Embed Size (px)

Citation preview

May 2016

INVESTOR PRESENTATION

2

Safe Harbor / Disclaimer

This presentation includes forward-looking statements within the meaning of the Private Securities Litigation Reform

Act of 1995, which relate to future, not past, events and are subject to risks and uncertainties. The forward-looking

statements, which address the Company's expected business and financial performance and financial condition,

among other matters, contain words such as: “believe,” “could,” “opportunities,” “continue,” “expect,” “may,” “will,” or

“would” and other words and terms of similar meaning.

Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as

statements about expected income; earnings; revenues; and growth. Although the Company believes the

expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no

assurance that the expectations will be attained or that any deviation will not be material. Readers are cautioned not to

place undue reliance on these forward-looking statements, which speak only as of the date on which they are made.

Factors that could cause actual results to differ materially from these forward-looking statements can be found in the

Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and the Company’s other reports filed with

the Securities and Exchange Commission. These or other uncertainties may cause the Company’s actual future

results to be materially different than those expressed in any forward-looking statements. The Company undertakes

no obligation to update or revise any forward-looking statements.

This presentation also contains estimates and other statistical data made by independent parties and by us relating to

market size and growth and other data about our industry. This data involves a number of assumptions and limitations,

and you are cautioned not to give undue weight to such estimates. In addition, projections, assumptions and estimates

of our future performance and the future performance of the markets in which we operate are necessarily subject to a

high degree of uncertainty and risk.

This presentation also contains non-GAAP financial measures. You can find a reconciliation of the non-GAAP financial

measures to the most directly comparable GAAP financial measures in the appendix to this presentation.

Press Ganey Overview

Mission

To help healthcare organizations reduce patient and caregiver

suffering and improve clinical quality, safety and the overall

patient experience

Transformational Solutions

Patient Experience

Caregiver Engagement

Clinical Quality

Reliability & Safety

3

4

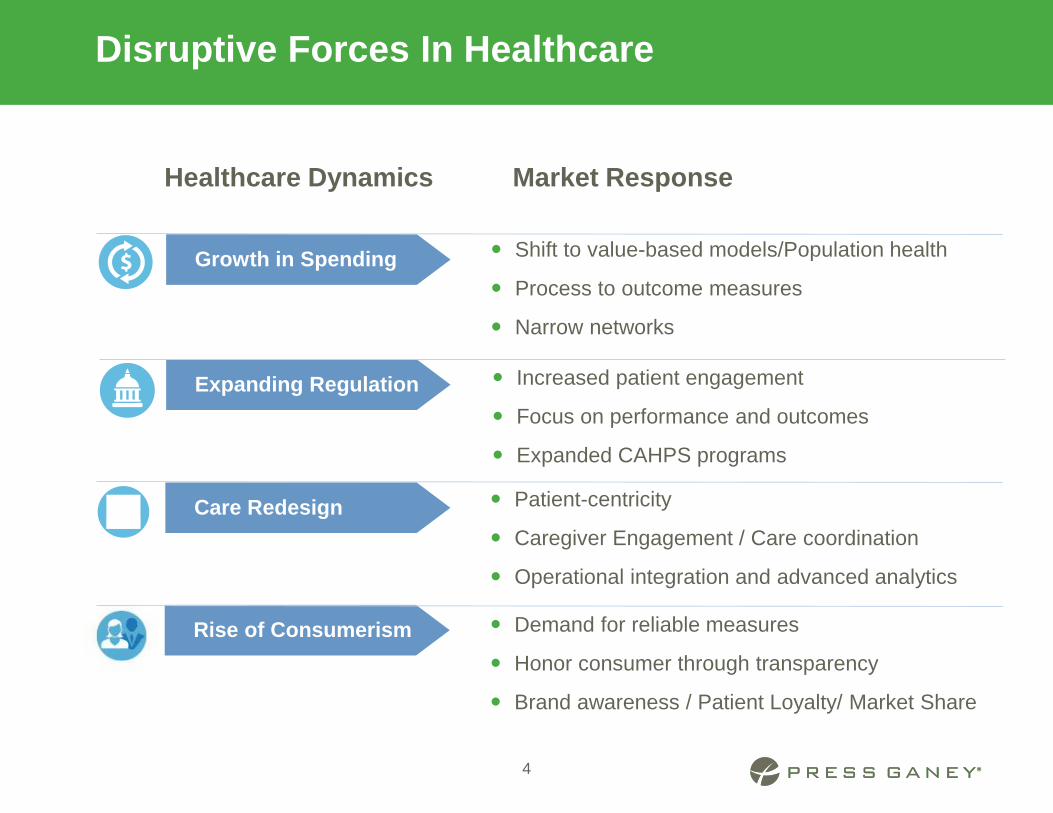

Disruptive Forces In Healthcare

Shift to value-based models/Population health

Process to outcome measures

Narrow networks

Growth in Spending

Patient-centricity

Caregiver Engagement / Care coordination

Operational integration and advanced analytics

Demand for reliable measures

Honor consumer through transparency

Brand awareness / Patient Loyalty/ Market Share

Increased patient engagement

Focus on performance and outcomes

Expanded CAHPS programs

Care Redesign

Market ResponseHealthcare Dynamics

Expanding Regulation

Rise of Consumerism

Industry Leader With Partners AcrossThe Continuum Of Care

80%+

60%+

80%+

70%+

Note: All information as of 12/31/155

Acute Hospitals

Major Teaching Hospitals

MD Groups w/ >50 Physicians

Acute Hospitals w/ 100+ Beds

6

Strategic Competitive Advantage

Competitive Forces Competitive Forces

Competitive Forces Competitive Forces

OUR SOLUTIONS

Actionable data targeting improvement opportunities

Drive patient loyalty, improve outcomes, optimize reimbursement

Operational, Clinical & Financial Performance Improvement

8

Engagement insights tiered for effective action planning

Retain caregivers, increase productivity, improve performance

Measure, report and act on clinical and quality performance

Achieve nursing excellence and quality standards, improve outcomes

Assess operational, quality and safety performance

Transform culture, reduce safety events, achieve high reliability

C-Level Solutions that Drive Performance Improvement

Patient

Experience

Dem

on

str

ate

d R

OI

Caregiver

Engagement

Clinical &

Quality Outcomes

Reliability &

Safety Consulting

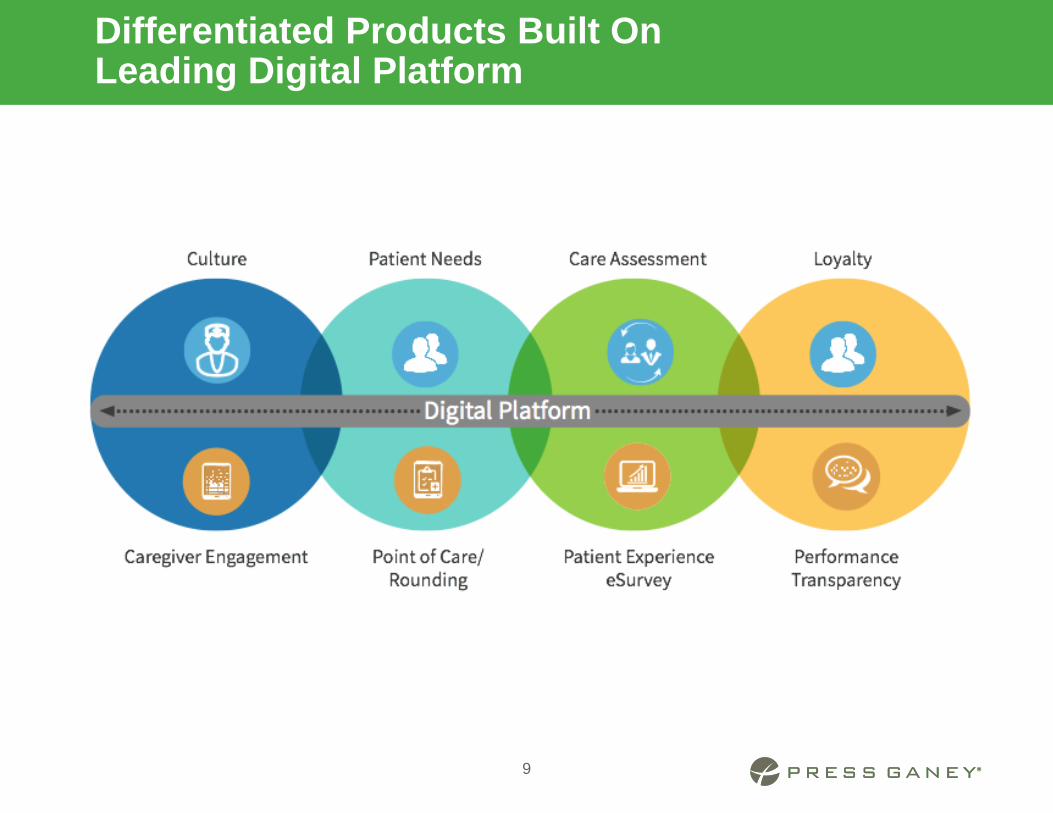

Differentiated Products Built On Leading Digital Platform

9

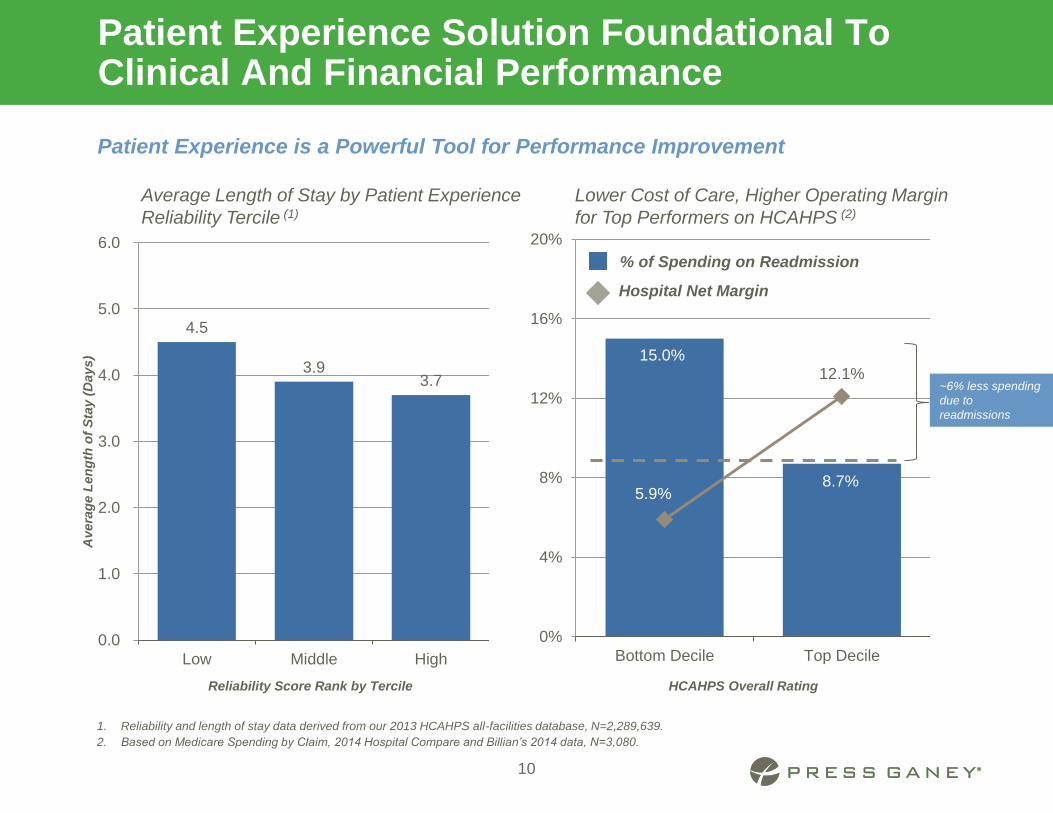

4.5

3.9 3.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Low Middle High

Avera

ge L

en

gth

of

Sta

y (

Days)

Reliability Score Rank by Tercile

1. Reliability and length of stay data derived from our 2013 HCAHPS all-facilities database, N=2,289,639.

2. Based on Medicare Spending by Claim, 2014 Hospital Compare and Billian’s 2014 data, N=3,080.

15.0%

8.7%5.9%

12.1%

0%

4%

8%

12%

16%

20%

Bottom Decile Top Decile

~6% less spending

due to

readmissions

Patient Experience Solution Foundational To Clinical And Financial Performance

Average Length of Stay by Patient Experience

Reliability Tercile (1)

Lower Cost of Care, Higher Operating Margin

for Top Performers on HCAHPS (2)

Patient Experience is a Powerful Tool for Performance Improvement

Hospital Net Margin

10

% of Spending on Readmission

HCAHPS Overall Rating

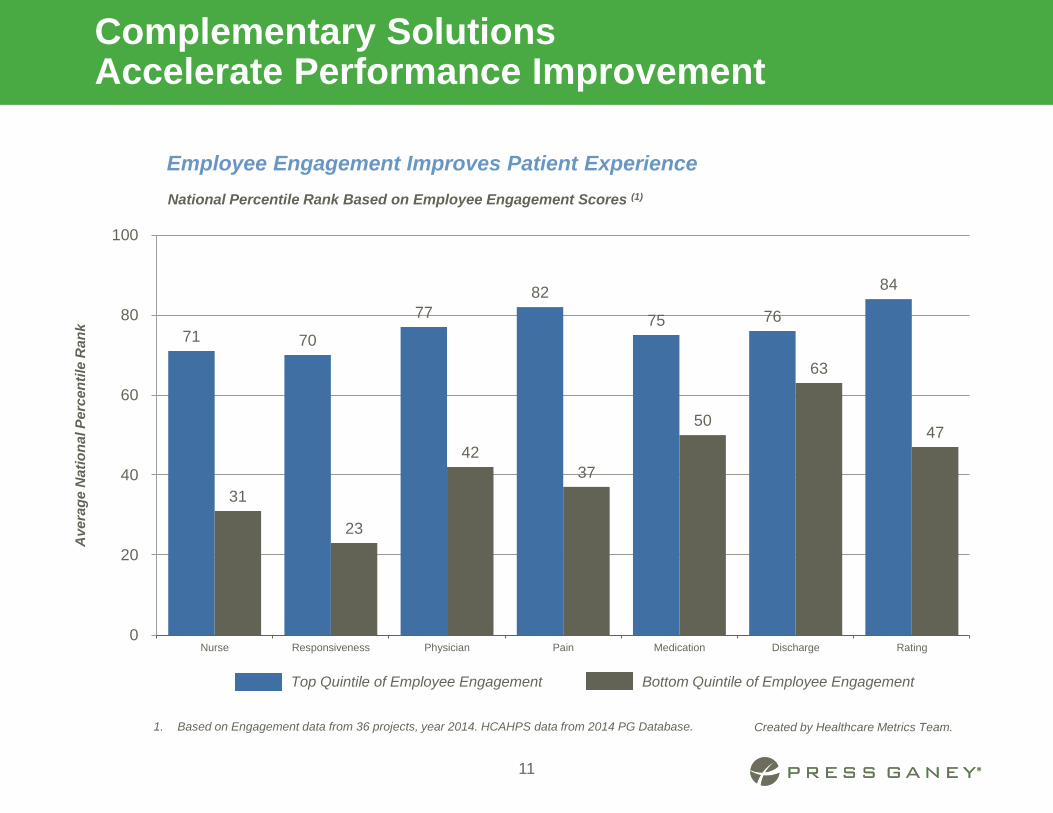

71 70

77

82

75 76

84

31

23

42

37

50

63

47

0

20

40

60

80

100

Nurse Responsiveness Physician Pain Medication Discharge Rating

Av

era

ge

Na

tio

na

l P

erc

en

tile

Ra

nk

Top Quintile of Employee Engagement Bottom Quintile of Employee Engagement

National Percentile Rank Based on Employee Engagement Scores (1)

Employee Engagement Improves Patient Experience

1. Based on Engagement data from 36 projects, year 2014. HCAHPS data from 2014 PG Database.

Complementary Solutions Accelerate Performance Improvement

11

Created by Healthcare Metrics Team.

12

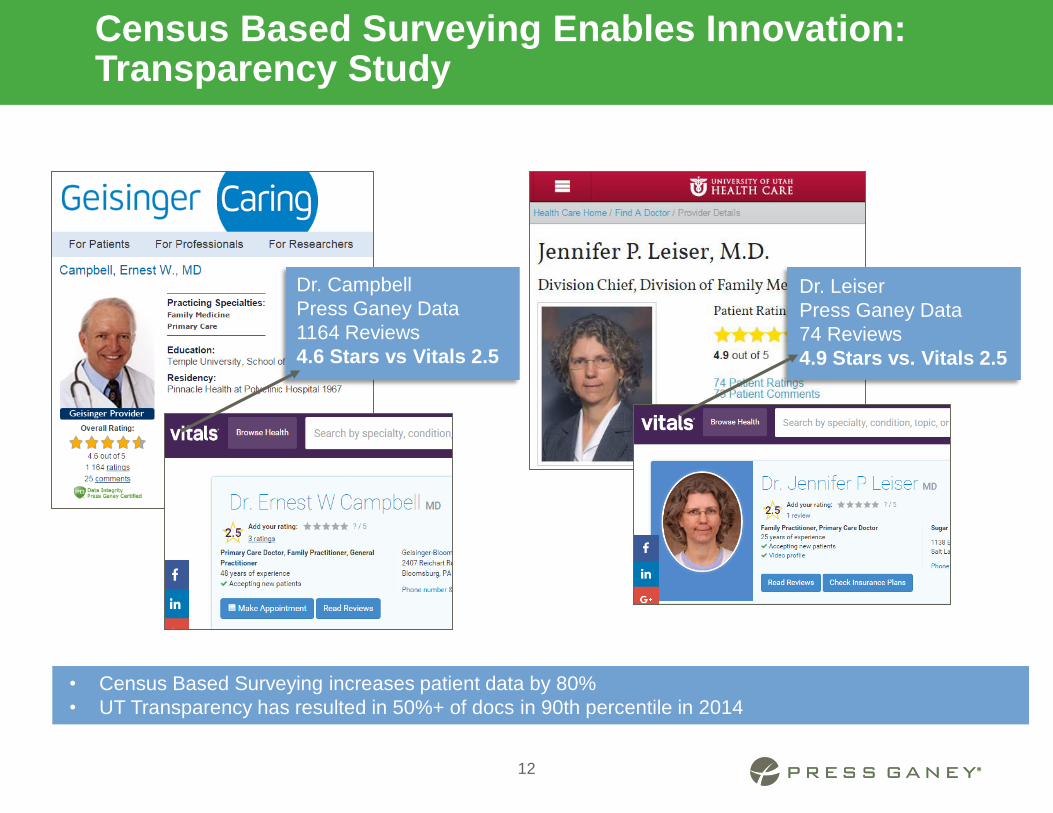

Census Based Surveying Enables Innovation: Transparency Study

• Census Based Surveying increases patient data by 80%

• UT Transparency has resulted in 50%+ of docs in 90th percentile in 2014

Dr. Campbell

Press Ganey Data

1164 Reviews

4.6 Stars vs Vitals 2.5

Dr. Leiser

Press Ganey Data

74 Reviews

4.9 Stars vs. Vitals 2.5

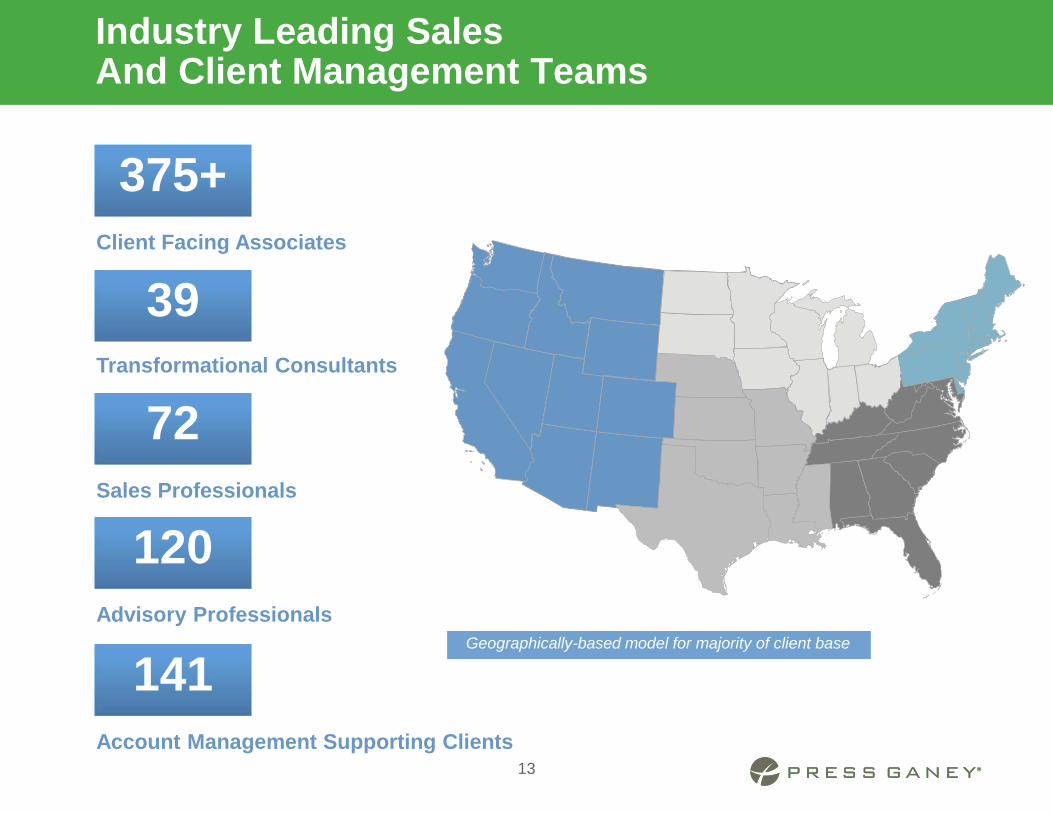

Industry Leading Sales And Client Management Teams

13

375+

Client Facing Associates

Transformational Consultants

Sales Professionals

Advisory Professionals

Account Management Supporting Clients

39

72

120

141Geographically-based model for majority of client base

Innovation And Thought Leadership Offer Deeper Value To Clients

Executive Council

members of Press

Ganey nonprofit

Speaking

engagements

Clients at national

conference

Attendees across

regional symposiums

Monthly user logins

for improvement

solutions

14

Investing in Thought Leadership

28 245+

2,800

1,000+

265,000+

Industry articles in key

trade publications

Participants in the

online community

Custom analytic reports

generated annually

300+

26,0003,000+

Participants in

CNO Quarterly Best

Practices Roundtable

250

GROWTH STRATEGY / TOTAL ADDRESSABLE MARKET

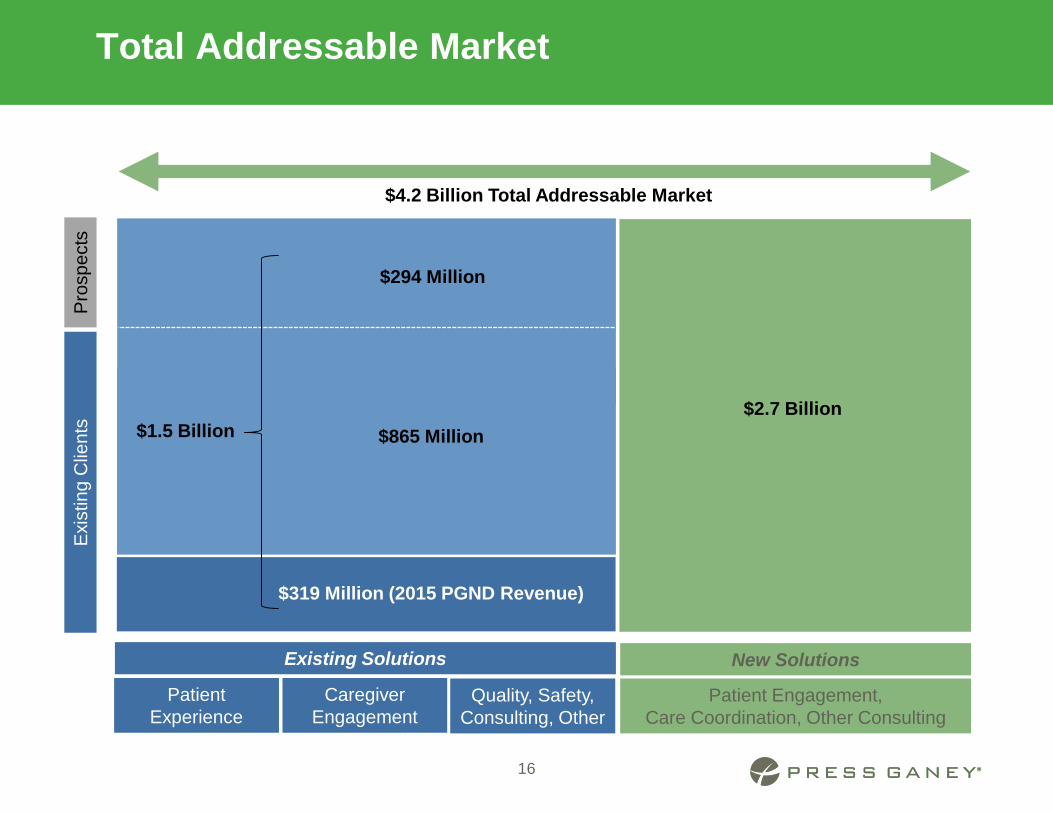

Total Addressable Market

16

Quality, Safety,

Consulting, Other

Exis

ting C

lients

Pro

spects

Patient

Experience

Caregiver

Engagement

$319 Million (2015 PGND Revenue)

Patient Engagement,

Care Coordination, Other Consulting

$865 Million

$294 Million

$2.7 Billion

New SolutionsExisting Solutions

$4.2 Billion Total Addressable Market

$1.5 Billion

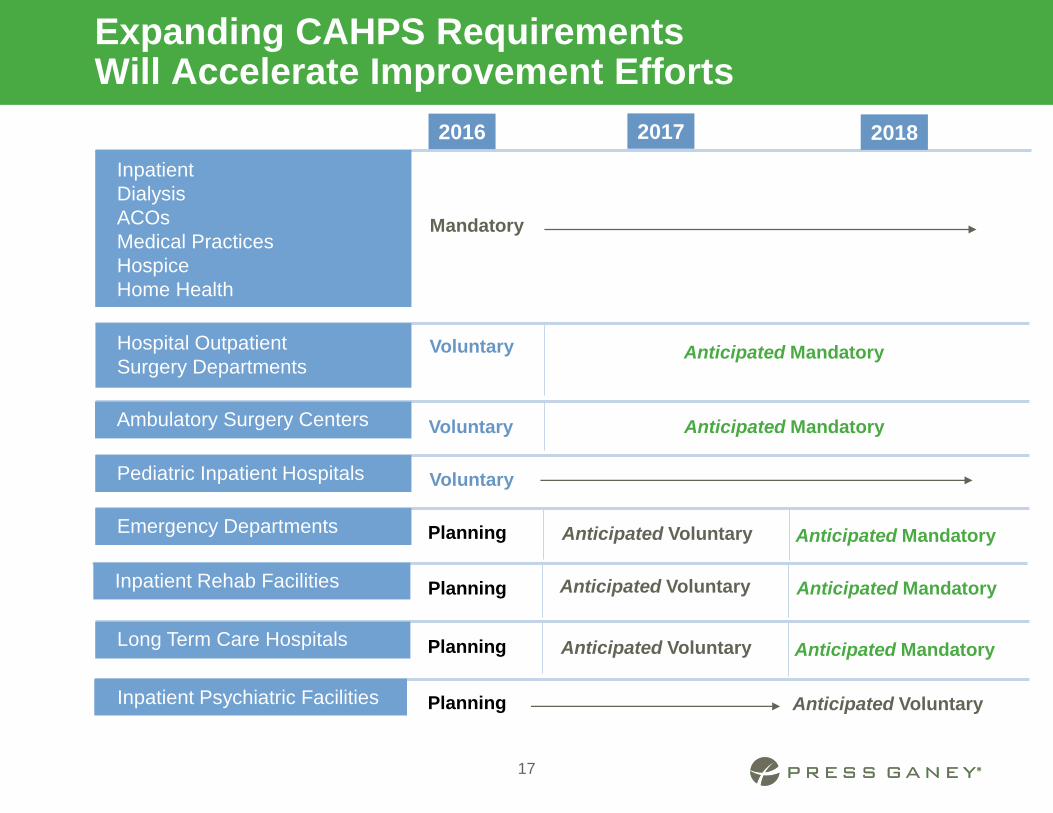

Expanding CAHPS Requirements Will Accelerate Improvement Efforts

2%17 2%2%

2%

Hospital Outpatient

Surgery DepartmentsVoluntary Anticipated Mandatory

2016 2017 2018

Ambulatory Surgery Centers Voluntary Anticipated Mandatory

Pediatric Inpatient Hospitals

Emergency Departments Planning Anticipated Voluntary Anticipated Mandatory

Long Term Care Hospitals Planning Anticipated Voluntary Anticipated Mandatory

Inpatient Psychiatric Facilities Planning Anticipated Voluntary

Inpatient

Dialysis

ACOs

Medical Practices

Hospice

Home Health

Mandatory

Inpatient Rehab Facilities Planning Anticipated Voluntary Anticipated Mandatory

Voluntary

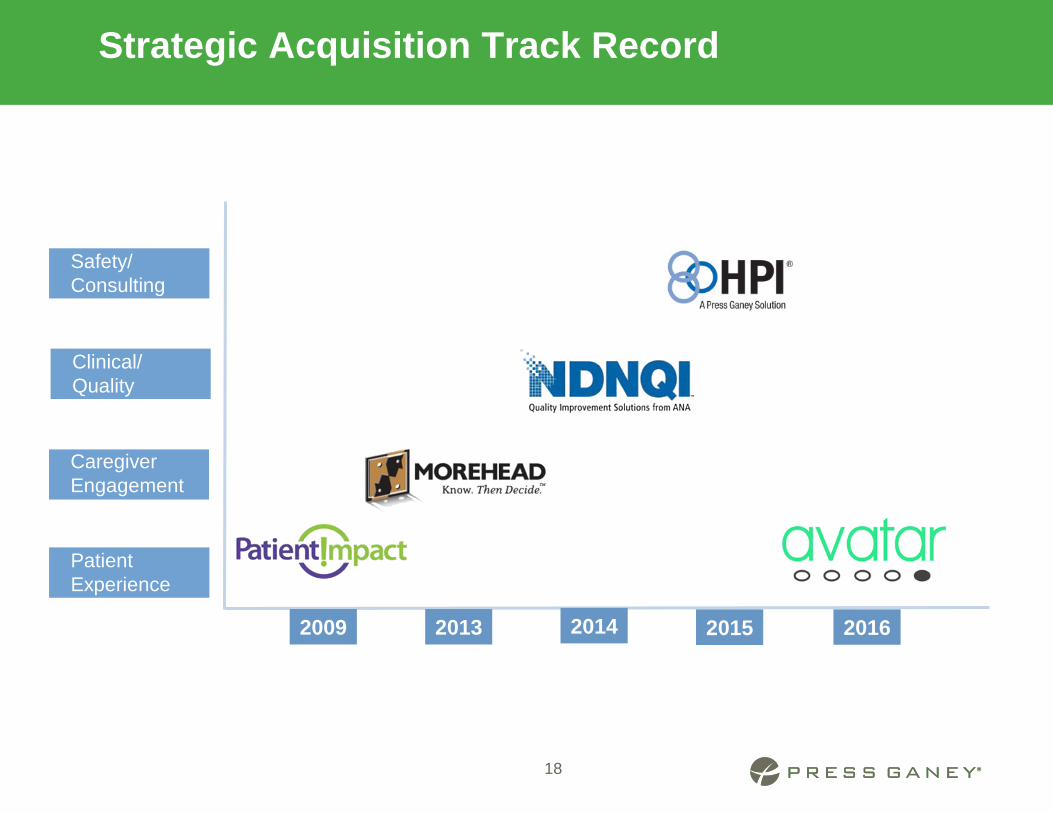

Strategic Acquisition Track Record

18

2009

Caregiver

Engagement

Safety/

Consulting

Clinical/

Quality

Patient

Experience

2013 2014 2015 2016

FINANCIAL REVIEW

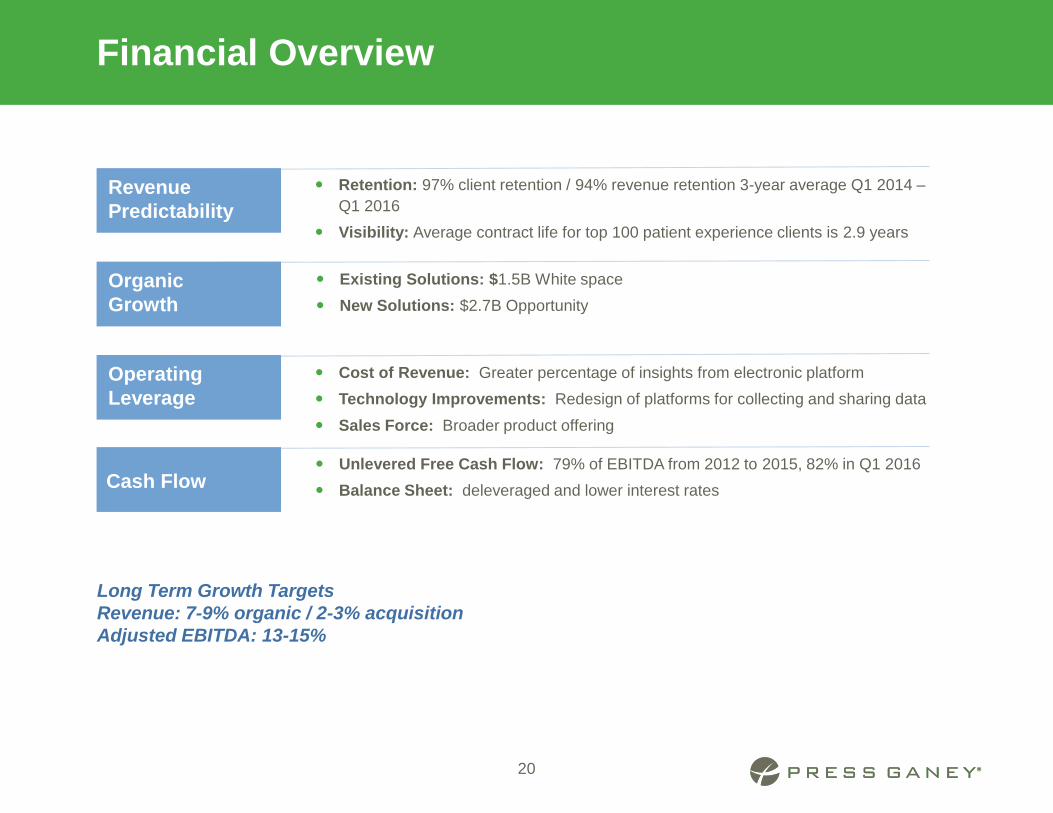

Financial Overview

20

Revenue

Predictability

Retention: 97% client retention / 94% revenue retention 3-year average Q1 2014 –

Q1 2016

Visibility: Average contract life for top 100 patient experience clients is 2.9 years

Existing Solutions: $1.5B White space

New Solutions: $2.7B Opportunity

Cost of Revenue: Greater percentage of insights from electronic platform

Technology Improvements: Redesign of platforms for collecting and sharing data

Sales Force: Broader product offering

Unlevered Free Cash Flow: 79% of EBITDA from 2012 to 2015, 82% in Q1 2016

Balance Sheet: deleveraged and lower interest rates

Organic

Growth

Operating

Leverage

Cash Flow

Long Term Growth Targets

Revenue: 7-9% organic / 2-3% acquisition

Adjusted EBITDA: 13-15%

$0

$50

$100

$150

$200

$250

$300

$350

2012 2013 2014 2015 1Q15 1Q16

Revenue

Growth Track Record

($ in millions)

$0

$25

$50

$75

$100

$125

2012 2013 2014 2015 1Q15 1Q16

Adjusted EBITDA

21

5.4x

4.6x

4.0x

1.3x1.0x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

2012 2013 2014 2015 1Q16

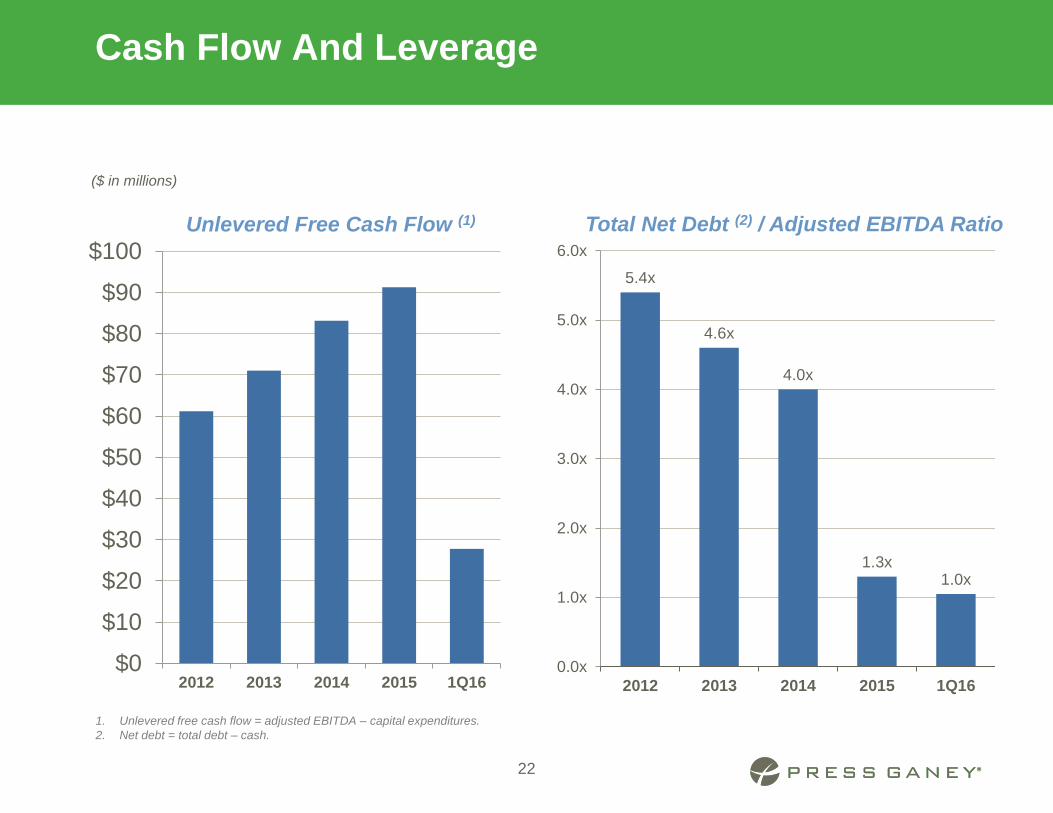

Total Net Debt (2) / Adjusted EBITDA Ratio

Cash Flow And Leverage

1. Unlevered free cash flow = adjusted EBITDA – capital expenditures.

2. Net debt = total debt – cash.

($ in millions)

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2012 2013 2014 2015 1Q16

Unlevered Free Cash Flow (1)

22

APPENDIX

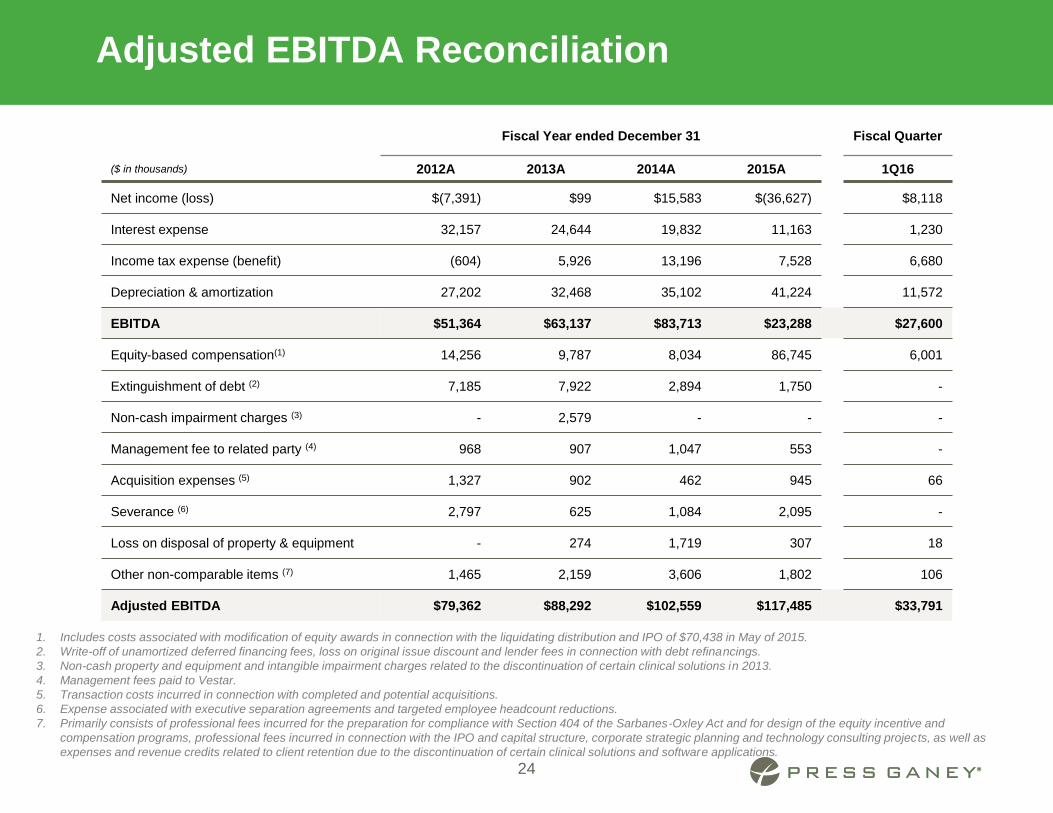

Adjusted EBITDA Reconciliation

1. Includes costs associated with modification of equity awards in connection with the liquidating distribution and IPO of $70,438 in May of 2015.

2. Write-off of unamortized deferred financing fees, loss on original issue discount and lender fees in connection with debt refinancings.

3. Non-cash property and equipment and intangible impairment charges related to the discontinuation of certain clinical solutions in 2013.

4. Management fees paid to Vestar.

5. Transaction costs incurred in connection with completed and potential acquisitions.

6. Expense associated with executive separation agreements and targeted employee headcount reductions.

7. Primarily consists of professional fees incurred for the preparation for compliance with Section 404 of the Sarbanes-Oxley Act and for design of the equity incentive and

compensation programs, professional fees incurred in connection with the IPO and capital structure, corporate strategic planning and technology consulting projects, as well as

expenses and revenue credits related to client retention due to the discontinuation of certain clinical solutions and software applications.

Fiscal Year ended December 31 Fiscal Quarter

($ in thousands) 2012A 2013A 2014A 2015A 1Q16

Net income (loss) $(7,391) $99 $15,583 $(36,627) $8,118

Interest expense 32,157 24,644 19,832 11,163 1,230

Income tax expense (benefit) (604) 5,926 13,196 7,528 6,680

Depreciation & amortization 27,202 32,468 35,102 41,224 11,572

EBITDA $51,364 $63,137 $83,713 $23,288 $27,600

Equity-based compensation(1) 14,256 9,787 8,034 86,745 6,001

Extinguishment of debt (2) 7,185 7,922 2,894 1,750 -

Non-cash impairment charges (3) - 2,579 - - -

Management fee to related party (4) 968 907 1,047 553 -

Acquisition expenses (5) 1,327 902 462 945 66

Severance (6) 2,797 625 1,084 2,095 -

Loss on disposal of property & equipment - 274 1,719 307 18

Other non-comparable items (7) 1,465 2,159 3,606 1,802 106

Adjusted EBITDA $79,362 $88,292 $102,559 $117,485 $33,791

24

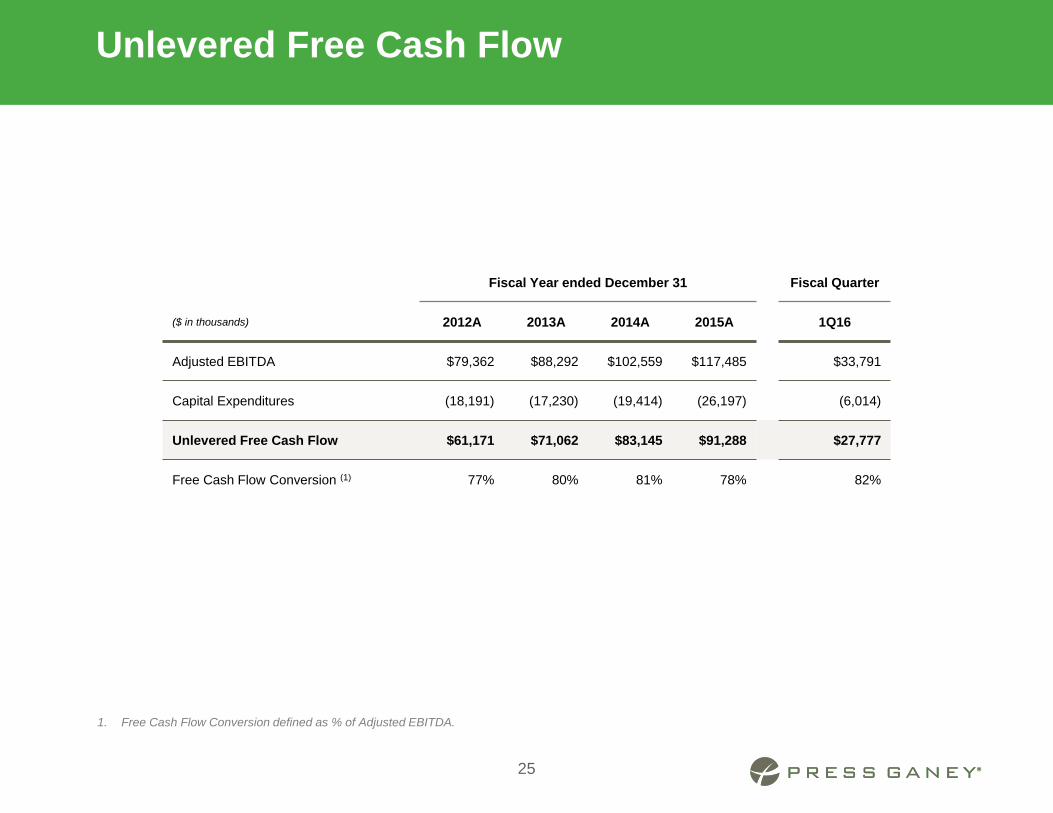

Unlevered Free Cash Flow

Fiscal Year ended December 31 Fiscal Quarter

($ in thousands) 2012A 2013A 2014A 2015A 1Q16

Adjusted EBITDA $79,362 $88,292 $102,559 $117,485 $33,791

Capital Expenditures (18,191) (17,230) (19,414) (26,197) (6,014)

Unlevered Free Cash Flow $61,171 $71,062 $83,145 $91,288 $27,777

Free Cash Flow Conversion (1) 77% 80% 81% 78% 82%

1. Free Cash Flow Conversion defined as % of Adjusted EBITDA.

25

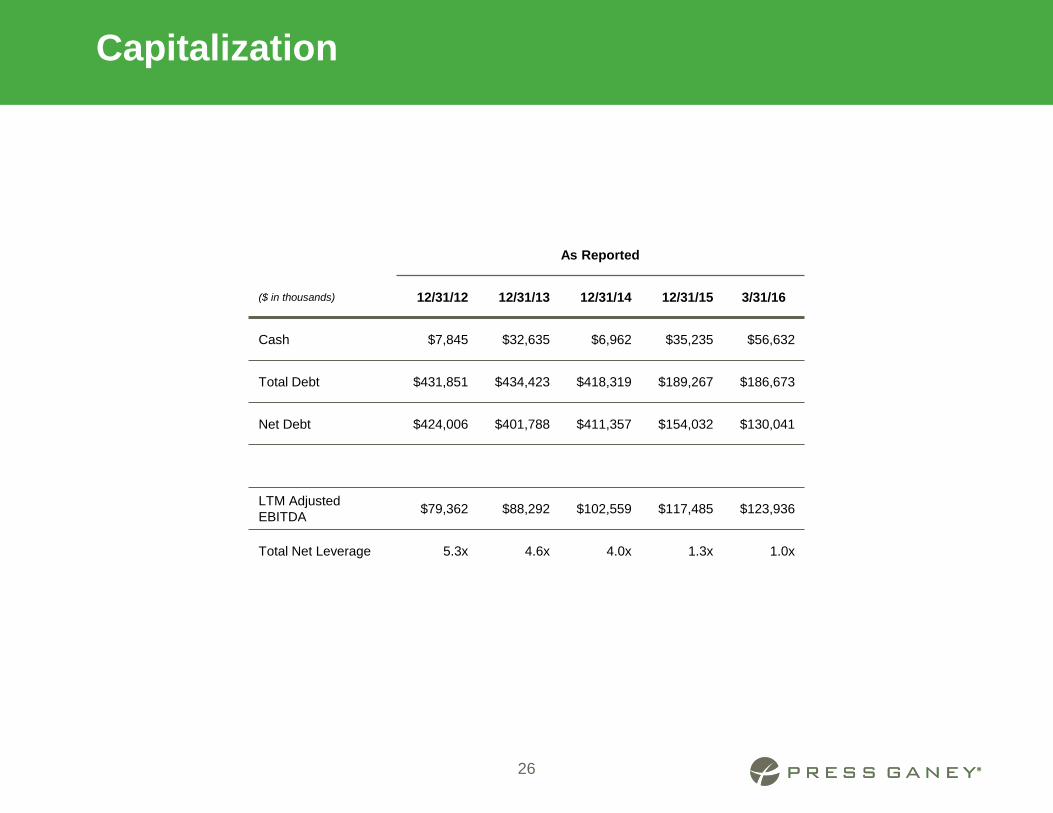

Capitalization

As Reported

($ in thousands) 12/31/12 12/31/13 12/31/14 12/31/15 3/31/16

Cash $7,845 $32,635 $6,962 $35,235 $56,632

Total Debt $431,851 $434,423 $418,319 $189,267 $186,673

Net Debt $424,006 $401,788 $411,357 $154,032 $130,041

LTM Adjusted

EBITDA $79,362 $88,292 $102,559 $117,485 $123,936

Total Net Leverage 5.3x 4.6x 4.0x 1.3x 1.0x

26

![Investor Relations - hanatourcompany.comhanatour]ir_presentation_june... · Investor Relations 1 Investor Relations Jun. 2009.(Korean) 2 ... (cf. 국내소비0.3% 증가, 자료:한국은행,2006)](https://img.dokumen.tips/doc/110x75/5a881d307f8b9a87368ecd91/investor-relations-hanatourirpresentationjuneinvestor-relations-1-investor.jpg)