Embed Size (px)

Citation preview

1

Earnings Release | Conference Call – 1Q14

May 14th, 2014

2

Agenda

Ricardo Ribeiro

Vice President

Carlos Wollenweber

CFO | IR Officer

Operational Highlights

Financial Highlights

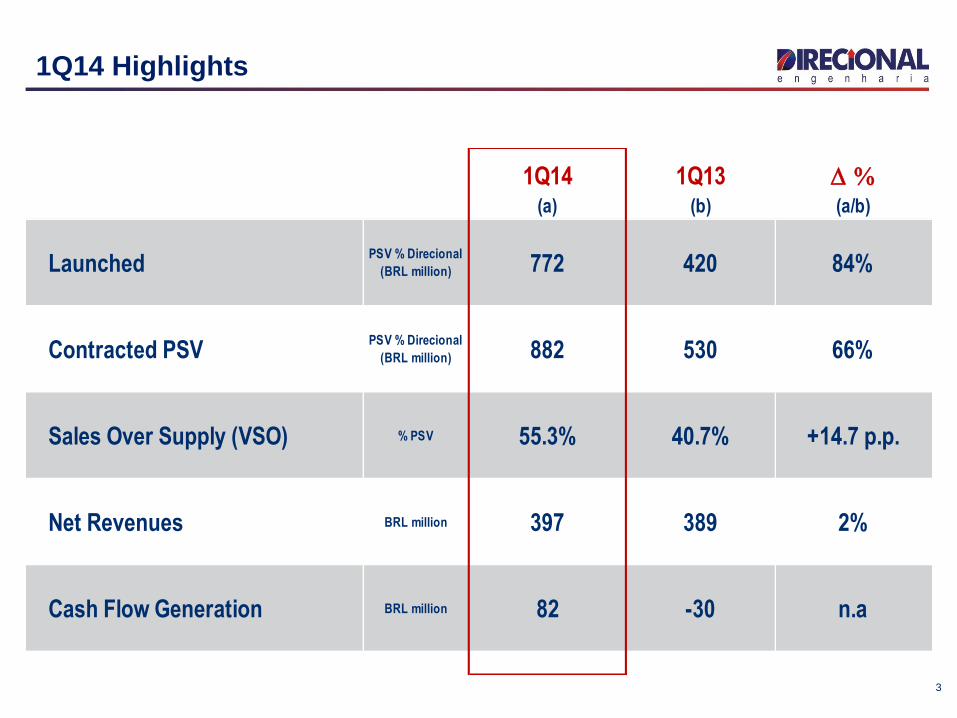

1Q14 1Q13 D %(a) (b) (a/b)

Launched PSV % Direcional

(BRL million) 772 420 84%

Contracted PSVPSV % Direcional

(BRL million) 882 530 66%

Sales Over Supply (VSO) % PSV 55.3% 40.7% +14.7 p.p.

Net Revenues BRL million 397 389 2%

Cash Flow Generation BRL million 82 -30 n.a

3

1Q14 Highlights

MG

RS

681,595PSV (R$'000)

Units

Granja Werneck

8,896

89,909PSV (R$'000)

Units

Irmãos Maristas

1,300

4

Launches - 1Q14

1Q14

88%

12%

1Q13

13%

87%

Launches by Region - MCMV Level 1

(% PSV)

South Southeast North

We launched two projects under the PMCMV Level 1 in 1Q14, the PSV totaled R$ 772 million

772

1Q13

+84%

1Q14

420

405

15

Launched PSV

(R$ million)

MCMV Level 1

Development

5

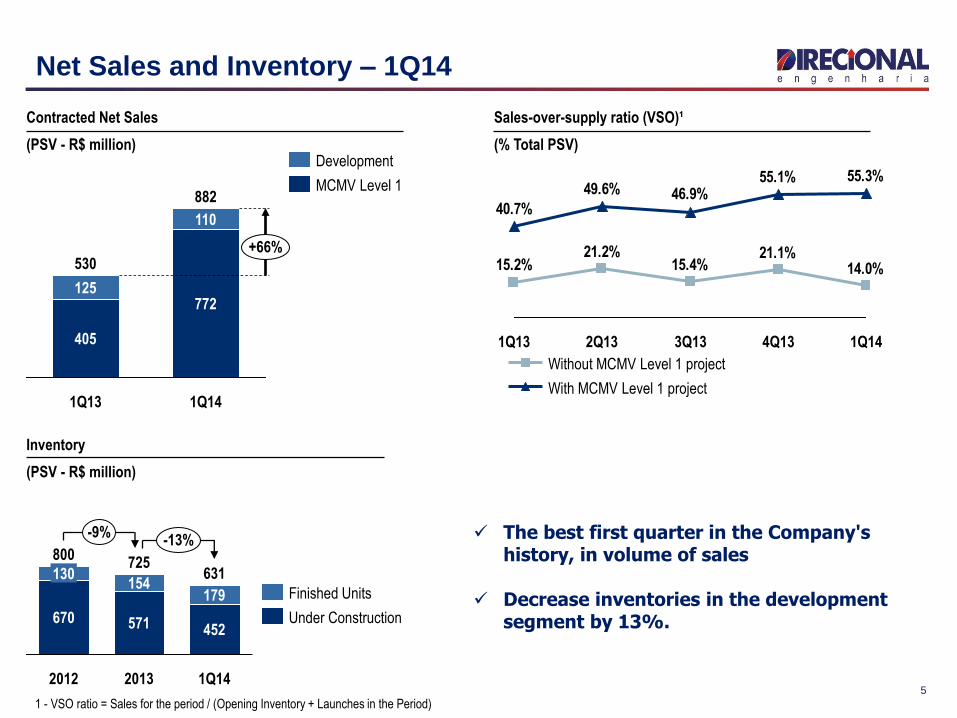

Net Sales and Inventory – 1Q14

-13% -9%

1Q14

631

452

179

2013

725

571

154

2012

800

670

130

Under Construction

Finished Units

Inventory

(PSV - R$ million)

882

+66%

1Q14

772

110

1Q13

530

405

125

Contracted Net Sales

(PSV - R$ million)

MCMV Level 1

Development

14.0%21.1%

15.4%21.2%

15.2%

55.3%55.1%46.9%49.6%

40.7%

1Q14 4Q13 3Q13 2Q13 1Q13

With MCMV Level 1 project

Without MCMV Level 1 project

Sales-over-supply ratio (VSO)¹

(% Total PSV)

1 - VSO ratio = Sales for the period / (Opening Inventory + Launches in the Period)

The best first quarter in the Company's history, in volume of sales

Decrease inventories in the development segment by 13%.

6

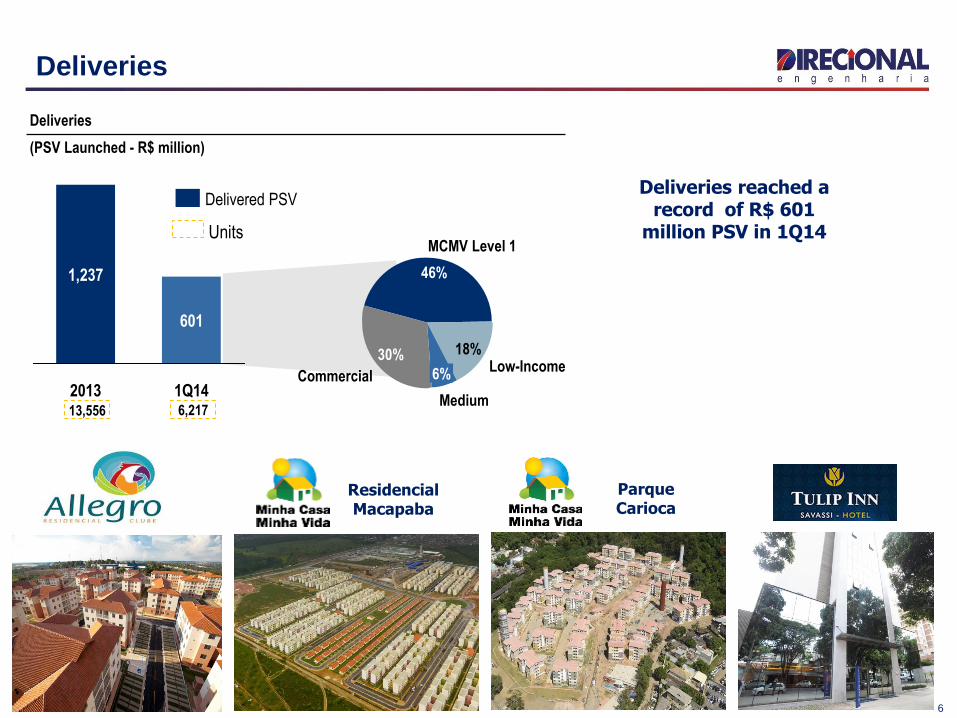

Deliveries

Deliveries

(PSV Launched - R$ million)

Units

6,217 13,556

1Q14

601

2013

1,237

Delivered PSV

30%

Commercial

18%

MCMV Level 1

46%

Medium

6% Low-Income

Residencial Macapaba

Parque Carioca

Deliveries reached a record of R$ 601

million PSV in 1Q14

7

Carlos Wollenweber

CFO | IR Officer

Financial Highlights

8

Results to be recognized

Service

78%

Development

22%

Service

87%

Development

13%

Breakdown of Results to be Recognized

(% Total – 1Q14)

1Q14 1Q13

+13%

4,214

+61%

1Q14

3,660

555

4Q13

3,746

3,160

586

1Q13

2,620

2,035

585

Level 1

Development

Revenues to be Recognized

(R$ million)

9

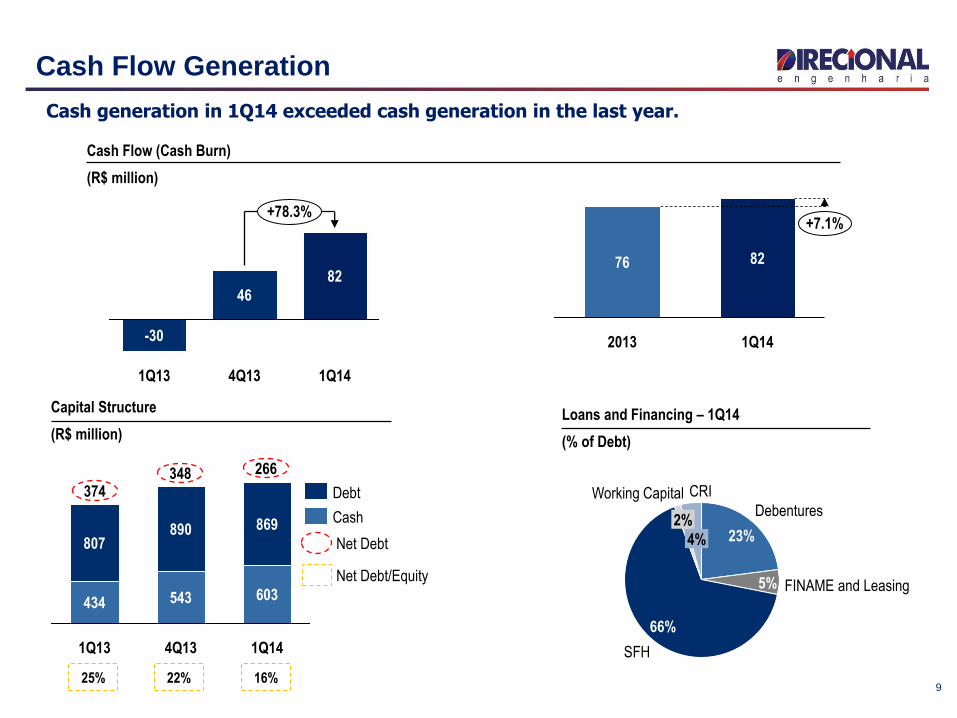

Cash Flow Generation

+7.1%

1Q14

82

2013

76

Cash Flow (Cash Burn)

(R$ million)

Capital Structure

(R$ million)

1Q14

603

869

4Q13

543

890

1Q13

434

807

Cash

Debt 374

Net Debt

25% 22% 16%

Net Debt/Equity

348 266

CRI

4%

Working Capital

2%

SFH

66%

FINAME and Leasing 5%

Debentures

23%

Loans and Financing – 1Q14

(% of Debt)

+78.3%

1Q14

82

4Q13

46

1Q13

-30

Cash generation in 1Q14 exceeded cash generation in the last year.

10

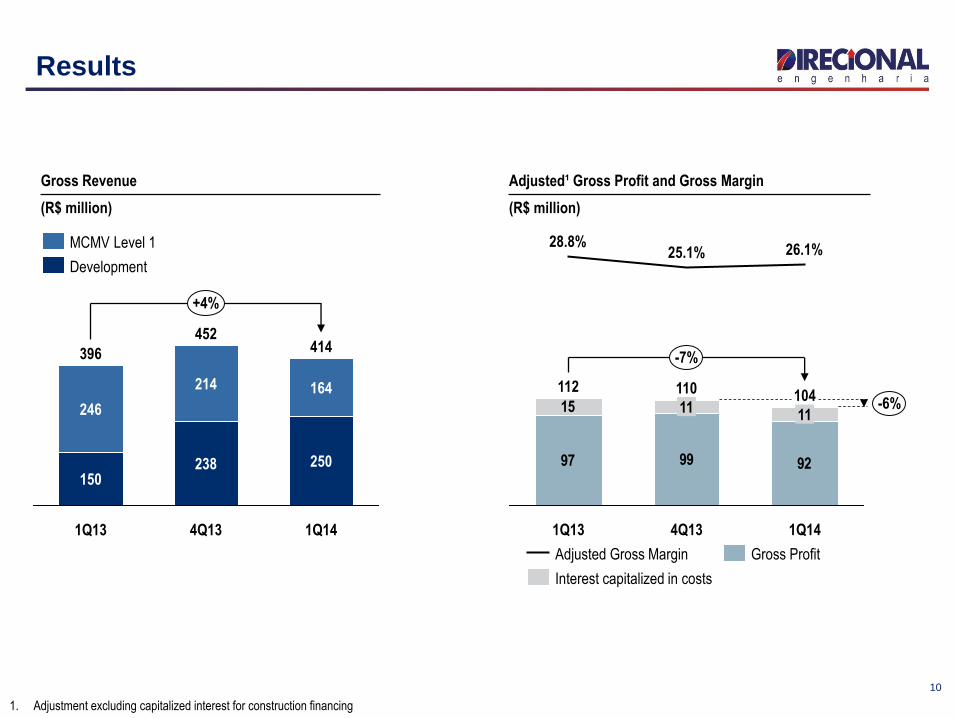

Results

Gross Revenue

(R$ million)

+4%

1Q14

414

250

164

4Q13

452

238

214

1Q13

396

150

246

Development

MCMV Level 1

1. Adjustment excluding capitalized interest for construction financing

Adjusted¹ Gross Profit and Gross Margin

(R$ million)

97 99 92

15104

-6%

-7%

1Q14

11

26.1%

4Q13

110

11

25.1%

1Q13

112

28.8%

Gross Profit

Interest capitalized in costs

Adjusted Gross Margin

11 11

Results

G&A

(R$ million)

+15%

1Q14

30

7.5%

4Q13

26

5.9%

1Q13

26

6.6%

% Net revenue

Selling Expenses

(R$ million)

14

3.3%

1Q13

6

1.6%

-27%

1Q14

11

2.7%

4Q13

% Net revenue

Net Income

(R$ million)

-8%

1Q14

46

11.7%

4Q13

50

11.5%

1Q13

55

14.1%

Net Margin

12

Disclosure and Contacts

This presentation contains certain forward-looking statements concerning the business prospects, projections of

operating and financial results and growth potential of the Company, which are based on management’s current

expectations and estimates of the future performance of the Company. Although the Company believes such

forward-looking statements are based on reasonable assumptions, it can give no assurance that its expectations

will be achieved. Expectations and estimates that are based on the future prospects of the Company are highly

dependent upon market behavior, Brazil’s political and economic situation, existing and future regulations of the

industry and international markets and, therefore, are subject to changes outside the Company’s and

management’s control. The Company undertakes no obligation to update any information contained herein or to

revise any forward-looking statement as a result of new information, future events or other information.

www.direcional.com.b/ir

(55 31) 3214-6200

(55 31) 3214-6450

Carlos Wollenweber

CFO | IR Officer

Paulo Sousa

IR Coordinator

Luiz Felipe Almeida

IR Analist

![1Q14 RESULTS PRESENTATION - NOS · 1Q14 RESULTS PRESENTATION Monthly Bill per Unique Corporate, SME and SoHo subscribers [Euros] 0 ä 200 ä 1Q13 2Q13 3Q13 4Q13 1Q14 Monthly Bill](https://img.dokumen.tips/doc/110x75/5f4bf904fbd0f2207a556b26/1q14-results-presentation-nos-1q14-results-presentation-monthly-bill-per-unique.jpg)