Embed Size (px)

Citation preview

Sri Lanka’s controversial bond issue: ethics, judgement and governance in financial services

Fresh look at bond saga in Sri Lanka - Strategist 27/07/2015

The purpose

This presentation is an attempt to shed light on the potential dark side of a recent bond issue in Sri Lanka. While relying on secondary information we also review some “unusual” events that have taken place. Like in many other countries regulators in Sri Lanka cannot make an absolutely safe environment for financial services. Financial services sector in general and central banking in particular depend on, to a large extent, on ethics, judgement and morals of participants. Here we look at whether it is the system or the responsible persons have failed.

Background

A recent government bond issue by the Central Bank of Sri Lanka has become a key discussion topic in Sri Lanka and overseas. The issue appears to have the hallmarks of mismanagement at best and fraud at worst. Many academics and professionals have participated in the discussion. The estimated accounting loss is estimated at Rs 6 billion. However, most of the analysts have not taken into account the resultant reputational damage and likely negative impact on future bond issues and economy in general.

Sri Lanka’s controversial bond issue in perspective

SL’s controversial bond issue is almost unprecedented

When a central banker had come under scrutiny governments have acted swiftly to remove or suspend them

Sri Lanka was slow to act Nigeria’s Central Bank governor was

suspended by the president for financial irregularities. Stern action was taken.

http://www.bbc.com/news/world-africa-26270561

Governance and compliance

There seems to be governance issues at high level Communication of facts has failed and/or facts

were communicated but ignored by the policymakers and lawmakers

Processes and procedures may not have been the best but they were sufficient

Real issue appears to be the failure to comply with existing processes and procedures

Lawmakers were at best slow to react and at worst covering up

Wrong start - political appointee not a central banker Appointment of a foreign citizen – unusual move Candidate with commercial experience but very

little central banking experience at senior level Candidate was not aware of the procedures of the

Central Bank Knowledge and skill of monetary policy setting was

also questionable. Consideration was not given to internal candidates Politics was a hindrance to rational thinking and

decision making Recruitment and appointment process was flawed

Triple “mistakes” – Volume, Price, Duration

Importance of metrics ignored - one cannot manage what one cannot measure

Volume: before purchase one needs to know how much to purchase. This should have been documented. It is the policy of any treasury operation. Transparency was lacking.

Communication of the volume is paramount to market efficiency – foundation of financial markets.

It appears reasonable effort was not made to communicate the volume needed in an impartial manner

Triple “mistakes” – Volume, Price, Duration

It appears that some of the participants were aware of the volume. This disadvantaged the other participants

Bank staff have raised this issue

Once again market efficiency was compromised

Determining price - know thy price

Trading price or price range should be realistic

It should be meaningful relative to the prevailing market conditions

Efficient markets should deliver efficient prices

Extreme price volatility is a sign of market distortions

Up to 300 b.p. (basis points) above the market is an unacceptable variation

Price does not reflect the prevailing interest rate structure. Global interest rates are stable.

Determining price – market efficiency Market distortion created by “unlimited information

to limited number of participants” created a privileged position for some

Arms length rule was not followed Prudent person rule was violated Relationship between the governor and a

participant was not disclosed Related party transaction gives rise to insider

trading claims which in turn is a serious offence Punishment for insider trading is a prison sentence

in many countries

Determining price – use of available information

Price is relative to the prevailing environment

Prevailing environment should have been analysed using available information

Dealing and research teams had the required information

Did decision makers “intentionally” ignore the information and recommendations?

In a well-developed central banking system why was the communication so poor between the governor and his advisors? Was advice ignored?

Duration – transparent information

Duration is basic information that any treasury manager should know

Duration of the portfolio should have been analysed and discussed in debt management strategy meetings

Yield curve – relationship between interest rates and time to maturity of the bonds – should have been available in documents and on computer screens (or even mobile phones)

Given the published information available better decisions on duration could have been made.

Duration – internal strategy ignored?

Required information was available

Duration was clear

Current interest structure and expectations were reasonably clear – global interest rates were unlikely to increase sharply

Shorter duration bonds would have been more appropriate to the requirements

Available information has not been taken into account

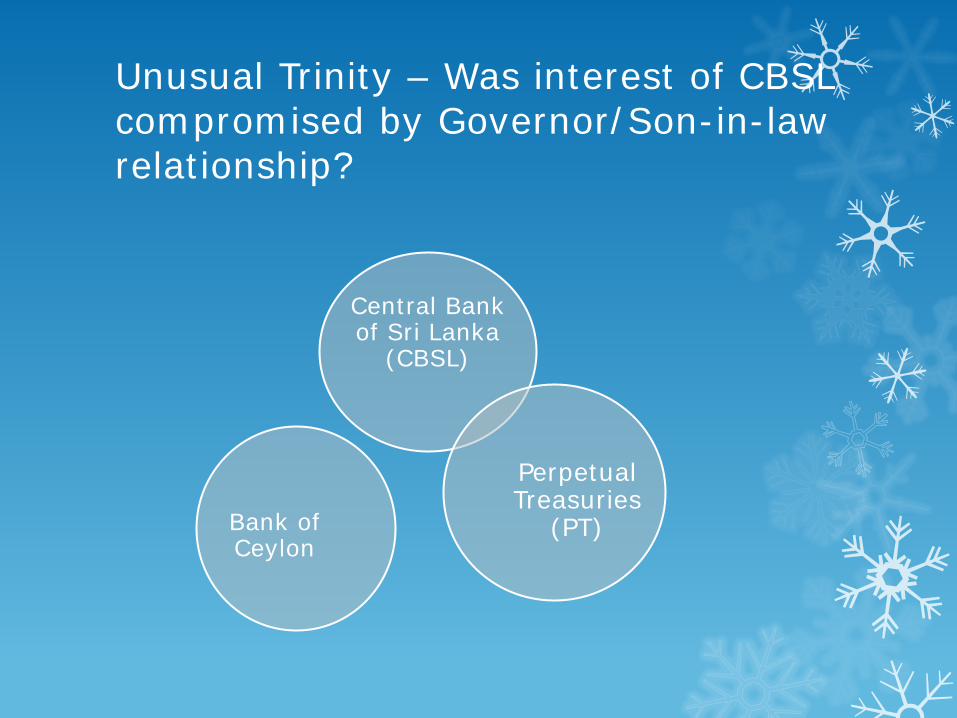

Unusual Trinity – Was interest of CBSL compromised by Governor/Son-in-law relationship?

Central Bank of Sri Lanka

(CBSL)

Perpetual Treasuries

(PT) Bank of Ceylon

Triple failures

Failure 1: Related party was not disclosed

Failure 2: Unusual related party transaction was not disclosed giving rise to an insider trading claim

Failure 3: Expert advice ignored

Dealer (PT) using another dealer (BOC)

One cannot help but question this relationship

Perpetual Trustees used another dealer

An “unusual” move

Why did a state-owned bank (BOC) act as a dealer to a dealer(PT)?

Slow response from regulators

Regulators’ response has been slow

Only after extreme pressure from the lawmakers the Prime Minister agreed to a parliamentary enquiry

It is reasonable to assume that “political obstacles” forced regulators go slow.

President the Whistleblower

President identified the problem

Some may argue that the President of Sri Lanka does not possess the required knowledge without giving credit to his senior advisors

Common procedure is for the CB Governor to step down.

Failure to do so created further interest on this controversial bond issue

Did the President stop short of his duty by the country?

Nigeria’s President Goodluck Jonathan suspended the Central Bank governor for “financial recklessness” and “far-reaching irregularities”

http://www.ft.com/cms/s/0/9c09b882-9a18-11e3-a407-00144feab7de.html#axzz3hK7ZGemd

http://www.economist.com/blogs/baobab/2014/02/trouble-nigerias-central-bank

Should Sri Lanka also follow Nigerian example?

President’s inaction is unexplained to the market

Unprecedented damage is underestimated

There are estimates of Rs. 6000 millions of damage

These estimates do not take into account the reputational damage and resultant increase in interest rates for future issues

Also they do not take into account cost of high interest to the wider economy and resultant drag on the economy as a whole