Embed Size (px)

Citation preview

Diplomat.is/more

I’m Jay.

I have chronic lymphocytic leukemia.

I’m a retired submarine commander,

a father, a husband, an avid woodcarver.

I bike 20 miles a day.

I know the Diplomat Difference.

Copyright © 2015 by Diplomat Pharmacy Inc. Diplomat is a registered

trademark of Diplomat Pharmacy Inc. All rights reserved.

J.P. Morgan Healthcare Conference

January 2016

Confidential

1

This presentation may contain “forward-looking” statements that involve risks, uncertainties and assumptions. If the risks or uncertainties ever materialize or the assumptions prove incorrect, our results may differ materially from those expressed or implied by such forward-looking statements. All statements other than statements of historical fact could be deemed forward-looking, including, but not limited to, any projections of financial information; any statements about historical results that may suggest trends for our business and results of operations; any statements of the plans, strategies and objectives of management for future operations; any statements of expectation or belief regarding future events, health care developments, or specialty pharmaceutical industry market sizes, shares, trends or growth; and any statements of assumptions underlying any of the foregoing.

Any forward-looking statements contained in this presentation are based on management's good-faith belief and reasonable judgment based on current information, and these statements are qualified by important factors, many of which are beyond our control, that could cause our actual results to differ materially from those in the forward-looking statements, including changes in global, regional or local economic, business, competitive, market, regulatory and other factors, many of which are beyond our control, including but not limited to the following risks related to our business: our ability to adapt to changes or trends within the specialty pharmacy industry; significant and increasing pricing pressure from third-party payors, our relationships with key pharmaceutical manufacturers; our limited history with integrating acquisitions; and the effects of competition. These and other risks and uncertainties associated with our business are described in the prospectus for our proposed follow-on offering, including under the heading “Risk Factors.” We assume no obligation and do not intend to update these forward-looking statements.

In addition to U.S. GAAP financials, this presentation includes certain non-GAAP financial measures. These historical and forward-looking non-GAAP measures are in addition to, not a substitute for or superior to, measures of financial performance prepared in accordance with GAAP. A reconciliation between GAAP and non-GAAP measures is included in the appendix to this presentation.

Diplomat is a registered trademark of Diplomat Pharmacy, Inc. This presentation also contains additional trademarks and service marks of ours and of other companies. We do not intend our use or display of other companies’ trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, these other companies.

Important note

Confidential

Investment Highlights

• Specialty Pharmacy industry is a high growth market (~20%)• Drug development pipeline remains robust• Limited distribution growing in importance

• Diplomat is unique within the specialty pharmacy industry• Taking market share as the largest independent specialty

pharmacy• Access to broad range of limited distribution drugs

• Strong financial performance• Five-year revenue CAGR of 42% & EBITDA CAGR of 65%• Diversified revenue and profitability streams• Modest balance sheet leverage – ample dry powder

• Experienced senior management team • CEO founded Diplomat 40+ years ago• Leadership team has broad ranging experience across the industry

2

Confidential

$27 $58$167

$271 $377$578

$772

$1,127

$1,515

$2,215

$3,325

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E

3

Diplomat at a glance

Founded: 1975; Headquarters: Flint, MI

Employees: ~1,700

2015E revenue: ~$3.3 billion

Diversified base of marquee partners

Corporate Overview

CVS Health/Omnicare

33%

Express Scripts25%

Walgreens10%

3%

OptumRx/Catamaran

8%

Avella 1%

Others20%

2014 Market share ($78 billion total market size) (1)

Exceptional above market revenue growth

Scaled business: National footprint

($ in millions)

(1) Source: 2014 – 2015 Economic Report on Retail, Mail and Specialty Pharmacies, Drug Channel Institute and Morgan Stanley Research

(2) Based on mid-point of management’s estimate range for FY 2015

(2)

Pharmacy Locations

Arizona

California

Connecticut

Florida

Illinois

Iowa

Massachusetts

Michigan

Minnesota

North Carolina

Ohio

Pennsylvania

Confidential

4

Diversified revenue and profit streams

Complementary Opportunities Minimize Payer/PBM Risk, AND Mitigate any risk of Inflation abatement

Other Services Retail Specialty Network

Hospital Specialty Network

HUB (Envoy Health)

340(b)

PAP

All services enhance DPLO’s

relevance in healthcare

Specialty Infusion Subset of specialty pharmacy

Many similar characteristics

(chronic, high cost, etc.)

Few differentiators (nursing

component, more medical billing)

Higher margin business

Unique/separate payer networks

Payer-driven site of care transition

opportunities

Core Specialty Pharmacy(orals and self-injectables)

Oncology dominance

Limited distribution expertise

Outpacing industry revenue growth

organically

Mix shift driving revenue and profit growth

Price inflation a very small component of

revenue

Serving open, preferred, narrow, and

exclusive payer networks

Pharmaceutical Manufacturer Services

Discounts, rebates, performance, services, data fees

High margin

Not dependent on payers or price inflation

Making progress, but significant upside opportunity remains

Revenue Source:

Payers

Revenue Source:

Pharma & Others

Financial Impact:

Higher Revenue,

Lower Margin

Financial Impact:

Lower Revenue,

Higher Margin

Confidential

Diplomat controls the journey of a specialty patient

5

Patient

Physician

Payor

Patient

Patient visits physician

Payor approves script

Diplomat monitors adherence and collects data for manufacturers

Diplomat dispenses drug

Diplomat provides:

Benefit verification

Prior authorization

Clinical intervention

Physician writes script

Patient receives

drugs

Confidential

6

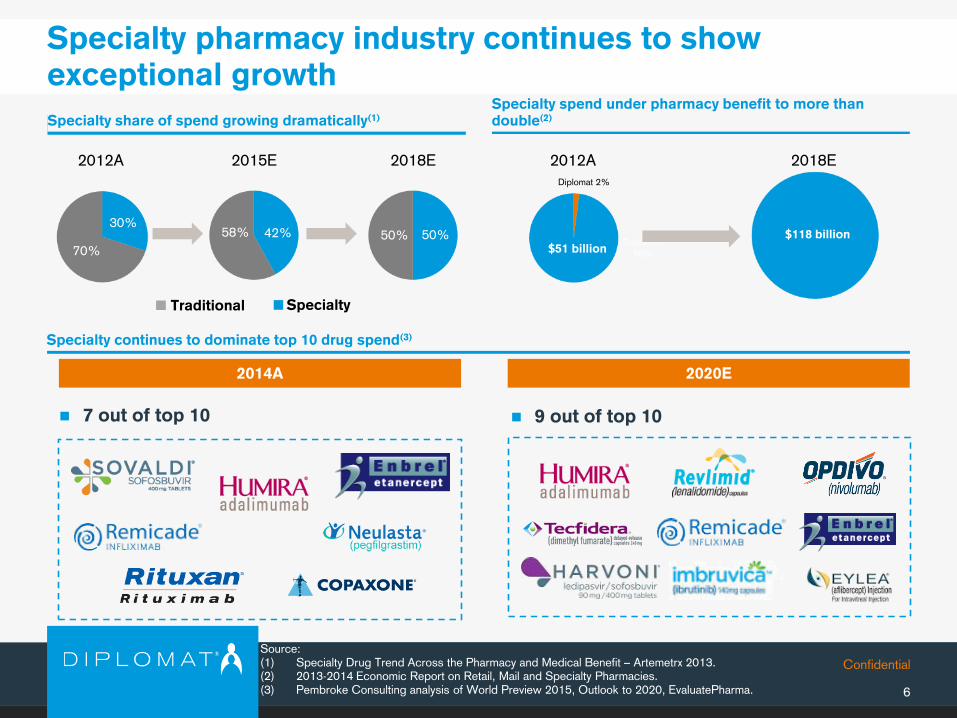

Specialty spend under pharmacy benefit to more than double(2)

Specialty pharmacy industry continues to show exceptional growth

Specialty share of spend growing dramatically(1)

Specialty continues to dominate top 10 drug spend(3)

Source:(1) Specialty Drug Trend Across the Pharmacy and Medical Benefit – Artemetrx 2013.(2) 2013-2014 Economic Report on Retail, Mail and Specialty Pharmacies.(3) Pembroke Consulting analysis of World Preview 2015, Outlook to 2020, EvaluatePharma.

7 out of top 10 9 out of top 10

2014A 2020E

70%

30%42%58% 50%50%

Traditional

58%

Diplomat 2%

$51 million

$118 billion

2012A 2018E

Traditional

2012A 2015E 2018E

$51 billion

Specialty

Confidential

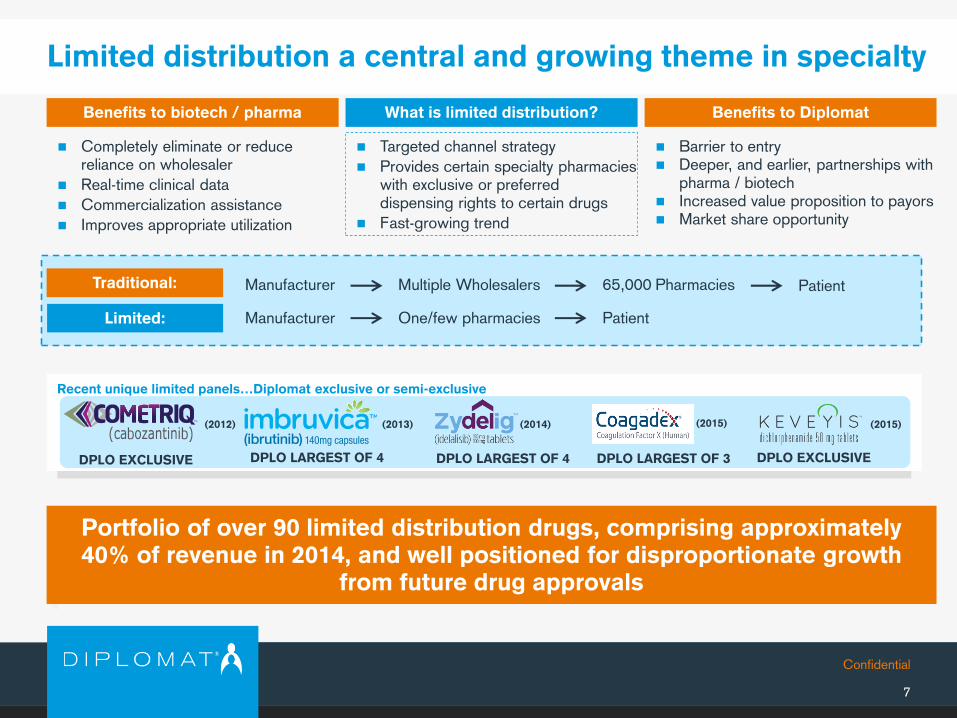

Limited distribution a central and growing theme in specialty

7

Benefits to DiplomatBenefits to biotech / pharma

Completely eliminate or reduce reliance on wholesaler

Real-time clinical data

Commercialization assistance

Improves appropriate utilization

Barrier to entry Deeper, and earlier, partnerships with

pharma / biotech Increased value proposition to payors Market share opportunity

Portfolio of over 90 limited distribution drugs, comprising approximately 40% of revenue in 2014, and well positioned for disproportionate growth

from future drug approvals

Recent unique limited panels…Diplomat exclusive or semi-exclusive

What is limited distribution?

Targeted channel strategy

Provides certain specialty pharmacies with exclusive or preferred dispensing rights to certain drugs

Fast-growing trend

(2013) (2015)(2012) (2014)

Traditional:

Limited:

Manufacturer Multiple Wholesalers 65,000 Pharmacies Patient

Manufacturer One/few pharmacies Patient

DPLO EXCLUSIVE DPLO LARGEST OF 4 DPLO LARGEST OF 4 DPLO EXCLUSIVEDPLO LARGEST OF 3

(2015)

Confidential

8

Unique competitive position

LARGE PBM / RETAILPHARMACY

SMALLER SPECIALTYPHARMACIES

Diversification distracts from specialty pharmacy

Less flexible / less nimble

Limited scale

Most focused on one or a few disease states

Fragmented market

Consolidation opportunity for Diplomat

Singularly focused on specialty

High-touch model

Flexible and nimble

Entrepreneurial culture

National reach

Scalable infrastructure

Confidential

9

Base business continues to gain momentum

Specialty pharmacy market grew 24% from $63bn in 2013 to $78bn in 2014

3,000+ oncology and immunology drugs in global drug development

Increased prevalence of limited distribution panels

Biosimilars launching in U.S.

2015 record year for drug approvals

Improving trends across specialty pharmacy…

…driving key milestones and achievements at Diplomat

Diplomat grew revenues by 59% from 3Q’14 to 3Q’15

Recent new drug contracts

The majority of which are limited distribution drugs

Oncology

Hepatitis C

Cystic Fibrosis

Other

• 51 total approvals:

- 45 NMEs and 6 biologics

• 21 of 45 NMEs were Orphan designation

• 16 of 45 NMEs were “First in Class”

• 69% of all approvals were specialty

Confidential

Accomplishments since the IPO

10

o Announced

access to ~20 LD

drugs

o Continued

oncology

dominance

o Growing theme of

excluding large

PBM-owned SPs

o Added key

industry

veterans; direct,

and via acquired

entities’

management

teams

o Added four

independent

board members;

now majority

independent

board

o Accelerated

higher margin

business

o Grew revenue by

~120%1

o Increased

EBITDA by

nearly 400%2

o Created a

nationwide

specialty infusion

platform with 3

strategic

acquisitions

o Broadened Hep-C

and technology

offerings through

Burman’s

acquisition

Expanded Access to

Limited Distribution

Drugs

Strengthened Leadership

Team

Delivered Strong Financial

Performance

Completed Strategic

Acquisitions

(1) 2015E $3,325 vs. 2013 $1,515(2) 2015E midpoint $94 versus 2013 $19

Confidential

11

Acquisitions create incremental revenue opportunities

Recent acquisitions of Burman’s Specialty Pharmacy and BioRX have created significant revenue synergies

BioRXAcquired by Diplomat on April 1, 2015

Burman’s Specialty PharmacyAcquired by Diplomat on June 19, 2015

• Strengthens Diplomat’s relationships with

Neurologists

• Provides BioRX sales force a broader portfolio

of drugs including Multiple Sclerosis services

• Cross selling infusion services to existing

managed market clients

Synergies

• Roll out software technology across our national

platform to drive patient adherence and

physician transparency

• Increased access to Gastroenterology thought

leaders

• Provides Burman’s sales force Diplomat’s full

therapeutic mix (incl. Crohn’s disease)

Synergies

Confidential

12

Future M&A criteria

When considering acquisitions, we look for targets that will potentially benefit Diplomat in one or more of the following ways:

Accelerate our higher margin business opportunities

Expand into new therapeutic areas and/or geographic regions

Enhance clinical capabilities to improve competitive advantage

Access to Limited Distribution drugs

Bring new services and technologies under our umbrella

Makes DPLO better, not just bigger

Confidential

13

Outstanding financial profile

Confidential

Traditional Drug Specialty Drug A Specialty Drug B Specialty Drug C Specialty Drug B

(10% price incr.)

Revenue $100 $3,700 $10,000 $27,000 $11,000

Gross Profit ($) $10 $185 $400 $810 $440

Gross Margin (%) 10% 5% 4% 3% 4%

14

RevenuePayors

Distributors / pharmaceutical manufacturers

Patient

DiplomatCOGS

Physical drug movement

$ flows

How we make money and grow profitability(Illustrative example)

How we make money

Drug mix and positive pricing trends are tremendous profit tailwinds for Diplomat

Inflation Impact

Diplomat mix shift movement over time

Our core focus

$301

Diplomat’s 3Q’15 Average

(AWP – Y%)(WAC – X%)

Note AWP = WAC x 1.20

(1)

(1)

Example:

AWP $12,000 - 15% = $10,200 Revenue

WAC $10,000 - 3% = $9,700 Cost

$500 Gross Profit

4.9% Gross Margin

Confidential

$185

$301

3Q14A 3Q15A

$10.6

$33.0

3Q14A 3Q15A

$596

$947

3Q14A 3Q15A

15

Recent quarterly highlights

(1) Based on dispensed scripts only.(2) Gross profit / net sales (i.e., based on dispensed and serviced scripts).

Revenue

EBITDAmargin

1.8%

Adjusted EBITDAGross Profit /Script($ in millions) ($ in millions)

3.5%8.0%6.7%

(1)

Grossmargin

(2)

130 bps expansion 170 bps expansion

Confidential

$25

$67

First Nine Monthsof 2014

First Nine Monthsof 2015

$1,603

$2,380

First Nine Months

of 2014

First Nine Months

of 2015

$8$15

$11

$19

$35

96% (28%) 75% 86%

1.3% 2.0% 1.0% 1.3%

2010A 2011A 2012A 2013A 2014A

16

Strong long-term financial performance…

Adjusted EBITDA2010 –First Nine Months of 2015

Total Revenue2010 –First Nine Months of 2015

% margin

% growth

($ in millions)

$578$772

$1,127$1,515

$2,215

34% 46% 34% 46%

2010A 2011A 2012A 2013A 2014A

% growth

($ in millions)

1.5% 2.8%

Infrastructure investments including IT, facilities and personnel

Volume, price and mix all driving superior revenue growth

Natural operating leverage and acquisitions driving EBITDA growth and margin expansion

53%

27%

Note: Historical financials are not pro forma for any acquisitions.

1.6%

Confidential

$161

$269

First Nine Monthsof 2014

First Nine Monthsof 2015

17

… with continued growth in profitability

Gross Profit / Script (1)

2010 –First Nine Months of 2015

Note: Financials are not pro forma for BioRx acquisition.(1) Based on dispensed scripts only.(2) Gross profit / net sales (i.e., based on dispensed and serviced scripts).

$71

$93 $97$116

$167

2010A 2011A 2012A 2013A 2014A% growth 12% 20%31% 4%

% margin 7.1% 5.9%7.3% 6.2%

Several factors drive growth in our Gross Profit / Script(1):

Continued mix shift towards higher price, higher profit drugs (including acquisitions)

Favorable pricing trends

(2)

Gross margin expansion opportunities:

Recent acquisitions with higher gross margins (%)

Fee-for-service/rebate opportunities with pharmaceutical manufacturers

Specialty generics and biosimilars (longer term)

44%

6.3% 6.2% 7.8%

Confidential

18

Multiple Components to Revenue Growth

Price inflation has comprised only

5-8% of revenue over the last 5

quarters Political pressure on price

inflation, if successful, will have

limited impact on Diplomat

Value added services to pharma

manufacturers are an

opportunity to offset

Chronic disease expertise

provides a stable and growing

annuity-like revenue base Limited distribution leadership

and rich drug pipeline driving

considerable revenue growth

from new drugs

Diplomat remains an organic

growth story Strategic M&A has

complemented growth

49% YOY

Growth(42% organic)

49% YOY

Growth(41% organic)

34% YOY

Growth(29% organic)

Quart

erly

Reve

nue

Inflation

Impact

Confidential

19

Balance Sheet summary (as of September 30, 2015)

(1) Includes $6mm in cash-based contingent consideration

($ in millions) Actual

Cash $16

Total Debt $147

Shareholders’ equity $502

Net Debt/Pro Forma EBITDA ~1.1x

Modest leverage

Ample dry powder for the right opportunities

(1)

Confidential

20

Appendix

Confidential

21

Diversified therapeutic mix

(FY 2014A)

Revenue mix by therapeutic category

Oncology

48%

Immunology

20%

Multiple

Sclerosis

10%

Other

22%

Confidential

Recent Acquisitions

22

Acquired Company Consideration Rationale Other

June 19, 2015

• $87M gross purchase price*

• $77M cash*, $10M stock

• ~4.2x CY 2014 EBITDA

• Hep C dominance in Mid Atlantic

• Hep C is a fast growing and highly profitable disease state

• Proprietary technology (HealthTrac) with applicability across Diplomat’s

Hep C platform

• Proven management team

• 50 year old company, run by 2nd generation pharmacist

• No marketed sales process – Diplomat had a one-off look

• Lack of

auction/marketed

process

• Founder/owner led

• Management all on

board at DPLO

April 1, 2015

• $272M adjusted purchase price*

(~$50M tax benefit)

• $217M cash*, $105M stock

• ~11.8x CY 2014 EBITDA

• One year earnout of 1.35M shares

(all stock)

• Adds significant scale to specialty infusion business

• Provides ability to compete for national contracts

• Increases exposure to higher margin businesses

• Addition of new disease states, therapeutic categories & 5 new LD’s

• Lack of

auction/marketed

process

• Founder/owner led

• Management all on

board at DPLO

June 27, 2014

• $68.5 million gross purchase price*

• $52M cash upfront, $12M stock

• ~8x CY 2013 EBITDA

• Two year earnout max. $11.5M (all

cash)

• Strong management team

• Strong therapy mix: IVIG and Hemophilia

• Favorable geographic footprint

• Lack of

auction/marketed

process

• Founder/owner led

• Management all on

board at DPLO

December 16, 2013

• $13.4 million gross purchase price*

• $12M cash upfront

• ~6x CY 2013 EBITDA

• Two year earnout max. $2M (all

cash)

• First DPLO acquisition

• More than doubled hemophilia/specialty infusion business

• High margins

• Lack of

auction/marketed

process

• Management all on

board at DPLO

* Value includes closing working capital adjustments

Confidential

Calendar year ending December 31,

($ in millions) 3Q'15 3Q'14 2014A 2013A 2012A 2011A 2010A

Net income (loss) attributable to Diplomat $16.0 $4.5 $4.8 ($26.1) ($2.6) $9.2 ($7.8)

Depreciation & Amortization $9.9 $2.8 $8.1 $3.9 $3.8 $3.1 $2.2

Interest Expense $1.5 $0.7 $2.5 $2.0 $1.1 $0.6 $0.5

Income tax expense $9.8 $2.4 $4.7 - - - -

EBITDA $37.2 $10.5 $20.1 ($20.2) $2.3 $12.8 ($5.2)

Share-based compensations expense $1.3 $0.7 $2.9 $0.9 $0.9 $1.4 $0.8

Change in fair value of redeemable common shares $(6.9) ($9.1) $34.3 $6.6 $10.7

Termination of existing stock redemption agreement $4.8 $4.8

Employer payroll taxes - option repurchases - -

Restructuring and impairment charges - - - $1.0 $0.4 $0.4 $1.5

Equity loss of non-consolidated entity - $0.4 $6.2 $1.1 $0.3 $0.1 -

Severance and related fees $0.1 $0.1 $0.4 $0.2 $0.4 $0.7 -

Merger and acquisition related expenses ($6.3) $0.6 $7.2 $0.7 - - -

Private company expenses - - $0.2 $0.2

Tax credits and other - - $1.0 - ($0.1) ($0.6) -

Other items $0.7 $0.4 $1.4 $0.7 $0.1 $0.2 ($0.0)

Adjusted EBITDA $33.0 $10.6 $35.2 $19.0 $10.9 $15.1 $7.7

Reconciliation of Net income (loss) and Adjusted EBITDA

23

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Note: Financials are not pro forma for acquisitions.Detailed footnotes on the following page.

Confidential

Reconciliation of Net income (loss) and Adjusted EBITDA

24

1) Share-based compensation expense relates to director and employee share-based awards.

(2) Restructuring and impairment charges reflect decreases in the fair market value of non-core property and assets, or actual losses on disposal of such assets. 2013 charges primarily relate to the $932 write-down of our former Swartz Creek, Michigan headquarters facility to its fair value, after we vacated it in favor of our present Flint, Michigan facility. 2012 charges primarily relate to our write-down of an externally purchased software package we no longer utilize, as well as sales of Company-owned vehicles. 2011 charges include expense associated with the closure of our former Cleveland, Ohio facility, the move of our Chicago, Illinois area facility, and sales of Company-owned vehicles.

(3) During the fourth quarter of 2014, we reassessed the recoverability of our investment in our non-consolidated entity, Ageology. Based upon this assessment, we determined that a full impairment of $4,869 was warranted, primarily due to updated projections of continuing losses into the foreseeable future. The remaining amounts in 2014, 2013 and 2012 represents our share of losses recognized by Ageology, using the equity method of accounting. We first invested in Ageology, an anti-aging physician network dedicated to nutrition, fitness and hormones, in October 2011, in connection with its formation.

(4) Employee severance and related fees primarily relates to severance for former management.

(5) Fees and expenses directly related to merger and acquisition activities, and the impact of changes in the fair value of related contingent consideration liabilities.

(6) Primarily includes philanthropic activities performed at the direction of our majority shareholder.

(7) Represents (a) various tax credits received from the state of Michigan for facility improvement and employee hiring initiatives, (b) the one-time costs associated with converting from an S-Corporation to a C-Corporation, and (c) a 2014 charge of $1,825 related to non-income tax obligations.

(8) Includes other expenses, predominantly option redemption payroll taxes and IT operating leases. Operating leases were initiated, in lieu of purchases or capital leases for a subset of our IT spend, for a short period of time in 2013 and 2014 for liquidity purposes. We have since discontinued the practice of leasing IT equipment. The cost of purchased IT equipment is reflected in depreciation and amortization.

![[JP Morgan] MBS Primer](https://img.dokumen.tips/doc/110x75/54a0e50fac7959027f8b45a3/jp-morgan-mbs-primer.jpg)

![[JP Morgan] Variance Swaps](https://img.dokumen.tips/doc/110x75/551e53714a795970108b4afb/jp-morgan-variance-swaps.jpg)