Embed Size (px)

Citation preview

THE SYSTEM OF ACCOUNTING

Volume III

WRITTEN BY:

SYED AQEEL RAZA MASTER OF COMMERCE & POLITICS

PURCHASES 1

ACCOUNTING FOR PURCHASES

The purchase is the result of exchanging values for material and work by means of money or its equivalent for the satisfaction of need and for generating profit in business by the process of purchasing and selling. There are three types of businesses involve purchases and sells as in trading business, the person purchases goods and sells it in anticipation of gain, in manufacturing business, the concern purchases materials, gives it any shape and sells and in services business which has no purchase apparently but actually the services which are given to service provider are the purchases for which the concern who does purchase the services pays money to service provider.

The purchases for business is considered a kind of temporary asset involve in profit and loss under income statement. It may also be said a kind of expense because of purchasing for goods or expense for goods involves in the cost of goods sold and can also say it the helping tool for generating profit.

Purchase plays an important role in accounting. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 2

The purchase is debited to purchase account which increases in expense or temporary asset and cash does credit to a cash account which decreases the assets of an entity.

There may be following three kinds of purchasing in accounting;

1- PURCHASE FOR PERSONAL 2- PURCHASE FOR BUSINESS 3- PURCHASE FOR EXPENSES

PURCHASE FOR PERSONAL

No purchase is allowed in business for personal use and if the proprietor does purchase something or takes anything from the purchased goods, he will be withdrawing his capital or goods at value.

If the owner or partner draw cash, the drawing is debited to drawing account; drawing is a contra capital account; and cash is credited which is a current asset and asset is decreasing as;

Purchase moves accounting cycle. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 3

Drawing (Cash)/debit Cash (credit)/asset In case of drawing goods by owner, the drawing reduces merchandise at the value to Inventory account. Drawing (Stock) /debit Inventory (credit) At the end of the period or in balance sheet the drawing account is reduced by owner’s equity or capital account as; Capital (Cash)/debit Drawing (Cash)/credit Capital (Stock)/debit Drawing (Inventory/Credit

No purchase is allowed in business for personal use.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 4

PURCHASES FOR BUSINESS:

- Merchandise for trading - Materials for manufacturing - Assets for business - Work against services - Direct purchases - Goods Receipt Note (GRN) - Debit Note - Account payable aging

Merchandise for Trading In trading business, merchandise is purchased for sale against profit. The trading business involves a person or persons who buy products and sell to customer and links with manufacturers and service providers.

Materials for manufacturing

The manufacturing business deals with materials wherein manufacturer does purchases materials for making goods which he wants to make something and then sells to traders, whole sellers and also to retailers. The manufacturing business requires manpower which is provided by services business in the shape of employees. Thus, manufacturing business needs the help of trading and services. It also requires land, building, plant and machinery for operation.

The purchase is made for sale against profit. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 5

Assets for business

In order to operate any business, assets are purchased like land, building, plant, machinery, furniture, office equipment, air conditioners, etc. etc. The depreciation does contra to the most of the assets.

Direct Expenses

Most of the purchases involve in cartage wages, labor, customs duty, octroi, taxes etc. are the direct expenses which we can say that the direct purchase is because of adding in the price of goods purchased and add in the purchase in the income statement.

Work against services

The plant, machinery, furniture, office equipment or any asset requires services for installation, inspection, fixing and like these works the services are purchased for the time being and the cost includes in the asset purchased. It does not belong to profit and loss but become the part of the asset.

Direct expenses are involved in business purchase.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 6

PURCHASES FOR EXPENSES

Actually, the expenses which are paid for operating business activities decrease income or increase loss than in other words we can say that the expenses belong to profit and loss as low expense high profit or high expense low income.

The purchases are made for operating business activities as to works and goods, reduce income and do not belong to merchandise.

TYPES OF PURCHSAES

All purchases revolve around cash purchases and credit purchases and any purchase can be made in cash or on credit. - Cash Purchases - Credit Purchases

The purchase against expense is the part of income.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 7

Cash Purchases The cash purchase is the purchase which is made on payment against getting anything on the spot or exchange of value on the spot.

When a cash purchase is made, the following double entry is made; Purchases (Debit/Income Statement) Cash (Credit/Asset)

The purchase is debited to purchase account which belongs to the cost of goods sold and cash is credited to cash account decreases assets of an entity.

Credit Purchase

Credit purchase is the purchase which is made later under an agreement or mutual understanding of seller and purchaser. Like this purchase, goods are obtained without paying cash and cash is paid later.

Cash purchase orders payments on the spot but credit on later. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 8

The credit purchase is the liability of purchaser and asset of seller when it made, the following double entry is made;

Purchase (Debit)/Income Statement Account Payable (Credit) Liability When the liability is paid, the balance in payable account will be reduced and to zero as; Account payable (Debit)/Liability Cash (Credit)/Asset

The result of purchase is to increase in purchase account or expense account and decrease in an asset of the entity. A purchase also results in the increase of inventory requires further discussion.

The result of purchase is to pay money. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 9

THE PROCEDURE OF PURCHASING AND RECORDING

The following documents or formats for purchasing and maintaining purchases are simply made depend on the nature of purchase;

- Purchase Requisition - Indent - Requisition - Job Order - Purchase Order - Delivery Order - Goods Receipt Note (GRN) - Debit Note - Account Payable Aging The formats work like ladder to support recording the system of accounting The formats are designed to reach the desired result and the desired to reach the balance of quantity and cost of the item which identified in summary of stock.

The purchase requires a procedure to control it. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 10

PURCHASE REQUISITION In case of having no store for consumable items, the purchases for departments are made by purchase requisition and the purchase requisition is the document which is prepared before purchasing of anything either on cash or on credit. It is an internal document which is made by the person who wants to require the item for his department and sends it to purchase manager. The purchase manager submits it to chief executive officer for approval and on approval; he arranges to buy the items required. The purchase requisition may contain serial number, description, quantity and cost approximately which is prepared by the person who wants to require the item or items for machinery, repair, maintenance, etc. for department and sends it to purchase department duly signed by the departmental head. The Purchase requisition will be checked by purchase department. The purchase department also ascertains the cost of the item or items approximately and submits gets it approved for purchase.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 11

The purchase requisition is designed below or may be designed according to the requirement;

The Purchase requisition is an order to purchase in cash. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 12

INDENT Indent means to ask for consumable items useable in office like printing, stationery, and general items. It will be required in case of having a store for these items. The indent for issuing consumable items may be specified below;

Indent means to ask for consumable items. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 13

REQUISITION The requisition may relate to production which requires raw materials, packing materials and plant, machinery and building require repair and maintenance. The requisition may be designed as;

Requisition relates items required for production and building use.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 14

JOB ORDER

Job order is a written instruction to provide a particular goods or services in order to perform a work according to specified requirements, time frame, and cost estimates. Generally, the Job order relates to services business and for manufacturing business wherein services or goods required. The following kinds of formats for job order or work order may be made; - Material issue for production - Acquiring services from customer - Issuing materials to engineers for outside clients;

It is also known as a work order form. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 15

Material issue order form;

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 16

Job order for acquiring services from customer;

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 17

PURCHASE ORDER:

The purchase order is an agreement between purchaser and seller and states that the purchaser indents to purchase goods and confirm the legal identity of the purchaser. It also helps in comparison with purchase invoice because of having column quantity, description, unit price and the value of goods. The deduction of sales tax or any other instruction is known by purchase order. The purchase order is placed to buy goods on credit subject to the delivery order. Purchase order means the agreement of purchase.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 19

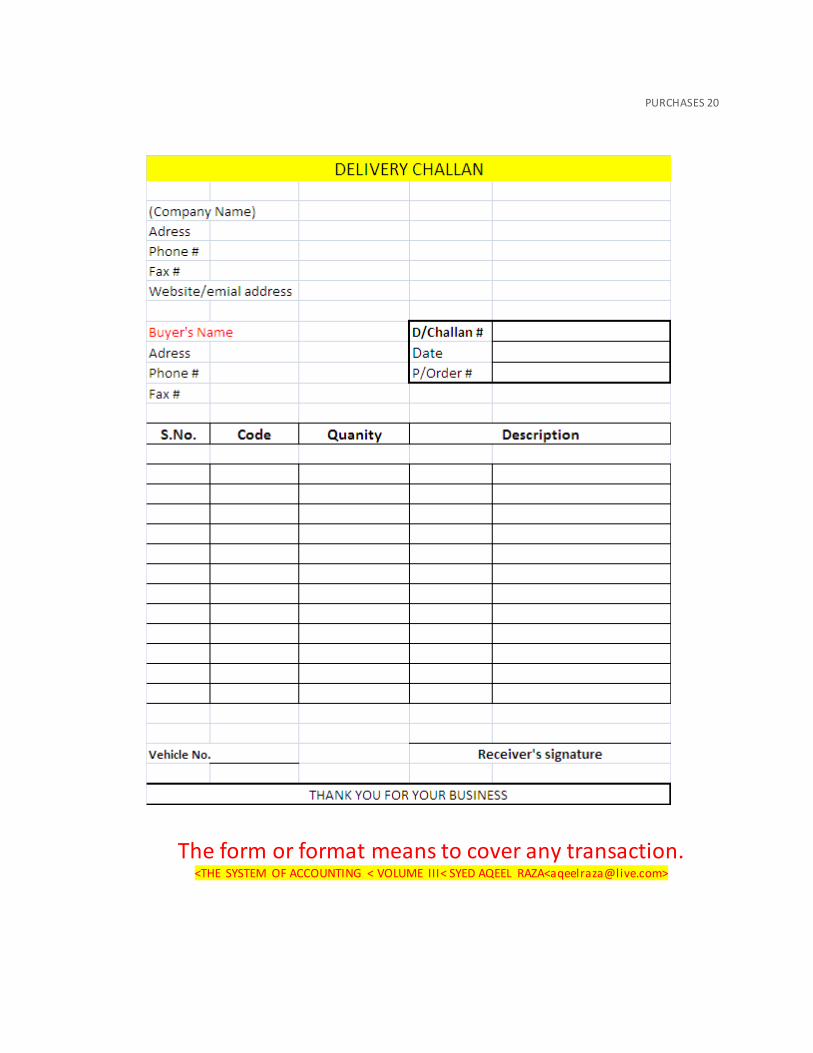

DELIVERY ORDER

The delivery order is a document which confirms the delivery of goods as per purchase order. It requires the receiving and checking of goods by the purchaser. The seller sends invoice, copy of purchase order and delivery challan duly checked and received by the purchaser.

Delivery order confirms the receipt goods ordered. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 20

The form or format means to cover any transaction. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 21

GOODS RECEIVED NOTE (GRN)

The Goods Received Note (GRN) indicates that the goods which were ordered have been received by the purchaser. On receiving the goods, the purchaser does a signature on Goods Received Note as a receipt of goods. The goods received note contains serial number, description of goods, pack size, price, ordered quantity, delivered quantity, and remarks. This document is very important for payment of invoice which confirms the transaction.

The goods receipt note works like delivery order. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 22

The form or format is made according to requirement.

<THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 23

DEBIT NOTE

If any defect in commodities is found, the purchaser will inform the supplier for deduction of the amount payable by debit memorandum. If the supplier accepts the request, he will issue a credit memorandum for the deduction of amount receivable.

The debit memorandum reduces the liability to vendor and credit memorandum reduces accounts receivable to the vendor.

Debit note is issued for deduction against the claim. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 24

ACCOUNT PAYABLE AGING Account payable aging is made to pay the amount which is payable to supplier against purchase on credit under the agreement of time for payment.

Account payable aging controls payments payable. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 25

KIND OF STORES

There may be required many kinds of stores in businesses dealing with materials or goods relating to trading and producing. The manufacturing business has wide expansion involves in materials and finished goods so that; it must have stores for consumable and materials in finished and unfinished forms when the trading business must have Store for trading goods. 1 - Consumable Store - Stationery - Machinery, Building Materials

2- Production Materials

- Materials - Finished goods

Goods require stores. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 26

CONSUMABLE STORES In case of having Store for consumable items, it must require stores where all general items relating to building, plant and machinery, office equipment and others in store 1 and stationery or office supplies in store 2 must be maintained. It depends on the volume of business. The benefit of maintaining stores for consumable is to save time and money because of purchasing small items in need requires person to purchase it, the person require time and money, and time and money can be wasted for in shape of conveyance and purchase from retailers for tiny items and time which can be utilized in other works. Besides time and money, the risk of handling cash is minimized. In order to purchase for stores, the purchase will be made in cash or credit from whole sellers against cheques instead of cash.

The items are of daily use in business come under consumable store. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 27

The purchase order and delivery order may be used for consumable stores in case of purchasing items on credit as they are mostly used for purchasing goods for business on credit. STORE I In case of maintaining store for general items relating to plant, machinery, office equipment and building, the procedure of keeping record must be considered.

STORE II

The office supplies and stationery are frequently used in business communication and maintaining records. The store for office supplies can be maintained which saves time, money and risk of cash.

The stores depend on the nature of business. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 28

MAINTAINING OF BUSINESS STOCK

In order to maintain stock of any kind either of consumable or of business, a device is required to

Stock register

The stock register

- Consumable items - Business stock

1- Trading 2- Manufacturing 3- Services

CONSUMABLE ITEMS

The stock register which contains pages of every item could work like ledger is required to control consumable items store one and store two which I have designed below. The format is designed to reach the desired result and the desired for them is a balance of quantity and cost of the item which identified in summary of stock.

The business stock must have store and recording. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 29

The designing of format is to focus the transaction. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 30

PURCHASES 31

The stock register controls stock received and issued. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 32

The summary of stock register facilitates in making cost of goods sold statement.

The result of stock is a summary of stock. <THE SYSTEM OF ACCOUNTING < VOLUME III< SYED AQEEL RAZA<[email protected]>

PURCHASES 33

WRITER’S VIEW

The purchase involves transactions and transaction is made through payment on cash on the spot or on later. As soon as the purchase occurs, the accounting cycle starts. The purchase relates to the cost of goods which is made after passing through many processes of purchasing. The profit or loss is generated by sale and purchase and purchase is the part of profit and loss. In the services business, the purchase is the service of a person acquired for completing the job just like employees, repairers etc.

The stock maintaining is because of purchasing.

Then we can say the purchase pays an important role in accounting because of which no concept of sale is created and the stock maintaining is because of purchasing.

WRITTEN BY:

SYED AQEEL RAZA MASTER OF COMMERCE & POLITICS