Embed Size (px)

Citation preview

Mastering Payroll

American Institute of Professional Bookkeepers

© 2014 American Institute of Professional Bookkeepers Mastering Payroll

Overview of Payroll TaxesAmounts paid to workers may be subject to the following withholdings and taxes: Federal income tax withheld (FITW) State income tax withheld (SITW) and local income

tax withheld Employment taxes (e.g., Social Security, Medicare) Unemployment insurance taxes State disability insurance (SDI)

Depending on how a worker is classified, employers may be responsible for withholding and depositing these taxes—and for paying employer payroll taxes Mastering Payroll

Overview of Payroll TaxesSome payroll taxes are employee paid, such as:FITW and SITW, which are withheld from wagesEmployee FICA tax, which consists of:

Social Security (OASDI) tax—6.2% of the employee’s first $117,000 of wages paid in 2014

Medicare (HI) tax, 1.45% of all the worker’s wages —plus an additional 0.9% of wages over $200,000

Other taxes are employer paid, such as:Employer FICA—OASDI of 6.2%, HI of 1.45%Federal unemployment insurance (FUTA), state unemployment insurance (SUI) and SDI

Mastering Payroll

Types of Workers

These workers are not employees

Employees of the temp agency—not the client firm

Passed the “common-law” test so they are treated as employees Subject to FICA and FIT, but no FIT is withheld

Employees of leasing agency—not the client firm

These workers are not employees

Common-law employees

Statutory employees

Statutory nonemployees

Independent contractors

“Temps” from an agency

Leased employees

Mastering Payroll

Common-Law EmployeesA worker is a common-law employee if the employer controls: who performs the work what work will be done how the work will be done when the work will be done where the work will be done

When unsure about a worker’s classification, file IRS Form SS-8 with the IRS. The IRS will classify the worker based on how the employer answers the questions on the SS-8

Mastering Payroll

Common-Law EmployeesCommon-law employees are workers for whom you must:withhold FIT (and SIT) and employee FICA on wages and other paymentsprovide an annual W-2 showing taxable wages paid and taxes withheldpay employer FICA and other employment taxes (e.g., FUTA, SUI, sometimes SDI)periodically remit to the IRS and other agencies both withheld employee taxes and employer taxes

Mastering Payroll

Statutory EmployeesStatutory employees are: drivers who are the employer’s agent or are paid

commissions full-time life insurance sales agents working primarily

for one insurance carrier certain home workers full-time traveling or in-city salespersons

Statutory employee wages: subject to FICA and FUTA (but not FITW)—and possibly to SITW, SUI and SDI, but this varies by state

Mastering Payroll

Statutory NonemployeesStatutory nonemployees are: direct sellers (e.g., those who deliver and distribute

newspapers or shopping news or sell consumer products in the home)

licensed real estate agents companion sittersStatutory nonemployee taxes: Exempt from FUTA,

FITW and FICA Statutory nonemployees pay all their own FIT and

FICA taxes, and are not subject to FUTAWho is responsible for paying SUI varies by state

Mastering Payroll

Independent Contractors (ICs) Independent contractors (ICs) are workers who: control the methods and means of their work perform services that are not integral to the

trade or business of the company using them do not have FIT, SIT or FICA withheld, nor do

FUTA or SUI apply—but if an IC fails to provide a taxpayer identification number (TIN) or SSN, backup FIT and possibly SIT must be withheld

have payments to them reported on Form 1099-MISC (not on a W-2) and are responsible for all of their FIT and FICA taxes

Mastering Payroll

Temporary Help Agency ReferralsTemps are workers who: are employed by a temp agency and work at

the client company on a temporary basis do not have FIT or FICA withheld by the client

company (because they are the agency’s employees)

are the temp agency’s employees—if the agency fails to pay employment taxes, the client firm may be responsible for these taxes

Mastering Payroll

Leased EmployeesLeased employees: are employed by a leasing agency and work at

the client company, which can hire or terminate them as it sees fit

do not have FIT or FICA withheld by the client company (because they are the agency’s employees)

are considered the leasing agency’s employees —if the agency fails to pay employment taxes, the client may be responsible for them

Mastering Payroll

Federal Wage-Hour LawEmployers covered by the Fair Labor Standards Act of 1938 (FLSA) must pay a minimum hourly wage and any overtime pay to employees covered by FLSA. The FLSA defines those hours of work for which employees must be paid. The “Enterprise Test” determines which businesses

are covered by, or exempt from FLSA. Virtually all employers are covered. Exception: “Mom and Pop” shops are not subject to

the enterprise test. If they hire only the owners’ children, these employers are exempt from FLSA.

Mastering Payroll

Which Firms Are Covered by FLSA?

Employers covered by FLSA include: Businesses started on or after March 31, 1990 that have

gross annual sales of at least $500,000 Dry cleaners and construction companies that started

before April 1, 1990 Retailers started before April 1, 1990 that have annual

gross sales of at least $362,500 Nonretail businesses started before April 1, 1990, that

have gross annual sales of at least $250,000 Schools, hospitals and nursing homes Business engaged in interstate commerce

Mastering Payroll

The Federal Minimum WageThe federal minimum wage changes periodically As of July 24, 2009, the minimum wage is $7.25/hour Tipped employees have a lower federal minimum

wage —but their total earnings must average at least the minimum wage

The formula: $2.13/hour tipped employee minimum wage + tips = federal minimum wage, or the employer must make up the difference

Under federal law an employee may not be docked an amount that reduces the employee’s wages for the workweek below the federal minimum wage

Mastering Payroll

Tipped Employee WagesExample: Darla, a waitress, earns $2.13 an hour plus tips. In March 2014, Darla works 35 hours one week and earns $280:

$74.55 wages ($2.13 × 35) + $205.45 in tips

Darla’s hourly pay: $280/35 = $8.00

$8 is more than the federal minimum wage of $8 is more than the federal minimum wage of $7.25, so no additional pay is required. Darla’s $7.25, so no additional pay is required. Darla’s employer can pay her $74.55 ($2.13 employer can pay her $74.55 ($2.13 ×× 35 hours) 35 hours) for the week.for the week.

Mastering Payroll

Tipped Employee Wages: ExampleExample: One week in May 2014, Darla works 40 hours and earns $240: $85.20 wages ($2.13 × 40) + $154.80 tips = $240

The required federal minimum wage is $7.25: 40 hours x $7.25 = $290 minimum pay for the week

Darla’s employer must make up the $50 difference:

$290 minimum pay for the week – $240 received= $50 still owed to Darla by her employer

Mastering Payroll

Federal Minimum Wage Exemptions

In addition to tipped employees, others exempt from the minimum wage include: Outside salespersons Employees under age 20 paid at least $4.25/hr.

(applies only to the first 90 days of employment) —provided that they do not displace or reduce the work hours of employees paid regular wages

Employees exempt by special certificate Children employed by their parents in a mom

and pop shop

Mastering Payroll

State LawsWage-hour rules covered by state law include: Frequency of wage payments When a terminating employee must be paid Method of payment (cash, check, debit card,

EFT, etc.) Rules for unclaimed wages: escheat law requires

employers to remit unclaimed wages to the state after a specified time period

When federal v. state laws conflict, generally the one most favorable to the employee applies

Mastering Payroll

Federal v. State LawExample: Jose works in a state with no minimum wage. For the first week in February 2014, he works 40 hours. What is the minimum he must be paid for the week?

$290 ($7.25 × 40 hours)

Federal minimum wageFederal minimum wage

Mastering Payroll

Federal v. State LawExample: Dan works in a state which has a minimum wage of $8.00 an hour. For one week in January 2014, Dan works 40 hours. What is the minimum he must be paid for the week?

$320 ($8.00 × 40 hours)

The greater of $7.25 or $8 an hourThe greater of $7.25 or $8 an hour

Mastering Payroll

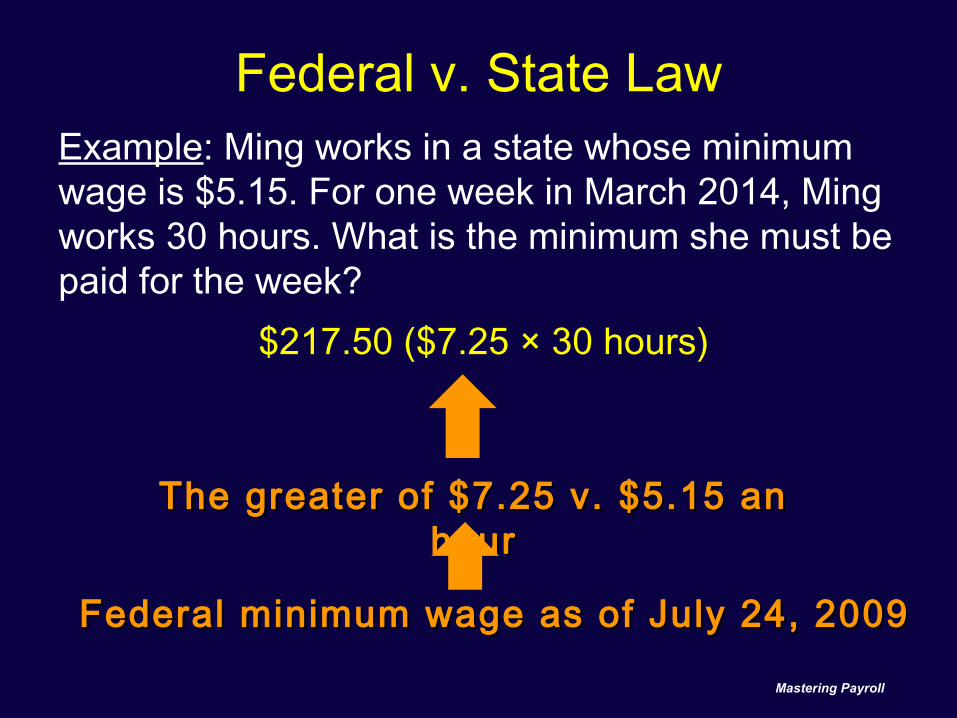

Federal v. State LawExample: Ming works in a state whose minimum wage is $5.15. For one week in March 2014, Ming works 30 hours. What is the minimum she must be paid for the week?

$217.50 ($7.25 × 30 hours)

The greater of $7.25 v. $5.15 an The greater of $7.25 v. $5.15 an hourhour

Federal minimum wage as of July 24, 2009Federal minimum wage as of July 24, 2009

Mastering Payroll

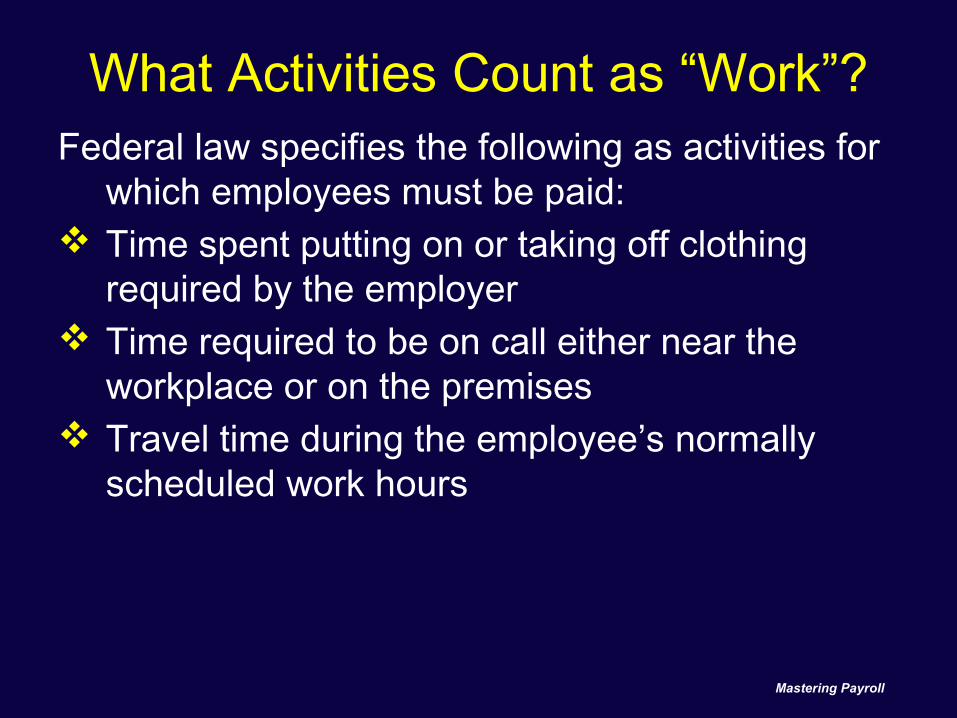

What Activities Count as “Work”?Federal law specifies the following as activities for

which employees must be paid: Time spent putting on or taking off clothing

required by the employer Time required to be on call either near the

workplace or on the premises Travel time during the employee’s normally

scheduled work hours

Mastering Payroll

Travel TimeEmployees must be paid for hours of travel: from one worksite to another during normal working hours to a worksite that is a significant distance from the

employee’s normal worksite

Employees need not be paid for time commuting to and from work—unless:

the employee is on 24-hour call and takes a company vehicle home to be able to respond to emergency calls

after finishing a normal shift, is called back to work at a job site other than the employee’s normal job site

Mastering Payroll

Travel TimeEmployees must be paid travel time for overnight trips—but only for those hours of travel that are during the employee’s normal working hoursnormal working hoursThe day of the week is irrelevant—what matters is whether the hours of travel coincide with the employee’s regularly scheduled hoursExample: Tyree normally works 9-5, M-F. If he travels on Monday from 6-8 p.m., he need not be paid for the travel time—but if he travels on any day from 1-3 p.m. he is due 2 hours’ pay.

Mastering Payroll

Travel TimeExample: Jan normally works 8 a.m. – 5 p.m., M - F. To attend a seminar, she leaves home for the airport Monday at 12 p.m. and arrives at her hotel in another city at 8 p.m. How many travel hours must Jan be paid for?Jan’s normal work hours are 8 a.m. – 5 p.m. She must be paid for travel time during these hours, which was 12 – 5 p.m. She does not have to be paid for her travel time between 5 p.m. and 8 p.m.

Mastering Payroll

Travel TimeExample: Chen normally works 7 a.m. - 4 p.m., M-F. He leaves home on a business trip Sunday at 5 a.m. arriving at the hotel at 11 a.m. The following Saturday, he leaves the hotel at 1 p.m. arriving home at 6 p.m. How many travel hours must Chen be paid for Sunday? for Saturday?

Sunday paid travel hours: 7 - 11 a.m. = 4 hours during Chen’s normal work hours, 7 a.m. - 4 p.m.

Saturday paid travel: 1 p.m. - 4 p.m. = 3 hours during Chen’s normal work hours, 7 a.m. - 4 p.m.

Mastering Payroll

Premium Pay for Overtime (OT)FLSA requires at least 1½ times employees’ regular hourly pay rate for each hour actually worked over 40 hours for the workweek A workweek is defined as 7 consecutive days or 168

consecutive hours—but need not be Monday - Sunday as long as the employer uses the same 7 days consistently

Excludable: Vacation, holiday or sick pay are not hours actually worked. Paid commuting time to and from work are not hours actually worked.

Prohibited: Applying one workweek’s overtime hours to another workweek to avoid paying OT. Exception: Health care and public sector employees.

Mastering Payroll

Premium Pay for Overtime (OT)How is a salaried employee’s regular hourly rate of pay calculated? Annual pay ÷ regular hours worked per year Monthly pay ÷ regular hours worked per month Weekly pay ÷ regular hours worked per week Biweekly pay ÷ regular hours worked per biweekly

period

Mastering Payroll

Premium Pay for Overtime (OT)Example: Serge’s son is getting married, so he arranges to work at the factory 48 hours this week and take off one day next week. His regular hourly pay rate is $24. How much must he be paid for this week? for next week?

Serge’s OT pay rate: $24 Serge’s OT pay rate: $24 ×× 1.5 = $36 1.5 = $36Week 1: (40 hrs ×× $24) + (8 hrs ×× $36) = $1,248 Serge must be paid 8 hours of OT for this weekWeek 2: 32 hrs ×× $24 = $768Serge’s employer may not apply the extra 8 hours in Week 1 to Week 2 to avoid OT pay in Week 1

Mastering Payroll

Premium Pay for Overtime (OT)Example: Marina’s workweek is Monday - Friday. She is out sick Monday and Tuesday, but is given 16 hours sick pay for the time. To make up for this time, Marina works 36 hours, Wednesday-Friday. If Marina’s hourly pay rate is $20, how much must she be paid this week?

$20 ×× 52 hrs (16 sick pay + 36 worked) = $1,040

The 16 hours sick pay are not hours actually worked, so they need not be included to determine if Marina is entitled to OT pay.

Mastering Payroll

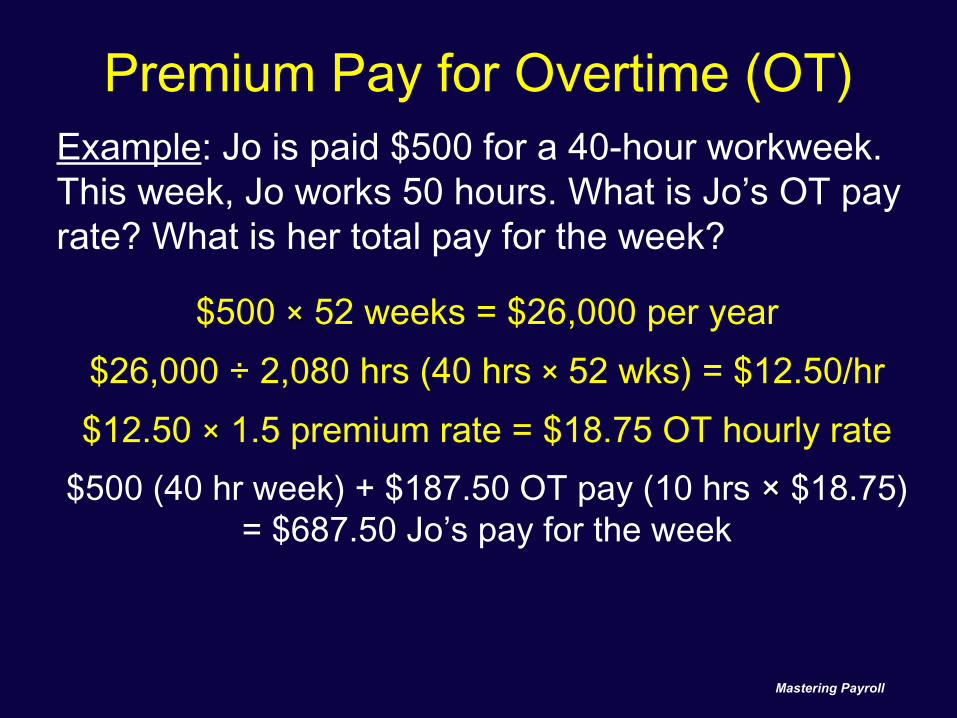

Premium Pay for Overtime (OT)Example: Jo is paid $500 for a 40-hour workweek. This week, Jo works 50 hours. What is Jo’s OT pay rate? What is her total pay for the week?

$500 ×× 52 weeks = $26,000 per year$26,000 ÷ 2,080 hrs (40 hrs × × 52 wks) = $12.50/hr$12.50 ×× 1.5 premium rate = $18.75 OT hourly rate

$500 (40 hr week) + $187.50 OT pay (10 hrs ×× $18.75) = $687.50 Jo’s pay for the week

Mastering Payroll

Premium Pay for Overtime (OT)Example: James is paid $1,200 for a 32-hour workweek. This week, James works 42 hours. What is James’s OT pay rate? What is his total pay for the week?

$1,200 × × 52 weeks = $62,400 per year$62,400 ÷ 1,664 hrs (32 hrs × × 52 wks) = $37.50/hr$37.50 × × 1.5 premium rate = $56.25 OT hourly rate

$1,200 (32 hrs × × $37.50) + $300 (8 hrs x $37.50) + $112.50 (2 hrs ×× $56.25) = $1,612.50 total pay

Mastering Payroll

Premium Pay for Overtime (OT)The following employees are exempt from OT (unless more employee-favorable state laws apply): Executives paid at least $455 a week Administrative personnel paid at least $455 a week

Persons actively responsible for establishing and enforcing company policy and general business operations

Professionals who do advanced work in science or learning and earn at least $455 a week. Includes computer systems professionals earning at least $27.63 an hour.

Outside salespersons—persons regularly and normally working away from the employer’s place of business to make sales calls

Mastering Payroll

Hiring EmployeesEmployers must obtain from new hires: A Social Security number (SSN)

Those without an SSN must obtain one by completing Form SS-5, Application for New Social Security Card

Form W-4, Employee Withholding Allowance Certificate Provides data that employers use to determine how

much FIT to withhold SIT withholding allowance certificate (if required) Age certificate (from those within 2 years of the legal

age they are allowed to work) State tax exemption certificate—e.g., when your state

has reciprocal agreements with neighboring states

Mastering Payroll

Form I-9An I-9 is completed as follows: Section 1. Completed by the employee

Employee provides name, address, DOB, SSN, and signs an oath that he or she is legally able to work in the U.S.

Section 2. Reviewed and signed by employer after viewing and recording documents that substantiate the employee’s identity and authorization to work in the U.S. To verify, examine just one document from List A

—or one each from Lists B and C

Mastering Payroll

Form I-9List A. Acceptable documents include: U.S. passport (expired or unexpired) Certain unexpired foreign passports Permanent resident card Alien registration receipt card

Employers need examine only Employers need examine only oneonedocument from this l ist to verify both document from this l ist to verify both the employee’s identity the employee’s identity andand eligibil i ty eligibil i ty

to work in the U.S.to work in the U.S.

Mastering Payroll

Form I-9

List B. Acceptable documents include: Driver’s license with photo School ID card with photograph Voter registration card with photo U.S. military card or draft record

List C. Acceptable documents include: U.S. Social Security Card Birth certificate U.S. citizen identification card

If a document from List A is not presented, If a document from List A is not presented, employers must use one document each employers must use one document each

from Lists B and Cfrom Lists B and C

Mastering Payroll

Form W-4All employees must complete Form W-4, Federal Withholding Allowance Certificate. The W-4 provides an employer with the data needed to withhold FIT from that employee’s pay Prohibited: Employers cannot withhold a flat

dollar amount or flat percentage of pay Permitted: Employees can ask to have an

additional flat dollar amount of FIT withheldUntil a W-4 is submitted, an employer must withhold FIT as

if the employee is single with zero allowances

Mastering Payroll

Form W-4Employers should not accept a W-4 that: is incomplete is altered by additions or deletions contains information that the employer knows to

be falseEmployers should refrain from giving tax advice on

employee withholding. Explain what data is needed but do not make suggestions—e.g., how many exemptions to take. Refer employees to IRS Publication 505 on the IRS website.

Mastering Payroll

Form W-4If an employee wants to change the number of withholding allowances, require a new W-4 Employers must implement a W-4 by the start

of the first payroll period ending on or after the 30th day from the date that a W-4 is submitted

Employers are not required to submit W-4 copies to the IRS unless the IRS asks for one

Mastering Payroll

Form W-4An employee may claim exempt from withholding —write “exempt” on Line 7—only if that employee: had no tax liability the previous year, and expects to have no tax liability in the current yearAn employee who claims exempt must file a new W-4 each year by February 15 (if this is a weekend or federal legal holiday, by the next business day)

Mastering Payroll

FICA TaxesFICA tax consists of Social Security and Medicare taxes. The 2014 rates are: Social Security tax—6.2% is withheld from the first $117,000

of an employee’s wages to a maximum $7,254.00 Medicare tax—1.45% is withheld on all wages (no limit) plus .9% of wages above $200,000

The employer matches some FICA taxes:Social Security tax—the employer pays 6.2% of the first $117,000 of the employee’s wages to a maximum $7,254.00Medicare tax—the employer pays 1.45% of wages (no limit)but not the additional .9% of wages above $200,000

Mastering Payroll

FICA TaxesExamples of employees exempt from FICA tax: Children, foster children and stepchildren under age

18 employed by sole proprietorships 100% owned by their parents

Children, foster children and stepchildren under age 18 employed by a partnership 100% owned by the parents

Children under age 21 doing domestic work in their parents’ home

Parents employed by their children for domestic work

Mastering Payroll

Federal Income Tax Withheld (FITW)Factors used to determine FITW: Employer pay period (weekly, biweekly, etc.) Employee marital status on the W-4 Employee personal allowances on the W-4 Employee federal taxable wages for the period Supplemental wages (e.g., bonuses)Find the correct amount of FITW for a paycheck

using IRS withholding tables in IRS Publication 15, Circular E, Employer’s Tax Guide.

Mastering Payroll

Form 941 Tax DepositsFITW + FICA are known as “941 taxes” because they are reported on Form 941, Employer’s Quarterly Federal Tax Return. The 941 shows the employer’s accumulated FITW + FICA withheld + employer FICA for the quarter When a pay period spans two quarters, report the liabilities for each quarter separately941 taxes not yet paid are “941 liabilities”

Mastering Payroll

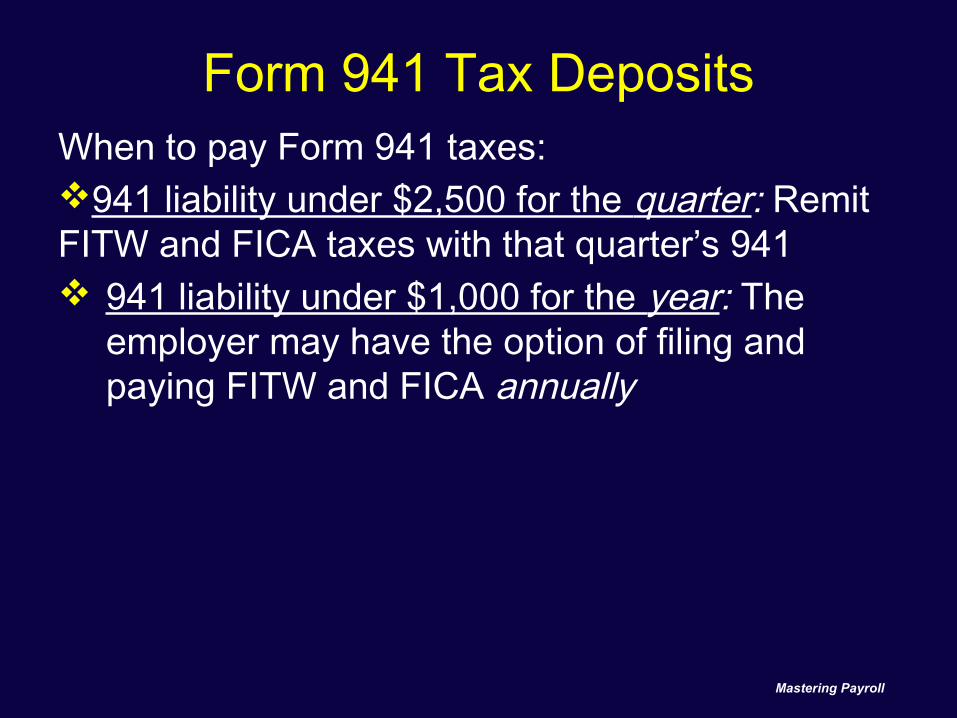

Form 941 Tax DepositsWhen to pay Form 941 taxes:941 liability under $2,500 for the quarter: Remit FITW and FICA taxes with that quarter’s 941 941 liability under $1,000 for the year: The

employer may have the option of filing and paying FITW and FICA annually

Mastering Payroll

Form 941 Tax Deposits941 liabilities must be deposited electronically using the IRS’s Electronic Federal Tax Payment System (EFTPS)Exception: An employer with 941 liabilities under $2,500 may pay the tax owed by check, credit or debit card, or electronic funds withdrawal (EFW)

Mastering Payroll

The Lookback Period for 941 TaxesThe lookback period is the 12-month period ending on June 30 of the prior year Example: The lookback period for depositing 941

taxes in 2014 is July 1, 2012–June 30, 2013

At the end of each calendar year, a monthly depositor uses the lookback period to determine its deposit status for next yearEmployers with up to $50,000 in accumulated 941 taxes for the lookback period are monthly depositors Employers with over $50,000 in accumulated 941

taxes for the lookback period become semiweekly depositors

Mastering Payroll

Form 941 Tax DepositsDue dates for depositing 941 liabilities A new employer is a monthly depositor through the

end of the first calendar year—with few exceptions An employer automatically becomes a semiweekly

depositor if it reaches a liability of: over $100,000 at any time during the calendar

year, or $50,000 for the lookback period

Mastering Payroll

How Monthly Depositors Remit Taxes

Monthly depositors must remit 941 taxes:by the 15th of the month following the month in which the liability is incurredby the next business day if the 15th falls on a weekend or federal legal holiday

Mastering Payroll

IRS Monthly Deposit ScheduleMonth Deposit Due DateJanuary February 15February March 15

March April 15April May 15May June 15June July 15July August 15

August September 15September October 15

October November 15November December 15December January 15

Mastering Payroll

Monthly Depositors: ExampleExample: Diaz Corporation is a monthly depositor. For March, Diaz’s’ s accumulated FITW and FICA tax liability is $3,500. When must Diaz remit its 941 taxes to the IRS?

Mastering Payroll

IRS Monthly Deposit ScheduleMonth Deposit Due Date

January February 15February March 15March April 15April May 15May June 15June July 15July August 15August September 15September October 15October November 15November December 15December January 15

Mastering Payroll

Monthly Depositors: ExampleExample: Diaz Corporation is a monthly depositor. For March, Diaz’s’ s accumulated FITW and FICA tax liability is $3,500. When must Diaz remit its 941 taxes to the IRS? Diaz must remit this 941 tax liability to the IRS:By April 15, using EFTPSIf April 15 is on a weekend or federal legal holiday, Diaz has until the next business day to make the deposit

Mastering Payroll

How Semiweekly Depositors Remit Taxes

Employers with accumulated 941 tax liabilities over $50,000 for the lookback period remit payment using the Wednesday/Friday rule

The due date is extended one business day if a federal legal holiday falls on any day between payday and the Wednesday/Friday deposit date

Mastering Payroll

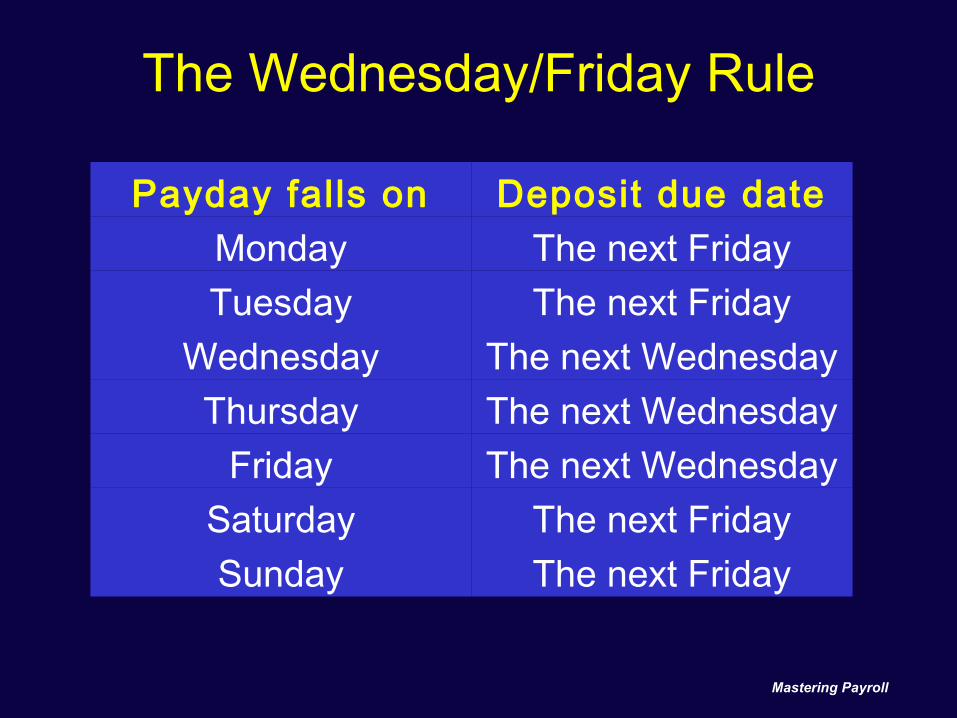

The Wednesday/Friday Rule

Payday falls on Deposit due dateMonday The next FridayTuesday The next Friday

Wednesday The next WednesdayThursday The next Wednesday

Friday The next WednesdaySaturday The next FridaySunday The next Friday

Mastering Payroll

Semiweekly DepositorsExample: Watson Co., a semiweekly depositor, pays its employees on the 15th and last day of the month. May 15 is a Tuesday. When must Watson remit its 941 taxes to the IRS?

Mastering Payroll

Semiweekly Depositors

Payday Falls on: Deposit Due DateMonday That FridayTuesday That Friday

Wednesday Next WednesdayThursday Next Wednesday

Friday Next WednesdaySaturday Next FridaySunday Next Friday

Mastering Payroll

Semiweekly Depositors: ExampleExample: Watson Co., a semiweekly depositor, pays its employees on the 15th and last day of the month. May 15, is a Tuesday. Watson must remit its 941 taxes to the IRS: that Friday, May 18If the taxes were due on a federal legal holiday that fell on any day from May 16–18, the taxes would be due on the next business day, Monday, May 21

Mastering Payroll

Semiweekly Depositors: ExampleExample: Watson Co.’s payday falls on May 31, a Thursday. When must Watson remit its 941 taxes to the IRS?

Mastering Payroll

Semiweekly Depositors

Payday Falls on: Deposit Due DateMonday The next FridayTuesday The next Friday

Wednesday The next WednesdayThursday The next Wednesday

Friday The next WednesdaySaturday The next FridaySunday The next Friday

Mastering Payroll

Semiweekly DepositorsExample: Watson Co.’s payday falls on May 31, a Thursday. When must Watson remit its 941 taxes to the IRS? Because May 31 is a Thursday, Watson must remits it 941 taxes by the following Wednesday, June 6 If any day from June 1–6 is a federal legal holiday, Watson has until the next business day, Thursday, June 7 to make the deposit

Mastering Payroll

Form 941 Deposit ShortfallsMonthly depositors remit a shortfall with their next 941Semiweekly depositors remit a shortfall by the earlier of: the Wednesday or Friday that falls after the 15th of

the month following the month of the shortfall the 941 due date

There are no penalties or interest if the shortfall does not exceed the greater of $100 or 2% of the liability, and the shortfall is deposited in a timely manner

Mastering Payroll

Shortfalls: Monthly DepositorsOn May 5, monthly depositor FreeCo discovers that its June 941 taxes deposited July 15 were short $95. FreeCo can avoid penalties and interest by paying the $95 by July 31, the due date of its second quarter 941.Caution: The IRS discourages casual use of the shortfall procedure—it is designed for unusual cases where estimates are required and for the occasional error.

Mastering Payroll

Shortfalls: Semiweekly DepositorsSemiweekly depositor, Redeye, Inc. discovers its 941 deposit for the period ending Friday, May 22, was short by $178—1.75% of its 941 liability for the period. Because the shortfall is less than 2% of Redeye’s 941 liabilities for the period, it can avoid penalties by depositing $178 by the first Wednesday or Friday after June 15 (the 15th of the month following the month of the shortfall).

Mastering Payroll

The One-Business-Day Deposit Rule

An employer that incurs a 941 liability of $100,000 at any time must remit its 941 taxes within one business day of reaching $100,000

Once the one-business-day deposit rule is triggered, that employer:

becomes a semiweekly depositor for the remainder of the year and

remains a semiweekly depositor in the following calendar year

Mastering Payroll

Form 941 RecapTo review: Form 941, Employer’s Quarterly Federal Tax

Return, reconciles wages paid and employment taxes withheld/owed with the amount of tax deposited for the quarter

Each quarter’s 941 is filed at the end of the month following the end of the quarter. For example, the first quarter ends March 31, so the first-quarter 941 is filed April 30 If deposits are timely made and for the full

amount, due date is extended 10 business days

Mastering Payroll

Quarterly Employment Tax Periods

Quarter Ending:Fil ing and

Deposit Due DateMarch 31 April 30June 30 July 31

September 30 October 31December 31 January 31

Mastering Payroll

FUTA Tax and Form 940FUTA (Federal Unemployment Tax Act) tax is paid

by the employer—not employees—to fund state unemployment benefit programs

Generally, an employer pays FUTA tax if it: pays wages of at least $1,500 in a calendar

quarter or employs at least one person for some part of any

day in 20 weeks during the current or previous year

All states impose a similar SUI tax on wages

Mastering Payroll

FUTA Tax and Form 940The FUTA tax rate for 2014 is 6.0% of the first

$7,000 of each employee’s taxable wages Employers are generally entitled to a maximum

FUTA credit of 5.4%, reducing their net FUTA rate to 0.6%

Some states took loans from the federal government to pay UI benefits. Employers in states that have not repaid their loan may not get the maximum 5.4% FUTA credit and will pay more than 0.6% of FUTA wages (generally referred to as a FUTA credit reduction).

Mastering Payroll

FUTA Tax and Form 940Form 940 and FUTA tax due dates Employers that deposited all FUTA taxes on time and in

full during the year have until Feb. 10 of the following year to file Form 940

Employers paying FUTA tax higher than 0.6% (due to unpaid state loans) must remit the additional tax by the following Jan. 31

If the FUTA tax liability for a quarter is: over $500—tax must be deposited before the end of

the month following the end of the quarter, even though the 940 is not due then

$500 or less, the liability can be rolled over to subsequent quarters until it exceeds $500, but is due the following Jan. 31

Mastering Payroll

Form 940: Electronic v. Paper FilingFUTA tax must be paid electronically via EFTPS

Exception: An annual FUTA liability of up to $500 may be paid by check, debit/credit card or EFW when filing the 940

Mastering Payroll

Mastering Payroll

Form 945Form 945, Annual Return of Withheld Federal

Income Tax, is used to report FITW on nonpayroll payments, including:

Backup withholding on certain payments, such as payments to independent contractors who failed to provide an SSN or TIN.

Gambling winnings Pensions, annuities and possibly interest and

dividends Military retirement

Form 945

Mastering Payroll

Form 945 reconciles FIT withheld from nonpayroll payments, such as pensions and other government payments

945 taxes normally are paid via EFTPSHowever, liabilities of less than $2,500 can be paid by check, debit/credit card or EFW when Form 945 is filed

Form 945 is an annual return, and accordingly, the lookback period is the second previous calendar year. For example, the lookback period for 2014 would be 945 taxes paid in 2012.

Form 945DryCo’s 945 liability for 2011 is $40,000. When must DryCo deposit its 945 tax liability for April 2014?Because DryCo’s total 945 taxes for 2012 did not exceed $50,000, it is a monthly depositor for 2014 and will deposit its 945 taxes by May 15, 2014 (or the next business day).

DryCo uses its 945 tax liability from 2012 (its second prior calendar year) to determine its 945 depositor status. When setting the 945 deposit schedule, 941 taxes are not considered.

Mastering Payroll

Form W-2Form W-2, Wage and Tax Statement, is a

summary of each employee’s taxable wages and taxes withheld for the year

Employers give copies B, C and 2 of the W-2 to employees, send Copy A to the SSA and keep Copy D for their records

Employees attach copies of their W-2 to their federal and state income tax returns

Some states and locals require that employers file copies of W-2

Mastering Payroll

Form W-2The W-2 must be provided to:Employees by Jan. 31 (or next business day) Terminated employees by the earlier of Jan. 31 or

within 30 days of their requestThe SSA by:the last day of February (or next business day)if filed electronically, by Mar. 31 (or next business day)States and local areas:dates vary by locale

Mastering Payroll

Form W-3Employers filing up to 249 Forms W-2 for the year file Copy A with Form W-3, Transmittal of Wage and Tax Statements, which is a summary of the data on the attached W-2s

Employers filing 250 or more W-2s for the year must file electronically with the SSA —but are not required to file a W-3

Mastering Payroll

How Long Must Records Be Retained?

FLSA requires keeping the records listed below for 3 years:

Payroll register Timecards Time sheets (reports of hours worked) Payroll tax records Tax deposit receipts W-4s Personnel files Cancelled and voided checks

Work schedules must be kept for 2 yearsMastering Payroll

How Long Must Records Be Retained?

The IRS requires keeping the following for 4 years from April 15 of the year following the year that the document applies to: Payroll register and payroll tax records Tax deposit receipts Personnel files Cancelled/voided checks Forms 941, 940, 945 and supporting documents

Mastering Payroll

How Long Must Records Be Retained?

The IRS requires keeping the following for 4 years: A returned W-2 from the date it was due A W-4 from the later of:

the date the company received it, or when last used to calculate FITW

Mastering Payroll

When Wages Become TaxableWages are taxable in the year that employees have constructive receipt of the pay—that is, when the pay is available to them:Example: December 2013 paychecks distributed to employees after Christmas but not picked up by some employees until 2014 are taxable to these employees in 2013.Example: Wages earned in late December 2013 but not paid to employees until 2014 are taxable to employees in 2014.

Mastering Payroll

When Wages Become TaxableWages are taxable in the year employees have

constructive receipt of their pay Unless the employer has a formal deferred

compensation plan, it cannot postpone paying wages to benefit itself or an employee

Advances and overpayments are taxable in the year that they are constructively received If repaid the same year, deduct from taxable wages If repaid in a subsequent year, consult a CPA or tax

attorney (rules are complex)

Mastering Payroll

SUI Tax Returns and DepositsReport SUI, the state version of FUTA, as follows: File SUI returns quarterly Taxes generally are due the last day of the month

following the end of the quarter Wage detail reports are generally filed quarterly SUI rates vary both by employer payments in

previous years for UI premiums and for UI benefits Some states also require employers, employees or

both to pay state disability insurance (SDI)

Mastering Payroll

Reporting SITWGenerally, employers must file a copy of employee W-2s with the state In most states, the deadline is the last day of

February—if filed electronically, March 31 Some—but not all—states require filing a state W-

2 or copy of the federal W-2 and may or may not have their own W-3 (check state law)

For states with no SIT, no W-2s are filed with the state

Mastering Payroll

Form 1099Form 1099 is filed to report payments to

independent contractors or investors 1099-MISC: reports nonemployee compensation

totaling at least $600 for the year in commissions, fees, royalties, rent and other payments—used primarily for independent contractors

1099-INT: reports interest paid 1099-DIV: reports dividends paid 1099-R: reports payments to retirees (for annuities,

pensions, etc.)

Mastering Payroll

Form 1099Form 1099 is due to: Recipients. Must receive their 1099s by Jan. 31 The IRS. Must be filed by the last day of February for

paper forms—by March 31, electronically File each kind of paper 1099s, a separate Form

1096, Annual Summary and Transmittal of U.S. Information Returns (electronic 1099s do not require a 1096)

Examples: With all paper Forms 1099-MISC, file a 1096; with all paper Forms 1099-INT, a separate 1096, etc.

Mastering Payroll

The Payroll RegisterA payroll register includes for each payment: Check number Employee’s name and SSN Gross wages or salary (regular pay, OT, bonus) Federal taxes withheld FICA taxes withheld State and local income taxes withheld Other deductions (health, dental or life insurance,

union dues, uniforms, etc.) Net payment to employee or employee’s financial

account(s)Mastering Payroll

Payroll Journal EntriesEach payday, you record two journal entries:First journal entry: Employee salaries and deductions ( “payroll distribution”)Second journal entry: Employer payroll tax expenses, such as FUTA and employer FICA

Mastering Payroll

Payroll Journal EntriesFirst journal entry: Employee salaries and deductions ( “payroll distribution”)

Salary ExpenseSalary Expense xxxxxxFICA EmployeeFICA Employee xxxxxxFITW PayableFITW Payable xxxxxxHealth Ins. Health Ins. −− employee contrib. employee contrib. xxxxxxUnion Dues Union Dues −− employee contrib. employee contrib. xxxxxxCashCash xxxxxx

Mastering Payroll

Payroll Journal EntriesExample: In the pay period ending May 9, 2014, XyCo’s gross wages are $25,000. XyCo withholds from employee pay $1,912.50 FICA, $4,500 FITW and $400 SITW

First journal entry: XyCo’s salaries and deductions XyCo’s salaries and deductions for the May 9for the May 9thth pay period: pay period:

Salary ExpenseSalary Expense 25,000.0025,000.00FICA EmployeeFICA Employee

1,912.501,912.50FITW PayableFITW Payable

4,500.004,500.00SITW PayableSITW Payable

400.00400.00CashCash

18,187.5018,187.50

Mastering Payroll

Payroll Journal EntriesSecond journal entry: Employer payroll taxesEach pay period, employers incur not only salary expense, but employer payroll expenses, such as the employer’s share of FICA, as well as FUTA and SUI taxes

Payroll Tax ExpensePayroll Tax Expense xxxxxxFICA EmployerFICA Employer

xxxxxxFUTA PayableFUTA Payable

xxxxxxSUI PayableSUI Payable

xxxxxxMastering Payroll

Payroll Journal EntriesExample: In the pay period ending May 9, 2014, XyCo’s incurs payroll expenses of $1,912.50 employer FICA, $200 FUTA and $295 SUI.

Second journal entry: XyCo’s employer payroll tax employer payroll tax expenses for the May 9expenses for the May 9 thth pay period: pay period:

Payroll Tax ExpensePayroll Tax Expense 2,407.502,407.50FICA EmployerFICA Employer

1,912.501,912.50FUTA PayableFUTA Payable

200.00200.00SUI PayableSUI Payable

295.00295.00 Mastering Payroll

Payroll Journal EntriesAnother journal entry is recorded when all withheld and employer taxes are remitted to federal and state agencies and vendors, such as insurance companies

FICA EmployeeFICA Employee xxxxxxFICA EmployerFICA Employer xxxxxxFITW PayableFITW Payable xxxxxxEmployee Health Ins.Employee Health Ins. xxxxxxEmployer Health Ins.Employer Health Ins. xxxxxx

CashCashxxxxxx

Mastering Payroll

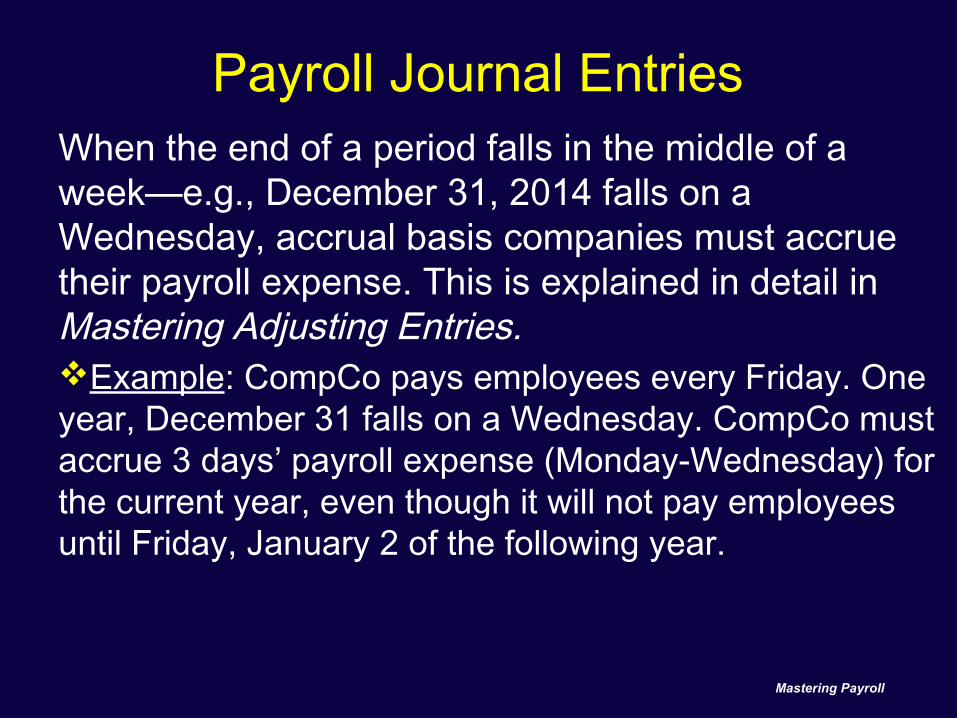

Payroll Journal EntriesWhen the end of a period falls in the middle of a week—e.g., December 31, 2014 falls on a Wednesday, accrual basis companies must accrue their payroll expense. This is explained in detail in Mastering Adjusting Entries.Example: CompCo pays employees every Friday. One year, December 31 falls on a Wednesday. CompCo must accrue 3 days’ payroll expense (Monday-Wednesday) for the current year, even though it will not pay employees until Friday, January 2 of the following year.

Mastering Payroll