Embed Size (px)

Citation preview

At the heart of the Verbund

INVESTOR DAY Chemicals segment 2014

Kurt Bock Chairman of the Board of Executive Directors Wayne T. Smith Member of the Board of Executive Directors Investor Day Chemicals segment May 22, 2014

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 2

Cautionary note regarding forward-looking statements

This presentation may contain forward-looking statements that are subject to risks and uncertainties, including those pertaining to the anticipated benefits to be realized from the proposals described herein. Forward-looking statements may include, in particular, statements about future events, future financial performance, plans, strategies, expectations, prospects, competitive environment, regulation and supply and demand. BASF has based these forward-looking statements on its views and assumptions with respect to future events and financial performance. Actual financial performance could differ materially from that projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and financial performance may be better or worse than anticipated. Given these uncertainties, readers should not put undue reliance on any forward-looking statements. The information contained in this presentation is subject to change without notice and BASF does not undertake any duty to update the forward-looking statements, and the estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 3

Why do we talk about Chemicals today?

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 4

Chemicals 28%

Chemicals 23%

2013: €74.0 billion* 2013: €10.4 billion*

Chemicals – strong contribution to BASF’s sales and profitability

Functional Materials & Solutions 23%

Performance Products 21%

2013

Sales* to 3rd parties

EBITDA*

Agricultural Solutions 7%

Oil & Gas 20%

Functional Materials & Solutions 15%

Performance Products 19%

2013 Agricultural Solutions 13%

Oil & Gas 30%

* Segment share excluding Other: Sales: €4.7 billion (6% of sales); EBITDA: - €533 million (-5% of total EBITDA )

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 5

Chemicals in a nutshell (2013)

~1,500 ~6,000 customers in all regions

Verbund site

Global

asset footprint

Core of each €6.4 billion transfers to BASF

downstream divisions

€178 million R&D

expenses

€17 billion sales to third parties

BASF Investor Day Chemicals segment – Key note speech, May 22, 2014 BASF Corp., Geismar, US 5

products*

€3.0 billion EBITDA

* without electronic materials

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 6

EBIT after cost of capital Chemicals

EBIT after cost of capital* in million €

restated

Chemicals earned a premium on cost of capital even during the 2008 / 2009 recession*** * EBIT after cost of capital concept was introduced in 2004.

*** The former Plastics segment also earned a premium on cost of capital during the 2008 / 2009 recession.

Chemicals is a strong earnings contributor

0

500

1.000

1.500

2.000

2004 2005 2006** 2007** 2008 2009 2010 2011 2012 2013

2,000

1,500

1,000

500

0

** Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 7

Several events shaped the Chemicals segment since 2008

Major events shaping Chemicals

Last Chemicals Investor Day

2008 / 2009 recession

Expansion BASF-YPC, Nanjing

New segment structure

Feedflex, Port Arthur

Acrylic acid to Petrochemicals

Major shale gas- based investment

projects*

Focus on organic growth capex

2009 2010 2012 2008 2013 2011 2014

* Under evaluation

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 8

Butadiene extraction Antwerp, Belgium

Ammonia and gas-to-propylene in USA*

Expansion Verbund site Nanjing, China

MDI plant Chongqing, China

Acrylic acid complex Camacari, Brazil

TDI plant Ludwigshafen, Germany

Chemicals: Strengthen our Verbund and secure growth

Major Chemicals investment projects

* Under evaluation

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 9

Agenda

Trends in the chemicals market

Chemicals segment within BASF

Chemicals: At the core of the Verbund

Chemicals support growth of BASF

Shale Gas – An opportunity

Chemicals 2020

Capital expenditures drive profit growth

Ludwigshafen

Antwerp

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 10

Current trends in the upstream chemical industry

Global growth Sustainability Raw material change

Dynamic competitive environment

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 11

Real chemical production excluding pharma (World)* in trillion US$

10%

CAGR 2010-2020 World: 4.3% (GDP: 3%)

Emerging Markets: 6.7% (GDP: 5%)

Source: BASF * Revised statistics with new baseline, recognizing larger market demand in Asia; ** BASF not focused on base-products, e.g. PVC, polyolefines, fertilizers

Chemical production continues to outpace GDP, especially in emerging markets

2020 4.7

trillion 2013 3.4

trillion

2010 3.1

trillion 57%

Asia Pacific

Rest of World Europe

North America

9%

18%

16%

50%

10%

22%

18%

45%

20%

25%

Global growth 11

Sustainability Raw material change Competitive environment

Strategically relevant market of BASF’s Chemicals segment 2013: ~US$550 billion**

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 12

Chemistry as an enabler: Global chemical market growth expected to accelerate

Global growth 12

Sustainability Raw material change

Chemistry as an enabler

Major growth drivers are

– Increasing standards of living in emerging markets

– Substitution of established materials

– New chemistry-based solutions

Competitive environment

Diapers in emerging markets

Functional textiles

High growth

examples

Coldchains in emerging markets

Lightweight materials in cars

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 13

Global growth 13

Sustainability as future growth driver

Enable customers to develop more sustainable solutions

Balancing of sustainability dimensions is key

Governments set regulatory framework

Key aspects for Chemicals

Downstream growth

Energy consumption

Emissions, climate protection

Occupational health and safety

Renewable resources

Sustainable chemicals production balances ecology, economy and society

Operational

Excellence

Society

Economy Ecology

Sustain- ability

Sustainability Raw material change Competitive environment

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 14

Global growth 14

Sustainability Raw material change Competitive environment

Sustainable solutions provide major business opportunities for BASF

Example: Solar power

Heat storage systems using

sodium nitrate

Specialty sealants made from Oppanol®

Insulation materials made from Basotect®

Plastics protected with light stabilizers and UV filters

Mounting systems made from polyamide

Chemistry as an enabler

Sustainability enables and supports long-term business success

Chemicals segment benefits from sustainability aspects, driving demand for chemicals

e.g. sodium nitrate

e.g. polyamide

e.g. precursors for Basotect®

e.g. precursors for Oppanol®

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 15

Fossil feedstocks to remain backbone Renewables provide new opportunities

“Renewed” availability, high public acceptance New technologies, processes emerge rapidly

Potentially higher total costs

► Opportunities can be captured by differentiation versus petrochemicals:

Better economics and / or better properties

Renewables based chemical process

Global growth 15

Sustainability Raw material change Competitive environment

Processes optimized for efficiency and economics

Further upside: Incremental improvements and step-changing / breakthrough innovation

► Fossil feedstock will remain backbone of chemical industry in mid-term future

Fossil feedstock based chemical process

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 16

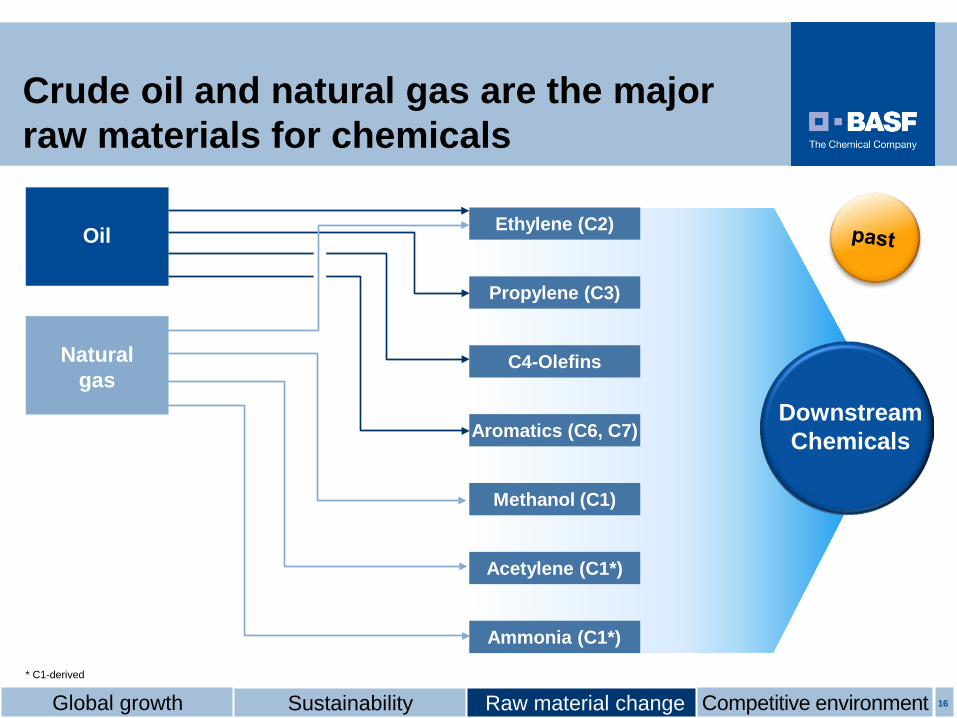

Crude oil and natural gas are the major raw materials for chemicals

Natural gas

Ethylene (C2)

Propylene (C3)

C4-Olefins

Aromatics (C6, C7)

Methanol (C1)

Acetylene (C1*)

Ammonia (C1*)

Downstream Chemicals

Oil

Global growth 16

Sustainability Raw material change * C1-derived

Competitive environment

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 17

.

Raw materials landscape is diversifying based on regional differences

Shale gas

Naphtha Renewables

Naphtha Abundant coal

Naphtha

Global growth 17

Sustainability Raw material change Competitive environment

Ethane, natural gas Mixed feed

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 18

Increasing usage of alternative feedstock in global chemicals market

Coal

Renewables

Ethylene

Propylene

C4 Olefins

Aromatics

Methanol

Ammonia

Downstream Chemicals

Oil

Intermediates

Global growth 18

Sustainability Raw material change Competitive environment

Natural gas

Shale gas

Acetylene

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 19

.

Europe Ongoing restructuring of olefins and polyolefins industry Focus on innovative chemistry Integrated production setups will remain competitive

North America New capacities based on shale gas Export of NGLs*/ LPG** and base-products

China Strong domestic demand will drive capacity additions Abundant coal reserves drive coal-to-chemicals investments Expected to remain a net importer of many basic chemicals

Middle East Diminishing feedstock advantage due to shale gas

(USA) and coal (China) Export hub for raw materials and base-products

South America Focus on renewable resources Will remain net importer of chemicals from the U.S.

Raw material supply and integration concepts will define competitiveness

* Natural Gas Liquids ** Liquefied Petroleum Gas

Global growth 19

Sustainability Raw material change Competitive environment

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 20

Changes in the competitive environment

Oil & Gas

Commodities

Specialties

Pharma

Crop protection Plant-Biotech

Petro– chemicals

1980

Dow

BASF DuPont

Shell

Hoechst

2013

Sanofi

Shell

Celanese

Conoco

Invista

DuPont

AstraZeneca

Sinopec

Rhône Poulenc

BASF

Ineos

Formosa

Bayer

Dow

Solvay

ICI

Sabic

Clariant

Reliance

Global growth 20

Sustainability Raw material change

Bayer

Competitive environment

Lanxess

Syngenta

AkzoNobel

Lyondell Basell

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 21

Engineering plastics Catalysts Construction chemicals Water-based resins Pigments, plastic additives Oil & Gas Personal care & food Battery materials Functional crop care Omega-3 fatty acids Enzymes …

BASF core business

Strong partnerships

Gazprom Monsanto Petronas Shell Sinopec Statoil Total

Selected transactions 2001 − today

Acquisitions

~ €16 billion sales

Divestitures

Pharma Agro generics Vitamins premix Printing systems Construction equipment,

wall & flooring systems Gas Trading* …

Global growth 21

Sustainability Raw material change Competitive environment * Closing expected by mid of 2014

~ €22 billion sales ** Transferred into Styrolution JV on Oct. 1, 2011

Fibers Polyolefins Fertilizers Styrenics**

Chemicals divestitures

Active portfolio management at BASF

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 22

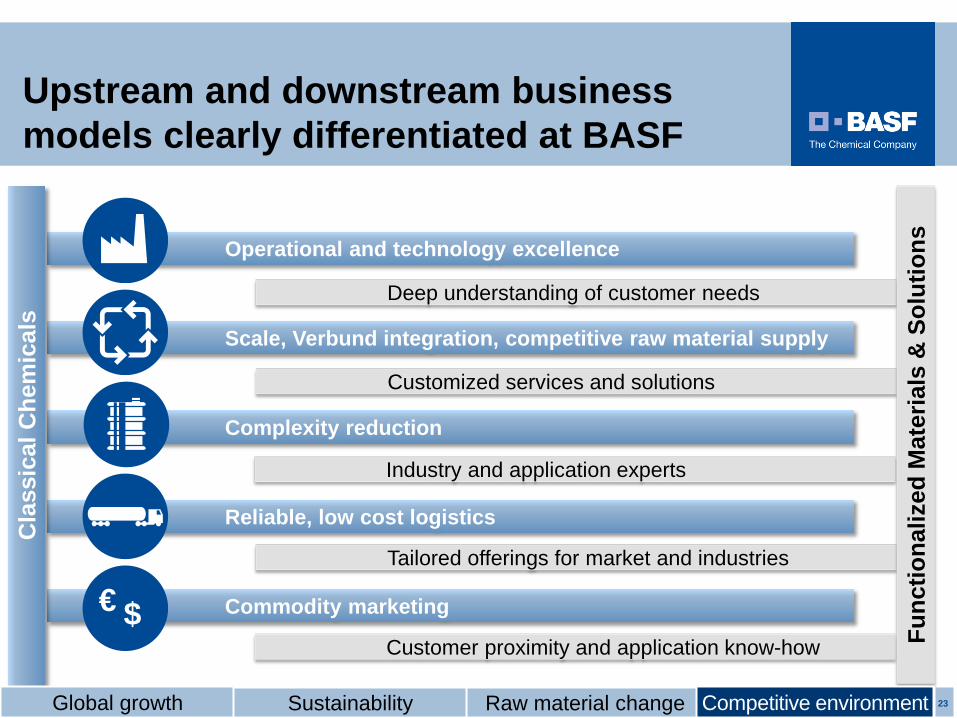

Operational and technology excellence

Commodity marketing

Reliable, low cost logistics

Complexity reduction

Scale, Verbund integration, competitive raw material supply

Cla

ssic

al C

hem

ical

s

Upstream and downstream business models clearly differentiated at BASF

Global growth 22

Sustainability Raw material change Competitive environment

€ $

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 23

Operational and technology excellence

Commodity marketing

Reliable, low cost logistics

Complexity reduction

Scale, Verbund integration, competitive raw material supply

Cla

ssic

al C

hem

ical

s

Global growth 23

Sustainability Raw material change

Customer proximity and application know-how

Tailored offerings for market and industries

Industry and application experts

Customized services and solutions

Deep understanding of customer needs

Func

tiona

lized

Mat

eria

ls &

Sol

utio

ns

Competitive environment

Upstream and downstream business models clearly differentiated at BASF

€ $

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 24

Agenda

Trends in the chemicals market

Chemicals segment within BASF

Chemicals: At the core of the Verbund

Chemicals support growth of BASF

Shale Gas – An opportunity

Chemicals 2020

Capital expenditures drive profit growth

Freeport

Geismar

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 25

BASF’s Chemicals segment is a strong cash and earnings contributor We will ► continue to strengthen the Verbund, create synergies and

add value ► maintain our high level of profitability through process

innovations and stringent cost management ► grow externally with the chemicals market

Our strategic focus is to enable and support growth of ► BASF’s downstream segments ► BASF in emerging markets

Shale gas is an opportunity for BASF

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 26

Sales to other BASF segments

Sales to 3rd parties

Chemicals segment grows by selling into the BASF Verbund and to the market

* IFRS 10 & 11 impact: -€1.3Bn; Impact of new segment structure: +€5.3Bn

0

5.000

10.000

15.000

20.000

25.000

2001 2002 2003 2004 2005 2006** 2007** 2008 2009 2010 2011 2012restated

2013

25,000

20,000

15,000

10,000

5,000

0

Sales Chemicals in million €

CAGR 2001-2013 11%

5% Volume CAGR 2001-2013

** Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 27

0

100

200

300

400

500

2001 2002 2003 2004 2005 2006* 2007* 2008 2009 2010 2011 2012restated

2013

EBITDA margin Chemicals / oil price Index 2001 = 100

Chemicals with stable profitability, little correlation to oil price

EBITDA margin Chemicals (as % of sales)

Oil price

* Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 28

Chemicals is a stable earnings contributor to BASF Group

EBITDA BASF Group in million €

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2001 2002 2003 2004 2005 2006* 2007* 2008 2009 2010 2011 2012restated

2013

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

thereof EBITDA Chemicals

EBITDA BASF Group

* Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 29

2001 2002 2003 2004 2005 2006* 2007* 2008 2009 2010 2011 2012restated

2013

Chemicals generates strong and steady free cash flow

Cash flow Chemicals in million €

* Without Catalysts (now part of Functional Materials & Solutions segment)

Free cash flow (EBITDA – additions to plant, property & equipment)

Since 2001, Chemicals contributed ~€17 billion of free cash flow to BASF Group

Operating cash flow (EBITDA)

2,000

3,000

4,000

1,000

-1,000

0

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 30

Chemicals – Three distinct divisions, one mission: Create value

Supply of cracker products and basic chemicals Focus on C3 and C4 value chain

Supply high-volume monomers and inorganic chemicals

Focus on aromatics and ammonia based value chains

Supply of broad portfolio of intermediates for the chemicals industry

Focus on C1 value chain

Intermediates

Monomers

Petrochemicals

Stefano Pigozzi

Sanjeev Gandhi

Rainer Diercks

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 31

Balanced portfolio of products for internal supply and merchant market sales

Industrial gases Acetylene Purified ethylene

oxide Formaldehyde Ammonia Cracker products Butanediol Caprolactam PBT** base resin Acrylic acid MDI

Internal supply driven

TDI PolyTHF®

Amines Higher alcohols Polyalcohols and

specialties Formic acid Inorganic salts Glues and resins

Merchant market driven

** Polybutylene terephthalate

captive use only

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 32

Principles for internal supply driven and merchant market driven products

Reliable supply of key raw materials

Access to chemicals not available in the market

Internal supply driven

Capture value of attractive chemicals markets

Top-3 position in target market

Merchant market driven

Economic advantages through superior technologies and

Verbund

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 33

2004 2005 2007 2008 2012 2013 1999 2006 2010 2011 2000

Continuous development of Chemicals global asset footprint

PVC Polyolefins

Minority share in ‘Williams cracker’

Styrenics

Acrylonitrile, Seal Sands

Divestitures / Joint ventures

BASF Petronas, Kuantan

BASF-YPC, Nanjing

Major investments

Polyamide fibers

Steam cracker, Port Arthur

Isocyanates, China

Expansion BASF-YPC, Nanjing

BASF Specialty Chemicals, Nanjing

Feedflex, Port Arthur

Expansion Antwerp cracker

Fertilizers

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 34

BASF has leading positions in the chemical markets

MDI, TDI Glacial acrylic acid Acrylic esters Polyamide film Oxo alcohols Polyalcohols

No.1 globally* Leading regional market position

Inorganic salts Glues and

impregnating resins Plasticizers Solvents Standard amines

Butanediol and derivatives

Purified ethylene oxide

Specialty amines Carboxylic acids

(~50% of sales of BASF Chemicals)

BASF Investor Day Chemicals segment – Key note speech, May 22, 2014 BASF SE, Antwerp, Belgium 34

* 2013

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 35

Agenda

Trends in the chemicals market

Chemicals segment within BASF

Chemicals: At the core of the Verbund

Chemicals support growth of BASF

Shale Gas – An opportunity

Chemicals 2020

Capital expenditures drive profit growth

Ludwigshafen

Antwerp

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 36

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 37

We add value as one company

People Verbund

Technology Verbund

Production Verbund

Customer Verbund BASF

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 38

Raw materials

Chemicals Segment

Ammonia

Methanol

Hydrogen

Chlorine

Sulfur dioxide

Sulfuric acid

Caustic soda

PSA

Carbon dioxide

Carbon oxide

C4-cut Propylene

Ethylene

Acetylene

Oxygen

AH-salts Adipic acid

Caprolactam

Hydrosulfites Na-bisulfites Na-sulfites

Na-nitrite, -nitrate

Propyleneglycoles

Melamine

Carbon dioxide liqu.

Butanoles Butyraldehydes

Acrylic acid ester

Tetrahydrofuran

Butyrolactone

Polyisobutene SB-copolymer

Glycole ethers

C13-C15-alcohols

Diethanol amine Ethanol amine

Propanole

Polyamides

Lutinol E Blankites Rongales

Rongalites Separoles

Urea-formaldehyde- condensation products

Carbon dioxide solid

Butylacetate Dispersions

Hexanediol Neopentylglykol

PBT

Trilon-brands Ethylenediamine

POM PolyTHF®

N-Methylpyrrolidone Pyrrolidone

Plurafac-brands Keropur

Plasticizers Lutensol-brands

Glyoxal

Polymin Ethylenimin

Propionic acid

Air

Natural gas

Naphtha

Phosphate Potassium

chloride

Vacuum residue

Salt

Sulfur

Benzene

Cyclohexane

o-Xylene

Ethyl benzene Styrene

Polystyrene styropor

Fertilizers

Hydrogen cyanide Acrylic acid

Dichlorethan

Nitric acid

Formaldehyde

Butanediol

Oxo alcohols

Ethylene oxide

Propionic aldehyde Vinylethers

Nitrogen oxide

Methyl amines

Hydroxylamine

Oxo C4 Formic acid

Acetic acid

Urea

Propylene oxid

Na-salts of Sulfuric acid

Textil chemicals

Ludwigshafen

Ethylhexanol

Toluene TDI Lupranat brands

Verbund is in our DNA and hard to copy!

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 39

Ludwigshafen – the role model Verbund site

2,000 buildings

250 production assets**

km pipeline 2,800

km rail tracks

2,100 trucks per day

230 barges per day

~400 ~20

rail cars per day

* Including production area Friesenheimer Insel; ** Organized in 120 production plants

km² *

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 40

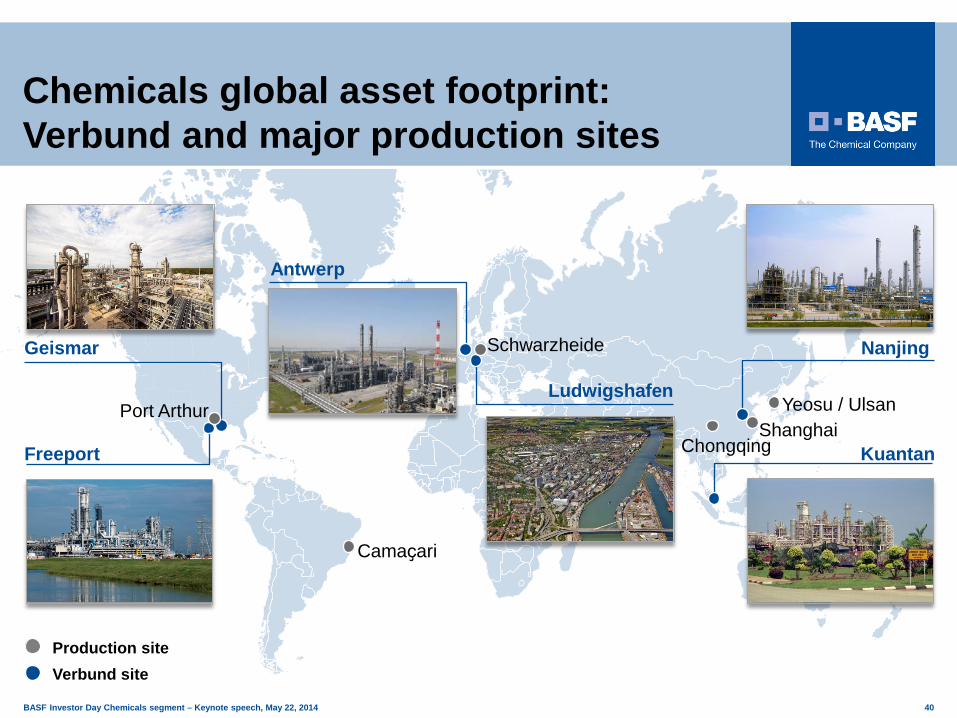

Chemicals global asset footprint: Verbund and major production sites

.

Kuantan

Nanjing

Antwerp

Ludwigshafen

Freeport

Geismar

Port Arthur Shanghai

Yeosu / Ulsan

Production site Verbund site

Chongqing

Schwarzheide

Camaҫari

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 41

Global reduction in carbon emissions of 6.1 million metric tons/a and reduction of waste

Example Ludwigshafen: avoidance of 7 million metric tons of freight/a = 280,000 fewer truckloads

Shared use of on-site facilities: fire department, security, waste water treatment and analytics

Verbund generates >€1 billion p.a. global cost savings*, supports sustainability

* Savings include only tangible synergies. Additional (intangible) benefits and retained profits are not included.

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 42

Verbund simulator enables

Optimized operations

Efficient utilization of assets

Management of value chains

Verbund proved flexible in 2008 / 2009 crisis

Capacity reductions

Flexible placement of people

Retained profitability

Flying start out of crisis

Verbund means efficiency and also flexibility – if steered intelligently

Verbund does allow for portfolio changes

e.g. fertilizers, styrenics

Demand forecast along BASF value chains

Optimized production

plan management

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 43

Philosophy of transfer pricing Safe and flexible supply at competitive prices Transfer prices linked to market prices No cross-subsidizing Value driven management in all steps of the

value chain

Additional Verbund benefits Flexible planning along value chains High security of supply, low logistics costs,

no sales and sourcing costs Joint quality management Joint engineering and process development Cross-functional knowledge exchange Additional capacity at Verbund sites dilutes fixed costs

Chemicals is at the heart of the BASF Production Verbund

Additional Verbund benefits

Transfer pricing

Downstream divisions

Chemicals segment

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 44

Propylene (Steam cracker)

Acrylic acid

Acrylic dispersions

Surfactants

Acrylic esters Acrylic resins

Superabsorbent polymers

Chemicals Performance Products

Case study acrylic acid: Value chain contributes cash flow of approx. €1 billion*

Each value chain step represents a potential merchant market outlet

* 2012

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 45

Case study acrylic acid: Leveraging the BASF Technology Verbund

Focused R&D to continuously improve acrylic acid process

Highly selective and efficient process catalysts

Proprietary technology for new process

– Higher yield

– Lower energy consumption

– Lower investment costs

In addition, four radically new processes being investigated in research

– One based on renewable raw materials

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 46

Case study acrylic acid: Leading technology strengthens profitability

Continuous productivity improvements

Smart production increase by run-time extension and higher throughput

All production sites contribute to innovation and improvement ideas

Quick transfer around the world ensured

Source: BASF estimate

Acrylic acid production technology benchmark Industry average costs = 100; normalized

BASF with best-in-class acrylic acid process

80

85

90

95

100

BASFnew process

BASFclassic process

Industry average

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 47

Natural Gas

Methanol Form-aldehyde

1,4-Butanediol

Tetra-hydrofuran PolyTHF®

POM***

Glues & Resins

gamma- Butyro- lactone

N-Methyl- pyrrolidone

Pyrroli-dones

PBT** Engineering plastics

Thermo- plastic PU

Personal care products

Case study acetylene value chain: cash flow of approx. €500 million*

Chemicals

Acetylene

* 2012 ** Polybutylene terephthalate *** Polyoxymethylene

Downstream units

Other specialties

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 48

Agenda

Trends in the chemicals market

Chemicals segment within BASF

Chemicals: At the core of the Verbund

Chemicals support growth of BASF

Shale Gas – An opportunity

Chemicals 2020

Capital expenditures drive profit growth Kuantan

Nanjing

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 49

Chemicals supplies key raw materials to Performance Products

Dispersions & Pigments

Acrylic acid Acrylates Butadiene Hydrochloric acid

Nutrition & Health

Isobutene Diethylketone Formic acid Propionic acid

Performance Chemicals

Isobutene Mono ethylene glycol Acrylates Amines Kerocom PIBA

Paper Chemicals

Acrylates Acrylic acid Butadiene Sodium hydroxide

Acrylic acid Ethylene oxide Propylene oxide Vinylpyrrolidone Specialty Amines

Care Chemicals

Performance Products

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 50

Chemicals supplies key raw materials to Functional Materials & Solutions

Construction Chemicals

Acrylic acid Acrylates Plasticizers Vinylethers TDI Chemicals Segment

Process catalysts

Coatings

Acrylates Plasticizers MDI Hexanediol

Catalysts

Solvents Zeolite templates

MDI & TDI Polyamides Mono ethylene glycol PBT PolyTHF®

Propylene oxide

Performance Materials

Functional Materials & Solutions

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 51

Chemicals supplies key raw materials to BASF Crop Protection

Crop Protection

Solvents Specialty amines Ethylene glycol Nitrotoluene Alcoholates

Agricultural Solutions

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 52

Merchant Market

Value chains of the BASF

Verbund

Ethylene Propylene Butadiene

Close to entire cracker output in Ludwigshafen is used within Verbund

<5%

Raffinates Aromatics …

Cracker products Ludwigshafen

>95%

BASF-YPC Nanjing supply for captive demand:

2006: 60% 2014: 75% BASF SE, Ludwigshafen, Germany BASF Investor Day Chemicals segment – Key note speech, May 22, 2014 52

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 53

MDI sales to downstream businesses Polyurethane system houses

Thermoplastic polyurethanes

High captive share of MDI for BASF’s polyurethane systems

MDI sales split

Europe & USA 2013

Global production network (capacity: 1,340 kt) Antwerp

Geismar

Caojing

Yeosu (Korea)

3rd Party sales Captive demand

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 54

3rd Party sales Captive demand

MDI global

sales split 2013

High captive share of MDI for BASF’s polyurethane systems

MDI sales to downstream businesses Polyurethane system houses

Thermoplastic polyurethanes

Global production network (capacity: 1,340 kt) Antwerp

Geismar

Caojing

Yeosu (Korea)

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 55

Acrylic acid sales to downstream businesses Superabsorbent polymers

Dispersions

Esters

Resins

Surfactants

High captive share of acrylic acid for BASF’s SAP* and dispersions

Acrylic acid sales split

Europe & USA 2013

Global production network (capacity: 1,350 kt) Ludwigshafen

Antwerp

Freeport

Nanjing

Kuantan 3rd Party sales Captive demand

* Superabsorbent polymers

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 56

Acrylic acid global

sales split 2013

3rd Party sales Captive demand

High captive share of acrylic acid for BASF’s SAP* and dispersions

* Superabsorbent polymers

Acrylic acid sales to downstream businesses Superabsorbent polymers

Dispersions

Esters

Resins

Surfactants

Global production network (capacity: 1,350 kt) Ludwigshafen

Antwerp

Freeport

Nanjing

Kuantan

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 57

Caprolactam sales to downstream businesses Engineering plastics

Polymers for packaging films

Monofilaments

Growing captive share of caprolactam for BASF’s downstream polyamide polymers

Caprolactam global

sales split 2013

Operational excellence in existing plants (capacity: 800 kt) Ludwigshafen

Antwerp

Freeport

3rd Party sales Captive demand

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 58

Caprolactam global

sales split 2015+

3rd party sales Captive demand

Growing captive share of caprolactam for BASF’s downstream polyamide polymers

Operational excellence in existing plants (capacity: 800 kt) Ludwigshafen

Antwerp

Freeport

Caprolactam sales to downstream businesses Engineering plastics

Polymers for packaging films

Monofilaments

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 59

Agenda

Trends in the chemicals market

Chemicals segment within BASF

Chemicals: At the core of the Verbund

Chemicals support growth of BASF

Shale Gas – An opportunity

Chemicals 2020

Capital expenditures drive profit growth

Freeport

Geismar

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 60

High capex intensity commands extraordinary focus on capex allocation and project control

Extensive use of cash-cost benchmarking

Preparation of solid business cases for all projects ensures sound decision-making

Projects approved only if cost of capital is earned even at hypothetical marginal producer price level

Capex Chemicals

Capex budget 2014-2018 by segment

Other 13%

Chemicals* 33%

Performance Products 15%

€ 20 billion

Agricultural Solutions 7%

Oil & Gas 20%

Functional Materials & Solutions 12%

* Including gas-to-propylene project U.S. Gulf Coast, TDI Ludwigshafen, MDI Chongqing, Isononanol Maoming

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 61

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

50

100

150

200

250

300

350

400

2000 2001 2002 2003 2004 2005 2006* 2007* 2008 2009 2010 2011 2012 2013 2014 2015 2016restated

Consolidated sales indexed (2000 = 100)

Capex as % of sales

Capex focused on organic growth as well as on bottom-line improving projects

Capex as % of sales Chemicals segment

Consolidated sales Chemicals segment

Capex outlook

* Without Catalysts (now part of Functional Materials & Solutions segment)

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 62

Modelling cost curve dynamics

Market demand

Marginal producer price Cas

h co

sts

Plant 1 Plant 2

Plant 3

Plant 4

Margin

Cash costs are a function of

Technology position

Degree of integration

Scale

Raw materials source

Competitiveness in the market also influenced by

Logistics costs

Sales costs

Production capacity

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 63

Continuous process innovation leads to best-in-class technology

Proprietary BASF technology, with best-in-class process

Significant cost synergies due to two parallel projects (Nanjing, Camacari)

Acrylic acid will supply downstream units (superabsorbent polymers; acrylates)

Cost curve case study: Acrylic acid China

Acrylic Acid cash cost curve, China average cash costs 2015 in US$/kg

Cas

h co

sts

BAS

F

clas

sic

proc

ess

BAS

F

new

pro

cess

Source: BASF estimate

Production capacity

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 64

Leading single-train technology

New TDI plant strengthens and benefits from Ludwigshafen Verbund

Schwarzheide plant to be closed after start-up of new plant

New TDI plant re-balances competitive environment of European TDI market

BAS

F Eu

rope

Production capacity

Cas

h co

sts

Source: BASF estimate

TDI cash cost curve, Europe average cash costs 2015 in US$/kg

BAS

F ne

w

Ludw

igsh

afen

BAS

F Sc

hwar

zhei

de

New Ludwigshafen TDI plant will provide superior cost structure in Europe

Cost curve case study: TDI Europe

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 65

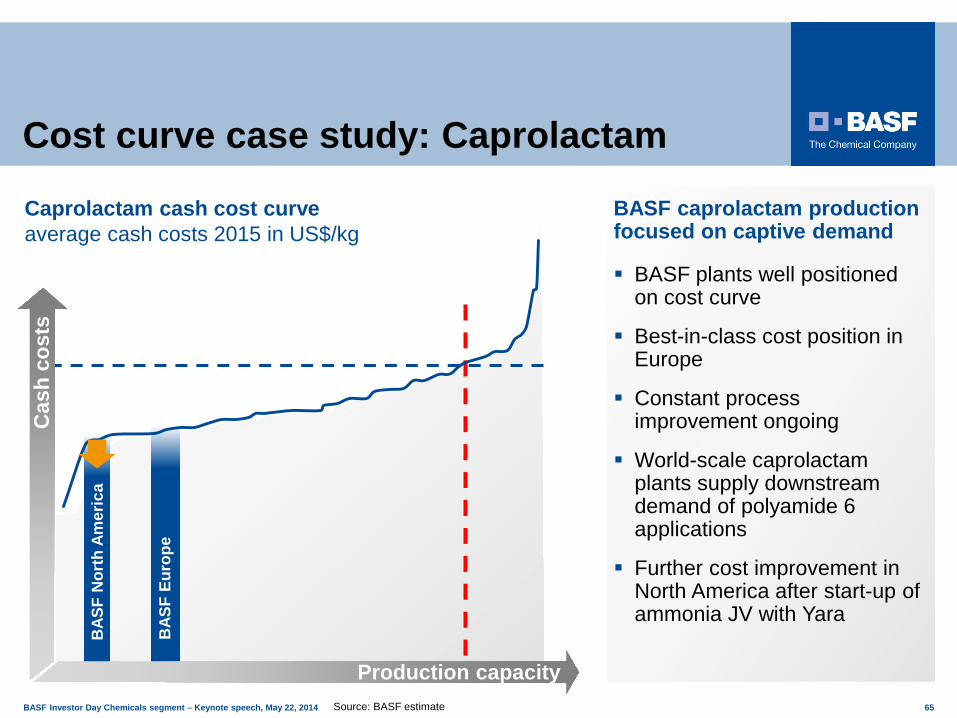

BASF caprolactam production focused on captive demand

BASF plants well positioned on cost curve

Best-in-class cost position in Europe

Constant process improvement ongoing

World-scale caprolactam plants supply downstream demand of polyamide 6 applications

Further cost improvement in North America after start-up of ammonia JV with Yara

Caprolactam cash cost curve average cash costs 2015 in US$/kg

BAS

F N

orth

Am

eric

a

BAS

F Eu

rope

Production capacity

Cas

h co

sts

Cost curve case study: Caprolactam

Source: BASF estimate

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 66

Sites with major announced investment projects

Camaҫari

Korla

Production site Verbund site

Chemicals investments support growth of downstream units in Emerging Markets

Chongqing

Nanjing Shanghai

Freeport

Geismar Port Arthur

Antwerp

Acrylic acid

Acrylic acid

Ludwigshafen

Kuantan Maoming

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 67

Sites with major announced investment projects

Korla

Chongqing

Production site Verbund site

Chemicals investments enable growth in Asia, especially in China

Kuantan

Nanjing

Freeport

Geismar Shanghai

Maoming

Port Arthur

MDI

Antwerp

Isononanol

Ludwigshafen

Camaҫari

Polyamides

Butanediol, PolyTHF®

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 68

.

Sites with major announced investment projects

Korla

Production site Verbund site

Chemicals investments support growth of the Verbund in Europe

Chongqing Barcelona

Freeport

Geismar

Antwerp Ludwigshafen

Shanghai

Maoming

Port Arthur

Butadiene extraction

Kuantan Camaҫari

TDI Nanjing

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 69

Agenda

Trends in the chemicals market

Chemicals segment within BASF

Chemicals: At the core of the Verbund

Chemicals support growth of BASF

Shale Gas – An opportunity

Chemicals 2020

Capital expenditures drive profit growth

Freeport

Geismar

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 70

Price development of oil / natural gas

Shale gas in the U.S.: Lower energy and feedstock cost

Increased U.S. shale gas production disconnected crude oil prices from natural gas prices in North America

Increased production of natural gas liquids (NGLs): ethane, propane, butane

NGL price drop drives shift to lighter cracker feed slates

– Improved profitability of light feed crackers

– Narrow cracker output

Game changer shale gas

Crude Oil WTI

0

5

10

15

20

0

20

40

60

80

100

120

1990 1995 2000 2005 2010 2015 2020

Source: IHS Inc. The use of this content was authorized in advance by IHS. Any further use or redistribution of this content is strictly prohibited without written permission by IHS. All rights reserved. Natural gas price Germany: Statistisches Bundesamt “Grenzübergabepreis” Germany

Natural Gas USA

Natural Gas Germany

Crude oil in US$/bbl

Natural gas in US$/MMBTU

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 71

North American shale gas will only have a limited impact on BASF in Europe

North America

Low raw material costs to be kept at chemical producer stage

Impact of low raw material costs to diminish in downstream production

Europe

BASF exited polyolefins and PVC more than 10 years ago

BASF is a net purchaser of methanol

Integrated production sites will remain competitive

Expected key exports: Polyolefines PVC Methanol

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 72

Natural Gas Liquids Ethane Propane Butane

► Cracker Feed

Shale gas is beneficial for methane and ethane based chemistry

Methane and ethane to retain their advantageous cost position in North America

Low transportability of ethane ► Shift to ethane crackers

Propane and butane easy to transport ► Export with link to global market

Very limited transportability of methane

Methane to remain an abundant product with low pricing in North America (despite LNG projects)

Methane ► Power plants ► Ammonia ► Methanol

Composition of shale gas

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 73

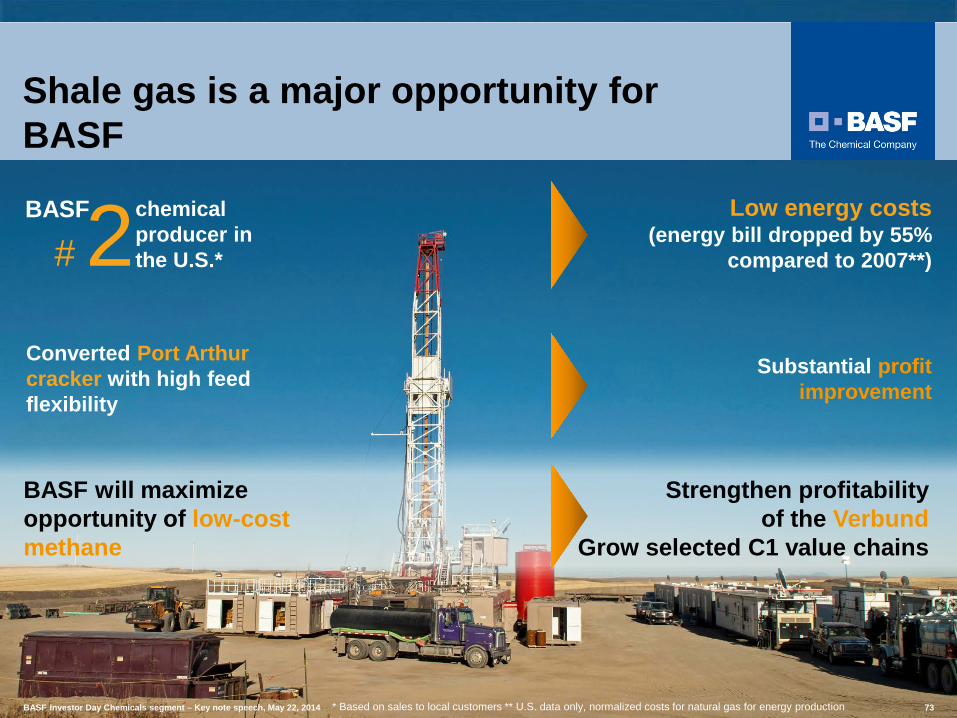

Converted Port Arthur cracker with high feed flexibility

# 2 chemical producer in the U.S.*

BASF

Shale gas is a major opportunity for BASF

Low energy costs (energy bill dropped by 55%

compared to 2007**)

Substantial profit improvement

BASF will maximize opportunity of low-cost methane

Strengthen profitability of the Verbund

Grow selected C1 value chains

* Based on sales to local customers ** U.S. data only, normalized costs for natural gas for energy production BASF Investor Day Chemicals segment – Key note speech, May 22, 2014 73

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 74

Port Arthur cracker* has full feed flexibility benefiting from low raw materials costs

Since Q1 2013, full flexibility to switch to most economic feed: naphtha, ethane, propane, butane

Cracker includes splitting unit, which optimizes quality of shale gas feed

Added 10th cracker furnace, increased capacity to 1 million metric tons

Improved cash margins through feed flexibility

* BASF Total Petrochemicals, LLC; Joint venture BASF 60%, Total 40%

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 75

Ammonia joint venture* enables low raw materials costs for BASF downstreams

World-scale producer economics plant with focus on captive demand only (BASF)

Site: BASF Verbund site Freeport, Texas

Capacity: 750 kt p.a.

Advantages of hydrogen & nitrogen based technology:

– Lower capital investment

– No greenhouse gas emissions

– Faster execution

Improved cost position for BASF’s downstream products

Caprolactam Isocyanates Amines

Yara

…

Long-term sourcing contracts

Yara-BASF joint venture

BASF Group

Ammonia

Nitrogen** Hydrogen**

merchant market

* Project under evaluation ** Hydrogen and nitrogen are available in the Freeport area

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 76

BASF is currently a net-purchaser of propylene in North America

Port Arthur propylene production insufficient to cover growing captive demand

Additional quantities are purchased from the market

Propylene is a key raw material for several value chains

Propylene supply North America

Acrylic acid Oxo-alcohols Polyols …

Flexible feed (NGL’s, Naphtha)

Propylene purchase from market

Propylene (Port Arthur cracker)

Downstream products

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 77

Gas-to-propylene complex* covers internal demand at attractive conditions

U.S. Gulf Coast location

World-scale plant

Start-up: ~2019

Port Arthur cracker and new on-purpose propylene complex to cover entire captive propylene demand

Mid-term no sales to merchant market

Lower cost than alternative PDH technology

Cost leading gas-to-propylene technology covers supply gap

Propylene supply North America

Acrylic acid Oxo-alcohols Polyols …

Propylene Propylene (Port Arthur cracker)

Downstream products

Methanol

Methane (from shale gas)

Flexible feed (NGL’s, Naphtha)

* Project under evaluation

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 78

Cost position of BASF plants in North America will be in top quartile

Shale gas based projects mostly to supply downstreams

Shale gas based projects will drive bottom line growth

Further selected projects under evaluation

Shale gas-driven investments will significantly improve BASF’s earnings

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 79

Agenda

Trends in the chemicals market

Chemicals segment within BASF

Chemicals: At the core of the Verbund

Chemicals support growth of BASF

Shale Gas – An opportunity

Chemicals 2020

Capital expenditures drive profit growth

Freeport

Geismar

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 80

Chemicals enable growth of downstream businesses

Chemicals benefit from downstream growth

Investment projects mainly improve cost positions

Key success factors Operational and commercial

excellence Process innovation Focused and disciplined

capex plan Further Verbund integration

Chemicals will continue to contribute to BASF profit

Sales Chemicals in billion €

BASF’s Chemicals segment: The success story continues!

EBITDA Chemicals in billion €

0

5

10

15

20

25

30

35

2013 Target 2020

Sales to third parties

Intersegmental transfers EBITDA Chemicals

CAGR 2013-2020 4-5%

0

5

10

15

2013 Target 2020

EBITDA upside range

CAGR 2013-2020 6-7.5%

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 81

BASF’s Chemicals segment is a strong cash and earnings contributor We will ► continue to strengthen the Verbund, create synergies and

add value ► maintain our high level of profitability through process

innovations and stringent cost management ► grow externally with the chemicals market

Our strategic focus is to enable and support growth of ► BASF’s downstream segments ► BASF in emerging markets

Shale gas is an opportunity for BASF

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 82

Key figures to remember about BASF Chemicals: ► Growth in line with market (until 2020) : ~4.3% p.a.

► Capex budget (2014 – 2018): ~€6.5 billion ► Consolidated sales 2013: €23.4 billion 2020:~€30 billion ► EBITDA: 2013: €3 billion 2020: €4.5 – €5.0 billion

BASF Investor Day Chemicals segment – Keynote speech, May 22, 2014 83