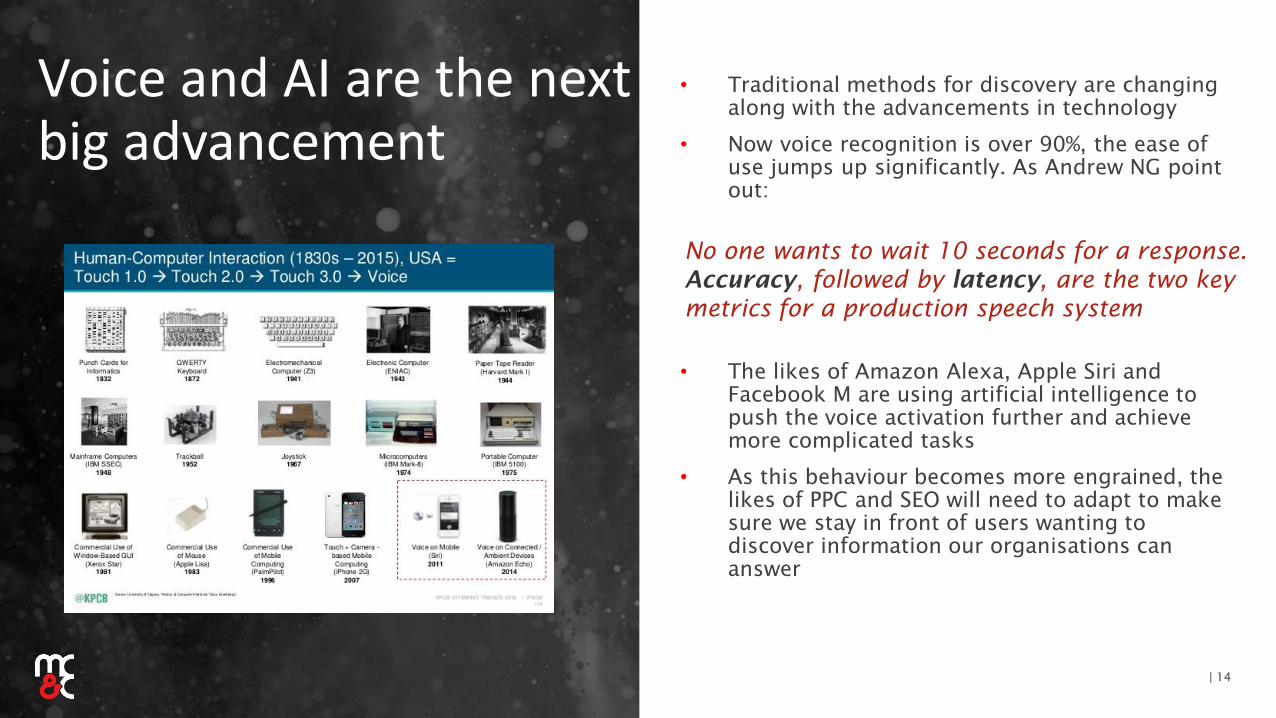

Voice and AI are the next big advancement

| 14

• Traditional methods for discovery are changing

along with the advancements in technology

• Now voice recognition is over 90%, the ease of

use jumps up significantly. As Andrew NG point

out:

• The likes of Amazon Alexa, Apple Siri and

Facebook M are using artificial intelligence to

push the voice activation further and achieve

more complicated tasks

• As this behaviour becomes more engrained, the

likes of PPC and SEO will need to adapt to make

sure we stay in front of users wanting to

discover information our organisations can

answer

No one wants to wait 10 seconds for a response.

Accuracy, followed by latency, are the two key

metrics for a production speech system

Thanks

Please contact [email protected] to

learn how we can build this into your

organisation’s thinking

![Mary meeker preso[1]](https://img.dokumen.tips/doc/110x75/553899da550346bf308b47e6/mary-meeker-preso1.jpg)