Embed Size (px)

Citation preview

Business Case for SmartFridge and Vaccine Transport Container – Final Report

Project Scope, Objectives, and Methodology

3

Project Scope

This project consisted of a global assessment of the value opportunities for a Vaccine Transport Container and SmartFridge. As part of this assessment, Harrison Hayes sought to develop a business case outlining the opportunities for each product. Although the primary focus of this project was vaccines, Harrison Hayes also sought to address other unmet needs.

4

Project Objectives

The primary objective of this project is to develop a complete and thorough business case for the introduction of a Vaccine Transport Container and Vaccine SmartFridge. Specific objectives include:

q Identification of market opportunities, barriers, risks, and challenges.

q Assessment and analysis of market drivers and inhibitors.

q Identification and analysis of critical success factors.

q Determination of market adoption rates and product pricing.

q Identification of therapeutic areas outside of vaccines that may best be able to utilize cold chain supply systems.

q Determination of the value that a Vaccine Transport Container and Vaccine SmartFridge may provide.

q Identification of regions/countries and therapeutic areas that would provide the greatest value.

5

Research Methodology

Market research for this project consisted of Primary and Secondary market research. Primary research included the conduction of one hundred four (104) Key Opinion Leader interviews on a global basis across a variety of specialties.

To supplement these Key Opinion Leader interviews, Harrison Hayes also conducted secondary research from publicly available information and syndicated sources.

General Observations on “Cold Chain”

7

“Cold Chain” Defined

When Key Opinion Leaders were asked to define “cold chain” they answered with the following:

Key Opinion Leaders identified/defined two (2) areas: Food/Beverage industryand Pharmaceutical/Healthcare.

Key Opinion Leaders further defined the cold chain in food/beverage industry asrelated to supermarkets, convenience stores, and end consumers.

The pharmaceutical market consisted of the supply chain, physicians, and theoverall patient base.

8

WHO and “Cool Chain”

Proper vaccine storage and transportation is a key issue in the developing world,which presents numerous challenges.

As such, the World Health Organization (WHO), has developed the Performance,Quality, and Safety (PQS) system of cooling technology prequalification.

WHO has identified the following three (3) categories within the “cool chain”:

1. Refrigeration

2. Passive Cooling

3. Temperature Monitoring

9

View of the “Cold Chain”

Key Opinion Leaders viewed the cold supply chain strictly as a regional businessmodel.

The interviewed Key Opinion Leaders noted that the industry is extremelyfragmented with a lack of consistent product/cooling technology, specifically inthe healthcare arena. There are too many marginal players in the space.

A cooling transport solution was addressed by a majority of the Key OpinionLeaders in unaided response.

The biggest problems were product maintenance and product temperature.

10

“Cold Chain” Market Players

Global Market Players

According to the WHO’s Product Information Sheets and Performance Quality andSafety Sheets there are thirty seven (37) approved refrigerators and freezers.

These refrigerators and freezers are broken down into compression units,absorption units, and solar units.

There are four (4) primary manufacturers: Dometic, Vestfrost, Sibir International,and Zero Appliances.

11

Requirements in the Cold Chain

Logistics is the central component to successful cold chain initiatives, especially as it relates to vaccines. Specific issues that must be taken into account include:

Storage Conditions (temperature)

Presentation (prefilled device, single dose vials, etc.)

Packaging (volume based)

Cost per dose

12

Cold Chain Distribution Models

The WHO identifies two (2) logistics models as it relates to the cold chain.

Distribution System

Collection System

The Key Opinion Leaders strongly believed that the Distribution Model was much more likely to provide a successful solution over the Collection system. This opinion was validated by the WHO.

Market Opportunities – United States

14

Market Size

Sales within the Global Refrigeration space is approximately $60B. The table below outlines these figures. Of this amount, less than 1% can be attributed to vaccine cold chain.

Vaccine Cold Chain Refrigerator sales are estimated to be $.566B worldwide.

Equipment Sales

Domestic Refrigerators $32.8B

Commercial Refrigeration Equipment

$18.6B

Cold Storage $2B

Refrigerated Transport Vehicles $2B

Refrigerated Containers $1.2B

Total: $56.6B

15

Market Opportunities

When the Key Opinion Leaders were asked what they believe the key market opportunities should be, they responded with the following:

Big Box/Chain pharmacies/Wal-Mart

Dermatologist offices

Insulin and Liquid Antibiotic storage (inclusive of insulin)

Neonatal centers

Plastic surgery offices

Prisons

Pediatrician offices

Third World Countries

Veterinarians

16

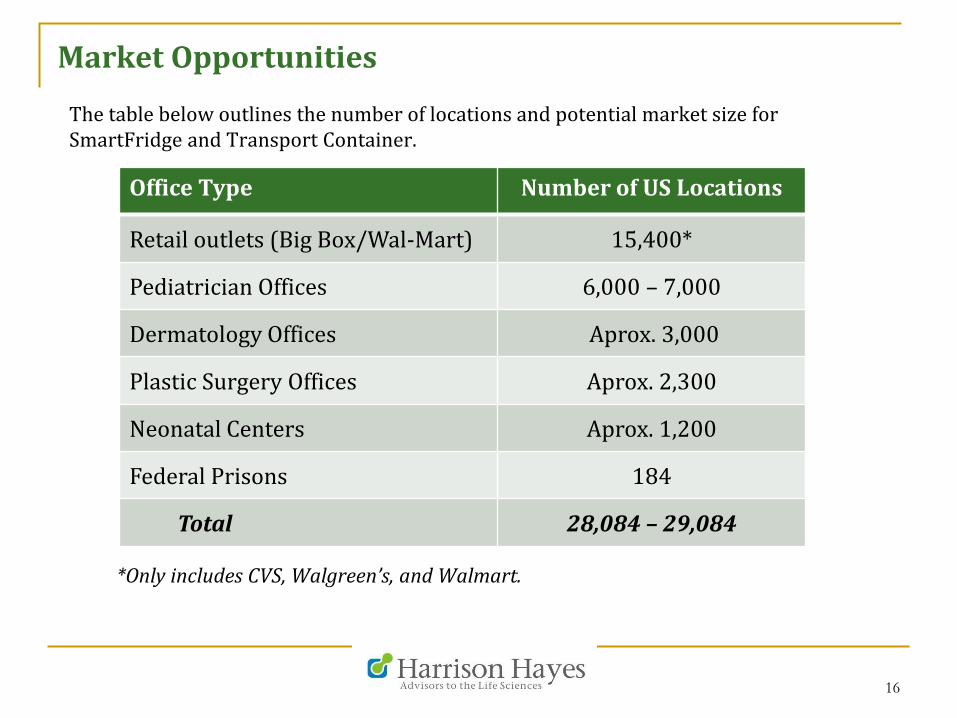

Market Opportunities

The table below outlines the number of locations and potential market size for SmartFridge and Transport Container.

*Only includes CVS, Walgreen’s, and Walmart.

Office Type Number of US Locations

Retail outlets (Big Box/Wal-Mart) 15,400*

Pediatrician Offices 6,000 – 7,000

Dermatology Offices Aprox. 3,000

Plastic Surgery Offices Aprox. 2,300

Neonatal Centers Aprox. 1,200

Federal Prisons 184

Total 28,084 – 29,084

17

Market Opportunities Con’t.

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000

The chart outlines the number of locations and potential market size (not dollar based).

Number of Locations

18

Market Opportunities- Key Opinion Leader Perspective

Early Adopters/Adoption Rate/Pricing for SmartFridge The U.S. based Key Opinion Leaders stated that the Pediatric Physician space

represented the clear target opportunity.

Dermatology Offices were mentioned as a secondary opportunity.

A significant majority (more than 75%) of the interviewed Key Opinion Leadersstated that early market adoption rates would approach 25% in Pediatricianand Dermatology offices.

NOTE: The market adoption rates assumes that the SmartFridge contains thedesired features/benefits and meets the market needs detailed in the “CriticalSuccess Factors” section.

Key Opinion Leaders noted that a leasing option would be the most ideal; Leasingamounts range from $100 to $200 per month.

19

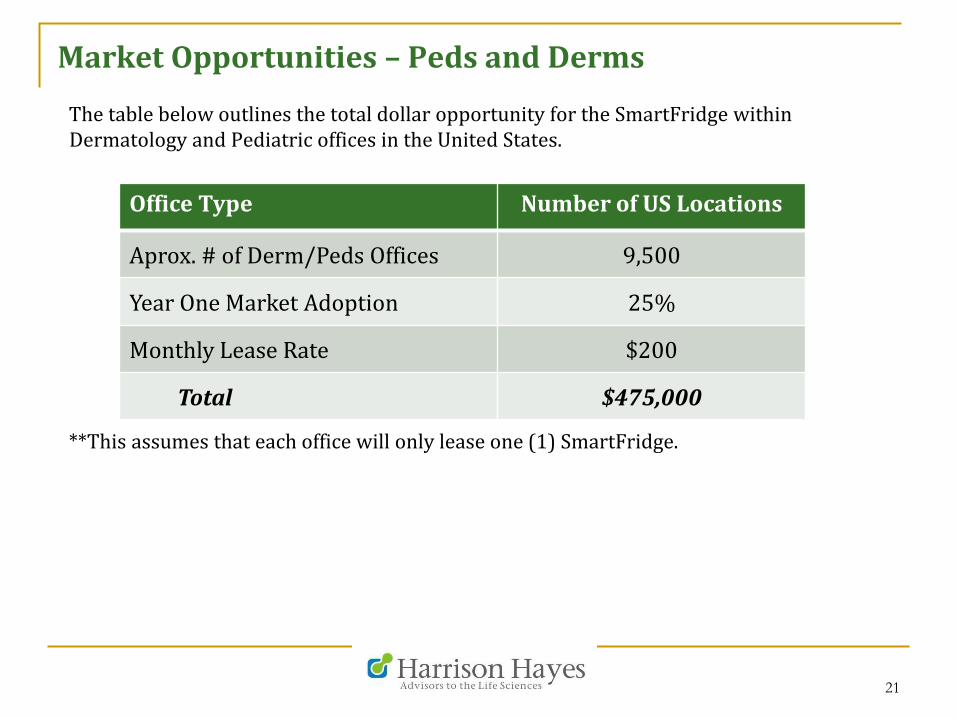

Market Opportunities – Peds and Derms

The table below outlines the total dollar opportunity for the SmartFridge within Dermatology and Pediatric offices in the United States.

**This assumes that each office will only lease one (1) SmartFridge.

Office Type Number of US Locations

Aprox. # of Derm/Peds Offices 9,500

Year One Market Adoption 25%

Monthly Lease Rate $150

Total $356,250

20

Market Opportunities – Peds and Derms

The table below outlines the total dollar opportunity for the SmartFridge within Dermatology and Pediatric offices in the United States.

**This assumes that each office will only lease one (1) SmartFridge.

Office Type Number of US Locations

Aprox. # of Derm/Peds Offices 9,500

Year One Market Adoption 25%

Monthly Lease Rate $100

Total $237,500

21

Market Opportunities – Peds and Derms

The table below outlines the total dollar opportunity for the SmartFridge within Dermatology and Pediatric offices in the United States.

**This assumes that each office will only lease one (1) SmartFridge.

Office Type Number of US Locations

Aprox. # of Derm/Peds Offices 9,500

Year One Market Adoption 25%

Monthly Lease Rate $200

Total $475,000

22

Market Opportunities - Derms and Peds Con’t.

On the Small Dollar Amount Based on the previous three (3) tables, initial dollar revenue is extremely small, at

less than $.5M. This estimate is based on the fact that each office would only leaseone (1) SmartFridge

It is important to note that Pediatrician market is extremely price sensitive andthat any new technology that is introduced must show cost savings.

Therefore, assuming the SmartFridge is successful and limits the amount ofvaccine waste, Pediatricians will then adopt the SmartFridge much more quickly.

23

Market Opportunities- Transport Container (USA)

Transport Container in the United States The U.S. based Key Opinion Leaders very easily understood the practicality and

applicability of the vaccine SmartFridge, but were not as impressed with theTransport Container.

It was unanimous among all Key Opinion Leaders that vaccine transportneeded to be improved, but physicians could not see how such a solution would fitinto their existing business model (i.e. they do not want to pay for this).

U.S. based physicians noted that they typically assume that vaccines are safe uponarrival; if refrigeration problems do arise, they assume the issue occurred in theoffice setting rather than transport.

In the United States, there is a relatively high level of confidence in the vaccinetransport system. This is not the case in the developing world.

Merck Vaccine Transport Container

Market Opportunities – Developing World

25

Market Opportunity – Developing World

Developing World There is a clear need for updated vaccine refrigeration in both transport and in

the clinical setting in the developing world.

Unlike the United States, the primary buyers of a vaccine SmartFridge and/orTransport Container in the Developing World are UNICEF and a correspondingcountry’s Ministry of Health.

26

Market Opportunity – Developing World Con’t.

Developing World Based on information from UNICEF, roughly 200,000 vaccine refrigerators are

currently used in immunization programs in the developing world.

UNICEF vaccine refrigerator purchases make up roughly 85% of the market;Between 1997 and 2003 UNICEF refrigeration expenditures totaled $77M.

Ministry of Health refrigeration expenditures over the same period wasestimated at $15M.

Countries with the most active Ministries of Health include India, Indonesia, andJapan.

27

Market Opportunity – Developing World Con’t.

Developing World Market Behavior Developing countries typically do not spend more than 10% of their EPI on cold

chain equipment.

Most financial decisions regarding cold chain are made during the fourth (4th)quarter each year.

South American countries, more than any other region, typically rely onrefrigerators that are intended for home use.

28

Market Opportunity – Defined

Defining/Describing the Opportunity In many areas of the developing world, electricity is not readily available. This

has led to a vaccine distribution model.

Vaccines are held in a “cold room” at a central location and distributed throughtransport coolers.

29

Market Opportunity – Defined

Recently Proposed Solutions In the developing world, there is a clear focus on the construction of “cold rooms”

rather than using vaccine refrigerators.

These cold rooms will need to be outside of existing buildings/structures andhave adequate power supply.

“Cold Rooms” will be larger than 40m3.

Air/Freight shipping containers will need to be larger than those currentlyavailable and have the ability to keep vaccines between 2 and 8 degrees Celsiusfor a minimum of ten (10) days.

30

Market Opportunity – Defined

Recently Proposed Solutions Con’t. In cases where refrigerators must be used, Ice-Lined Refrigerators (ILRs) are

the most acceptable. These ILRs must have a capacity of at least 400 liters.

Key Opinion Leaders in developing countries believed traditional “cold boxes”may no longer be appropriate.

Instead, Passive Container Systems (similar to those used in supermarkets) mayrepresent the best known solution.

Traditional Ice Packs will be too heavy for people to carry given the increase inthe volume of vaccines.

Passive Container System

Ice Lined Refrigerator

31

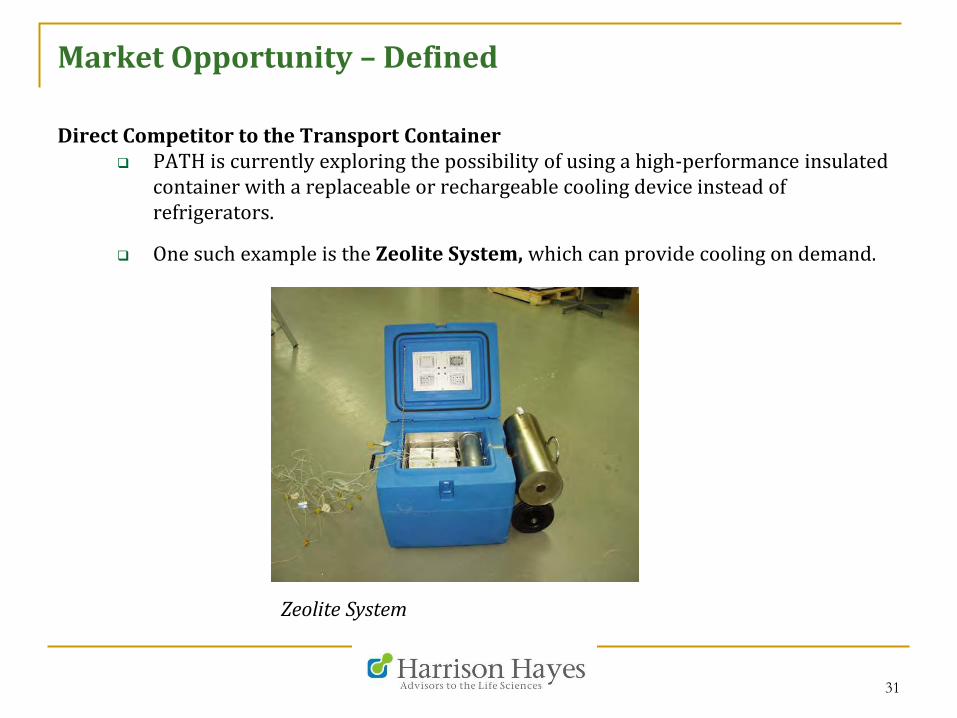

Market Opportunity – Defined

Direct Competitor to the Transport Container PATH is currently exploring the possibility of using a high-performance insulated

container with a replaceable or rechargeable cooling device instead ofrefrigerators.

One such example is the Zeolite System, which can provide cooling on demand.

Zeolite System

32

Market Opportunity – Cooling System Competitor

Zeolite The Zeolite System is currently being developed and produced by Dometic.

Zeolite is a mineral that has the property to absorb water vapor while releasingheat.

This system has the ability to store energy and transform it in heating or coolingagents.

Additional information on Zeolite can be found in the attached, separatedocument.

Zeolite System

Market Opportunities – Product Areas

34

Market Opportunity – Product Specific

When the Key Opinion Leaders were asked what products would most benefit from SmartFridge and Transport Container like devices, the following answers were given:

1. Vaccines

2. Insulin

3. Injectables

4. Re-fill Devices

5. Antibiotics

Note: This is a stack ranking in regards to number of responses.

35

Market Opportunity – Product Specific

Vaccines and Insulin Vaccines were mentioned as the primary product area of focus by every Key

Opinion Leader interviewed, regardless of background.

Insulin was mentioned by all physician/healthcare specific Key Opinion Leadersmentioned.

Vaccines and insulin were by far the most important products the Key OpinionLeaders believed to have the most applicability to a SmartFridge and/orTransport Container.

There was equal distribution of the other responses, none of which were asignificant threshold.

36

Market Opportunity – Additional Products

The following products were mentioned by less than five (5) Key Opinion Leaders:

Dermatology fillers

Misc. dermatology products

Plastic Surgery materials

BoTox

Market Drivers

38

Market Drivers – Overview

Based on Key Opinion Leader feedback and Secondary research, the following items were mentioned as the primary market drivers for Cold Chain improvement:

1. Vaccine Wastage (Cost)

2. Rising Cost of Vaccines

3. Existing technology inadequate

39

Market Drivers – Wastage

Vaccine Wastage:

Not surprisingly, vaccine wastage was identified as the primary market driver ofdriving the need for improvement in the cold chain.

Depending on the source, between $400 and $500M is lost on vaccine wastageeach year. Half of this amount is directly related to breakdown in the coldchain.

The primary causes of this vaccine wastage include:

Cold chain issues

Expired vaccines

Damaged vials (broken during transport)

Doses diverted from target population

Accidental waste (throwing away good vaccines)

40

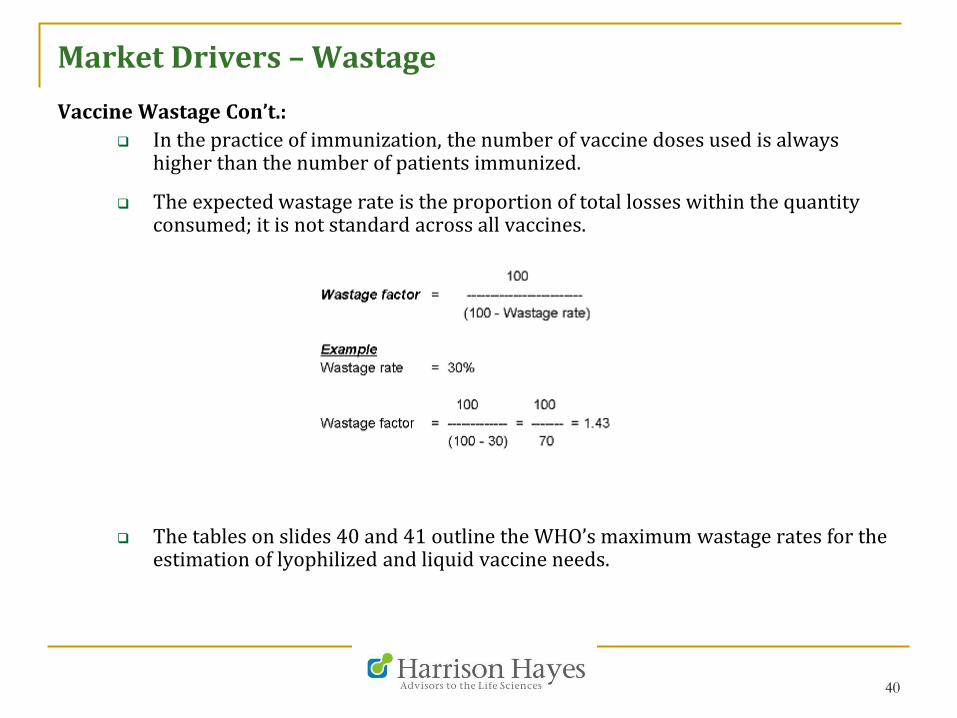

Market Drivers – Wastage

Vaccine Wastage Con’t.:

In the practice of immunization, the number of vaccine doses used is alwayshigher than the number of patients immunized.

The expected wastage rate is the proportion of total losses within the quantityconsumed; it is not standard across all vaccines.

The tables on slides 40 and 41 outline the WHO’s maximum wastage rates for theestimation of lyophilized and liquid vaccine needs.

41

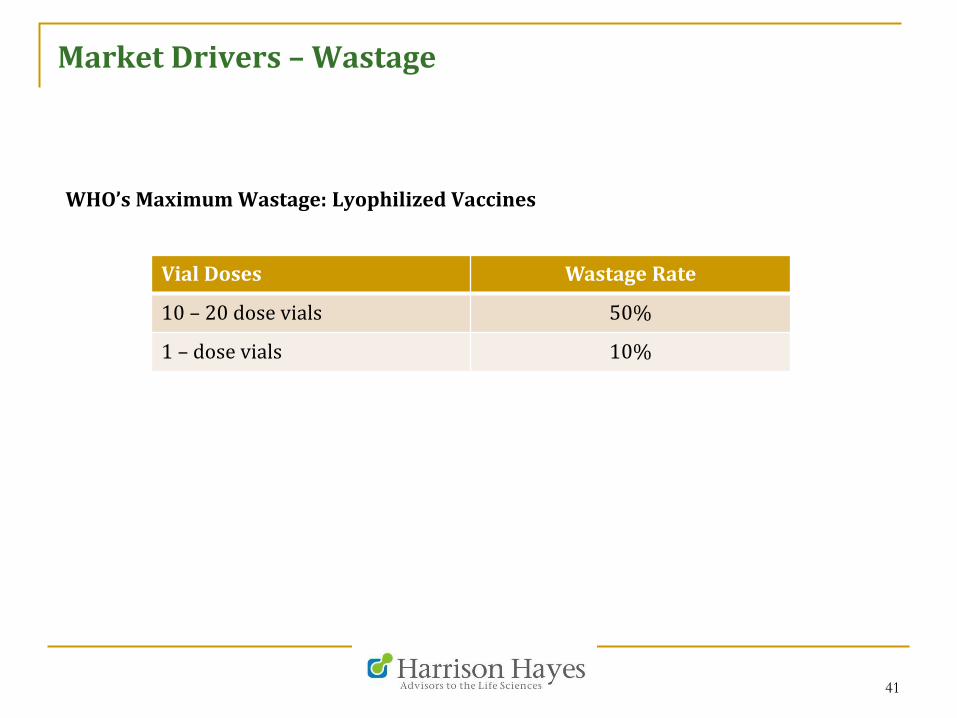

Market Drivers – Wastage

WHO’s Maximum Wastage: Lyophilized Vaccines

Vial Doses Wastage Rate

10 – 20 dose vials 50%

1 – dose vials 10%

42

Market Drivers – Wastage

WHO’s Maximum Wastage: Liquid Vaccines

Vial Doses Wastage Rate

10 – 20 dose vials 25%

1 – dose vials 10%

43

Market Drivers – Vaccine Cost

Vaccine Cost:

Traditional vaccines (measles, DPT, Polio, etc.) have been on the market ordecades, which results in a low cost.

These legacy vaccines general cost between $0.10 and $0.25, which makes themvery affordable and wastage is less of a concern.

New vaccines come with significantly higher costs, generally between $4 and $15per dose. Note: There are some vaccines that cost more than $15.

The high costs of these vaccines has heightened the need to reduce vaccinewastage.

44

Market Drivers – Vaccine Cost Con’t.

The image below portrays the increase in the cost of newer vaccines compared to legacy vaccines:

Image courtesy of Project Optimize and PATH

45

Market Drivers – Vaccine Cost Con’t.

Vaccine Cost: Legacy Vaccines v. Current Vaccines

When vaccines cost less than $1, the total cost associated with vaccine wastagewas manageable.

With lower costs, problems with logistics and the cold chain could be addressedby maintaining high stock levels. Due to the cost of vaccines, this is no longercost effective.

The cost of vaccines has caused vaccine administrators to maintain lower stocklevels, forecast vaccine demand, better prevent vaccine breakdowns and reduceoverall wastage.

46

Market Drivers – Existing Cold Chain Solutions

Existing Cold Chain Solutions are Insufficient

The Key Opinion Leaders interviewed in this study were adamant that the currenttechnologies related to the cold chain are inefficient. Specific problems mentionedinclude:

1. Freezing

2. Heat

3. Moisture in refrigerator

4. Light Exposure

47

Market Drivers – Existing Cold Chain Solutions

Standard Refrigerators

A significant majority (more than 75%) of the physician Key Opinion Leadersinterviewed in the United States noted that they use standard refrigerators tostore vaccines.

In standard refrigerators, Freezing was noted to be the primary issue. Vaccinesplaced at the back of the refrigerator typically freeze.

The temperature variance is not uniform in standard refrigerators, which causesproblems with vaccines.

Moisture was the second greatest concern when using standard refrigerators. Inmany cases the Key Opinion Leaders noted that this moisture would often ruin thevaccine, creating waste.

Heat and Light Exposure was mentioned as areas of concern, specifically whenthe refrigerator door is left ajar.

48

Market Drivers – Existing Cold Chain Solutions

Standard Refrigerators v. Vaccine Refrigerators

All of the interviewed Key Opinion Leaders had a very low confidence level invaccine/healthcare specific refrigerators.

Vaccine/Healthcare Refrigerators are used because they are “the bestavailable” according to the industry.

Key Opinion Leaders believed that standard refrigerators were on par withhealthcare/vaccine specific refrigerators. The only difference is cost.

Vaccine Refrigerator Standard white refrigerator

Market Barriers, Challenges, and Inhibitors

50

Market Barriers, Challenges, Inhibitors

When the Key Opinion Leaders were asked what they believed to be the primary market barriers/challenges/inhibitors related to cold chain, the following answers were provided:

1. Lack of Viable Technology

2. Container Size and Cost

3. Reliability

4. Power Source

5. Storage

51

Market Barriers, Challenges, Inhibitors

Lack of Viable Technology

Numerous technologies have been explored, examined, and tested but none todate have truly stood out.

Tested technologies include:

Cool packs

Peltier Element

Insulation Materials

Sugar Molecules

52

Market Barriers, Challenges, Inhibitors

Lack of Viable Technology: Peltier Element

q Due to the primary interest in the Peltier Element, Harrison Hayes specifically explored the pros and cons of this technology.

q A majority of the interviewed Key Opinion Leaders were extremely skeptical of the Peltier Element. “Peltier is not an efficient technology…I wouldn’t think it is an applicable technology for cold chain improvement.”

q The primary issue with Peltier was the issue with heat; in general, Peltier feedback was not positive.

53

Market Barriers, Challenges, Inhibitors

Lack of Viable Technology: Peltier Element PROS

Compared to standard refrigerators, the Peltier Element does not have anymoving parts.

When Peltier is used to cool electronic elements, it has relatively high reliabilityrates.

A “cascading Peltier” will enable electronic components to cool below freezingtemperatures.

54

Market Barriers, Challenges, Inhibitors

Lack of Viable Technology: Peltier Element CONS

Peltier modules release a large amount of heat and require “heat-sinks” and fans,which take up space.

In the event that a Peltier module fails, the cooled space is isolated from the heat-sinks. This leads to a extremely fast breakdown of the cool/stable temperatureand could cause overheating.

Peltier cooling elements may cause moisture/condensation. This couldpotentially harm the vaccines.

55

Market Barriers, Challenges, Inhibitors

Vaccine Container Size

Unlike legacy vaccines, new vaccines are packed much differently in order tominimize waste and be cost effective.

Legacy vaccines are packaged in 10 and 20 dose vials; New vaccines are packedin 1 and 2 dose vials to minimize wastage.

In some cases, new vaccines are bundled with delivery devices requiring larger,bulkier packaging.

While cold chain research used to focus on creating smaller cooling apparatuses,the need is really for larger more efficient solutions.

56

Market Barriers, Challenges, Inhibitors

Vaccine Container Size: How Pack-out is Affecting Cost

Image courtesy of PATH

57

Market Barriers, Challenges, Inhibitors

Vaccine Container Size Con’t.

Today, a refrigerator full of new vaccines will destroy thousands of dollarsrather than a few hundred dollars as is the case with legacy vaccines.

Additionally, the volume of vaccines that need to be refrigerated is expected togrow eight-fold.

This increase in packaging size and vaccine volume will create a need for larger,efficient cold rooms and refrigerators.

58

Market Barriers, Challenges, Inhibitors

Vaccine Container: In Transport

Today, vaccines are typically transported in cold boxes of 20 - 25 liter capacity. Ofthis amount, 15 liters is made up of cold packs.

Current cold box designs have extensive insulation, which further limits thecapacity of the cold box transport.

Refrigerated transport is an option in some areas, but often times roadinfrastructure is poor and refrigerated transport is extremely unreliable.

59

Market Barriers, Challenges, Inhibitors

Power Supply and Reliability

A primary challenge is finding and implementing a reliable power supply.

Power supply in the cold chain has consisted of the following:

Electricity

Kerosene

Gasoline

Solar Photovoltaic

Note: These power supplies have been used for both refrigerators andtransport containers.

60

Market Barriers, Challenges, Inhibitors

Power Supply and Reliability: Electricity

In the United States and developed world, electricity is the primary power supply.

Electricity is typically reliable in both a refrigerator setting and in a cooledtransport setting.

Electricity as a power supply in transport is reliable only as far as the reliability ofthe highway infrastructure.

61

Market Barriers, Challenges, Inhibitors

Power Supply and Reliability: Gasoline and Kerosene

Cooling technologies powered by gasoline or kerosene are extremely inefficientand unreliable (according to PATH Key Opinion Leaders).

As expected, these refrigerators are not environmentally compatible.

Kerosene refrigerators were banned by the WHO in 2009.

Gasoline powered refrigeration is forecasted to be the most expensive coolingoption over the next ten (10) years.

62

Market Barriers, Challenges, Inhibitors

Power Supply and Reliability: Solar Photovoltaic

Solar photovoltaic technology may be a viable alternative to electricity, especiallyin areas where electricity is unavailable.

There is still much to be explored and studied within Solar photovoltaictechnology. It is soon to tell how this technology may truly affect the cold chainand vaccines as a whole.

63

Market Drivers Con’t.

Storage: Concern regarding vaccines in storage facilities is an ever growing concern

according to the Key Opinion Leaders interviewed.

“Stock levels are rarely accurate and it results in too many vaccines lying around inwarehouses where stock is out in places that desperately need it.”

“Some 20-30% of warehouses do not conduct physical stock counts; only a third ofwarehouses have correct stock and only half of those have stock counts in an orderlyfashion.”

Critical Success Factors

65

Critical Success Factors

Areas Examined q In determining the critical success factors of the SmartFridge and Transport

Container, Harrison Hayes took into account:

§ Features and Benefits

§ Overall Construction

§ Financial Component

§ Supply Chain Elements

§ Wastage Reduction

§ Potential Partnerships

66

Critical Success Factors - Features

Features Sought by Key Opinion Leaders (Stack Ranking)

RFID/Barcode Tracking

Adjustable temperature zones

Data collection interface

Data monitoring software

Defrost /condensation removal

Alarms

Remote monitoring

Easy to use/visual controls

Battery back-up

Security option

67

Critical Success Factors - Features

Features Sought by Key Opinion Leaders: KOL Commentary

Tracking vaccines via RFID or barcodes is extremely important to the KeyOpinion Leaders, especially due to the overall cost.

Temperature monitoring and controls were important to the Key OpinionLeaders especially while in transport and while in refrigerators.

Key Opinion Leaders believed that with temperature control and remotemonitoring they could better prevent freezing and over-heating.

68

Critical Success Factors - Features

Key Opinion Leader Feedback

A majority of the interviewed Key Opinion Leaders felt that the SmartFridgeneeded multiple compartments with segmented temperature controls;this would be a key differentiator from current vaccine storage models.

Three sizes would be ideal: One big storage unit, intermediate unit, and asmall unit.

69

Critical Success Factors - Features

Notable Features and Benefits:

Alarm system – must be known if a vaccine/drug becomes too hot or too cold The alarms may either be audible or visual

There is a need for manual or automatic defrost technology Manual defrost is the preferred method

Easy to read display panels that can be manipulated

It would be preferred if product is cooled from the top down

70

Critical Success Factors - Features

SmartFridge Example:

RFID Software that locates vaccines.

Internal cameras that link with visual panelsor smartphones – see inside without openingthe refrigerator.

Capacity data and information

Cooling controls and protocol

71

Critical Success Factors - Benefits

Key Benefits Sought by the SmartFridge/Transport Container:

Easy of tracking supply usage

Reduce Manual process

Reduction of stock-outs

Measurable return on investment

Accuracy in billing

Standardize inventory

Mistake reduction

Efficient workflow

72

Critical Success Factors - Financial

Financial Component: Key Opinion Leaders were skeptical of the potential revenues and cost savings

component of the SmartFridge and Transport Container.

It was most commonly noted that revenues can come from the manufacturers andnot the market. Manufacturers should compensate users for the units so that itwould make financial sense and be embraced by the market.

In pediatric offices, cost savings must be clearly shown. “I do not want to spendmoney on something that cannot show a return on investment.”

In order to be successful in the pediatric market, Key Opinion Leaders stated thata reduction in wastage should be at least 25%.

73

Critical Success Factors – Supply Chain

Inventory Control

The inventory control component was viewed by Key Opinion Leaders asparticularly important.

“I think the big issue is the whole inventory control management within cold chain. If inventory control could be added to a “SmartFridge,” that would make it extremely attractive. Everything from reimbursement to patient coding, I could go on and on. Add to that any type of tag/barcode, that would be a very effective solution that I would really like to see.”

74

Critical Success Factors – Supply Chain

In the Supply Chain: It is critically important that the SmartFridge and Transport Container easily

assimilate into the existing supply chain. This was echoed with the introductionof new vaccines.

“Manufacturers should consider vaccine quantity impact packaging beforedesigning vaccines and introducing them into unfamiliar areas with limitedresources.”

Within the supply chain, transport containers and cooling systems must bereliable. The current “solutions” are not very good according to the Key OpinionLeaders interviewed.

“Cold storage must be reliable and transportable. Think of all the places thatvaccines are shipped where it can be damaged, exposed to light, or with greattemperature fluctuations.”

75

Critical Success Factors – Supply Chain & Partnership

Automation and Supply Chain: “An ideal solution would have a digital management system that automated the re-

ordering system and also handle reimbursement. If we could eliminate paperworkand simplify everything for doctors and nurses, in combination with a reduction inwastage, this may be worth the investment.”

Several Key Opinion Leaders responded similarly and stated that there may be anopportunity for the SmartFridge to be similar to a Automation System that isprovided by McKesson or CareFusion.

Potential Designs

77

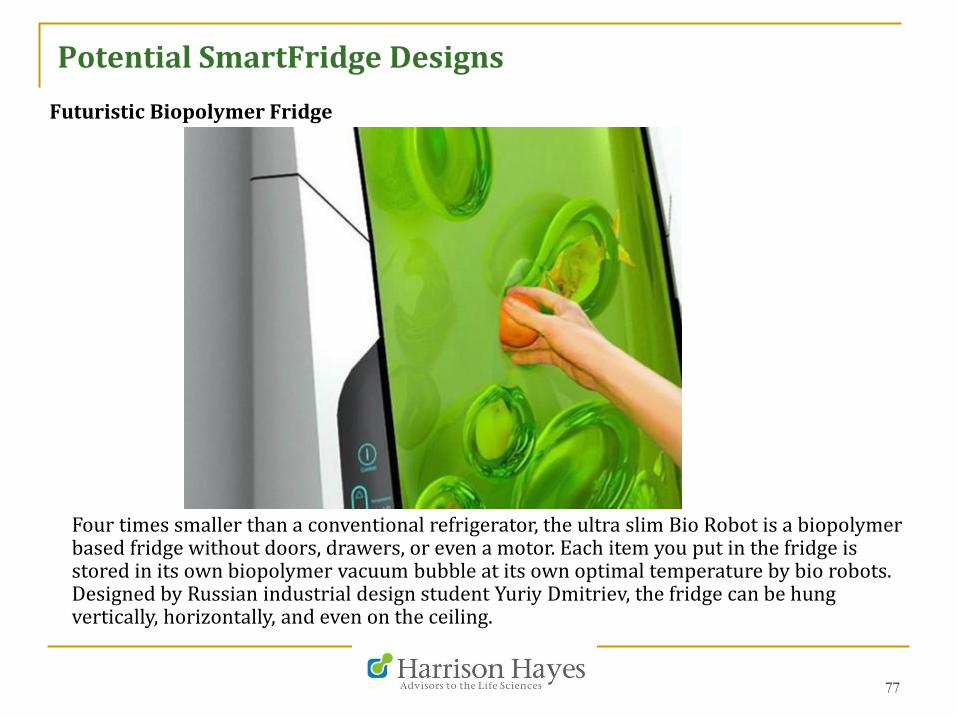

Potential SmartFridge Designs

Futuristic Biopolymer Fridge

Four times smaller than a conventional refrigerator, the ultra slim Bio Robot is a biopolymer based fridge without doors, drawers, or even a motor. Each item you put in the fridge is stored in its own biopolymer vacuum bubble at its own optimal temperature by bio robots. Designed by Russian industrial design student Yuriy Dmitriev, the fridge can be hung vertically, horizontally, and even on the ceiling.

78

Potential SmartFridge Designs

Smart Fridge Concept

Smart Fridge is a concept that turns your fridge into a trust-worthy cooking companion. The fridge can track the ingredients available inside it, make a menu list of all that can be prepared with the available ingredients, and give a step-by-step instruction of the dish being prepared. The Smart Fridge also tells you when you are running low on a particular ingredient. The concept was conceived by Ashley Legg, while the visual impressions of the gadget were done by Yanko Designs.

79

Potential SmartFridge Designs

IceCloud Fridge

IceCloud Fridge by Fanni Csernátony is a futuristic makeover of Nigeria’s zeer pot for the year 2050 when space, energy and water will be our most precious treasures. The fridge uses evaporating water to keep things cool naturally. The hanging structure makes it perfect choice for houses with limited space.

80

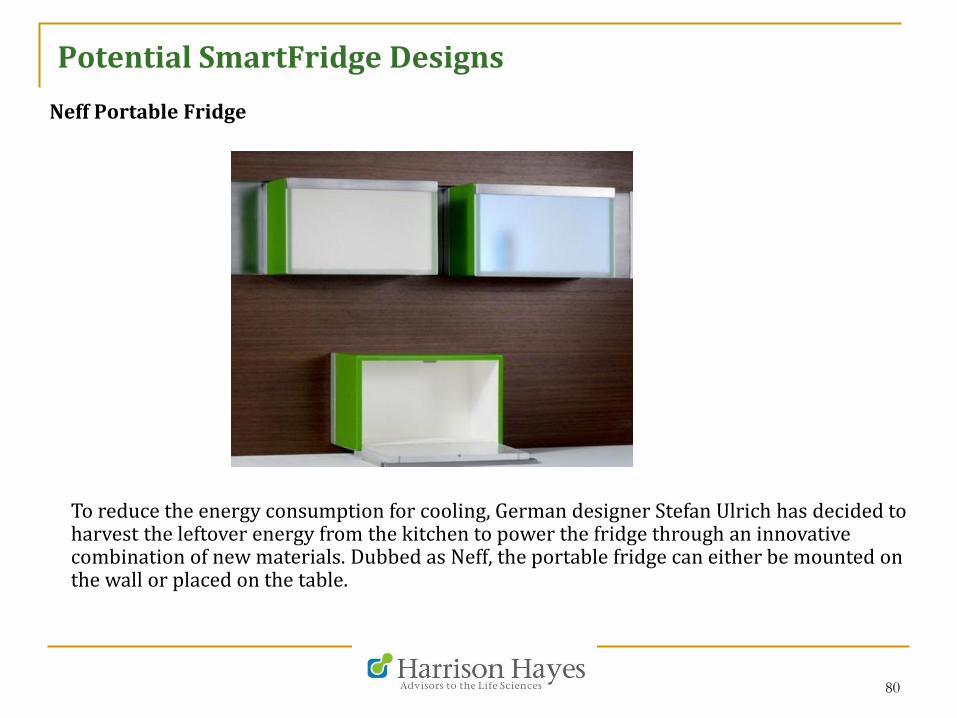

Potential SmartFridge Designs

Neff Portable Fridge

To reduce the energy consumption for cooling, German designer Stefan Ulrich has decided to harvest the leftover energy from the kitchen to power the fridge through an innovative combination of new materials. Dubbed as Neff, the portable fridge can either be mounted on the wall or placed on the table.

81

Potential SmartFridge Designs

Electrolux Flatshare Fridge

The Lego-like fridge design is Stefan Buchberger’s solution to the food conflict between roommates who share one fridge. The Flatshare fridge consists of up to four stackable modules on top of a base station which allows each roommate to have his or her own secure and secluded refrigerator space. Each module can be further customized with add-ons like bottle openers or a whiteboard.

82

Potential SmartFridge Designs

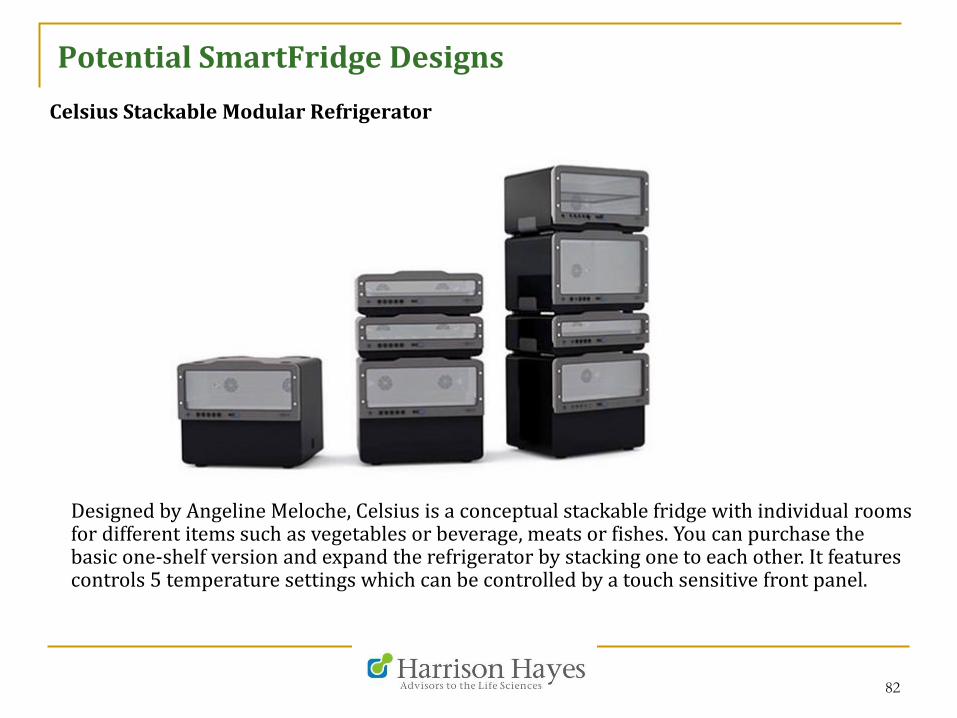

Celsius Stackable Modular Refrigerator

Designed by Angeline Meloche, Celsius is a conceptual stackable fridge with individual rooms for different items such as vegetables or beverage, meats or fishes. You can purchase the basic one-shelf version and expand the refrigerator by stacking one to each other. It features controls 5 temperature settings which can be controlled by a touch sensitive front panel.

83

Potential SmartFridge Designs

Koolie Shopping Cart Fridge

Koolie is a space-saving fridge design which doubles as a shopping cart or a picnic basket. The fridge features a built-in RFID field that detects all the new food items placed inside and charges a predefined credit or debit card automatically when you leave the store through cashier gates.

84

Potential SmartFridge Designs

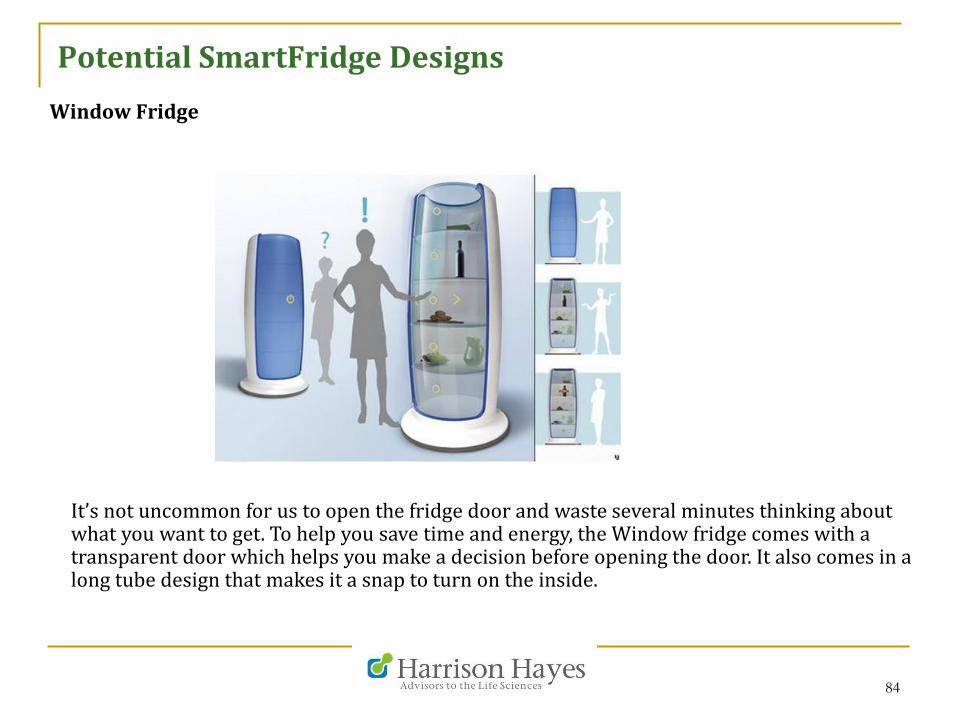

Window Fridge

It’s not uncommon for us to open the fridge door and waste several minutes thinking about what you want to get. To help you save time and energy, the Window fridge comes with a transparent door which helps you make a decision before opening the door. It also comes in a long tube design that makes it a snap to turn on the inside.

Key Takeaways and Recommendations

86

Key Takeaways

Key Takeaways for the SmartFridge and Transport Container

There is a clear need for improvement in the cold chain.

SmartFridge would be of great value on a global basis.

The Transport Container seems to have more applicability in developingcountries.

The SmartFridge/Transport Container must be easily assimilated into theoverall vaccine supply chain.

Several key features must be included.

87

Recommendations

Recommendation I - WHO

It is imperative that the Vaccine SmartFridge and Transport Container meet theWorld Health Organizations Performance, Quality, and Safety Standards sheet.

Meeting these standards is extremely important when selling/leasing devicesinternationally and specifically to UNICEF.

88

Recommendations

Recommendation II – More Research is Needed

Ø Harrison Hayes recommends to conduct additional research to specifically examine SmartFridge and Transport Container size. This is especially true in developing countries.

Ø Harrison Hayes recommends technologies outside of the Peltier Element be explored. There was an overwhelming negative reaction to this type of technology.

89

Recommendations

Recommendation III – Features to be Included

There are several features that must be included.

Remote temperature monitors

Visual and Audio Alarms (temperature related)

RFID System

Different temperature zones

90

Recommendations

Recommendation IV – Find a Partner

Ø It was extremely important to Key Opinion Leaders that the SmartFridge and Transport Container be automated.

Ø A specialized, automation partner would be of great benefit in developing this type of system.

Ø Potential partners may be McKesson (Robot-Rx technology) or CareFusion with Pyxis technology.

Ø “Mini-Bar” may also be a viable partner, but would not be as respected as a McKesson or CareFusion.

91

Recommendations

Recommendation V – Proof of Technology

Ø Proof of concept must show that it will reduce vaccine wastage by an absolute minimum of 25%.

Ø 25% appears to be the threshold for market viability on a global basis.

Ø The dollar amount of this will vary depending on the vaccine.

Ø Proof of technology must also show that it will save time for nurses and physicians.

92

Recommendations

Recommendation VI – Entering the Market

Ø Harrison Hayes would recommend a “phased” approach to entering the market.

Ø In the United States the pediatric space is the initial target audience and appear to serve as the “early adopters.”

Ø Dermatology offices represent a secondary market.

Ø Assuming the cold chain solution reduces cost and wastage, a national roll-out to pharmacies and general practitioners would be advised.

Ø Company should develop a Leasing Option for domestic customers.

Ø Globally, a partnership with PATH and UNICEF must be created in regard to the cold chain solution.

About Harrison Hayes

94

About Harrison Hayes

Harrison Hayes is a strategic consulting firm to the life, chemical, and material science industries. Specific areas of expertise reside in our unique and proprietary research methodologies that support strategic and tactical decision making processes for our clients.

![Complex Variable Interest Entity [sanitized]](https://img.dokumen.tips/doc/110x75/58ecd6c41a28ab877f8b458d/complex-variable-interest-entity-sanitized.jpg)