Embed Size (px)

Citation preview

1

Executive Summary

The link between sound and well-developed financial systems and economic

growth is a fundamental one. Empirical evidence, both in developing and

advanced economies, has shown that countries with developed financial systems

grow at faster rates. Efficient and prudent allocations of resources by the financial

system is crucial for increasing productivity, boosting economic development,

enhancing equality of opportunity, and reducing poverty. Getting the financial

systems of developing countries to function more effectively in providing the full

range of financial services is thus a task that will be well rewarded with economic

growth.

The banking system is still by far the most important part of the financial system,

accounting for more than 75 percent of the assets. It is very hard to imagine a

modern national economy without a financial sector without functioning banks

the supply of money would collapse. A smooth-running financial sector is

therefore an essential requirement for a prospering national economy.

2

Legal provisions

Definition of banking:

“ Banking is one of the key drivers of the U.S. economy. Why? It provides the

liquidity needed for families and businesses to invest for the future. Bank loans

and credit means families don't have to save up before going to college or buying

a house, and companies can start hiring immediately to build for future demand

and expansion. Credit has gotten a bad name, thanks to the 2008 financial crisis,

but that's only because it was unregulated, used for consumption instead of

investment, and allowed to create a bubble.”

Definition of Banking company :

A financial institution that accepts deposits and channels the money into lending

activities; "he cashed a check at the bank"; "that bank holds the mortgage on my

home."

Statues Governing Banking Companies:

The law governing banks, bank accounts, and lending in the United States is a

hybrid of federal and state statutory law. Consumers and businesses may establish bank accounts in banks and savings associations chartered under state or

federal law. The law under which a bank is chartered regulates that particular bank. A mix of state and federal law, however, governs most operations and

transactions by bank customers.

Article 3 of the Uniform Commercial Code, as adopted by the various states, governs transactions involving negotiable instruments, including checks. Article 4 of the Uniform Commercial Code governs bank deposits and collections,

including the rights and responsibilities of depository banks, collecting banks, and banks responsible for the payment of a check. Other provisions of the

Uniform Commercial Code are also relevant to banking and lending law, including Article 4A (related to funds transfers), Article 5 (related to letters of credit), Article 8 (related to securities), and Article 9 (related to secured

transactions).

A number of regulations govern a check when it passes through the Federal

Reserve System. These regulations govern the availability of funds available to a

depositor in his or her bank account, the delay between the time a bank receives a

3

deposit and the time the funds should be made available, and the process to follow when a check is dishonored for non-payment. Federal law also provides

protection to bank customers. Prompted by banking crises in the 1930s, the federal government established the Federal Deposit Insurance Corporation, which

insures bank accounts of individuals and institutions in amounts up to $100,000.

A number of laws have been passed affecting banks, banking, and lending. A brief summary of these is as follows:

National Bank Act of 1864 established a national banking systems and

chartering of national banks. Federal Reserve Act of 1913 established the Federal Reserve System.

Banking Act of 1933 (Glass-Steagall Act) established the Federal Deposit

Insurance Corporation (FDIC), originally intended to be temporary. Banking Act of 1935 established the FDIC as a permanent agency.

Federal Deposit Insurance Act of 1950 revised and consolidated previous laws governing the FDIC.

Bank Holding Company Act of 1956 set forth requirements for the

establishment of bank holding companies. International Banking Act of 1978 required foreign banks to fit within the

federal regulatory framework. Financial Institutions Regulatory and Interest Rate Control Act of 1978

created the Federal Financial Institutions Examination Council; it also

established limits and reporting requirements for insider transactions involving banks and modified provisions governing transfers of electronic funds.

Depository Institutions Deregulation and Monetary Control Act of 1980 began to eliminate ceilings on interest rates of savings and other accounts

and raised the insurance ceiling of insured account holders to $100,000. Depository Institutions Act of 1982 (Gar-St. Germain Act) expanded the

powers of the FDIC and further eliminated ceilings on interest rates.

Competitive Equality Banking Act of 1987 established new standards for the availability of expedited funds and further expanded FDIC authority.

Financial Institutions Reform, Recovery, and Enforcement Act of 1989 set forth a number of reforms and revisions, designed to ensure trust in the savings and loan industry.

Crime Control Act of 1990 expanded the ability of federal regulators to combat fraud in financial institutions.

Federal Deposit Insurance Corporation Act of 1991 expanded the power and authority of the FDIC considerably.

4

Housing and Community Development Act of 1992 set forth provisions to combat money laundering and provided some regulatory relief to certain

financial institutions. Riegle Community Development and Regulatory Improvement Act of

1994 established the Community Development Financial Institutions Fund to provide assistance to community development financial institutions.

Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

permitted bank holding companies that were adequately capitalized and managed to acquire banks in any state.

Economic Growth and Regulatory Paperwork Reduction Act of 1996 brought forth a number of changes, many of which related to the modification of regulation of financial institutions.

Gramm-Leach Bliley Act of 1999 brought forth numerous changes, including the restriction of disclosure of nonpublic customer information

by financial institutions. The Act provided penalties for anyone who obtains nonpublic customer information from a financial institution under false pretenses.

Numerous federal agencies promulgate regulations relevant to banks and banking,

including the Federal Deposit Insurance Corporation, Federal Reserve Board, General Accounting Office, National Credit Union Administration, and Treasury

Department.

The ability for bank customers to engage in electronic banking has had a significant effect on the laws of banking in the United States. Some laws that govern paper checks and other traditional instruments are difficult to apply to

corresponding electronic transfers. As technology develops and affects the banking industry, banking law will likely change even more.

Functions of Banks:

How is money created? Other than the currency and bills that are made in a

national mint, the money that our nation uses on a daily basis is actually created

by commercial banks in the form of deposits and other things.

A bank depends on the misfortune of its customers to create money. Someone must be in debt to commercial banks in order for money and credit systems to work. When a borrower spends the money he or she has been loaned, the recipient

deposits it in another bank. That deposit represents the creation of new money. A bank pays its bills by borrowing if people don't pay their taxes. The interest that a

bank charges customers on the loans it gives becomes that bank's profit. A

5

customer's assets and liabilities add up equally. When a bank makes unnecessary profit, it makes for a burden on taxpayers.

The Federal Reserve processes checks and cash. Banks order cash from the Fed

when they need it, and ship it cash when they have too much. Checks can even be processed cross-country; for instance, if someone from Los Angeles writes a

check in Philadelphia, the Philly bank credits the person's account and sends the check to the Federal Reserve of Philadelphia, then the check is sent to the Federal Reserve of Los Angeles where it goes to the bank of Los Angeles. The Fed

processes one third of all checks written in America. Many of them are deposited electronically. High-tech machines are used for all sorts of transactions. Fedwire

is a program that allows money to be transferred over seconds. ACH allows for constant, direct payments. There are also machines designed to detect bill denominations, extent of use, and authenticity.

Banks can borrow money from the Fed as well, although it is considered a last resort lender. It acts to prevent too much borrowing. Types of loans are adjustment credit, for overnight loans or short-term problems; seasonal loans,

which are extended up to nine months to help in seasonal swings in deposits and loans; and extended loans, which are prolonged because of financial difficulties if

banks have a plan to correct the problems. Banks aren't allowed to take advantage of interest or discount rates and make profits by borrowing, either.

The Fed keeps the banking system competitive by creating new banks and mergers frequently. It examines bank information for security, and the banks

themselves for safety. The Fed will fine banks, suspend employees, or pass new laws if they feel the need to.

There are 12 Fed district banks, member banks, and the Board of Governors,

which heads the Federal Reserve. Each member of the Board is appointed to 14-year terms so the members are well insulated from outside political pressures. It is financially self-sufficient as a bank; it doesn't rely on Congress appropriations,

but rather on interest from large holdings on US government securities.

The Board gives the Treasury the excess of what it took as opposed to what it spent. It sets reserve requirements (a monetary policy tool, along with discount

rates and open-market operations); this is important because it affects the amount of loans and bank money commercial banks have. (Commercial banks are those that take deposits and give loans on an individual basis.) Reserve requirements are

percentages of money or credit banks must keep on hand or on deposit at the Federal Reserve Bank.

6

System of book keeping in banks

Obectives & System

An accounting system can be defined as the series of tasks in an entity by

which transactions are processed as a means of maintaining financial records. Such a system recognizes, calculates, classifies, posts, analyses, summarizes and report Transaction.

The auditor of a bank needs to obtain a thorough understanding of the

accounting system of the bank to assess the relevance and reliability of the accounting records and other source data underlying the financial statements. He should gain an understanding of the books of account and other related

records maintained by the auditee. He should also understand the flow of various kinds of transactions. The auditor can gain such understanding through

enquiries of appropriate personnel, by making reference to documents such as accounting manual, procedures manual and flow charts, and by observing the actual conduct of operations.

It may be stated here that even in a fully computerised branch, some work is

presently carried out manually, e.g., preparation of vouchers, preparation of letters of credit and guarantees, preparation of some returns and statements, etc. In partly computerised branches, generally the back-office work (i.e. the

internal processing of transactions of the branch) is carried out on computers whereas the customers transactions (i.e. the front-office work) are processed

manually. Many of the banks in the private sector have networked all or most of their branches in the country; this has given them the capability of handling most of the transactions of their customers at any of the branches.

Banks, like most other large-sized institutions, follow the mercantile system of accounting. Thus, the system of recording, classifying and summarizing the transactions in a bank is in substance no different from that followed in other

entities having similar volume of operations. However, in the case of banks, the need for the ledger accounts, especially those of customers, being accurate and up-to-date is much stronger than in most other types of enterprises. A bank

cannot afford to ignore its ledgers particularly those containing the accounts of its customers and has to enter into the ledgers every transaction as soon as it

takes place. In the case of banks, relatively lesser emphasis is placed on books of prime entry such as cash books or journals. This is unlike most other types of enterprises where books of prime entry are generally kept up-to-date while

7

ledgers, including the general ledger and subsidiary ledgers for debtors, creditors, etc., are written up afterwards

Banks follow the accounting procedure of voucher posting under which the vouchers are straightaway posted to the individual accounts in the subsidiary

ledgers. At the end of each day, the debit and credit vouchers relating to a particular type of transactions (e.g. savings bank accounts, current accounts, demand loans, cash credit accounts, etc.) are entered on separate voucher

summary sheets and the total thereof is posted to the respective control account in the General Ledger. The general ledger trial balance is prepared

every day.

Books of Accounts

General ledger

General ledger contains all the accounts for recording transactions relating to a

company's assets, liabilities, owners' equity, revenue, and expenses. In modern

accounting software or ERP, the general ledger works as a central repository for

accounting data transferred from all subledgers or modules like accounts payable,

accounts receivable, cash management, fixed assets, purchasing and projects. The

general ledger is the backbone of any accounting system which holds financial

and non-financial data for an organization. The collection of all accounts is

known as ledger account. This may be a large book.

The statement of financial position and the statement of income and

comprehensive income are both derived from the general ledger. Each account in

the general ledger consists of one or more pages. The general ledger is where

posting to the accounts occurs. Posting is the process of recording amounts as

credits (right side), and amounts as debits (left side), in the pages of the general

ledger. Additional columns to the right hold a running activity total (similar to a

checkbook).

The listing of the account names is called the chart of accounts. The extraction of

account balances is called a trial balance. The purpose of the trial balance is, at a

preliminary stage of the financial statement preparation process, to ensure the

equality of the total debits and credits.

8

The general ledger should include the date, description and balance or total

amount for each account. It is usually divided into at least seven main categories.

These categories generally include assets, liabilities, owner's equity, revenue,

expenses, gains and losses. The main categories of the general ledger may be

further subdivided into subledgersto include additional details of such accounts as

cash, accounts receivable, accounts payable, etc.

Because each bookkeeping entry debits one account and credits another account

in an equal amount, the double-entry bookkeeping system helps ensure that the

general ledger is always in balance, thus maintaining the accounting equation:

The accounting equation is the mathematical structure of the balance sheet.

Although a general ledger appears to be fairly simple, in large or complex

organizations or organizations with various subsidiaries, the general ledger can

grow to be quite large and take several hours or days to audit or balance.

Subsidiary Books

Subsidiary Books refers to books meant for specific transactions of similar nature.

Subsidiary Books are also known as Special journals or day books. To overcome

shortcoming of the use of the journal only as a book of original entry, the journal

is subdivided into specific journals or subsidiary books .

NEED OF SUBSIDIARY BOOKS

To avoid repetition.

To provide information on a prompt basis.

To facilitate internal check system.

To classify transactions.

To avoid bulky & voluminous records

9

TYPES OF SUBSIDIARY BOOKS

CASH BOOKS

A cash book is a special journal which is used for recording all cash receipts &

cash payments .

TYPES OF CASH BOOKS

1 ) Single- column cash books .

2) Double-column cash books.

3) Triple-column cash books.

4) Petty cash books.

DATE RECEIPT RECEIPT No. L.F AMOUNT DATE PAYMENT VOUCHER

No. L.F AMOUNT DATE RECEIPT CASH BANK DATE PAYMENTS CASH

BANK

DATE RECEIPT DISCOUNT CASH BANK DATE PAYMENT DISCOUNT

CASH BANK

PURCHASE BOOKS

These are the b ooks used for recording purchases on credit .

Things purchased on credit for personal use are not recorded in this

book. It also does not record the fixed assets purchased .

DATE PARTICULAR INVOICE NO. L.F AMOUNT

SALES BOOKS Books used for recording goods sold on credit. DATE

PARTICULAR OUTWARD INVOICE NO. L.F AMOUNT

PURCHASE RETURN BOOKS Books used for recording goods returned to the

seller. DATE PARTICULARS L.F DEBIT NOTES AMOUNT

SALES RETURN BOOKS Books used for recording the goods returned by the

buyer. DATE PARTICULARS L.F CREDIT NOTE AMOUNT

10

BILLS RECEIVABLE BOOKS(B/R)

This is used for the purpose of recording the details of bills receivable. The

individual accounts of parties from whom bills are received will be credited with

the amount in the bills receivable book.

DATE FROM WHOM READ ACCEPTOR DATE OF BILLS TERM DATE OF

MATURITY WHERE PAYABLE AMOUNT HOW DEPOSED

BILLS PAYABLE BOOK (B/P)

This is used for the purpose of recording the details of bills payable. The

individual accounts of the parties to whom the bills are issued will be debited with

the corresponding amount in the bills payable book. The periodic total is posted to

the credit of bills payable account in the ledger by writing “By Sundries as per

Bills Payable Book”.

Example:

S.NO. DATE NAME OF DRAWER PAYEE DATE OF BILL TERM DATE OF

MATURITY WHERE PAYABLE AMOUNT REMARK 16 May S&Co. Arya

mills 16 may 2006 30 days 16 June 2006 Central bank 5000

PETTY CASH BOOK

This book keeps account of all the miscellaneous spending. This might include:

child fees, window-cleaning bills, stationery, postage, cleaning supplies and any

other sundry item.

AMT. RECEIVED DATE PARTICULAR AMOUNT POSTAGE CARRIAGE

TRAVELLING SUNDRY EXP.

11

Memorandum Books

To maintain the records of company in proper way, accountant needs lots of

books. One of them is memorandum book or waste book. Memorandum or waste

book is that note book which is used to write the transactions when it happened

before writing all these transactions in journal. It is needed where there

are thousands of transactions are done within one day on the sale point. This book

is very helpful to record in journal. Its other name is rough book, long book and

rough copy book.

Final Accounts

Legal provisions

Section 29 in BANKING REGULATION ACT,1949

Accounts and balance-sheet.—

(1) At the expiration of each calendar year 1[or at the expiration of a period of

twelve months ending with such date2 as the Central Government may, by noti-

fication in the Official Gazette, specify in this behalf,] every banking company

incorporated 3[in India], in respect of all business transacted by it, and every

banking company incorporated 4[outside India], in respect of all business

transacted through its branches 3[in India], shall prepare with reference to 5[that

year or period, as the case may be,] a balance-sheet and profit and loss account as

on the last working day of 6[that year or the period, as the case may be,] in the

Forms set out in the Third Schedule or as near thereto as circumstances admit:

7[Provided that with a view to facilitating the transition from one period, of

accounting to another period of accounting under this sub-section, the Central

Government may, by order published in the Official Gazette, make such

provisions as it considers necessary or expedient for the preparation of, or for

other matters relating to, the balance sheet or profit and loss account in respect of

the concerned year or period, as the case may be.]

(2) The balance-sheet and profit and loss account shall be signed—

12

(a) in the case of a banking company incorporated 3[in India], by the manager or

the principal officer of the company and where there are more than three directors

of the company, by at least three of those directors, or where there are not more

than three directors, by all the directors, and

(b) in the case of a banking company incorporated 4[outside India] by the

manager or agent of the principal office of the company 3[in India].

(3) Notwithstanding that the balance-sheet of a banking company is under sub-

section (1) required to be prepared in a form other than the form 3[set out in Part I

of Schedule VI to the Companies Act, 1956 (1 of 1956)], the requirements of that

relating to the balance-sheet and profit and loss account of a company shall, in so

far as they are not inconsistent with this Act, apply to the balance-sheet or profit

and loss account, as the case may be, of a banking company. 9[(3A)

Notwithstanding anything to the contrary contained in sub-section (3) of section

210 of the Companies Act, 1956 (1 of 1956), the period to which the profit and

loss account relates shall, in the case of a banking company, be the period ending

with the last working day of the year immediately preceding the year in which the

annual general meeting is held.] 10[Explanation.—In sub-section (3A), “year”

means the year or, as the case may be, the period referred to in sub-section (1).]

(4) The Central Government, after giving not less than three months’ notice of its

intention so to do by a notification in the Official Gazette, may from time to time

by a like notification amend the Form set out in the Third Schedule.

Section 33 in BANKING REGULATION ACT,1949

Display of audited balance-sheet by companies incorporated outside India.—Every banking company incorporated 1[outside India] shall, not later than the first Monday in August of any year in which it carries on

business, display in a conspicuous place in its principal office and in every branch office 2[in India] a copy of its last audited balance-sheet and profit

and loss account prepared under section 29, and shall keep the copy so displayed until replaced by a copy of the subsequent balance-sheet and profit and loss account so prepared, and every such banking company shall

display in like manner copies of its complete audited balance-sheet and profit and loss account relating to its banking business as soon as they are

available, and shall keep the copies so displayed until copies of such subsequent accounts are available.

13

COMPANY’S PROFILE

DEVELOPMENT CREDIT BANK

DCB Bank (Formerly Development Credit Bank Ltd.) is private sector

scheduled commercial bank in India. It has a network of 130 branches[5] and 236

ATMs in the country.[6] It offers products to individuals, small and medium

businesses, rural banking and corporates in selective regions. The Bank is present

in 16 states and 2 Union Territories. Metros having DCB Bank branches are

Ahmedabad, Bengaluru, Chennai, Delhi, Gurgaon, Hyderabad Kolkata, Mumbai

and Pune. The Bank has dedicated rural banking branches in Andhra Pradesh,

Chhattisgarh, Gujarat, Madhya Pradesh, Odisha and Rajasthan. Other DCB Bank

locations are; State of Gujarat - Ahmedabad, Ankleshwar, Bhuj, Daman (Union

Territory), Gandhinagar, Rajkot, Sidhpur, Silvassa (Union Territory), Surat, Vapi

and Vadodara. Branches in the state of Goa - Mapusa, Margao, Panjim and

Vasco. Branches in Rajasthan - Jaipur and Jodhpur. DCB Bank has recently

inaugurated a branch at Minjur, Tamil Nadu. The Aga Khan Fund for Economic

Development (AKFED) in the promoter of the Bank with around 18% stake.

Public shareholding under the Resident Individual category is approximately

39.4%. The Bank received the Scheduled Commercial Bank licence from the

Reserve Bank of India on 31 May 1995.[7]

DCB Bank's financial products and services range from loans for Small and

medium enterprises, Wealth Management, banking for Non Resident Indians,

Internet Banking, Mobile Banking, Business Finance, Home Loans .[2] It also

offers banking solutions for resident Indians such as savings account, current

account, fixed deposit, recurring deposit, PayLess Credit Card, international Debit

cum ATM card, insurance products and financial services like Electronic funds

transfer (NEFT & RTGS), online income tax payment, online bill payment for

utilities, card to card money transfer, DCB on the Go - instant mobile banking,

SMS banking, telephone banking, Visa money transfer, foreign exchange

remittance service amongst others.

14

DCB Bank is a modern emerging new generation private sector bank with 130 plus branches across 17 states and 2 union territories. It is a scheduled commercial

bank regulated by the Reserve Bank of India. It is professionally managed and governed. DCB Bank has contemporary technology and infrastructure including

state of the art internet banking for personal as well as business banking customers.

DCB Banks business segments are Retail, micro-SMEs, SMEs, mid-Corporate, Agriculture, Commodities, Government, Public Sector, Indian Banks, Co-

operative Banks and Non Banking Finance Companies (NBFC). DCB Bank has approximately 450,000 customers.

DCB Bank has deep roots in India since its inception in 1930s. Its promoter and

promoter group the Aga Khan Fund for Economic Development (AKFED) & Platinum Jubilee Investments Ltd. holds over 19% stake. AKFED is an

international development enterprise. It is dedicated to promoting entrepreneurship and building economically sound companies.

History

Founded in the1930s, in Mumbai from a series of Co-operative bank mergers with

the Ismailia Co-operative Bank Limited and the Masalawala Co-operative Bank

respectively. These 2 banks later merged to form Development Co-operative

Bank, that changed to Development Credit Bank after it was granted the

scheduled bank license by the Reserve Bank of India in May 1995. The Bank

went on to successfully offer shares to the public by an Initial Public Offering

(IPO) in 2006. DCB Bank Limited is the new name of the Bank, changed with

due regulatory approval in January 2014.

Development Credit Bank (DCB) is the only co-operative bank which has successfully attained prosperity in the face of change. On May 31, 1995 bank was

converted into a Scheduled Commercial Bank. The bank has considerably expanded the DCB network by 2008 through shared networks. It is not just a bank

butafinancialsupermarket.

15

Bank offers an extensive range of products through its branches. The low-cost

products have been designed to cater the needs of small and medium businesses in selective regions. asic products like savings and current accounts and innovative

products like ‘DCB Trio’ and ‘Easy Business,’ are also being offered. Bank also offers demat account and a range of investment products like mutual funds, insurance and bonds make the product offering complete.

Development Credit Bank (DCB) is emerging private sector banks in India has the Network of 80 state-of-the-art branches and extension counters spread across

the states of Maharashtra, Gujarat, Andhra Pradesh, Karnataka, New Delhi, Rajasthan, Goa, Tamil Nadu, Haryana, West Bengal, Union Territories of Daman & Diu and Dadra & Nagar Haveli.

The terms of the banking license issued to the Bank under Section 22 of the

Banking regulation Act stipulated, amongst others, that: a) the Bank must comply with the Guidelines on Entry of Private Sector Banks

dated January 22, 1993 issued by the Reserve Bank of India;

b) on the date of conversion, the unimpaired value of the paid up capital and reserves of the Bank together with the share application money received by it should not be less than Rs.1000 million;

c) the Bank must make a public issue of its equity and arrange to have its shares

listed on stock exchanges immediately after one year of its operations; d) the Bank must comply with the priority sector lending norms of 40% as

applicable to private sector banks; and that

e) the Bank must ensure that not less than 25% of its branches are in rural/semi-urban areas within three years of its operations.

The Guidelines on Entry of Private Sector Banks which chalk out the scheme for permitting the entry of new private sector banks, prescribe, in relation to such a

new private sector bank that: a) the new bank may be listed in the Second Schedule of the Reserve Bank, 1934;

b) shares of the banks should be listed on stock exchanges;

c) voting rights of the shareholders of the bank shall be governed by the ceiling of

16

1% (now increased to 10%) of the total voting rights as stipulated in Section 12(2) of the Banking Regulations Act;

d) the new bank must not have as its director any person who is a director of any

other banking company or of companies which are entitled to exercise voting rights in excess of 20% of the total voting rights of all the shareholders of the banking company as laid down in the Banking Regulation Act, 1949;

e) the bank must achieve capital adequacy of 8% (now increased to 9%) of the

risk weighted assets from the beginning. Similarly norms for income recognition, asset classification, and provisioning will also be applicable to it from the beginning. The bank must also comply with the single borrower and group

borrower exposure limits that will be in force from time to time;

f) though the bank must comply with the norms for priority sector lending, some modification in the composition of the priority sector lending may be considered by the RBI for an initial period of three years;

g) the bank may be issued an authorised dealer’s license to deal in foreign

exchange when applied for; h) it shall be governed by the policy that banks are free to open branches at

various centres including that banks are free to open branches at various centres including urban/metropolitan centres without the prior approval of the RBI once

they satisfy the capital adequacy and prudential accounting norms. However, to avoid over-concentration of their branches in metropolitan areas and cities, a new bank must open rural and semi-urban branches also; and that

i) such a new bank must make full use of modern infrastructural facilities in office

equipment, computer, telecommunications etc. in order to provide good customer service.

2007

- Development Credit Bank Ltd (DCB) has appointed Mr. D E Udwadia as an Additional Director of the Bank.

2009

- Development Credit Bank Ltd (DCB) has appointed Mr. Suhail Nathani as an Additional Director of the Bank at the Meeting of the Board of Directors of the

17

Bank held on January 29, 2009.

- Development Credit Bank Ltd (DCB) has appointed Mr. Murali M Natrajan as an Additional Director of the Bank w.e.f April 29, 2009. Further, pursuant to

approval of the Reserve Bank of India, Mr. Murali M Natrajan has been appointed as Managing Director (MD) & CEO of the Bank for a period of three years from April 29, 2009.

2010

- DCB Appoints Mr J.K Vishwanath as Chief Credit Officer.

- Development Credit Bank Ltd. and ICICI Lombard GIC Ltd. in Bancassurance partnership.

- DCB received permission to open two Semi-Urban / Rural branches in Gujarat. The locations are Netrang, a Rural branch in Bharuch district and Mandvi, a Semi

Urban branch in Surat district.

2011 - Development Credit Bank (DCB) inaugurated its newest branch in Gujarat at

Vadodara . The branch is located at Ground floor of Startrek Building, Opposite ABS Tower, OP Road, Vadodara.

- DCB Bank inaugurates 81st branch at Mandvi, Surat District, Gujarat.

- DCB presents Aga Khan Hockey Tournament May 15, 21, 2011.

2012 - Development Credit Bank Ltd has informed BSE regarding updates on Capital

raising plan - QIP issue and preferential issue.

- DCB Bank inaugurates new branches in Itarsi and Pipariya, Madhya Pradesh. -DCB Bank and ITZ Cash launch Freedom Pre-Paid Card.

18

DCB’S vision is to be the most innovative and responsive neighbourhood

community bank in India serving entrepreneurs, individuals and businesses.

DCB’s Value

Treat Everyone with Dignity - Respect

Do What is Right - Ethical

Be Open & Transparent - Fair

Sense of Urgency, Passion & Energy - Dynamic

Go the Extra Mile & Find Solutions - Stretch

Improve Continuously - Excellence

Play as a Team, To Win - Teamwork

Support the Society – Contribute

Quick Facts

DCB Bank reported full year Net Profit of 151 Cr. in FY 2014 as against full year Net Profit of 102 Cr. in FY 2013. The Banks Net Profit for Q4

FY 2014 was 39 Cr. as against Net Profit of 34 Cr. in Q4 FY 2013 and 36 Cr. in Q3 FY 2014.

As on March 31, 2014, the Balance Sheet was at 12,923 Cr. as against

11,279 Cr. as on March 31, 2013, a growth rate of 15%. Retail Deposits (Retail CASA and Retail Term Deposits) continued to

provide a stable resource base to the Bank. Retail Deposits were at 77% of Total Deposits as on March 31, 2014.

CASA ratio as on March 31, 2014 was at 25% as against 27% as on March

31, 2013. Net Advances grew to 8,140 Cr. as on March 31, 2014 from 6,586 Cr. as

on March 31, 2013 a growth rate of 24%. Capital Adequacy Ratio (CAR) was at 13.71% as on March 31, 2014 with

Tier I at 12.86% and Tier II at 0.85% as per Basel III norms.

Crisil Ratings assigned "CRISIL A1+" (pronounced as "CRISIL A one plus") rating for Short Term Fixed Deposit Programme (with a contracted

maturity of upto 1 year). Share Holding Pattern (as on March 31, 2014)

19

Key non-promoter shareholders %

*AKFED and PJI

18.46%

***Institutions

Others (Non-Institutions)** 28.55%

8.35%

Individuals

31.96%

Bodies Corporate

12.68%

*AKFED – Aga Khan Fund for Economic Development and PJI –

Platinum Jubilee Investment Ltd.

**Includes Clearing Members (0.75%), Non Resident Indians (2.39%),

Foreign Corporate Bodies (4.69%), Trusts (0.34%) & Directors and their

relatives (0.18%)

***Institutions includes 12.31% held by FII

Tano Mauritius India FVCI II 4.76%

WCP Holdings III 4.69%

Ambit Corporate Finance Pvt. Ltd. 4.18%

The South India Bank Ltd 3.31%

Tata Capital Financial Services Ltd 2.63%

TVS Shriram Growth Fund India 2.51%

Sundaram Mutual Fund A/c Sundaram Select Midcap 2.19%

Code of Conduct For Members of the Board of Directors

This Code of Conduct (the “Code”) has been adopted by DCB's Board of Directors and summarizes the standards that must guide their actions. While

covering a wide range of business practices and procedures, these standards cannot and do not cover every issue that may arise, or every situation where

ethical decisions must be made, but rather set forth key guiding principles that represent the DCB's policies, regulators intent and Clause 49 requirements in this regard. Reference to the Code set forth below and reliance on common sense and

good judgment will help resolve issues not specifically dealt with in the Code.

20

However, for interpretation / understanding the wider meaning or scope of the terms “Clause 49”, “Confidential Information”, Insider Trading” and “Conflict of

Interest”, a reference may be made to the Chairman who may consult his advisors / Head Legal and Compliance or seek any general advice. In particular, following

should be observed as a code;

1. Board members should observe the highest standards of ethical conduct and abide by all applicable laws and regulations (including on insider trading) to which they are subject.

2. When exercising the powers and carrying out the tasks and duties conferred upon them, Board members are expected to act in the interests

of DCB to the best of their ability and judgement, consistent with their responsibilities to the regulators.

3. As a part of good corporate governance practices, the members of the

Board are expected to attend the Board meetings regularly and participate in the deliberations and discussion effectively.

4. As Directors on the Board be providing broad directions to the management team and would undertake such steps as necessary for good corporate governance and compliance of all regulatory requirements. They

will monitor the performance of the bank on a periodic basis and provide guidance to the Management on key aspects relating to key policy matters.

5. Board Members are expected to maintain the Confidentiality of non-public information about the DCB or its activities or operation to which they have access by virtue of their functions as Board Members (Confidential

Information). If Board members are required to disclose “Confidential Information” by reason of legal requirements, they should inform the

Chairman of any such requirement, if practicable in advance, who may, if appropriate, raise the matter with the Board.

6. When making public statements on DCB related matters, Board members

will refrain from making any statements on behalf of the Bank and in case there is a need, they will consult the Chairman

7. If a conflict of interest or appearance of a conflict of interest, with the DCB arises, the Board members are expected to take action, as appropriate, to address the conflict. The Board member should inform the

Chairman, who may, if appropriate raise the matter with the Board.

21

8. The members of the Board of Directors may seek information in the interest of the Bank from the CEO directly and from the members of the

management committee of the Bank if necessary.

9. It is expected from the members of the Board of Directors that they would

not involve themselves in general or personal administration or day to day functioning of the Bank, in conformance with Clause 49 of the Listing Agreement entered into with the stock exchanges.

10. The obligations set out in paragraph 6 of this Code shall continue after the Board member steps down or ceases to be on the Board.

22

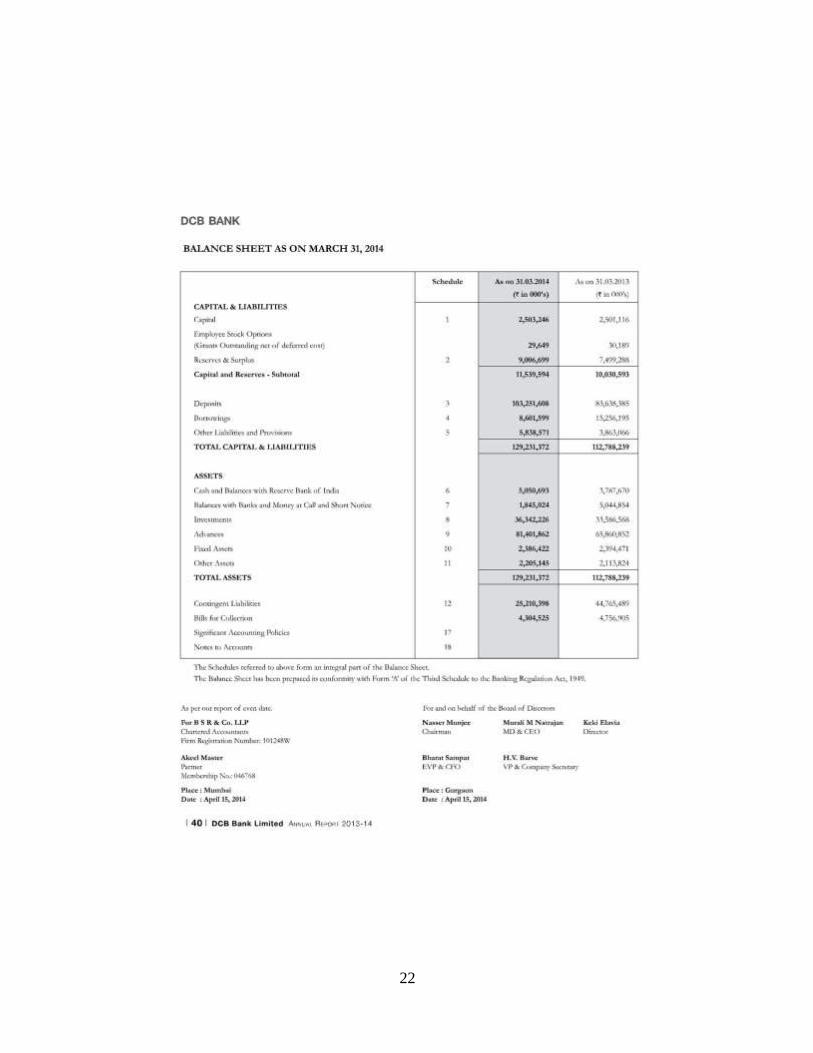

23

24

25

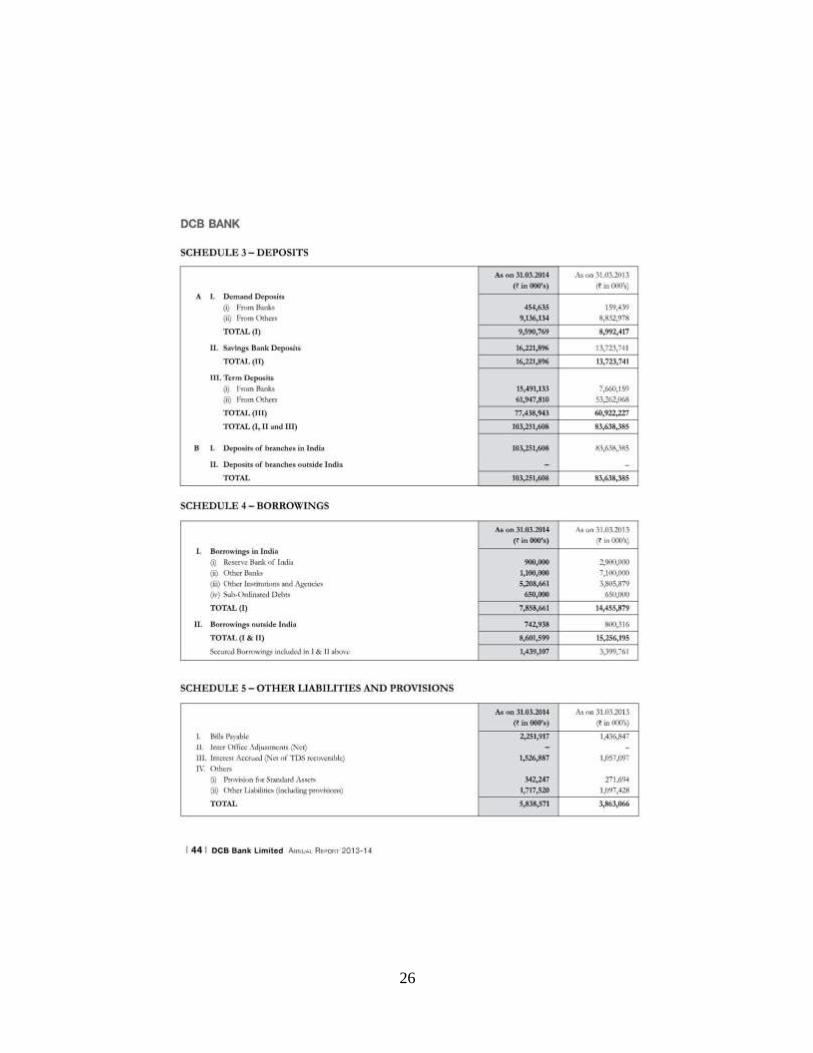

26

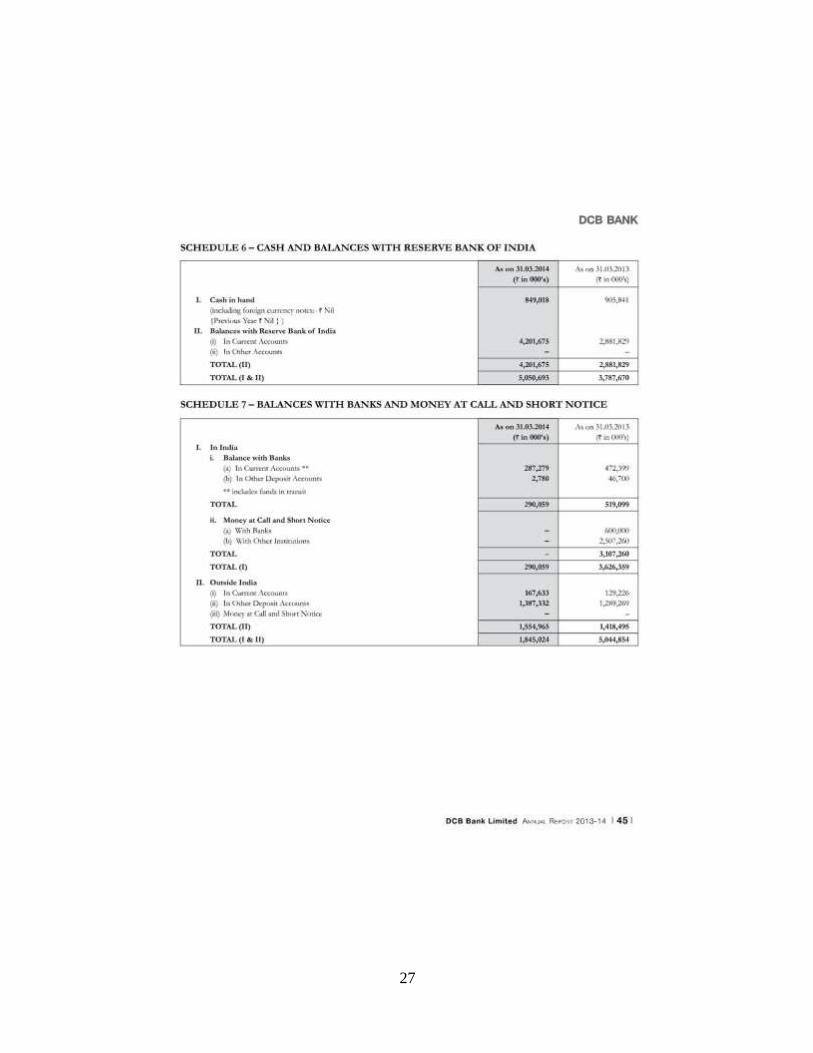

27

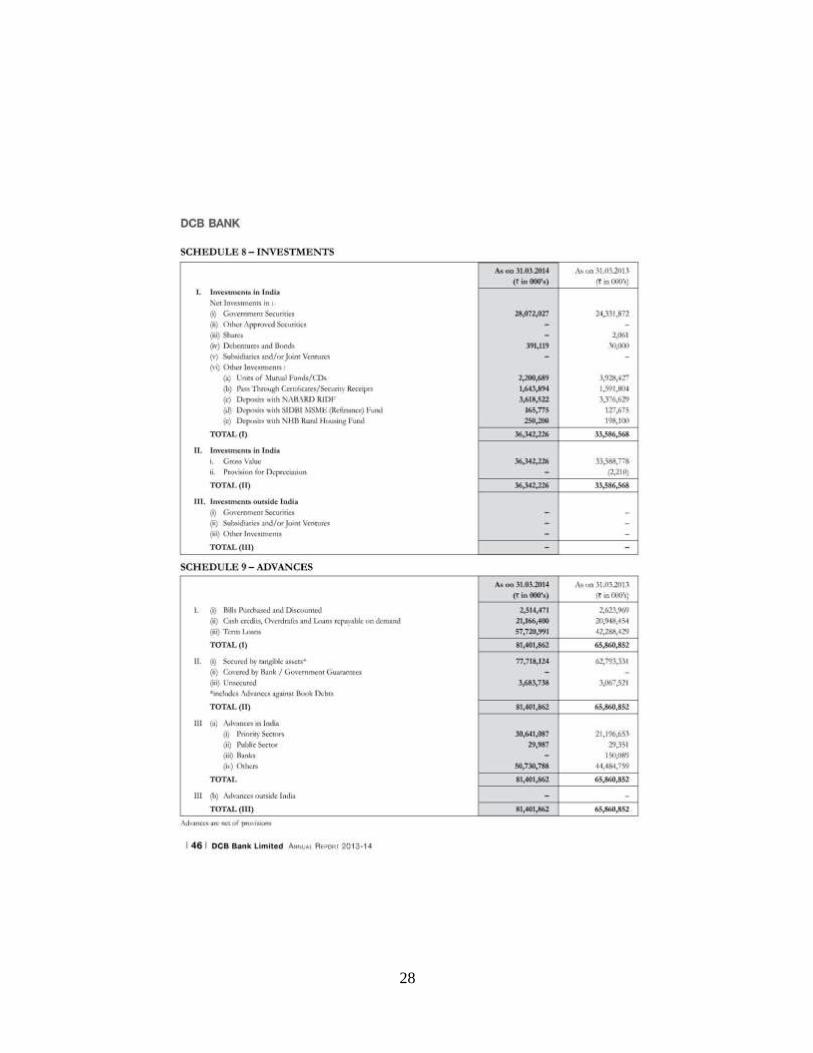

28

29

30

31

32

SCHEDULE 17 – SIGNIFICANT ACCOUNTING POLICIES

1. BACKGROUND

DCB Bank Limited (“DCB” or “the Bank”), incorporated in Mumbai, India is a

publicly held banking company engaged in providing banking

and fi nancial services. DCB is a banking company governed by the Banking

Regulation Act, 1949.

Pursuant to the approval received from the Registrar of Companies, Maharashtra

-Mumbai and from the Reserve Bank of India (‘RBI’) vide

their letter no. DBOD.No.Ret.BC/ 83 /12.06.097/2013-14 dated 10 January, 2014

the Bank has changed its name from Development Credit

Bank Limited to ‘DCB Bank Limited’ with effect from 24 October, 2013.

2. BASIS OF PREPARATION

The fi nancial statements have been prepared and presented under the historical

cost convention on the accrual basis of accounting, and comply

with the Generally Accepted Accounting Principles in India (‘GAAP’), statutory

requirements prescribed under the Banking Regulation Act,

1949, circulars and guidelines issued by the RBI from time to time and the notifi

ed Accounting Standards under the Companies (Accounting

Standards) Rules, 2006, (as amended) to the extent applicable and the current

practices prevailing within the banking industry in India.

3. USE OF ESTIMATES

The preparation of the fi nancial statements in conformity with GAAP requires

the management to make estimates and assumptions that affect the reported

amounts of assets and liabilities and disclosure of contingent liabilities at the date

of the fi nancial statements and the results of operations during the reporting

period.Although these estimates are based upon the management’s best

33

knowledge of current events and actions, actual results could differ from these

estimates. Any revisions to the accounting estimates are recognised prospectively

in the current and future periods.

4. INVESTMENTS

4.1 Classifi cation:

The investment portfolio comprising approved securities (predominantly

Government Securities) and other securities (Shares, Debentures and Bonds, etc.)

are classifi ed at the time of acquisition in accordance with the RBI guidelines

under three categories viz. ‘Held to Maturity’ (‘HTM’), ‘Available for Sale’

(‘AFS’) and ‘Held for Trading’ (‘HFT’). For the purposes of disclosure in the

Balance Sheet, they are classifi ed under six groups viz. Government Securities,

Other Approved Securities, Shares, Debentures and Bonds, Subsidiaries and/or

joint ventures and Other Investments. The Bank follows ‘Settlement Date’

accounting for recording purchase and sale transactions.

4.2 Basis of Classifi cation:

Investments that are held principally for resale within 90 days from the date of

purchase are classifi ed as HFT securities. As per the RBI guidelines, HFT

securities, which remain unsold for a period of 90 days are reclassifi ed as AFS

securities as on that date. Investments which the Bank intends to hold till maturity

are classifi ed as HTM securities. Investments which are not classifi ed in the

above categories are classifi ed under AFS category.

4.3 Transfer of Securities between Categories:

The transfer/shifting of securities between categories of investments is accounted

as per the RBI guidelines.

4.4 Valuation:

Held for Trading and Available for Sale categories: Investments classifi ed under

HFT and AFS are marked to market as per the RBI guidelines. These securities

are valued scrip-wise and any resultant depreciation or appreciation is aggregated

for each category. The net depreciation for each category is provided for, whereas

the net appreciation for each category is ignored. The book value of individual

34

securities is not changed consequent to periodic valuation of investments. Traded

investments are valued based on the trades / quotes from the recognised stock

exchanges, price list of RRBI guidelines, HFT securities, which remain unsold for

a period of 90 days are reclassifi ed as AFS securities as on that date. Investments

which the Bank intends to hold till maturity are classifi ed as HTM securities.

Investments which are not classifi ed in the above categories are classifi ed under

AFS category.

4.3 Transfer of Securities between Categories:

The transfer/shifting of securities between categories of investments is accounted

as per the RBI guidelines.

4.4 Valuation:

Held for Trading and Available for Sale categories: Investments classifi ed under

HFT and AFS are marked to market as per the RBI guidelines. These securities

are valued scrip-wise and any resultant depreciation or appreciation is aggregated

for each category. The net depreciation for each category is provided for, whereas

the net appreciation for each category is ignored. The book value of individual

securities is not changed consequent to periodic valuation of investments.

Traded investments are valued based on the trades / quotes from the recognised

stock exchanges, price list of RBI or prices declared by Primary Dealers

Association of India (‘PDAI’) jointly with Fixed Income Money Market and

Derivatives Association (‘FIMMDA’), periodically. The market value of

unquoted government securities which qualify for determining the Statutory

Liquidity Ratio (‘SLR’) included in the AFS and HFT categories is computed as

per the Yield-to-Maturity (‘YTM’) rates published by FIMMDA.The valuation of

other unquoted fi xed income securities (viz. State government securities, Other

approved securities, Bonds and debentures) wherever linked to the YTM rates, is

computed with a mark-up (refl ecting associated credit and liquidity risk) over the

YTM rates for government securities with similar maturity profi le published by

FIMMDA. Unquoted equity shares are valued at the break-up value, if the latest

Balance Sheet is available or at `1 as per the RBI guidelines. Units of mutual

funds are valued at the latest repurchase price / net asset value declared by the

mutual fund. Treasury bills, commercial papers and certifi cate of deposits, being

discounted instruments, are valued at carrying cost.DC.

35

36

37

Conclusion:

DCB banks should adapt themselves quickly to the changing norms. The system

is getting internationally standardized with the coming of BASELL II accords

sothe DCB bank and Indian banks should strengthen internal processes so as to

cope withthe standards.

DCB bank should maintain a 0% NPA by always lending and investing or

creating qualityassets which earn returns by way of interest and profits. DCB

bank should find more avenues to hedge risks as the market is very sensitive to

risk of any type. Have good appraisal skills, system, and proper follow up to

ensure that DCB bank is above the risk. And DCB bank should always tries to

keep their customers aways from risk.

38

Bibliography:

http://useconomy.about.com/od/glossary/g/Banking.htm

http://www.thefreedictionary.com/banking+company

http://bankinglaw.uslegal.com/

http://indiankanoon.org/doc/1817338/

http://indiankanoon.org/doc/1817338/

http://www.dcbbank.com/

ww.rupeetimes.com/banks/development_credit_bank_ltd.html

http://economictimes.indiatimes.com/development-credit-bank-

ltd/infocompanyhistory/companyid-4940.cms

http://www.dcbbank.com/about/financials.html.