Embed Size (px)

Citation preview

Black & Veatch Insights Group

2017 STRATEGIC DIRECTIONS: SMART CITY/SMART UTILITY REPORT SURVEY RESULTS

30 January 2017Questions: [email protected]

Download the full report at www.bv.com/reports.

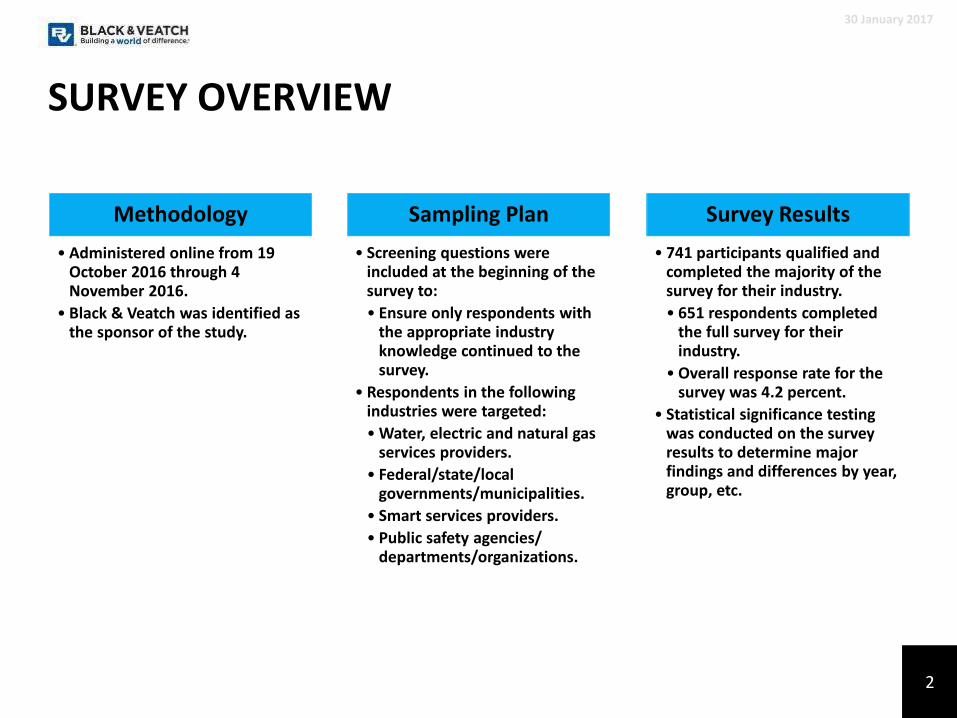

SURVEY OVERVIEW

30 January 2017

Methodology

• Administered online from 19 October 2016 through 4 November 2016.

• Black & Veatch was identified as the sponsor of the study.

Sampling Plan

• Screening questions were included at the beginning of the survey to:

• Ensure only respondents with the appropriate industry knowledge continued to the survey.

• Respondents in the following industries were targeted:

• Water, electric and natural gas services providers.

• Federal/state/local governments/municipalities.

• Smart services providers.

• Public safety agencies/ departments/organizations.

Survey Results

• 741 participants qualified and completed the majority of the survey for their industry.

• 651 respondents completed the full survey for their industry.

• Overall response rate for the survey was 4.2 percent.

• Statistical significance testing was conducted on the survey results to determine major findings and differences by year, group, etc.

2

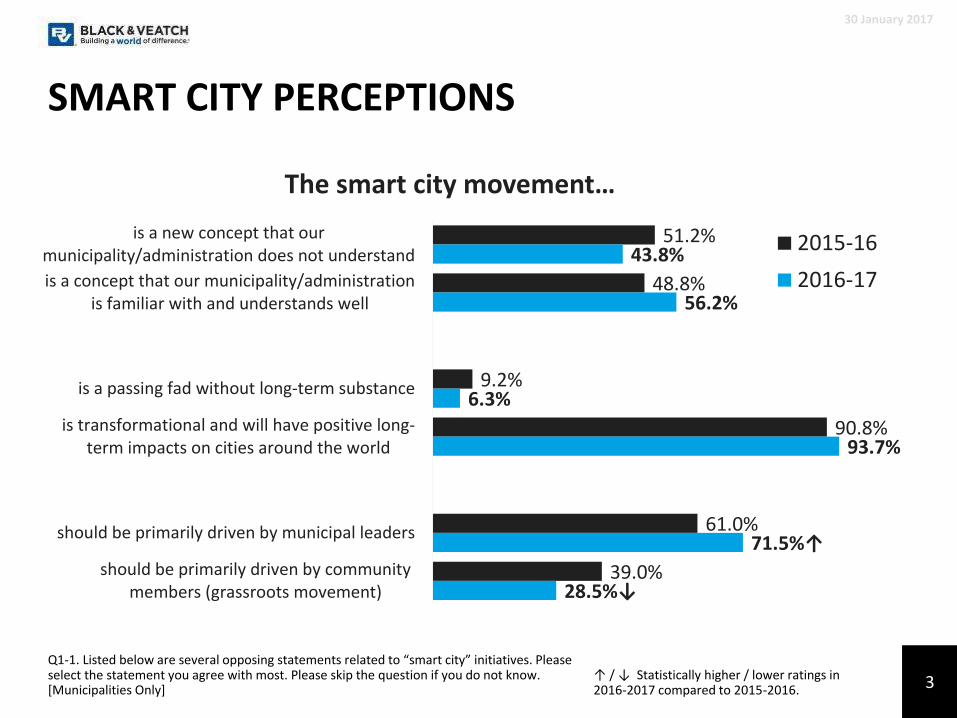

SMART CITY PERCEPTIONS

30 January 2017

↑ / ↓ Statistically higher / lower ratings in 2016-2017 compared to 2015-2016.

Q1-1. Listed below are several opposing statements related to “smart city” initiatives. Please select the statement you agree with most. Please skip the question if you do not know. [Municipalities Only]

51.2%

48.8%

9.2%

90.8%

61.0%

39.0%

43.8%

56.2%

6.3%

93.7%

71.5%↑

28.5%↓

is a new concept that ourmunicipality/administration does not understand

is a concept that our municipality/administrationis familiar with and understands well

is a passing fad without long-term substance

is transformational and will have positive long-term impacts on cities around the world

should be primarily driven by municipal leaders

should be primarily driven by communitymembers (grassroots movement)

The smart city movement…

2015-16

2016-17

3

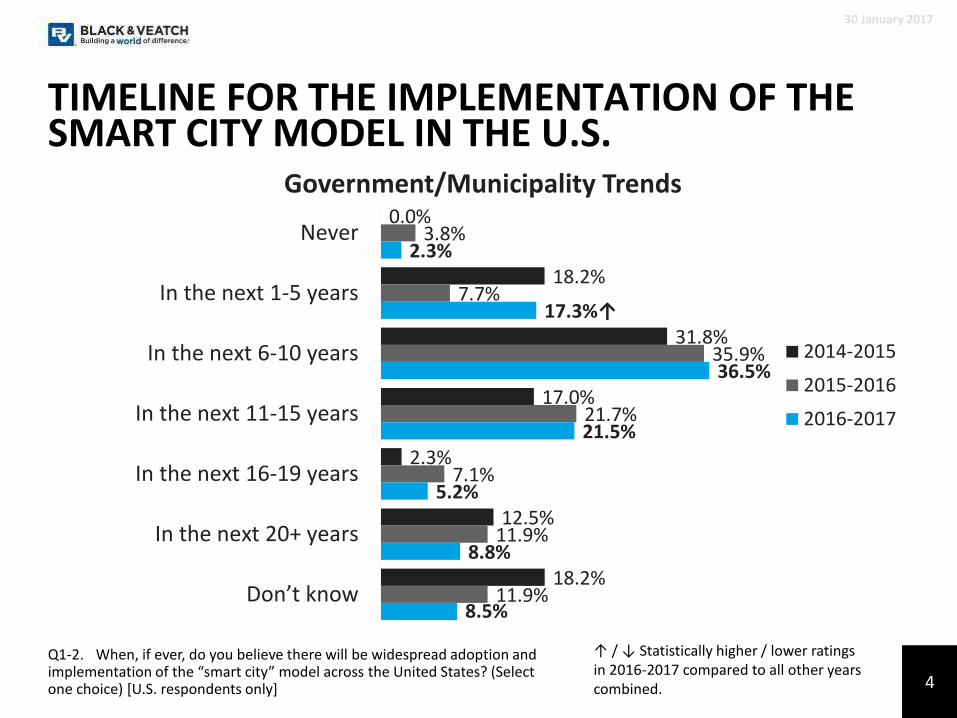

0.0%

18.2%

31.8%

17.0%

2.3%

12.5%

18.2%

3.8%

7.7%

35.9%

21.7%

7.1%

11.9%

11.9%

2.3%

17.3%↑

36.5%

21.5%

5.2%

8.8%

8.5%

Never

In the next 1-5 years

In the next 6-10 years

In the next 11-15 years

In the next 16-19 years

In the next 20+ years

Don’t know

Government/Municipality Trends

2014-2015

2015-2016

2016-2017

TIMELINE FOR THE IMPLEMENTATION OF THE SMART CITY MODEL IN THE U.S.

30 January 2017

↑ / ↓ Statistically higher / lower ratings in 2016-2017 compared to all other years combined.

Q1-2. When, if ever, do you believe there will be widespread adoption and implementation of the “smart city” model across the United States? (Select one choice) [U.S. respondents only] 4

12%

36%

25%

56%

49%

54%

18%

12%

14%

14%

3%

7%

0% 20% 40% 60% 80% 100%

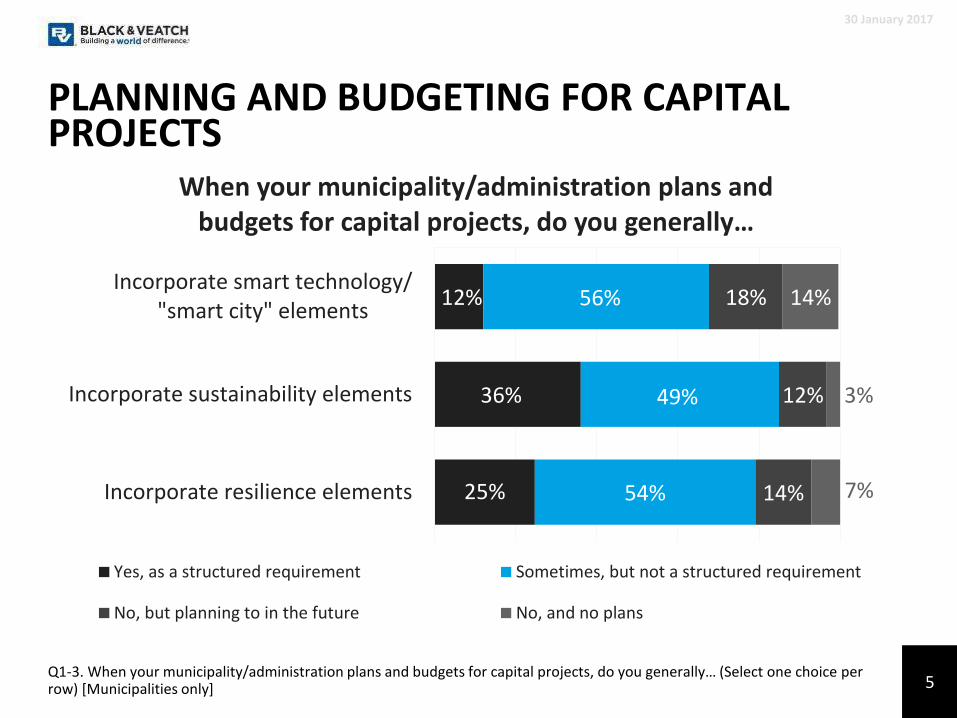

Incorporate smart technology/"smart city" elements

Incorporate sustainability elements

Incorporate resilience elements

When your municipality/administration plans and budgets for capital projects, do you generally…

Yes, as a structured requirement Sometimes, but not a structured requirement

No, but planning to in the future No, and no plans

PLANNING AND BUDGETING FOR CAPITAL PROJECTS

30 January 2017

Q1-3. When your municipality/administration plans and budgets for capital projects, do you generally… (Select one choice per row) [Municipalities only] 5

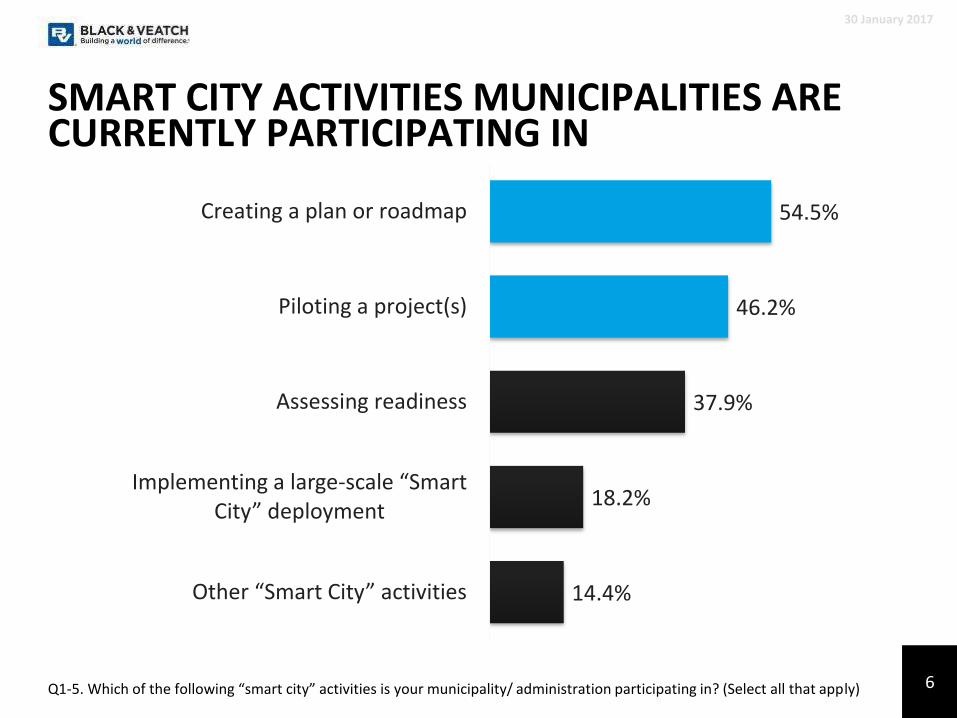

SMART CITY ACTIVITIES MUNICIPALITIES ARE CURRENTLY PARTICIPATING IN

30 January 2017

Q1-5. Which of the following “smart city” activities is your municipality/ administration participating in? (Select all that apply)

54.5%

46.2%

37.9%

18.2%

14.4%

Creating a plan or roadmap

Piloting a project(s)

Assessing readiness

Implementing a large-scale “Smart City” deployment

Other “Smart City” activities

6

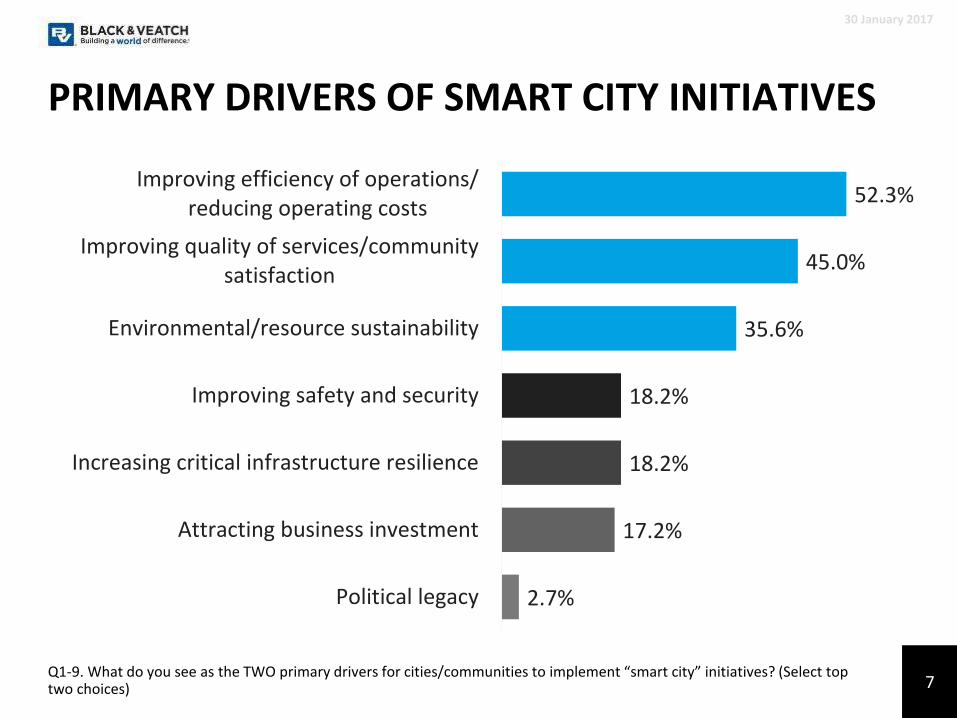

PRIMARY DRIVERS OF SMART CITY INITIATIVES

30 January 2017

Q1-9. What do you see as the TWO primary drivers for cities/communities to implement “smart city” initiatives? (Select top two choices)

52.3%

45.0%

35.6%

18.2%

18.2%

17.2%

2.7%

Improving efficiency of operations/reducing operating costs

Improving quality of services/communitysatisfaction

Environmental/resource sustainability

Improving safety and security

Increasing critical infrastructure resilience

Attracting business investment

Political legacy

7

MOST CRITICAL BUILDING BLOCKS OF A SMART COMMUNITY

30 January 2017

Q1-13. Beyond the foundational physical infrastructure, which of the following do you feel are the TOP THREE most critical building blocks of a “smart city”/“smart community?” (Select three choices)

47.9%

46.3%

39.0%

38.7%

35.1%

31.3%

31.0%

Integrated data repository/datamanagement system

“Smart City” plan/roadmap

Automation and control systems

Customer/citizen engagementplatforms or apps

Networks of smart sensors

Data visualization and analytics

Ubiquitous wide-area connectivity

8

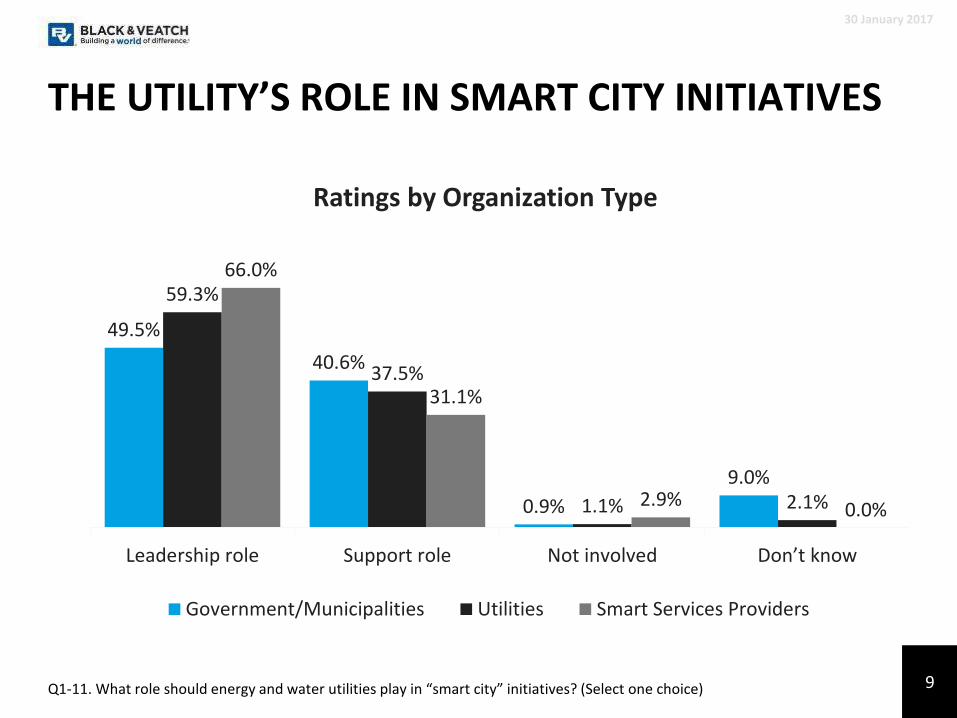

THE UTILITY’S ROLE IN SMART CITY INITIATIVES

30 January 2017

Q1-11. What role should energy and water utilities play in “smart city” initiatives? (Select one choice)

49.5%

40.6%

0.9%

9.0%

59.3%

37.5%

1.1% 2.1%

66.0%

31.1%

2.9% 0.0%

Leadership role Support role Not involved Don’t know

Ratings by Organization Type

Government/Municipalities Utilities Smart Services Providers

9

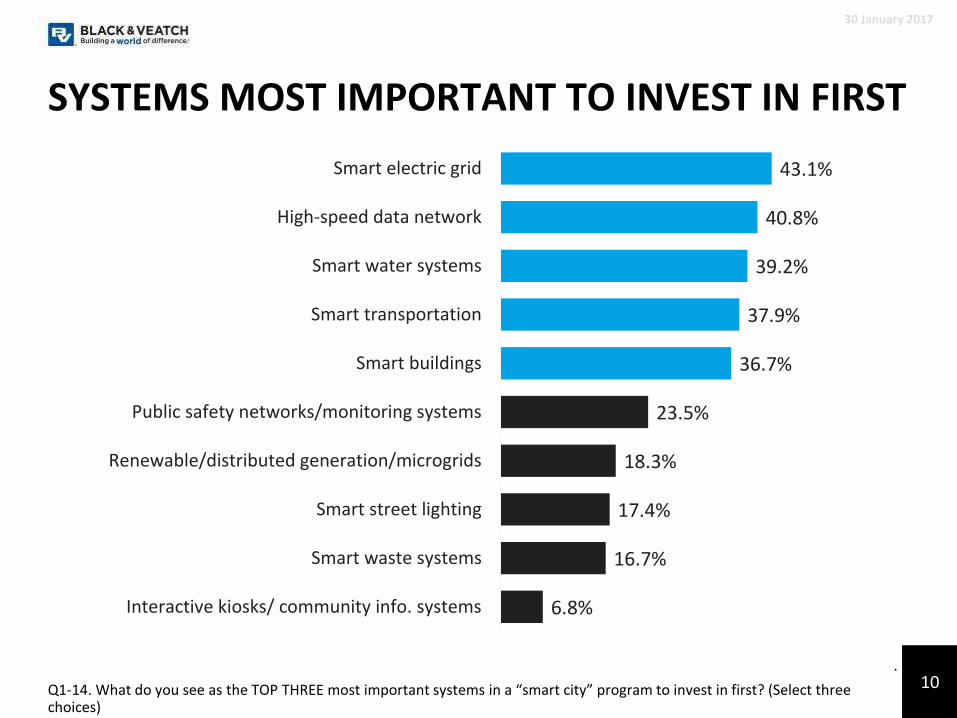

SYSTEMS MOST IMPORTANT TO INVEST IN FIRST

30 January 2017

Q1-14. What do you see as the TOP THREE most important systems in a “smart city” program to invest in first? (Select three choices)

.

43.1%

40.8%

39.2%

37.9%

36.7%

23.5%

18.3%

17.4%

16.7%

6.8%

Smart electric grid

High-speed data network

Smart water systems

Smart transportation

Smart buildings

Public safety networks/monitoring systems

Renewable/distributed generation/microgrids

Smart street lighting

Smart waste systems

Interactive kiosks/ community info. systems

10

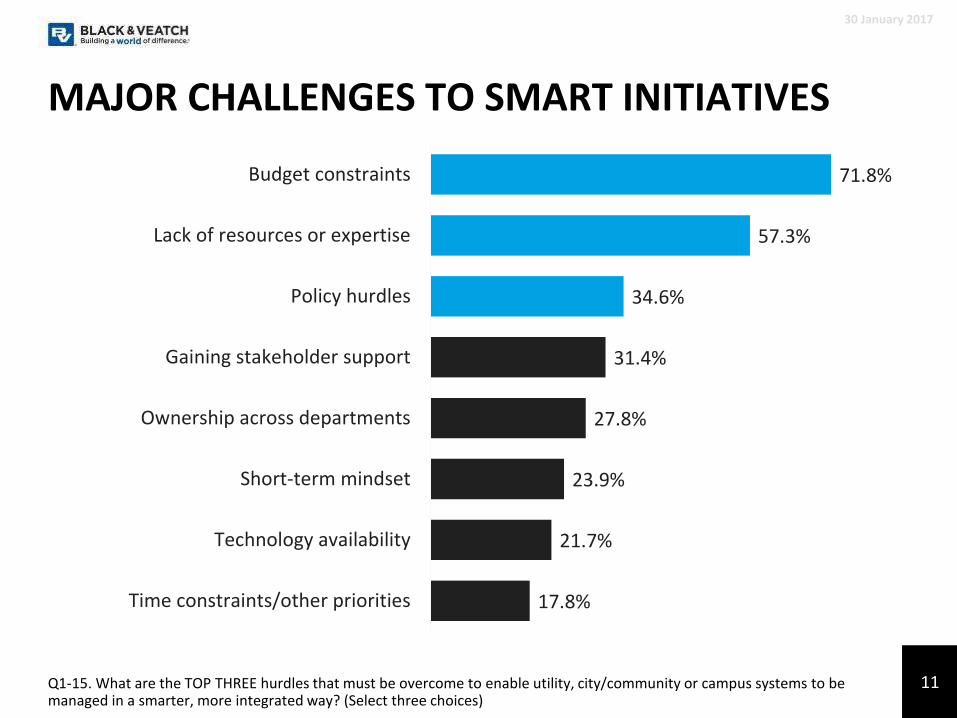

MAJOR CHALLENGES TO SMART INITIATIVES

30 January 2017

Q1-15. What are the TOP THREE hurdles that must be overcome to enable utility, city/community or campus systems to be managed in a smarter, more integrated way? (Select three choices)

71.8%

57.3%

34.6%

31.4%

27.8%

23.9%

21.7%

17.8%

Budget constraints

Lack of resources or expertise

Policy hurdles

Gaining stakeholder support

Ownership across departments

Short-term mindset

Technology availability

Time constraints/other priorities

11

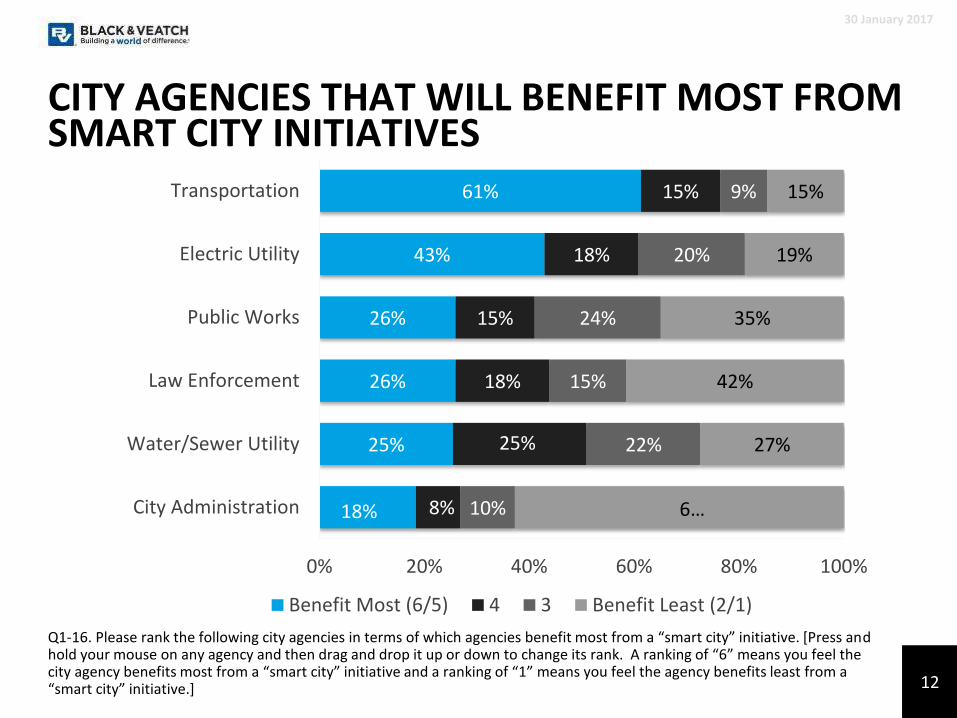

CITY AGENCIES THAT WILL BENEFIT MOST FROM SMART CITY INITIATIVES

30 January 2017

Q1-16. Please rank the following city agencies in terms of which agencies benefit most from a “smart city” initiative. [Press and hold your mouse on any agency and then drag and drop it up or down to change its rank. A ranking of “6” means you feel the city agency benefits most from a “smart city” initiative and a ranking of “1” means you feel the agency benefits least from a“smart city” initiative.]

18%

25%

26%

26%

43%

61%

8%

25%

18%

15%

18%

15%

10%

22%

15%

24%

20%

9%

6…

27%

42%

35%

19%

15%

0% 20% 40% 60% 80% 100%

City Administration

Water/Sewer Utility

Law Enforcement

Public Works

Electric Utility

Transportation

Benefit Most (6/5) 4 3 Benefit Least (2/1)

12

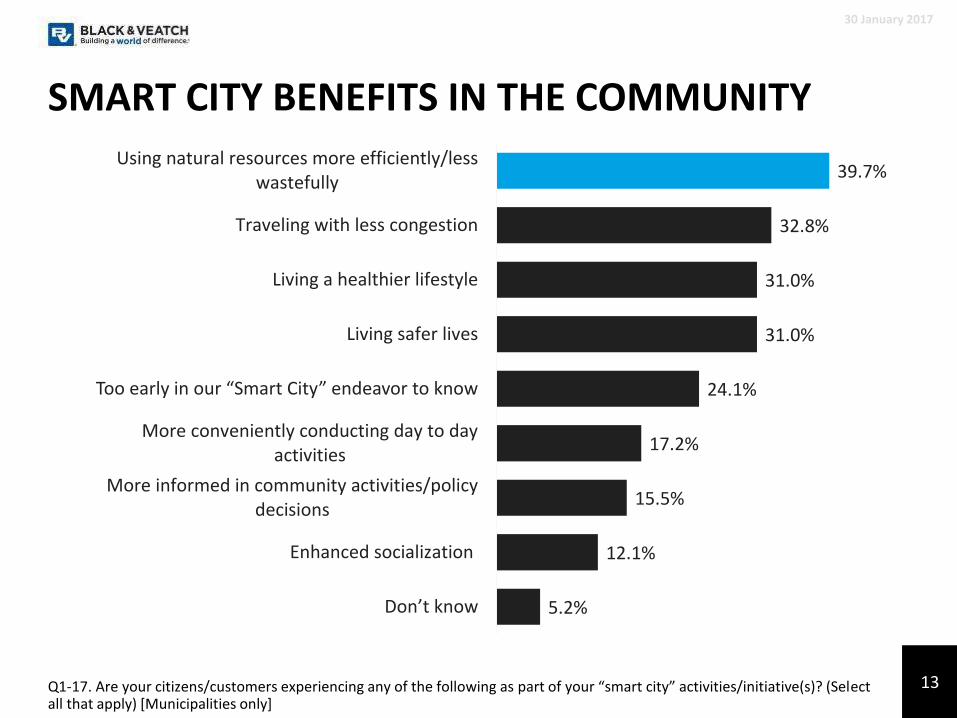

SMART CITY BENEFITS IN THE COMMUNITY

30 January 2017

Q1-17. Are your citizens/customers experiencing any of the following as part of your “smart city” activities/initiative(s)? (Select all that apply) [Municipalities only]

39.7%

32.8%

31.0%

31.0%

24.1%

17.2%

15.5%

12.1%

5.2%

Using natural resources more efficiently/lesswastefully

Traveling with less congestion

Living a healthier lifestyle

Living safer lives

Too early in our “Smart City” endeavor to know

More conveniently conducting day to dayactivities

More informed in community activities/policydecisions

Enhanced socialization

Don’t know

13

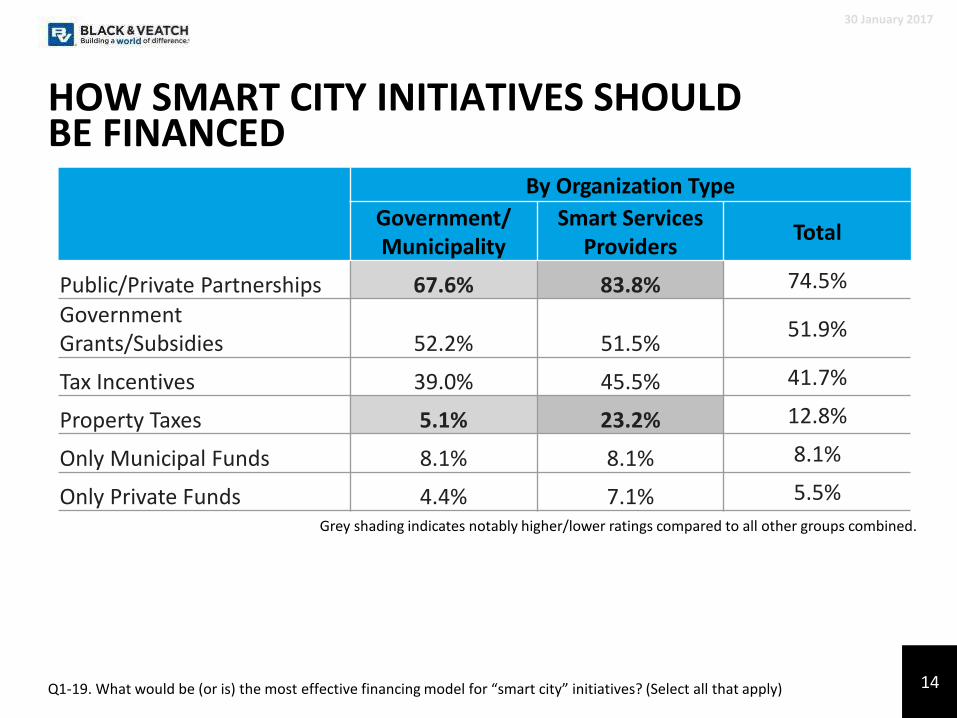

HOW SMART CITY INITIATIVES SHOULD BE FINANCED

30 January 2017

Q1-19. What would be (or is) the most effective financing model for “smart city” initiatives? (Select all that apply)

By Organization Type

Government/Municipality

Smart Services Providers

Total

Public/Private Partnerships 67.6% 83.8% 74.5%

Government Grants/Subsidies 52.2% 51.5%

51.9%

Tax Incentives 39.0% 45.5% 41.7%

Property Taxes 5.1% 23.2% 12.8%

Only Municipal Funds 8.1% 8.1% 8.1%

Only Private Funds 4.4% 7.1% 5.5%

Grey shading indicates notably higher/lower ratings compared to all other groups combined.

14

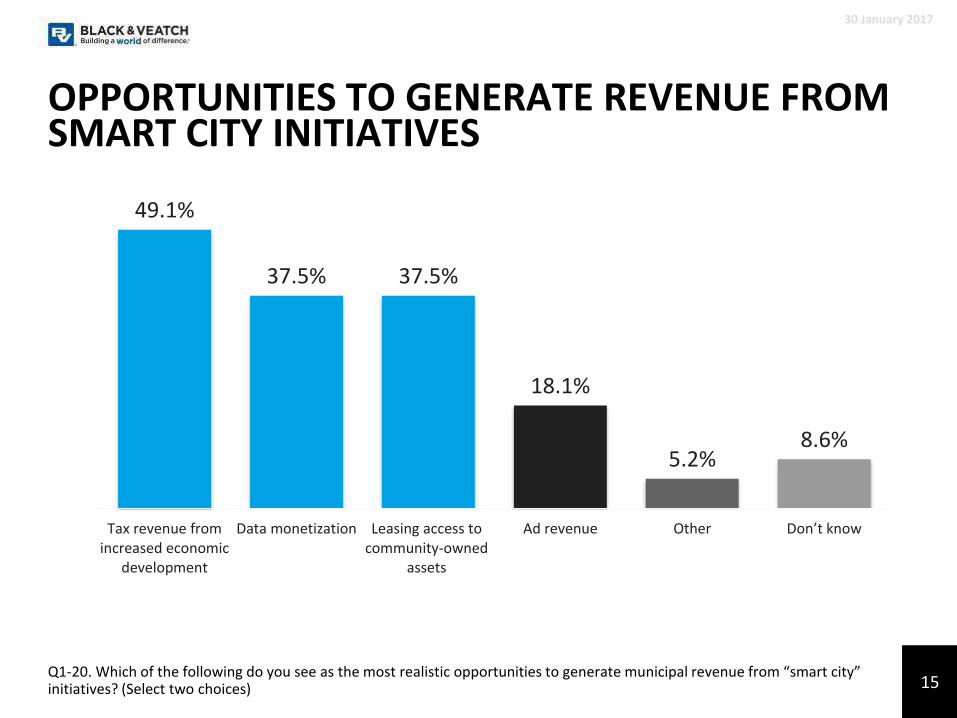

49.1%

37.5% 37.5%

18.1%

5.2%8.6%

Tax revenue fromincreased economic

development

Data monetization Leasing access tocommunity-owned

assets

Ad revenue Other Don’t know

OPPORTUNITIES TO GENERATE REVENUE FROM SMART CITY INITIATIVES

30 January 2017

Q1-20. Which of the following do you see as the most realistic opportunities to generate municipal revenue from “smart city” initiatives? (Select two choices) 15

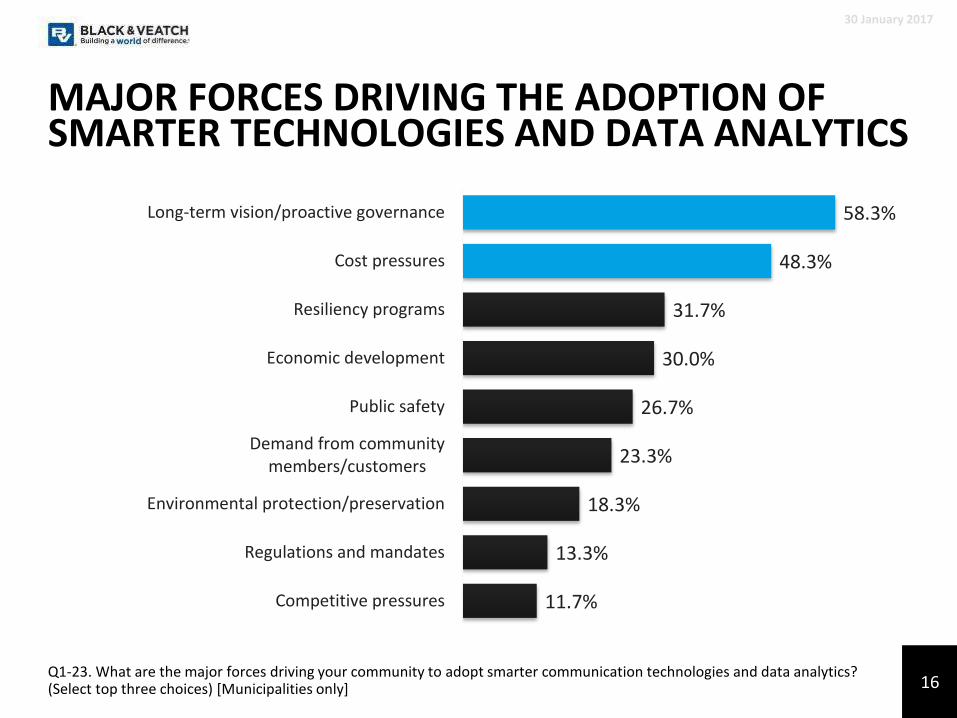

MAJOR FORCES DRIVING THE ADOPTION OF SMARTER TECHNOLOGIES AND DATA ANALYTICS

30 January 2017

Q1-23. What are the major forces driving your community to adopt smarter communication technologies and data analytics? (Select top three choices) [Municipalities only]

58.3%

48.3%

31.7%

30.0%

26.7%

23.3%

18.3%

13.3%

11.7%

Long-term vision/proactive governance

Cost pressures

Resiliency programs

Economic development

Public safety

Demand from communitymembers/customers

Environmental protection/preservation

Regulations and mandates

Competitive pressures

16

66.7%

52.4%

38.1%

9.5%4.8%

9.5%

Personaltransit

Medium-duty/fleets

Electrifiedmass transit

Heavy-duty/trucking

Other None, this isnot a priority

TOP PRIORITIES FOR EXPANDING THE USE OF ELECTRIC VEHICLES

30 January 2017

Q1-29. What are your community’s TOP TWO priorities for expanding the use of electric vehicles (EV)? (Select top two choices) [Municipalities only]

Small number of respondents (n=21)

17

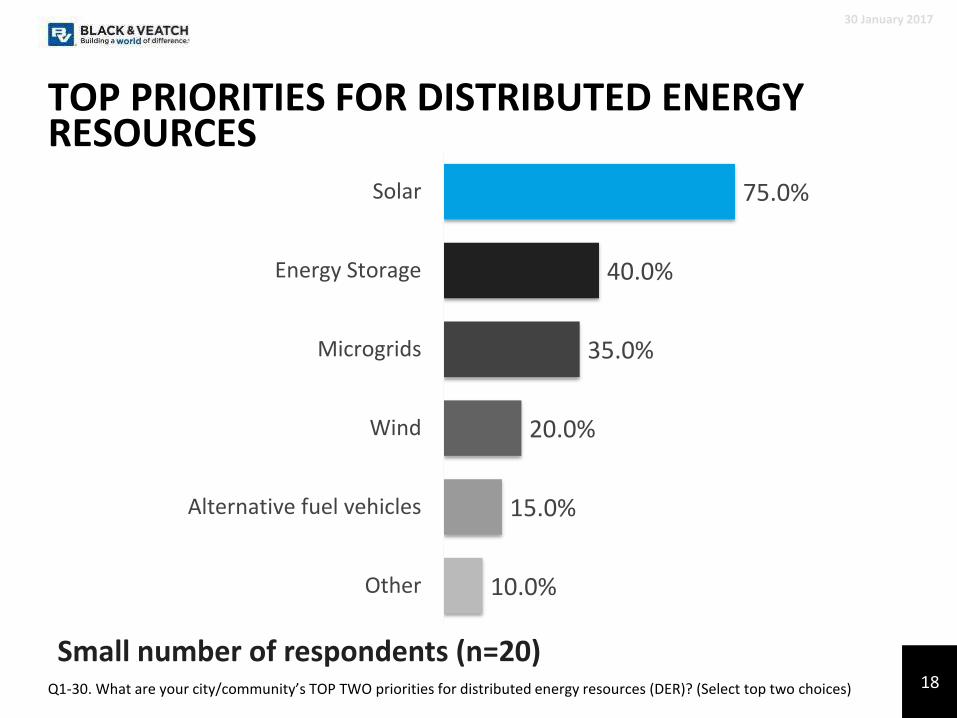

TOP PRIORITIES FOR DISTRIBUTED ENERGY RESOURCES

30 January 2017

Q1-30. What are your city/community’s TOP TWO priorities for distributed energy resources (DER)? (Select top two choices)

75.0%

40.0%

35.0%

20.0%

15.0%

10.0%

Solar

Energy Storage

Microgrids

Wind

Alternative fuel vehicles

Other

Small number of respondents (n=20)18

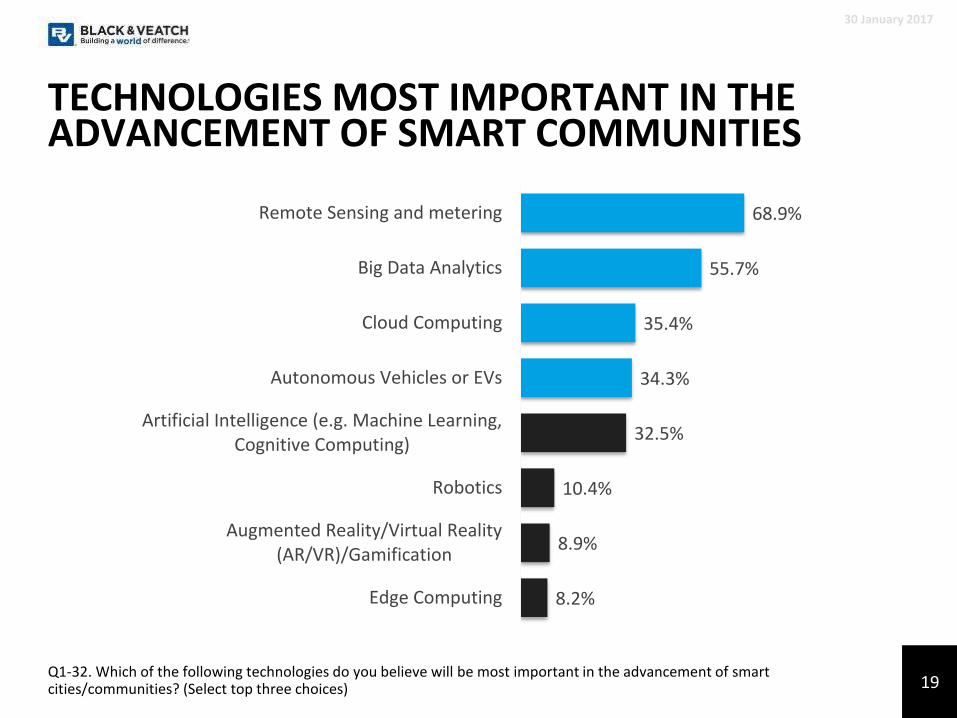

TECHNOLOGIES MOST IMPORTANT IN THE ADVANCEMENT OF SMART COMMUNITIES

30 January 2017

Q1-32. Which of the following technologies do you believe will be most important in the advancement of smart cities/communities? (Select top three choices)

68.9%

55.7%

35.4%

34.3%

32.5%

10.4%

8.9%

8.2%

Remote Sensing and metering

Big Data Analytics

Cloud Computing

Autonomous Vehicles or EVs

Artificial Intelligence (e.g. Machine Learning,Cognitive Computing)

Robotics

Augmented Reality/Virtual Reality(AR/VR)/Gamification

Edge Computing

19

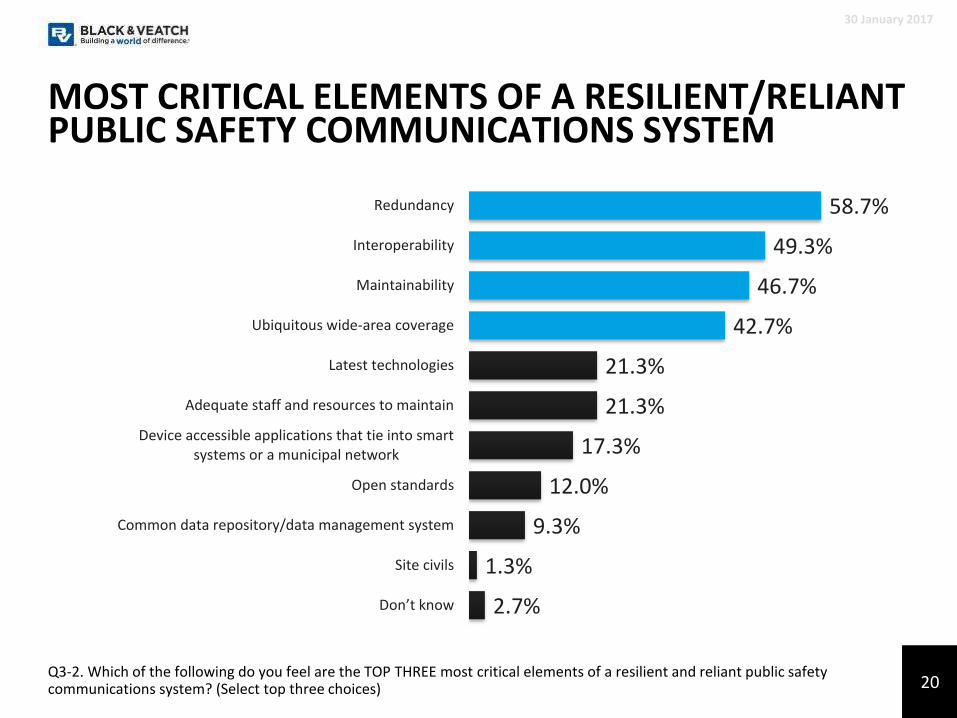

MOST CRITICAL ELEMENTS OF A RESILIENT/RELIANT PUBLIC SAFETY COMMUNICATIONS SYSTEM

30 January 2017

Q3-2. Which of the following do you feel are the TOP THREE most critical elements of a resilient and reliant public safety communications system? (Select top three choices)

58.7%

49.3%

46.7%

42.7%

21.3%

21.3%

17.3%

12.0%

9.3%

1.3%

2.7%

Redundancy

Interoperability

Maintainability

Ubiquitous wide-area coverage

Latest technologies

Adequate staff and resources to maintain

Device accessible applications that tie into smartsystems or a municipal network

Open standards

Common data repository/data management system

Site civils

Don’t know

20

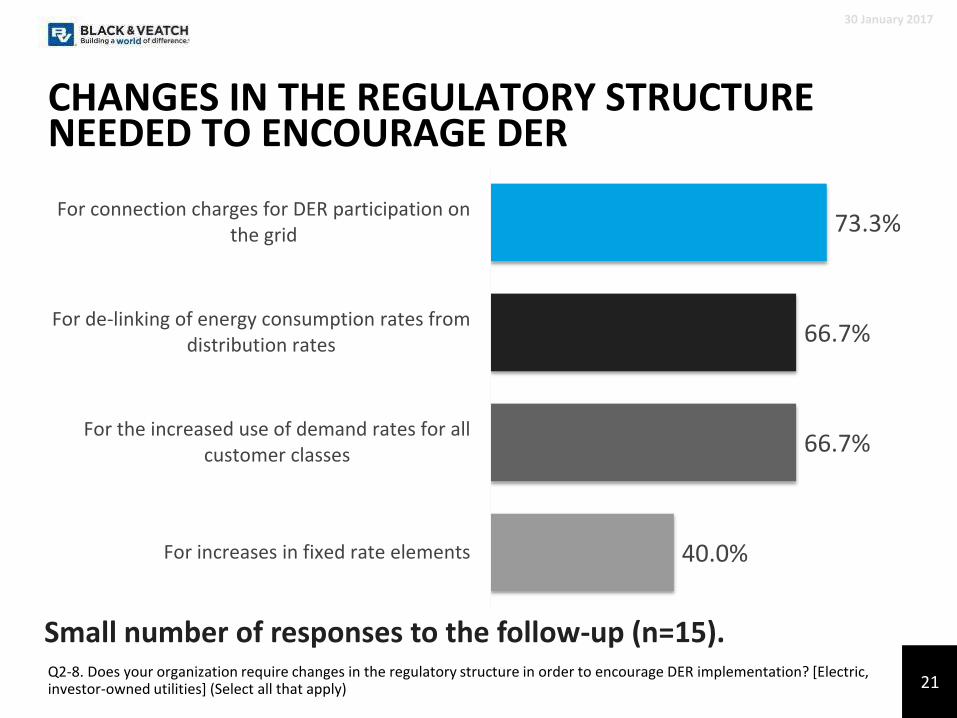

CHANGES IN THE REGULATORY STRUCTURE NEEDED TO ENCOURAGE DER

30 January 2017

21Q2-8. Does your organization require changes in the regulatory structure in order to encourage DER implementation? [Electric, investor-owned utilities] (Select all that apply)

73.3%

66.7%

66.7%

40.0%

For connection charges for DER participation onthe grid

For de-linking of energy consumption rates fromdistribution rates

For the increased use of demand rates for allcustomer classes

For increases in fixed rate elements

Small number of responses to the follow-up (n=15).

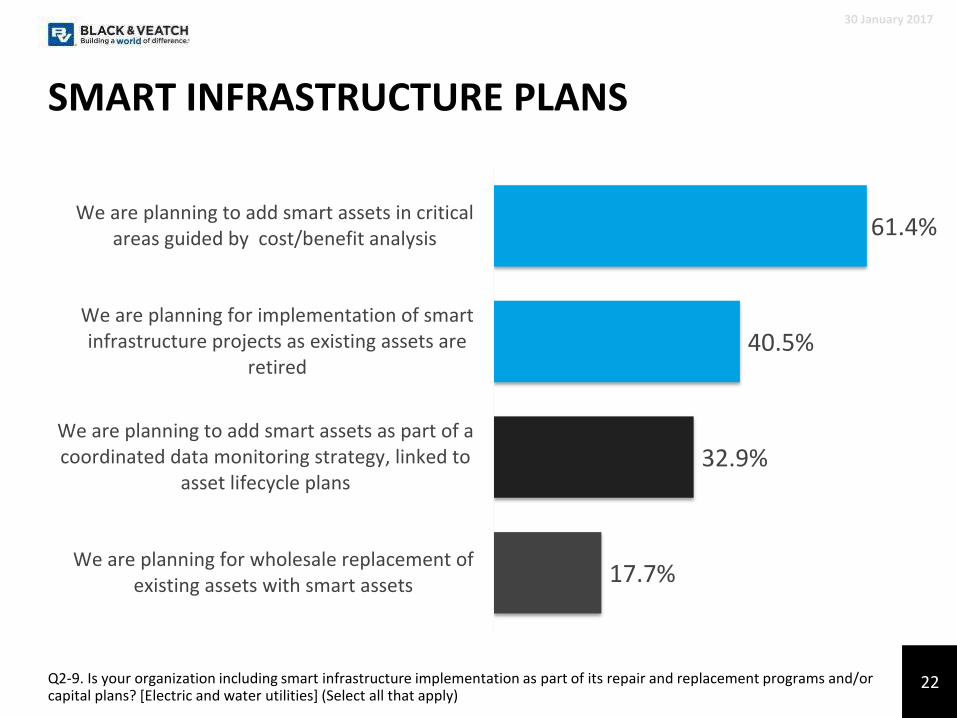

SMART INFRASTRUCTURE PLANS

30 January 2017

22Q2-9. Is your organization including smart infrastructure implementation as part of its repair and replacement programs and/or capital plans? [Electric and water utilities] (Select all that apply)

61.4%

40.5%

32.9%

17.7%

We are planning to add smart assets in criticalareas guided by cost/benefit analysis

We are planning for implementation of smartinfrastructure projects as existing assets are

retired

We are planning to add smart assets as part of acoordinated data monitoring strategy, linked to

asset lifecycle plans

We are planning for wholesale replacement ofexisting assets with smart assets

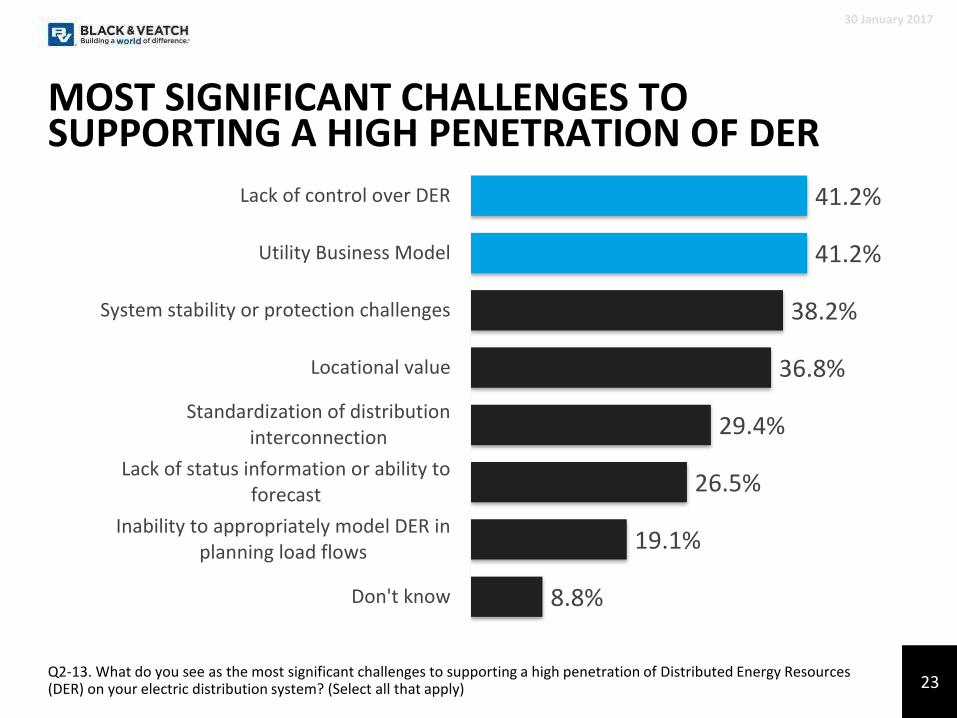

MOST SIGNIFICANT CHALLENGES TO SUPPORTING A HIGH PENETRATION OF DER

30 January 2017

23Q2-13. What do you see as the most significant challenges to supporting a high penetration of Distributed Energy Resources (DER) on your electric distribution system? (Select all that apply)

41.2%

41.2%

38.2%

36.8%

29.4%

26.5%

19.1%

8.8%

Lack of control over DER

Utility Business Model

System stability or protection challenges

Locational value

Standardization of distributioninterconnection

Lack of status information or ability toforecast

Inability to appropriately model DER inplanning load flows

Don't know

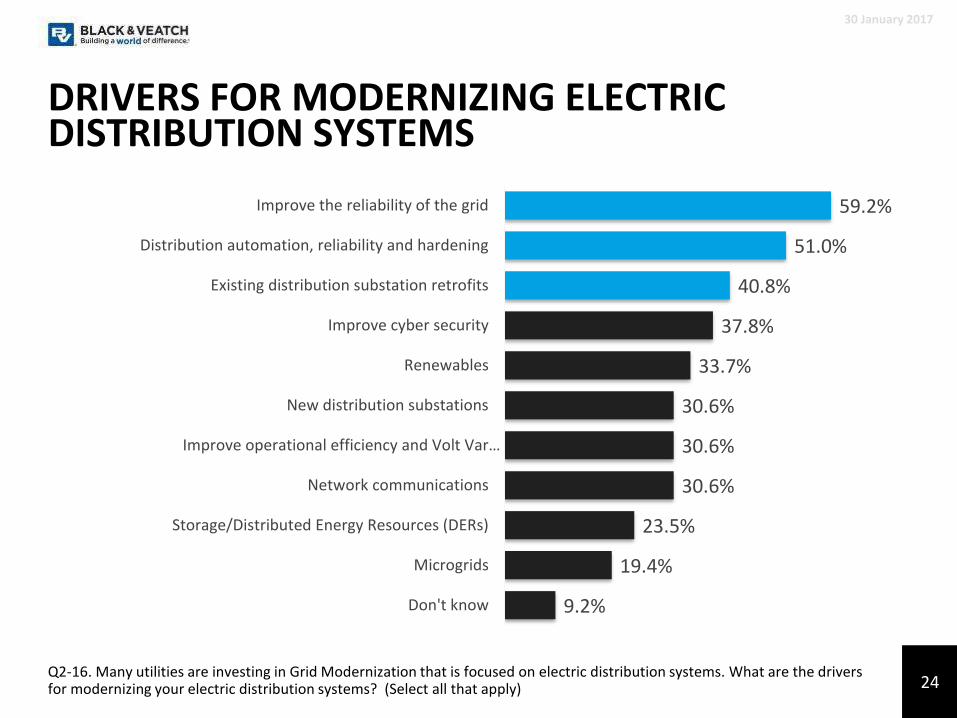

DRIVERS FOR MODERNIZING ELECTRIC DISTRIBUTION SYSTEMS

30 January 2017

24Q2-16. Many utilities are investing in Grid Modernization that is focused on electric distribution systems. What are the driversfor modernizing your electric distribution systems? (Select all that apply)

59.2%

51.0%

40.8%

37.8%

33.7%

30.6%

30.6%

30.6%

23.5%

19.4%

9.2%

Improve the reliability of the grid

Distribution automation, reliability and hardening

Existing distribution substation retrofits

Improve cyber security

Renewables

New distribution substations

Improve operational efficiency and Volt Var…

Network communications

Storage/Distributed Energy Resources (DERs)

Microgrids

Don't know

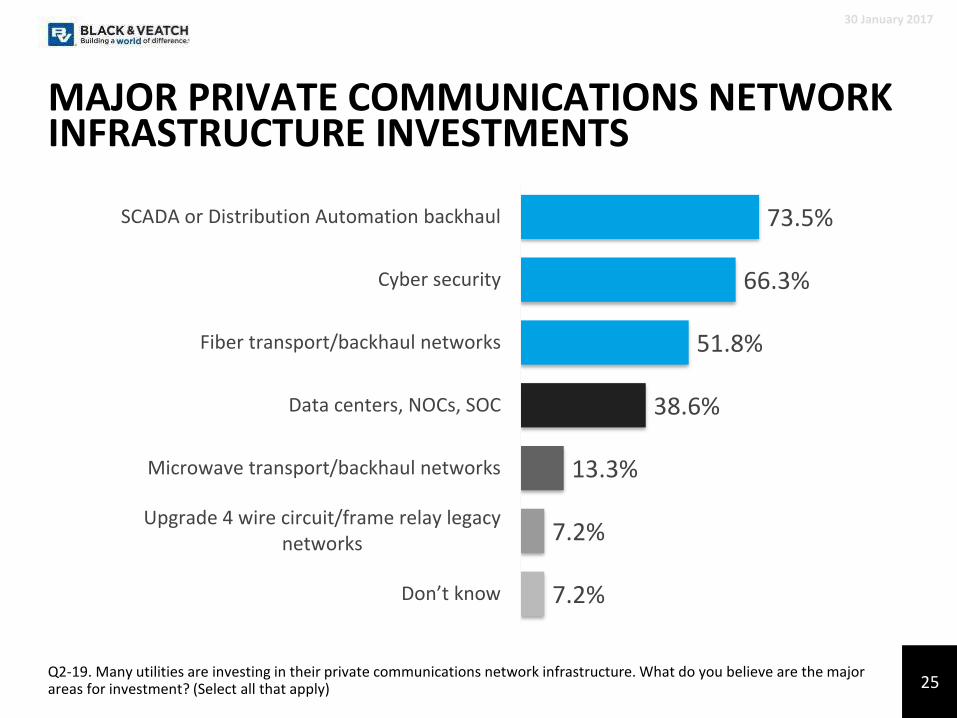

MAJOR PRIVATE COMMUNICATIONS NETWORK INFRASTRUCTURE INVESTMENTS

30 January 2017

25Q2-19. Many utilities are investing in their private communications network infrastructure. What do you believe are the major areas for investment? (Select all that apply)

73.5%

66.3%

51.8%

38.6%

13.3%

7.2%

7.2%

SCADA or Distribution Automation backhaul

Cyber security

Fiber transport/backhaul networks

Data centers, NOCs, SOC

Microwave transport/backhaul networks

Upgrade 4 wire circuit/frame relay legacynetworks

Don’t know

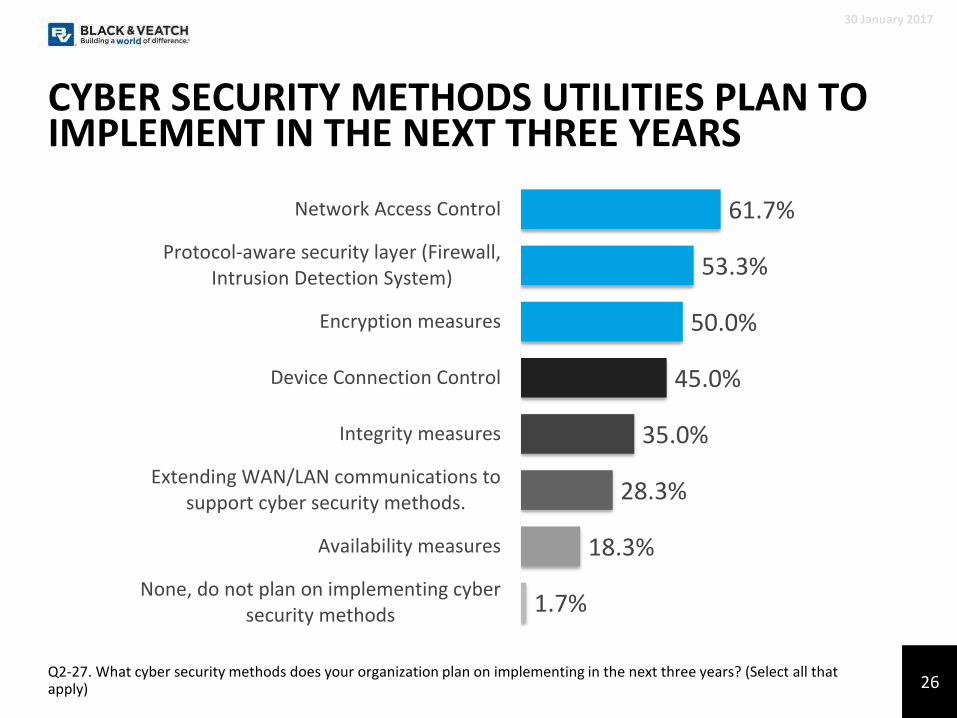

CYBER SECURITY METHODS UTILITIES PLAN TO IMPLEMENT IN THE NEXT THREE YEARS

30 January 2017

26Q2-27. What cyber security methods does your organization plan on implementing in the next three years? (Select all that apply)

61.7%

53.3%

50.0%

45.0%

35.0%

28.3%

18.3%

1.7%

Network Access Control

Protocol-aware security layer (Firewall,Intrusion Detection System)

Encryption measures

Device Connection Control

Integrity measures

Extending WAN/LAN communications tosupport cyber security methods.

Availability measures

None, do not plan on implementing cybersecurity methods

Black & Veatch Insights Group

2017 STRATEGIC DIRECTIONS: SMART CITY/SMART UTILITY REPORT SURVEY RESULTS

30 January 2017Questions: [email protected]

Download the full report at www.bv.com/reports.