Embed Size (px)

Citation preview

1/18

Results

3Q12

Nov. 06, 2012

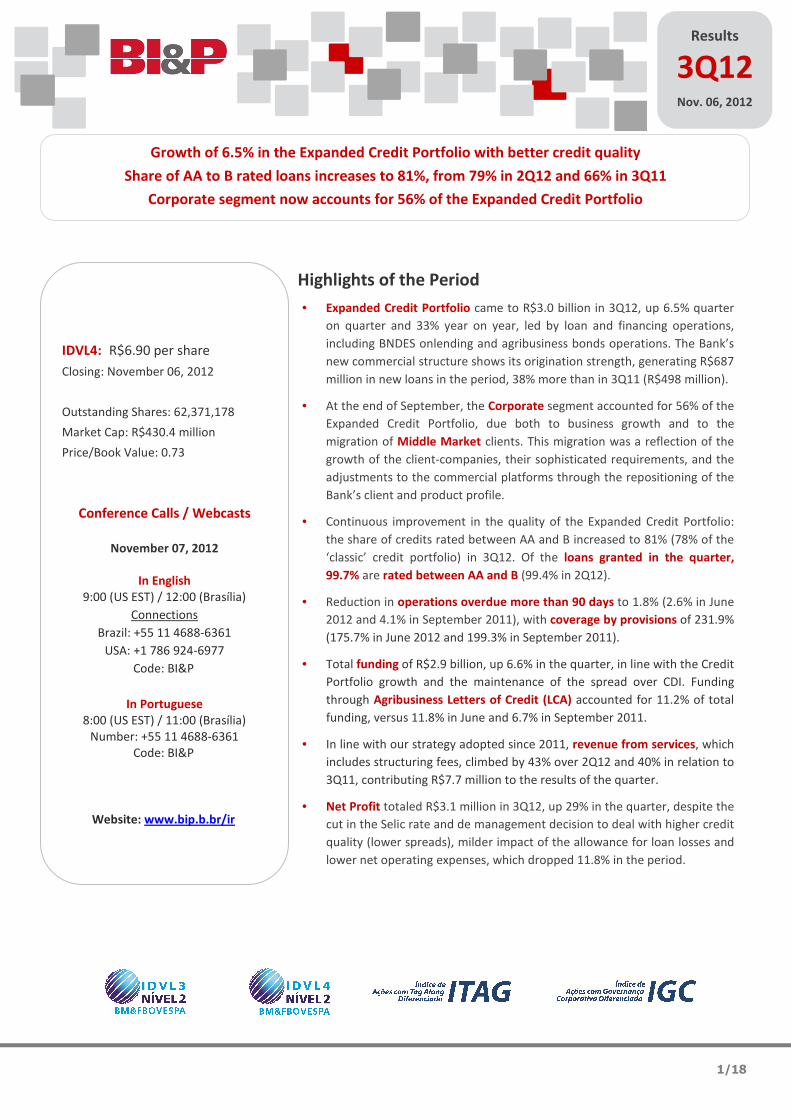

IDVL4: R$6.90 per share

Closing: November 06, 2012

Outstanding Shares: 62,371,178

Market Cap: R$430.4 million

Price/Book Value: 0.73

Conference Calls / Webcasts

November 07, 2012

In English

9:00 (US EST) / 12:00 (Brasília)

Connections

Brazil: +55 11 4688-6361

USA: +1 786 924-6977

Code: BI&P

In Portuguese

8:00 (US EST) / 11:00 (Brasília)

Number: +55 11 4688-6361

Code: BI&P

Website: www.bip.b.br/ir

Growth of 6.5% in the Expanded Credit Portfolio with better credit quality

Share of AA to B rated loans increases to 81%, from 79% in 2Q12 and 66% in 3Q11

Corporate segment now accounts for 56% of the Expanded Credit Portfolio

Highlights of the Period

• Expanded Credit Portfolio came to R$3.0 billion in 3Q12, up 6.5% quarter

on quarter and 33% year on year, led by loan and financing operations,

including BNDES onlending and agribusiness bonds operations. The Bank’s

new commercial structure shows its origination strength, generating R$687

million in new loans in the period, 38% more than in 3Q11 (R$498 million).

• At the end of September, the Corporate segment accounted for 56% of the

Expanded Credit Portfolio, due both to business growth and to the

migration of Middle Market clients. This migration was a reflection of the

growth of the client-companies, their sophisticated requirements, and the

adjustments to the commercial platforms through the repositioning of the

Bank’s client and product profile.

• Continuous improvement in the quality of the Expanded Credit Portfolio:

the share of credits rated between AA and B increased to 81% (78% of the

‘classic’ credit portfolio) in 3Q12. Of the loans granted in the quarter,

99.7% are rated between AA and B (99.4% in 2Q12).

• Reduction in operations overdue more than 90 days to 1.8% (2.6% in June

2012 and 4.1% in September 2011), with coverage by provisions of 231.9%

(175.7% in June 2012 and 199.3% in September 2011).

• Total funding of R$2.9 billion, up 6.6% in the quarter, in line with the Credit

Portfolio growth and the maintenance of the spread over CDI. Funding

through Agribusiness Letters of Credit (LCA) accounted for 11.2% of total

funding, versus 11.8% in June and 6.7% in September 2011.

• In line with our strategy adopted since 2011, revenue from services, which

includes structuring fees, climbed by 43% over 2Q12 and 40% in relation to

3Q11, contributing R$7.7 million to the results of the quarter.

• Net Profit totaled R$3.1 million in 3Q12, up 29% in the quarter, despite the

cut in the Selic rate and de management decision to deal with higher credit

quality (lower spreads), milder impact of the allowance for loan losses and

lower net operating expenses, which dropped 11.8% in the period.

2/18

Summary

Message from the Management ................................................................................................................ 3

Macroeconomic Environment .................................................................................................................... 4

Key Indicators .............................................................................................................................................. 5

Operating Performance .............................................................................................................................. 6

Credit Portfolio ............................................................................................................................................ 9

Funding ..................................................................................................................................................... 12

Liquidity ..................................................................................................................................................... 13

Capital Adequacy ...................................................................................................................................... 13

Risk Ratings ............................................................................................................................................... 14

Capital Markets ......................................................................................................................................... 14

Balance Sheet ............................................................................................................................................ 16

Income Statement .................................................................................................................................... 18

3/18

Message from the Management

With the Brazilian economy’s growth improving in the third quarter, in reaction to the government’s economic incentives,

our credit portfolio resumed growth, especially in loans and financing, which include BNDES onlendings, and agro bonds

(Rural Product Certificates (CPR), Agribusiness Credit Rights Certificate (CDCA) and Agribusiness Deposit Certificates and

Warrants (CDA/WA). Our expanded credit portfolio reached R$3.0 billion, up 6.5% in the quarter and 33% in a year,

increasing the share of loans rated between AA and B to 81% (compared to 76% in September 2011), in line with our

strategy of growth combined with quality. In this regard, considering the economic scenario until June, in the second half

we decided to focus further on better quality credits, even if with lower spreads and shorter terms, resulting in a higher

share of the Corporate segment (companies with annual revenue of between R$400 million and R$2.0 billion). This client

portfolio currently accounts for 56% of total loans granted. In a more favorable scenario, expected in 2013, we should

resume Middle Market segment growth retaking the strategic 45% Corporate and 55% Middle Market mix.

Loan operations overdue more than 90 days dropped from 2.6% in 2Q12 to 1.8% in 3Q12, reflecting both the better quality

of the portfolio generated in the past 18 months and the write-offs of R$16 million in the quarter.

Funding stood at R$2.9 billion, an increase of 6.6%, in line with the credit portfolio, growing by 21% in relation to

September 2011. Deposits in Real still account for 75% of total funding, maintaining lower costs in relation to the same

period in 2011. In view of the uncertainties in the international scenario and a possible negative reaction to the recent

developments in Brazil’s financial system, we decided to increase our long-term funding operations at the end of the

quarter, while preserving the limit available for DPGE I, as its extinction is imminent due to the availability of DPGE II for

corporate loans, expected in the first half of 2013.

The development of products continues to deserve mention, not only because of the business growth driven by products

launched last year - related to the agricultural sector and to the production chains of our large clients - but also due to the

beginning of funding through real estate letters of credit in the third quarter.

As already mentioned several times, our business plan is not short-term and is only just beginning. We don’t just have a

vision, but rather a project to build a bank that serves as a benchmark in the Brazilian market. This project will be rolled out

in the long term, sustained by a strategy architecture whose foundations were laid 18 months ago. The bases of the pillars

that sustain this architecture have been under construction since March 2011. Our vision and our project are grounded in

five main pillars:

People – Structural and systematic planning of people, valuing and consolidating meritocracy in an objective

manner.

Processes and technology – Continuous review of processes in the pursuit of speed, efficiency and safety, creating

technological differentials in terms of both processes and customer service, while seeking technological excellence

in all of the Bank’s areas.

Services and products – Incentives to cross-selling, development and growth of investment bank and fixed income

activities, creation of alternative distribution channels and structuring of innovation groups.

Creation of franchise value – Development of expertise in credit and risk analysis as well as in structures that

create competitive advantages in certain segments of the economy.

Planning of strategic moves – The scenario in which we operate is constantly changing and, in order for us to

adjust to these changes, we have to constantly monitor the market and its trends, and to be open and prepared

for business opportunities that are in line with our vision and our values.

We will not grow at any cost. Nevertheless, we wish to control our own destiny and lead the careful construction of these

pillars, which, grounded in our values, will sustain our future growth in a secure and profitable manner, while supporting

our vision in the direction of the Bank we want to build.

4/18

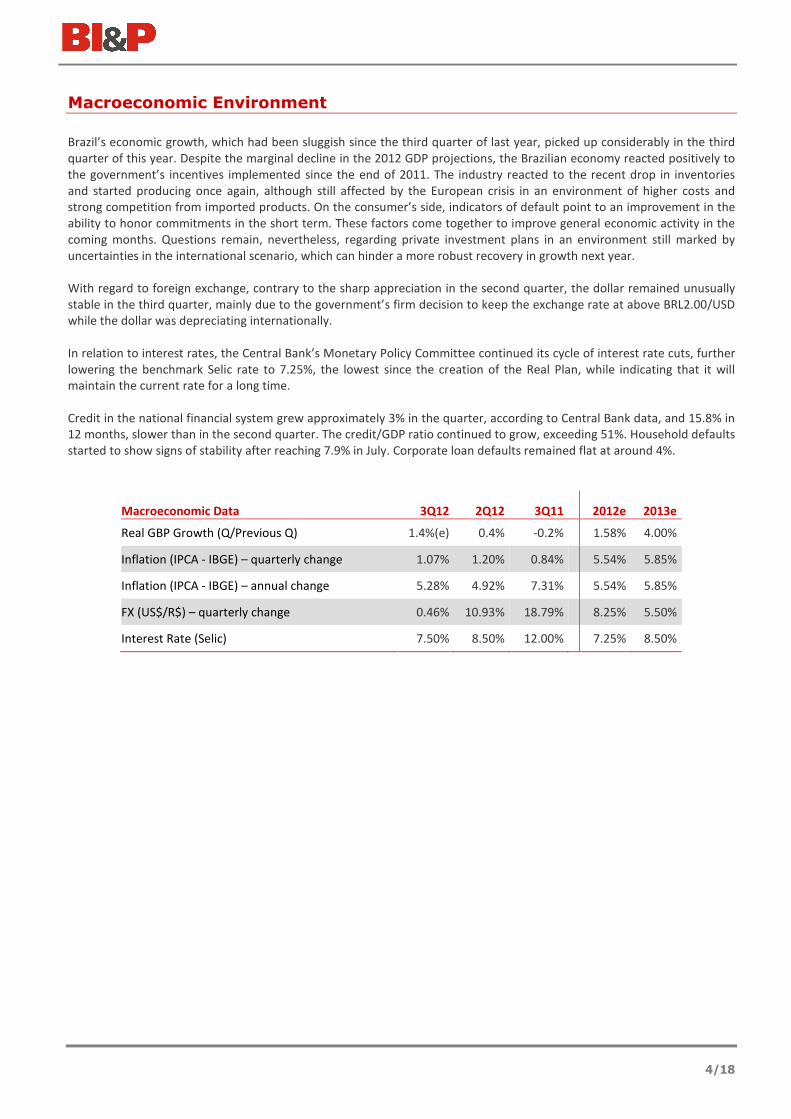

Macroeconomic Environment

Brazil’s economic growth, which had been sluggish since the third quarter of last year, picked up considerably in the third

quarter of this year. Despite the marginal decline in the 2012 GDP projections, the Brazilian economy reacted positively to

the government’s incentives implemented since the end of 2011. The industry reacted to the recent drop in inventories

and started producing once again, although still affected by the European crisis in an environment of higher costs and

strong competition from imported products. On the consumer’s side, indicators of default point to an improvement in the

ability to honor commitments in the short term. These factors come together to improve general economic activity in the

coming months. Questions remain, nevertheless, regarding private investment plans in an environment still marked by

uncertainties in the international scenario, which can hinder a more robust recovery in growth next year.

With regard to foreign exchange, contrary to the sharp appreciation in the second quarter, the dollar remained unusually

stable in the third quarter, mainly due to the government’s firm decision to keep the exchange rate at above BRL2.00/USD

while the dollar was depreciating internationally.

In relation to interest rates, the Central Bank’s Monetary Policy Committee continued its cycle of interest rate cuts, further

lowering the benchmark Selic rate to 7.25%, the lowest since the creation of the Real Plan, while indicating that it will

maintain the current rate for a long time.

Credit in the national financial system grew approximately 3% in the quarter, according to Central Bank data, and 15.8% in

12 months, slower than in the second quarter. The credit/GDP ratio continued to grow, exceeding 51%. Household defaults

started to show signs of stability after reaching 7.9% in July. Corporate loan defaults remained flat at around 4%.

Macroeconomic Data 3Q12 2Q12 3Q11 2012e 2013e

Real GBP Growth (Q/Previous Q) 1.4%(e) 0.4% -0.2%

1.58% 4.00%

Inflation (IPCA - IBGE) – quarterly change 1.07% 1.20% 0.84%

5.54% 5.85%

Inflation (IPCA - IBGE) – annual change 5.28% 4.92% 7.31%

5.54% 5.85%

FX (US$/R$) – quarterly change 0.46% 10.93% 18.79%

8.25% 5.50%

Interest Rate (Selic) 7.50% 8.50% 12.00%

7.25% 8.50%

5/18

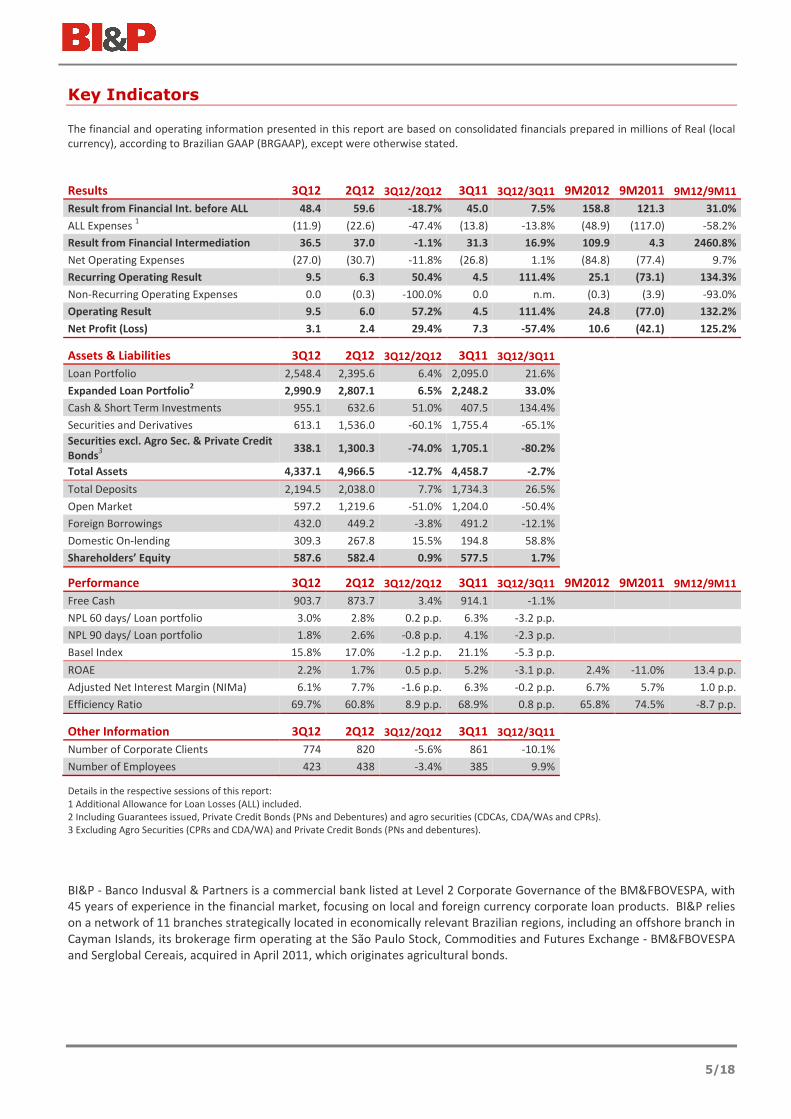

Key Indicators

The financial and operating information presented in this report are based on consolidated financials prepared in millions of Real (local

currency), according to Brazilian GAAP (BRGAAP), except were otherwise stated.

Results 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11 9M2012 9M2011 9M12/9M11

Result from Financial Int. before ALL 48.4 59.6 -18.7% 45.0 7.5% 158.8 121.3 31.0%

ALL Expenses 1 (11.9) (22.6) -47.4% (13.8) -13.8% (48.9) (117.0) -58.2%

Result from Financial Intermediation 36.5 37.0 -1.1% 31.3 16.9% 109.9 4.3 2460.8%

Net Operating Expenses (27.0) (30.7) -11.8% (26.8) 1.1% (84.8) (77.4) 9.7%

Recurring Operating Result 9.5 6.3 50.4% 4.5 111.4% 25.1 (73.1) 134.3%

Non-Recurring Operating Expenses 0.0 (0.3) -100.0% 0.0 n.m. (0.3) (3.9) -93.0%

Operating Result 9.5 6.0 57.2% 4.5 111.4% 24.8 (77.0) 132.2%

Net Profit (Loss) 3.1 2.4 29.4% 7.3 -57.4% 10.6 (42.1) 125.2%

Assets & Liabilities 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11

Loan Portfolio 2,548.4 2,395.6 6.4% 2,095.0 21.6%

Expanded Loan Portfolio2 2,990.9 2,807.1 6.5% 2,248.2 33.0%

Cash & Short Term Investments 955.1 632.6 51.0% 407.5 134.4%

Securities and Derivatives 613.1 1,536.0 -60.1% 1,755.4 -65.1%

Securities excl. Agro Sec. & Private Credit

Bonds3

338.1 1,300.3 -74.0% 1,705.1 -80.2%

Total Assets 4,337.1 4,966.5 -12.7% 4,458.7 -2.7%

Total Deposits 2,194.5 2,038.0 7.7% 1,734.3 26.5%

Open Market 597.2 1,219.6 -51.0% 1,204.0 -50.4%

Foreign Borrowings 432.0 449.2 -3.8% 491.2 -12.1%

Domestic On-lending 309.3 267.8 15.5% 194.8 58.8%

Shareholders’ Equity 587.6 582.4 0.9% 577.5 1.7%

Performance 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11 9M2012 9M2011 9M12/9M11

Free Cash 903.7 873.7 3.4% 914.1 -1.1%

NPL 60 days/ Loan portfolio 3.0% 2.8% 0.2 p.p. 6.3% -3.2 p.p.

NPL 90 days/ Loan portfolio 1.8% 2.6% -0.8 p.p. 4.1% -2.3 p.p.

Basel Index 15.8% 17.0% -1.2 p.p. 21.1% -5.3 p.p.

ROAE 2.2% 1.7% 0.5 p.p. 5.2% -3.1 p.p. 2.4% -11.0% 13.4 p.p.

Adjusted Net Interest Margin (NIMa) 6.1% 7.7% -1.6 p.p. 6.3% -0.2 p.p. 6.7% 5.7% 1.0 p.p.

Efficiency Ratio 69.7% 60.8% 8.9 p.p. 68.9% 0.8 p.p. 65.8% 74.5% -8.7 p.p.

Other Information 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11

Number of Corporate Clients 774 820 -5.6% 861 -10.1%

Number of Employees 423 438 -3.4% 385 9.9%

Details in the respective sessions of this report:

1 Additional Allowance for Loan Losses (ALL) included.

2 Including Guarantees issued, Private Credit Bonds (PNs and Debentures) and agro securities (CDCAs, CDA/WAs and CPRs).

3 Excluding Agro Securities (CPRs and CDA/WA) and Private Credit Bonds (PNs and debentures).

BI&P - Banco Indusval & Partners is a commercial bank listed at Level 2 Corporate Governance of the BM&FBOVESPA, with

45 years of experience in the financial market, focusing on local and foreign currency corporate loan products. BI&P relies

on a network of 11 branches strategically located in economically relevant Brazilian regions, including an offshore branch in

Cayman Islands, its brokerage firm operating at the São Paulo Stock, Commodities and Futures Exchange - BM&FBOVESPA

and Serglobal Cereais, acquired in April 2011, which originates agricultural bonds.

6/18

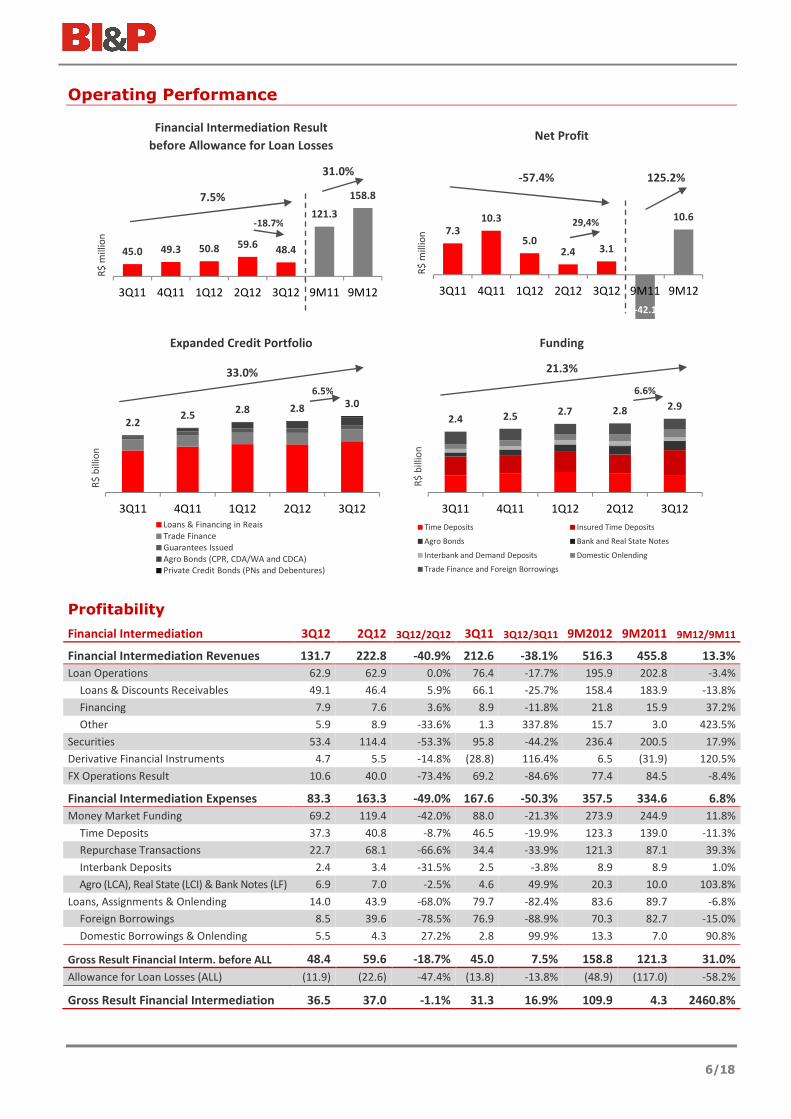

Operating Performance

Financial Intermediation Result

before Allowance for Loan Losses

Net Profit

Expanded Credit Portfolio Funding

Profitability

Financial Intermediation 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11 9M2012 9M2011 9M12/9M11

Financial Intermediation Revenues 131.7 222.8 -40.9% 212.6 -38.1% 516.3 455.8 13.3%

Loan Operations 62.9 62.9 0.0% 76.4 -17.7% 195.9 202.8 -3.4%

Loans & Discounts Receivables 49.1 46.4 5.9% 66.1 -25.7% 158.4 183.9 -13.8%

Financing 7.9 7.6 3.6% 8.9 -11.8% 21.8 15.9 37.2%

Other 5.9 8.9 -33.6% 1.3 337.8% 15.7 3.0 423.5%

Securities 53.4 114.4 -53.3% 95.8 -44.2% 236.4 200.5 17.9%

Derivative Financial Instruments 4.7 5.5 -14.8% (28.8) 116.4% 6.5 (31.9) 120.5%

FX Operations Result 10.6 40.0 -73.4% 69.2 -84.6% 77.4 84.5 -8.4%

Financial Intermediation Expenses 83.3 163.3 -49.0% 167.6 -50.3% 357.5 334.6 6.8%

Money Market Funding 69.2 119.4 -42.0% 88.0 -21.3% 273.9 244.9 11.8%

Time Deposits 37.3 40.8 -8.7% 46.5 -19.9% 123.3 139.0 -11.3%

Repurchase Transactions 22.7 68.1 -66.6% 34.4 -33.9% 121.3 87.1 39.3%

Interbank Deposits 2.4 3.4 -31.5% 2.5 -3.8% 8.9 8.9 1.0%

Agro (LCA), Real State (LCI) & Bank Notes (LF) 6.9 7.0 -2.5% 4.6 49.9% 20.3 10.0 103.8%

Loans, Assignments & Onlending 14.0 43.9 -68.0% 79.7 -82.4% 83.6 89.7 -6.8%

Foreign Borrowings 8.5 39.6 -78.5% 76.9 -88.9% 70.3 82.7 -15.0%

Domestic Borrowings & Onlending 5.5 4.3 27.2% 2.8 99.9% 13.3 7.0 90.8%

Gross Result Financial Interm. before ALL 48.4 59.6 -18.7% 45.0 7.5% 158.8 121.3 31.0%

Allowance for Loan Losses (ALL) (11.9) (22.6) -47.4% (13.8) -13.8% (48.9) (117.0) -58.2%

Gross Result Financial Intermediation 36.5 37.0 -1.1% 31.3 16.9% 109.9 4.3 2460.8%

45.0 49.3 50.8 59.648.4

121.3

158.8

3Q11 4Q11 1Q12 2Q12 3Q12 9M11 9M12

R$

mill

ion

7.310.3

5.02.4 3.1

10.6

3Q11 4Q11 1Q12 2Q12 3Q12 9M11 9M12

R$

mill

ion

2.22.5

2.8 2.8 3.0

3Q11 4Q11 1Q12 2Q12 3Q12

R$

bill

ion

Loans & Financing in Reais

Trade Finance

Guarantees Issued

Agro Bonds (CPR, CDA/WA and CDCA)

Private Credit Bonds (PNs and Debentures)

2.4 2.5 2.7 2.8 2.9

3Q11 4Q11 1Q12 2Q12 3Q12

R$

bill

ion

Time Deposits Insured Time Deposits

Agro Bonds Bank and Real State Notes

Interbank and Demand Deposits Domestic Onlending

Trade Finance and Foreign Borrowings

7.5%

31.0% -57.4% 125.2%

-42.1

33.0%

6.5%

21.3%

6.6%

29,4% -18.7%

7/18

Result from Financial Intermediation before expenses with the allowance for loan losses totaled R$48.4 million in 3Q12,

down 18.7% in the quarter and up 7.5% year on year, chiefly due to the lowering of the benchmark Selic rate and lower

spreads on loans as a result of the greater share of the Corporate segment in the credit portfolio, as detailed below:

Revenue from Loan Operations remained flat in relation to 2Q12, despite the cuts in the Selic rate and the impact of the

international crisis on the Brazilian economy. The Corporate segment accounted for 54% of total loans and financing

disbursed in local and foreign currency, versus 45% in 2Q12, accompanied by a natural trend of lower spreads and better

quality of credit. Therefore, the fact that Revenue from Loan Operations remained flat reflects the growth in the average

balances of loans, discounted bills and BNDES onlending operations. Another factor that contributed to this result was

credit recovery totaling R$5.7 million in 3Q12 (compared to R$8.5 million in 2Q12).

Income from Securities, which includes the results from the treasury’s directional portfolio and CPR, CDA/WA and

Debenture operations, is offset by funding expenses. The quarter-on-quarter reduction of 53.3% seen in Income from

Securities resulted from the cut in the benchmark interest rate and, mainly, from the lower balance of securities subject to

repurchase agreements, which dropped from R$724.7 million at the end of 2Q12 to R$9.0 million on September 30. These

operations also led to a reduction in open market funding expenses, from R$1,220 million on June 30 to R$597 million on

September 30. The combination of lower volume and the cut in the interest rate resulted in a 66.6% decline in expenses

with repo operations.

The Result from Derivative Financial Instruments includes results from operations involving swaps, forwards, futures and

options used to hedge against exchange exposure and interest rates for funding operations indexed to the IPCA and IGPM,

as well as foreign borrowings (non-trade related), to hedge coffee prices resulting from CPR operations and indexers of

federal government bonds held in the securities portfolio, in addition to the directional portfolio. Thus, the result from

derivative financial instruments has offsets in both revenues and expenses from financial intermediation resulting from

operations in local and foreign currency, commodities and indexes.

After deducting the expenses with allowance for loan losses of R$11.9 million in the quarter (R$22.6 million in 2Q12), as a

reflection of the improved quality of the credit portfolio since March 2011, the Result from Financial Intermediation was

R$36.5 million, remaining at the same level as in the previous quarter.

In the nine-month period ended September 30, Revenues from Financial Intermediation totaled R$516.3 million, up 13.3%

over the same period in 2011, while expenses from financial intermediation (excluding expenses with allowance for loan

losses) increased only slightly by 6.8% to R$357.5 million. Thus, the comparison of the Result from Financial Intermediation

in the nine-month periods of the last two years pointed to a 31.0% growth which, consequent to the drop in expenses with

allowance for loan losses, from R$117.0 million until September 2011 to R$48.9 million (-58.2%) in the same periods,

increased the Result from Financial Intermediation from R$4.3 million until September 2011 to R$109.9 million in the nine

months of 2012.

Net Interest Margin

Adjusted net interest margin stood at 6.1%, down 1.6 p.p. from the previous quarter, and only 0.2 p.p. lower than the 6.3%

recorded in 3Q11, especially due to the lower income from securities and the result from derivative financial instruments,

the former due to the cut in the interest rates and reduced average volumes of repos. Additionally, as detailed in the 2Q12,

NIM of that quarter received contribution of higher credit recoveries and extraordinary derivative revenues.

When comparing the nine-month periods of 2012 and 2011, net interest margin grew 1.5 p.p., from 8.8% in 2011 to 10.2%

in 2012, despite the sharp cut in the benchmark interest rate, the higher share of the Corporate segment in the Credit

Portfolio and the pressure to reduce spreads in the periods compared.

Net Interest Margin 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11 9M2012 9M2011 9M12/9M11

A. Result from Financial Interm. before ALL 48.4 59.6 -18.7% 45.0 7.5% 158.8 121.3 31.0%

B. Average Interest bearing Assets 4,106.5 4,193.6 -2.1% 4,042.6 1.6% 4,178.2 3,880.4 7.7%

Adjustment for non-remunerated avg assets 1 (874.3) (1,006.7) -13.2% (1,134.5) -22.9% (992.6) (1,051.2) -5.6%

B.a Adj. Average Interest bearing Assets 3,232.2 3,186.9 1.4% 2,908.1 11.1% 3,185.5 2,829.1 12.6%

Net Interest Margin (NIM) (A/B) 4.8% 5.8% -1.0 p.p. 4.5% 0.3 p.p. 7.7% 6.3% 1.4 p.p.

Adj. Net Interest Margin (NIMa) (Aa/Ba) 6.1% 7.7% -1.6 p.p. 6.3% -0.2 p.p. 10.2% 8.8% 1.5 p.p.1 Repos with equivalent volumes, tenors and rates both in assets and liabilities.

8/18

Efficiency Ratio

Efficiency Ratio 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11 9M2012 9M2011 9M12/9M11

Personnel Expenses 21.4 21.9 -2.3% 17.8 20.7% 66.1 50.3 31.4%

Contributions and Profit-sharing 3.0 2.3 32.1% 1.7 72.5% 7.4 4.9 51.3%

Administrative Expenses 13.0 13.6 -4.3% 12.7 2.8% 39.8 36.2 9.9%

Taxes 2.3 2.3 -3.8% 3.6 -38.1% 8.3 10.1 -18.0%

A- Total Operating Expenses 39.7 40.2 -1.1% 35.8 10.9% 121.6 101.5 19.8%

Gross Income Fin. Interm. (w/o ALL) 48.4 59.6 -18.7% 45.0 7.5% 158.8 121.3 31.0%

Income from Services Rendered 7.7 5.4 42.7% 5.5 40.2% 19.6 13.0 50.4%

Income from Banking Tariffs 0.2 0.2 19.4% 0.2 -6.1% 0.5 0.7 -20.0%

Other Net Operating Income (*) 0.7 1.0 -28.0% 1.3 -44.1% 5.8 1.4 319.5%

B- Total Operating Income 57.0 66.1 -13.8% 52.0 9.6% 184.7 136.3 35.5%

Efficiency Ratio (A/B) 69.7% 60.8% 8.9 p.p. 68.9% 0.8 p.p. 65.8% 74.5% -8.7 p.p.

(*) Net of other Operating Expenses to offset the cost of acquisition and income on sale of commodities in the activity of Serglobal Cereais.

Operating expenses remained virtually stable in 3Q12, mainly due to stricter control of administrative expenses and lower

tax expenses. Nevertheless, the upturn in revenue from services, reflecting the strategy of expanding the product offering,

especially of structured products, was not sufficient to offset the 18.7% drop in the Result from Financial Intermediation.

As a result, Efficiency Ratio decreased by 8.9 p.p. in relation to 2Q12, and remained virtually flat in relation to 3Q11.

Comparing the nine-month periods of 2012 and 2011, the Efficiency Ratio improved by 8.7 p.p., standing at 65.8%.

Considering the seasonality of the operations of Serglobal Cereais (the wholly-owned subsidiary) related to the coffee

harvest, in order to eliminate the effects of the costs of acquisition and revenue from the sale of products received in

physical settlement of the Rural Product Certificates (CPR) processed by the Bank, booked under Other Operating Income

and Expenses in the Consolidated Income Statement, we are now utilizing the net result of these lines to calculate our

efficiency.

Our Efficiency Ratio, despite improving in recent quarters, still falls short of our objectives. However, it will converge

towards its adequate level as we gain scale by increasing our business volume, without compromising on quality, and by a

higher contribution of revenue from services (fees), especially from new products, including structured operations.

Net Profit

The operating income of R$9.5 million in 3Q12, after (i) the non-operating loss from the sale of properties and idle assets,

(ii) taxes and contributions, and (iii) profit sharing, resulted in a net profit of R$3.1 million, up 29.4% in the quarter, mainly

due to the decrease in the allowance for loan losses. Net profit in the first nine months of 2012 amounted to R$10.6

million, versus a loss of R$42.1 million in the same period last year.

9/18

Credit Portfolio

Expanded Credit Portfolio

At the end of September 2012, the Expanded Credit Portfolio totaled R$3.0 billion, up 6.5% in the quarter and 33.0% in 12

months, reflecting the efforts by the sales department, now with fully structured teams and a fresh focus on clients and

products and relying on the support of the Business Development and Monitoring department.

The Expanded Credit Portfolio includes loan and financing operations in Real and Trade Finance operations, detailed in

note 6(a) to the financial statements, as well as: (i) guarantees issued (sureties, guarantees and letters of credit), (ii)

agribusiness bonds originated from the absorption of the operations of Serglobal Cereais (CPR and CDA/WA), which are

booked under Securities as per the Central Bank regulations; and (iii) Private Credit Bonds (promissory notes and

debentures).

Expanded Credit Portfolio by Product Group 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11

Loans & Financing in Real 1,974.4 1,844.4 7.0% 1,627.6 21.3%

Trade Finance (ACC/ACE/IMPFIN) 463.0 449.4 3.0% 433.1 6.9%

Guarantees Issued (LGs & L/Cs) 167.5 175.8 -4.7% 102.8 62.9%

Agro Bonds (Securities: CPRs & CDA/WA; Credit: CDCAs) 306.7 267.0 14.9% 52.4 485.9%

Private Credit Bonds (Securities: PNs & Debentures) 41.1 30.7 34.1% 10.0 311.5%

Other 38.1 39.8 -4.3% 22.3 70.9%

TOTAL 2,990.9 2,807.1 6.5% 2,248.2 33.0%

Loans and financing operations in Real, which include loans, discounted bills, acquisition of client receivables and BNDES

onlendings, represented 66.0% of the Expanded Credit Portfolio. Notable were the increase of 7.9% in the quarter and

16.9% in the year in loan operations, which totaled R$1.6 billion at the end of September 2012, and in BNDES onlending

operations, which totaled R$301.0 million, an increase of 15.4% in the quarter and 66.0% in 12 months.

Trade Finance operations, which accounted for 15.5% of the Expanded Credit Portfolio, include import financing (R$115.3

million) and export financing (ACC/ACE in the amount of R$347.7 million).

The guarantees issued (sureties, guarantees and import letters of credit) represented 5.6% of the Expanded Credit

Portfolio, down 4.7% in the quarter and up 62.9% in the year.

Though agribusiness bonds and private credit bonds represent credit exposure, they are classified under Marketable

Securities in the balance sheet, in accordance with Brazilian Central Bank regulations on account of their negotiability.

These bonds jointly represented 9.2% of the Expanded Credit Portfolio, up 16.7% in the quarter and 446.4% in 12 months.

Our Expanded Credit Portfolio breakdown is as follows:

By Economic Activity By Region By Customer Segment

Commerce

20%

Industry

57%

Financial

Institution

2%

Other

Services

18%

Individuals

3% Southeast

61%

South

16%Midwest

19%

Northeast

3%

North

1%

Corporate

56%

Middle

Market

42%

Other

2%

10/18

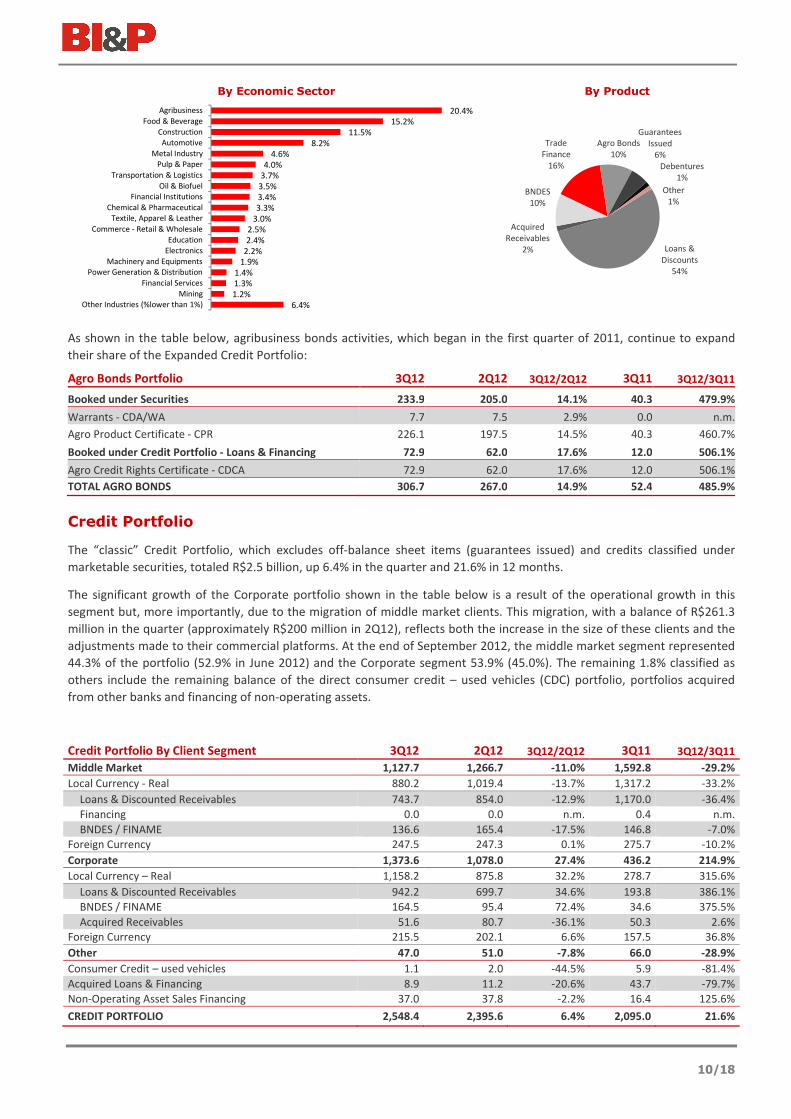

By Economic Sector By Product

As shown in the table below, agribusiness bonds activities, which began in the first quarter of 2011, continue to expand

their share of the Expanded Credit Portfolio:

Agro Bonds Portfolio 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11

Booked under Securities 233.9 205.0 14.1% 40.3 479.9%

Warrants - CDA/WA 7.7 7.5 2.9% 0.0 n.m.

Agro Product Certificate - CPR 226.1 197.5 14.5% 40.3 460.7%

Booked under Credit Portfolio - Loans & Financing 72.9 62.0 17.6% 12.0 506.1%

Agro Credit Rights Certificate - CDCA 72.9 62.0 17.6% 12.0 506.1%

TOTAL AGRO BONDS 306.7 267.0 14.9% 52.4 485.9%

Credit Portfolio

The “classic” Credit Portfolio, which excludes off-balance sheet items (guarantees issued) and credits classified under

marketable securities, totaled R$2.5 billion, up 6.4% in the quarter and 21.6% in 12 months.

The significant growth of the Corporate portfolio shown in the table below is a result of the operational growth in this

segment but, more importantly, due to the migration of middle market clients. This migration, with a balance of R$261.3

million in the quarter (approximately R$200 million in 2Q12), reflects both the increase in the size of these clients and the

adjustments made to their commercial platforms. At the end of September 2012, the middle market segment represented

44.3% of the portfolio (52.9% in June 2012) and the Corporate segment 53.9% (45.0%). The remaining 1.8% classified as

others include the remaining balance of the direct consumer credit – used vehicles (CDC) portfolio, portfolios acquired

from other banks and financing of non-operating assets.

Credit Portfolio By Client Segment 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11

Middle Market 1,127.7 1,266.7 -11.0% 1,592.8 -29.2%

Local Currency - Real 880.2 1,019.4 -13.7% 1,317.2 -33.2%

Loans & Discounted Receivables 743.7 854.0 -12.9% 1,170.0 -36.4%

Financing 0.0 0.0 n.m. 0.4 n.m.

BNDES / FINAME 136.6 165.4 -17.5% 146.8 -7.0%

Foreign Currency 247.5 247.3 0.1% 275.7 -10.2%

Corporate 1,373.6 1,078.0 27.4% 436.2 214.9%

Local Currency – Real 1,158.2 875.8 32.2% 278.7 315.6%

Loans & Discounted Receivables 942.2 699.7 34.6% 193.8 386.1%

BNDES / FINAME 164.5 95.4 72.4% 34.6 375.5%

Acquired Receivables 51.6 80.7 -36.1% 50.3 2.6%

Foreign Currency 215.5 202.1 6.6% 157.5 36.8%

Other 47.0 51.0 -7.8% 66.0 -28.9%

Consumer Credit – used vehicles 1.1 2.0 -44.5% 5.9 -81.4%

Acquired Loans & Financing 8.9 11.2 -20.6% 43.7 -79.7%

Non-Operating Asset Sales Financing 37.0 37.8 -2.2% 16.4 125.6%

CREDIT PORTFOLIO 2,548.4 2,395.6 6.4% 2,095.0 21.6%

6.4%

1.2%

1.3%

1.4%

1.9%

2.2%

2.4%

2.5%

3.0%

3.3%

3.4%

3.5%

3.7%

4.0%

4.6%

8.2%

11.5%

15.2%

20.4%

Other Industries (%lower than 1%)

Mining

Financial Services

Power Generation & Distribution

Machinery and Equipments

Electronics

Education

Commerce - Retail & Wholesale

Textile, Apparel & Leather

Chemical & Pharmaceutical

Financial Institutions

Oil & Biofuel

Transportation & Logistics

Pulp & Paper

Metal Industry

Automotive

Construction

Food & Beverage

Agribusiness

Loans &

Discounts

54%

Acquired

Receivables

2%

BNDES

10%

Trade

Finance

16%

Agro Bonds

10%

Guarantees

Issued

6%

Debentures

1%

Other

1%

11/18

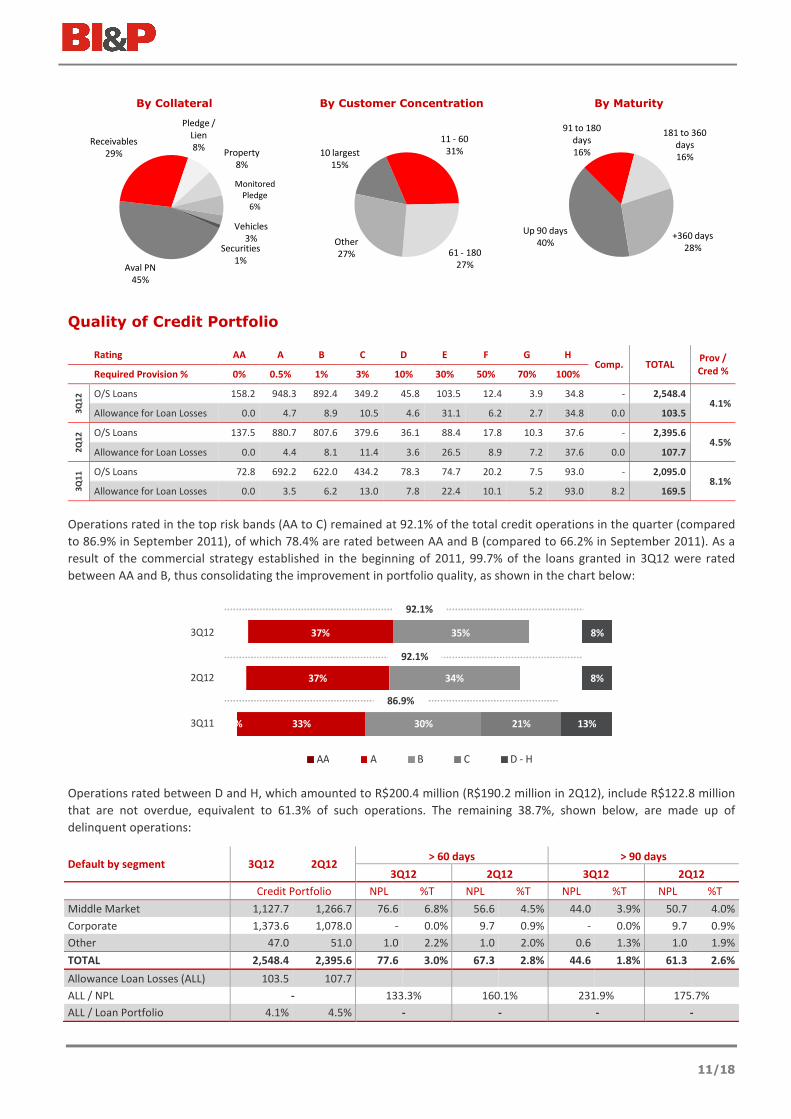

By Collateral By Customer Concentration By Maturity

Quality of Credit Portfolio

Rating AA A B C D E F G H Comp. TOTAL

Prov /

Cred % Required Provision % 0% 0.5% 1% 3% 10% 30% 50% 70% 100%

3Q

12

O/S Loans 158.2 948.3 892.4 349.2 45.8 103.5 12.4 3.9 34.8 - 2,548.4 4.1%

Allowance for Loan Losses 0.0 4.7 8.9 10.5 4.6 31.1 6.2 2.7 34.8 0.0 103.5

2Q

12

O/S Loans 137.5 880.7 807.6 379.6 36.1 88.4 17.8 10.3 37.6 - 2,395.6 4.5%

Allowance for Loan Losses 0.0 4.4 8.1 11.4 3.6 26.5 8.9 7.2 37.6 0.0 107.7

3Q

11

O/S Loans 72.8 692.2 622.0 434.2 78.3 74.7 20.2 7.5 93.0 - 2,095.0 8.1%

Allowance for Loan Losses 0.0 3.5 6.2 13.0 7.8 22.4 10.1 5.2 93.0 8.2 169.5

Operations rated in the top risk bands (AA to C) remained at 92.1% of the total credit operations in the quarter (compared

to 86.9% in September 2011), of which 78.4% are rated between AA and B (compared to 66.2% in September 2011). As a

result of the commercial strategy established in the beginning of 2011, 99.7% of the loans granted in 3Q12 were rated

between AA and B, thus consolidating the improvement in portfolio quality, as shown in the chart below:

Operations rated between D and H, which amounted to R$200.4 million (R$190.2 million in 2Q12), include R$122.8 million

that are not overdue, equivalent to 61.3% of such operations. The remaining 38.7%, shown below, are made up of

delinquent operations:

Default by segment 3Q12 2Q12 > 60 days > 90 days

3Q12 2Q12 3Q12 2Q12

Credit Portfolio NPL %T NPL %T NPL %T NPL %T

Middle Market 1,127.7 1,266.7 76.6 6.8% 56.6 4.5% 44.0 3.9% 50.7 4.0%

Corporate 1,373.6 1,078.0 - 0.0% 9.7 0.9% - 0.0% 9.7 0.9%

Other 47.0 51.0 1.0 2.2% 1.0 2.0% 0.6 1.3% 1.0 1.9%

TOTAL 2,548.4 2,395.6 77.6 3.0% 67.3 2.8% 44.6 1.8% 61.3 2.6%

Allowance Loan Losses (ALL) 103.5 107.7

ALL / NPL - 133.3% 160.1% 231.9% 175.7%

ALL / Loan Portfolio 4.1% 4.5% - - - -

Aval PN

45%

Receivables

29%

Pledge /

Lien

8%Property

8%

Monitored

Pledge

6%

Vehicles

3%Securities

1%

10 largest

15%

11 - 60

31%

61 - 180

27%

Other

27%

Up 90 days

40%

91 to 180

days

16%

181 to 360

days

16%

+360 days

28%

3%

6%

6%

33%

37%

37%

30%

34%

35%

21%

16%

14%

13%

8%

8%

3Q11

2Q12

3Q12

AA A B C D - H

92.1%

92.1%

86.9%

12/18

The default rates on loans overdue by more than 60 days (NPL 60 days) increased slightly in the quarter (0.2 p.p.), as a

result of the middle market portfolio, still reflecting loans granted before 2011. The default rates on loans overdue by more

than 90 days (NPL 90 days) fell by 0.8 p.p. in the quarter. In relation to September 2011, both indicators improved

substantially, by 3.2 p.p. and 2.3 p.p., respectively, for loans overdue by more than 60 and 90 days.

The improvement in these ratios in recent quarters is the result of the strategy, adopted last year, of expanding the credit

portfolio through better quality loans. This evolution is evident from the potential default rate (ratio of installments

overdue between 15 and 60 days to the credit portfolio), which dropped from 1.5% in September 2011 to 0.65% in June

2012 and 0.31% in September 2012. During the quarter, R$16.1 million in loan operations, already fully provisioned in

previous quarters, was written off as losses.

The allowance for loan losses, amounting to R$103.5 million, provides coverage to 133.3% of the loans overdue more than

60 days and 231.9% of the loans overdue more than 90 days.

Once more we highlight the relevance of the restructuring of the commercial area in the last 18 months with the

renovation of teams, multiproduct offering training, and improved customer segmentation in the search for a better credit

quality customer profile also to promote improved cross selling. All these actions are supported by the Business

Development and Monitoring unit and the product areas, both for market intelligence and strategic business monitoring,

as well as with the expertise to detect business opportunities and deliver customer solutions. These areas combined efforts

reflected in the increase of 45% in the accumulated volume of disbursements within 3Q12, in comparison to 2Q12.

Funding

Funding totaled R$2.9 billion, up 6.6% in the quarter and 21.3% in 12 months. It is worth noting that in the past 12 months,

although modestly, the Bank started funding operations by the issuing of bank notes (LF) and real estate letters of credit

(LCI), accompanied by a significant increase in the funding volume through agribusiness letters of credit (LCA), replacing a

part of the funding through CDBs. These new instruments improved the balance in funding costs and made other sources

of funds possible. However, Term Deposits via the issue of Bank Deposit Certificates (CDB) and Term Deposits with Special

Guarantee (DPGE I) still account for the bulk of the funding operations (57.3% in September 2012). Funding through DPGE

represented 34.7% of total funding at the end of September, up 32.0% in the quarter and 37.9% in 12 months. DPGE I

funding increased at the end of the quarter as a strategy to strengthen liquidity in light of the uncertainties in the

international market and the possible resistance from the investor community to the recent events in Brazil’s financial

system. In addition, with the creation of DPGE II, whose availability for operations backed by corporate credit is expected in

the first half of 2013, these funding operations preserve the volume of funds we can raise via DPGE I.

Funding in foreign currency is specially allocated to Trade Finance operations and its balance is impacted by foreign

exchange variations.

Total Funding 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11

Total Deposits 2,194.5 2,038.0 7.7% 1,734.3 26.5%

Time Deposits 664.6 744.9 -10.8% 689.2 -3.6%

Insured Time Deposits (DPGE) 1,019.0 771.9 32.0% 739.0 37.9%

Agro Notes (LCA) 328.8 324.2 1.4% 163.2 101.5%

Bank Notes (LF) 36.4 30.6 18.9% 7.6 378.0%

Real State Notes (LCI) 5.3 0.0 n.m. 0.0 n.m.

Interbank Deposits 92.1 137.0 -32.8% 75.6 21.8%

Demand Deposits and Other 48.3 29.5 63.7% 59.7 -19.0%

Domestic Onlending 309.3 267.8 15.5% 194.8 58.8%

Foreign Borrowings 432.0 449.2 -3.8% 491.2 -12.1%

Trade Finance 381.1 398.6 -4.4% 426.2 -10.6%

Other Foreign Borrowings 50.8 50.5 0.6% 65.0 -21.8%

TOTAL 2,935.8 2,755.0 6.6% 2,420.4 21.3%

13/18

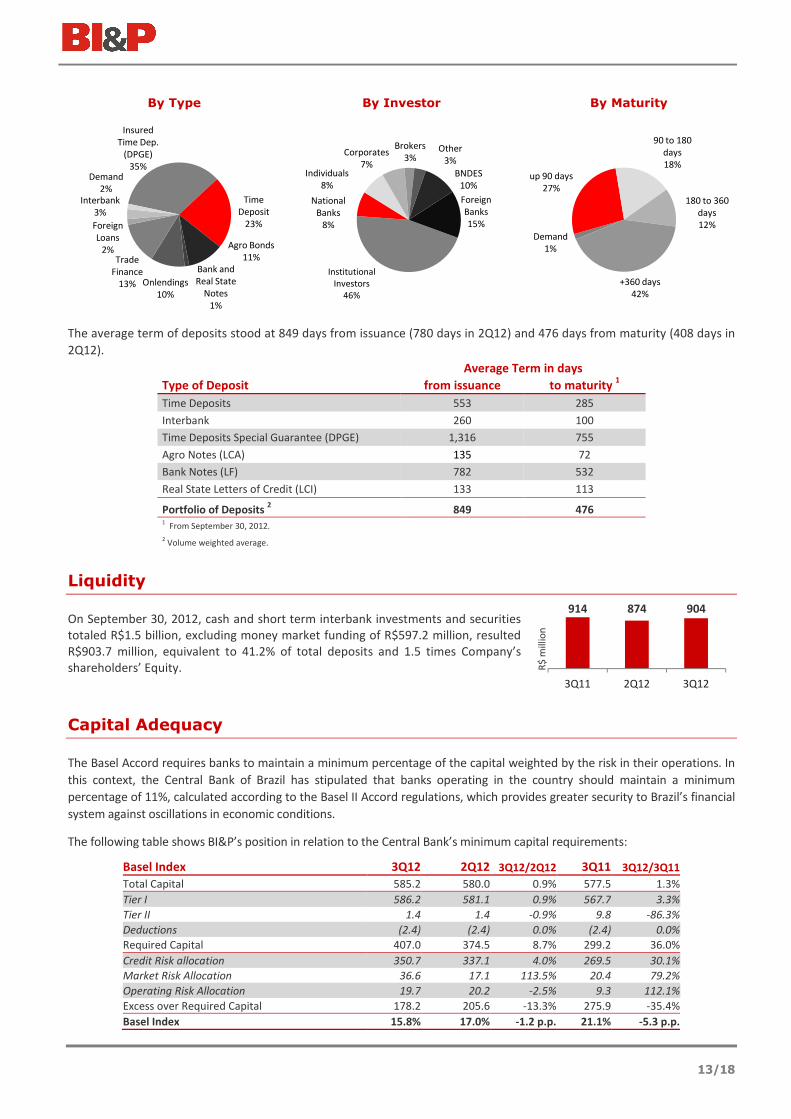

By Type By Investor By Maturity

The average term of deposits stood at 849 days from issuance (780 days in 2Q12) and 476 days from maturity (408 days in

2Q12).

Average Term in days

Type of Deposit from issuance to maturity 1

Time Deposits 553 285

Interbank 260 100

Time Deposits Special Guarantee (DPGE) 1,316 755

Agro Notes (LCA) 135 72

Bank Notes (LF) 782 532

Real State Letters of Credit (LCI) 133 113

Portfolio of Deposits 2 849 476

1 From September 30, 2012.

2 Volume weighted average.

Liquidity

On September 30, 2012, cash and short term interbank investments and securities

totaled R$1.5 billion, excluding money market funding of R$597.2 million, resulted

R$903.7 million, equivalent to 41.2% of total deposits and 1.5 times Company’s

shareholders’ Equity.

Capital Adequacy

The Basel Accord requires banks to maintain a minimum percentage of the capital weighted by the risk in their operations. In

this context, the Central Bank of Brazil has stipulated that banks operating in the country should maintain a minimum

percentage of 11%, calculated according to the Basel II Accord regulations, which provides greater security to Brazil’s financial

system against oscillations in economic conditions.

The following table shows BI&P’s position in relation to the Central Bank’s minimum capital requirements:

Basel Index 3Q12 2Q12 3Q12/2Q12 3Q11 3Q12/3Q11

Total Capital 585.2 580.0 0.9% 577.5 1.3%

Tier I 586.2 581.1 0.9% 567.7 3.3%

Tier II 1.4 1.4 -0.9% 9.8 -86.3%

Deductions (2.4) (2.4) 0.0% (2.4) 0.0%

Required Capital 407.0 374.5 8.7% 299.2 36.0%

Credit Risk allocation 350.7 337.1 4.0% 269.5 30.1%

Market Risk Allocation 36.6 17.1 113.5% 20.4 79.2%

Operating Risk Allocation 19.7 20.2 -2.5% 9.3 112.1%

Excess over Required Capital 178.2 205.6 -13.3% 275.9 -35.4%

Basel Index 15.8% 17.0% -1.2 p.p. 21.1% -5.3 p.p.

Insured

Time Dep.

(DPGE)

35%

Time

Deposit

23%

Agro Bonds

11%

Bank and

Real State

Notes

1%

Onlendings

10%

Trade

Finance

13%

Foreign

Loans

2%

Interbank

3%

Demand

2%

Institutional

Investors

46%

National

Banks

8%

Individuals

8%

Corporates

7%

Brokers

3%Other

3%

BNDES

10%

Foreign

Banks

15%

Demand

1%

up 90 days

27%

90 to 180

days

18%

180 to 360

days

12%

+360 days

42%

914 874 904

3Q11 2Q12 3Q12

R$

mill

ion

14/18

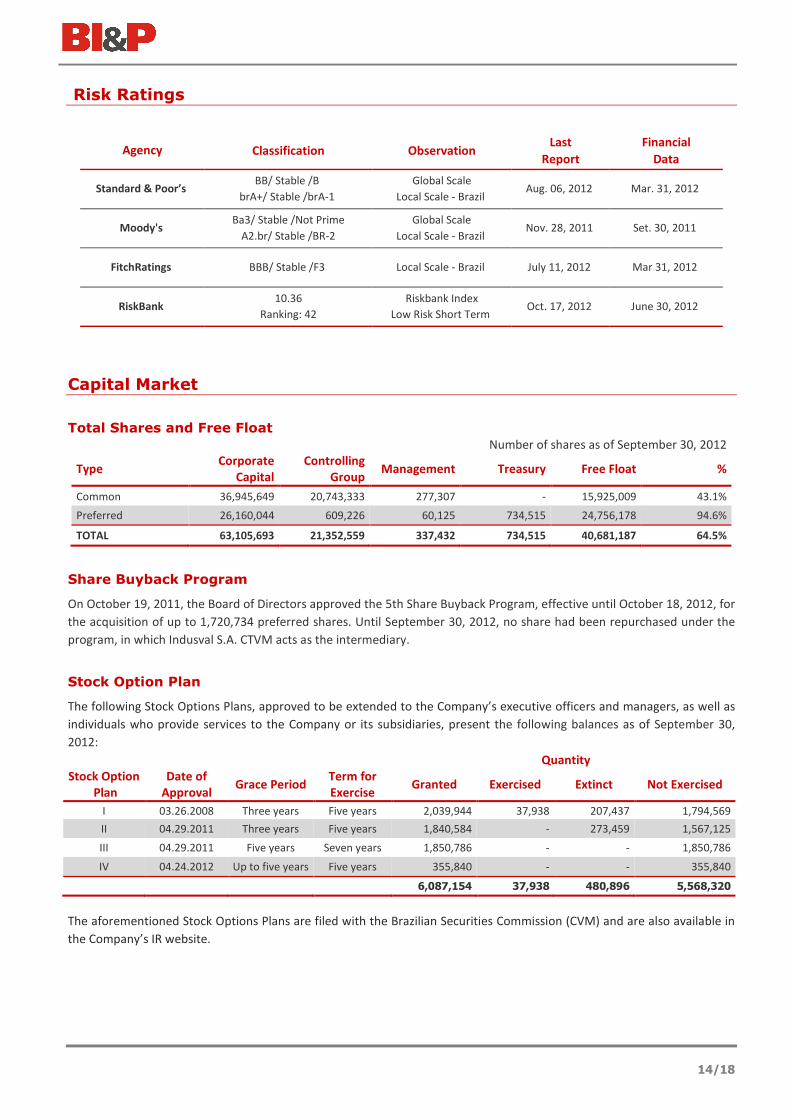

Risk Ratings

Agency Classification Observation Last

Report

Financial

Data

Standard & Poor’s BB/ Stable /B

brA+/ Stable /brA-1

Global Scale

Local Scale - Brazil Aug. 06, 2012 Mar. 31, 2012

Moody's Ba3/ Stable /Not Prime

A2.br/ Stable /BR-2

Global Scale

Local Scale - Brazil Nov. 28, 2011 Set. 30, 2011

FitchRatings BBB/ Stable /F3 Local Scale - Brazil July 11, 2012 Mar 31, 2012

RiskBank 10.36

Ranking: 42

Riskbank Index

Low Risk Short Term Oct. 17, 2012 June 30, 2012

Capital Market

Total Shares and Free Float

Number of shares as of September 30, 2012

Type Corporate

Capital

Controlling

Group Management Treasury Free Float %

Common 36,945,649 20,743,333 277,307 - 15,925,009 43.1%

Preferred 26,160,044 609,226 60,125 734,515 24,756,178 94.6%

TOTAL 63,105,693 21,352,559 337,432 734,515 40,681,187 64.5%

Share Buyback Program

On October 19, 2011, the Board of Directors approved the 5th Share Buyback Program, effective until October 18, 2012, for

the acquisition of up to 1,720,734 preferred shares. Until September 30, 2012, no share had been repurchased under the

program, in which Indusval S.A. CTVM acts as the intermediary.

Stock Option Plan

The following Stock Options Plans, approved to be extended to the Company’s executive officers and managers, as well as

individuals who provide services to the Company or its subsidiaries, present the following balances as of September 30,

2012:

Quantity

Stock Option

Plan

Date of

Approval Grace Period

Term for

Exercise Granted Exercised Extinct Not Exercised

I 03.26.2008 Three years Five years 2,039,944 37,938 207,437 1,794,569

II 04.29.2011 Three years Five years 1,840,584 - 273,459 1,567,125

III 04.29.2011 Five years Seven years 1,850,786 - - 1,850,786

IV 04.24.2012 Up to five years Five years 355,840 - - 355,840

6,087,154 37,938 480,896 5,568,320

The aforementioned Stock Options Plans are filed with the Brazilian Securities Commission (CVM) and are also available in

the Company’s IR website.

15/18

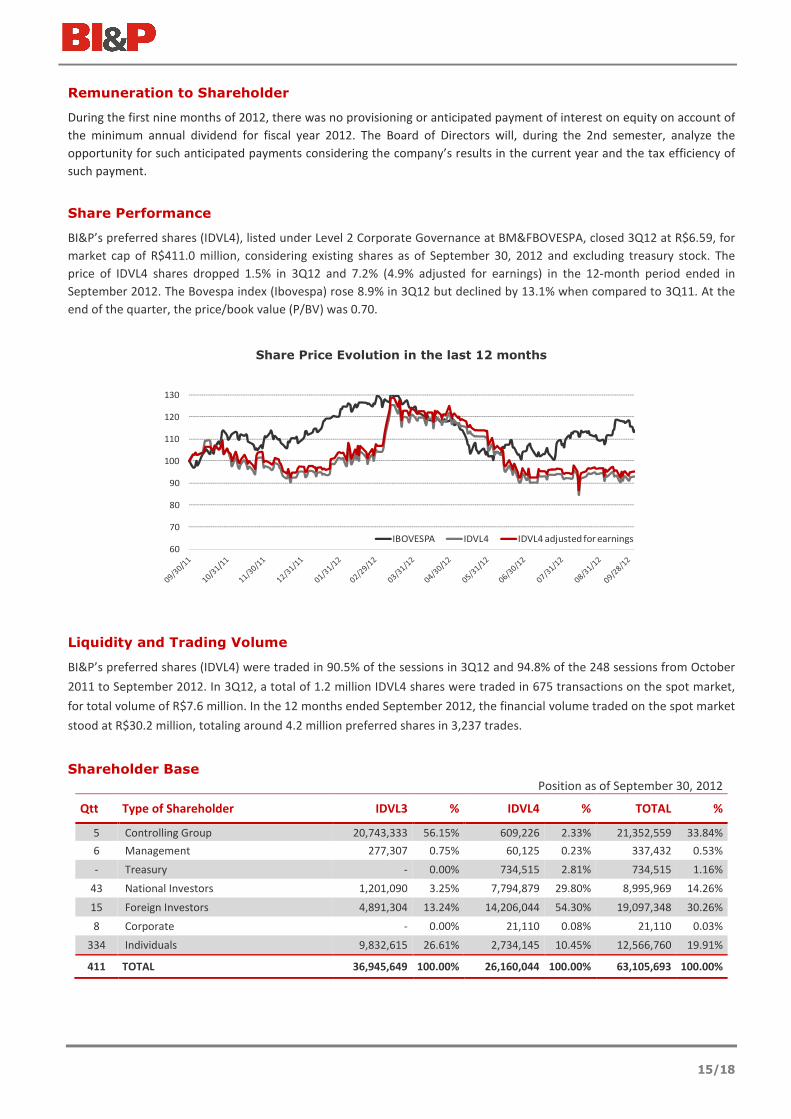

Remuneration to Shareholder

During the first nine months of 2012, there was no provisioning or anticipated payment of interest on equity on account of

the minimum annual dividend for fiscal year 2012. The Board of Directors will, during the 2nd semester, analyze the

opportunity for such anticipated payments considering the company’s results in the current year and the tax efficiency of

such payment.

Share Performance

BI&P’s preferred shares (IDVL4), listed under Level 2 Corporate Governance at BM&FBOVESPA, closed 3Q12 at R$6.59, for

market cap of R$411.0 million, considering existing shares as of September 30, 2012 and excluding treasury stock. The

price of IDVL4 shares dropped 1.5% in 3Q12 and 7.2% (4.9% adjusted for earnings) in the 12-month period ended in

September 2012. The Bovespa index (Ibovespa) rose 8.9% in 3Q12 but declined by 13.1% when compared to 3Q11. At the

end of the quarter, the price/book value (P/BV) was 0.70.

Share Price Evolution in the last 12 months

Liquidity and Trading Volume

BI&P’s preferred shares (IDVL4) were traded in 90.5% of the sessions in 3Q12 and 94.8% of the 248 sessions from October

2011 to September 2012. In 3Q12, a total of 1.2 million IDVL4 shares were traded in 675 transactions on the spot market,

for total volume of R$7.6 million. In the 12 months ended September 2012, the financial volume traded on the spot market

stood at R$30.2 million, totaling around 4.2 million preferred shares in 3,237 trades.

Shareholder Base

Position as of September 30, 2012

Qtt Type of Shareholder IDVL3 % IDVL4 % TOTAL %

5 Controlling Group 20,743,333 56.15% 609,226 2.33% 21,352,559 33.84%

6 Management 277,307 0.75% 60,125 0.23% 337,432 0.53%

- Treasury - 0.00% 734,515 2.81% 734,515 1.16%

43 National Investors 1,201,090 3.25% 7,794,879 29.80% 8,995,969 14.26%

15 Foreign Investors 4,891,304 13.24% 14,206,044 54.30% 19,097,348 30.26%

8 Corporate - 0.00% 21,110 0.08% 21,110 0.03%

334 Individuals 9,832,615 26.61% 2,734,145 10.45% 12,566,760 19.91%

411 TOTAL 36,945,649 100.00% 26,160,044 100.00% 63,105,693 100.00%

60

70

80

90

100

110

120

130

IBOVESPA IDVL4 IDVL4 adjusted for earnings

16/18

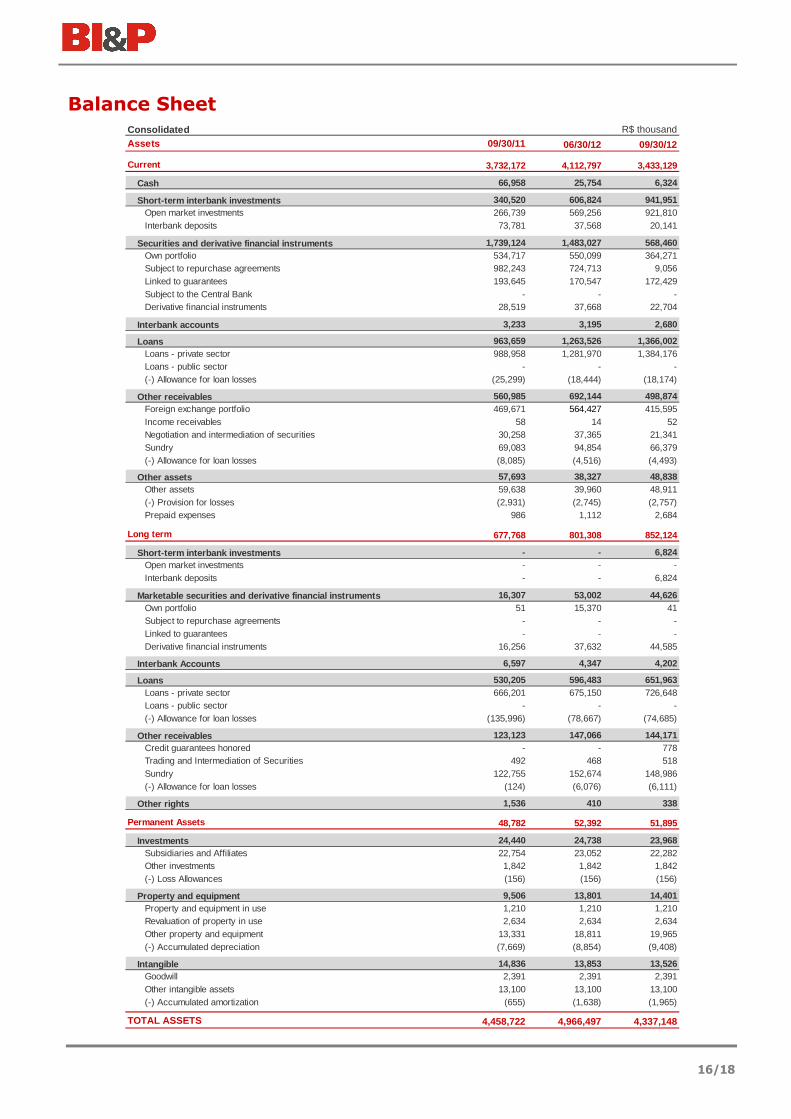

Balance Sheet

Consolidated R$ thousand

Assets 09/30/11 06/30/12 09/30/12

Current 3,732,172 4,112,797 3,433,129

Cash 66,958 25,754 6,324

Short-term interbank investments 340,520 606,824 941,951 Open market investments 266,739 569,256 921,810 Interbank deposits 73,781 37,568 20,141

Securities and derivative financial instruments 1,739,124 1,483,027 568,460 Own portfolio 534,717 550,099 364,271 Subject to repurchase agreements 982,243 724,713 9,056 Linked to guarantees 193,645 170,547 172,429 Subject to the Central Bank - - - Derivative financial instruments 28,519 37,668 22,704

Interbank accounts 3,233 3,195 2,680

Loans 963,659 1,263,526 1,366,002 Loans - private sector 988,958 1,281,970 1,384,176 Loans - public sector - - - (-) Allowance for loan losses (25,299) (18,444) (18,174)

Other receivables 560,985 692,144 498,874 Foreign exchange portfolio 469,671 564,427 415,595 Income receivables 58 14 52 Negotiation and intermediation of securities 30,258 37,365 21,341 Sundry 69,083 94,854 66,379 (-) Allowance for loan losses (8,085) (4,516) (4,493)

Other assets 57,693 38,327 48,838 Other assets 59,638 39,960 48,911 (-) Provision for losses (2,931) (2,745) (2,757)Prepaid expenses 986 1,112 2,684

Long term 677,768 801,308 852,124

Short-term interbank investments - - 6,824 Open market investments - - - Interbank deposits - - 6,824

Marketable securities and derivative financial inst ruments 16,307 53,002 44,626 Own portfolio 51 15,370 41 Subject to repurchase agreements - - - Linked to guarantees - - - Derivative financial instruments 16,256 37,632 44,585

Interbank Accounts 6,597 4,347 4,202

Loans 530,205 596,483 651,963 Loans - private sector 666,201 675,150 726,648 Loans - public sector - - - (-) Allowance for loan losses (135,996) (78,667) (74,685)

Other receivables 123,123 147,066 144,171 Credit guarantees honored - - 778 Trading and Intermediation of Securities 492 468 518 Sundry 122,755 152,674 148,986 (-) Allowance for loan losses (124) (6,076) (6,111)

Other rights 1,536 410 338

Permanent Assets 48,782 52,392 51,895

Investments 24,440 24,738 23,968 Subsidiaries and Affiliates 22,754 23,052 22,282 Other investments 1,842 1,842 1,842 (-) Loss Allowances (156) (156) (156)

Property and equipment 9,506 13,801 14,401 Property and equipment in use 1,210 1,210 1,210 Revaluation of property in use 2,634 2,634 2,634 Other property and equipment 13,331 18,811 19,965 (-) Accumulated depreciation (7,669) (8,854) (9,408)

Intangible 14,836 13,853 13,526 Goodwill 2,391 2,391 2,391 Other intangible assets 13,100 13,100 13,100 (-) Accumulated amortization (655) (1,638) (1,965)

TOTAL ASSETS 4,458,722 4,966,497 4,337,148

17/18

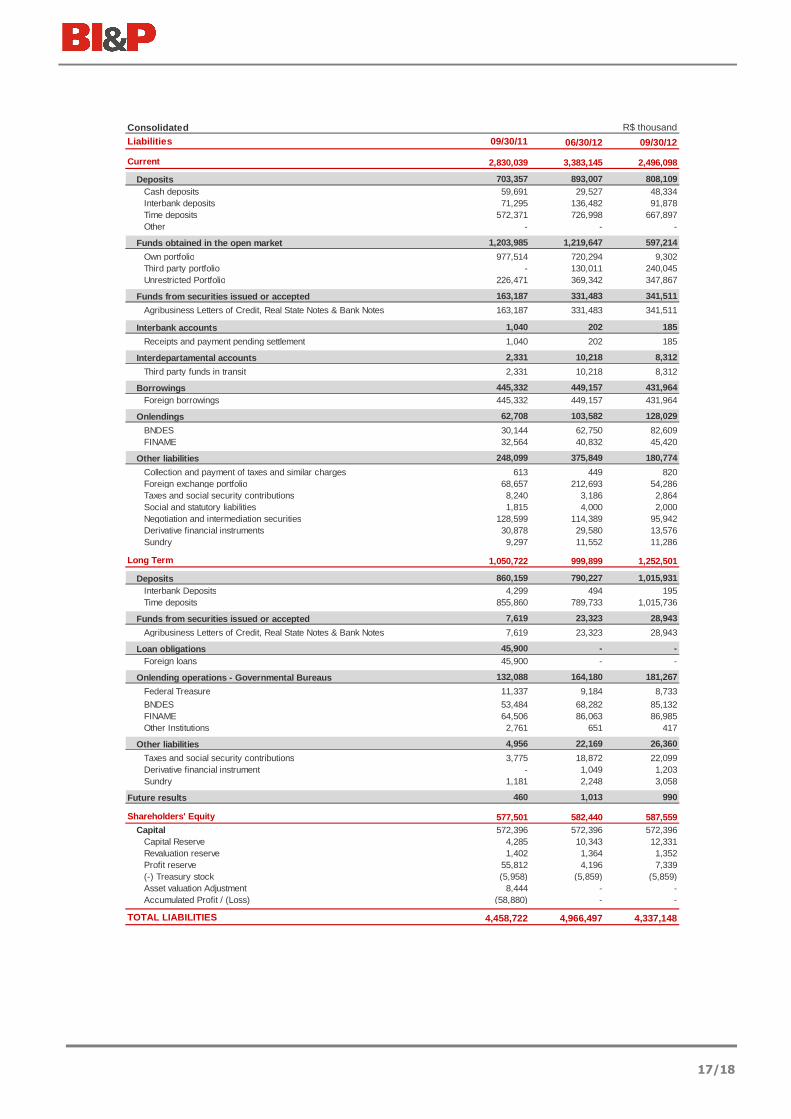

Consolidated R$ thousand

Liabilities 09/30/11 06/30/12 09/30/12

Current 2,830,039 3,383,145 2,496,098

Deposits 703,357 893,007 808,109 Cash deposits 59,691 29,527 48,334 Interbank deposits 71,295 136,482 91,878 Time deposits 572,371 726,998 667,897 Other - - -

Funds obtained in the open market 1,203,985 1,219,647 597,214

Own portfolio 977,514 720,294 9,302 Third party portfolio - 130,011 240,045 Unrestricted Portfolio 226,471 369,342 347,867

Funds from securities issued or accepted 163,187 331,483 341,511

Agribusiness Letters of Credit, Real State Notes & Bank Notes 163,187 331,483 341,511

Interbank accounts 1,040 202 185

Receipts and payment pending settlement 1,040 202 185

Interdepartamental accounts 2,331 10,218 8,312

Third party funds in transit 2,331 10,218 8,312

Borrowings 445,332 449,157 431,964 Foreign borrowings 445,332 449,157 431,964

Onlendings 62,708 103,582 128,029

BNDES 30,144 62,750 82,609 FINAME 32,564 40,832 45,420

Other liabilities 248,099 375,849 180,774

Collection and payment of taxes and similar charges 613 449 820 Foreign exchange portfolio 68,657 212,693 54,286 Taxes and social security contributions 8,240 3,186 2,864 Social and statutory liabilities 1,815 4,000 2,000 Negotiation and intermediation securities 128,599 114,389 95,942 Derivative financial instruments 30,878 29,580 13,576 Sundry 9,297 11,552 11,286

Long Term 1,050,722 999,899 1,252,501

Deposits 860,159 790,227 1,015,931 Interbank Deposits 4,299 494 195 Time deposits 855,860 789,733 1,015,736

Funds from securities issued or accepted 7,619 23,323 28,943

Agribusiness Letters of Credit, Real State Notes & Bank Notes 7,619 23,323 28,943

Loan obligations 45,900 - - Foreign loans 45,900 - -

Onlending operations - Governmental Bureaus 132,088 164,180 181,267

Federal Treasure 11,337 9,184 8,733

BNDES 53,484 68,282 85,132 FINAME 64,506 86,063 86,985 Other Institutions 2,761 651 417

Other liabilities 4,956 22,169 26,360

Taxes and social security contributions 3,775 18,872 22,099 Derivative financial instrument - 1,049 1,203 Sundry 1,181 2,248 3,058

Future results 460 1,013 990

Shareholders' Equity 577,501 582,440 587,559 Capital 572,396 572,396 572,396

Capital Reserve 4,285 10,343 12,331 Revaluation reserve 1,402 1,364 1,352 Profit reserve 55,812 4,196 7,339 (-) Treasury stock (5,958) (5,859) (5,859)Asset valuation Adjustment 8,444 - - Accumulated Profit / (Loss) (58,880) - -

TOTAL LIABILITIES 4,458,722 4,966,497 4,337,148

18/18

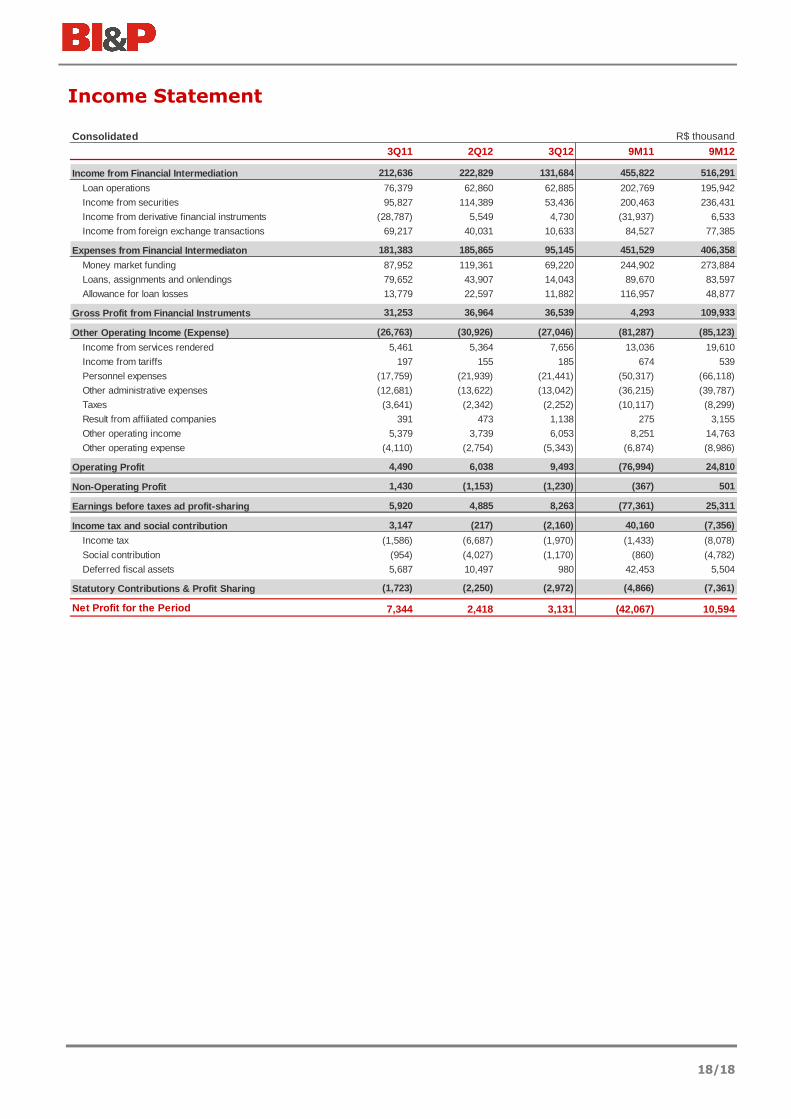

Income Statement

Consolidated R$ thousand

3Q11 2Q12 3Q12 9M11 9M12

Income from Financial Intermediation 212,636 222,829 131,684 455,822 516,291

Loan operations 76,379 62,860 62,885 202,769 195,942

Income from securities 95,827 114,389 53,436 200,463 236,431

Income from derivative financial instruments (28,787) 5,549 4,730 (31,937) 6,533

Income from foreign exchange transactions 69,217 40,031 10,633 84,527 77,385

Expenses from Financial Intermediaton 181,383 185,865 95,145 451,529 406,358

Money market funding 87,952 119,361 69,220 244,902 273,884

Loans, assignments and onlendings 79,652 43,907 14,043 89,670 83,597

Allowance for loan losses 13,779 22,597 11,882 116,957 48,877

Gross Profit from Financial Instruments 31,253 36,964 36,539 4,293 109,933

Other Operating Income (Expense) (26,763) (30,926) (27,046) (81,287) (85,123)

Income from services rendered 5,461 5,364 7,656 13,036 19,610

Income from tariffs 197 155 185 674 539

Personnel expenses (17,759) (21,939) (21,441) (50,317) (66,118)

Other administrative expenses (12,681) (13,622) (13,042) (36,215) (39,787)

Taxes (3,641) (2,342) (2,252) (10,117) (8,299)

Result from affiliated companies 391 473 1,138 275 3,155

Other operating income 5,379 3,739 6,053 8,251 14,763

Other operating expense (4,110) (2,754) (5,343) (6,874) (8,986)

Operating Profit 4,490 6,038 9,493 (76,994) 24,810

Non-Operating Profit 1,430 (1,153) (1,230) (367) 501

Earnings before taxes ad profit-sharing 5,920 4,885 8,263 (77,361) 25,311

Income tax and social contribution 3,147 (217) (2,160) 40,160 (7,356)

Income tax (1,586) (6,687) (1,970) (1,433) (8,078)

Social contribution (954) (4,027) (1,170) (860) (4,782)

Deferred fiscal assets 5,687 10,497 980 42,453 5,504

Statutory Contributions & Profit Sharing (1,723) (2,250) (2,972) (4,866) (7,361)

Net Profit for the Period 7,344 2,418 3,131 (42,067) 10,594