Embed Size (px)

DESCRIPTION

Market analysis of emerging healthcare technology products.

Citation preview

Healthcare Technology Emerging Market

DevelopmentBioTech For Wall Street Bros: A Series of White

Papers

Market Participation

• Health IT Integration Market

• Healthcare Information Exchange Market

• Healthcare Analytics

• Remote Patient Monitoring

• Chronic Disease Management

• TeleHealth Services

Health IT Integration Marketplace Summary

• Healthcare IT integration involves the implementation of a wide variety of electronic platforms that help in maintaining information about health and healthcare in general, which could be both for individuals as well as a group of patients. HCIT integration includes collection, storage, retrieval, and sharing of information between consumers, providers, governments, and insurers, among others. The information covered by HCIT can range from demographics, medical history, medications and allergies, and immunization status to radiology images and vital signs of the patient.

• The healthcare IT integration market is influenced by an increasing need for integration in continually expanding hospitals and other healthcare organizations, which demands healthcare IT integration tools for building the interfaces between various departments/systems. As the adoption of electronic medical records grows, so does the importance of integrating increasingly complex data sets. The increasing healthcare costs, the increase in the aging population in most of the developed countries across Europe and North America, strong government support and initiatives, growing need to integrate healthcare systems, and high returns on investment are factors that further drive the market for healthcare IT integration across the globe. However, interoperability issues, the high cost of installation of healthcare IT integration solutions, and a fragmented end-users market are factors that limit the growth of this market to a certain extent.

• North America commanded the largest share of 69.4% in the global market, with U.S. commanding the largest share of around 86.6% in 2013. This large share of the U.S. can be attributed to the fact that the U.S. is a well-established market for healthcare IT and HCIT integration. However, this market still has many opportunities within the U.S mainly due to the various initiatives taken by the government to promote HCIT. In addition, the presence of a large number of major hospitals in the country that demand an integrated healthcare network is another factor that is driving the market.

• The prominent players in the market are InterSystems (U.S.), Corepoint (U.S.), Siemens (Germany), Orion Health (New Zealand), Infor (U.S.), Interfaceware (Canada), Enovacom (France), Cerner Corporation (U.S.), Capsule (U.S.), Accenture (Ireland), Capgemini (France), IBM Corporation (U.S.), Allscripts (U.S.), Oracle (U.S.), and AVI-SPL (U.S.).

Market Participation: Health IT Integration

• The healthcare service provider industry has a plethora of information in the form of patient records, medical images, patient bills, prescriptions, insurance claims, and research data. Healthcare providers and healthcare organizations are not only required to store data but are also required to process and maintain this data using various data management and processing solutions. The healthcare providers are also required to make this data available on demand and across boundaries, and at the same time to focus on their core function of delivery of patient care.

• Generally, hospitals and other healthcare providers have various systems for different aspects of services they provide, which are often unable to communicate with each other. In such cases, Healthcare IT (HCIT) integration is recognized as one of the most effective tools for providing a framework for the exchange, integration, sharing, and retrieval of electronic health information with advanced security. Thus, driven by information needs, technologies from healthcare IT integration market are increasingly being adopted by healthcare organizations to mobilize the healthcare information across or within the organization. This also helps healthcare organizations to enhance the quality of care provided.

• This report analyzes the global healthcare IT integration market based on products (integration/interface engines, device integration software, media integration solutions, and other integration tools), services (implementation, support and maintenance, and training), applications (hospitals, laboratories, radiology centers, clinics, device integration, HIE, and others), and geography (North America, Europe, Asia, and the Rest of the World).

• The market is expected to grow at a CAGR of 9.6% in the forecast period, to reach $2,745.9 million by 2018 from $1,737.3 million in 2013. Factors such as the rising healthcare costs, presence of strong government support and initiatives, growing need to integrate healthcare systems, and high returns on investment have increased the demand for healthcare IT integration. However, various interoperability issues, presence of a fragmented end-users market, and the high cost of implementation of healthcare IT integration are the factors that are restraining the growth of this market to a certain extent.

• North America accounted for the largest share of 65% to 70% of the global Healthcare IT integration market, followed by Europe with a share of nearly 20%. However, the Asian countries represent the fastest-growing markets. The high growth in these countries can be attributed to the increasing awareness regarding healthcare, growth in healthcare spending in emerging countries, and the presence of a large and diverse population in this region.

• The prominent players in the market are InterSystems (U.S.), Corepoint Health (U.S.), Siemens AG (Germany), Orion Health (New Zealand), Infor (U.S.), Interfaceware (Canada), Enovacom (France), Cerner Corporation (U.S.), Capsule (U.S.), Accenture (Ireland), Capgemini (France), IBM Corporation (U.S.), Allscripts (U.S.), Oracle (U.S.), and AVI-SPL (U.S.).

Healthcare Analytics/Medical Analytics Market

• The global healthcare analytics market is segmented based on products, applications, components, delivery modes, end users, and geography. On the basis of product type, the market is divided into descriptive, predictive, and prescriptive analytics. The healthcare analytics market, by component, is divided into hardware, software, and services. Based on the mode of delivery, the market is classified into on-premise models, web-hosted models, and cloud-based models. Based on end users, the market is segmented into healthcare and others. The healthcare segment is further divided into payers, providers, Health Information Exchanges (HIEs), and others. Based on geography, the market is classified into the U.S., Europe, Asia, and the Rest of the world (RoW).

• The market shows a double-digit growth rate due to supportive elements such as digitization of world commerce, the emergence of Big Data, and also due to the increase in the number of advanced technologies. Factors such as federal healthcare mandates, growing healthcare IT adoption across the globe, growing fields of predictive and prescriptive analytics, and venture capital investments are driving the market. However, factors such as data security issues, patient data confidentiality, cultural barriers to IT adoption, and lack of manpower with cross-functional analytical skills may hinder the growth of this market.

• The U.S. healthcare analytics market is a well-established yet lucrative market. The European market is the second-largest market, growing at a lower rate mainly due to the economic crisis and lack of government initiatives for analytics. The Asian market is relatively new to medical analytics; however, the increasing HCIT adoption, IT skills, and outsourcing trend will drive this market.

• The market is a highly fragmented market with some major players such as IBM Corporation (U.S.), Oracle Corporation (U.S.), Truven Health Analytics, Inc. (U.S.), Verisk Health, Inc. (U.S.), Optum, Inc. (U.S.), MedeAnalytics, Inc. (U.S.), McKesson Corporation (U.S.), SAS Institute, Inc. (U.S.), LexisNexis Risk Solutions (U.S.), Inovalon, Inc. (U.S.), Predixion Software (U.S.), iHealth Analytics, Inc. (U.S.), Predilytics (U.S.), and Cerner Corporation (U.S.), among others.

Healthcare Analytics Market Details

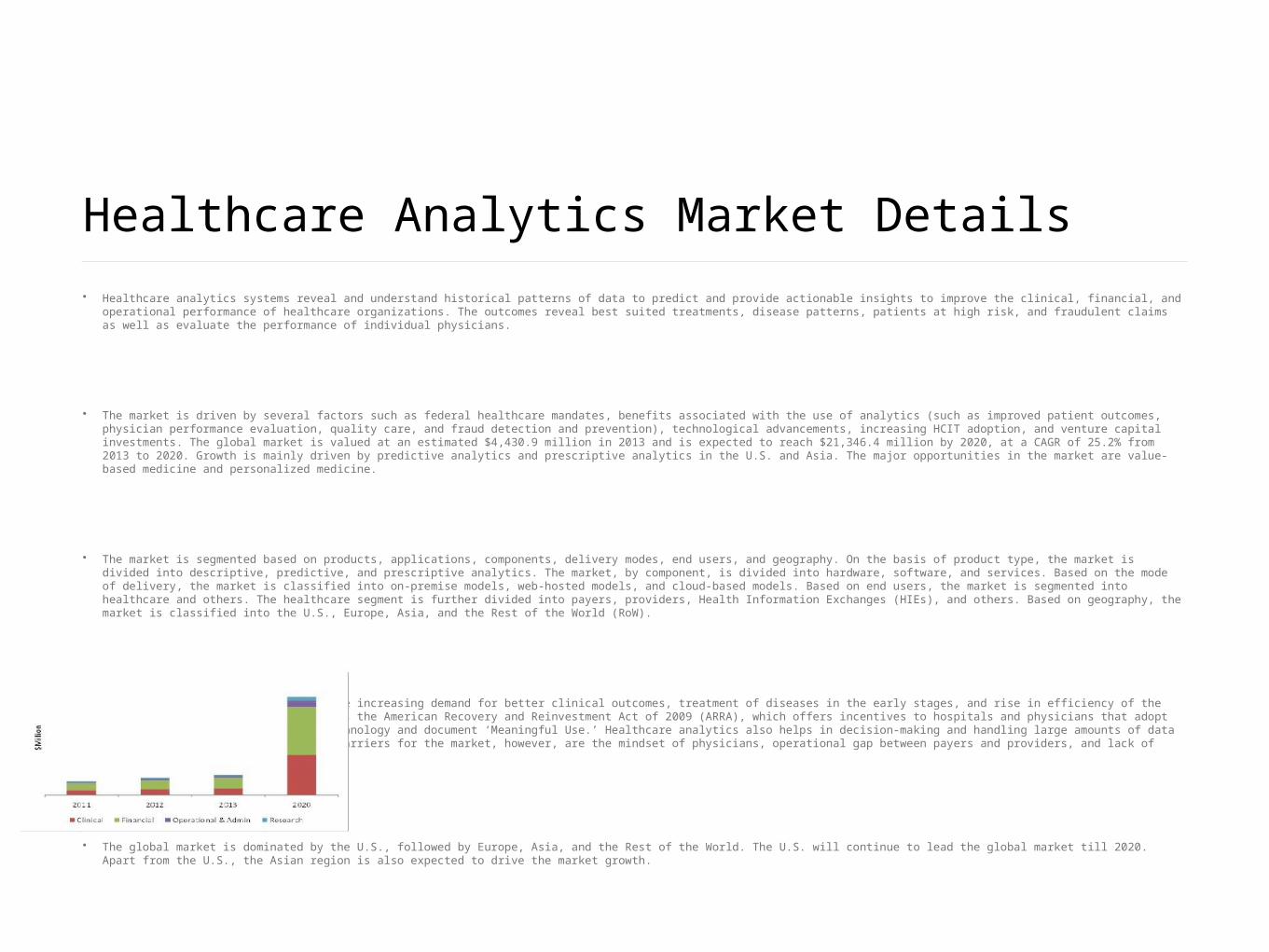

• Healthcare analytics systems reveal and understand historical patterns of data to predict and provide actionable insights to improve the clinical, financial, and operational performance of healthcare organizations. The outcomes reveal best suited treatments, disease patterns, patients at high risk, and fraudulent claims as well as evaluate the performance of individual physicians.

• The market is driven by several factors such as federal healthcare mandates, benefits associated with the use of analytics (such as improved patient outcomes, physician performance evaluation, quality care, and fraud detection and prevention), technological advancements, increasing HCIT adoption, and venture capital investments. The global market is valued at an estimated $4,430.9 million in 2013 and is expected to reach $21,346.4 million by 2020, at a CAGR of 25.2% from 2013 to 2020. Growth is mainly driven by predictive analytics and prescriptive analytics in the U.S. and Asia. The major opportunities in the market are value-based medicine and personalized medicine.

• The market is segmented based on products, applications, components, delivery modes, end users, and geography. On the basis of product type, the market is divided into descriptive, predictive, and prescriptive analytics. The market, by component, is divided into hardware, software, and services. Based on the mode of delivery, the market is classified into on-premise models, web-hosted models, and cloud-based models. Based on end users, the market is segmented into healthcare and others. The healthcare segment is further divided into payers, providers, Health Information Exchanges (HIEs), and others. Based on geography, the market is classified into the U.S., Europe, Asia, and the Rest of the World (RoW).

• The global market is propelled by the increasing demand for better clinical outcomes, treatment of diseases in the early stages, and rise in efficiency of the healthcare process. A major driver is the American Recovery and Reinvestment Act of 2009 (ARRA), which offers incentives to hospitals and physicians that adopt electronic health records (EHRs) technology and document ‘Meaningful Use.’ Healthcare analytics also helps in decision-making and handling large amounts of data generated in healthcare. The major barriers for the market, however, are the mindset of physicians, operational gap between payers and providers, and lack of trained IT staff in healthcare.

• The global market is dominated by the U.S., followed by Europe, Asia, and the Rest of the World. The U.S. will continue to lead the global market till 2020. Apart from the U.S., the Asian region is also expected to drive the market growth.

• Healthcare analytics is a highly fragmented market with some major players such as IBM Corporation (U.S.), Oracle Corporation (U.S.), Truven Health Analytics, Inc. (U.S.), Verisk Health, Inc. (U.S.), Optum, Inc. (U.S.), MedeAnalytics, Inc. (U.S.), McKesson Corporation (U.S.), SAS Institute, Inc. (U.S.), LexisNexis Risk Solutions (U.S.), Inovalon, Inc. (U.S.), Predixion Software (U.S.), iHealth Analytics, Inc. (U.S.), Predilytics (U.S.), and Cerner Corporation (U.S.), among others.

HIE Market Summary

• The Health Information Exchange market is expected to grow at a strong CAGR during the study period. This is due to factors such as incentives by the U.S. federal government, improvements in patient care and safety, and reduction in healthcare costs. However, factors such as high implementation costs, slow returns on investment, and interoperability issues are hampering the growth of this market.

• The Health Information Exchange systems market is mainly categorized by set-up type, vendor, implementation model, and application. Based on the type of set-up, the market is further segmented into public and private HIEs. Depending on the type of vendor, the market is classified into portal-centric, messaging-centric, platform-centric, and others. Based on implementation models, the market is categorized into centralized, decentralized, hybrid, switch, and patient-managed models. The applications considered for Healthcare Information Exchange systems are classified into interfacing internal applications, workflow management, secure messaging, web portal development, patient safety, and others.

• The web portal development segment commanded the largest share of the global Health Information Exchange applications market. It is expected to grow at a strong CAGR during the study period. The large share and high growth of this segment can be attributed to the increasing number of physicians opting for electronic medical records driven by the convenience of web-based portals to retrieve information on patients.

• North America dominated the market, accounting for a share of more than 80%. The leading market share of the North American region can be attributed to the presence of a large number of major manufacturers, such as AT&T, CareEvolution, Cerner Corporation, IBM Corporation, Intersystems, Medicity, and Oracle in this region. Additionally, the rising adoption of HIE and EHR technologies driven by the incentive programs introduced by the federal government are favorable factors driving the market growth.

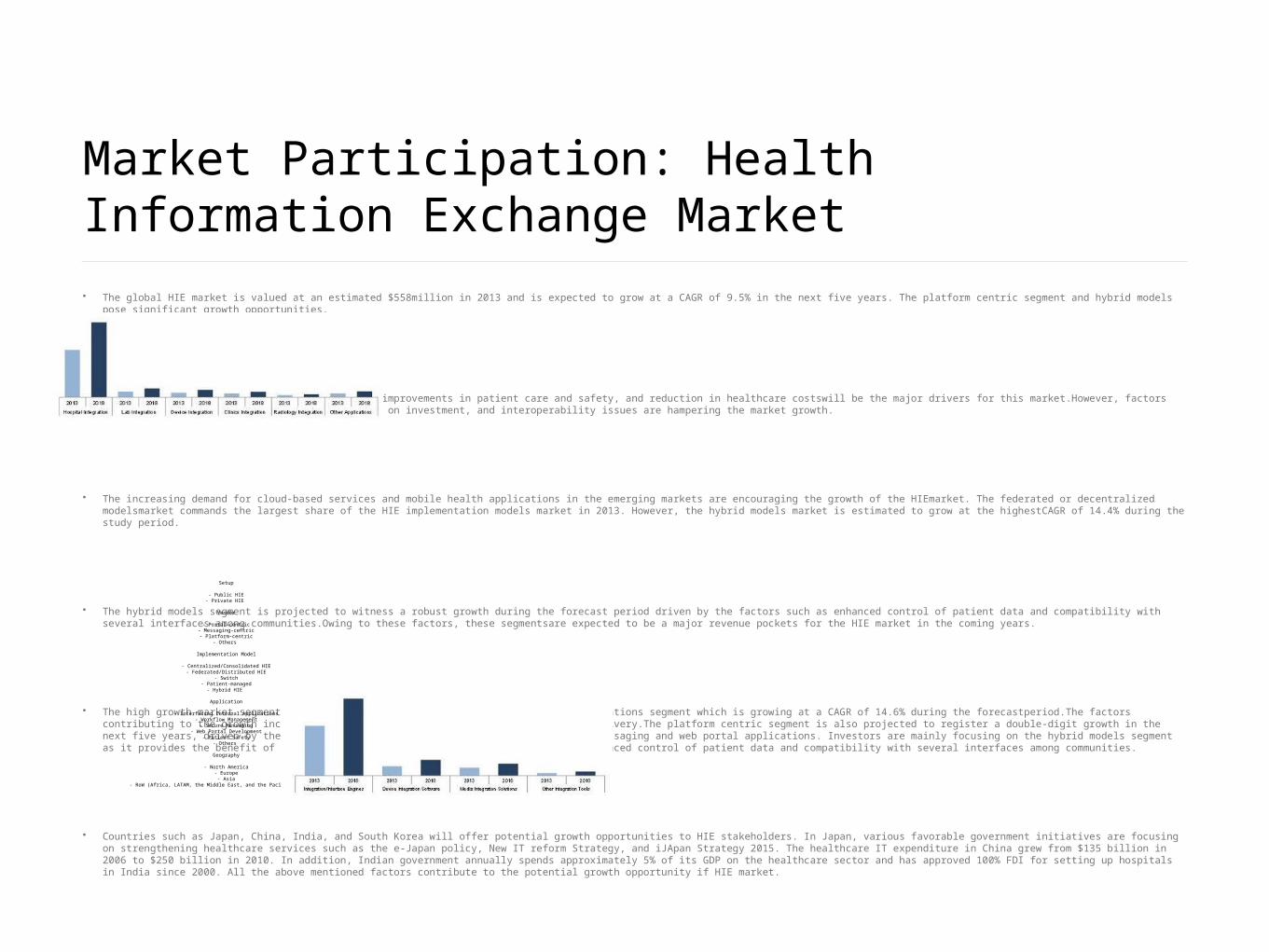

Market Participation: Health Information Exchange Market• The global HIE market is valued at an estimated $558million in 2013 and is expected to grow at a CAGR of 9.5% in the next five years. The platform centric segment and hybrid models pose significant growth

opportunities.

• The incentives by the U.S. federal government, improvements in patient care and safety, and reduction in healthcare costswill be the major drivers for this market.However, factors such as high implementation costs, slow returns on investment, and interoperability issues are hampering the market growth.

• The increasing demand for cloud-based services and mobile health applications in the emerging markets are encouraging the growth of the HIEmarket. The federated or decentralized modelsmarket commands the largest share of the HIE implementation models market in 2013. However, the hybrid models market is estimated to grow at the highestCAGR of 14.4% during the study period.

• The hybrid models segment is projected to witness a robust growth during the forecast period driven by the factors such as enhanced control of patient data and compatibility with several interfaces among communities.Owing to these factors, these segmentsare expected to be a major revenue pockets for the HIE market in the coming years.

• The high growth market segments in the HIE market include interfacing internal applications segment which is growing at a CAGR of 14.6% during the forecastperiod.The factors contributing to the growth include reliability and flexibility of healthcare data delivery.The platform centric segment is also projected to register a double-digit growth in the next five years, driven by the enhanced adoption rates due to rise in the clinical messaging and web portal applications. Investors are mainly focusing on the hybrid models segment as it provides the benefit of both federated and centralized models and helps in enhanced control of patient data and compatibility with several interfaces among communities.

• Countries such as Japan, China, India, and South Korea will offer potential growth opportunities to HIE stakeholders. In Japan, various favorable government initiatives are focusing on strengthening healthcare services such as the e-Japan policy, New IT reform Strategy, and iJApan Strategy 2015. The healthcare IT expenditure in China grew from $135 billion in 2006 to $250 billion in 2010. In addition, Indian government annually spends approximately 5% of its GDP on the healthcare sector and has approved 100% FDI for setting up hospitals in India since 2000. All the above mentioned factors contribute to the potential growth opportunity if HIE market.

• The grey area while estimating the market size is the cost of the HIE installations as most of the EHR vendors offer the HIE platformas a courtesy,which increased the difficulty level in estimating the market revenue gained through the installations.

• - Public HIE

• - Private HIE

• Vendor

• - Portal-centric

• - Messaging-centric

• - Platform-centric

• - Others

• Implementation Model

• - Centralized/Consolidated HIE

• - Federated/Distributed HIE

• - Switch

• - Patient-managed

• - Hybrid HIE

• Application

• - Interfacing Internal Applications

• - Workflow Management

• - Secure Messaging

• - Web Portal Development

• - Patient Safety

• - Others

• Geography

• - North America

• - Europe

• - Asia

• - RoW (Africa, LATAM, the Middle East, and the Pacific countries)

Setup

- Public HIE- Private HIE

Vendor

- Portal-centric- Messaging-centric- Platform-centric

- Others

Implementation Model

- Centralized/Consolidated HIE- Federated/Distributed HIE

- Switch- Patient-managed

- Hybrid HIE

Application

- Interfacing Internal Applications- Workflow Management

- Secure Messaging- Web Portal Development

- Patient Safety- Others

Geography

- North America- Europe

- Asia- RoW (Africa, LATAM, the Middle East, and the Pacific countries)

Market Participation: TeleHealth Services

• The Telehealth Services industry uses digital technology to deliver medical services and health education by connecting multiple users in different locations. Telehealth services include diagnosis, treatment, assessment, monitoring, communication and education. The industry includes a wide range of information, networking and digital imaging technologies, delivered primarily in three ways: videoconferencing, which provides real-time patient-provider consultations and provider-to-provider discussions; remote patient monitoring, in which electronic devices transmit patient health information to healthcare providers; and store-and-forward technologies, which transmit digital images, such as X rays, computerized tomography (CT) scans and video clips between primary care providers and medical specialists. “Technology serves as the backbone of this industry, and therefore, advancements in medical technology and telecommunications will drive industry performance,” says IBISWorld Industry Analyst Stephen Morea.

• The Telehealth Services industry is rapidly expanding. Advances in communication technology and medical technology, such as wearable self-monitoring devices and digitized medical scans, have propelled the industry forward. Furthermore, industry growth has been supported by a healthcare system suffering from skyrocketing costs, a looming doctor shortage and an aging population susceptible to chronic disease. As a result, industry revenue is expected to increase by an annualized 30.7% to $320.2 million in the five years to 2014, including revenue growth of 23.1% in 2014.

• “Over the next five years, the industry will continue to benefit from the demographic and structural factors affecting the healthcare industry as telehealth will emerge as a cost-effective solution to meeting the medical needs of an expanding and aging population,” says Morea. In addition, existing legislation, such as the Affordable Care Act, and pending legislation will increase federal support for telehealth services, benefiting patients, healthcare providers and industry operators. Last, future innovations will likely increase the scope and availability of telehealth services.

• The Telehealth Services industry has a low level of market share concentration. Barriers to entry in this industry are moderate and potential entrants may have difficulty sourcing talent for product and software development. Additionally, this industry has a moderate degree of patent protection and new companies must develop telehealth services systems that are not in violation of existing patents. Nevertheless, this developing industry is rapidly expanding, with the number of industry enterprises expected to increase in the five years to 2019.

North American Healthcare Cloud Computing Market

• The North American Healthcare Cloud Computing Market is segmented on the basis of applications, deployment mode, services, pricing model, components, end users, and geography. The applications market includes clinical and non-clinical information systems applicable for the healthcare providers and payers industry. The clinical information systems are further classified into EMR, PACS, CPOE, RIS, LIS, PIS, and Others. The non-clinical information systems include revenue cycle management, automatic patient billing, payroll, claims management, cost accounting, and others.

• The market by deployment model is segmented into private, public, and hybrid clouds. The services market in cloud computing comprises software-as-a-service (SaaS), infrastructure-as-a-service (IaaS), and platform-as-a-service (PaaS). The pricing model market consists of the two majorly adopted models, namely, Pay-As-You-Go and Spot Pricing. The cloud computing market by components includes software, hardware, and services. The North American Healthcare Cloud Computing market by end-users is broadly categorized into healthcare payers and providers. Based on geography, the market is divided into the U.S. and Canada.

• A number of factors such as the legislative reform of the Patient Protection and Affordable Care Act (PPACA), the requirement to demonstrate meaningful use, ICD 10 transition, federal mandates for providing insurance for every U.S. citizen, and proliferation of new payment models are driving the growth of this market. Moreover, the benefits provided by cloud computing such as cost reduction, positive returns on investment, improved accessibility and mobility, improvements in storage technology, and greater flexibility and scalability of data are resulting in the rising deployment of healthcare applications on cloud. However, security concerns over patient data and reduced control over applications and data are the major factors hindering the growth of this market.

• The major players in the North American Healthcare Cloud Computing Market include athenahealth, Inc., CareCloud Corporation, Carestream Health, Inc., ClearData Networks, Inc., Cisco Systems, Inc., Dell, Inc., EMC Corporation, Global Net Access (GNAX) Health, Hewlett-Packard Company, IBM Corporation, Iron Mountain, Inc., Merge Healthcare, Inc., Microsoft Corporation, Oracle Corporation, and VMware, Inc.

NA Healthcare Cloud Computing • Cloud computing is increasingly being adopted by healthcare providers and payers in North America. This report studies the North American healthcare cloud computing market over the forecast period of 2013 to

2018. This market was valued at $1.7 billion in 2013 and is expected to grow at a CAGR of 29.8% from 2013 to 2018, to reach $6.5 billion by 2018.

• The healthcare cloud computing market is categorized into five broad segments, namely, applications, deployment modes, services, pricing models, components, end users, and geography. The healthcare cloud computing market, by application, comprises clinical and non-clinical information systems applicable for the healthcare providers and payers industry. The clinical information system segment accounted for the largest share of the North American cloud computing market in 2013. Clinical information systems are further classified into EMR, PACS, CPOE, RIS, LIS, PIS, and Others. The non-clinical information systems are segmented into revenue cycle management, automatic patient billing, payroll, claims management, cost accounting, and others.

• The market by deployment model includes private, public, and hybrid clouds. In 2013, the private cloud segment accounted for the largest share of the cloud computing market, by deployment. The services market in cloud computing is divided into software-as-a-service (SaaS), infrastructure-as-a-service (IaaS), and platform-as-a-service (PaaS). The pricing model market comprises the two majorly adopted models, namely, Pay-As-You-Go and Spot Pricing; the Pay-As-You-Go model accounted for the largest share of this market in 2013. The cloud computing market, by components, includes software, hardware, and services. The software segment accounted for the largest share of the North American healthcare cloud computing market, by component, in 2013. The North American healthcare cloud computing market by end-users is broadly categorized into healthcare payers and providers. Based on geography, the market is divided into the U.S. and Canada.

• The adoption of the cloud technology enables the healthcare industry to reduced costs. Furthermore, this technology provides positive returns on investment. These are the key factors that are expected to drive the growth of this market. Furthermore, legislative reforms of the patient protection and affordable care act, improvements in storage technology, proliferation of new payment models, and greater flexibility and scalability of data have stimulated the use of cloud computing in the healthcare industry. The primary factors that are restraining the growth of this market include security and privacy concerns over the medical and patient data.

• The U.S. market dominated the North American Healthcare Cloud Computing market in the forecast period. The U.S. has been a pioneer in terms of developing and adopting the cloud technology. Even though EMR systems with a computerized provider order entry (CPOE) have existed for more than 30 years, till 2006, less than 10% of hospitals in the U.S. had a fully integrated system. With an aim to change this existing scenario, the Obama administration passed laws to provide the healthcare industry with $19 billion in subsidies over the next few years, to persuade doctors and hospitals to go digital. Big firms have already perceived this as an opportunity to venture into the cloud market. These federal measures are also likely to augment the adoption of cloud computing in rural areas, which will propel the growth of the cloud computing market in the U.S.

• The major players in the North American Healthcare Cloud Computing Market include athenahealth, Inc., CareCloud Corporation, Carestream Health, Inc., ClearData Networks, Inc., Cisco Systems, Inc., Dell, Inc., EMC Corporation, Global Net Access (GNAX) Health, Hewlett-Packard Company, IBM Corporation, Iron Mountain, Inc., Merge Healthcare, Inc., Microsoft Corporation, Oracle Corporation, and VMware, Inc.

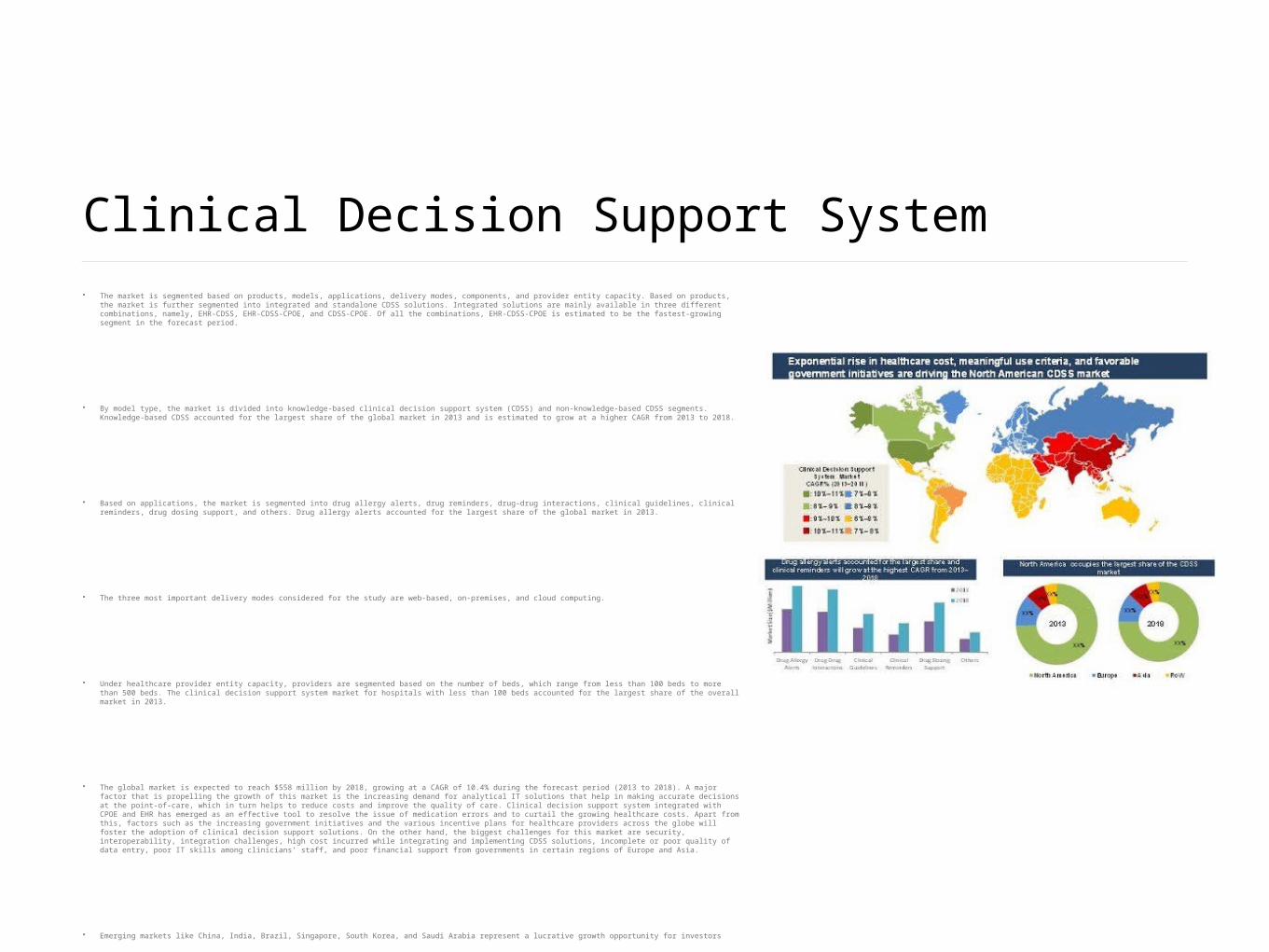

Clinical Decision Support System• The market is segmented based on products, models, applications, delivery modes, components, and provider entity capacity. Based on products, the market is further

segmented into integrated and standalone CDSS solutions. Integrated solutions are mainly available in three different combinations, namely, EHR-CDSS, EHR-CDSS-CPOE, and CDSS-CPOE. Of all the combinations, EHR-CDSS-CPOE is estimated to be the fastest-growing segment in the forecast period.

• By model type, the market is divided into knowledge-based clinical decision support system (CDSS) and non-knowledge-based CDSS segments. Knowledge-based CDSS accounted for the largest share of the global market in 2013 and is estimated to grow at a higher CAGR from 2013 to 2018.

• Based on applications, the market is segmented into drug allergy alerts, drug reminders, drug-drug interactions, clinical guidelines, clinical reminders, drug dosing support, and others. Drug allergy alerts accounted for the largest share of the global market in 2013.

• The three most important delivery modes considered for the study are web-based, on-premises, and cloud computing.

• Under healthcare provider entity capacity, providers are segmented based on the number of beds, which range from less than 100 beds to more than 500 beds. The clinical decision support system market for hospitals with less than 100 beds accounted for the largest share of the overall market in 2013.

• The global market is expected to reach $558 million by 2018, growing at a CAGR of 10.4% during the forecast period (2013 to 2018). A major factor that is propelling the growth of this market is the increasing demand for analytical IT solutions that help in making accurate decisions at the point-of-care, which in turn helps to reduce costs and improve the quality of care. Clinical decision support system integrated with CPOE and EHR has emerged as an effective tool to resolve the issue of medication errors and to curtail the growing healthcare costs. Apart from this, factors such as the increasing government initiatives and the various incentive plans for healthcare providers across the globe will foster the adoption of clinical decision support solutions. On the other hand, the biggest challenges for this market are security, interoperability, integration challenges, high cost incurred while integrating and implementing CDSS solutions, incomplete or poor quality of data entry, poor IT skills among clinicians’ staff, and poor financial support from governments in certain regions of Europe and Asia.

• Emerging markets like China, India, Brazil, Singapore, South Korea, and Saudi Arabia represent a lucrative growth opportunity for investors

• The key players in this market are Agfa Healthcare (Belgium), athenahealth, Inc. (U.S.), Allscripts Healthcare Solutions, Inc. (U.S.), Carestream Health, Inc. (U.S.), Cerner Corporation (U.S.), Epic (U.S.), GE Healthcare (U.K.), McKesson Corporation (U.S.), MEDITECH (U.S.), NextGen Healthcare Information System LLC (U.S.), Novarad Corporation (U.S.), Philips Healthcare (Netherlands), Siemens Healthcare (Germany), Wolters Kluwer (U.S.), and Zynx Health (U.S.).

Clinical Decision Support System Market Details • The global clinical decision support system market is estimated to cross $550 million by 2018, at a CAGR of close to 10.0% between 2013 and 2018. The rising budgetary pressure to reduce healthcare expenditures,

growth in aging population, rising incidences of various diseases due to medication errors, growing need to integrate healthcare IT solutions, improved quality of care and clinical outcomes, and presence of favorable government initiatives are the significant factors propelling the growth of this market in the forecast period. However, rising incidences of data breach and loss of confidentiality, high maintenance and service expenses, shortage of trained IT professionals, and high cost of CDSS solutions are the factors that are hindering the market growth.

• The emergence of the cloud computing mode of delivery and the presence of government initiatives for implementing clinical decision support system solutions in emerging markets offer ample opportunities for healthcare IT vendors to invest in research and development, product modification, application software development, and service provision. The recent arrival of IBM Watson, a cognitive computing-based supercomputer is likely to revolutionize the market. However, this supercomputer is still under trial phase.

• Geographic analysis reveals that North America is the largest contributor to the global market and is expected to grow at the highest rate. Europe holds the second position which is attributed to the growing demand for EHR with clinical decision support system modules in The Netherlands and Spain, initiatives by European Commission such as eGovernment action plan 2011-2015 to support and complement Information and Communication Technologies (ICT) including eHealth, and improving economic condition.Asia (China, India, and South Korea), and Latin America (Brazil) are also poised to grow at high double-digit CAGRs.

• The key players in this market are Agfa Healthcare (Belgium), athenahealth, Inc. (U.S.), Allscripts Healthcare Solutions, Inc. (U.S.), Carestream Health, Inc. (U.S.), Cerner Corporation (U.S.), Epic (U.S.), GE Healthcare (U.K.), McKesson Corporation (U.S.), MEDITECH (U.S.), NextGen Healthcare Information System LLC (U.S.), Novarad Corporation (U.S.), Philips Healthcare (Netherlands), Siemens Healthcare (Germany), Wolters Kluwer (U.S.), and Zynx Health (U.S.).

• The study covers the revenue markets of integrated CDSS solutions and standalone CDSS solutions—the two major classes of the global market. Knowledge-based CDSS and non-knowledge-based CDSS models have also been covered in the study. The volume market is also estimated based on the number of installations in registered hospitals with different bed sizes.

• The definition of CDSS for this market study is as follows: Clinical decision support systems is defined as information technology solutions designed to provide clinicians, staff, and other individuals with knowledge and person-specific information, intelligently filtered or presented at appropriate times, to enhance healthcare quality. The three basic components of CDSS are medical knowledge base, inference mechanism, and a communicator.

mHealth• Mobile health apps & solutions bring offer a successful combination of healthcare and mobile technology. iOS and Android-based medical devices majorly contribute to the healthcare market. Though Android-based

smartphones have outpaced the market share of iOS-based smartphone, the healthcare industry prefers iOS-based devices.

• The market is broadly categorized into connected medical devices and healthcare applications; connected devices dominate the current market with around 80% of the total revenue contribution. Patient monitoring and fitness-wellness are the major application areas of mobile health technology. The most commonly used device and app are cardiac monitoring and exercise app, respectively.

• The connected devices market is segmented into cardiac monitoring, diabetes management device, multi-parameter tracker, and other devices like sleep apnea devices, and respiratory monitors. The global connected devices market is estimated at $5.3 billion in 2013 and is poised to reach $16.4 billion by 2018 at a CAGR of more than 25.0%. Cardiac monitoring and fitness tracking are the most prominent uses of mobile-enabled connected devices owing to the increasing awareness of the need for healthy lifestyles. On the other hand, the diabetes management connected devices market is on the rise to capitalize on the continuous monitoring products of the blood glucose market.

• The mobile health apps market is majorly classified into health and medical apps. The market is dominated by health app with more than 85% volume contribution to the healthcare application market. Health apps are segmented into exercise, weight loss, womens health, sleep and meditation, medication reminder and other apps, while the medical apps market is segmented into medical reference, and other applications like apps for mental health, dermatological treatment, and emergency response.

• The major hindrances in the paid apps market include the availability of free apps almost in all application areas and its low price range ($1-$2 each). Moreover, an interoperable business model integrates various business entities such as application developers, download centers, and platform developers, thus diluting individual quality contributions to the end solution. Exercise app gains the maximum popularity as it transforms the daily-used gadget, smartphone, into a personal workout trainer without significant investment.

• North America contributes the maximum to both the devices and applications market, whereas the increasing number of chronic disease, faster adoption of smartphones and related advanced connectivity and network drive the Asian and African mHealth markets at a brisk rate. Besides, different government initiatives such as Operation Smile by USAID (India), the Indo-Dutch Project Management Society (India), and Mobile Alliance for Maternal Action (South Africa, Bangladesh, India) encourage the local healthcare market to adopt this novel technology.

• The device-software interlinked ecosystem makes the mobile health apps market highly fragmented with an ample number of software developers and network providers. Philips (The Netherlands), Medtronic (U.S.), Nike (U.S.), Omron (Japan), and Alere (U.S.) are notable players in the connected devices market, while AT&T (U.S.), Qualcomm (U.S.), Cerner (U.S.), and Diversinet (Canada) have emerged as significant solution enhancers in 2013.

Market Information• The mobile healthcare market integrates the mobile technology and healthcare application in the global healthcare solution market. The market is segmented into connected medical devices (cardiac monitoring

device, diabetes management device, multi-parameter tracker, and so others), and paid healthcare apps (health apps and medical apps). The connected medical devices market contributes the maximum share (~85%) to the mhealthcare solutions market; whereas paid healthcare apps market is expected to grow at the highest CAGR (33.8%) during the forecast period.

• The mobile healthcare market exhibits a complex business ecosystem where medical device manufacturers, mobile application developers, and healthcare providers are the prime contributors; while network providers and mobile phone manufacturers enhance the quality of mhealthcare solutions. Market dynamics analysis identifies major drivers, restraints, threats, and opportunities of the market. Significant factors ensuring a healthy growth of the market include increasing adoption of smart gadgets for healthcare application, a growing awareness for chronic disease management, and the rapid penetration of advanced network and connectivity. On the other hand, stringent regulations at the product introduction phase and a risk of data theft during mobile transfer are considered as significant hindrances in the market. The factors that pave the way for market expansion in future include expanding business opportunities in emerging countries to capitalize on lower patient-doctor ratio and the introduction of an advanced medium such as a smart TV.

• Product life cycle and market chasm analysis identify significant positive factors that propel the mobile connected medical devices market and the factors that restrain the growth of paid healthcare apps in the global healthcare market. The study provides in-depth information with regards to the regulatory guideline and approval process. Moreover, venture capital analysis spots significant market segments that fetched the maximum capital investments in the recent years. An analysis of benchmarking strategies identifies dominant strategies adopted by leading players in the device manufacturer and network provider markets. Amongst all connected medical devices, the diabetes management devices market is expected to grow at the highest CAGR of 27.7%, while, ‘weight loss’ and ‘sleep and meditation’ apps are poised to showcase the highest growth in the paid healthcare apps market from 2013 to 2018.

• The study analyzes regional markets such as North America, Europe, Asia, and Rest of the World (RoW) for individual product and application segments. In-depth geographic analysis deals with significant government and private initiatives, investments, and regulations to provide a holistic market landscape. India and Japan in the Asian market, and Africa in the RoW market are considered the most potential markets in future. Operation Smile by USAID, the Indo-Dutch Project Management Society (India), and Mobile Alliance for Maternal Action (South Africa, Bangladesh, and India) are the significant initiatives taken in the emerging nations.

• The mobile healthcare market is highly fragmented, since the device and apps market are integrated at several points and enriched with ample number of software developers and network providers. The future of this solution market is expected to be more complex when the device and companion apps market would merge to provide a comprehensive solution.

Healthcare IT Outsourcing Market• Outsourcing is an emerging phenomenon in the healthcare information technology market. It is a screening process wherein an organization selects the most efficient third-party service provider to effectively operate

its management and administrative unit. Outsourcing of IT solutions in the healthcare industry has emerged as an efficient solution to mitigate rising healthcare costs and to meet the growing demand for quality care. Over the years, the trend of healthcare IT outsourcing solutions has grown significantly among large organizations and has also attracted mid-sized organizations. In some cases, the entire information management system is outsourced, while in others, only key application services such as implementation of EMR, CRM, and billing systems are outsourced.

• The market for this report has been segmented by application and by industry. The application market is further classified as provider healthcare IT outsourcing, payer healthcare IT outsourcing, life science healthcare IT outsourcing, operational IT outsourcing, and infrastructure IT outsourcing, while the market by industry is segmented as healthcare (including hospitals, diagnostic laboratories, and clinics), biotechnology, pharmaceutical, clinical research organizations, and health insurance.

• The global market is forecast to grow at a CAGR of 7.6%, to reach $50.4 billion by 2018 from $35 billion in 2013. The health insurance industry, healthcare systems industry, and pharmaceutical industry are driving the HCIT outsourcing market. These industries follow the healthcare IT outsourcing model to enhance their focus on core business, reduce operational and maintenance costs, increase access to IT skilled and trained staff (further reducing hiring and training costs), share risk, and quickly implement new technologies.

• Factors propelling the growth of the market are the rising pressure to curb healthcare costs across the globe and the growing need to manage cash flow in back-office administration and IT management systems of healthcare provider, payers, and the life science segment. Lack of in-house IT expertise, rise in demand for integrating solutions, growing pressure on healthcare providers to meet the “Meaningful Criteria” set by the U.S. Federal Government, new ICD-10 conversion guidelines for coding, rise in aging population, and growing medical tourism in Asia are also likely to drive this market.

• However, factors such as the fragmented nature of the healthcare system and HCIT outsourcing market, requirement for high investment in outsourcing IT solutions, growing concern for data security, and cultural and language barriers restrain the growth of the market.

• North America accounts for the largest share - 72% - of the global HCIT outsourcing market and is expected to reach $36 billion by 2018 from $25 billion in 2013. Asia-Pacific and RoW are expected to register CAGRs of 8.1% and 7.8% (2013 to 2018) respectively, followed by North America (7.6%), and Europe (7.2%).

• Major players in the market are Accenture Plc. (Ireland), Accretive Health, Inc. (U.S.), Allscripts Healthcare Solutions, Inc. (U.S.), Anthelio Healthcare Solutions (U.S.), Cognizant Technology Solutions (U.S.), Dell, Inc. (U.S.), HCL Technologies (India), Hewlett-Packard Company (U.S.), International Business Machines (IBM) Corporation (U.S.), Infosys Limited (India), McKesson Corporation (U.S.), Siemens Healthcare (Germany), Tata Consultancy Services Ltd. (India), Wipro Ltd. (India), Xerox Corporation (U.S.), Epic System (U.S.), and Computer Sciences Corporation (U.S.).

Healthcare IT Outsourcing Market Details

• The introduction of information technology in the healthcare and life sciences industries has quickened the healthcare process, thereby reducing costs while efficiently managing huge amounts

of patient data. However, the adoption rate of healthcare information technology is still low in many regions due to the high costs incurred for implementation, maintenance, and up-gradation

services; poor in-house IT skilled resources; and inadequate IT infrastructure. Outsourcing has emerged as an effective tool to combat these challenges. Outsourcing enables the healthcare and

life sciences industries to focus more on their core businesses. Furthermore, it offers various benefits such as reduced operating costs, access to skilled resources, quick deployment, flexibility

in the choice of technology and modules, improved cash flow, and risk sharing. The global HCIT outsourcing market is forecast to grow at a CAGR of 7.6%, to reach $50.4 billion by 2018 from

$35 billion in 2013.

• The market for this report has been segmented by application and by industry. The application market is further classified as provider IT outsourcing, payer healthcare IT outsourcing, life

science healthcare IT outsourcing, operational healthcare IT outsourcing, and infrastructure healthcare IT outsourcing. Provider HCIT outsourcing is further segmented into electronic health

records (EHR), laboratory information management system (LIMS), pharmacy information system (PIS), and revenue cycle management (RCM) systems. Payer HCIT outsourcing includes the

following sub-segments, namely, customer relation management (CRM), claim processing, billing system, and fraud and detection. Life science HCIT outsourcing is divided into enterprise

resource planning (ERP), clinical trial management system (CTMS), clinical data management system (CDMS), and R&D IT services. The sub-segments of operational HCIT outsourcing included

for study are supply chain management (SCM), and business process management (BPM) outsourcing. IT infrastructure outsourcing is further divided into two prominent sub-segments, namely,

infrastructure management services (IMS), and cloud computing. The market by industry is segmented as healthcare provider system (including hospitals, diagnostic laboratories, and clinics),

biotechnology, pharmaceutical, clinical research organizations, and health insurance.

• Factors propelling the growth of the market are the rising pressure to curb healthcare costs across the globe and the growing need to manage cash flow in back-office administration and IT

management systems of healthcare providers, payers, and the life science segment. Lack of in-house IT expertise, rise in demand for integrating solutions, growing pressure on healthcare

providers to meet the “Meaningful Criteria” set by the U.S. Federal Government, new ICD-10 conversion guidelines for coding, rise in aging population, and growing medical tourism in Asia are

some of the other factors that are also likely to drive the healthcare IT outsourcing market.

• However, factors such as the fragmented nature of the healthcare system and healthcare IT outsourcing market, requirement for high investment in outsourcing IT solutions, growing concern

for data security, and cultural and language barriers restrain the growth of the market.

• Major players in the market are Accenture Plc (Ireland), Accretive Health, Inc. (U.S.), Allscripts Healthcare Solutions, Inc. (U.S.), Anthelio Healthcare Solutions, Inc. (U.S.), Cognizant Technology

Solutions (U.S.), Dell, Inc. (U.S.), HCL Technologies (India), Hewlett-Packard Company (U.S.), International Business Machines (IBM) Corporation (U.S.), Infosys Limited (India), McKesson

Corporation (U.S.), Siemens Healthcare (Germany), Tata Consultancy Services Ltd. (India), Wipro Ltd. (India), Xerox Corporation (U.S.), Epic System (U.S.), and Computer Sciences Corporation

(U.S.).

Medical Image Analysis Software Market• The growth of the medical image analysis market is mainly contributed by the standalone software market which is accelerating at a faster pace as compared to the integrated software market which is moving at a

stable rate. The market has seen a boost since the IT revolution in healthcare, but is still dominated by OEMs. Many smaller players are making efforts to make a mark in the medical image analysis market. But the major revenues are generated through supplying services and programs to the OEM. This report covers definition, description, and forecast of the global medical image analysis software market in terms of integrated and standalone software, by modalities, by image type, by indications and by end-users. The medical image analysis market is estimated to be $1.7 billion in 2012 and is growing at a rate of 7.2% from 2012 to 2017 to reach $2.4 billion.

• Software has become the work horse of any machine or equipment used in today’s world, medical devices are no exception. Software is used in the medical industry for varied purposes such as training, viewing, storing data, sharing data etc; thereby increasing the efficiency and effectiveness of medical procedures.

• The global medical image analysis software market is growing at a higher rate as compared to the equipment market. The image analysis software market is driven by higher demand for diagnostic procedures globally, technology improvements and demand from the consumer end. The major restraints are the inherent drawbacks associated with software. The major trends seen in the market are towards open source software, online portals and 30 day trials for software. The major challenges from the end-users are restriction in terms of software usage and major challenge for standalone vendors is the OEM manufacturers.

• Medical device market represents the second largest market after pharmaceutical market in the healthcare industry and diagnostic imaging market represents around 35% of the total medical device market in the year 2010. Medical image analysis software is a small fraction of the diagnostic market, growing at a slightly higher rate as compared to equipment market.

• Scope of the report

• This research report covers the global medical image analysis market which has been segmented into integrated and standalone software. Both of these markets are further broken down into segments and sub-segments based on modalities, image type, indications and end-users.

• The global medical image analysis market segmentation by modalities, image type, indications and end-users include:

• Global medical image analysis market, by modalities

• X-ray

• Ultrasound

• Computed Tomography (CT)

• Magnetic Resonance Imaging (MRI)

• Nuclear Imaging (PET & SPECT)

• Global medical image analysis market, by image type

• 2D

• 3D

• 4D

• Global medical image analysis market, by indications

• Radiology

• Cardiology

• Oncology

• Neurology

• Obstetrics & gynecology

• Breast mammography

• Global medical image analysis market, by end-users

• Hospitals

• Diagnostic centers

• Research centers

• The major players in this market include GE Healthcare (U.K.), Siemens (Germany), Philips (The Netherlands), Toshiba Medical systems (Japan), Agfa healthcare (Belgium), etc. The smaller players include Claron Technologies (Canada), Care stream Health, Inc. (U.S.), Medviso AB (Sweden), Merge Healthcare (U.S.), etc.

Medical Image Analysis Market Details

• The market for image analysis software is broadly divided into integrated software and standalone market. The growth of the medical image analysis market is mainly contributed by the standalone software market which is accelerating at a faster pace as compared to the integrated software market which is moving at a stable rate. The market has seen a boost since the IT revolution in healthcare, but is still dominated by OEMs. Many smaller players are making efforts to make a mark in the medical image analysis market. But the major revenues are generated through supplying services and programs to the OEM. This report covers definition, description, and forecast of the global medical image analysis software market in terms of integrated and standalone software, by modalities, by image type, by indications and by end-users.

• Medical image analysis process includes activities such as identification, measurement and/or judgment, it requires computational support to handle the size, heterogeneity, and complexity of the data and methods involved in the medical imaging process. The main goal of the software is to provide automatic or semi-automatic medical diagnosis. With the advent of computers there has been a continuous development in the medical image analysis software.

• The medical image analysis software market is driven by the increasing demand of the imaging modalities across various indications such as oncology, cardiology and neurology. Fusion of technologies, CAD increasing applications in diagnostic and automated image analysis are the major drivers of the medical image analysis market. The major restraints of the market are inherent difficulties associated with software and hacking which is a major concern associated with software. The major opportunities are developing countries where the market is untapped and medical device security software market is an interesting and growing segment.

• Applied medical research is dependent on imaging for evaluation of therapeutic effects of new drugs or therapies. Thus, dedicated image analysis software had become mandatory for quantitative medical imaging.

• Based on the principle, macroscopic medical imaging is basically divided as external source and internal source. In external source, X-ray, CT and projected radiography are based on transmission principle whereas Ultrasound follows refraction/reflection principle. Under internal source, PET and SPECT follow internal tracer principle.

Competitive Landscape • Inadequate It Infrastructure Amongst Payers - A Major Growth Factor• 12.1 Athenahealth, Inc.• 12.2 Carecloud Corporation• 12.3 Carestream Health, Inc.• 12.4 Cisco Systems, Inc.• 12.5 Cleardata Networks, Inc.• 12.6 Dell, Inc.• 12.7 Emc Corporation• 12.8 Global Net Access (Gnax) Health• 12.9 Hewlett-Packard Company• 12.10 Ibm Corporation• 12.11 Iron Mountain, Inc.• 12.12 Merge Healthcare, Inc.• 12.13 Microsoft Corporation• 12.14 Oracle Corporation• 12.15 Vmware, Inc.

• The web portal development segment commanded the largest share of the global Health Information Exchange applications market. It is expected to grow at a strong CAGR during the study period. The large share and high growth of this segment can be attributed to the increasing number of physicians opting for electronic medical records driven by the convenience of web-based portals to retrieve information on patients.