Embed Size (px)

Citation preview

Sponsored by:

Unleashing rural economies

1© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Contents

Executive summary 2

Introduction 3

About The Economist Intelligence Unit’s model 4

Acknowledgements 7

Angola 8

Argentina 11

China 14

France 17

India 21

Nigeria 24

Conclusions 27

2 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

The Economist Intelligence Unit’s scenario model, developed for this report, demonstrates that promoting rural development has the potential to unlock US$2trn of annual rural output across the globe by 2030—boosting baseline rural GDP of US$14.8trn by 13.4%, to US$16.8trn.

Rural economic development holds the key to ensuring that the nutritional needs of a growing global population are met, and poverty in rural areas is eased, narrowing the gaps between rural and urban populations. By promoting rural development, governments not only have signifi cant scope to unlock economic growth, they also have the potential to change fundamentally the structure of the economy.

Yet, a number of obstacles stand in the way of stronger rural economic growth. In this report, our focus on six nations—Angola, Argentina, China, France, India and Nigeria—highlights some of these key barriers:

Policy. A lack of focus on rural development is exacerbated by the absence of political will, weak rule of law and poor enforcement of rural policy.

Land rights. Restrictions on land use or land rights and lack of adequate land documentation result in signifi cant underinvestment in the agricultural sector.

Operational infrastructure. Transportation, power and water infrastructure are often lacking;

Executive summary

investment is needed in rural supply chains, productivity improvements, roads and irrigation.

Social infrastructure. Investment in healthcare and education, as well as in broadband Internet and mobile-communication networks is needed to make rural areas more attractive.

To probe the untapped potential of the world’s rural economies, we modelled how GDP, rural GDP and rural populations evolve up to 2030, according to three scenarios:

1. A scenario extrapolated from our baseline long-term forecast.

2. A scenario in which rural growth is unleashed as policymakers around the globe implement measures to stimulate rural development, following a hard landing in China.

3. A scenario that assumes a gradual decline in rural economies’ contribution to GDP growth.

This long-term forecasting model includes variables ranging from trade to population growth at country level. In turn, these variables produced output data in three key areas: GDP, rural GDP and rural population. We then produced country-specifi c forecasts under each of the three scenarios, forming the forecast basis of this research.

3© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Policymakers have tended to overlook rural development as a critical part of overall economic and social wellbeing. Yet, the importance of rural economies is intensifying as the world faces signifi cant challenges in meeting the nutritional needs of a growing human population. Today, hunger persists in many developing economies as food prices hit the poorest members of society hardest. Looking ahead, as the world’s population grows to at least 7.6bn by 2030, concerns around food security are likely to intensify.

At the same time, rural areas have a critical role to play in the fi ght against poverty. While much progress has been made in improving living standards across the globe, it is in the world’s rural areas that many of the world’s areas of extreme poverty are to be found. Around 1.4bn people live on less than US$1.25 a day, more than two-thirds of these in rural areas of developing countries. Promoting sustainable growth in rural areas is not only a means by which to improve food security and bolster economic performance, but is also an important tool with which to eradicate extreme poverty.

Crucially, rural areas offer potential for untapped economic growth. In this, the importance of the rural economy extends beyond agriculture: ancillary industries that support or service farming also have a critical role to play in rural development, including food processing,

Introduction

packaging and logistics. Food production aside, leisure and tourism are among the sectors increasingly underpinning rural economic development; there is scope, too, for growth in education, healthcare and other services that improve quality of life in rural areas.

To be sure, the multiplier effect at play in rural economies (see below) means that, as policymakers foster conditions that promote economic development in rural areas, demand for products and services in rural territories will expand—providing opportunities for new economic activities to take root in these areas. In turn, this rural economic development has the potential to support a convergence of economic prosperity in rural and urban areas—effectively reducing income disparities between rural and urban dwellers and bringing rural living standards into line with those in urban areas.

In 2013 rural areas accounted for 16.2% of global economic output—making them a key source of economic activity. In addition to productivity gains in agriculture and other rural activities already seen, there remains considerable scope for growth in rural output. Our estimates indicate that unlocking rural growth could see hundreds of billions of dollars of additional output by 2030, with rural economies accounting for an increased share of world economic output and raising overall economic-growth rates.

4 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

We need to understand that rural development is part of the general economic and social development of any given country

Eugenia Serova of the Rural Infrastructure and Agro-Industries Division of the Food and Agriculture Organisation of the UN

The focus of this research project is a better understanding of the macro- and microeconomic conditions that would enable rural economies to deliver a more signifi cant contribution to economic growth. To do so, The Economist Intelligence Unit has undertaken extensive economic modelling, based on a number of scenarios. We asked nine expert panellists to identify the major forces that will infl uence the future prospects of rural economies. They identifi ed the trends that they considered to be most important in political, economic, social, technological, legal and environmental areas, with a 2030 time horizon. From there, we developed a range of inputs that would differ across the various scenarios. At the heart of these is the baseline scenario, characterised by a continuation of the status quo and extrapolated from our in-house long-term economic forecast.

We also selected two further scenarios that our panellists developed, as follows:

A) An “unleashing” of the rural economy, which results in an increased contribution of the rural economy to overall economic growth. This scenario is driven by a series of events and their consequences:

A “hard landing” in China’s economy, causing a global downturn and a reorientation towards

About The Economist Intelligence Unit’s model

Clearly, rural development offers signifi cant opportunity. To best tap that opportunity, says Eugenia Serova, director of the Rural Infrastructure and Agro-Industries Division of the Food and Agriculture Organisation of the UN, policymakers must adopt a holistic approach to rural development. She points out that the

rural economy is inextricably linked to the wider economy—and to political, cultural and social issues. “We need to understand that rural development is part of the general economic and social development of any given country,” Ms Serova notes.

currently neglected areas of growth, in particular using rural development as a means of raising incomes and reducing poverty.

In this scenario, many developing countries are hit by the marked decline in demand for raw materials and there are risks of signifi cantly increased social unrest, particularly across large swathes of rural regions.

Weaker economic growth, coupled with civil unrest, is projected to trigger a government response, stimulating growth in rural areas in order to reduce rural poverty and rebalance development opportunities.

Several other scenarios not represented in the modelling fi gures are also able to deliver growth and reforms in line with the forecast above. Prominent among these is a scenario of incremental improvements without a specifi c trigger, or a switch towards a greener, more broadly sustainable growth trajectory, in China in particular. The key to this scenario is undertaking reform in order to align the correct macro- and microeconomic forces to unleash stronger development.

B) In the interest of scope and balance, we also modelled an incremental decline in the contribution of the rural economy to global economic growth that is driven by the following forces:

5© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Rural GDP, real(2005 prices; US$ bn)

World

Source: The Economist Intelligence Unit.

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000Incremental decline scenario: WorldBaseline scenario: WorldUnleashing scenario: World

203020292028202720262025202420232022202120202019201820172016201520142013

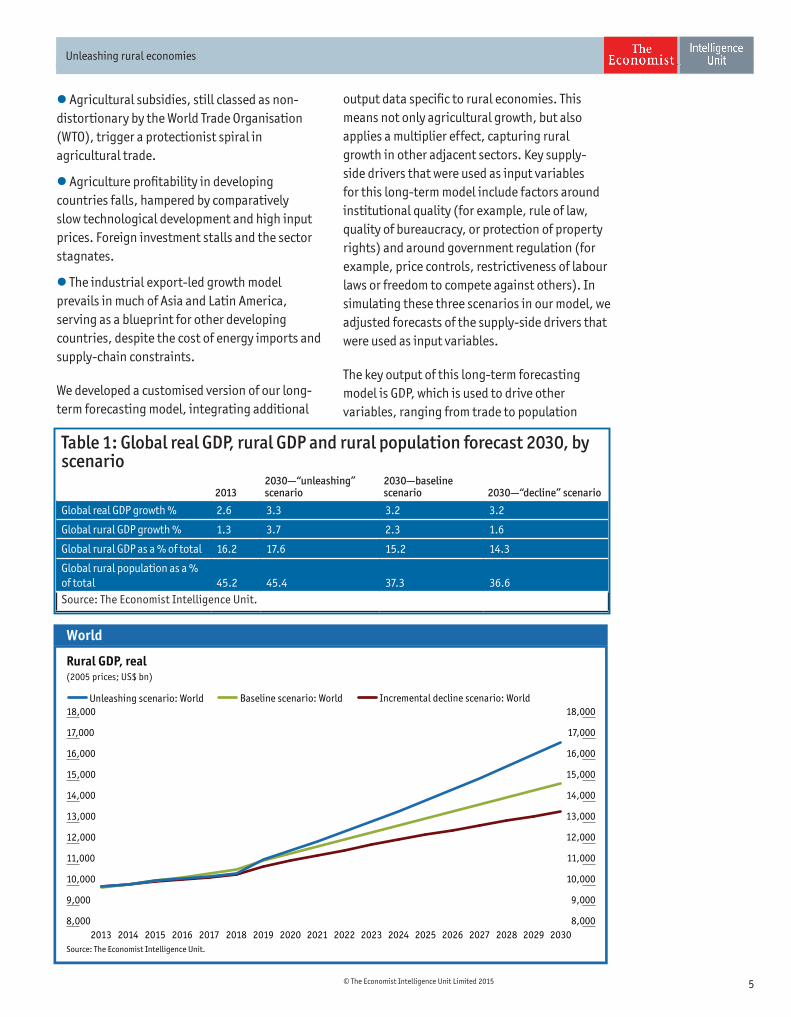

Table 1: Global real GDP, rural GDP and rural population forecast 2030, by scenario

20132030—“unleashing” scenario

2030—baseline scenario 2030—“decline” scenario

Global real GDP growth % 2.6 3.3 3.2 3.2

Global rural GDP growth % 1.3 3.7 2.3 1.6

Global rural GDP as a % of total 16.2 17.6 15.2 14.3

Global rural population as a % of total 45.2 45.4 37.3 36.6Source: The Economist Intelligence Unit.

Agricultural subsidies, still classed as non-distortionary by the World Trade Organisation (WTO), trigger a protectionist spiral in agricultural trade.

Agriculture profi tability in developing countries falls, hampered by comparatively slow technological development and high input prices. Foreign investment stalls and the sector stagnates.

The industrial export-led growth model prevails in much of Asia and Latin America, serving as a blueprint for other developing countries, despite the cost of energy imports and supply-chain constraints.

We developed a customised version of our long-term forecasting model, integrating additional

output data specifi c to rural economies. This means not only agricultural growth, but also applies a multiplier effect, capturing rural growth in other adjacent sectors. Key supply-side drivers that were used as input variables for this long-term model include factors around institutional quality (for example, rule of law, quality of bureaucracy, or protection of property rights) and around government regulation (for example, price controls, restrictiveness of labour laws or freedom to compete against others). In simulating these three scenarios in our model, we adjusted forecasts of the supply-side drivers that were used as input variables.

The key output of this long-term forecasting model is GDP, which is used to drive other variables, ranging from trade to population

6 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

The fi ndings of this report indicate the existence of an alternative long-term path for rural development.

growth. We focused the analysis on output data in three key areas: GDP, rural GDP and rural population. Based on the three scenarios, we then produced country-specifi c forecasts, as well as global aggregates (see Table 1). Under the “unleashing” scenario, for example, rural GDP growth will be 3.7% in 2030, markedly higher than the 2.3% forecast under the baseline scenario.

Under the unleashing scenario, reforms aimed at stimulating rural development bolster rural economic growth markedly from 2019 (see Chart 1). The long time horizon needed to surpass the current growth trajectory is partly a construction of the particular scenario employed; a less severe trigger for reform than a hard landing in China could open up substantial growth prospects, without a medium-term dip in growth. However, this also refl ects the need to undergo substantial reform and investment to realise improved long-term growth potential.

While it is unlikely that policymakers across the globe will spontaneously take co-ordinated action to stimulate rural development, leading to the economic-development forecast in the chart above, the output of our model clearly demonstrates the untapped potential in rural

economies. Under the right conditions, these rural economies have the potential to be much larger in absolute terms and to make a greater relative contribution to the wider economy by 2030. As such, the fi ndings of this report indicate the existence of an alternative long-term path for rural development.

We selected the six countries profi led in this report—Angola, Argentina, China, France, India and Nigeria—for the broad range of geographic and economic profi les that they represent. These nations illustrate the variety of challenges that countries across the globe face as they seek to unlock rural economic growth, and serve to provide some sense of the scale of extra growth that can be unlocked by other nations around the world.

A hard landing in China is just one of several events or triggers that could lead to an upturn in rural economic growth. Naturally, policymakers in many countries across the world have the tools at their disposal to progress—to whatever extent—towards any of the outcomes presented here, regardless of exogenous factors. This research provides a glimpse of the rural economic growth that it may be possible for policymakers to unlock, if they are committed to doing so.

7© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

The Economist Intelligence Unit would like to thank the following individuals (listed alphabetically by organisation name) for sharing their insights and expertise during the research for this paper:

Louis-Pascal Mahé, professor emeritus, Agrocampus Ouest, France

Luc Rigouzzo, managing partner and executive president, Amethis Finance, France

Albert Keidel, senior fellow, Atlantic Council, US

Jikun Huang, Founder and Director, Centre for Agricultural Policy, Chinese Academy of Sciences, China

Lucio Castro, director of economic development, Centre for the Implementation of Public Policies Promoting Equity and Growth, Argentina

Steven Kyle, associate professor, Department of Applied Economics and Management, Cornell University, US

Kolawole Adebayo, professor of rural development communication, Federal University of Agriculture, Abeokuta, Nigeria

Eugenia Serova, director, Rural Infrastructure and Agro-Industries Division, Food and Agriculture Organisation of the UN, Italy

Robin Bourgeois, senior foresight and development policies expert, Global Forum on

Agricultural Research, Italy

Horacio Busanello, CEO, Grupo Los Grobo, Argentina

Cherian Thomas, CEO, IDFC Foundation, India

Claus Reiner, country programme manager for Argentina, International Fund for Agricultural Development, Italy

Gao Yu, country director, Landesa, China

Srikumar Misra, founder and CEO, Milk Mantra, India

François Houllier, president and CEO, National Institute for Agricultural Research, France

Hervé Guyomard, economist, National Institute for Agricultural Research, France

M V Rao, director-general, National Institute of Rural Development and Panchayati Raj, India

Hans Jöhr, corporate head of agriculture, Nestlé, Switzerland

Louw Burger, managing director, Thai Farm International, Nigeria

James Oehmke, senior food security and nutrition advisor, Bureau for Food Security, USAID, US

Philippe Scholtès, director, Agribusiness Development Branch, UN Industrial Development Organisation, Austria

Acknowledgements

8 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Angola1Angola’s oil industry accounts for over 46% of the country’s GDP and 95% of its export revenue; understandably, this has created some imbalances in the economy. In coastal cities, oil drives what is almost an enclave economy: the strength of the Angolan currency, the kwanza, enables cities to source food cheaply via imports, rather than from Angola’s rural areas. The rural economy makes up 24.1% of Angola’s total real GDP, even though its rural population of 9m accounts for around 42% of the country’s total 21.5m inhabitants. This makes for a sharp divide in quality of life and economic-development prospects between rural and urban residents.

By the time the country emerged from decades of confl ict, in 2002, much of its physical infrastructure had been destroyed. Moreover, socio-demographic challenges abound. Almost 4m people, one-third of Angola’s population, were obliged to leave their homes; in many cases, rural skills have not been passed on to the next generation as a result of this dislocation. And rural regions continue to face shortages of livestock and other key agricultural inputs.

Neverthless, Angola’s rural economies hold remarkable promise. “Agriculture can thrive there,” says Steven Kyle, an associate professor at Cornell University. “Angola has the potential to have a strong agricultural sector, which satisfi es national needs and can export the surplus.” He points out that the country has some of the best natural resources in southern Africa in terms of soil, climate and water conditions. “It would be possible to develop the country and have the urban demand centres supplied from the domestic farm sector,” Mr Kyle suggests.

Yet, political will is absent, at least in part because oil is higher than rural development on the list of policymakers’ priorities. “For all the government occasionally implies to the contrary, agriculture does not get a lot of money,” says Mr Kyle. “The ruling Mouvement populaire de libération de l’Angola (MPLA) are okay with people trying to develop agriculture, but, for the people in charge, that is not where their money comes from—it comes from oil. Their focus is not there; that is not part of their life or their future.”

Furthermore, if Angola’s rural economy is to fulfi l its potential, policymakers must also strengthen the rule of law. Angola places 141st in a ranking of 144 countries, based on ethics and corruption, which forms part of the World Economic Forum’s Global Competitiveness Index. Much of Angola’s economy is subject to arbitrary or unfair decisions by offi cials, according to Mr Kyle: “If you are a peasant out in the countryside, you are at the mercy of any petty offi cial at the intersection who wants to tax you or just steal stuff outright.”

A further issue is basic infrastructure. There is a need for policymakers to address shortfalls in basic transportation infrastructure, enabling more effi cient movement of farm produce to markets. In Angola’s poorer rural areas, much of the population are subsistence farmers that remain disconnected from the wider economy, in part because of the lack of a road network. “From a physical point of view, roads and bridges have been destroyed, and, as yet, some have not been rebuilt,” says Mr Kyle.

Angola has the potential to have a strong agricultural sector, which satisfi es national needs and can export the surplus.

Steven Kyle, Professor at Cornell University

9© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

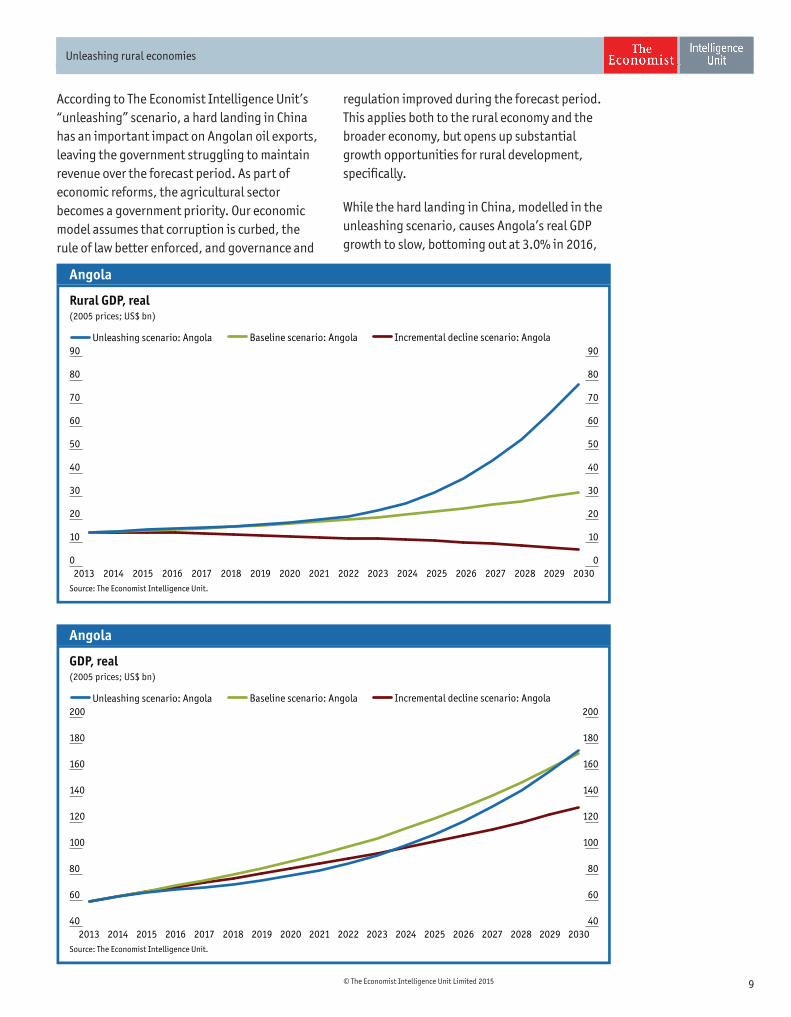

According to The Economist Intelligence Unit’s “unleashing” scenario, a hard landing in China has an important impact on Angolan oil exports, leaving the government struggling to maintain revenue over the forecast period. As part of economic reforms, the agricultural sector becomes a government priority. Our economic model assumes that corruption is curbed, the rule of law better enforced, and governance and

regulation improved during the forecast period. This applies both to the rural economy and the broader economy, but opens up substantial growth opportunities for rural development, specifi cally.

While the hard landing in China, modelled in the unleashing scenario, causes Angola’s real GDP growth to slow, bottoming out at 3.0% in 2016,

Angola

Source: The Economist Intelligence Unit.

0

10

20

30

40

50

60

70

80

90

0

10

20

30

40

50

60

70

80

90

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: AngolaBaseline scenario: AngolaUnleashing scenario: Angola

Rural GDP, real(2005 prices; US$ bn)

Angola

Source: The Economist Intelligence Unit.

40

60

80

100

120

140

160

180

200

40

60

80

100

120

140

160

180

200

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: AngolaBaseline scenario: AngolaUnleashing scenario: Angola

GDP, real (2005 prices; US$ bn)

10 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Angola

Source: The Economist Intelligence Unit.

0

2

4

6

8

10

12

0

2

4

6

8

10

12

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: AngolaBaseline scenario: AngolaUnleashing scenario: Angola

Real GDP growth(%)

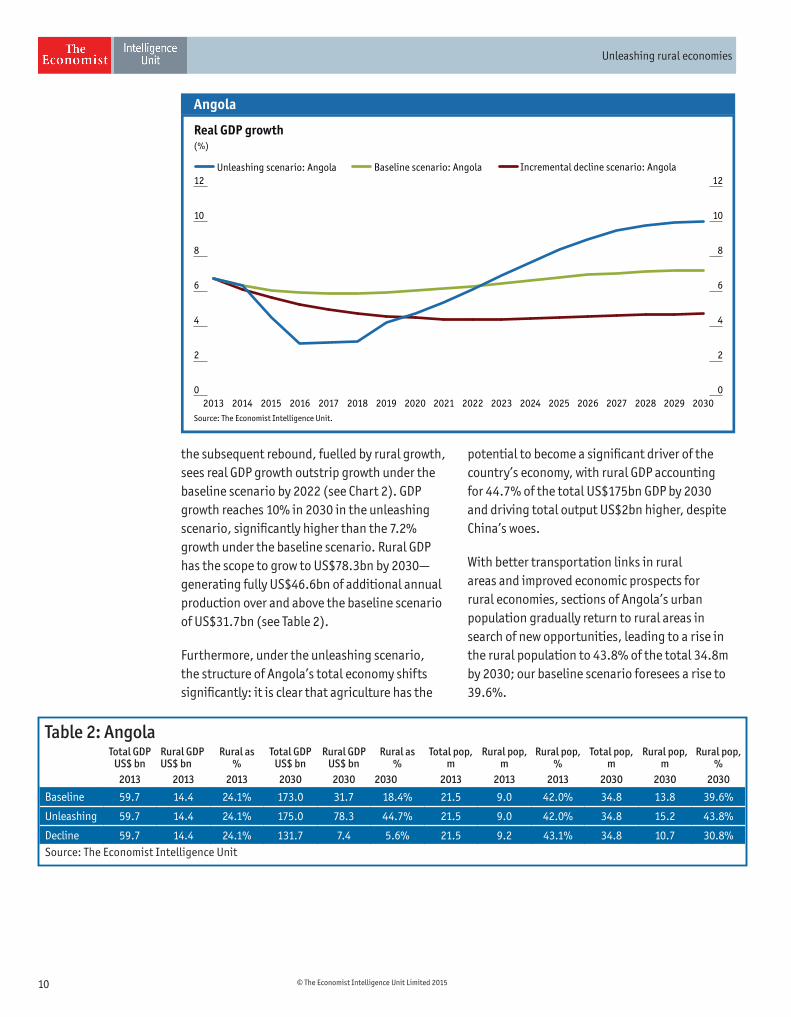

the subsequent rebound, fuelled by rural growth, sees real GDP growth outstrip growth under the baseline scenario by 2022 (see Chart 2). GDP growth reaches 10% in 2030 in the unleashing scenario, signifi cantly higher than the 7.2% growth under the baseline scenario. Rural GDP has the scope to grow to US$78.3bn by 2030—generating fully US$46.6bn of additional annual production over and above the baseline scenario of US$31.7bn (see Table 2).

Furthermore, under the unleashing scenario, the structure of Angola’s total economy shifts signifi cantly: it is clear that agriculture has the

potential to become a signifi cant driver of the country’s economy, with rural GDP accounting for 44.7% of the total US$175bn GDP by 2030 and driving total output US$2bn higher, despite China’s woes.

With better transportation links in rural areas and improved economic prospects for rural economies, sections of Angola’s urban population gradually return to rural areas in search of new opportunities, leading to a rise in the rural population to 43.8% of the total 34.8m by 2030; our baseline scenario foresees a rise to 39.6%.

Table 2: AngolaTotal GDP

US$ bnRural GDP US$ bn

Rural as %

Total GDP US$ bn

Rural GDP US$ bn

Rural as %

Total pop, m

Rural pop, m

Rural pop, %

Total pop, m

Rural pop, m

Rural pop, %

2013 2013 2013 2030 2030 2030 2013 2013 2013 2030 2030 2030

Baseline 59.7 14.4 24.1% 173.0 31.7 18.4% 21.5 9.0 42.0% 34.8 13.8 39.6%

Unleashing 59.7 14.4 24.1% 175.0 78.3 44.7% 21.5 9.0 42.0% 34.8 15.2 43.8%

Decline 59.7 14.4 24.1% 131.7 7.4 5.6% 21.5 9.2 43.1% 34.8 10.7 30.8%Source: The Economist Intelligence Unit

11© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Argentina’s rural economy is largely based on effi cient, capital-intensive agriculture. “Most of the sector uses advanced technology and most of it is close to international [standards] in terms of productivity,” says Lucio Castro, director of economic development at the Centre for the Implementation of Public Policies Promoting Equity and Growth (CIPPEC) in Argentina. While agriculture accounts for over half of Argentina’s foreign-exchange revenue, it employs a relatively low proportion of the workforce. At the same time, the rural population of 3m accounts for just 7.1% of the country’s total 41.7m population.

Yet, since Argentina’s economic crisis of 2001–02, economic mismanagement and interference by successive governments has eroded the country’s competitive advantage in agriculture. Poorly conceived policies have left the rural economy, as well as the wider economy, signifi cantly weakened and have led to high-infl ation, low-growth conditions. Nevertheless, there is signifi cant scope for Argentina’s rural economy to regain its competitive advantage and to strengthen its contribution to the country’s overall economic health.

Indeed, it is this economic mismanagement that is one of the biggest challenges that policymakers must tackle to unlock growth in Argentina’s rural economy. In the World Economic Forum’s Global Competitiveness Report 2014–2015, Argentina’s macroeconomic environment ranks just 102nd of 144 countries. The strong devaluation of the Argentinian peso may have made exports more competitive, yet export taxes, quotas and exchange-rate controls that hamper trade must be eased. Similarly,

Argentina 2government restrictions on imports that limit the agricultural sector’s access to capital goods and other technologies must be lifted.

Another challenge lies in the form of trade restrictions imposed by the government in the wake of the 2001–02 economic crisis, which weigh heavily on Argentina’s rural economy. Not least among these is the quota system for cereal exports known as the registro de exportación. With elections due in October 2015, some experts hope a new government will lift trade restrictions. Yet, in the short term, this may be diffi cult to achieve without further fuelling infl ation and worsening state fi nances, argues Mr Castro. However, he hopes that reforms will, in time, enable the lifting of such trade restrictions.

A further issue is taxes. “We need to address the fi scal burden on agricultural activity that erodes farmers’ profi tability,” says Horacio Busanello, CEO of Argentinian agribusiness company, Grupo Los Grobo. “It is not only about export duties, but also the combination of national, provincial and county taxes.” By easing restrictions that are holding back the agricultural sector, he believes, crop production can be increased by 50% by 2020. Increasing yearly exports in line with higher production could generate additional revenue of around US$10bn annually for Argentina, according to Mr Busanello.

Logistics costs are a further burden on Argentina’s rural economy; 80% of Argentina’s agricultural produce is transported by road, yet logistics costs are increasing at a double-digit percentage rate due to rising wage costs, higher fuel prices, and underinvestment in roads. At

Most of the sector uses advanced technology and most of it is close to international [standards] in terms of productivity

Lucio Castro director of the Centre for the Implementation of Public Policies Promoting Equity and Growth

12 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

the same time, 70% of total agricultural exports go through a single port, Rosario Port, posing a strategic risk for Argentina’s economy. Unless Argentina invests a further 1–2% of GDP in transportation infrastructure, highlights Mr Castro, the agricultural sector will struggle to increase exports.

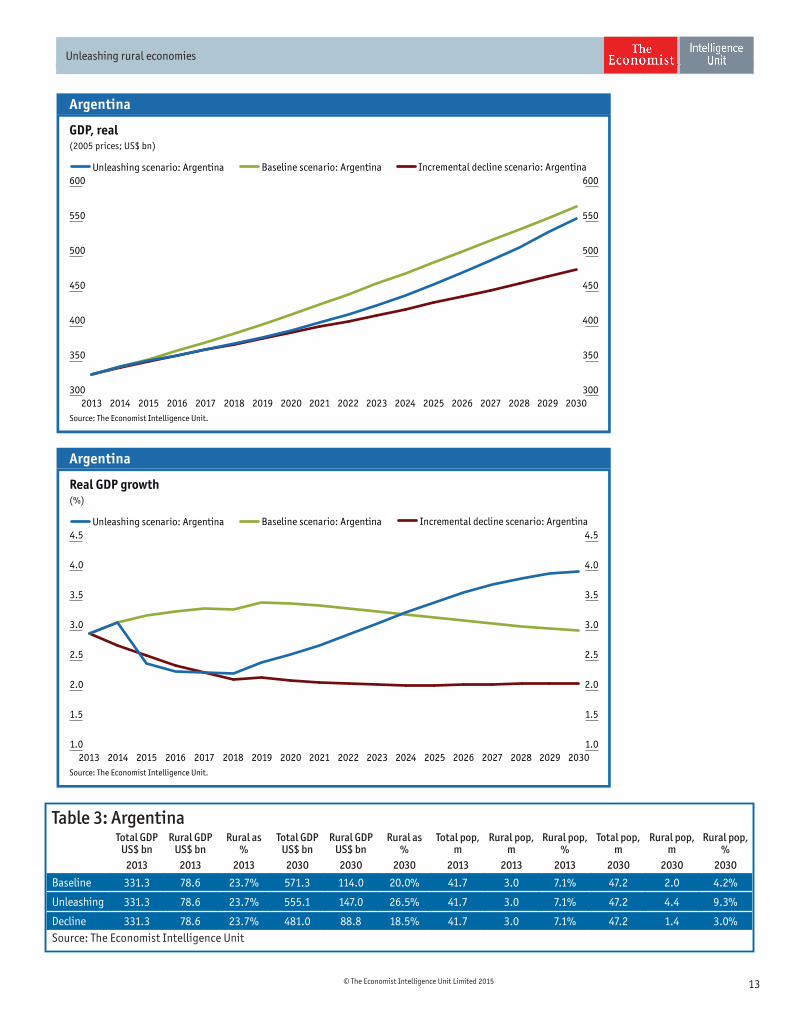

The Economist Intelligence Unit’s “unleashing” scenario forecasts that a hard landing in the Chinese economy hits prices of Argentina’s agricultural exports and the subsequent deterioration in the balance of payments causes macroeconomic diffi culties. In 2013 Argentina’s exports to China amounted to US$5.5bn, or 7.2% of all its exports, according to International Trade Centre (ITC) data; of those exports to China, around US$4.3bn, or 78%, were agricultural exports.

However, should policymakers embrace structural reforms in an effort to trigger growth, there is ample scope for increased economic activity—in particular, the upside potential from Argentina’s agricultural resources is substantial. Accordingly, among the input factors we have adjusted for in our economic model are the effects of a gradual easing of price controls and a lifting of market distortions.

While the China hard landing causes Argentina’s real GDP growth to slow, bottoming out at 2.2% in 2018, the subsequent rebound, fuelled by renewed competitiveness of the country’s agricultural sector and stronger exports, sees real GDP growth outstrip growth under the baseline scenario in 2024 (see Chart 3). Real GDP growth in 2030, for example, is 4% in the unleashing scenario, signifi cantly above the 3% under the baseline scenario.

In the unleashing scenario, Argentina’s rural GDP expands to US$147bn by 2030, accounting for 26.5% of the total US$555.1bn GDP at that time, and representing a full US$33bn of annual additional productivity in Argentina’s rural areas over and above our 2030 baseline scenario (see Table 3).

Moreover, additional productivity and income in rural areas bolsters rural populations to 4.4m, or 9.3% of the total 47.2m population by 2030. In the baseline scenario, the rural population accounts for just 2m, or 4.2% of the total, by 2030, refl ecting a signifi cant depletion of human capital in rural areas as agricultural-employment opportunities stagnate.

Argentina

Source: The Economist Intelligence Unit.

60

70

80

90

100

110

120

130

140

150

160

60

70

80

90

100

110

120

130

140

150

160

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: ArgentinaBaseline scenario: ArgentinaUnleashing scenario: Argentina

Rural GDP, real(2005 prices; US$ bn)

It is not only about export duties, but also the combination of national, provincial and county taxes.

Horacio Busanello, CEO of Grupo Los Grobo

13© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Table 3: ArgentinaTotal GDP

US$ bnRural GDP

US$ bnRural as

%Total GDP

US$ bnRural GDP

US$ bnRural as

%Total pop,

mRural pop,

mRural pop,

%Total pop,

mRural pop,

mRural pop,

%2013 2013 2013 2030 2030 2030 2013 2013 2013 2030 2030 2030

Baseline 331.3 78.6 23.7% 571.3 114.0 20.0% 41.7 3.0 7.1% 47.2 2.0 4.2%

Unleashing 331.3 78.6 23.7% 555.1 147.0 26.5% 41.7 3.0 7.1% 47.2 4.4 9.3%

Decline 331.3 78.6 23.7% 481.0 88.8 18.5% 41.7 3.0 7.1% 47.2 1.4 3.0%Source: The Economist Intelligence Unit

Argentina

Source: The Economist Intelligence Unit.

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: ArgentinaBaseline scenario: ArgentinaUnleashing scenario: Argentina

Real GDP growth(%)

Argentina

Source: The Economist Intelligence Unit.

300

350

400

450

500

550

600

300

350

400

450

500

550

600

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: ArgentinaBaseline scenario: ArgentinaUnleashing scenario: Argentina

GDP, real(2005 prices; US$ bn)

14 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Over the past three decades, economic reform in China has led to a surge in growth in the wider economy, as well as in the rural economy. “China went from a command and control economy to one in which agriculture smallholders are much more able to take advantage of their own opportunities, starting with the removal of the quota system in 1979,” explains James Oehmke, a senior food security and nutrition advisor in USAID’s Bureau for Food Security. Stressing the linkage of urban and rural areas, China has invested considerable resources in transportation networks; this helps connect its 739.8m rural population, which accounts for 54.8% of the total 1.35bn.

While developed coastal areas have been growing faster than rural inland regions, as Albert Keidel, a senior fellow at the Atlantic Council in the US, points out, family incomes in these inland regions have nevertheless been expanding at between 6% and 9% annually. “Income disparities between the coastal regions and the interior are overshadowed by the speed with which the standards of living have improved everywhere,” he explains.

However, a signifi cant issue in rural development in China is property development. Local governments that generate income through land sales are fuelling China’s real-estate boom—driving up indebtedness and increasing the risk of a hard landing. Illegal conversion of land use reduces arable land available for crops and leads to land being taken from farmers. Farmers are granted 30-year land-use rights, but the law provides for expropriation in the public interest.

China3Land expropriation has been on the rise, but is often not in line with regulation, according to Gao Yu, country director at Landesa in China. Farmers rarely receive adequate compensation.

Underinvestment in agriculture is one consequence. “Farmers don’t invest enough in land because they have concerns that their land could be taken in the next months or next years,” says Mr Gao. This reluctance to invest more is also clear among farmers who do not have adequate documentation for their land, which adds to insecurity. “If farmers receive proper land certifi cates, they are 77% more likely to make mid- and long-term investments in land than those with non-compliant ones,” Mr Gao adds, citing a survey published in 2012 by Landesa.

In tackling rural property development, according to Mr Gao, the fi rst priority is to regulate land expropriations and defi ne “public interest” more clearly, in order to minimise abuse. Furthermore, compensation levels need to be brought into line with market valuations. Farmers’ rights in contesting expropriation ought to be more clearly laid out and existing laws enforced. Already, in October 2014, China’s agriculture minister had announced land reforms aimed at promoting agricultural competitiveness; he warned against “forcing land transfers against farmers’ will, which violates their rights”.

China’s grain self-suffi ciency policy is a further issue holding back its rural economy. Many farmers are required to allocate land to low-margin grain—just as growing prosperity and urbanisation drive demand for higher-quality foods. “A lot of farmers are earning less money

Farmers don’t invest enough in land because they have concerns that their land could be taken in the next months or next years

Gao Yu, country director at Landesa in China

15© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

than they could if they put their land into vegetables and fruit,” says Mr Keidel.

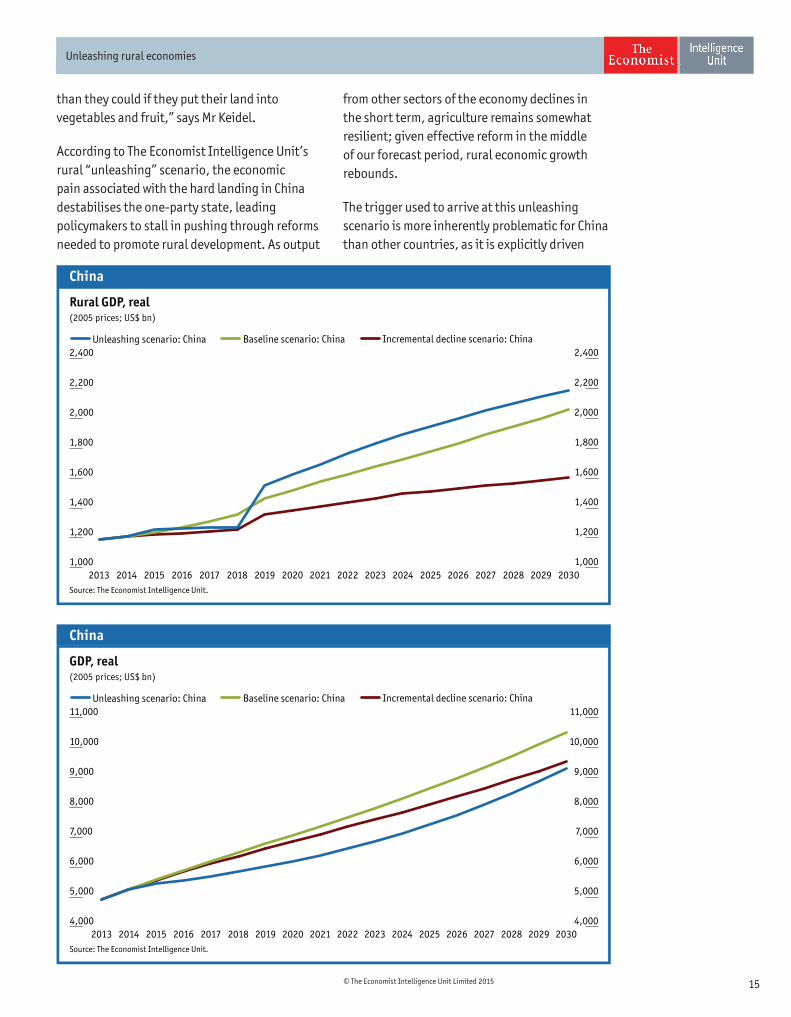

According to The Economist Intelligence Unit’s rural “unleashing” scenario, the economic pain associated with the hard landing in China destabilises the one-party state, leading policymakers to stall in pushing through reforms needed to promote rural development. As output

from other sectors of the economy declines in the short term, agriculture remains somewhat resilient; given effective reform in the middle of our forecast period, rural economic growth rebounds.

The trigger used to arrive at this unleashing scenario is more inherently problematic for China than other countries, as it is explicitly driven

China

Source: The Economist Intelligence Unit.

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: ChinaBaseline scenario: ChinaUnleashing scenario: China

Rural GDP, real(2005 prices; US$ bn)

China

Source: The Economist Intelligence Unit.

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: ChinaBaseline scenario: ChinaUnleashing scenario: China

GDP, real(2005 prices; US$ bn)

16 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

China

Source: The Economist Intelligence Unit.

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: ChinaBaseline scenario: ChinaUnleashing scenario: China

Real GDP growth(%)

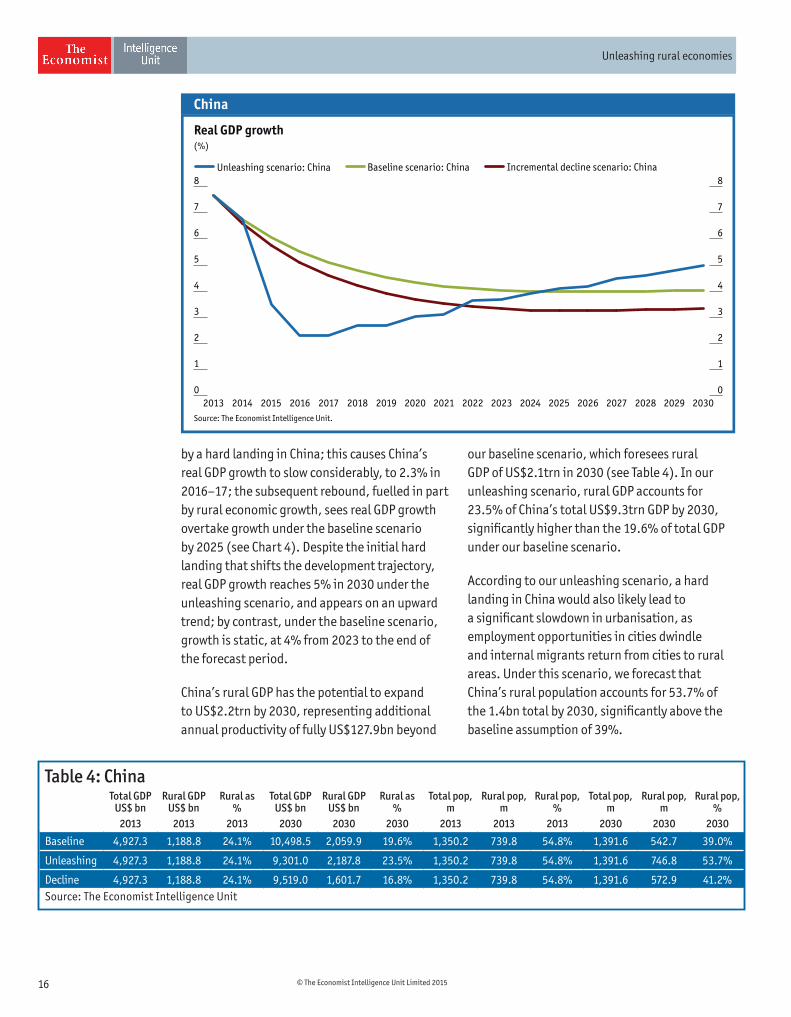

by a hard landing in China; this causes China’s real GDP growth to slow considerably, to 2.3% in 2016–17; the subsequent rebound, fuelled in part by rural economic growth, sees real GDP growth overtake growth under the baseline scenario by 2025 (see Chart 4). Despite the initial hard landing that shifts the development trajectory, real GDP growth reaches 5% in 2030 under the unleashing scenario, and appears on an upward trend; by contrast, under the baseline scenario, growth is static, at 4% from 2023 to the end of the forecast period.

China’s rural GDP has the potential to expand to US$2.2trn by 2030, representing additional annual productivity of fully US$127.9bn beyond

our baseline scenario, which foresees rural GDP of US$2.1trn in 2030 (see Table 4). In our unleashing scenario, rural GDP accounts for 23.5% of China’s total US$9.3trn GDP by 2030, signifi cantly higher than the 19.6% of total GDP under our baseline scenario.

According to our unleashing scenario, a hard landing in China would also likely lead to a signifi cant slowdown in urbanisation, as employment opportunities in cities dwindle and internal migrants return from cities to rural areas. Under this scenario, we forecast that China’s rural population accounts for 53.7% of the 1.4bn total by 2030, signifi cantly above the baseline assumption of 39%.

Table 4: ChinaTotal GDP

US$ bnRural GDP

US$ bnRural as

%Total GDP

US$ bnRural GDP

US$ bn Rural as

%Total pop,

mRural pop,

mRural pop,

%Total pop,

mRural pop,

mRural pop,

%2013 2013 2013 2030 2030 2030 2013 2013 2013 2030 2030 2030

Baseline 4,927.3 1,188.8 24.1% 10,498.5 2,059.9 19.6% 1,350.2 739.8 54.8% 1,391.6 542.7 39.0%

Unleashing 4,927.3 1,188.8 24.1% 9,301.0 2,187.8 23.5% 1,350.2 739.8 54.8% 1,391.6 746.8 53.7%

Decline 4,927.3 1,188.8 24.1% 9,519.0 1,601.7 16.8% 1,350.2 739.8 54.8% 1,391.6 572.9 41.2%Source: The Economist Intelligence Unit

17© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

France is Europe’s leading agricultural producer, though the country’s advanced, service-oriented economy means that rural activities account for no more than 13.1% of total economic output. By most measures, France’s agricultural sector is strong—but there remains considerable scope to unlock further growth in its rural economy.

Over the past four decades, some migration patterns have shifted. Some city-dwellers who move to rural areas may be escaping the high cost of living in urban centres or seeking a better quality of life. Today, France’s rural population of 14.3m accounts for 22.3% of the country’s 64.3m total population. Productivity improvements in agricultural have led to declining employment in the sector across France’s rural areas, while services, including tourism and leisure, account for a growing proportion of job creation.

Indeed, opportunities for the further development of France’s rural economy lie principally in sectors other than agriculture. François Houllier, president and CEO of the Institut national de la récherche agronomique (INRA, French National Institute for Agricultural Research) points out that a shift has occurred in recent decades, as France’s rural economy has evolved: “Job creation mainly occurs in public and private services, in the tertiary sector, and especially with regard to services that are offered to the residents, be they tourists or local residents,” he says. This shift serves to emphasise the importance of multiplier effects in France’s rural economies, especially in tourism and leisure.

One obstacle to the development of the rural economy is France’s application of the EU Common Agricultural Policy, according to experts. The policy comprises two pillars: income support and rural development. Hervé Guyomard, an economist with INRA, points out that France’s application is insuffi ciently based on an integrated approach to rural development. “There is an excessive focus on agricultural activities, when you compare how other countries like Germany, Austria, or the UK use the second pillar,” he says. As such, France may be neglecting potentially benefi cial initiatives, such as boosting innovation, promoting economic diversifi cation and improving the quality of life in rural areas.

Louis-Pascal Mahé, professor emeritus at Agrocampus Ouest in France, advocates adopting a territorial approach to policy, rather than a sector-based approach, making regional-development efforts more effective. An emphasis on the diversity of activities involved in rural economies would strengthen multiplier effects present in rural growth, he argues. “It would be better to focus on the rural areas that are in trouble, instead of spreading the agricultural funds all over France, much of it to those who are already well-off,” he says. However, a change of approach risks leaving some farmers with excessive cuts in funds, as Professor Guyomard points out. Nevertheless, while this may be politically diffi cult, signifi cant progress in rural development could follow.

An increasing challenge is seasonality, as rural employment shifts from agriculture to services,

France4

18 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

including leisure and tourism. When agricultural activity—by its nature seasonal—was a stronger component of rural economies, local inhabitants remained present in rural areas year-round and organised their lives according to the cycle of the seasons. By contrast, the growth of seasonal activities such as leisure and tourism, with their sporadic labour needs, may mean that employers

are reluctant to invest in training and that rural areas struggle to retain skills and experience. The issue is complicated further, Mr Guyomard says, by France’s labour legislation.

A third issue is provision of services in remote areas of rural France to improve quality of life and attract young people. “One challenge is how

France

Source: The Economist Intelligence Unit.

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: FranceBaseline scenario: FranceUnleashing scenario: France

Rural GDP, real(2005 prices; US$ bn)

France

Source: The Economist Intelligence Unit.

2,000

2,200

2,400

2,600

2,800

3,000

3,200

2,000

2,200

2,400

2,600

2,800

3,000

3,200

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: FranceBaseline scenario: FranceUnleashing scenario: France

GDP, real(2005 prices; US$ bn)

19© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

France

Source: The Economist Intelligence Unit.

0.0

0.5

1.0

1.5

2.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: FranceBaseline scenario: FranceUnleashing scenario: France

Real GDP growth(%)

to improve the supply and the accessibility of services to residents and to businesses, especially in those areas which are the most neglected,” says Mr Houllier. “If there are no services, people will not stay for long.” These services include healthcare, education and transport, but also broadband Internet and mobile connectivity. “The key to rural development lies in providing the public goods and an attractive social and natural environment to ensure quality of life,” concludes Mr Mahé.

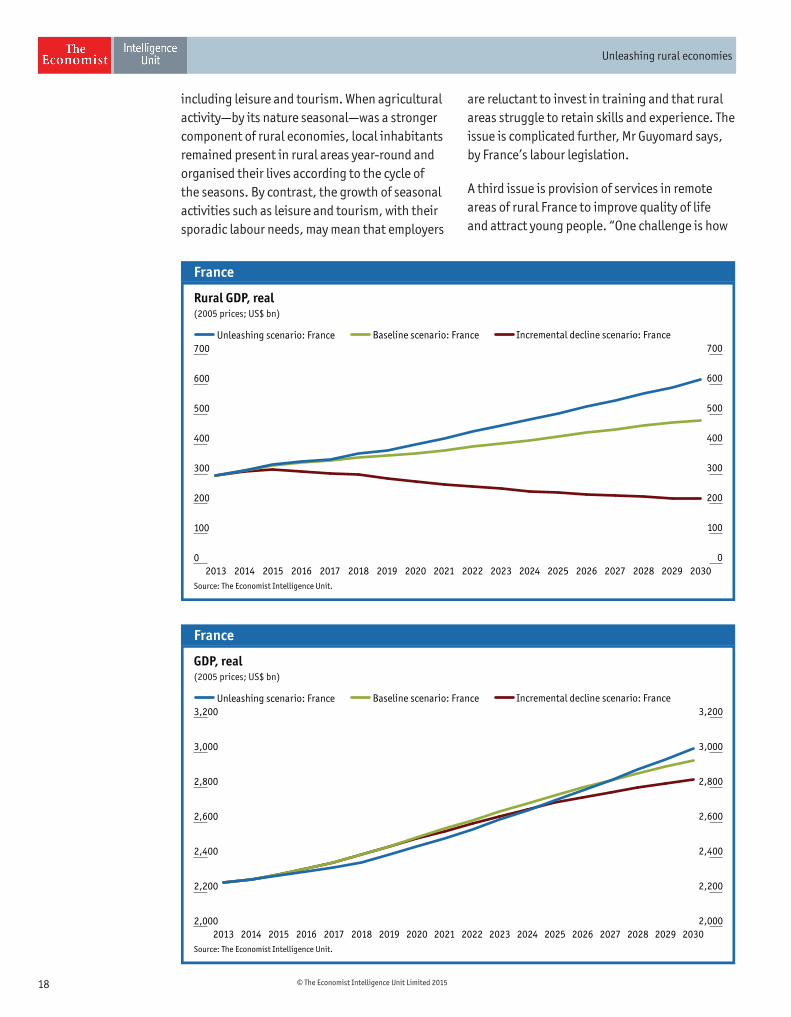

Forecasts under The Economist Intelligence Unit’s “unleashing” scenario indicate that, in the case of a hard landing in China, France’s GDP growth initially slows under the impact of the global economic downturn on exports, confi dence and fi nancing. The crisis forces the government to undertake structural reforms to boost growth prospects, including loosening the country’s strict labour laws so as to encourage investment and employment growth. Increased productivity raises growth rates in the agricultural sector, as well as in broader elements of the rural economy.

Under the unleashing scenario, the hard landing in China sees France’s recovery falter, but resume again in 2016 (see Chart 5). The rural economy fuels GDP growth to the extent that total GDP growth following the hard landing in the unleashing scenario outstrips baseline GDP growth by 2021 and continues making a signifi cant contribution to growth beyond. Real GDP growth is forecast to ease to 2% by 2030 under the unleashing scenario, which is nevertheless signifi cantly higher than the 1.3% expected under the baseline scenario.

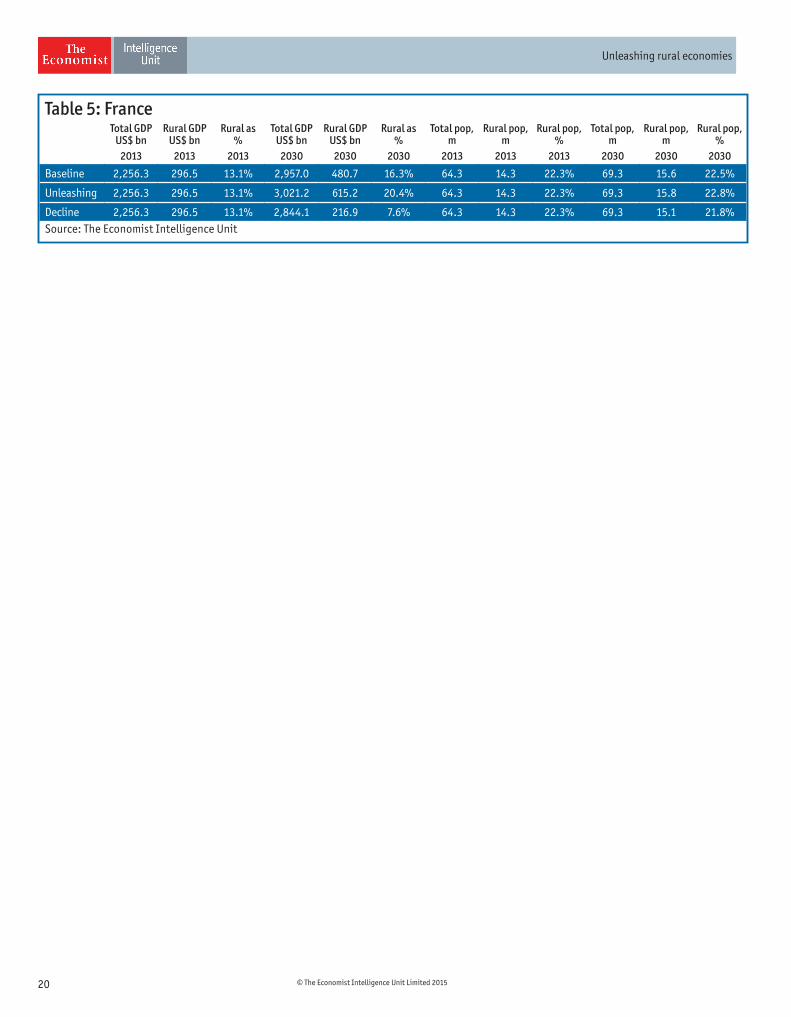

Our model foresees growth in rural GDP to US$615.2bn by 2030 under the unleashing scenario—representing fully US$134.5bn of annual output on top of the US$480.7bn foreseen under our baseline scenario (see Table 5). Because structural reforms also boost job creation elsewhere, the share of the rural population does not rise dramatically compared with the baseline. However, the unleashing scenario sees a rural population slightly above the baseline expectation, as rural areas maintain their importance in a growing, more dynamic economy.

The key to rural development lies in providing the public goods and an attractive social and natural environment to ensure quality of life

Louis-Pascal Mahé, professor emeritus at Agrocampus Ouest in France

20 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Table 5: FranceTotal GDP

US$ bnRural GDP

US$ bnRural as

%Total GDP

US$ bnRural GDP

US$ bnRural as

%Total pop,

mRural pop,

mRural pop,

%Total pop,

mRural pop,

mRural pop,

%2013 2013 2013 2030 2030 2030 2013 2013 2013 2030 2030 2030

Baseline 2,256.3 296.5 13.1% 2,957.0 480.7 16.3% 64.3 14.3 22.3% 69.3 15.6 22.5%

Unleashing 2,256.3 296.5 13.1% 3,021.2 615.2 20.4% 64.3 14.3 22.3% 69.3 15.8 22.8%

Decline 2,256.3 296.5 13.1% 2,844.1 216.9 7.6% 64.3 14.3 22.3% 69.3 15.1 21.8%Source: The Economist Intelligence Unit

21© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

India’s government has invested heavily in rural areas in the past decade, strengthening road networks, power and communications infrastructure, and education and healthcare facilities. “The facilities we associate with normal towns and cities can now be found in villages and fringe areas,” points out M V Rao, director-general of the National Institute of Rural Development in India. Nevertheless, while India’s 850m rural population amounts to 68.7% of the country’s 1.24bn total, rural inhabitants are continuing to move towards the cities.

Poor local governance is one factor hampering rural development, according to experts interviewed for this research. India’s constitution provides for powers in 29 areas—for example, local planning, education, and healthcare—to be devolved to local-government institutions, or panchayats. However, “The local panchayat institutions have not been able to function to their full potential,” observes Mr Rao. The Roadmap for the Panchayati Raj (2011–17)1, published by the government of India, highlights a lack of adequate devolution to many regional authorities, excessive bureaucracy, and a heavy dependence on government funding among the reasons that local government tends to be ineffective.

A further hurdle to development in rural India is the lack of an organised supply chain. “Where I work, in the eastern part of India, the organised sector penetration in dairy is just about 10%,” says Srikumar Misra, founder and CEO of Milk Mantra, an Indian dairy company. The remaining dairy production, he says, goes through informal networks, preventing farmers from benefi ting from transparency and market pricing. “Unless these producers are connected to the processors

India5or the markets through organised value chains, their growth becomes completely stunted and is absolutely unreliable as a sustainable economic model for them,” he says.

Moreover, to unlock potential growth in India’s rural economies, further investment is needed in food-processing and supply-chain infrastructure, according to experts. “A lot of agricultural produce does not reach consumers in time because there are transportation and storage bottlenecks,” points out Mr Rao, who estimates that up to 40% of perishable commodities and food grains are wasted. What is needed is “larger markets, storage facilities, processing facilities and also cold storage for perishable commodities like fruits, fi sh, and vegetables,” he says.

Another requirement to bolster rural economies is further investment in irrigation, including improved management of rainwater. According to Mr Rao, better management of water resources would enable many farmers to plant a second crop, where today almost 60% of the land cultivated in India is single-crop. “When we look at the poverty map of India and the single-crop map, wherever there is single crop, you can also see the poverty zones,” says Mr Rao. “A second crop will defi nitely improve living conditions.” Provisioning the infrastructure to enable this would unlock growth, reduce poverty and improve the quality of life in rural areas.

In the hard landing that triggers the scenario modelled by The Economist Intelligence Unit for the “unleashing” of rural growth, India sees considerable outfl ows of foreign capital, weakening the rupee and eroding the current-account surplus. Real incomes are reduced across the board, causing tensions among

1 http://www.panchayat.gov.in/documents/10198/370581/Panchayati_Raj_Final_pdf_02-5-11.pdf

When we look at the poverty map of India and the single-crop map, wherever there is single crop, you can also see the poverty zones,” says Mr Rao.

M V Rao, director-general of the National Institute of Rural Development in India.

22 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

India’s rural population. In response, India’s government implements further initiatives to ease rural poverty, including investment in rural infrastructure. In addition, laws against foreign investment in retail are repealed or reformed. Farmers receive a greater share of the fi nal sale price of agricultural commodities, pushing up profi tability and engaging market forces to reward productivity increases.

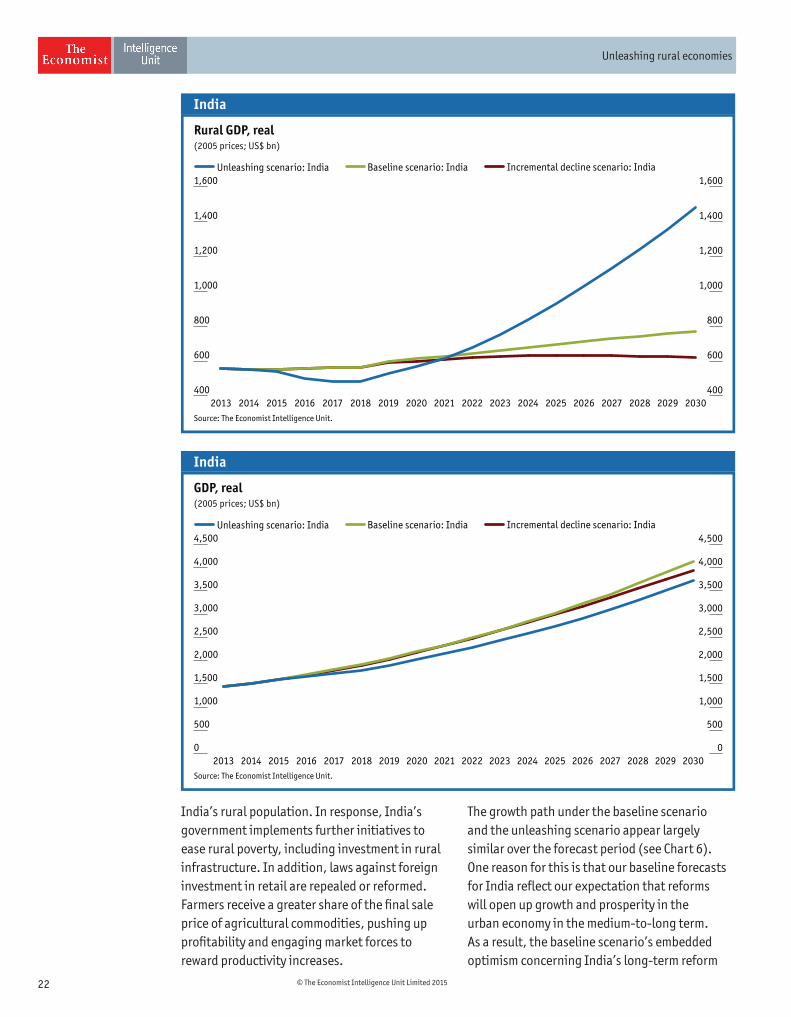

The growth path under the baseline scenario and the unleashing scenario appear largely similar over the forecast period (see Chart 6). One reason for this is that our baseline forecasts for India refl ect our expectation that reforms will open up growth and prosperity in the urban economy in the medium-to-long term. As a result, the baseline scenario’s embedded optimism concerning India’s long-term reform

India

Source: The Economist Intelligence Unit.

400

600

800

1,000

1,200

1,400

1,600

400

600

800

1,000

1,200

1,400

1,600

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: IndiaBaseline scenario: IndiaUnleashing scenario: India

Rural GDP, real(2005 prices; US$ bn)

India

Source: The Economist Intelligence Unit.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: IndiaBaseline scenario: IndiaUnleashing scenario: India

GDP, real(2005 prices; US$ bn)

23© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

India

Source: The Economist Intelligence Unit.

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: IndiaBaseline scenario: IndiaUnleashing scenario: India

Real GDP growth(%)

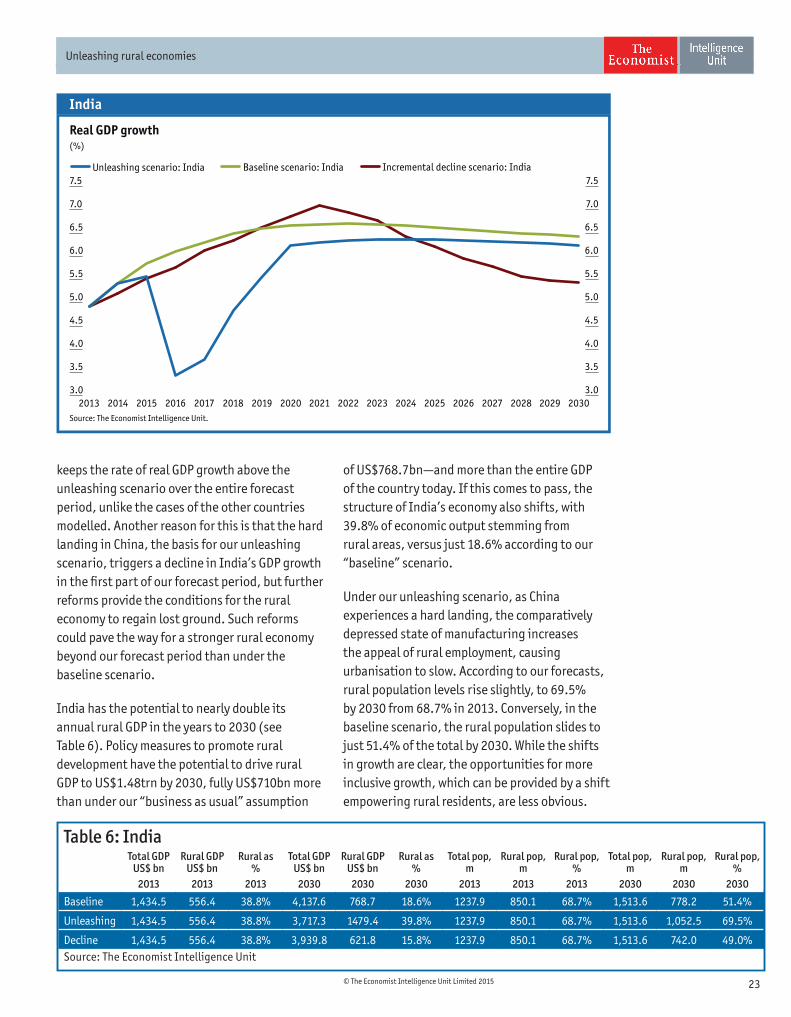

keeps the rate of real GDP growth above the unleashing scenario over the entire forecast period, unlike the cases of the other countries modelled. Another reason for this is that the hard landing in China, the basis for our unleashing scenario, triggers a decline in India’s GDP growth in the fi rst part of our forecast period, but further reforms provide the conditions for the rural economy to regain lost ground. Such reforms could pave the way for a stronger rural economy beyond our forecast period than under the baseline scenario.

India has the potential to nearly double its annual rural GDP in the years to 2030 (see Table 6). Policy measures to promote rural development have the potential to drive rural GDP to US$1.48trn by 2030, fully US$710bn more than under our “business as usual” assumption

of US$768.7bn—and more than the entire GDP of the country today. If this comes to pass, the structure of India’s economy also shifts, with 39.8% of economic output stemming from rural areas, versus just 18.6% according to our “baseline” scenario.

Under our unleashing scenario, as China experiences a hard landing, the comparatively depressed state of manufacturing increases the appeal of rural employment, causing urbanisation to slow. According to our forecasts, rural population levels rise slightly, to 69.5% by 2030 from 68.7% in 2013. Conversely, in the baseline scenario, the rural population slides to just 51.4% of the total by 2030. While the shifts in growth are clear, the opportunities for more inclusive growth, which can be provided by a shift empowering rural residents, are less obvious.

Table 6: IndiaTotal GDP

US$ bnRural GDP

US$ bnRural as

%Total GDP

US$ bnRural GDP

US$ bnRural as

%Total pop,

mRural pop,

mRural pop,

%Total pop,

mRural pop,

mRural pop,

%2013 2013 2013 2030 2030 2030 2013 2013 2013 2030 2030 2030

Baseline 1,434.5 556.4 38.8% 4,137.6 768.7 18.6% 1237.9 850.1 68.7% 1,513.6 778.2 51.4%

Unleashing 1,434.5 556.4 38.8% 3,717.3 1479.4 39.8% 1237.9 850.1 68.7% 1,513.6 1,052.5 69.5%

Decline 1,434.5 556.4 38.8% 3,939.8 621.8 15.8% 1237.9 850.1 68.7% 1,513.6 742.0 49.0%Source: The Economist Intelligence Unit

24 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Nigeria’s rural economy accounts for 47.7% of the country’s total GDP. In Nigeria, oil production has led to signifi cant environmental damage around the Niger Delta, affecting the ability of rural populations to maintain their livelihood there. A total of 85.8m people live in Nigeria’s rural areas, equivalent to 49.2% of the total 174.5m population. Expected population growth to around 272m in 20302 is likely to place emphasis on the need for food security.

Some states in Nigeria have invested in developing urban infrastructure projects as part of their urbanisation policies, at times at the expense of investment in the rural economy. “What is tending to happen in some states is that resources are almost 100% committed to [high-profi le urban-development projects, in preference to less visible rural-development projects],” says Kolawole Adebayo, a lecturer at the Federal University of Agriculture in Abeokuta (FUNAAB). Nevertheless, urbanisation is creating new markets for farm produce. Luc Rigouzzo, managing partner at Amethis Finance in France, points out that the main markets for Nigerian farm produce are now urban, rather than export-led. As Nigeria’s urban population continues to expand, Mr Rigouzzo expects, “You will see a gradual shift, where Nigerian farmers will produce more and more food crops for the urban consumer.”

A barrier to better rural economic performance is local governance. Nigeria operates a three-tier government system, comprising the federal, state and local governments. “I would look for a more decentralised Nigeria, with local government being in charge of municipal

Nigeria6facilities,” says Mr Adebayo. He believes decentralisation would free up funds that are currently earmarked for rural areas, but do not reach them, because they are blocked at federal or state level, or are used for other purposes; under decentralisation, local governments would gain autonomy that he says will allow them to have a meaningful impact on rural economies.

A further obstacle to rural economic development in Nigeria is poor social infrastructure; not least of these concerns is the fact that further investment in education is needed. Levels of literacy and education in general remain low, points out Louw Burger, managing director at Thai Farm International, which processes cassava tubers in Osasa, 120km north-east of the capital, Lagos. “As a consequence, there is reluctance to build a factory in rural areas,” he says. “The processing of the agricultural goods tends to concentrate around bigger urban areas.” Rural economies not only miss out on jobs in agriculture, but, crucially, also in ancillary sectors.

More investment in healthcare facilities and other social services is also needed. “If social infrastructure is lagging behind—if you don’t have a minimum social infrastructure or schooling or medical care—it is not very attractive for young farmers to stay in a certain region,” says Hans Jöhr, corporate head of agriculture at Nestlé in Switzerland. The point is underscored by Mr Adebayo: “The facilities in rural areas are terrible,” he says. “The more skilled human resources don’t want to stay in rural areas because they feel like second-class citizens.”

2 Economist Intelligence Unit forecast.

There is reluctance to build a factory in rural areas. The processing of the agricultural goods tends to concentrate around bigger urban areas.

Louw Burger, managing director at Thai Farm International

25© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Moreover, Nigeria’s physical infrastructure is also in need of further investment. “Fundamental infrastructure is either non-existent, bad, or very fragile at best,” observes Mr Burger. Private operators such as Thai Farm have to bear the cost of providing their own power and water: “We are not even connected to the national grid,” says Mr Burger. “We generate about a megawatt of power to provide for our own electricity needs”. Thai

Farm also relies on boreholes for water, which the fi rm purifi es itself.

The Economist Intelligence Unit’s forecasting models around the “unleashing” scenario indicate that a hard landing in China has negative consequences for Nigeria in the short-to-medium term, as oil demand from China drops. We would expect signifi cant discontent,

Nigeria

Source: The Economist Intelligence Unit.

0

50

100

150

200

250

300

350

400

450

0

50

100

150

200

250

300

350

400

450

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: NigeriaBaseline scenario: NigeriaUnleashing scenario: Nigeria

Rural GDP, real(2005 prices; US$ bn)

Nigeria

Source: The Economist Intelligence Unit.

200

300

400

500

600

700

800

900

200

300

400

500

600

700

800

900

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: NigeriaBaseline scenario: NigeriaUnleashing scenario: Nigeria

GDP, real(2005 prices; US$ bn)

26 © The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Nigeria

Source: The Economist Intelligence Unit.

0

1

2

3

4

5

6

7

8

9

0

1

2

3

4

5

6

7

8

9

203020292028202720262025202420232022202120202019201820172016201520142013

Incremental decline scenario: NigeriaBaseline scenario: NigeriaUnleashing scenario: Nigeria

Real GDP Growth(%)

which the government would address through reforms to boost agricultural performance and broader rural growth. Modelling this scenario, we included adjustments to factor in improved institutional quality and improved governance. We expect growth in capital investment, including in social infrastructure, which results in improved education outcomes, a better-educated workforce and improving economic growth.

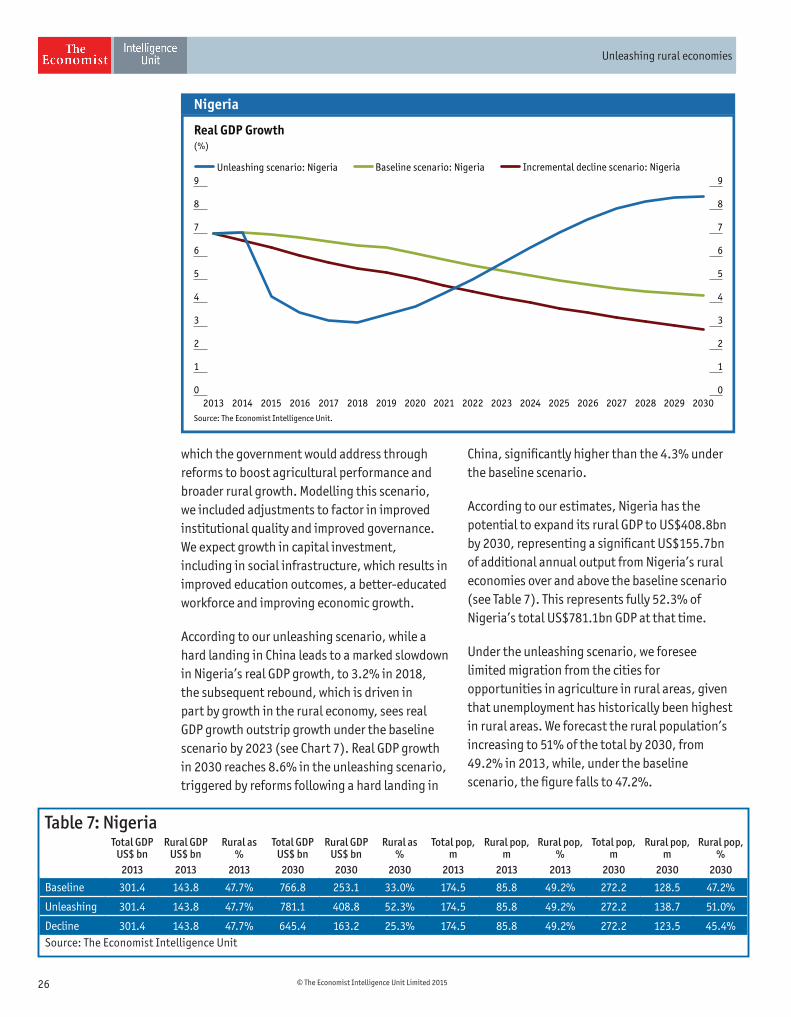

According to our unleashing scenario, while a hard landing in China leads to a marked slowdown in Nigeria’s real GDP growth, to 3.2% in 2018, the subsequent rebound, which is driven in part by growth in the rural economy, sees real GDP growth outstrip growth under the baseline scenario by 2023 (see Chart 7). Real GDP growth in 2030 reaches 8.6% in the unleashing scenario, triggered by reforms following a hard landing in

China, signifi cantly higher than the 4.3% under the baseline scenario.

According to our estimates, Nigeria has the potential to expand its rural GDP to US$408.8bn by 2030, representing a signifi cant US$155.7bn of additional annual output from Nigeria’s rural economies over and above the baseline scenario (see Table 7). This represents fully 52.3% of Nigeria’s total US$781.1bn GDP at that time.

Under the unleashing scenario, we foresee limited migration from the cities for opportunities in agriculture in rural areas, given that unemployment has historically been highest in rural areas. We forecast the rural population’s increasing to 51% of the total by 2030, from 49.2% in 2013, while, under the baseline scenario, the fi gure falls to 47.2%.

Table 7: NigeriaTotal GDP

US$ bnRural GDP

US$ bn Rural as

%Total GDP

US$ bnRural GDP

US$ bn Rural as

%Total pop,

mRural pop,

mRural pop,

%Total pop,

mRural pop,

mRural pop,

%2013 2013 2013 2030 2030 2030 2013 2013 2013 2030 2030 2030

Baseline 301.4 143.8 47.7% 766.8 253.1 33.0% 174.5 85.8 49.2% 272.2 128.5 47.2%

Unleashing 301.4 143.8 47.7% 781.1 408.8 52.3% 174.5 85.8 49.2% 272.2 138.7 51.0%

Decline 301.4 143.8 47.7% 645.4 163.2 25.3% 174.5 85.8 49.2% 272.2 123.5 45.4%Source: The Economist Intelligence Unit

27© The Economist Intelligence Unit Limited 2015

Unleashing rural economies

Conclusion

Policies aimed at stimulating rural development have the potential to unlock US$2trn of extra rural economic output across the globe by 2030, our forecasts indicate.

Within this headline fi gure, reforms aimed at promoting rural development are signifi cant, because a strong rural economy, in itself, has the potential to add balance to, and, indeed, to bolster overall economic growth.

Crucially, a strong rural economy has the opportunity to benefi t from the multiplier effect across the agricultural sector and ancillary industries that operate around food production and related manufacturing activities. Moreover, a diversifi ed rural economy will see the growth of service sectors such as healthcare, education, leisure and tourism.

Investing in rural growth may also offer a means by which to lessen the economy’s exposure to exogenous events—such as a global economic slowdown—for example, in the case of economies that are heavily reliant on manufacturing exports.

Not least, solid rural economic performance is critical for individual regions and nations as a tool with which to reduce income disparities between the rural and urban populations, reducing poverty and bringing rural living standards into line with those in urban areas.

The fi ndings of the economic-modelling exercise and in-depth interview programme that form part of this research demonstrate that policymakers across the globe have a number of policy levers at their disposal with which to strengthen rural

development and unlock rural economic growth, with positive consequences for overall growth and development.

These policy levers may be applied to a number of different—but interlinked—areas, including reform of rural governance, legal reforms addressing land ownership and use, investment in operational infrastructure, such as roads or storage facilities, as well as investment in social infrastructure, such as education and healthcare facilities.

As Robin Bourgeois, senior foresight expert at the Global Forum on Agricultural Research, asserts, “One of the key drivers is the willingness to invest, from a policy point of view, in a more balanced, territorial development.”

This research also demonstrates that policymakers have the opportunity to take a holistic approach to government—embracing rural development as an integral part of national economic growth—to promote rural development as an integral part of wider economic and social wellbeing.

The steps necessary to unlock growth, as discussed in this report, provide an indication of the measures that are possible. The trigger employed in this modelling endeavour and the reforms highlighted as part of this research by no means represent the only path to unleashing rural economic growth. Rather, this report lays out some of the options and routes forward. A more dynamic trajectory for rural economies is possible, and effective reforms would meaningfully improve the lives of billions.

While every effort has been taken to verify the accuracy of this information, The Economist Intelligence Unit cannot accept any responsibility or liability for reliance by any person on this report or any of the information, opinions or conclusions set out in this report.

LONDON20 Cabot SquareLondonE14 4QWUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8500E-mail: [email protected]

NEW YORK750 Third Avenue5th FloorNew York, NY 10017United StatesTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

HONG KONG6001, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

GENEVARue de l’Athénée 321206 GenevaSwitzerlandTel: (41) 22 566 2470Fax: (41) 22 346 93 47E-mail: [email protected]