Embed Size (px)

DESCRIPTION

AACIMP 2011 Summer School. Operational Research stream. Lecture by Gerhard-Wilhelm Weber.

Citation preview

Portfolio Optimization

Gerhard-Wilhelm Weber1 Erik Kropat2 Zafer-Korcan Görgülü3

1Institute of Applied MathematicsMiddle East Technical University

Ankara, Turkey

2Department of MathematicsUniversity of Erlangen-Nuremberg

Erlangen, Germany

3University of the Federal Armed ForcesMunich, Germany

2008

1 / 477

Outline I

1 The Mean-Variance Approach in a One-Period ModelIntroduction

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

2 / 477

Outline II

3 Option PricingIntroductionExamplesThe Replication PrincipleArbitrage OpportunityContinuationPartial Differential Approach (PDA)Arbitrage & Option Pricing

3 / 477

Outline III

4 Pricing of Exotic Options and Numerical AlgorithmsIntroductionExamplesExamplesEquivalent Martingale MeasureExotic Options with Explicit Pricing FormulaeWeak Convergence of Stochastic ProcessesMonte-Carlo SimulationApproximation via Binomial TreesThe Pathwise Binomial Approach of Rogers and Stapleton

4 / 477

Outline IV

5 Optimal PortfoliosIntroduction and Formulation of the ProblemThe martingale methodOptimal Option PortfoliosExcursion 8: Stochastic ControlMaximize expected value in presence of quadratic control costsIntroductionPortfolio Optimization via Stochastic Control Method

5 / 477

Outline

1 The Mean-Variance Approach in a One-Period Model

6 / 477

Outline

1 The Mean-Variance Approach in a One-Period ModelIntroduction

7 / 477

Introduction

MVA Based on H. MARKOWITZ

OPM • Decisions on investment strategies only at the beginning of theperiod

• Consequences of these decisions will be observed at the end of theperiod (−→ no action in between: static model )

8 / 477

The one-period model

Market with d traded securitiesd different securities with positive prices p1, . . . , pd at time t = 0

Security prices P1(T ), . . . , Pd (T ) at final time t = T notforeseeable−→ modeled as non-negative random variables on probability space

(Ω,F ,P)

9 / 477

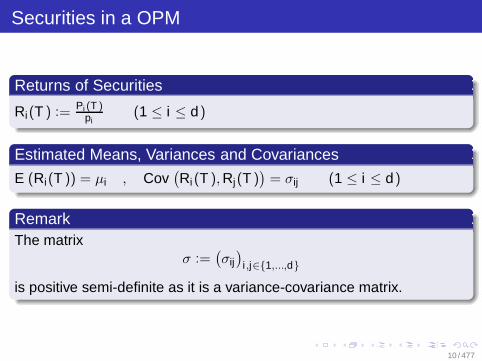

Securities in a OPM

Returns of Securities

Ri(T ) := Pi (T )pi

(1 ≤ i ≤ d)

Estimated Means, Variances and Covariances

E (Ri(T )) = µi , Cov(Ri(T ), Rj(T )

)= σij (1 ≤ i ≤ d)

RemarkThe matrix

σ :=(σij)

i ,j∈1,...,d

is positive semi-definite as it is a variance-covariance matrix.

10 / 477

Securities in a OPM

Each security perfectly divisable

Hold ϕi ∈ R shares of security i (1 ≤ i ≤ d)

Negative position (ϕi < 0 for some i) corresponds to a selling−→ Not allowed in OPM

−→ No negative positions: pi ≥ 0 (1 ≤ i ≤ d)−→ No transaction costs

11 / 477

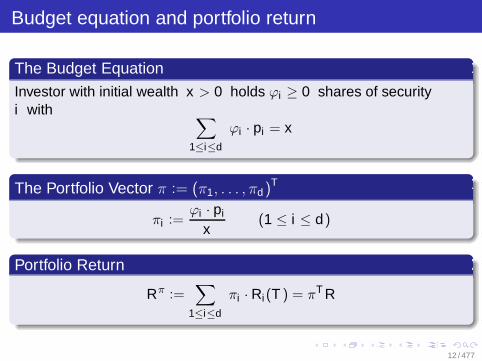

Budget equation and portfolio return

The Budget EquationInvestor with initial wealth x > 0 holds ϕi ≥ 0 shares of securityi with ∑

1≤i≤d

ϕi · pi = x

The Portfolio Vector π := (π1, . . . , πd)T

πi :=ϕi · pi

x(1 ≤ i ≤ d)

Portfolio Return

Rπ :=∑

1≤i≤d

πi · Ri(T ) = πT R

12 / 477

Budget equation and portfolio return

Remarkπi . . . fraction of total wealth invested in security i

∑

1≤i≤d

πi =

∑1≤i≤d

ϕi · pi

x=

xx

= 1

Xπ(T ) . . . final wealth corresponding to x and π

Xπ(T ) =∑

1≤i≤d

ϕi · Pi(T )

13 / 477

Budget equation and portfolio return

Remark (continued)Portfolio Return

Rπ =∑

1≤i≤d

πi · Ri(T ) =∑

1≤i≤d

ϕi · pi

x· Pi(T )

pi=

Xπ(T )

x

Portfolio Mean and Portfolio Variance

E (Rπ) =∑

1≤i≤d

πi · µi , Var (Rπ) =∑

1≤i ,j≤d

πi · σij · πj

14 / 477

Selection of a portfolio–criterion

(i) Maximize mean return (choose security of highest mean return)−→ risky, big fluctuations of return

(ii) Minimize risk of fluction

15 / 477

Selection of a portfolio–approach by Markowitz (MVA)

Balance Risk (Portfolio Variance) and Return (Portfolio Mean)(i) Maximize E (Rπ) under given upper bound c1 for Var (Rπ)

maxπ∈Rd

E (Rπ) subject to

πi ≥ 0 (1 ≤ i ≤ d)∑

1≤i≤d

πi = 1

Var (Rπ) ≤ c1

(ii) Minimize Var (Rπ) under given lower bound c2 for E (Rπ)

minπ∈Rd

Var (Rπ) subject to

πi ≥ 0 (1 ≤ i ≤ d)∑

1≤i≤d

πi = 1

E (Rπ) ≥ c2

16 / 477

Solution methods

(i) Linear Optimization Problem with quadratic constraint−→ No standard algorithms, numerical inefficient

(ii) Quadratic Optimization Problem with positive semidefiniteobjective matrix σ

−→ efficient algorithms (i.e., GOLDFARB/IDNANI, GILL/MURRAY)Feasible region non-empty if c2 ≤ max

1≤i≤dµi

σ positive definite and feasible region non-empty−→ unique solution (even if one security riskless)

17 / 477

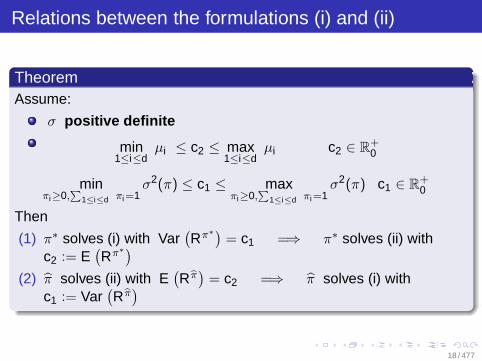

Relations between the formulations (i) and (ii)

TheoremAssume:

σ positive definite

min1≤i≤d

µi ≤ c2 ≤ max1≤i≤d

µi c2 ∈ R+0

minπi≥0,

∑1≤i≤d πi=1

σ2(π) ≤ c1 ≤ maxπi≥0,

∑1≤i≤d πi=1

σ2(π) c1 ∈ R+0

Then

(1) π∗ solves (i) with Var(Rπ∗)

= c1 =⇒ π∗ solves (ii) withc2 := E

(Rπ∗)

(2) π solves (ii) with E(Rπ)

= c2 =⇒ π solves (i) withc1 := Var

(Rπ)

18 / 477

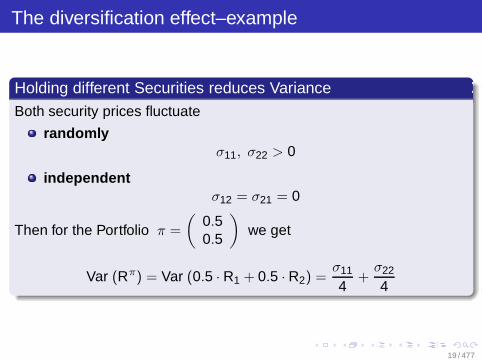

The diversification effect–example

Holding different Securities reduces VarianceBoth security prices fluctuate

randomlyσ11, σ22 > 0

independentσ12 = σ21 = 0

Then for the Portfolio π =

(0.50.5

)we get

Var (Rπ) = Var (0.5 · R1 + 0.5 · R2) =σ11

4+

σ22

4

19 / 477

The diversification effect–example

Holding different Securities reduces Variance

−→ If σ11 = σ22 then the Variance of Portfolio(

0.50.5

)is half as big

as that of(

10

)or(

01

)

−→ Reduction of Variance . . . Diversification Effect depends onnumber of traded securities

20 / 477

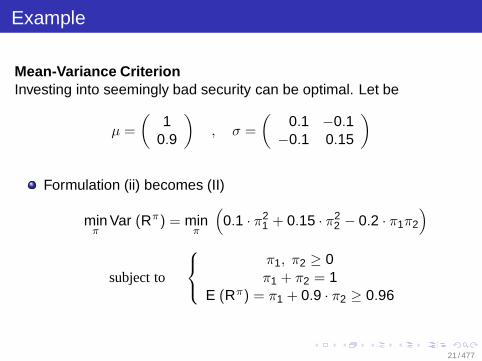

Example

Mean-Variance CriterionInvesting into seemingly bad security can be optimal. Let be

µ =

(1

0.9

), σ =

(0.1 −0.1

−0.1 0.15

)

Formulation (ii) becomes (II)

minπ

Var (Rπ) = minπ

(0.1 · π2

1 + 0.15 · π22 − 0.2 · π1π2

)

subject to

π1, π2 ≥ 0π1 + π2 = 1

E (Rπ) = π1 + 0.9 · π2 ≥ 0.96

21 / 477

Example

Consider Portfolios(

10

)and

(0.50.5

)(does not satify

expectation constraint)

Var(

R(1,0)T)

= 0.1 , E(

R(1,0)T)

= 1

Var(

R(0.5,0.5)T)

= 0.125 , E(

R(0.5,0.5)T)

= 0.95

22 / 477

Example

Ignore expectation constraint and rememberπ1, π2 ≥ 0 π1 + π2 = 1. Hence

minπ

(0.1 · π2

1 + 0.15 · (1 − π1)2 − 0.2 · π1 · (1 − π1)

)

= minπ

(0.45 · π2

1 − 0.5 · π1 + 0.15)

−→ Minimizing Portfolio (No solution of (II) but better than(

0.50.5

))

π =19·(

54

)

−→ Portfolio Return Variance Var(

R( 59 ,

49 )

T)= 0.001

−→ Portfolio Return Mean E(

R( 59 ,

49 )

T)= 0.95

23 / 477

Example

0.0 0.5 0.6 1.00.0

0.4

0.5

1.0

π1

π2

Pairs (π1, π2) satisfying expectation constraint are above thedotted line

Intersect with line π1 + π2 = 1−→ Feasible region of MeanVariance Problem (bold line)

24 / 477

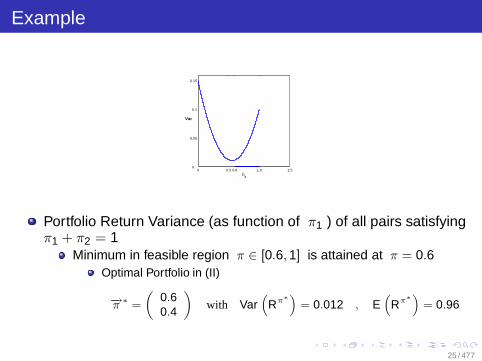

Example

0 0.5 0.6 1.0 1.50

0.05

0.1

0.15

π1

Var

Portfolio Return Variance (as function of π1 ) of all pairs satisfyingπ1 + π2 = 1

Minimum in feasible region π ∈ [0.6, 1] is attained at π = 0.6Optimal Portfolio in (II)

−→π

∗ =

(0.60.4

)with Var

(Rπ∗

)= 0.012 , E

(Rπ∗

)= 0.96

25 / 477

Stock price model

OPMNo assumption on distribution of security returns

Solving MV Problem just needed expectations and covariances

26 / 477

Stock price model

OPM with just one security (price p1 at time t = 0 )At time T security may have price d · p1 or u · p1

q : probability of decreasing by factor d1 − q : probability of increasing by factor u (u > d)

Mean and Variance of Return

E (R1(T )) = E(

P1(T )

p1

)= q · u + (1 − q) · d

Var (R1(T )) = Var(

P1(T )

p1

)= q · u2 + (1 − q) · d2

− (q · u + (1 − q) · d)2

27 / 477

Stock price model

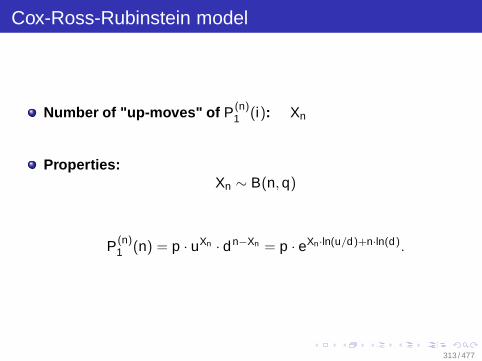

OPM with just one security (price p1 at time t = 0 )After n periods the security has price

P1(n · T ) = p1 · uXn · dn−Xn

with Xn ∼ B(n, p) number of up-movements of price inn periods

28 / 477

Comments on MVA

Only trading at initial time t = 0

No reaction to current price changes possible( −→ static model )

Risk of investment only modeled by variance of return

Need of Continuous-Time Market ModelsDiscrete-time multi-period models(many periods −→ no fast algorithms)

29 / 477

Outline

2 The Continuous-Time Market Model

30 / 477

Outline

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

31 / 477

Modeling the security prices

Market with d+1 securitiesd risky stocks withprices p1, p2, . . . , pd at time t = 0 andrandom prices P1(t), P2(t), . . . , Pd (t) at times t > 0

1 bond withprice p0 at time t = 0 anddeterministic price P0(t) at times t > 0.

Assume: Perfectly devisible securities, no transaction costs.

⇒ Modeling of the price development on the time interval [0, T ].

32 / 477

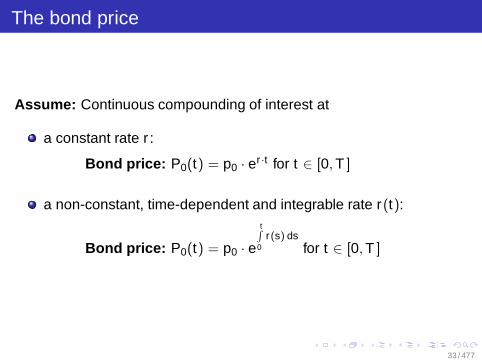

The bond price

Assume: Continuous compounding of interest at

a constant rate r :

Bond price: P0(t) = p0 · er ·t for t ∈ [0, T ]

a non-constant, time-dependent and integrable rate r(t):

Bond price: P0(t) = p0 · e

t∫

0r(s) ds

for t ∈ [0, T ]

33 / 477

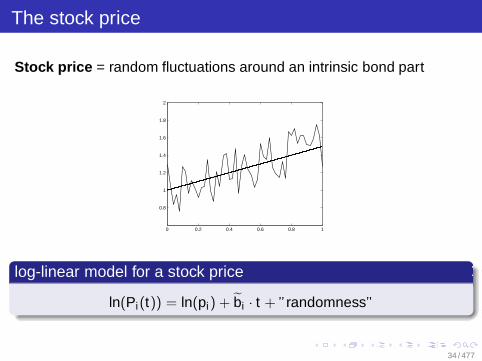

The stock price

Stock price = random fluctuations around an intrinsic bond part

0 0.2 0.4 0.6 0.8 1

0.8

1

1.2

1.4

1.6

1.8

2

log-linear model for a stock price

ln(Pi(t)) = ln(pi) + bi · t + ”randomness”

34 / 477

The stock price

Randomness is assumed

to have no tendency, i.e., E("randomness") = 0,

to be time-dependent,

to represent the sum of all deviations ofln(Pi(t)) from ln(pi) + bi · t on [0, T ],

∼ N (0, σ2t) for some σ > 0.

35 / 477

The stock price

Deviation at time t

Y (t) := ln(Pi(t)) − ln(pi) − bi · t

withY (t) ∼ N (0, σ2t)

Properties:

E(Y (t)) = 0,

Y (t) is time-dependent.

36 / 477

The stock price

Y (t) = Y (δ) + (Y (t) − Y (δ)), δ ∈ (0, t)

Distribution of the increments of the deviation Y (t) − Y (δ)

depends only on the time span t − δ

is independent of Y (s), s ≤ δ

=⇒ Y (t) − Y (δ) ∼ N(0, σ2(t − δ)

)

37 / 477

The stock price

Existence and properties of the stochastic process

Y (t)t∈[0,∞)

will be studied in the excursion on the Brownian motion .

38 / 477

Outline

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

39 / 477

General assumptions

General assumptionsLet (Ω,F , P) be a complete probability space with sample space Ω,σ-field F and probability measure P.

40 / 477

Filtration

DefinitionLet Ftt∈I be a family of sub-σ-fields of F , I be an ordered index setwith Fs ⊂ Ft for s < t , s, t ∈ I. The family Ftt∈I is called a filtration.

A filtration describes flow of information over time.

Ft models events observable up to time t .

If a random variable Xt is Ft -measurable, we are able todetermine its value from the information given at time t .

41 / 477

Stochastic process

DefinitionA set (Xt , Ft)t∈I consisting of a filtration Ftt∈I and a family ofR

n-valued random variables Xtt∈I with Xt being Ft -measurable iscalled a stochastic process with filtration Ftt∈I .

42 / 477

Remark

RemarkI = [0,∞) or I = [0, T ].

Canoncial filtration (natural filtration) of Xtt∈I :

Ft := FXt := σXs | s ≤ t , s ∈ I.

Notation: Xtt∈I = X (t)t∈I = X .

43 / 477

Sample path

Sample pathFor fixed ω ∈ Ω the set

X .(ω) := Xt(ω)t∈I = X (t , ω)t∈I

is called a sample path or a realization of the stochastic process.

44 / 477

Identification of stochastic processes

Can two stochastic processes be identified with each other?

DefinitionLet (Xt , Ft)t∈[0,∞) and (Yt , Gt)t∈[0,∞) be two stochastic processes.Y is a modification of X , if

Pω |Xt(ω) = Yt(ω) = 1 for all t ≥ 0.

DefinitionLet (Xt , Ft)t∈[0,∞) and (Yt , Gt)t∈[0,∞) be two stochastic processes.X and Y are indistinguishable, if

Pω |Xt(ω) = Yt(ω) for all t ∈ [0,∞) = 1.

45 / 477

Identification of stochastic processes

RemarkX , Y indistinguishable ⇒ Y modification of X .

TheoremLet the stochastic process Y be a modification of X . If both processeshave continuous sample paths P-almost surely, then X and Y areindistinguishable.

46 / 477

Brownian motion

DefinitionThe real-valued process Wtt≥0 with continuous sample paths and

i) W0 = 0 P-a.s.

ii) Wt − Ws ∼ N (0, t − s) for 0 ≤ s < t"stationary increments"

iii) Wt − Ws independent of Wu − Wr for 0 ≤ r ≤ u ≤ s < t"independent increments"

is called a one-dimensional Brownian motion.

47 / 477

Brownian motion

RemarkBy an n-dimensional Brownian motion we mean the R

n-valued process

W (t) = (W1(t), . . . , Wn(t)),

with components Wi being independent one-dimensional Brownianmotions.

48 / 477

Brownian motion and filtration

Brownian motion can be associated with

natural filtration

FWt := σWs |0 ≤ s ≤ t, t ∈ [0,∞)

P-augmentation of the natural filtration (Brownian filtration)

Ft := σFWt ∪ N |N ∈ F , P(N) = 0, t ∈ [0,∞)

49 / 477

Brownian motion and filtration

Requirement iii) of a Brownian motion with respect to a filtrationFtt≥0 is often stated as

iii)∗ Wt − Ws independent of Fs, 0 ≤ s < t .

Ftt≥0 natural filtration (Brownian filtration)

⇒ iii) and iii)∗ are equivalent.

Ftt≥0 arbitrary filtration

⇒ iii) and iii)∗ are usually not equivalent.

ConventionIf we consider a Brownian motion (Wt ,Ft)t≥0 with an arbitraryfiltration we implicitly assume iii)∗ to be fulfilled.

50 / 477

Existence of the Brownian motion

How can we show the existence of a stochastic process satisfying therequirements of a Brownian motion?

Construction and existence proofs are long and technical.

Construction based on weak convergence and approximation byrandom walks [Billingsley 1968].

Wiener measure, Wiener process.

51 / 477

Brownian motion and filtration

TheoremThe Brownian filtration Ftt≥0 is right-continuous as well asleft-continuous, i.e., we have

Ft = Ft+ :=⋂

ε>0

Ft+ε and Ft = Ft− := σ

(⋃

s<t

Fs

).

DefinitionA filtration Gtt≥0 satifies the usual conditions, if it is right-continuousand G0 contains all P-null sets of F .

General assumption for this sectionLet Ftt≥0 be a filtration which satisfies the usual conditions.

52 / 477

Martingales

DefinitionThe real-valued process (Xt ,Ft)t∈I with E |Xt | < ∞ for all t ∈ I(where I is an ordered index set), is called

a super-martingale, if for all s, t ∈ I with s ≤ t we have

E(Xt |Fs) ≤ Xs P-a.s. ,

a sub-martingale, if for all s, t ∈ I with s ≤ t we have

E(Xt |Fs) ≥ Xs P-a.s. ,

a martingale, if for all s, t ∈ I with s ≤ t we have

E(Xt |Fs) = Xs P-a.s. .

53 / 477

Interpretation of the martingale concept

Example: Modeling games of chance

Xn: Wealth of a gambler after n-th participation in a fair game

Martingale condition: E(Xn+1|Fn) = Xn P-a.s.

⇒ "After the game the player is as rich as he was before"

favorable game = sub-martingalenon-favorable game = super-martingale

54 / 477

Interpretation of the martingale concept

Example: Tossing a fair coin

"Head": Gambler receives one dollar

"Tail": Gambler loses one dollar

⇒ Martingale

55 / 477

Interpretation of the martingale concept

TheoremA one-dimensional Brownian motion Wt is a martingale.

RemarkEach stochastic process with independent, centered increments isa martingale with respect to its natural filtration.

The Brownian motion with drift µ and volatility σ

Xt := µt + σWt , µ ∈ R, σ ∈ R

is a martingale if µ = 0, a super-martingale if µ ≤ 0 and asub-martingale if µ ≥ 0.

56 / 477

Interpretation of the martingale concept

Theorem(1) Let (Xt , Ft)t∈I be a martingale and ϕ : R → R be a convex

function with E |ϕ(Xt)| < ∞ for all t ∈ I. Then

(ϕ(Xt ),Ft)t∈I

is a sub-martingale.

(2) Let (Xt , Ft)t∈I be a sub-martingale and ϕ : R → R a convex,non-decreasing function with E |ϕ(Xt)| < ∞ for all t ∈ I. Then

(ϕ(Xt ),Ft)t∈I

is a sub-martingale.

57 / 477

Interpretation of the martingale concept

Remark(1) Typical applications are given by

ϕ(x) = x2, ϕ(x) = |x |.

(2) The theorem is also valid for d -dimensional vectors

X (t) = (X1(t), . . . , Xd(t))

of martingales and convex functions ϕ : Rd → R.

58 / 477

Stopping time

DefinitionA stopping time with respect to a filtration Ftt∈[0,∞)

(or Fnn∈N) is an F-measurable random variable

τ : Ω → [0,∞] (or τ : Ω → N ∪ ∞)

with ω ∈ Ω | τ(ω) ≤ t ∈ Ft for all t ∈ [0,∞)(or ω ∈ Ω | τ(ω) ≤ n ∈ Fn for all n ∈ N).

TheoremIf τ1, τ2 are both stopping times then τ1 ∧ τ2 := minτ1, τ2 is also astopping time.

59 / 477

The stopped process

The stopped processLet (Xt , Ft)t∈I be a stochastic process, let I be either N or [0,∞),and τ a stopping time. The stopped process Xt∧τt∈I is defined by

Xt∧τ (ω) :=

Xt(ω) if t ≤ τ(ω),

Xτ(ω)(ω) if t > τ(ω).

Example: Wealth of a gambler who participates in a sequence ofgames until he is either bankrupt or has reached a given level ofwealth.

60 / 477

The stopped filtration

The stopped filtrationLet τ be a stopping time with respect to a filtration Ftt∈[0,∞).

σ-field of events determined prior to the stopping time τ

Fτ := A ∈ F |A ∩ τ ≤ t ∈ Ft for all t ∈ [0,∞)

Stopped filtrationFτ∧tt∈[0,∞).

61 / 477

The stopped filtration

What will happen if we stop a martingale or a sub-martingale?

Theorem: Optional sampling

Let (Xt , Ft)t∈[0,∞) be a right-continuous sub-martingale (ormartingale). Let τ1, τ2 be stopping times with τ1 ≤ τ2. Then for allt ∈ [0,∞) we have

E(Xt∧τ2 | Ft∧τ1) ≥ Xt∧τ1 P-a.s.

(orE(Xt∧τ2 | Ft∧τ1) = Xt∧τ1 P-a.s.).

62 / 477

The stopped filtration

CorollaryLet τ be a stopping time and (Xt , Ft)t∈[0,∞) a right-continuoussub-martingale (or martingale). Then the stopped process(Xt∧τ ,Ft)t∈[0,∞) is also a sub-martingale (or martingale).

63 / 477

The stopped filtration

TheoremLet (Xt , Ft)t∈[0,∞) be a right-continuous process. Then Xt is amartingale if and only if for all bounded stopping times τ we have

EXτ = EX0.

→ Characterization of a martingale

64 / 477

The stopped filtration

DefinitionLet (Xt , Ft)t∈[0,∞) be a stochastic process with X0 = 0. If there is anon-decreasing sequence τnn∈N of stopping times with

P(

limn→∞

τn = ∞)

= 1,

such that (X (n)

t := (Xt∧τn ,Ft)

)

t∈[0,∞)

is a martingale for all n ∈ N, then X is a local martingale. Thesequence τnn∈N is called a localizing sequence corresponding to X .

65 / 477

The stopped filtration

Remark(1) Each martingale is a local martingale.

(2) A local martingale with continuous paths is calledcontinuous local martingale.

(3) There exist local martingales which are not martingales.

E(Xt) need not exist for a local martingale. However, theexpectation has to exist along the localizing sequence t ∧ τn.

The local martingale is a martingale on the random timeintervals [0, τn].

TheoremA non-negative local martingale is a super-martingale.

66 / 477

The stopped filtration

Theorem: Doob’s inequalityLet Mtt≥0 be a martingale with right-continuous paths andE(M2

T ) < ∞ or all T > 0. Then, we have

E((

sup0≤t≤T

|Mt |)2)

≤ 4 · E(M2T ).

TheoremLet (Xt , Ft)t∈[0,∞) be a non-negative super-martingale withright-continuous paths. Then, for λ > 0 we obtain

λ · P

ω

∣∣∣∣ sup0≤s≤t

Xs(ω) ≥ λ

≤ E(X0).

67 / 477

Outline

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

68 / 477

Continuation: The stock price

log-linear model for a stock price

ln(Pi(t)) = ln(pi) + bi · t + ”randomness”

Brownian motion (Wt , Ft)t≥0 is the appropriate stochastic process tomodel the "randomness"

69 / 477

Continuation: The stock price

Market with one stock and one bond (d=1)

ln(P1(t)) = ln(p1) + b1 · t + σ11Wt

P1(t) = p1 · exp(b1 · t + σ11Wt

)

Market with d stocks and one bond (d>1)

ln(Pi(t)) = ln(pi) + bi · t +

m∑

j=1

σijWj(t), i = 1, . . . , d

Pi(t) = pi · exp(

bi · t +

m∑

j=1

σijWj(t))

, i = 1, . . . , d

70 / 477

Continuation: The stock price

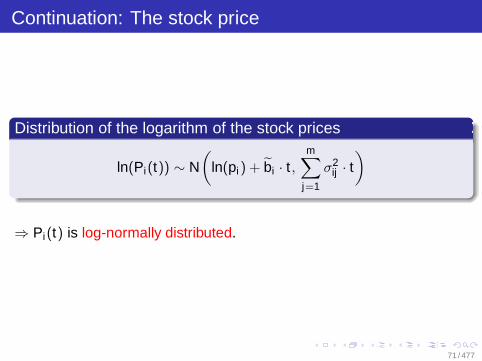

Distribution of the logarithm of the stock prices

ln(Pi(t)) ∼ N(

ln(pi) + bi · t ,m∑

j=1

σ2ij · t)

⇒ Pi(t) is log-normally distributed.

71 / 477

Continuation: The stock price

Lemma

Let bi := bi + 12

m∑

j=1

σ2ij for i = 1, . . . , d.

(1) E(Pi(t)) = pi · ebi t .

(2) Var(Pi(t)) = p2i · exp(2bi t) ·

(exp

( m∑

j=1

σ2ij t)− 1)

.

(3) Xt := a · exp( m∑

j=1

(cjWj(t) −

12

c2j t))

with a, cj ∈ R, j = 1, . . . , m

is a martingale.

72 / 477

Interpretation of the stock price model

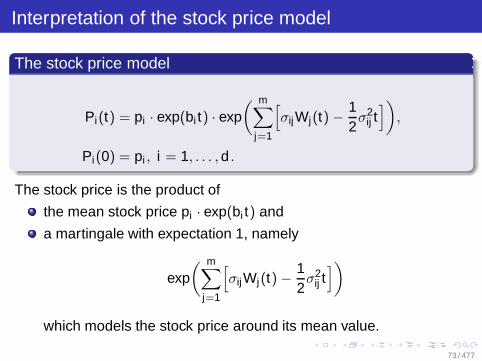

The stock price model

Pi(t) = pi · exp(bi t) · exp( m∑

j=1

[σijWj(t) −

12σ2

ij t])

,

Pi(0) = pi , i = 1, . . . , d .

The stock price is the product of

the mean stock price pi · exp(bi t) and

a martingale with expectation 1, namely

exp( m∑

j=1

[σijWj(t) −

12σ2

ij t])

which models the stock price around its mean value.

73 / 477

Interpretation of the stock price model

Vector of mean rates of stock returns

b = (b1, . . . , bd )T

Volatility matrix

σ =

σ11 . . . σ1m...

. . ....

σd1 . . . σdm

Pi(t) is a geometric Brownian motion with drift bi and volatilityσi . = (σi1, . . . , σim)T .

74 / 477

Summary: Stock prices

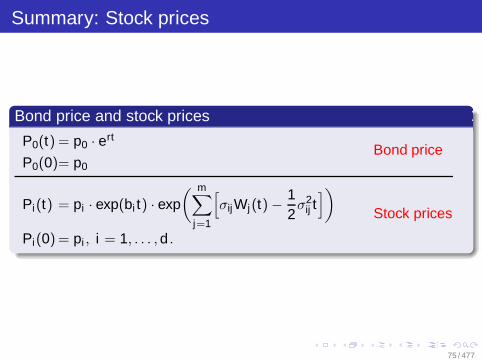

Bond price and stock prices

P0(t) = p0 · ertBond price

P0(0)= p0

Pi(t) = pi · exp(bi t) · exp( m∑

j=1

[σijWj(t) −

12

σ2ij t])

Stock prices

Pi(0) = pi , i = 1, . . . , d .

75 / 477

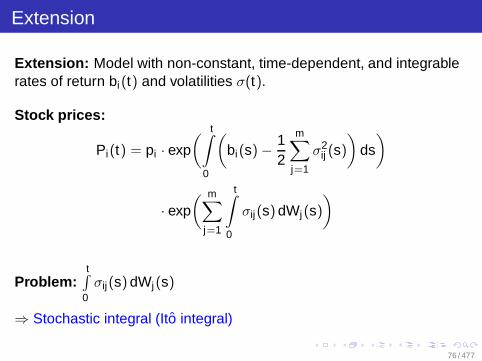

Extension

Extension: Model with non-constant, time-dependent, and integrablerates of return bi(t) and volatilities σ(t).

Stock prices:

Pi(t) = pi · exp( t∫

0

(bi(s) − 1

2

m∑

j=1

σ2ij (s)

)ds)

· exp( m∑

j=1

t∫

0

σij(s) dWj(s)

)

Problem:t∫

0σij(s) dWj(s)

⇒ Stochastic integral (Ito integral)

76 / 477

Outline

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

77 / 477

The Ito integral

Is it possible to define the stochastic integral

t∫

0

Xs(ω) dWs(ω)

ω-wise in a reasonable way?

78 / 477

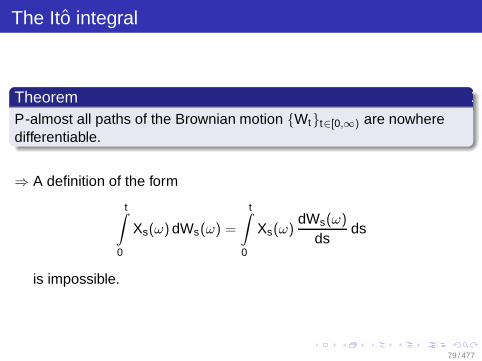

The Ito integral

TheoremP-almost all paths of the Brownian motion Wtt∈[0,∞) are nowheredifferentiable.

⇒ A definition of the form

t∫

0

Xs(ω) dWs(ω) =

t∫

0

Xs(ω)dWs(ω)

dsds

is impossible.

79 / 477

The Ito integral

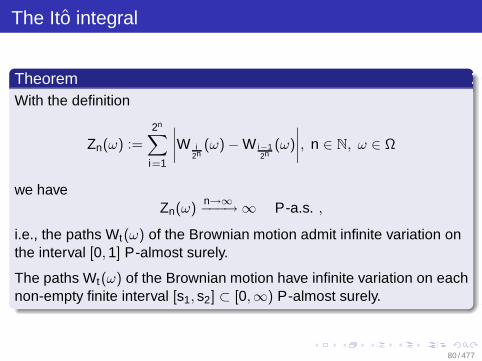

TheoremWith the definition

Zn(ω) :=

2n∑

i=1

∣∣∣∣W i2n

(ω) − W i−12n

(ω)

∣∣∣∣, n ∈ N, ω ∈ Ω

we haveZn(ω)

n→∞−−−→ ∞ P-a.s. ,

i.e., the paths Wt(ω) of the Brownian motion admit infinite variation onthe interval [0, 1] P-almost surely.

The paths Wt(ω) of the Brownian motion have infinite variation on eachnon-empty finite interval [s1, s2] ⊂ [0,∞) P-almost surely.

80 / 477

General assumptions

General assumptions for this sectionLet (Ω,F , P) be a complete probability space equipped with a filtrationFtt satisfying the usual conditions. Further assume that on thisspace a Brownian motion (Wt ,Ft)t∈[0,∞) with respect to this filtrationis defined.

81 / 477

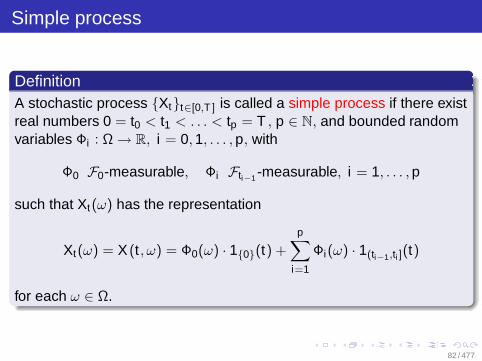

Simple process

DefinitionA stochastic process Xtt∈[0,T ] is called a simple process if there existreal numbers 0 = t0 < t1 < . . . < tp = T , p ∈ N, and bounded randomvariables Φi : Ω → R, i = 0, 1, . . . , p, with

Φ0 F0-measurable, Φi Fti−1 -measurable, i = 1, . . . , p

such that Xt(ω) has the representation

Xt(ω) = X (t , ω) = Φ0(ω) · 10(t) +

p∑

i=1

Φi(ω) · 1(ti−1,ti ](t)

for each ω ∈ Ω.

82 / 477

Simple process

RemarkXt is Fti−1-measurable for all t ∈ (ti−1, ti ].

The paths X (., ω) of the simple process Xt are left-continuous stepfunctions with height Φi(ω) · 1(ti−1,ti ](t).

0 T0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

t

X(.,ω)

t1

t2

t3

83 / 477

Stochastic integral

DefinitionFor a simple process Xtt∈[0,T ] the stochastic integral I.(X ) fort ∈ (tk , tk+1] is defined according to

It(X ) :=

t∫

0

Xs dWs :=∑

1≤i≤k

Φi(Wti − Wti−1) + Φk+1(Wt − Wtk ),

or more generally for t ∈ [0, T ]:

It(X ) :=

t∫

0

Xs dWs :=∑

1≤i≤p

Φi(Wti∧t − Wti−1∧t).

84 / 477

Stochastic integral

Theorem: Elementary properties of the stochastic integral

Let X := Xtt∈[0,T ] be a simple process. Then we have

(1) It(X )t∈[0,T ] is a continuous martingale with respect to Ftt∈[0,T ].In particular, we have E(It(X )) = 0 for all t ∈ [0, T ].

(2) E( t∫

0Xs dWs

)2

= E( t∫

0X 2

s ds)

for t ∈ [0, T ].

(3) E(

sup0≤t≤T

∣∣∣∣t∫

0Xs dWs

∣∣∣∣)2

≤ 4 · E( T∫

0X 2

s ds)

.

85 / 477

Stochastic integral

Remark(1) By (2) the stochastic integral is a square-integrable stochastic

process.

(2) For the simple process X ≡ 1 we obtain

t∫

0

1 dWs = Wt

and

E( t∫

0

dWs

)2

= E(W 2t ) = t =

t∫

0

ds.

86 / 477

Stochastic integral

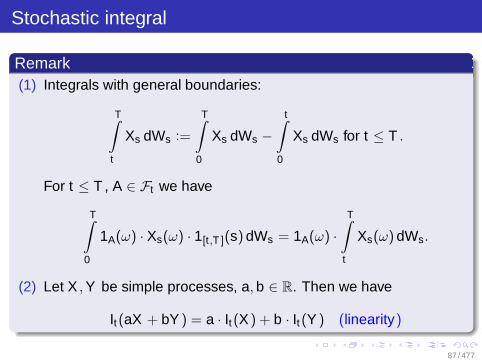

Remark(1) Integrals with general boundaries:

T∫

t

Xs dWs :=

T∫

0

Xs dWs −t∫

0

Xs dWs for t ≤ T .

For t ≤ T , A ∈ Ft we have

T∫

0

1A(ω) · Xs(ω) · 1[t,T ](s) dWs = 1A(ω) ·T∫

t

Xs(ω) dWs.

(2) Let X , Y be simple processes, a, b ∈ R. Then we have

It(aX + bY ) = a · It(X ) + b · It(Y ) (linearity)

87 / 477

Measurability

DefinitionA stochastic process (Xt , Gt)t∈[0,∞) is called measurable if themapping

[0,∞) × Ω → Rn

(s, ω) 7→ Xs(ω)

is B([0,∞)) ⊗F-B(Rn)-measurable.

RemarkMeasurability of the process X implies that X (., ω) isB([0,∞))-B(Rn)-measurable for a fixed ω ∈ Ω. Thus, for all t ∈ [0,∞),

i = 1, . . . , n, the integralt∫

0X 2

i (s) ds is defined.

88 / 477

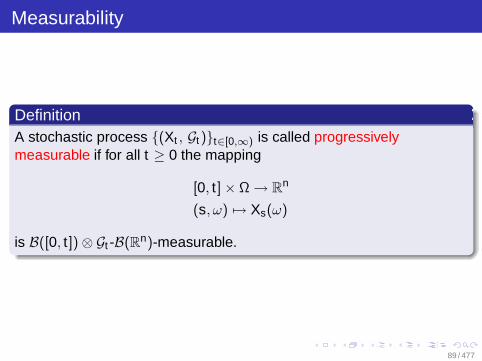

Measurability

DefinitionA stochastic process (Xt , Gt)t∈[0,∞) is called progressivelymeasurable if for all t ≥ 0 the mapping

[0, t] × Ω → Rn

(s, ω) 7→ Xs(ω)

is B([0, t]) ⊗ Gt -B(Rn)-measurable.

89 / 477

Measurability

Remark(1) If the real-valued process (Xt , Gt)t∈[0,∞) is progressively

measurable and bounded, then for all t ∈ [0,∞) the integralt∫

0Xs ds is Gt -measurable.

(2) Every progressively measurable process is measurable.

(3) Each measurable process possesses a progressively measurablemodification.

90 / 477

Measurability

TheoremIf all paths of the stochastic process (Xt , Gt)t∈[0,∞) areright-continuous (or left-continuous), then the process is progressivelymeasurable.

TheoremLet τ be a stopping time with respect to the filtration Gtt∈[0,∞). If thestochastic process (Xt , Gt)t∈[0,∞) is progressively measurable, thenso is the stopped process (Xt∧τ , Gt)t∈[0,∞). In particular, Xt∧τ is Gt

and Gt∧τ -measurable.

91 / 477

Extension of the stochastic integral toL2[0, T ]-processes

Definition

L2[0, T ] := L2([0, T ],Ω,F , Ftt∈[0,T ], P

)

:=

(Xt ,Ft)t∈[0,T ] real-valued stochastic process

∣∣∣∣

Xtt progressively measurable, E( T∫

0

X 2t dt

)<∞

Norm on L2[0, T ]: ‖X‖2T := E

( T∫0

X 2t dt

).

92 / 477

Extension of the stochastic integral toL2[0, T ]-processes

‖ · ‖2T L2-norm on the probability space(

[0, T ]× Ω, B([0, T ]) ⊗F , λ ⊗ P).

‖ · ‖2T semi-norm (‖X − Y‖2

T = 0 6⇒ X = Y ).

X equivalent to Y :⇔ X = Y a.s. λ ⊗ P.

93 / 477

Extension of the stochastic integral toL2[0, T ]-processes

Ito isometryLet X be a simple process. The mapping X 7→ I.(X ) induces by

‖I.(X )‖2LT

:= E( T∫

0

Xs dWs

)2

= E( T∫

0

X 2s ds

)= ‖X‖2

T

a norm on the space of stochastic integrals.

⇒ I.(X ) linear, norm-preserving (= isometry)

⇒ I.(X ) Ito isometry

94 / 477

Extension of the stochastic integral toL2[0, T ]-processes

Use processes X ∈ L2[0, T ] approximated by a sequence X (n) ofsimple processes.

I.(X (n)) is a Cauchy-sequence with respect to ‖ · ‖LT.

To show: I.(X (n)) is convergent, limit independent of X (n).

Denote limit by

I(X ) =

∫Xs dWs.

95 / 477

Extension of the stochastic integral toL2[0, T ]-processes

X ∈ L2[0, T ]J(.) //_______ J(X ) ∈ MC

2

X (n)

‖·‖T

OO

I(.)// I(X (n))

‖·‖LT

OO

simple process stochastic integralfor simple processes

96 / 477

Extension of the stochastic integral toL2[0, T ]-processes

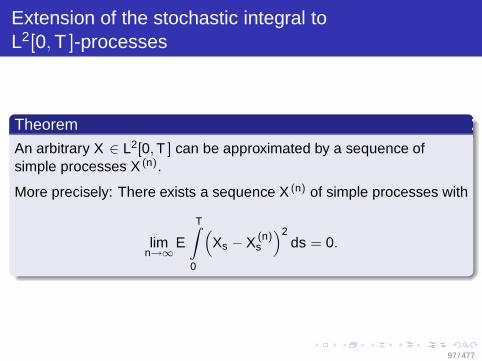

Theorem

An arbitrary X ∈ L2[0, T ] can be approximated by a sequence ofsimple processes X (n).

More precisely: There exists a sequence X (n) of simple processes with

limn→∞

E

T∫

0

(Xs − X (n)

s

)2ds = 0.

97 / 477

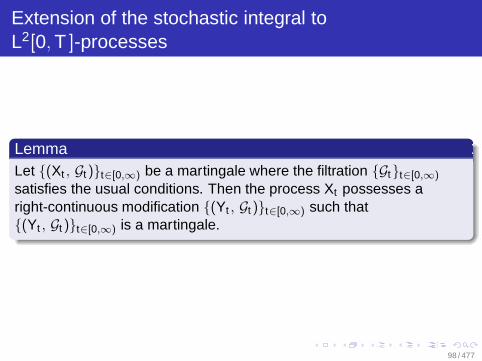

Extension of the stochastic integral toL2[0, T ]-processes

LemmaLet (Xt , Gt)t∈[0,∞) be a martingale where the filtration Gtt∈[0,∞)

satisfies the usual conditions. Then the process Xt possesses aright-continuous modification (Yt , Gt)t∈[0,∞) such that(Yt , Gt)t∈[0,∞) is a martingale.

98 / 477

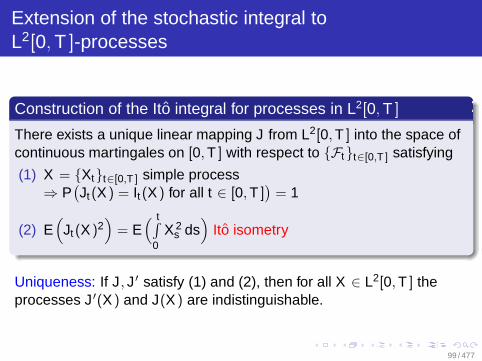

Extension of the stochastic integral toL2[0, T ]-processes

Construction of the Ito integral for processes in L2[0, T ]

There exists a unique linear mapping J from L2[0, T ] into the space ofcontinuous martingales on [0, T ] with respect to Ftt∈[0,T ] satisfying

(1) X = Xtt∈[0,T ] simple process⇒ P

(Jt(X ) = It(X ) for all t ∈ [0, T ]

)= 1

(2) E(

Jt(X )2)

= E( t∫

0X 2

s ds)

Ito isometry

Uniqueness: If J, J ′ satisfy (1) and (2), then for all X ∈ L2[0, T ] theprocesses J ′(X ) and J(X ) are indistinguishable.

99 / 477

Extension of the stochastic integral toL2[0, T ]-processes

Definition

For X ∈ L2[0, T ] and J as before we define by

t∫

0

Xs dWs := Jt(X )

the stochastic integral (or Ito integral) of X with respect to W .

100 / 477

Extension of the stochastic integral toL2[0, T ]-processes

Theorem: Special case of Doob’s inequality

Let X ∈ L2[0, T ]. Then we have

E(

sup0≤t≤T

∣∣∣∣

t∫

0

Xs dWs

∣∣∣∣)2

≤ 4 · E( T∫

0

X 2s ds

).

101 / 477

Extension of the stochastic integral toL2[0, T ]-processes

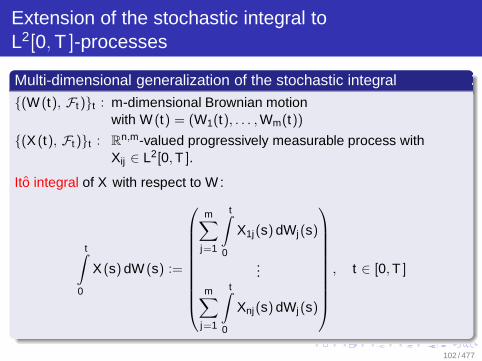

Multi-dimensional generalization of the stochastic integral

(W (t), Ft)t : m-dimensional Brownian motionwith W (t) = (W1(t), . . . , Wm(t))

(X (t), Ft)t : Rn,m-valued progressively measurable process with

Xij ∈ L2[0, T ].

Ito integral of X with respect to W :

t∫

0

X (s) dW (s) :=

m∑

j=1

t∫

0

X1j(s) dWj(s)

...m∑

j=1

t∫

0

Xnj(s) dWj(s)

, t ∈ [0, T ]

102 / 477

Further extension of the stochastic integral

Definition

H2[0, T ] := H2([0, T ], Ω, F , Ftt∈[0,T ], P

)

:=

(Xt ,Ft)t∈[0,T ] real-valued stochastic process

∣∣∣∣

Xtt progressively measurable,

T∫

0

X 2t dt < ∞ P-a.s.

103 / 477

Further extension of the stochastic integral

Processes X ∈ H2[0, T ]

do not necessarily have a finite T -norm→ no approximation by simple processes as for

processes in L2[0, T ]

can be localized with suitable sequences of stopping times

Stopping times (with respect to Ftt ):

τn(ω) := T ∧ inf

0 ≤ t ≤ T

∣∣∣∣

t∫

0

X 2s (ω) ds ≥ n

, n ∈ N

Sequence of stopped processes:

X (n)t (ω) := Xt(ω) · 1τn(ω)≥t

⇒ X (n) ∈ L2[0, T ] ⇒ Stochastic integral already defined.

104 / 477

Further extension of the stochastic integral

Stochastic integral:

It(X ) := It(X (n)) for 0 ≤ t ≤ τn

Consistence property:

It(X ) = It(X (m)) for 0 ≤ t ≤ τn(≤ τm), m ≥ n

⇒ It(X ) well-defined for X ∈ H2[0, T ]

105 / 477

Further extension of the stochastic integral

Stopping times:τn

n→∞−−−→ +∞ P-a.s.

⇒ It(X ) local martingale with localizing sequence τn.

⇒ Stochastic integral is linear and possesses continuous paths.

106 / 477

Outline

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

107 / 477

The Ito formula

General assumptions for this sectionLet (Ω,F , P) be a complete probability space equipped with a filtrationFtt satisfying the usual conditions. Further, assume that on thisspace a Brownian motion (Wt ,Ft)t∈[0,∞) with respect to this filtrationis defined.

108 / 477

The Ito formula

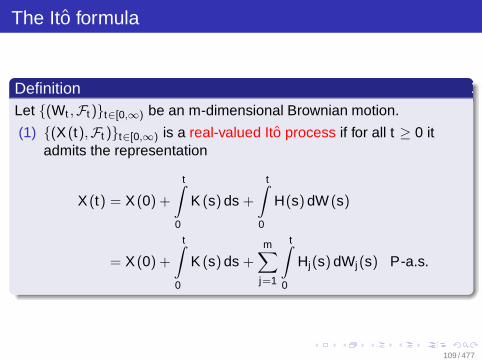

DefinitionLet (Wt ,Ft)t∈[0,∞) be an m-dimensional Brownian motion.

(1) (X (t),Ft )t∈[0,∞) is a real-valued Ito process if for all t ≥ 0 itadmits the representation

X (t) = X (0) +

t∫

0

K (s) ds +

t∫

0

H(s) dW (s)

= X (0) +

t∫

0

K (s) ds +

m∑

j=1

t∫

0

Hj(s) dWj(s) P-a.s.

109 / 477

The Ito formula

X (0) F0-measurable,K (t)t∈[0,∞), H(t)t∈[0,∞) progressively measurable with

t∫

0

|K (s)|ds < ∞,

t∫

0

H2i (s) ds < ∞ P-a.s.

for all t ≥ 0, i = 1, . . . , m.

(2) n-dimensional Ito process X = (X (1), . . . , X (n))= vector with components being real-valued Ito processes.

110 / 477

The Ito formula

Remark

Hj ∈ H2[0, T ] for all T > 0.

The representation of an Ito process is unique up toindistinguishability of the representing integrands Kt , Ht .

Symbolic differential notation:

dXt = Kt dt + Ht dWt

111 / 477

The Ito formula

DefinitionLet X and Y be two real-valued Ito processes with

X (t) = X (0) +

t∫

0

K (s) ds +

t∫

0

H(s) dW (s),

Y (t) = Y (0) +

t∫

0

L(s) ds +

t∫

0

M(s) dW (s).

Quadratic covariation of X and Y :

〈X , Y 〉t :=

m∑

i=1

t∫

0

Hi(s) · Mi(s) ds.

112 / 477

The Ito formula

DefinitionQuadratic variation of X

〈X 〉t := 〈X , X 〉t .

NotationLet X be a real-valued Ito process, and Y a real-valued, progressivelymeasurable process. We set

t∫

0

Y (s) dX (s) :=

t∫

0

Y (s) · K (s) ds +

t∫

0

Y (s) · H(s) dW (s)

if all integrals on the right-hand side are defined.

113 / 477

The Ito formula

Theorem: One-dimensional Ito formulaLet Wt be a one-dimensional Brownian motion, and Xt a real-valued Itoprocess with

Xt = X0 +

t∫

0

Ks ds +

t∫

0

Hs dWs.

Let f ∈ C2(R). Then, for all t ≥ 0 we have

f (Xt) = f (X0) +

t∫

0

f ′(Xs) dXs +12

t∫

0

f ′′(Xs) d〈X 〉s

= f (X0) +

t∫

0

(f ′(Xs) · Ks +

12· f ′′(Xs) · H2

s

)ds +

t∫

0

f ′(Xs)Hs dWs

114 / 477

The Ito formula

RemarkThe Ito formula differs from the fundamental theorem of calculusby the additional term

12

t∫

0

f ′′(Xs) d〈X 〉s.

The quadratic variation 〈X 〉t is an Ito process.

Differential notation:

df (Xt) = f ′(Xt) dXt +12· f ′′(Xt) d〈X 〉t .

115 / 477

The Ito formula

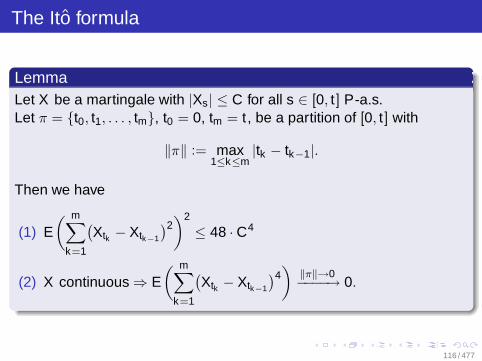

LemmaLet X be a martingale with |Xs| ≤ C for all s ∈ [0, t] P-a.s.Let π = t0, t1, . . . , tm, t0 = 0, tm = t , be a partition of [0, t] with

‖π‖ := max1≤k≤m

|tk − tk−1|.

Then we have

(1) E( m∑

k=1

(Xtk − Xtk−1

)2)2

≤ 48 · C4

(2) X continuous ⇒ E( m∑

k=1

(Xtk − Xtk−1

)4)

‖π‖→0−−−−→ 0.

116 / 477

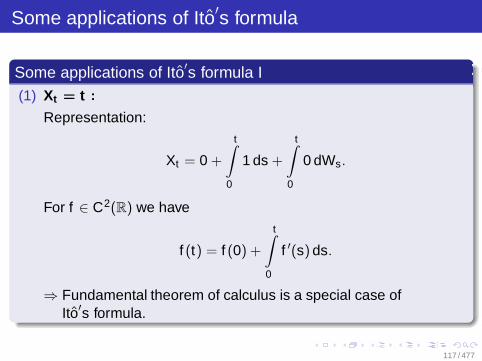

Some applications of Ito′s formula

Some applications of Ito′s formula I(1) Xt = t :

Representation:

Xt = 0 +

t∫

0

1 ds +

t∫

0

0 dWs.

For f ∈ C2(R) we have

f (t) = f (0) +

t∫

0

f ′(s) ds.

⇒ Fundamental theorem of calculus is a special case ofIto′s formula.

117 / 477

Some applications of Ito′s formula II

Some applications of Ito′s formula

(2) Xt = h(t) :

For h ∈ C1(R) Ito′s formula implies the chain rule

Xt = h(0) +

t∫

0

h′(s) ds +

t∫

0

0 dWs

⇒ (f h)(t) = (f h)(0) +

t∫

0

f ′(h(s)) · h′(s) ds.

118 / 477

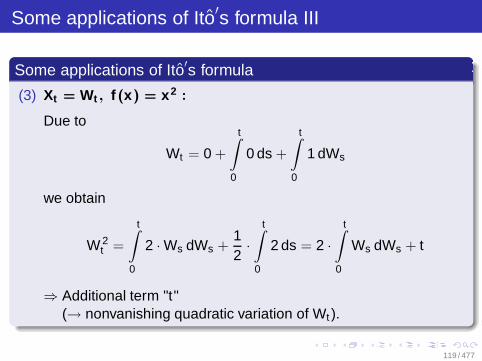

Some applications of Ito′s formula III

Some applications of Ito′s formula

(3) Xt = Wt , f (x) = x2 :

Due to

Wt = 0 +

t∫

0

0 ds +

t∫

0

1 dWs

we obtain

W 2t =

t∫

0

2 · Ws dWs +12·

t∫

0

2 ds = 2 ·t∫

0

Ws dWs + t

⇒ Additional term "t"(→ nonvanishing quadratic variation of Wt ).

119 / 477

The Ito formula

Theorem: Multi-dimensional Ito formula

X (t) =(X1(t), . . . , Xn(t)

)n-dimensional Ito process with

Xi(t) = Xi(0) +

t∫

0

Ki(s) ds +m∑

j=1

t∫

0

Hij(s) dWj(s), i = 1, . . . , n

where W (t) =(W1(t), . . . , Wm(t)

)is an m-dimensional Brownian motion.

Let f : [0,∞) × Rn → R be a C1,2-function. Then, we have

f (t , X1(t), . . . , Xn(t)) = f (0, X1(0), . . . , Xn(0))

+

t∫

0

ft(s, X1(s), . . . , Xn(s)) ds +

n∑

i=1

t∫

0

fxi (s, X1(s), . . . , Xn(s)) dXi(s)

+12·

n∑

i ,j=1

t∫

0

fxi xj (s, X1(s), . . . , Xn(s)) d〈Xi , Xj〉s.

120 / 477

Product rule or partial integration

Corollary: Product rule or partial integration

Let Xt , Yt be one-dimensional Ito processes with

Xt = X0 +

t∫

0

Ks ds +

t∫

0

Hs dWs,

Yt = Y0 +

t∫

0

µs ds +

t∫

0

σs dWs.

Then we have

Xt · Yt = X0 · Y0 +

t∫

0

Xs dYs +

t∫

0

Ys dXs +

t∫

0

d〈X , Y 〉s

= X0 · Y0 +

t∫

0

(Xsµs + YsKs + Hsσs

)ds +

t∫

0

(Xsσs + YsHs

)dWs.

121 / 477

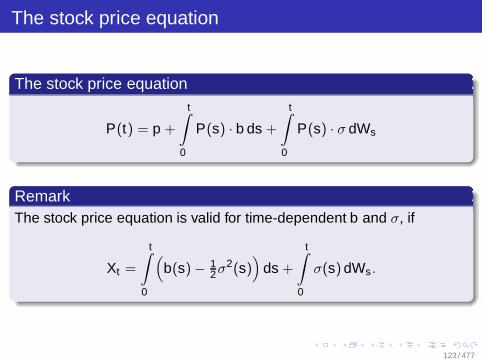

The stock price equation

Simple continuous-time market model (1 bond, one stock).Stock price influenced by a one-dimensional Brownian motion

Price of the stock at time t :

P(t) = p · exp((

b − 12σ2)

t + σWt

)

Choose

Xt = 0 +

t∫

0

(b − 1

2σ2)

ds +

t∫

0

σ dWs, f (x) = p · ex

Ito formula implies

f (Xt) = p +

t∫

0

[f (Xs)(b − 1

2σ2) + 12 f (Xs) · σ2]ds +

t∫

0

f (Xs) · σ dWs

122 / 477

The stock price equation

The stock price equation

P(t) = p +

t∫

0

P(s) · b ds +

t∫

0

P(s) · σ dWs

RemarkThe stock price equation is valid for time-dependent b and σ, if

Xt =

t∫

0

(b(s) − 1

2σ2(s))

ds +

t∫

0

σ(s) dWs.

123 / 477

The stock price equation

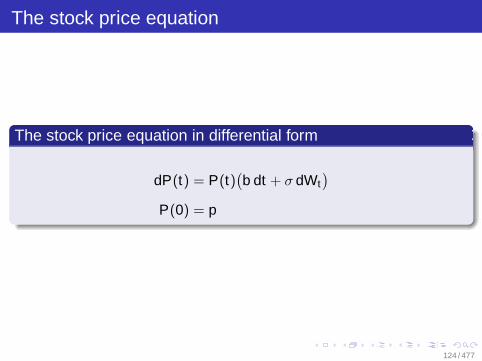

The stock price equation in differential form

dP(t) = P(t)(b dt + σ dWt

)

P(0) = p

124 / 477

The stock price equation

Theorem: Variation of constantsLet (W (t), Ft)t∈[0,∞) be an m-dimensional Brownian motion.Let x ∈ R and A, a, Sj , σj be progressively measurable, real-valuedprocesses with

t∫

0

(|A(s)| + |a(s)|

)ds < ∞ for all t ≥ 0 P-a.s.

t∫

0

(S2

j (s) + σ2j (s)

)ds < ∞ for all t ≥ 0 P-a.s. .

125 / 477

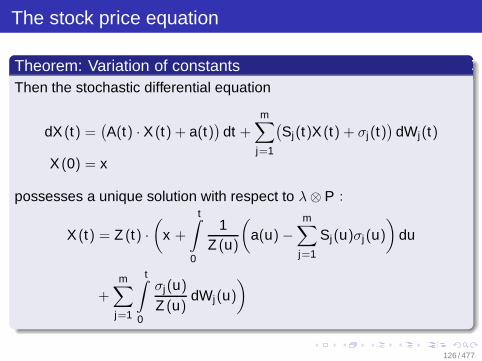

The stock price equation

Theorem: Variation of constantsThen the stochastic differential equation

dX (t) =(A(t) · X (t) + a(t)

)dt +

m∑

j=1

(Sj(t)X (t) + σj(t)

)dWj(t)

X (0) = x

possesses a unique solution with respect to λ ⊗ P :

X (t) = Z (t) ·(

x +

t∫

0

1Z (u)

(a(u) −

m∑

j=1

Sj(u)σj(u)

)du

+m∑

j=1

t∫

0

σj(u)

Z (u)dWj(u)

)

126 / 477

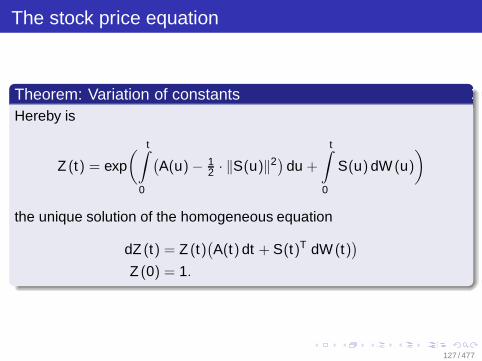

The stock price equation

Theorem: Variation of constantsHereby is

Z (t) = exp( t∫

0

(A(u) − 1

2 · ‖S(u)‖2) du +

t∫

0

S(u) dW (u)

)

the unique solution of the homogeneous equation

dZ (t) = Z (t)(A(t) dt + S(t)T dW (t)

)

Z (0) = 1.

127 / 477

The stock price equation

RemarkThe process (X (t), Ft)t∈[0,∞) solves the stochastic differentialequation in the sense that X (t) satisfies

X (t) = x +

t∫

0

(A(s) · X (s) + a(s)

)ds

+

m∑

j=1

t∫

0

(Sj(s) X (s) + σj(s)

)dWj(s)

for all t ≥ 0 P-almost surely.

128 / 477

Outline

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

129 / 477

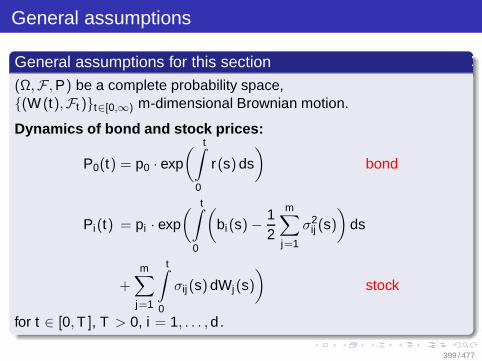

General assumptions

General assumptions for this section(Ω,F , P) be a complete probability space,(W (t),Ft )t∈[0,∞) m-dimensional Brownian motion.

Dynamics of bond and stock prices:

P0(t) = p0 · exp( t∫

0

r(s) ds)

bond

Pi(t) = pi · exp( t∫

0

(bi(s) − 1

2

m∑

j=1

σ2ij (s)

)ds

+m∑

j=1

t∫

0

σij(s) dWj(s)

)stock

for t ∈ [0, T ], T > 0, i = 1, . . . , d .

130 / 477

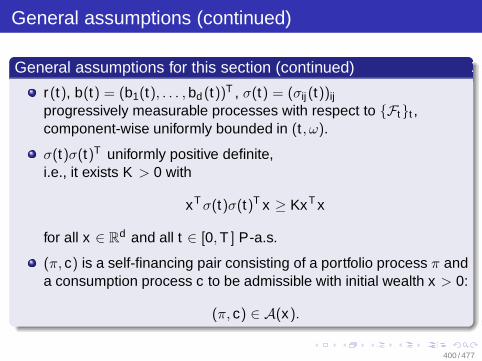

General assumptions (continued)

General assumptions for this section (continued)

r(t), b(t) = (b1(t), . . . , bd (t))T , σ(t) = (σij(t))ij

progressively measurable processes with respect to Ftt ,component-wise uniformly bounded in (t , ω).

σ(t)σ(t)T uniformly positive definite,i.e., it exists K > 0 with

xT σ(t)σ(t)T x ≥ KxT x

for all x ∈ Rd and all t ∈ [0, T ] P-a.s.

Deterministic rate of return r(t) is not requiredr(t) can be a stochastic process⇒ bond is no longer riskless.

131 / 477

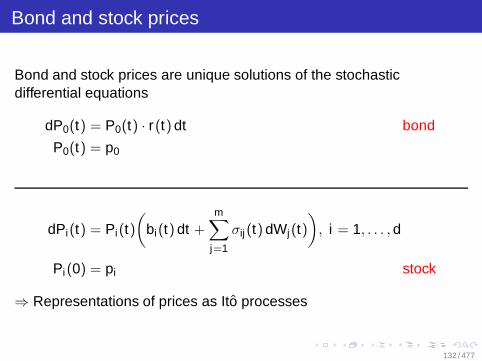

Bond and stock prices

Bond and stock prices are unique solutions of the stochasticdifferential equations

dP0(t) = P0(t) · r(t) dt bond

P0(t) = p0

dPi(t) = Pi(t)(

bi(t) dt +

m∑

j=1

σij(t) dWj(t))

, i = 1, . . . , d

Pi(0) = pi stock

⇒ Representations of prices as Ito processes

132 / 477

Possible actions of investors

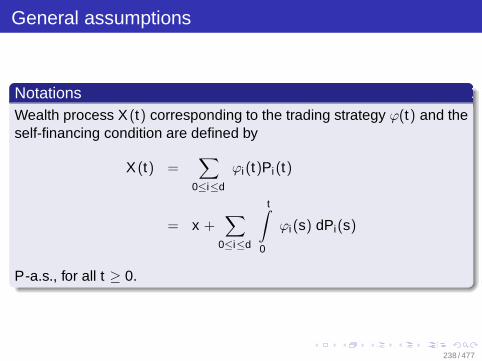

(1) Investor can rebalance his holdings→ sell some securities→ invest in securities⇒ Portfolio process / trading strategy.

(2) Investor is allowed to consume parts of his wealth⇒ Consumption process.

133 / 477

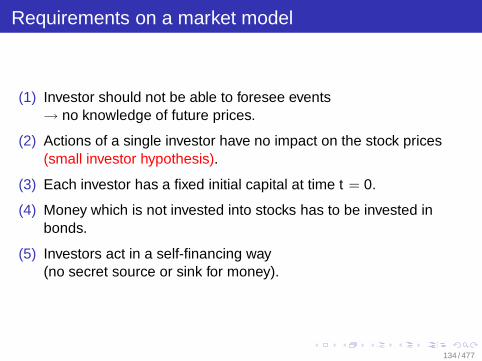

Requirements on a market model

(1) Investor should not be able to foresee events→ no knowledge of future prices.

(2) Actions of a single investor have no impact on the stock prices(small investor hypothesis).

(3) Each investor has a fixed initial capital at time t = 0.

(4) Money which is not invested into stocks has to be invested inbonds.

(5) Investors act in a self-financing way(no secret source or sink for money).

134 / 477

Requirements on a market model

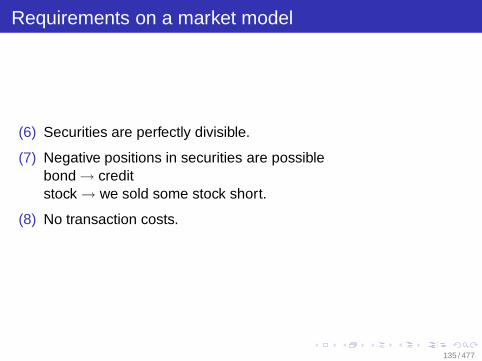

(6) Securities are perfectly divisible.

(7) Negative positions in securities are possiblebond → creditstock → we sold some stock short.

(8) No transaction costs.

135 / 477

Negative bond positions and credit interest rates

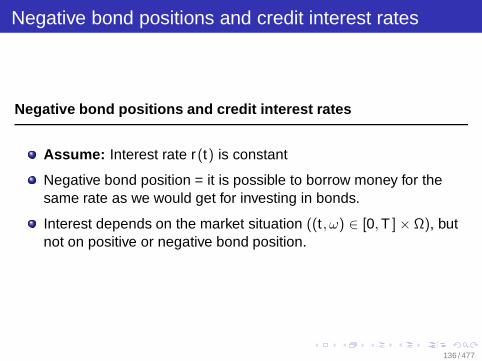

Negative bond positions and credit interest rates

Assume: Interest rate r(t) is constant

Negative bond position = it is possible to borrow money for thesame rate as we would get for investing in bonds.

Interest depends on the market situation ((t , ω) ∈ [0, T ] × Ω), butnot on positive or negative bond position.

136 / 477

Mathematical realizations of some requirements

Market with 1 bond and d stocks

Time t = 0: – Initial capital of investor: x > 0

– Buy a selection of securities

ϕ(0) =(ϕ0(0), ϕ1(0), . . . , ϕd(0)

)T

Time t > 0: – Trading strategy: ϕ(t)

(1) ⇒ trading strategy is progressively measurablewith respect to Ftt

Decisions on buying and selling are made on basis of informationavailable at time t (→ modelled by Ftt )

(5) ⇒ only self-financing trading strategies should be used.

137 / 477

Discrete-time example: self-financing strategy

Market with 1 riskless bond and 1 stock

Two-period model for time points t = 0, 1, 2.

Number of shares of bond and stock at time t :

(ϕ0(t), ϕ1(t))T ∈ R2

Consumption of investor at time t : C(t)

Wealth at time t : X (t)

Bond/stock prices at time t : P0(t), P1(t)

Initial conditions: C(0) = 0, X (0) = x

138 / 477

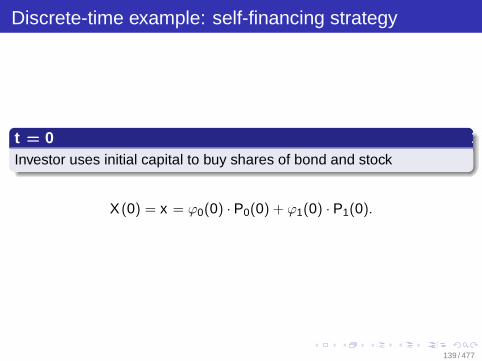

Discrete-time example: self-financing strategy

t = 0Investor uses initial capital to buy shares of bond and stock

X (0) = x = ϕ0(0) · P0(0) + ϕ1(0) · P1(0).

139 / 477

Discrete-time example: self-financing strategy

t = 1Security prices have changed, investor consumes parts of his wealth

Current wealth:

X (1) = ϕ0(0) · P0(1) + ϕ1(0) · P1(1) − C(1).

Total:

X (1) = x + ϕ0(0) ·(P0(1) − P0(0)

)+ ϕ1(0) ·

(P1(1) − P1(0)

)− C(1)

Wealth = initial wealth + gains/losses - consumption

Invest remaining capital at the market:

X (1) = ϕ0(1) · P0(1) + ϕ1(1) · P1(1).

140 / 477

Discrete-time example: self-financing strategy

t = 2Invest remaining capital at the market

Wealth:X (2) = ϕ0(2) · P0(2) + ϕ1(2) · P1(2).

Wealth = total wealth of shares held

Total:

X (2) = x +2∑

i=1

[ϕ0(i − 1) · (P0(i) − P0(i − 1))

+ϕ1(i − 1) · (P1(i) − P1(i − 1))]

−2∑

i=1

C(i).

141 / 477

Discrete-time example: self-financing strategy

Self-financing trading strategy:

wealth before rebalancing - consumption = wealth after rebalancing

Condition:

ϕ0(i) · P0(i) + ϕ1(i) · P1(i)

= ϕ0(i − 1) · P0(i) + ϕ1(i − 1) · P1(i) − C(i)

⇒ Useless in continuous-time setting

(securities can be traded at each time instant /"before" and "after" cannot be distinguished)

142 / 477

Discrete-time example: self-financing strategy

Continuous-time setting

Wealth process corresponding to strategy ϕ(t):

X (t) = x +

t∫

0

ϕ0(s) dP0(s) +

t∫

0

ϕ1(s) dP1(s) −t∫

0

c(s) ds

⇒ Price processes are Ito processes.

143 / 477

Trading strategy and wealth processes

Definition(1) A trading strategy ϕ with

ϕ(t) :=(ϕ0(t), ϕ1(t), . . . , ϕd (t)

)T

is an Rd+1-valued progressively measurable process with respect

to Ftt∈[0,T ] satisfying

T∫

0

|ϕ0(t)|dt < ∞ P-a.s.

d∑

j=1

T∫

0

(ϕi(t) · Pi(t)

)2 dt < ∞ P-a.s. for i = 1, . . . , d .

144 / 477

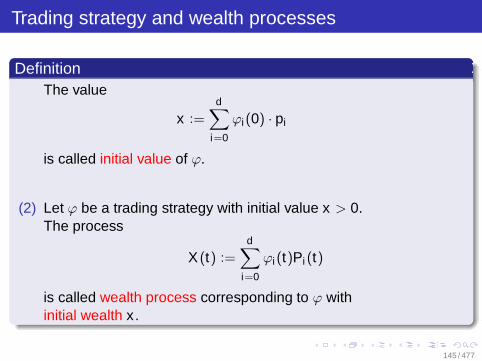

Trading strategy and wealth processes

DefinitionThe value

x :=

d∑

i=0

ϕi(0) · pi

is called initial value of ϕ.

(2) Let ϕ be a trading strategy with initial value x > 0.The process

X (t) :=d∑

i=0

ϕi(t)Pi (t)

is called wealth process corresponding to ϕ withinitial wealth x .

145 / 477

Trading strategy and wealth processes

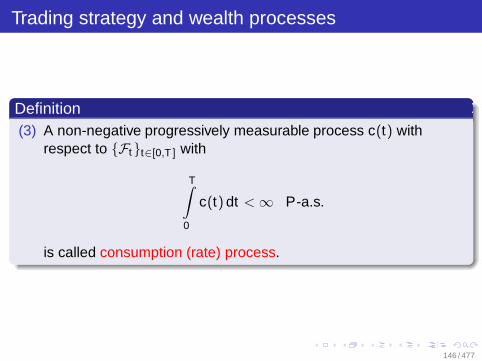

Definition(3) A non-negative progressively measurable process c(t) with

respect to Ftt∈[0,T ] with

T∫

0

c(t) dt < ∞ P-a.s.

is called consumption (rate) process.

146 / 477

Trading strategy and wealth processes

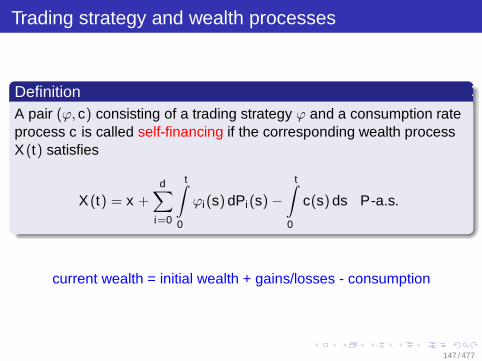

DefinitionA pair (ϕ, c) consisting of a trading strategy ϕ and a consumption rateprocess c is called self-financing if the corresponding wealth processX (t) satisfies

X (t) = x +

d∑

i=0

t∫

0

ϕi(s) dPi(s) −t∫

0

c(s) ds P-a.s.

current wealth = initial wealth + gains/losses - consumption

147 / 477

Trading strategy and wealth processes

RemarkWe have

t∫

0

ϕ0(s) dP0(s) =

t∫

0

ϕ0(s) P0(s) r(s) ds

t∫

0

ϕi(s) dPi(s) =

t∫

0

ϕi(s) Pi(s) bi(s) ds

+

m∑

j=1

t∫

0

ϕi(s) Pi (s)σij(s) dWj(s), i = 1, . . . , d .

148 / 477

Self-financing portfolio process

DefinitionLet (ϕ, c) be a self-financing pair consisting of a trading strategy and aconsumption process with corresponding wealth process X (t) > 0P-a.s. for all t ∈ [0, T ]. Then the R

d -valued process

π(t) =(π1(t), . . . , πd (t)

)T with πi(t) =ϕi(t) · Pi(t)

X (t)

is called a self-financing portfolio process corresponding to thepair (ϕ, c).

149 / 477

Portfolio processes

Remark(1) The portfolio process denotes the fractions of total wealth invested

in the different stocks.

(2) The fraction of wealth invested in the bond is given by

(1 − π(t)T 1

)=

ϕ0(t) · P0(t)X (t)

, where 1 := (1, . . . , 1)T ∈ Rd .

(3) Given knowledge of wealth X (t) and prices Pi(t), it is possible foran investor to describe his activities via a self-financing pair (π, c).→ Portfolio process and trading strategy are

equivalent descriptions of the same action.

150 / 477

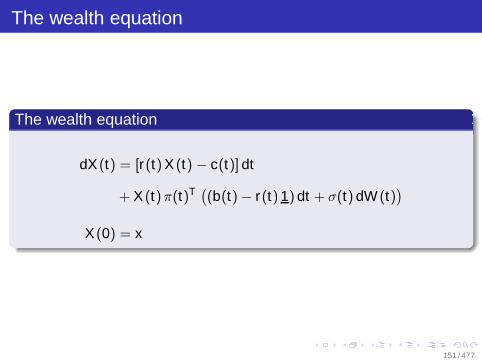

The wealth equation

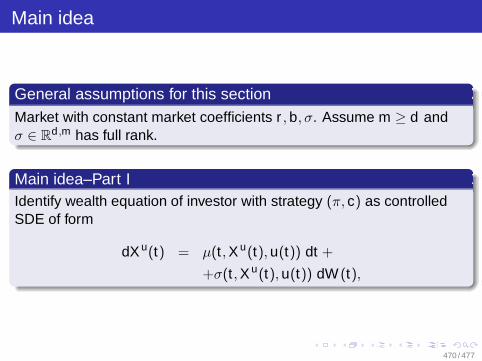

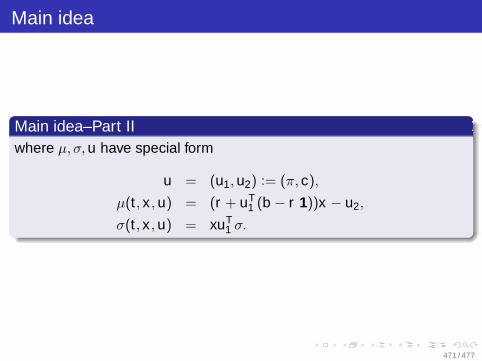

The wealth equation

dX (t) = [r(t) X (t) − c(t)] dt

+ X (t)π(t)T ((b(t) − r(t) 1) dt + σ(t) dW (t))

X (0) = x

151 / 477

Alternative definition of a portfolio process

Definition

The progressively measurable Rd -valued process π(t) is called a

self-financing portfolio process corresponding to the consumptionprocess c(t) if the corresponding wealth equation possesses a uniquesolution X (t) = Xπ,c(t) with

T∫

0

(X (t) · πi(t)

)2 dt < ∞ P-a.s. for i = 1, . . . , d .

152 / 477

Admissibility

DefinitionA self-financing pair (ϕ, c) or (π, c) consisting of a trading strategy ϕ ora portfolio process π and a consumption process c will be calledadmissible for the initial wealth x > 0, if the corresponding wealthprocess satisfies

X (t) ≥ 0 P-a.s. for all t ∈ [0, T ].

The set of admissible pairs will be denoted by A(x).

153 / 477

An example

Portfolio process:π(t) ≡ π ∈ R

d constant

Consumption rate:c(t) = γ · X (t), γ > 0

Wealth process corresponding to (π, c) :

X (t)

Investor rebalances his holdings in such a way that the fractions ofwealth invested in the different stocks and in the bond remainconstant over time.

Consumption rate is proportional to the current wealth of theinvestor.

154 / 477

An example

Wealth equation:

dX (t) = [r(t) − γ] X (t) dt

+ X (t)πT ((b(t) − r(t) 1) dt + σ(t) dW (t))

X (0) = 0

Wealth process:

X (t) = x · exp( t∫

0

[r(s) − γ + πT (b(s) − r(s) · 1

)− 1

2‖πT σ(s)‖2

]ds

+

t∫

0

πT σ(s) dW (s)

)

155 / 477

Outline

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

156 / 477

Properties of the continuous-time market model

Assumptions:

Dimension of the underlying Brownian motion= number of stocks

Past and present prices are the only sources of information for theinvestors⇒ Choose Brownian filtration Ftt∈[0,T ]

Aim: Final wealths X (T ) when starting with initial capital of x .

157 / 477

General assumption / notation

General assumption for this section

d = m

Notation

γ(t) := exp(−

t∫

0

r(s) ds)

θ(t) := σ−1(t)(b(t) − r(t) 1

)

Z (t) := exp(−

t∫

0

θ(s)T dW (s) − 12

t∫

0

‖θ(s)‖2 ds)

H(t) := γ(t) · Z (t)

158 / 477

Properties of the continuous-time market model

b, r uniformly boundedσσT uniformly positive definite⇒ ‖θ(t)‖2 uniformly bounded

Interpretation of θ(t): Relative risk premium for stock investment.

Process H(t) is important for option pricing .

H(t) is positive, continuous, and progressively measurable withrespect to Ftt∈[0,T ].

H(t) is the unique solution of the SDE

dH(t) = −H(t)(r(t) dt + θ(t)T dW (t)

)

H(0) = 1.

159 / 477

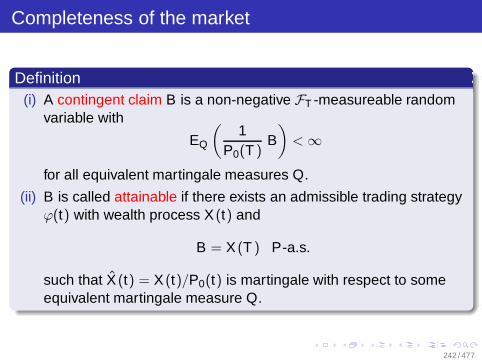

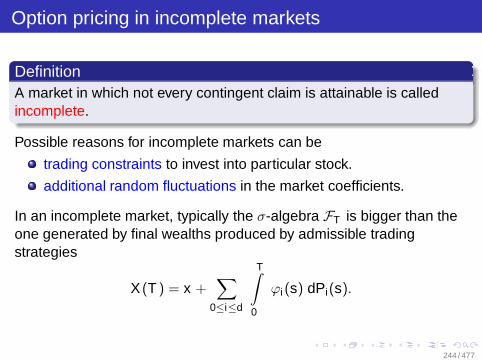

Completeness of the market

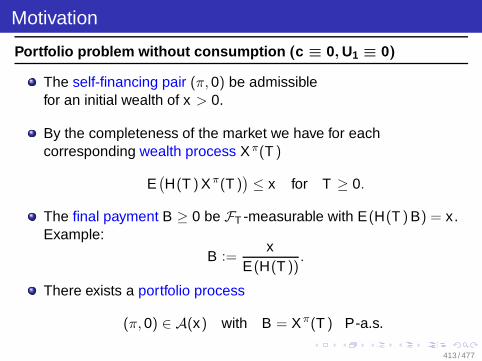

Theorem: Completeness of the market(1) Let the self-financing pair (π, c) consisting of a portfolio process π

and a consumption process c be admissible for an initial wealth ofx ≥ 0, i.e.,

(π, c) ∈ A(x).

Then the corresponding wealth process X (t) satisfies

E(

H(t) X (t) +

t∫

0

H(s)c(s) ds)

≤ x for all t ∈ [0, T ].

160 / 477

Completeness of the market

Theorem: Completeness of the market(2) Let B ≥ 0 be an FT -measurable random variable and c(t) a

consumption process satisfying

x := E(

H(T ) B +

T∫

0

H(s)c(s) ds)

< ∞.

Then there exists a portfolio process π(t) with (π, c) ∈ A(x) andthe corresponding wealth process X (t) satisfies

X (T ) = B P-a.s.

161 / 477

Completeness of the market

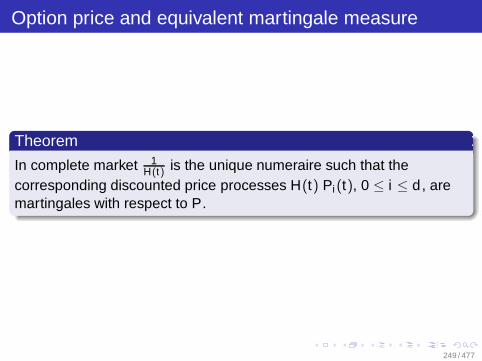

H(t) can be regarded as the appropriate discounting process thatdetermines the initial wealth at time t = 0

E( T∫

0

H(s) · c(s) ds)

+ E(H(T ) · B)

which is necessary to attain future aims.

(1) puts bounds on the desires of an investor given his initialcapital x ≥ 0.

(2) proves that future aims which are feasible in the sense of part(1) can be realized.

(2) says that each desired final wealth in t = T can be attainedexactly via trading according to an appropriate self-financing pair(π, c) if one possesses sufficient initial capital(completeness/complete model) .

162 / 477

Completeness of the market

Remark1/H(t) is the wealth process corresponding to the pair

(π(t), c(t)

)=(σ−1(t)T θ(t), 0

)

with initial wealth x := 1/H(0) = 1

and final wealth B:= 1/H(T ).

163 / 477

Outline

2 The Continuous-Time Market ModelModeling the Security PricesExcursion 1: Brownian Motion and MartingalesContinuation: Modeling the Security pricesExcursion 2: The Ito IntegralExcursion 3: The Ito FormulaTrading Strategy and Wealth ProcessProperties of the Continuous-Time Market ModelExcursion 4: The Martingale Representation Theorem

164 / 477

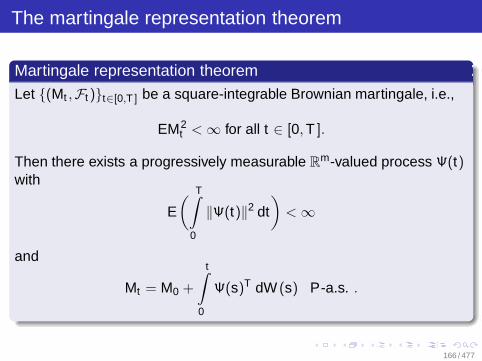

Excursion 4: The martingale representation theorem

General assumptions(Ω,F , P) complete probability space.(Wt ,Ft)t∈[0,∞) m-dimensional Brownian motion.Ftt Brownian filtration.

DefinitionA real-valued martingale (Mt ,Ft)t∈[0,T ] with respect to the Brownianfiltration Ftt is called a Brownian martingale.

165 / 477

The martingale representation theorem

Martingale representation theorem

Let (Mt ,Ft)t∈[0,T ] be a square-integrable Brownian martingale, i.e.,

EM2t < ∞ for all t ∈ [0, T ].

Then there exists a progressively measurable Rm-valued process Ψ(t)

with

E( T∫

0

‖Ψ(t)‖2 dt)

< ∞

and

Mt = M0 +

t∫

0

Ψ(s)T dW (s) P-a.s. .

166 / 477

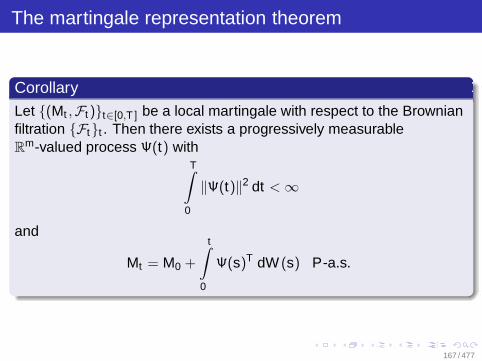

The martingale representation theorem

CorollaryLet (Mt ,Ft)t∈[0,T ] be a local martingale with respect to the Brownianfiltration Ftt . Then there exists a progressively measurableR

m-valued process Ψ(t) withT∫

0

‖Ψ(t)‖2 dt < ∞

and

Mt = M0 +

t∫

0

Ψ(s)T dW (s) P-a.s.

167 / 477

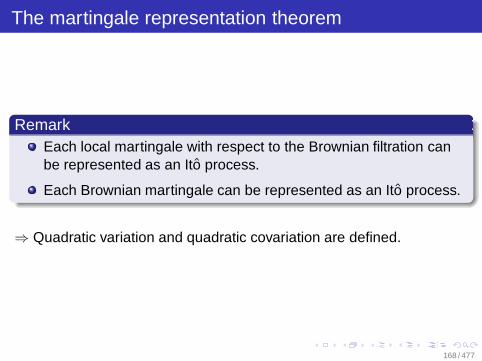

The martingale representation theorem

RemarkEach local martingale with respect to the Brownian filtration canbe represented as an Ito process.

Each Brownian martingale can be represented as an Ito process.

⇒ Quadratic variation and quadratic covariation are defined.

168 / 477

Outline

3 Option Pricing

169 / 477

Outline

3 Option PricingIntroductionExamplesThe Replication PrincipleArbitrage OpportunityContinuationPartial Differential Approach (PDA)Arbitrage & Option Pricing

170 / 477

Introduction

Option derivative security (i.e., from underlying assets)

call buy fixed amount of asset at fixed time in future forfixed strike price

put sell fixed amount of asset for strike price

American Option Sell/buy asset during timespan of contract

European Option Act at maturity ( =⇒ expiry )

171 / 477

Outline

3 Option PricingIntroductionExamplesThe Replication PrincipleArbitrage OpportunityContinuationPartial Differential Approach (PDA)Arbitrage & Option Pricing

172 / 477

European call

European callRight to buy security at time t = T for strike price K > 0fixed at time t = 0

P(T ) > K Gain (P(T ) − K )+

P(T ) ≤ K No gain (Holder will buy in market)

173 / 477

European put

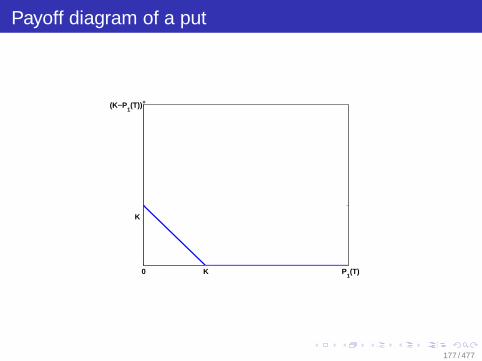

European putRight to sell security at time t = T for price K > 0 fixed at time t = 0

P(T ) ≥ K No gain (Holder will sell in market)

P(T ) < K Gain (K − P(T ))+

174 / 477

The payoff diagram

The payoff diagramGraph of final gain (through the option) as function of the stock price attime T

175 / 477

Payoff diagram of a call

P1(T)

(P1(T)−K)+

K

K0

176 / 477

Payoff diagram of a put

P1(T)

(K−P1(T))+

K

K0

177 / 477

The sense of options

Hedge against price fluctuations of underlying asset

Bound risks of future cash flows

Risks of option speculationHigh losses not unusual

178 / 477

Outline

3 Option PricingIntroductionExamplesThe Replication PrincipleArbitrage OpportunityContinuationPartial Differential Approach (PDA)Arbitrage & Option Pricing

179 / 477

Option pricing

Option PricingBond Interest Rate (BIR) r constant

Fixed deterministic payment of B at time T has present value of

e−rT · B

Sum to be invested at t = 0 to obtain amount of B at maturity.

180 / 477

Option pricing

Option Pricing

BIR r(t) time dependent and random variableExpected value

E(

e−

T∫

0r(s) ds

· B)

181 / 477

Examples of option pricing

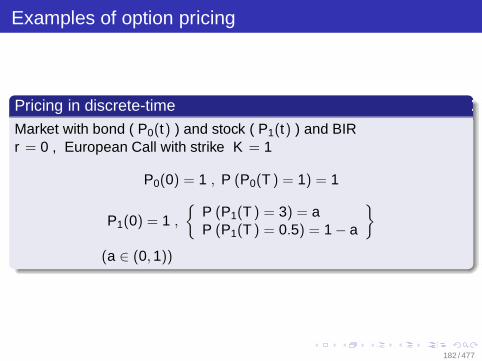

Pricing in discrete-time

Market with bond ( P0(t) ) and stock ( P1(t) ) and BIRr = 0 , European Call with strike K = 1

P0(0) = 1 , P (P0(T ) = 1) = 1

P1(0) = 1 ,

P (P1(T ) = 3) = aP (P1(T ) = 0.5) = 1 − a

(a ∈ (0, 1))

182 / 477

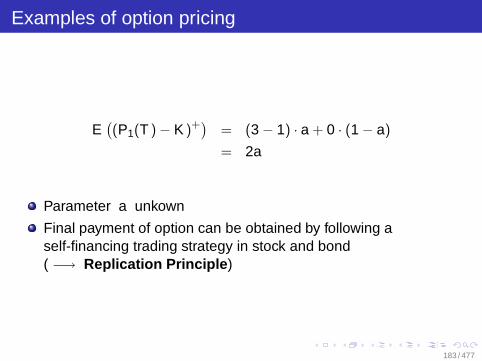

Examples of option pricing

E((P1(T ) − K )+

)= (3 − 1) · a + 0 · (1 − a)

= 2a

Parameter a unkown

Final payment of option can be obtained by following aself-financing trading strategy in stock and bond( −→ Replication Principle )

183 / 477

Examples of option pricing

Determine (ϕ0(0), ϕ1(0)) such that

X (T ) = ϕ0(0) · P0(T ) + ϕ1(0) · P1(T )

= (P1(T ) − K )+

184 / 477

Examples of option pricing

Option Price

p = ϕ0(0) · P0(0) + ϕ1(0) · P1(0)

equals capital in t = 0 to buy replication strategy (ϕ0(0), ϕ1(0))

For all other choices riskless gains are possible without initialcapital −→ arbitrage opportunities

185 / 477

Examples of option pricing

Proof– Part 1(i) Be option price p < p. Then buy option for p and sell

(ϕ0(0), ϕ1(0)) for p(Hold position (−ϕ0(0),−ϕ1(0)) )

=⇒ Initial gain of p − p without own capital

186 / 477

Examples of option pricing

Proof– Part 2(ii) Be option price p > p. Then sell call and hold position

(ϕ0(0), ϕ1(0)) for p

=⇒ Initial gain of p − p without own capital

187 / 477

Examples of option pricing

Our example yields the system of equations

ϕ0(0) · 1 + ϕ1(0) · 3 = 2

ϕ0(0) · 1 + ϕ1(0) · 0.5 = 0

with unique solution

(ϕ0(0), ϕ1(0)) = (−0.4, 0.8)

=⇒ Option price p = −0.4 · 1 + 0.8 · 1 = 0.4

188 / 477

Examples of option pricing

Option price independent of unknown probability a

No arbitrage opportunities in market

Calculated call price p equals expected discounted terminalpayment of call ⇐⇒ a = 0.2−→ P1(t) is martingale

189 / 477

General assumptions

Assumptions for this sectionSelf-financing pair (π, c) ∈ A(x) admissible for initial capital x ≥ 0

190 / 477

Outline

3 Option PricingIntroductionExamplesThe Replication PrincipleArbitrage OpportunityContinuationPartial Differential Approach (PDA)Arbitrage & Option Pricing

191 / 477

Arbitrage opportunity

DefinitionBe

(ϕ, c) a self-financing and admissible pair

ϕ a trading strategy

c a consumption process

(ϕ, c) is called arbitrage opportunity ⇐⇒ corresponding wealthprocess satisfies

192 / 477

Arbitrage opportunity

Definition continued

X (0) = 0 , X (T ) ≥ 0 P-a.s.

P (X (T ) > 0) > 0 or P

T∫

0

c(t) dt > 0

> 0

193 / 477

Arbitrage opportunity

CorollaryIn the complete continuous-time market model there is no arbitrageopportunity.

194 / 477

Contingent claim

DefinitionA contingent claim (g, B) consists of an Ftt -progressivelymeasurable payout rate process g(t), t ∈ [0, T ], g(t) ≥ 0, and aFT -measurable terminal payment B ≥ 0 at T with

E

T∫

0

g(t) dt + B

µ < ∞

for some µ > 1.

195 / 477

Replication strategy

Definition(π, c) is called replication strategy for the contingent claim (g, B) if

g(t) = c(t) P-a.s. ∀ t ∈ [0, T ]

X (T ) = B P-a.s.

where X (t) is wealth process corresponding to (π, c).

196 / 477

Set of replication strategies of price x

Definition

D(x) := D (x ; (g, B))

:= (π, c) ∈ A(x)| (π, c) replication

strategy for (g, B)

197 / 477

Fair price

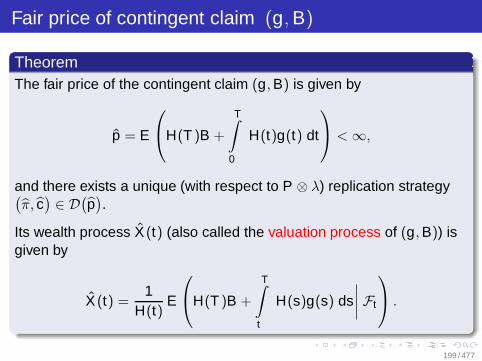

DefinitionThe fair price of the contingent claim (g, B) is defined as

p := inf p | D(p) 6= ∅ .

198 / 477

Fair price of contingent claim (g, B)

TheoremThe fair price of the contingent claim (g, B) is given by

p = E

H(T )B +

T∫

0

H(t)g(t) dt

< ∞,

and there exists a unique (with respect to P ⊗ λ) replication strategy(π, c

)∈ D

(p).

Its wealth process X (t) (also called the valuation process of (g, B)) isgiven by

X (t) =1

H(t)E

H(T )B +

T∫

t

H(s)g(s) ds

∣∣∣∣ Ft

.

199 / 477

The valuation process

RemarkThe above theorem gives us the fair price of the contingent claim(g, B) at time t as this price p(t) has to coincide with X (t). Otherwise,there would be arbitrage opportunities in the market consisting ofstock, bond, and contingent claim.

200 / 477

Black-Scholes formula

TheoremConsider a market model with just one stock and a bond with constantmarket coefficients, i.e.,

d = m = 1

andr(t) ≡ r , b(t) ≡ b , σ(t) ≡ σ > 0

for all t ∈ [0, T ], T > 0, r , b, σ ∈ R.

201 / 477

Black-Scholes formula

(i) The price XC(t) of a European call with strike price K > 0 andmaturity T is given by

XC(t) = P1(t)Φ(d1(t)) − Ke−r(T−t)Φ(d2(t))

d1(t) =ln(

P1(t)K

)+ (r + 0.5σ2)(T − t)

σ√

T − t

d2(t) =ln(

P1(t)K

)+ (r − 0.5σ2)(T − t)

σ√

T − t

= d1(t) − σ√

T − t

where Φ is the distribution function of the standard normaldistribution.

202 / 477

Black-Scholes formula

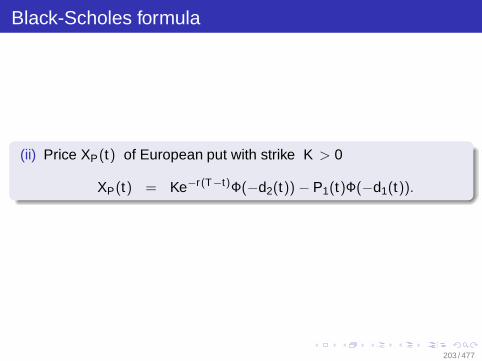

(ii) Price XP(t) of European put with strike K > 0

XP(t) = Ke−r(T−t)Φ(−d2(t)) − P1(t)Φ(−d1(t)).

203 / 477

The change of measure

W Q(t) := W (t) + θt =⇒

p = XC(0) = EQ

(e−rT (P1(T ) − K )+

)

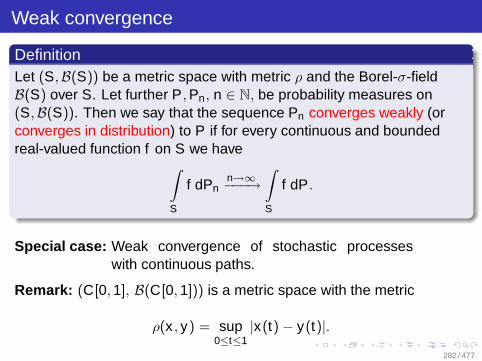

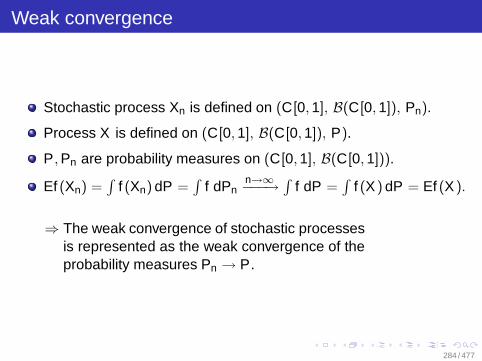

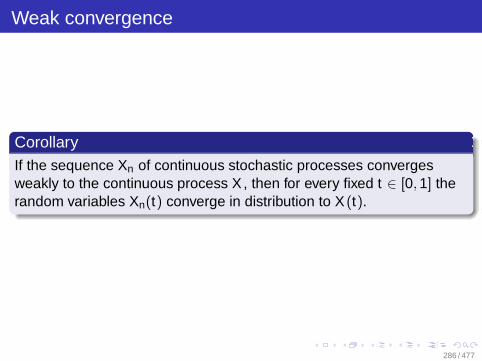

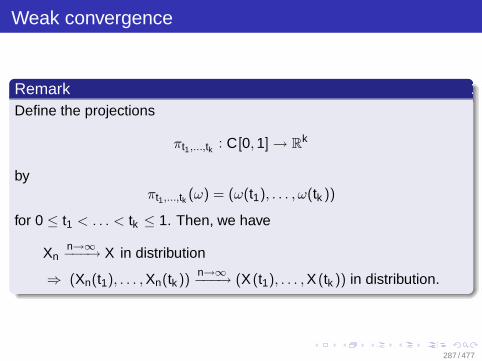

where EQ(·) denotes expected value with respect to measure Q givenby Radon-Nikodym derivative

dQdP

= e−0.5θ2T−θW (T ).

204 / 477

General assumptions of this section

General Assumptions of this SectionBe (X (t),Ft )t≥0 an m-dimensional progressively measurableprocess, Ft the Brownian filtration with

t∫

0

X 2i (s) ds < ∞ P-a.s. for all t ≥ 0, i = 1, . . . , m.

Let further

Z (t , X ) := exp(−

m∑

i=1

t∫

0

Xi(s) dWi(s) − 12

t∫

0

‖X (s)‖2 ds)

.

205 / 477

Consequences

The argument in Z (t , X ) is an Ito process and we have

Z (t , X ) = 1 −m∑

i=1

t∫

0

Z (s, X )Xi(s) dWi(s).

Z (t , X ) is a continuous local martingale with Z (0, X ) = 1.

206 / 477

Girsanov’s theorem

Girsanov’s theoremBe process Z (t , X ) a martingale and define process(

W Q(t),Ft)

t≥0 by

W Qi (t) := Wi(t) +

t∫

0

Xi(s) ds (1 ≤ i ≤ m, t ≥ 0)

Then, for each fixed T ∈ [0,∞) the process(

W Q(t),Ft)

t∈[0,T ]is

an m-dimensional Brownian motion on (Ω,FT , QT ) with probabilitymeasure

QT (A) := E (1A · Z (T , X )) ∀ A ∈ FT

207 / 477

The Novikov condition

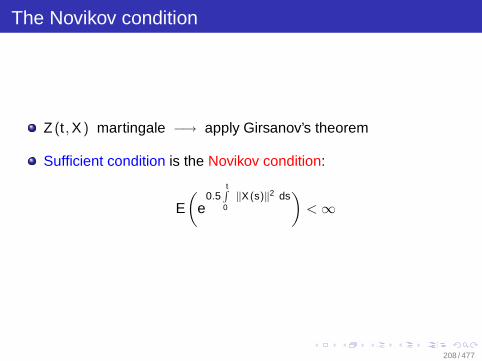

Z (t , X ) martingale −→ apply Girsanov’s theorem

Sufficient condition is the Novikov condition:

E(

e0.5

t∫

0‖X(s)‖2 ds

)< ∞

208 / 477

The Novikov condition

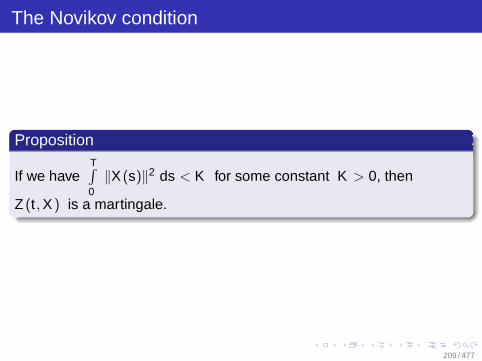

Proposition

If we haveT∫0

‖X (s)‖2 ds < K for some constant K > 0, then

Z (t , X ) is a martingale.

209 / 477

Outline

3 Option PricingIntroductionExamplesThe Replication PrincipleArbitrage OpportunityContinuationPartial Differential Approach (PDA)Arbitrage & Option Pricing

210 / 477

Girsanov’s theorem & Option Pricing

LemmaBe Q a probability measure which is equivalent to P restricted onFT . Then the density process Dtt∈[0,T ] defined by

Dt :=dQdP

∣∣∣∣Ft

, t ∈ [0, T ]

satisfies: (Dt ,Ft)t∈[0,T ] is a positive Brownian martingale withrespect to P satisfying

Dt = 1 +

∫ t

0Ψ(s)T dW (s)

for a progressively measurable d -dimensional process Ψ with

T∫

0

‖Ψ(s)‖2 ds < ∞ P-a.s.

211 / 477

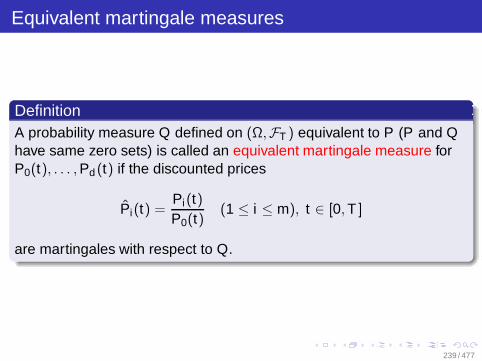

Uniqueness of the equivalent martingale measure

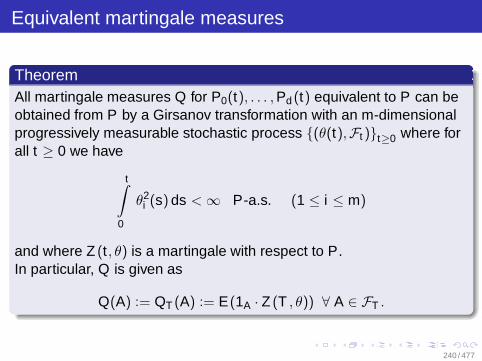

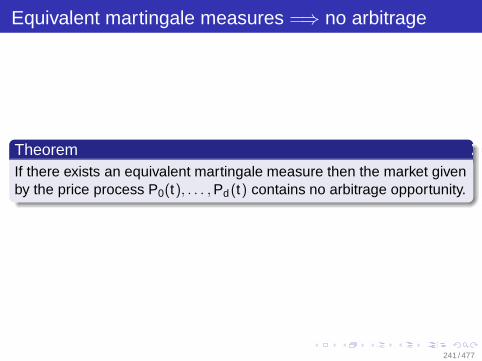

TheoremIn the complete market model QT is the unique equivalent martingalemeasure on Ftt∈[0,T ] for the price processes Pi(t), 0 ≤ i ≤ d .

RemarkThe existence of an equivalent martingale measure implies theabsence of arbitrage opportunities in the market.

The absence of arbitrage implies the existence of an equivalentmartingale measure.

212 / 477

Option pricing & equivalent martingale measure

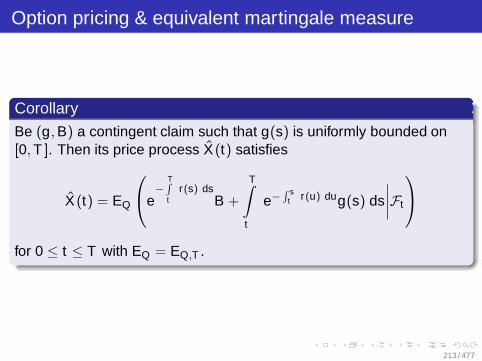

CorollaryBe (g, B) a contingent claim such that g(s) is uniformly bounded on[0, T ]. Then its price process X (t) satisfies

X (t) = EQ

e

−T∫t

r(s) dsB +

T∫

t

e−∫ s

t r(u) dug(s) ds

∣∣∣∣Ft

for 0 ≤ t ≤ T with EQ = EQ,T .

213 / 477

Independence of the option price

In the case of g ≡ 0 we have

p = EQ

e

−T∫

0r(s) ds

B

Thus, p equals the natural price with respect to a new (uniquelydetermined) probability measure Q.

214 / 477

European digital call

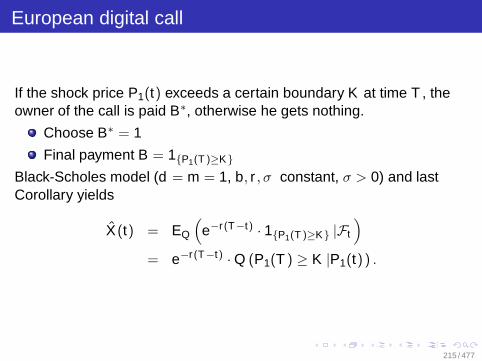

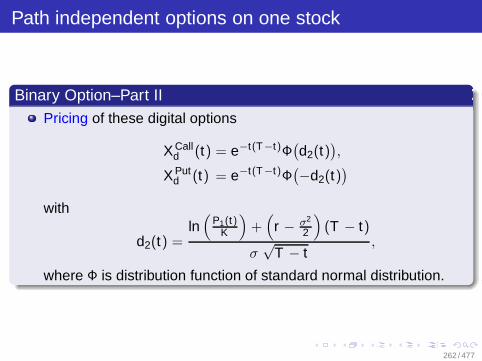

If the shock price P1(t) exceeds a certain boundary K at time T , theowner of the call is paid B∗, otherwise he gets nothing.

Choose B∗ = 1

Final payment B = 1P1(T )≥KBlack-Scholes model (d = m = 1, b, r , σ constant, σ > 0) and lastCorollary yields

X(t) = EQ

(e−r(T−t) · 1P1(T )≥K |Ft

)

= e−r(T−t) · Q (P1(T ) ≥ K |P1(t) ) .

215 / 477

European digital call

For fixed t we have P1(T ) ≥ K ⇐⇒

W Q(T ) − W Q(t) ≥ln(

KP1(t)

)−(

r − σ2

2

)(T − t)

σ︸ ︷︷ ︸:=K

As W Q(T ) − W Q(t) is normally distributed with expectation 0 andvariance T − t , we obtain

216 / 477

European digital call

X (t) = e−r(T−t)∫ ∞

K

1√2π(T − t)

e− x2

2(T−t) dx

= e−r(T−t) Φ

ln(

P1(t)K

)+(

r − σ2

2

)(T − t)

σ√

T − t

217 / 477

Outline

3 Option PricingIntroductionExamplesThe Replication PrincipleArbitrage OpportunityContinuationPartial Differential Approach (PDA)Arbitrage & Option Pricing

218 / 477

Option pricing by PDA

General Assumptions nowConsider a Black-Scholes model, i.e.,

d = m = 1

andb, r , σ constant with σ > 0.

219 / 477

Option pricing by PDA

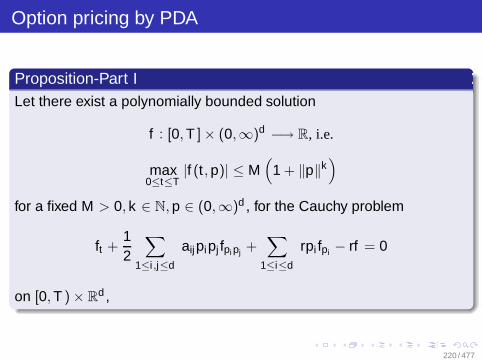

Proposition-Part ILet there exist a polynomially bounded solution

f : [0, T ]× (0,∞)d −→ R, i.e.

max0≤t≤T

|f (t , p)| ≤ M(

1 + ‖p‖k)

for a fixed M > 0, k ∈ N, p ∈ (0,∞)d , for the Cauchy problem

ft +12

∑

1≤i ,j≤d

aijpipj fpi pj +∑

1≤i≤d

rpi fpi − rf = 0

on [0, T ) × Rd ,

220 / 477

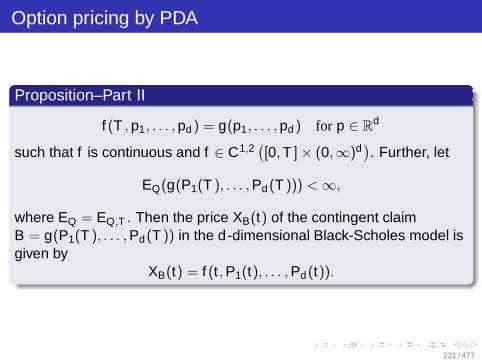

Option pricing by PDA

Proposition–Part II

f (T , p1, . . . , pd ) = g(p1, . . . , pd ) for p ∈ Rd

such that f is continuous and f ∈ C1,2([0, T ] × (0,∞)d

). Further, let

EQ(g(P1(T ), . . . , Pd (T ))) < ∞,

where EQ = EQ,T . Then the price XB(t) of the contingent claimB = g(P1(T ), . . . , Pd(T )) in the d -dimensional Black-Scholes model isgiven by

XB(t) = f (t , P1(t), . . . , Pd (t)).

221 / 477

Option pricing by PDA

Proposition–Part IIIFurther for 1 ≤ i ≤ d ,

Ψi(t) = fpi (t , P1(t), . . . , Pd (t))

Ψ0(t) =

f (t , P1(t), . . . , Pd (t)) − ∑1≤i≤d

Ψi(t)Pi(t)

P0(t)

is a replication strategy for B.

222 / 477

SDE

Definition–Part IIf on (Ω,F , P) there exists a d -dimensional continuous process(X (t),Ft )t≥0 with X (0) = x , x ∈ R

d fixed,

Xi(t) = xi +

t∫

0

bi(s, X (s)) ds +∑

0≤j≤m

t∫

0

σij(s, X (s)) dWj(s)

P-a.s. for all t ≥ 0, 1 ≤ i ≤ d , satisfying

t∫

0

|bi(s, X (s))| +

∑

1≤j≤m

σ2ij (s, X (s))

ds < ∞

P-a.s. for all t ≥ 0, 1 ≤ i ≤ d ,

223 / 477

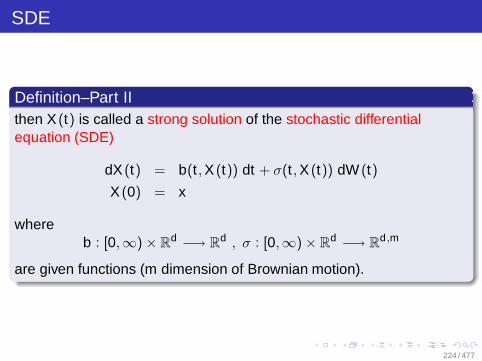

SDE

Definition–Part IIthen X (t) is called a strong solution of the stochastic differentialequation (SDE)

dX (t) = b(t , X (t)) dt + σ(t , X (t)) dW (t)

X (0) = x

whereb : [0,∞) × R

d −→ Rd , σ : [0,∞) × R

d −→ Rd ,m

are given functions (m dimension of Brownian motion).

224 / 477

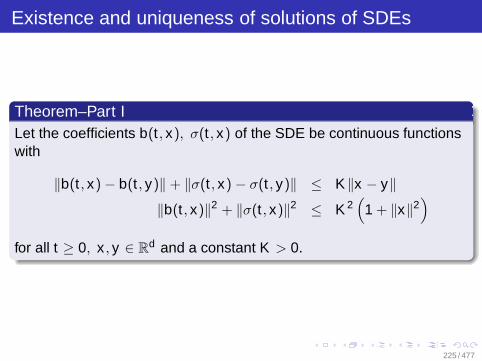

Existence and uniqueness of solutions of SDEs

Theorem–Part ILet the coefficients b(t , x), σ(t , x) of the SDE be continuous functionswith

‖b(t , x) − b(t , y)‖ + ‖σ(t , x) − σ(t , y)‖ ≤ K‖x − y‖‖b(t , x)‖2 + ‖σ(t , x)‖2 ≤ K 2

(1 + ‖x‖2

)

for all t ≥ 0, x , y ∈ Rd and a constant K > 0.

225 / 477

Existence and uniqueness of solutions of SDEs

Theorem–Part IIThen there exists a continuous, strong solution (X (t),Ft )t≥0 of theSDE with

E(‖X (t)‖2

)≤ C

(1 + ‖x‖2

)eCT ∀ t ∈ [0, T ]

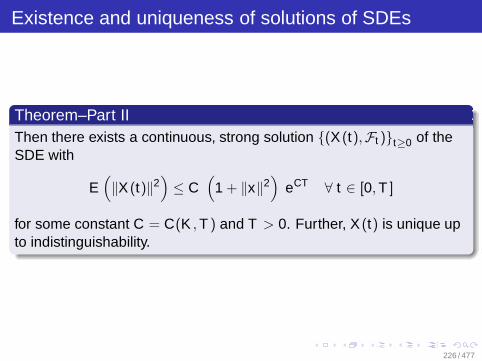

for some constant C = C(K , T ) and T > 0. Further, X (t) is unique upto indistinguishability.

226 / 477

Existence and uniqueness of solutions of SDEs

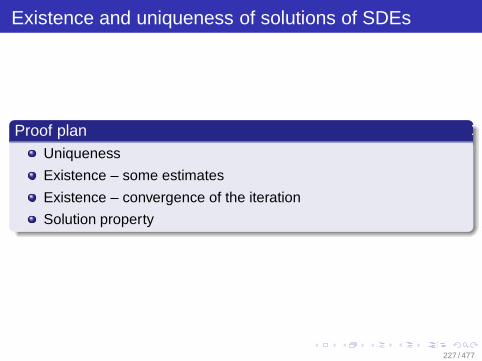

Proof planUniqueness

Existence – some estimates

Existence – convergence of the iteration

Solution property

227 / 477

Existence and uniqueness of solutions of SDEs

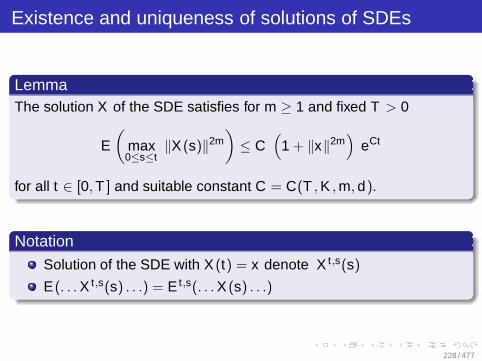

LemmaThe solution X of the SDE satisfies for m ≥ 1 and fixed T > 0

E(

max0≤s≤t

‖X (s)‖2m)

≤ C(

1 + ‖x‖2m)

eCt

for all t ∈ [0, T ] and suitable constant C = C(T , K , m, d).

Notation

Solution of the SDE with X (t) = x denote X t,s(s)

E(. . . X t,s(s) . . .) = E t,s(. . . X (s) . . .)

228 / 477

SDEs

DefinitionBe X (t) unique solution of the SDE under the introduced conditions.For f : R

d −→ Rd , f ∈ C2

(R

d), the operator At defined by

(At f )(x) :=12

∑

1≤i≤d

∑

1≤k≤d

aik (t , x)∂2f

∂xi∂xk(x)

+∑

1≤i≤d

bi(t , x)∂f∂xi

(x)

withaik (t , x) :=

∑

1≤j≤m

σij(t , x)σkj (t , x)

is called the characteristic operator corresponding to X (t).

229 / 477

The Cauchy problem

Description of the Cauchy problem IBe T > 0 fixed. Consider the following Cauchy problem correspondingto operator At :Find a function v(t , x) : [0, T ]× R

d −→ R with

−vt + kv = Atv + g on [0, T ] × Rd

v(T , x) = f (x) for x ∈ Rd

where

f : Rd −→ R , g : [0, T ] × R

d −→ R , k : [0, T ] × Rd −→ (0,∞).

230 / 477

The Cauchy problem

Description of the Cauchy problem IITo ensure the uniqueness of a solution we require that v obeys apolynomial growth condition:

max0≤t≤T

|v(t , x)| ≤ M(

1 + ‖x‖2µ)

with M > 0 , µ ≥ 1.

231 / 477

The Cauchy problem

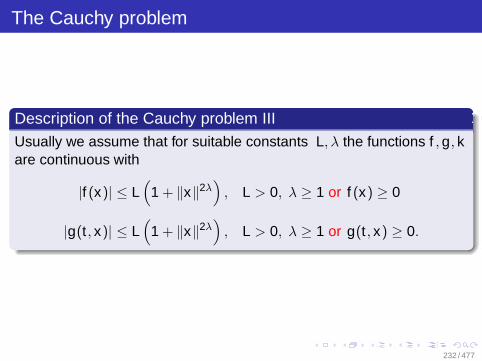

Description of the Cauchy problem IIIUsually we assume that for suitable constants L, λ the functions f , g, kare continuous with

|f (x)| ≤ L(

1 + ‖x‖2λ)

, L > 0, λ ≥ 1 or f (x) ≥ 0

|g(t , x)| ≤ L(

1 + ‖x‖2λ)

, L > 0, λ ≥ 1 or g(t , x) ≥ 0.

232 / 477

The Feynman-Kac representation

Theorem–Part ILet the inequalities for f and g be satisfied. Let furtherv(t , x) : [0, T ] × R

d −→ R be continuous solution of the Cauchyproblem with v ∈ C1,2([0, T ) × R

d). Denote by At the characteristicoperator corresponding to the unique solution X (t) of the SDE withcontinuous coefficients b, σ with

bi(t , x), σ(t , x) : [0,∞) × Rd −→ R

for 1 ≤ i ≤ d , 1 ≤ j ≤ m.

233 / 477

The Feynman-Kac representation

Theorem–Part IIIf v(t , x) satisfies the polynomial growth condition we have therepresentation

v(t , x) = E t,x

f (X (T )) e

−T∫t

k(θ,X(θ)) dθ

+

+

T∫

t

g(s, X (s)) e−

s∫t

k(θ,X(θ)) dθ

ds

.

In particular, v(t , x) is unique solution.

234 / 477

Outline