Embed Size (px)

Citation preview

the beautiful door

Fall 2016

Investor Presentation

NYSE: DOOR

2

Safe Harbor / Non-GAAP Financial Measures

SAFE HARBOR / FORWARD LOOKING STATEMENT

This investor presentation contains forward-looking information and other forward-looking statements within the meaning of applicable Canadian and/or U.S. securities laws, including our discussion of

improvements in the housing market and related markets and the effects of our pricing and other strategies. When used in this Investor Presentation, such forward-looking statements may be identified

by the use of such words as “may,” might, “could,” “will,” would,” “should,” “expect,” “believes,” “outlook,” “predict,” “forecast,” “framework,” “objective,” “remain,” “anticipate,” “estimate,” “potential,”

“continue,” “plan,” “project,” “targeting,” or the negative of these terms or other similar terminology.

Forward-looking statements involve significant known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of Masonite, or industry

results, to be materially different from any future plans, goals, targets, objectives, results, performance or achievements expressed or implied by such forward-looking statements. As a result, such

forward-looking statements should not be read as guarantees of future performance or results, should not be unduly relied upon, and will not necessarily be accurate indications of whether or not such

results will be achieved. Factors that could cause actual results to differ materially from the results discussed in the forward-looking statements include, but are not limited to, our ability to successfully

implement our business strategy; general economic, market and business conditions; levels of residential new construction, residential repair, renovation and remodeling and non-residential building

construction activity; competition; our ability to manage our operations including integrating our recent acquisitions and companies or assets we acquire in the future; our ability to generate sufficient

cash flows to fund our capital expenditure requirements and to meet our debt service obligations, including our obligations under our senior notes and our senior secured asset-backed credit facility;

labor relations (i.e., disruptions, strikes or work stoppages), labor costs, and availability of labor; increases in the costs of raw materials or any shortage in supplies; our ability to keep pace with

technological developments; the actions by, and the continued success of, certain key customers; our ability to maintain relationships with certain customers; new contractual commitments; our ability to

generate the benefits of our restructuring activities; retention of key management personnel; environmental and other government regulations; limitations on operating our business as a result of

covenant restrictions under our existing and future indebtedness, including our senior notes and senior secured asset-based credit facility; and other factors publicly disclosed by the company from time

to time.

NON-GAAP FINANCIAL MEASURES

Our management reviews net sales and Adjusted EBITDA (as defined below) to evaluate segment performance and allocate resources. Net assets are not allocated to the reportable segments.

Adjusted EBITDA is a non-GAAP financial measure which does not have a standardized meaning under GAAP and is unlikely to be comparable to similar measures used by other companies. Adjusted

EBITDA should not be considered as an alternative to either net income or operating cash flows determined in accordance with GAAP. Additionally, Adjusted EBITDA is not intended to be a measure of

free cash flow for management's discretionary use, as it does not include certain cash requirements such as interest payments, tax payments and debt service requirements. Beginning with the third

quarter of 2015, we revised our calculation of Adjusted EBITDA to separately exclude loss (gain) on disposal of subsidiaries. The revision to this definition had no impact on our reported Adjusted

EBITDA for the three months ended March 29, 2015. Adjusted EBITDA (as revised) is defined as net income (loss) attributable to Masonite adjusted to exclude the following items: depreciation;

amortization; share based compensation expense; loss (gain) on disposal of property, plant and equipment; registration and listing fees; restructuring costs; asset impairment; loss (gain) on disposal of

subsidiaries; interest expense (income), net; loss on extinguishment of debt; other expense (income), net; income tax expense (benefit); loss (income) from discontinued operations, net of tax; and net

income (loss) attributable to non-controlling interest. This definition of Adjusted EBITDA differs from the definitions of EBITDA contained in the indenture governing the 2023 Notes and the credit

agreement governing the ABL Facility. Adjusted EBITDA, as calculated under our ABL Facility or senior notes would also include, among other things, additional add-backs for amounts related to: cost

savings projected by us in good faith to be realized as a result of actions taken or expected to be taken prior to or during the relevant period; fees and expenses in connection with certain plant closures

and layoffs; and the amount of any restructuring charges, integration costs or other business optimization expenses or reserve deducted in the relevant period in computing consolidated net income,

including any one-time costs incurred in connection with acquisitions. The tables in the appendix to this presentation reconcile Adjusted EBITDA to net income (loss) attributable to Masonite for the

periods indicated. We are not providing a quantitative reconciliation of our Adjusted EBITDA outlook to the corresponding GAAP information because the GAAP measures that we exclude from our

Adjusted EBITDA outlook are difficult to predict and are primarily dependent on future uncertainties.

3

Company & Industry Update

the beautiful door

4

Company & Industry Update

Masonite Is a Leading Building Products Company

Company Overview

Net Sales of $1.9 billion and approximately

33 million doors sold in 2015.

Served more than 8,000 customers in 73

countries.

One of only two vertically integrated

residential molded door manufacturers and

the only vertically integrated architectural

door manufacturer in North America.

Established leadership positions in all

targeted product categories in North

America.

Leading value proposition, acquisition

activity and Lean Sigma efforts have

transformed Masonite into a better

positioned, more efficient operating

company

5

North American Residential, 64%

Europe, 17%

Architectural, 16%

Corp & Other, 4%

Company & Industry Update

Diversified End Markets

Primarily serves new residential

construction and residential

repair, renovation and remodel

(RRR) market Tied substantially to the UK new

residential construction and RRR

market.

Serves the North American

commercial construction market

Masonite’s diverse customer base and end markets provide multiple growth avenues

2015 Net Sales

6

RRR, 55%

New Residential Construction,

45%

Company & Industry Update

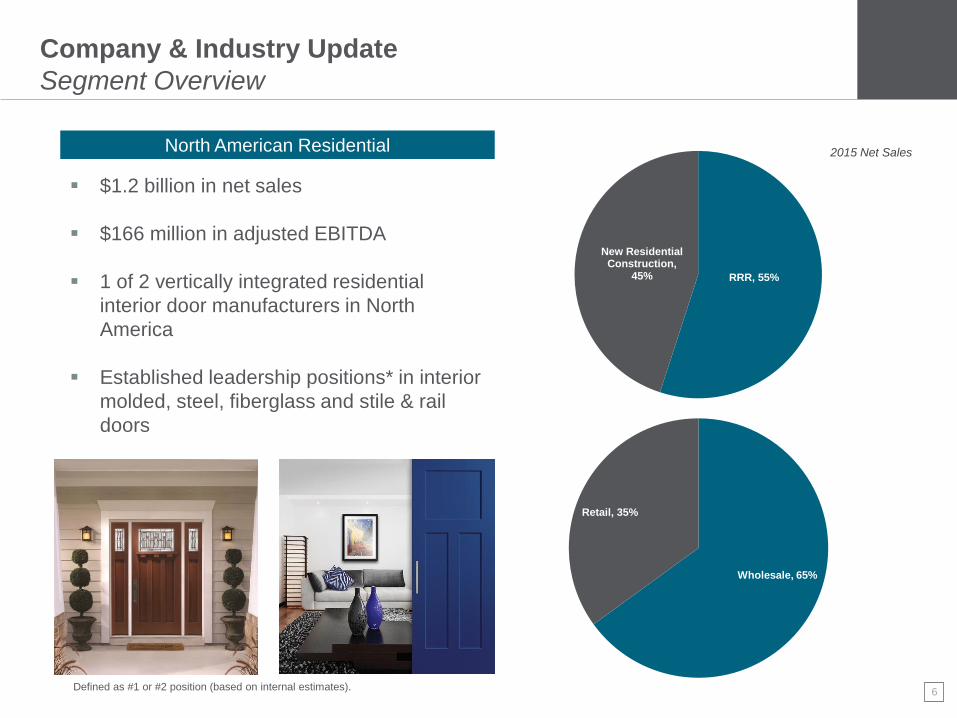

Segment Overview

North American Residential

$1.2 billion in net sales

$166 million in adjusted EBITDA

1 of 2 vertically integrated residential

interior door manufacturers in North

America

Established leadership positions* in interior

molded, steel, fiberglass and stile & rail

doors

2015 Net Sales

Wholesale, 65%

Retail, 35%

Defined as #1 or #2 position (based on internal estimates).

7

UK, 90%

Other, 10%

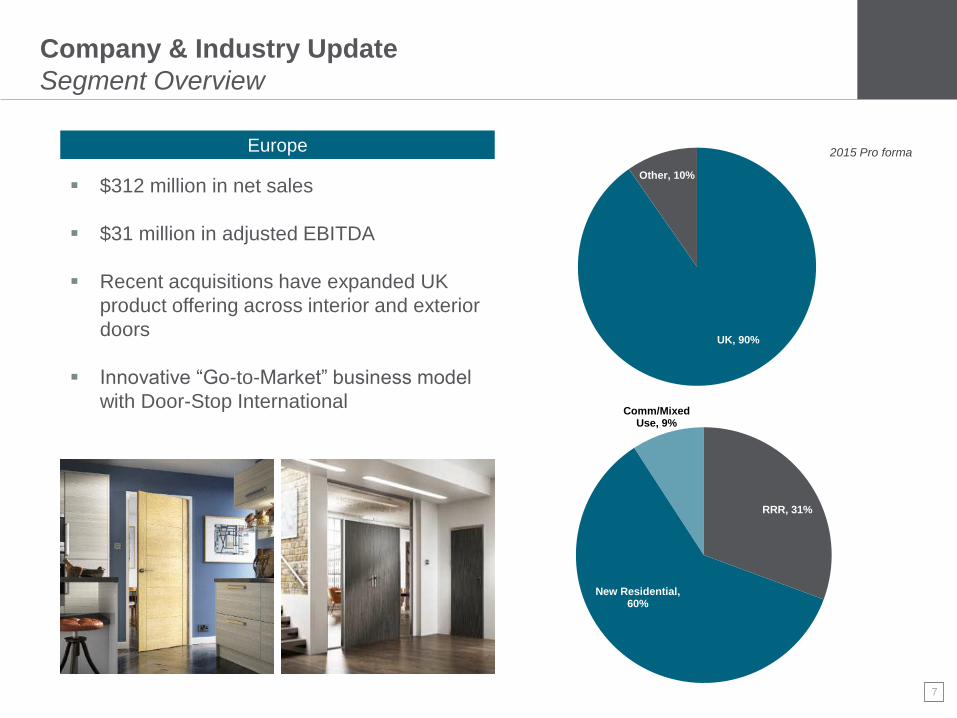

Company & Industry Update

Segment Overview

Europe

RRR, 31%

New Residential, 60%

Comm/Mixed Use, 9%

2015 Pro forma

$312 million in net sales

$31 million in adjusted EBITDA

Recent acquisitions have expanded UK

product offering across interior and exterior

doors

Innovative “Go-to-Market” business model

with Door-Stop International

8

Health Care

Education

Office

Stock

Lodging

Other

Commercial

Company & Industry Update

Segment Overview

Architectural 2015 Net Sales

$292 million in net sales

$23 million in adjusted EBITDA

ONLY vertically integrated Architectural

door manufacturer in North America

Established leadership positions* in interior

wood doors, door core and veneers

Institutional

Defined as #1 or #2 position (based on internal estimates).

9

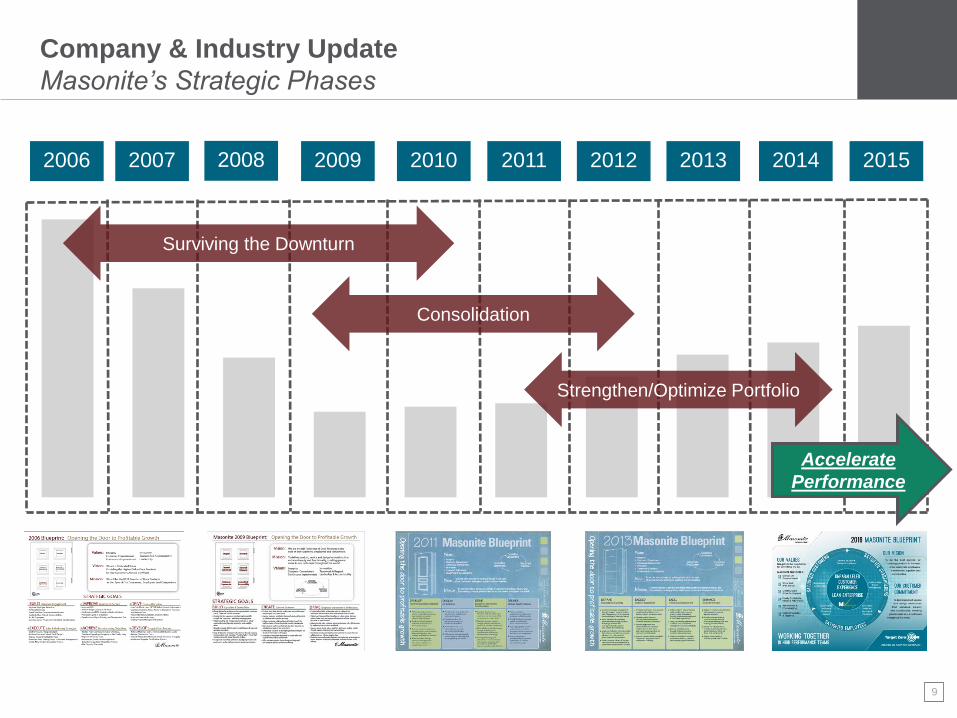

Company & Industry Update

Masonite’s Strategic Phases

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Surviving the Downturn

Consolidation

Strengthen/Optimize Portfolio

Accelerate

Performance

10

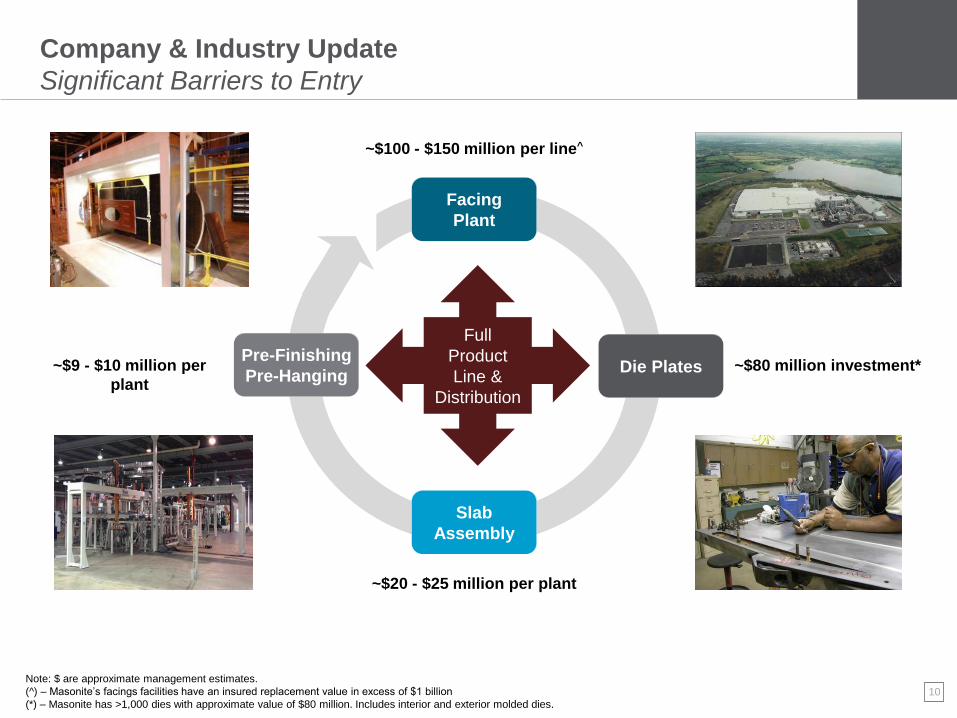

Company & Industry Update

Significant Barriers to Entry

Die Plates

Facing

Plant

Pre-Finishing

Pre-Hanging

Slab

Assembly

Full

Product

Line &

Distribution

~$100 - $150 million per line^

~$80 million investment*

~$20 - $25 million per plant

~$9 - $10 million per

plant

Note: $ are approximate management estimates.

(^) – Masonite’s facings facilities have an insured replacement value in excess of $1 billion

(*) – Masonite has >1,000 dies with approximate value of $80 million. Includes interior and exterior molded dies.

11

Company & Industry Update

Innovative Products to Drive Mix Shift Higher

Mix Shift Trade Up New Products

Hollow core to solid core Steel to fiberglass/wood Old styles to new styles

Average unit price increases through a combination of price and mix

12

Company & Industry Update

Driving Operational Efficiencies

Innovative products, services & processes

Cutting edge digital interactions

Automation, efficiency, simplicity & speed

Continuous Improvement / Lean Enterprise

13

Company & Industry Update

Acquisition Strategy Is a Key Growth Initiative

Value Added

Services

Niche Products

Components

14

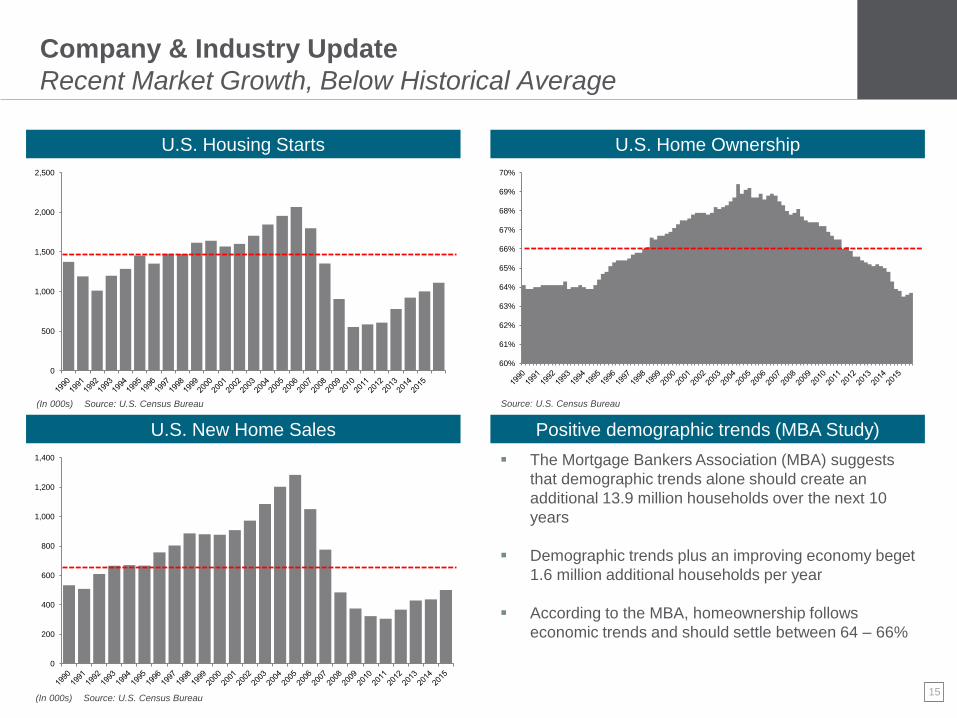

U.S. Residential Doors Sold Architectural Door Spending UK Housing Starts

Company & Industry Update

Opportunity for Continued Growth Across End Markets

83.6

60.1

45.2

76.5

2003 2008 2013 2018F 2003 2008 2013 2018F

$3.6

$5.4

$4.5

$6.5

(in billions of $ spent on doors)

Source: Freedonia Group

(in millions of doors sold)

Source: Freedonia Group

133

144

166

185

2011 2013 2015 2018F

(in 000s of UK housing starts)

Source: Experian

Forecast 11% CAGR from

2013-2018

Forecast 5% CAGR from

2013-2018

Forecast 8% CAGR from

2013-2018

Growth projected across all segments

15

U.S. Housing Starts U.S. Home Ownership

60%

61%

62%

63%

64%

65%

66%

67%

68%

69%

70%

0

500

1,000

1,500

2,000

2,500

U.S. New Home Sales Positive demographic trends (MBA Study)

0

200

400

600

800

1,000

1,200

1,400

(In 000s) Source: U.S. Census Bureau Source: U.S. Census Bureau

The Mortgage Bankers Association (MBA) suggests

that demographic trends alone should create an

additional 13.9 million households over the next 10

years

Demographic trends plus an improving economy beget

1.6 million additional households per year

According to the MBA, homeownership follows

economic trends and should settle between 64 – 66%

(In 000s) Source: U.S. Census Bureau

Company & Industry Update

Recent Market Growth, Below Historical Average

16

the beautiful door

Financial Overview

17

Financial Overview

Leveraging Growth Into Free Cash Flow

$1,964.9#

Net Sales Gross Profit

Adjusted EBITDA* Free Cash Flow^

+4% 2 Year CAGR

+39% 2 Year CAGR +60% 2 Year CAGR

+25% 2 Year CAGR

(*) – See appendix for non-GAAP reconciliations.

(^) – Defined as Adjusted EBITDA less Capex.

$1,731

$1,838 $1,872

2013 2014 2015

$226

$265

$351

2013 2014 2015

$106

$137

$204

2013 2014 2015

$60

$87

$153

2013 2014 2015

18

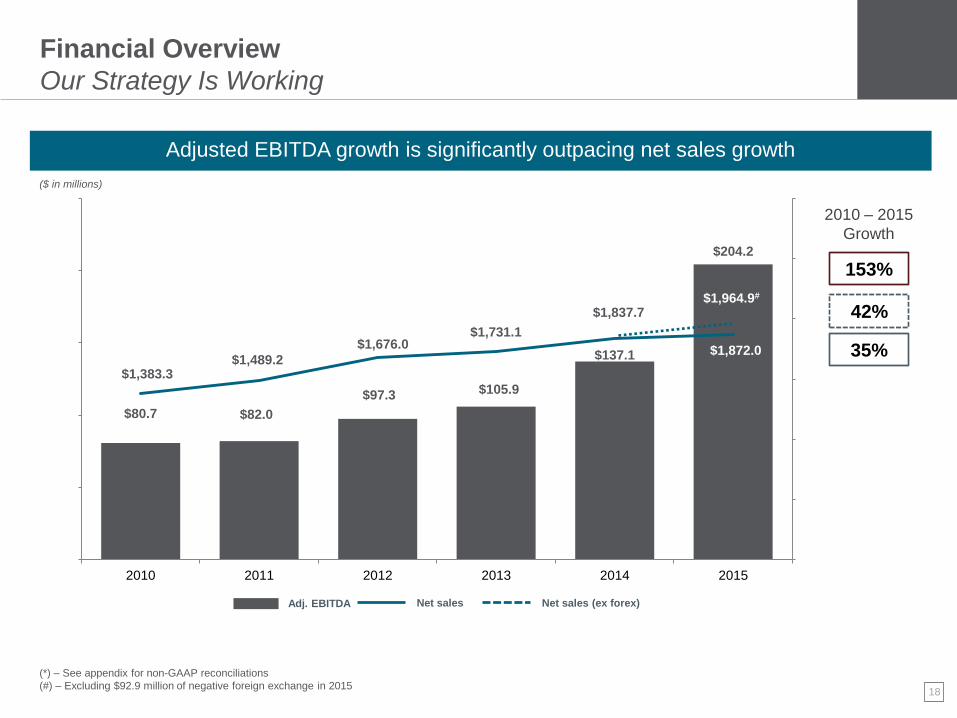

Financial Overview

Our Strategy Is Working

$1,964.9#

$80.7 $82.0

$97.3 $105.9

$137.1

$204.2

$1,383.3 $1,489.2

$1,676.0 $1,731.1

$1,837.7

$1,872.0

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$0

$50

$100

$150

$200

$250

2010 2011 2012 2013 2014 2015

(*) – See appendix for non-GAAP reconciliations

(#) – Excluding $92.9 million of negative foreign exchange in 2015

2010 – 2015

Growth

Adj. EBITDA

35%

Net sales

42%

Net sales (ex forex)

153%

($ in millions)

Adjusted EBITDA growth is significantly outpacing net sales growth

$1,964.9#

19

Financial Overview

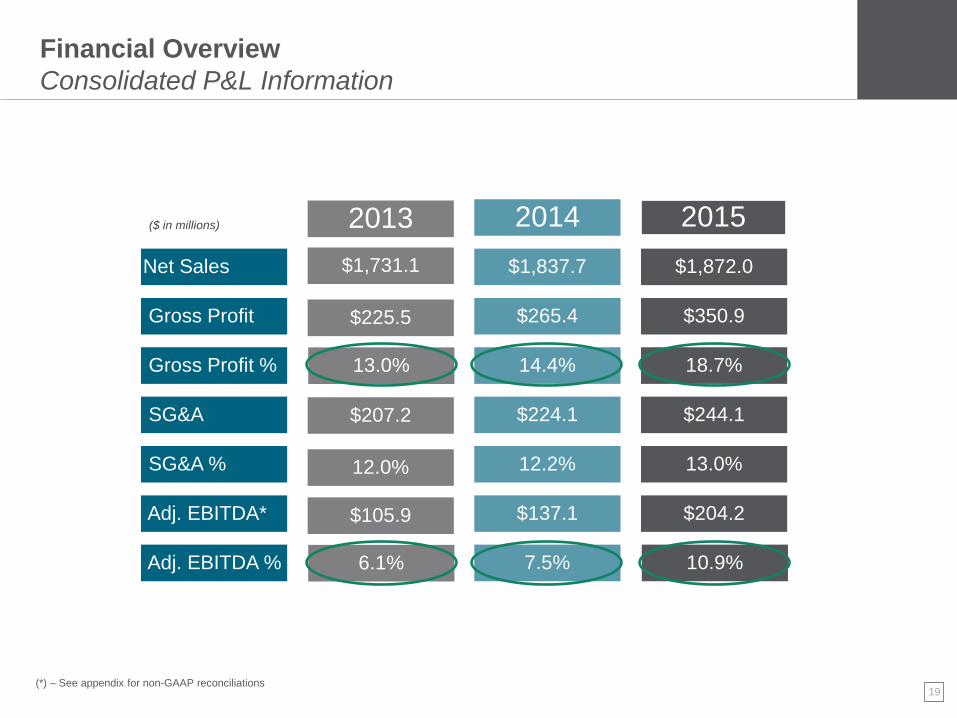

Consolidated P&L Information

Net Sales

Gross Profit

Gross Profit %

SG&A

SG&A %

Adj. EBITDA*

Adj. EBITDA %

2013

$1,731.1

$225.5

13.0%

$207.2

12.0%

$105.9

6.1%

2014

$1,837.7

$265.4

14.4%

$224.1

12.2%

$137.1

7.5%

2015

$1,872.0

$350.9

18.7%

$244.1

13.0%

$204.2

10.9%

($ in millions)

(*) – See appendix for non-GAAP reconciliations

20

Financial Overview

2016 Macro Outlook

Headwinds

Continued U.S. housing market growth

Expect mid to high-single digit growth in

U.S. housing completions

Expect mid-single digit growth in the

U.S. RRR market

New product investments driving higher AUP

Benign commodities market

Tightening labor market in U.S.

“Brexit” risk impact in UK housing market

Weak and uneven housing market in Canada

due to lower commodities prices

Uncertain foreign exchange environment

Tailwinds

21

10.9%

0%

5%

10%

15%

20%

25%

2015 2018

$1.9

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

2015 2018

Financial Overview

Long Term Growth Framework^

Net Sales

($ in billions)

Adjusted EBITDA* Margin

7% - 10%

CAGR

14% - 15%

( )̂ - Company long term growth framework is a forward-looking statement and subject to risks and uncertainties. See "Safe Harbor/Forward Looking Statement”

(*) – See definition of Adjusted EBITDA on page 2. We are not providing a quantitative reconciliation of our Adjusted EBITDA outlook to the corresponding GAAP information because the GAAP measures that we

exclude from our Adjusted EBITDA outlook are difficult to predict and are primarily dependent on future uncertainties.

22

Financial Overview

Cash Flow Deployment

1) Fund working capital

3) Strategic acquisitions

4) Return cash to shareholders

Continue to target Net Working Capital of

12-15% of net sales

Acquisitions to enhance portfolio and

value-added service offerings

Opportunistic share repurchases

2) Invest in growth initiatives Investment in new products and

technology enablers (~3% of Net Sales)

Cash Priorities

Strong liquidity allows simultaneous execution across all layers

23

Financial Overview

Liquidity, Credit and Debt Profile

Credit & Debt (millions of USD)

TTM Adj. EBITDA $234.1 $170.2

TTM Interest Expense $28.5 $39.5

Total Debt $471.0 $468.2

Net Debt* $408.6 $331.9

2Q16 2Q15

Six months

ended 7/3/2016

Six months

ended 6/28/2015

Unrestricted cash $62.4 $136.3

Total available liquidity $228.8 $278.3

Cash flow from operations $57.0 $40.2

Capital expenditures $38.1 $17.9

Liquidity & Cash Flow (millions of USD)

(*) – Net debt equals total debt less cash

24

Summary / Q&A

the beautiful door

25

Summary

What’s Expected

Deliver an unparalleled customer experience

Deliver product, service and design innovations

that enhance beauty and functionality

Expansion of MVantage and our lean operating

environment

Continued growth across end markets

the beautiful door

Appendix

27

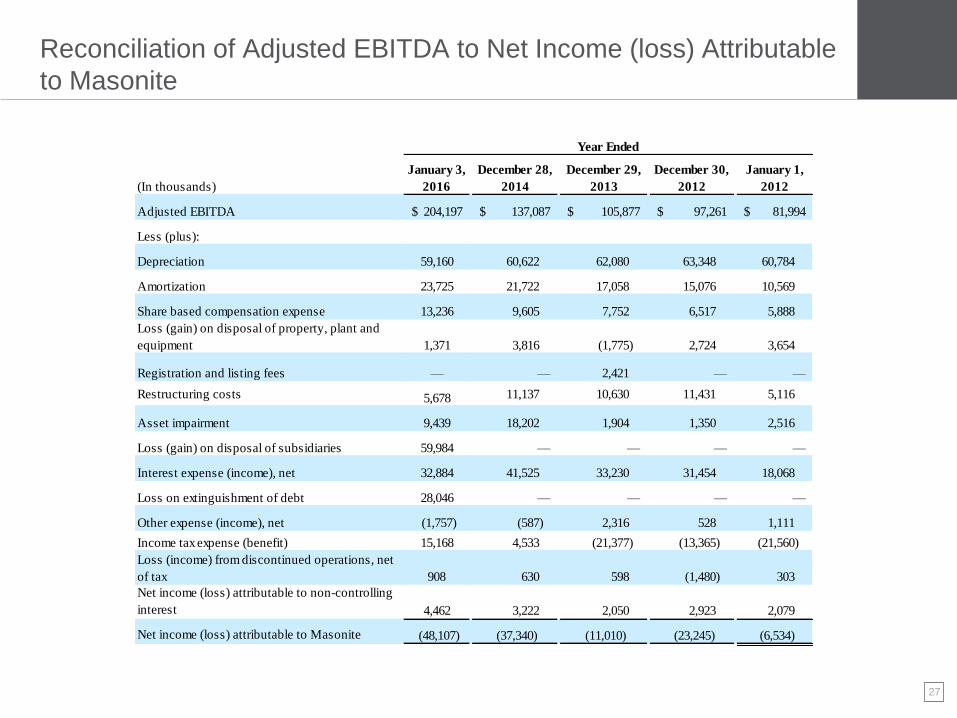

Reconciliation of Adjusted EBITDA to Net Income (loss) Attributable

to Masonite

(In thousands)

January 3,

2016

December 28,

2014

December 29,

2013

December 30,

2012

January 1,

2012

Adjusted EBITDA 204,197$ 137,087$ 105,877$ 97,261$ 81,994$

Less (plus):

Depreciation 59,160 60,622 62,080 63,348 60,784

Amortization 23,725 21,722 17,058 15,076 10,569

Share based compensation expense 13,236 9,605 7,752 6,517 5,888

Loss (gain) on disposal of property, plant and

equipment 1,371 3,816 (1,775) 2,724 3,654

Registration and listing fees — — 2,421 — —

Restructuring costs 5,678 11,137 10,630 11,431 5,116

Asset impairment 9,439 18,202 1,904 1,350 2,516

Loss (gain) on disposal of subsidiaries 59,984 — — — —

Interest expense (income), net 32,884 41,525 33,230 31,454 18,068

Loss on extinguishment of debt 28,046 — — — —

Other expense (income), net (1,757) (587) 2,316 528 1,111

Income tax expense (benefit) 15,168 4,533 (21,377) (13,365) (21,560)

Loss (income) from discontinued operations, net

of tax 908 630 598 (1,480) 303

Net income (loss) attributable to non-controlling

interest 4,462 3,222 2,050 2,923 2,079

Net income (loss) attributable to Masonite (48,107) (37,340) (11,010) (23,245) (6,534)

Year Ended

28

Reconciliation of Adjusted EBITDA to Net Income (loss) Attributable

to Masonite

Year Ended January 3, 2016

(In thousands)

North American

Residential Europe Architectural Corporate & Other Total

Adjusted EBITDA $ 165,560 $ 30,468 $ 23,281 $ (15,112 ) $ 204,197

Less (plus):

Depreciation 31,456 8,105 8,223 11,376 59,160

Amortization 4,954 6,860 8,428 3,483 23,725

Share based compensation expense — — — 13,236 13,236

Loss (gain) on disposal of property, plant and equipment 796

325

548

(298 ) 1,371

Restructuring costs 10 2,501 — 3,167 5,678

Asset impairment — 9,439 — — 9,439

Loss (gain) on disposal of subsidiaries — 29,721 — 30,263 59,984

Interest expense (income), net — — — 32,884 32,884

Loss on extinguishment of debt — — — 28,046 28,046

Other expense (income), net (50 ) 1,087 — (2,794 ) (1,757 )

Income tax expense (benefit) — — — 14,172 14,172

Loss (income) from discontinued operations, net of tax —

—

—

908

908

Net income (loss) attributable to non-controlling interest 3,323

—

—

1,139

4,462

Net income (loss) attributable to Masonite $ 125,071 $ (27,570 ) $ 6,082 $ (150,694 ) $ (47,111 )

29

the beautiful door