Embed Size (px)

Citation preview

Raymond James 36th Annual Institutional Investors Conference

March 2015

Forward-Looking Statements

This presentation contains certain statements that may be deemed to be forward-looking

statements within the meaning of the Securities Acts. All statements, other than statements of

historical facts, that address activities, events or developments that the Partnership expects,

projects, believes or anticipates will or may occur in the future, including, without limitation, the

outlook for population growth and death rates, general industry conditions including future

operating results of the Partnership’s properties, capital expenditures, asset sales, expansion and

growth opportunities, bank borrowings, financing activities and other such matters, are forward-

looking statements. Although the Partnership believes that its expectations stated in this

presentation are based on reasonable assumptions, actual results may differ from those projected in

the forward-looking statements. When considering forward-looking statements, the reader should

keep in mind the risk factors and other cautionary statements set forth in StoneMor’s Annual

Report on Form 10-K and Quarterly Reports filed with the Securities and Exchange Commission.

Except as required under applicable law, StoneMor assumes no obligation to update or revise

any forward-looking statements made herein or any other forward-looking statements made by

StoneMor, whether as a result of new information, future events, or otherwise.

2

StoneMor at a Glance

3

Second-largest owner and operator of cemeteries in the U.S.

303 cemeteries/98 funeral homes, located across 28 states and Puerto Rico

Complete range of funeral merchandise and services, along with cemetery property, merchandise and services, both at the time of need and on a pre-need basis

Over 12,490 acres of land, equivalent to a weighted average sales life of 240 years

45,470 annual burials / 12,535 funeral service calls

$841 million in Merchandise and Perpetual Care Trusts as of September 30, 2014

We are the only deathcare company structured as a master limited partnership (MLP)

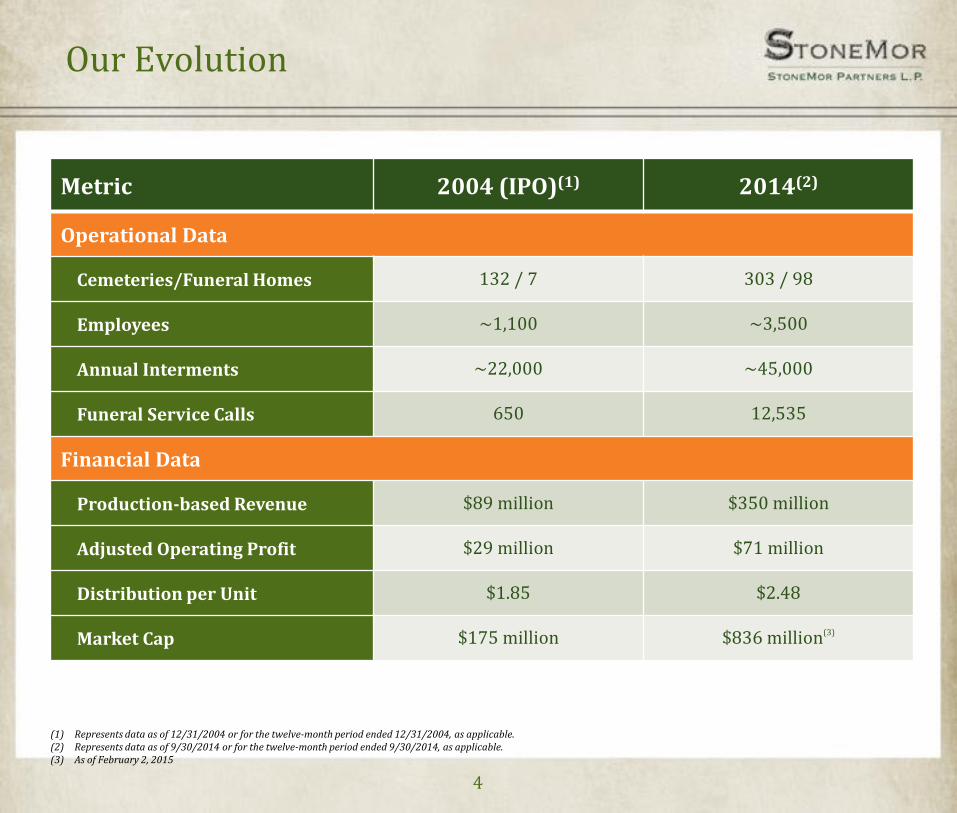

Our Evolution

4

Metric 2004 (IPO)(1) 2014(2)

Operational Data

Cemeteries/Funeral Homes 132 / 7 303 / 98

Employees ~1,100 ~3,500

Annual Interments ~22,000 ~45,000

Funeral Service Calls 650 12,535

Financial Data

Production-based Revenue $89 million $350 million

Adjusted Operating Profit $29 million $71 million

Distribution per Unit $1.85 $2.48

Market Cap $175 million $836 million(3)

(1) Represents data as of 12/31/2004 or for the twelve-month period ended 12/31/2004, as applicable. (2) Represents data as of 9/30/2014 or for the twelve-month period ended 9/30/2014, as applicable. (3) As of February 2, 2015

Our Footprint Today

Significantly enhanced geographic scale and diversity

5

303 Cemeteries

+98 Funeral Homes

= 401 Total Locations

WA

OR

CA CO

KS

IA

IL

MO

AR

IN

MI

OH

PA

WV

KY

TN

VA

NC

SC

GA AL MS

FL

Washington 3 Cemeteries 2 Funeral Homes

Oregon 6 Cemeteries 12 Funeral Homes

California 6 Cemeteries 9 Funeral Homes

Colorado 2 Cemeteries

Kansas 3 Cemeteries 2 Funeral Homes

Hawaii 1 Cemetery

Iowa 1 Cemetery

Illinois 8 Cemeteries 22Funeral Homes

Indiana 11 Cemeteries 5 Funeral Homes Michigan

13 Cemeteries

Kentucky 2 Cemeteries

Ohio 14 Cemeteries 2 Funeral Homes

Rhode Island 2 Cemeteries

Pennsylvania 52 Cemeteries 8 Funeral Homes

New Jersey 6 Cemeteries

Delaware 1 Cemetery

Maryland 10 Cemeteries 1 Funeral Home

West Virginia 33 Cemeteries 2 Funeral Homes

Virginia 31 Cemeteries 2 Funeral Homes

North Carolina 16 Cemeteries South Carolina

8 Cemeteries 3 Funeral Homes

Puerto Rico 7 Cemeteries 5 Funeral Homes

Georgia 7 Cemeteries

Florida 4 Cemeteries 17 Funeral Homes

Tennessee 11 Cemeteries 5 Funeral Homes

Alabama 9 Cemeteries 6 Funeral Homes

Mississippi 2 Cemeteries 1 Funeral Home

Arkansas 2 Funeral Homes

Missouri 6 Cemeteries 5 Funeral Homes

As of September 30, 2014

Diversified Revenue Streams

6

• More than 60% of revenues generated through highly predictable and at-need business.

• StoneMor’s 800+ person sales team creates an unparalleled advantage in pre-need sales.

Pre-need Sales, 37.0%

At-need Sales, 30.6%

Investment Income, 9.9%

Interest Income, 2.8%

Funeral Home Revenues,

18.2%

Other Cemetery

Revenues, 1.5%

Year ended December 31, 2013

BUSINESS MIX BY REVENUE STREAM

Mission-Driven Strategy

7

Mission

Vision

Strategy

To help families memorialize every life with dignity.

To be the preferred operator of deathcare facilities and preferred provider of deathcare services.

To use an opportunistic, yet conservatively financed acquisition strategy to build market share. Leverage these positions to expand service offerings.

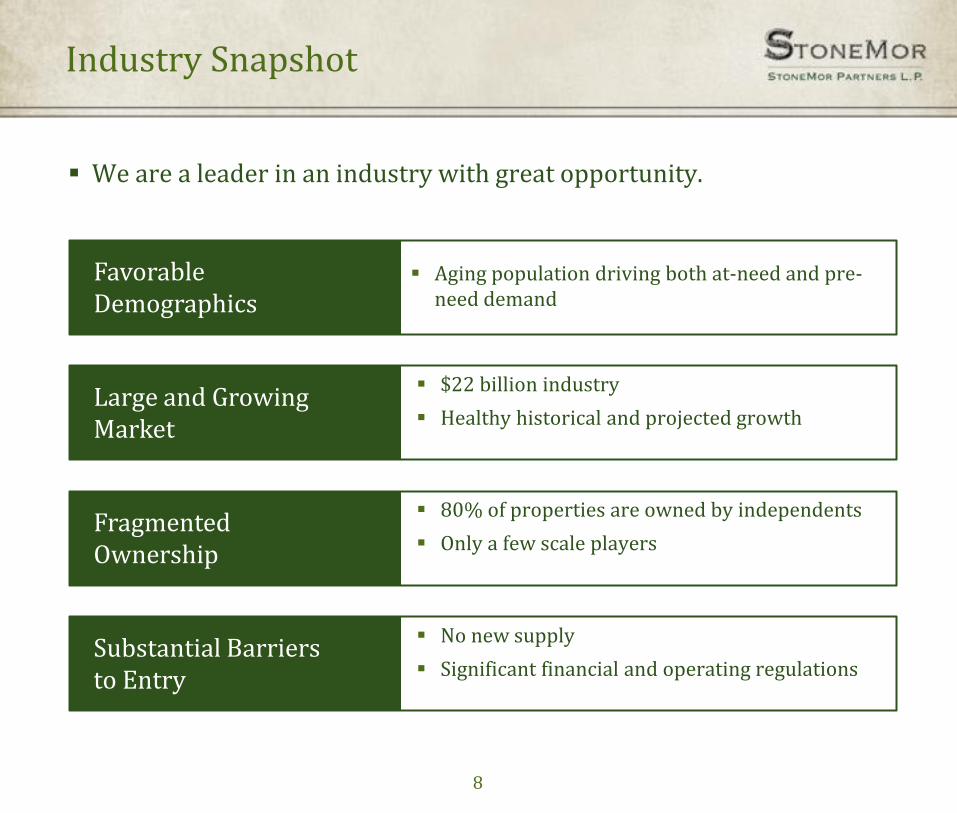

Industry Snapshot

8

We are a leader in an industry with great opportunity.

Aging population driving both at-need and pre-need demand

$22 billion industry

Healthy historical and projected growth

80% of properties are owned by independents

Only a few scale players

No new supply

Significant financial and operating regulations

Favorable Demographics

Large and Growing Market

Fragmented Ownership

Substantial Barriers to Entry

Demographic Tailwinds

9

Source: Department of Health and Human Services.

ANNUAL BIRTHS IN THE U.S. (1930-1960)

Aging of the Baby Boom Generation will:

1. Accelerate the death rate at-need sales

2. Expand our target pre-need market (55 to 65 age range)

− More financially stable and resilient to economic downturns

− Beginning to think of legacy

Source: U.S. Department of Commerce Census Bureau.

PROJECTED U.S. POPULATION OVER 55

87

98 106

112 118

130

2015 2020 2025 2030 2035 2040

(in millions)

1.5

2.0

2.5

3.0

3.5

4.0

4.5

(in millions)

Cemeteries, 10,500, 27%

Funeral Homes &

Crematories 22,000,

73%

$16 billion

$6 billion

Source: National Funeral Directors Association. Source: National Funeral Directors Association; U.S. Census Bureau.

$22 Billion Market

DEATHCARE MARKET SIZE

Large and Growing Industry

Industry growth driven by demographics and supported by ever-

present demand for memorialization and celebrations of life

10

CONTINUED GROWTH

2.1

2.4

2.6

3.3

1990 2000 2010 2030P

Deaths in the U.S. (millions)

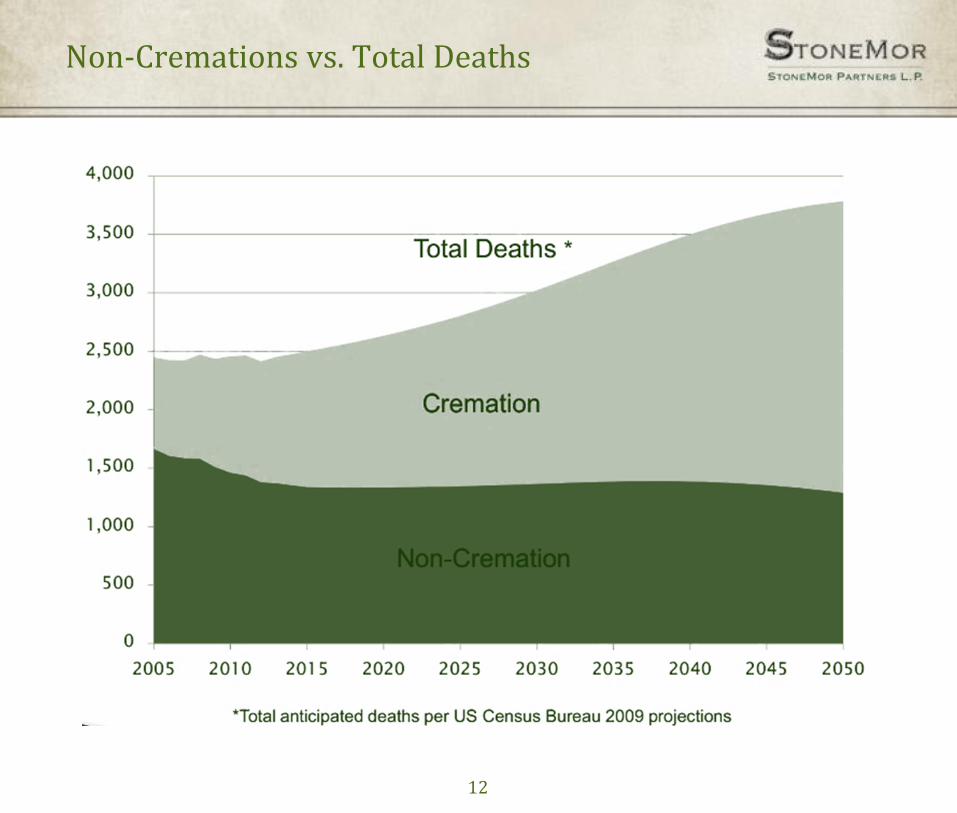

Cremation: Friend (not Foe)

Cremation projected to rise to >50% of total deaths in the U.S. by 2020.

– Well established trend presents a slight headwind for traditional cemetery burials.

However, also represents a key component of our growth strategy.

– Western society still memorializes life regardless of the method of disposition.

11

0%

10%

20%

30%

40%

50%

60%

70%

80%

1995 2000 2005 2010 2015 2020 2025

Cremation as a Percentage of Total Deaths

RISE IN CREMATION…

Stronger linkage between cremation and

memorialization options

− Cremation gardens

− Cremation-related products and services

Increased land utilization

Higher profit margins

Source: National Funeral Directors Association.

…CREATES OPPORTUNITY

12

Non-Cremations vs. Total Deaths

Our Acquisition Approach

13

Disciplined target selection: “never break the model”

Strategic locations to create and/or enhance market clusters

Cemetery

− 25+ year sales life

− 200+ annual interments

Seasoned, professional management

Consolidate office functions into home office

Institute pre-need sales program

Leverage buying power to reduce product costs

Professional trust fund management

Philosophy

Target Criteria

Integration

Funeral

− 150+ Annual Calls

− Strong legacy

Accretive from day one

IRR > cost of capital

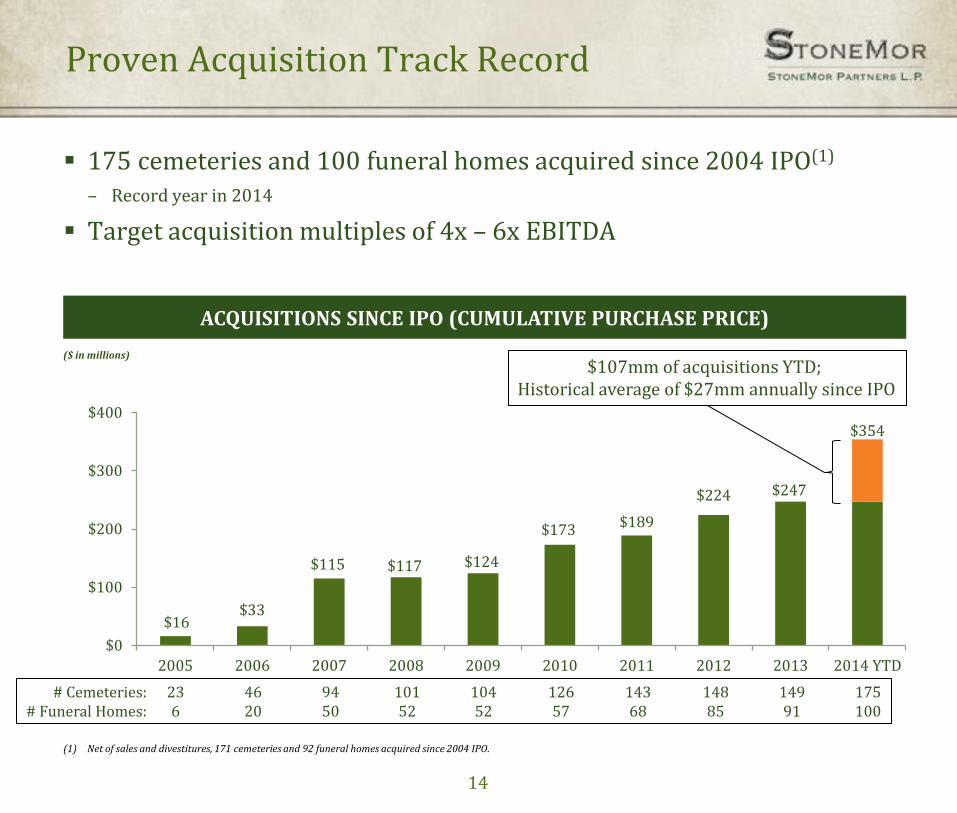

Proven Acquisition Track Record

14

175 cemeteries and 100 funeral homes acquired since 2004 IPO(1)

– Record year in 2014

Target acquisition multiples of 4x – 6x EBITDA

$16 $33

$115 $117 $124

$173 $189

$224 $247

$354

$0

$100

$200

$300

$400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD

ACQUISITIONS SINCE IPO (CUMULATIVE PURCHASE PRICE)

# Cemeteries: # Funeral Homes:

($ in millions)

23 6

46 20

94 50

101 52

104 52

126 57

143 68

148 85

149 91

175 100

(1) Net of sales and divestitures, 171 cemeteries and 92 funeral homes acquired since 2004 IPO.

$107mm of acquisitions YTD; Historical average of $27mm annually since IPO

Key Stats 13 cemeteries leased

60-year management agreement

7,000 existing burials per year

Rationale Strengthen market position in Philadelphia backyard

Introduce pre-need sales to large and growing population

Upside from optimizing productivity of land

Significant opportunities for other Archdioceses

2014 Acquisition Highlights: Archdiocese of Philadelphia

Closed in May 2014 with $53 million initial lease payment

15

Key Stats 12 cemeteries, 9 funeral homes

1,140 acres of land: FL, NC, PA, VA

3,500 annual interments

1,900 annual funeral home calls

Rationale Improve footprint in attractive markets

Upside from implementation of pre-need sales

Significant administrative synergies

$54 million acquisition closed in June 2014

2014 Acquisition Highlights: Service Corporation International

16

Keys to Our Success

17

Growth Through

Disciplined Acquisition

Underwriting

Prudent Balance Sheet Management

Deliver Reliable,

Consistent Value to

Unitholders

We have delivered steady, conservatively financed growth.

Transformational 2014 is an inflection point toward future growth.

Avg. $27mm annual acquisitions (’05-’13)

Target 4x – 6x EBITDA purchase prices

$1.90 $1.93 $2.03 $2.12 $2.22 $2.23 $2.33 $2.35 $2.39 $2.43

2005 2006 2007 2008 2009 2010 2011 2012 2013 TTM

Distributions/LP Unit

Proven Track Record Recent Developments

56%

43% 33% 32%

40% 36% 27%

12/08 12/09 12/10 12/11 12/12 12/13 9/14

Debt / Enterprise Value

2014 acquisitions ~4x average annual pace

AOP and SCI properties operating on plan

Well capitalized GP with AIM’s investment

Two equity raises ($120mm) to de-lever

Refinance senior notes to lower cost of debt

Distributions expected to grow by $0.01 per unit each quarter through the end of 2015

Trust Management

18

Merchandise Trust and

Perpetual Care Trust

Measured Performance*

$492 million (Merchandise Trust)

– All principal, interest and dividends accrue to StoneMor over time

$360 Million (Perpetual Care)

– Principal remains in trust in perpetuity

– Interest and dividends accrue to StoneMor

6% 7%

6% 8%

7%

9%

12/08 12/09 12/10 12/11 12/12 12/13

Merchandise Trust

Investment Management

Governed by investment guidelines adopted by Trust and Compliance Committee of BOD

Balanced approach to preservation of capital

Variety of intermediate-term, investment-grade, fixed income securities, high-yield securities, REITS, MLPs, other equities and cash

8% 8% 7%

6% 6% 5%

12/08 12/09 12/10 12/11 12/12 12/13

Perpetual Care Trust

*Past performance is not indicative of future performance

19

Strong Recent Results

PRODUCTION-BASED REVENUE

($ in millions)

ADJUSTED OPERATING PROFIT

($ in millions)

DISTRIBUTABLE FCF

($ in millions)

We deliver reliable, predictable yield with accelerating growth.

We focus on three financial metrics. – Production-based Revenue: total value of contracts written, investment and other income

– Adjusted Operating Profit: normalizes timing-related differences between GAAP and accrual

– Distributable Free Cash Flow: indicator of our ability to pay distributions to our unitholders

$296

$327

$240

$264

$0

$50

$100

$150

$200

$250

$300

$350

2012 2013 Q3'13YTD

Q3'14YTD

$54

$67

$47 $50

$0

$10

$20

$30

$40

$50

$60

$70

$80

2012 2013 Q3'13YTD

Q3'14YTD

$53

$76

$57

$50

$0

$10

$20

$30

$40

$50

$60

$70

$80

2012 2013 Q3'13YTD*

Q3'14YTD

*Includes $11.9 million one-time gain from legal settlement

($ in millions) ($ in millions)

REVENUE OPERATING PROFIT

Historical Performance

Steady growth as we have built the business through acquisitions and pre-need sales efforts

GAAP results not indicative of true financial performance

20

$13

$3

$10

$14

$6

$13

$36 $38

$49

$54

$67 $71

2009 2010 2011 2012 2013 Q3'14TTM

GAAP Old GAAP

$181 $197

$228 $243 $246

$277

$218

$247

$281 $296

$327

$350

2009 2010 2011 2012 2013 Q3'14TTM

GAAP Old GAAP

Low-Risk Balance Sheet

Marketable assets provide full debt protection

21

$656

$191

$41

$154

$270

$0

$100

$200

$300

$400

$500

$600

$700

Cash, AR andMerchandise Trust

AP and AccruedLiabilities

Merchandise Liability Debt Excess Cash and Assets

NET LIQUID ASSETS

($ in millions)

Significant additional value from long-term assets

− Cemetery Property

• Approximately 12,490 acres, weighted average sales life of over 240 years

• $341 million book value as of September 30, 2014

− Perpetual Care Trusts

• Fund future maintenance costs

• Assets of $349 million as of September 30, 2014

22

Substantial Distribution Coverage

History of sustained distributions and significant coverage

($ in millions)

ADJUSTED OPERATING PROFIT AND DISTRIBUTIONS

$36 $38

$49

$54

$67 $71

$27

$32

$45 $47

$51

$59

$13

$3

$10 $14

$6

$13

$0

$10

$20

$30

$40

$50

$60

$70

$80

2009 2010 2011 2012 2013 Q3'14 TTM

Adjusted Operating Profit Distributions GAAP Operating Profit

StoneMor Value Proposition Recap

23

Stable and Growing Cash Flow

Key Attributes of High-Performing MLPs StoneMor?

Long-lived, Secure Assets

Defensible Competitive Advantage

Attractive Industry Fundamentals

Conservative Financial Profile

StoneMor features the key attributes of high-performing MLPs, as well as an attractive total return profile.

STON TEN YEAR AVERAGE ANNUAL TOTAL RETURN vs. BENCHMARK ASSET CLASSES

Total Return Results

24

13.5% 12.8%

11.0% 10.5%

7.8% 7.6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

StoneMor Alerian MLP Index NASDAQ 100 DJ Utility Index Russell 2000 S&P 500

Source: Bloomberg and Index monthly reports. Market data as of 2-26-15.

Total Return %

Thank You