Embed Size (px)

Citation preview

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web:

www.cathakkar.in

� What if your idea is not just an idea?

� What if it sees light?

� What if it’s really born?

� What if you can get someone to believe in it?

� And help you nurture it?� And help you nurture it?

� What if you can set a clear path for it?

� What if it can actually travel?

� What if it grows and blooms?

� What if the whole world embraces it?

� What if your idea is not just an idea?

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

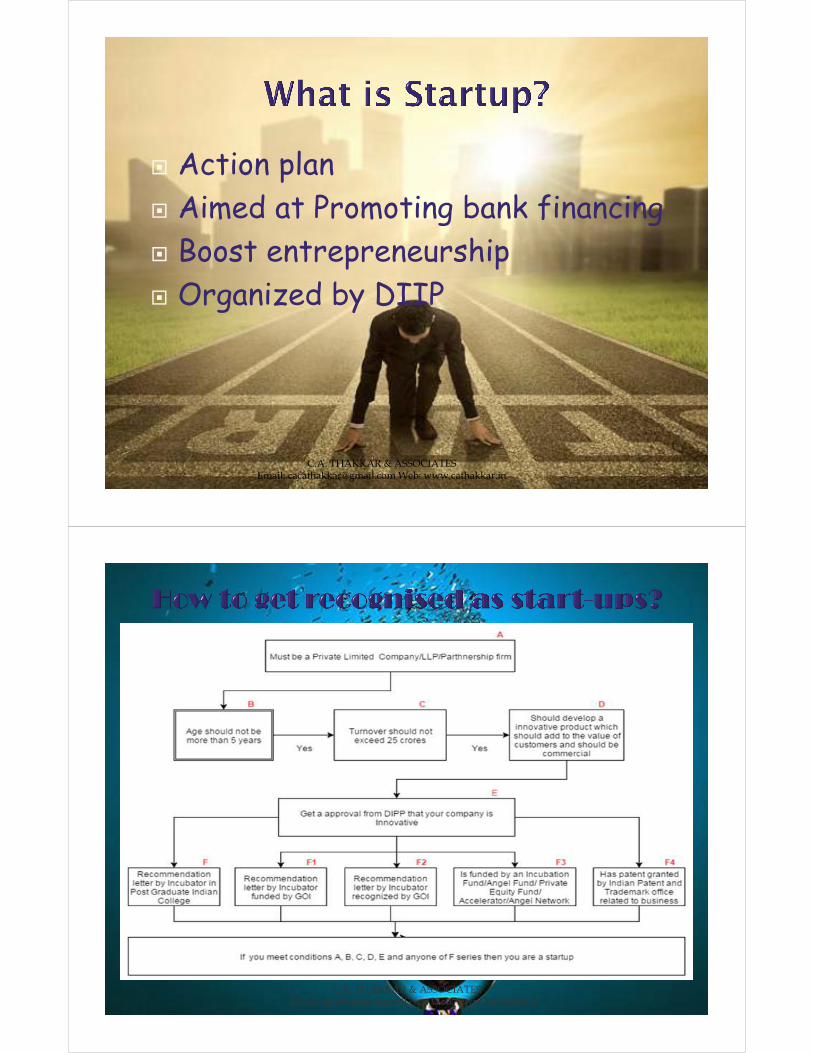

� Action plan

� Aimed at Promoting bank financing

� Boost entrepreneurship � Boost entrepreneurship

� Organized by DIIP

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Startups would be allowed self certification of compliances with certain labour laws and environment laws so as to reduce the regulatory burden. Further in case of the labour laws, no inspections will be conducted labour laws, no inspections will be conducted for initial period of 3 years.

� Funded by an Incubation Fund/Angel Fund/Private Equity Fund/Accelerator/ Angel Network duly registered with SEBI* that endorses innovative nature of the business; or

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Patent applications of Startups shall be fast tracked for examination and disposal, so that they can realize the value of their IPR at the earliest possible. A Panel of facilitators will be empanelled to assist in facilitators will be empanelled to assist in filing of IP applications. The Government shall bear the entire fees of the facilitators and the Startup shall bear the cost of only statutory fees. Further, Startups shall be provided 80% rebate in filing of patents visàvis other companies.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� The Government of India shall provide mobile app for:

A. Registering Startups with relevant agencies of Government

B. Tracking the status of registration application and downloading of the registration certificate.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

C. Filing for compliances and obtaining information on various clearances and approval required.

D. Applying for various schemes being undertaken under the Startup India Action Plan.Plan.

The Mobile App shall be made available from April 1, 2016 on all leading mobile/ smart devices' platforms.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� In terms of the Insolvency and Bankruptcy Bill 2015, Startups with simple debt structures or those meeting such criteria as may be meeting such criteria as may be specified may be wound up within a period of 90 days from making of an application for winding up on a fast track basis.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Exemption shall be given in respect of a capital gain which is invested in the Exemption shall be given in respect of a capital gain which is invested in the Startup ecosystem. This will increase the funds available to various VCs (Venture Capital Funds ) / AIFs (Alternative Investment Funds ) for investment in Startups.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Profits shall be exempted from income tax for a � Profits shall be exempted from income tax for a period of 3 years.

� The exemption shall be available subject to no distribution of dividend by the Startup. A Startup shall be eligible for tax benefits only after it has obtained certification from the Inter-Ministerial Board, setup for such purpose.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Consideration received by a Startups for issuing shares at a price higher than its Fair Market Value would not be taxable as Value would not be taxable as income from other Sources in the hands of recipient under section 56(2)(viib) of the Incometax Act.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� single point of contact for the entire Startupecosystem and enable knowledge exchange and access to funding. The "Startup India Hub" will be a key stakeholder in this vibrant ecosystem and will:and will:

A. Work in a hub and spoke model and collaborate with Central & State Governments of Indian and foreign VCs, angel networks, banks, incubators, legal partners, consultants, universities and R&D institutions.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

B. Assist Startups through their lifecycle with specific focus on important aspects like

obtaining financing,

feasibility testing, feasibility testing,

business structuring advisory,

enhancement of marketing skills,

technology commercialization

and management evaluation.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

C. Organize mentorship programs in collaboration with

Government organizations,

Incubation centers,

Educational institutions Educational institutions

& Private organizations to aspire foster innovation.

� Startup India Hub will be guide, friend and a mentor for the people who has courage to enter in environment of risk.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Typically whenever a tender is floated by a Government entity or by a PSU, a very often eligibility condition specifies either "prior experience/turnover". Such a stipulation prohibits/impedes Startups from participating in such tenders. 1st April 2015 Central Government, such tenders. 1st April 2015 Central Government, State Government and PSUs have to mandatorily procure at least 20% from the Micro Small and Medium Enterprise (MSME). In order to promote Startups, Government shall exempt Startups (in the manufacturing sector) from the criteria of "prior experience/turnover" for filing of public tenders.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Government will set up a fund with an initial corpus of Rs. 2,500 crore and a total corpus of Rs. 10,000 crore over a period 4 years (i.e. Rs. 2,500 crore per year). year).

� The Fund will be in the nature of fund of funds, which means that it will not invest directly into Startups, but shall participate in the capital of SEBI registered Venture Funds.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

�Features of the Fund of Funds are below:

The Fund of Funds shall be managed by a Board with private professionals drawn from industry bodies, academia, and successful Startupssuccessful Startups

Life Insurance Corporation (LIC) shall be a co-investor in the Fund of Funds

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

The Fund of Funds shall contribute to a maximum of 50% of the stated daughter fund size. In order to be able to receive the contribution, the daughter fund should have already raised the balance 50% or more of the stated fund size as the case maybe. The Fund of Funds shall have representation on the

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

of Funds shall have representation on the governance structure/ board of the venture fund based on the contribution made.

The Fund shall ensure support to a broad mix of sectors such as manufacturing, agriculture, health, education, etc.

� Grameen Capital

� Car Dekho

� Paytm

� Swasth India� Swasth India

� Urban ladder

� Blue Stone

� Snap deal

� Altaero Energies

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Debt funding to Startups is also perceived as high risk area and to encourage Banks and other Lenders to provide Venture Debts to Startups, Credit guarantee Startups, Credit guarantee mechanism through National Credit Guarantee Trust Company (NCGTC)/ SIDBI is being envisaged with a budgetary Corpus of INR 500 crore per year for the next four years.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Government has introduce a new section and amended some old sections under Income Tax Act to promote Start Ups.

New sections:

� Section 80-IAC

� Section 54EE

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Section 54EE

� Section 115BA

� Section 115BBF

� Section 80-IBA

� Section 56(2)(viib)

� Government has amended some old sections under Income Tax Act to promote Start Ups.

Amended sections:

� Section 54GB� Section 54GB

� Section 80JJAA

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

A new section 80-IAC is inserted.

� Benefit:

� Deduction up to 100% of the profits for three years out of five consecutive years.

� Eligibility:

� Eligible startup i.e. person involving in a business of innovation, development, deployment or

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

innovation, development, deployment or commercialization of new products, processes or services driven by technology or intellectual property.

� Condition:

� The deduction shall be available only to start-ups set-up before 01.04.2019.

Amendment in section 54GB

� Benefit:

Long-term capital gains arising from transfer of residential property of individual or HUF shall not be charged to tax.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

be charged to tax.

� Eligibility:

To take the benefit of this section capital gain has to be invested in shares of an eligible start-up.

� Condition:

� Individual or HUF holds more than 50% shares of such start-up; and

� Such investment is utilized by the start-up to

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Such investment is utilized by the start-up to purchase new assets before due date of filing of return of investor.

A new section 54EE is inserted.

� Benefit:

Exemption up to Rs. 50 lakhs for long-term capital gain.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Eligibility:

Capital gains has to be invested in units of funds set-up by Government to promote start-ups.

� Condition:

� Exemption shall be reversed if amount invested is withdrawn within 3 years from date of making investment in specified funds.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� If assessee takes any loan and/or advance against such investment then he is deemed to have transferred such specified asset on the date on which such loan or advance is taken.

� A new section 115BA is inserted.

� Benefit: � Lower tax rate @25% (plus surcharge and cess).

� w.e.f: 1stmarch 2016

� Eligibility: Manufacturing companies incorporated on or after 1.3.2016.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Manufacturing companies incorporated on or after 1.3.2016.

� Condition: � The option shall be available to companies which do not claim profit linked or investment linked deductions and do not avail of investment allowance and accelerated depreciation.

� A new section 115BBF is inserted.

� Benefit:

� Any income by way of royalty received in respect of a patent developed and registered in India shall be taxable at the rate of ten per cent (plus applicable surcharge and cess) on gross basis. This benefit applies to the new patents that would be registered

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

surcharge and cess) on gross basis. This benefit applies to the new patents that would be registered and also to the existing patents.

� Condition:

� Benefits are available to the person resident in India, who is the true and first inventor of the patent.

�Substitution of new section for section 80JJAA

� Benefit:

� 30% of emoluments paid to employees would be allowed as a deduction provided emolument per employee per month is less than or equal to Rs. 25,000.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

employee per month is less than or equal to Rs. 25,000.

� Eligibility:

� all assesses who are required to get their accounts audited and has to be a start up.

� Condition:

� No deduction is available where Government is paying for EPF to employees.

� It is further proposed to reduce the minimum number of days of employment in a financial year from 300 days to 240 days and also the condition of 10% increase in number of employees every

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

of 10% increase in number of employees every year is proposed to be withdrawn.

� an employee’s emoluments has to be less than or equal to twenty-five thousand rupees per month.

� A new section 80-IBA is inserted:

� Benefit:

� Hundred per cent deduction of the profits of an assesseedeveloping and building affordable housing projects.

� w.e.f: 1st june 2016

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

w.e.f: 1 june 2016

� Eligibility:

� Housing project is approved by the competent authority after 1st june 2016 and before the 31st March, 2019

� Condition:

� The project is completed within a period of 3 years from the date of approval;

� The project is on a plot of land measuring not less than 1,000 sq. meters where the project is within 25 km from the municipal limits of four metros and in any other area, it is measuring not less than 2000 sq. meters where the size of the residential

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

2000 sq. meters where the size of the residential unit in the said areas is not more than thirty sq. meters and sixty sq. meters, respectively.

� Where residential unit is allotted to an individual, no such unit shall be allotted to him or any member of his family, etc.

� Section 56(2)(viib)

� Benefit: � Consideration received by a Startups for issuing

shares at a price higher than its Fair Market Value would not be taxable as income from other Sources in the hands of recipient

Earlier section 56(2)(viib)

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

� Earlier section 56(2)(viib)� where a company, not being a company in which the

public are substantially interested, receives, in any previous year, from any person being a resident, any consideration for issue of shares that exceeds the face value of such shares, the aggregate consideration received for such shares as exceeds the fair market value of the shares:

� Provided that this clause shall not apply where the consideration for issue of shares is received—

� (i) by a venture capital undertaking from a venture capital company or a venture capital fund; or

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in

fund; or

� (ii) by a company from a class or classes of persons as may be notified by the Central Government in this behalf.

� (1) Where at any time, a company having a share capital proposes to increase its subscribed capital by the issue of further shares, such shares shall be offered—

� (c) to any persons, if it is authorised by a special resolution, whether or not those persons include the persons referred to in clause (a) or clause (b), either for persons referred to in clause (a) or clause (b), either for cash or for a consideration other than cash, if the price of such shares is determined by the valuation report of a registered valuer subject to such conditions as may be prescribed.

C.A. THAKKAR & ASSOCIATES Email: [email protected] Web: www.cathakkar.in