Embed Size (px)

Citation preview

Greek Market Update

October 16, 2015

2

Greek Equity Research October 16, 2015

Greek Market Update

Natasha Roumantzi Tel: +30 210 335 4065 Email: [email protected] George Doukas Tel: +30 210335 4093 Email: [email protected] Iakovos Kourtesis Tel: +30 210335 4083 Email: [email protected]

3

Key Investment Considerations

We reiterate our Top Pick list, which includes OPAP and Motor Oil. These two stocks have outperformed the market since our last strategy report of early-September. MOH enjoys a favorable benchmark margin environment, as well as favorable FX dynamics. MOH’s possible inflow from the revision of the MSCI index could also boost further the stock. OPAP should witness the successful launch of VLTs sometime in 2016, which will further diversify OPAP’s gaming portfolio.

Apart from Motor Oil and OPAP, we have Outperform ratings on Aegean Airlines, Frigoglass, FFGROUP, Jumbo, Fourlis and Athex.

We trim our target price on Jumbo to EUR 9.80 from EUR 10.0 and reiterate Outperform rating.

We downgrade CCHBC to Underperform from Neutral on valuation grounds. We think current price levels imply stretched valuation metrics. Recent sugar price spikes should inflate the cost base in the mid term, while we are cautious on the recovery of EE markets and particularly Russia. We would therefore sell the stock at current price levels.

The valuation of our non-banks universe implies an upside potential of 5.9% from 14.5% previously. We think that the market will need the contribution of the banking sector in order to move meaningfully higher.

Upside risks to our valuation include a) further decline of GGB rates as a result of positive programme review (within November), political stability and debt relief measures; b) better than currently anticipated economy dynamics with key catalyst being the privatization programme (i.e. regional airports, ports, Hellinikon and energy market) and efficient absorption of EU funds; and c) successful conclusion of banks’ recap accompanied by the formulation of an effective legal framework for the management of NPLs.

In the banking space, the pressure continued unabated in the last month, putting pressure in the wider market. The banking index plunged by 22.1% from September 10, when we released our latest strategy report, until October 14. In terms of newsflow, the management teams of the four systemic banks met with ECB/SSM in Frankfurt on October 14-15 in order to receive preliminary and partial data on the comprehensive assessment exercise. The regulatory framework that will detail the recap terms is expected to be submitted to Parliament by October 20. The final recap amount should have been formulated by October 20 and the official announcement is expected on October 31-November 1. In the context of the recapitalization project, Piraeus Bank announced LME on its junior and senior debt, while other banks are expected to follow. The capital increases should start in November and be concluded prior to end-2015.

4

4Q 2015 milestones that could affect Greek assets

31 Oct./1 Nov.: AQR and Stress test results are expected to be officially released

Mid-October: Expected start of 1st Review of 3rd bailout programme

9 November: Eurogroup23 November: Eurogroup

20 October: regulatory framework of bank's recaps to be submitted to Parliament

13 November: Fitch sovereign rating assessment 20 November: Moody's

sovereign rating assessment

8 December : Eurogroup

23 December: Eurogroup

End-December: conclusion of bank recaps

4Q 2015 timetable of events

15 November : Deadline for the release of additional EUR 15bn recap funds

November-December: Recapitalization process under way

Greek Sovereign/Corporate Events | 4Q 2015

29 October Railway bond due EUR 174mn

31 October Banks: Deadline for the release of 1H 2015 results

1-30 November Q3 reporting season

1 November PPC (PPC GA)bond coupon payment

6 November T-Bills redemption; EUR 1.4bn

10 November Hellenic Petroleum (ELPE GA) bond coupon payment

13 November T-Bills redemption; EUR 1.4bn

15 November Frigoglass (FRIGO GA), Intralot (INLOT GA) &

Motor Oil (MOH GA)bond coupon payments

16 November Coca Cola HBC (CCH LN) bond coupon payment

7 December IMF loan due EUR 279mn

11 December T-Bills redemption; EUR 2.0bn

16 December IMF loan due EUR 509mn

18 December T-Bills redemption; EUR 1.6bn

21 December IMF loan due EUR 313mn

5

ATHEX moved into positive territory since our last strategy report on the back of strong performance by non financials, which have massively outperformed banks. On a y-t-d basis the Greek equity market remains an underperformer compared to its European peers.

ATHEX turns positive Month-on-Month

0

20

40

60

80

100

120

140Greek large caps vs Greek banks 2015 y-t-d (indexed)

Greek Large caps (ex-banks) Greek Banks

ATHEX reopens Capital controls ATHEX ceases trading

Elections

4.6% 4.7%

1.9% 1.7%

-1.2%

0.8% 2.2%

4.6%

-3.0% -5.00%

-3.00%

-1.00%

1.00%

3.00%

5.00%

7.00%

9.00%

11.00%

13.00%

15.00%

GreeceATHEX

Composite

MSCI EM(EmergingMarkets)

FranceCAC 40

FTSE MIB GermanyDAX (TR)

STOXXEurope

600

Spain IBEX35

PortugalPSI 20

IrelandISEQ

General

ATHEX vs peers October/September 2015

-18.16%

-6.02%

7.87%

14.87%

1.12% 3.87%

-2.35%

10.18%

18.84%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

GreeceATHEX

Composite

MSCI EM(EmergingMarkets)

FranceCAC 40

FTSE MIB GermanyDAX (TR)

STOXXEurope

600

Spain IBEX35

PortugalPSI 20

IrelandISEQ

General

ATHEX vs peers y-t-d

6

…still though lagging GGBs

Greek sovereign debt has outperformed the equity market since the restart of the ATHEX in early August. 10Y GGB currently trades at 7.8%, a level last printed in December last year, when Greek equities were trading 20-52% higher. Note that GGBs were trading at a YTM of 11.7% in early August and slightly above 8% at the time of the elections. The Greek equity market on the other hand is trading close to 3Y lows.

7.00

7.50

8.00

8.50

9.00

9.50

10.00

10.50

11.00

11.50

12.00

550

570

590

610

630

650

670

690

710

730

ATHEX GI vs 10Y GGB Yield since the restart of the Greek Equity Market

ATHEX GI - Left axis 10Y GGB yield - Right axis

Elections

7

Breaking the link between debt and equity

It is the first time in the last 5 years that a compression in yields is not combined with a rise in the Greek equity market. The reason is the plunge in banking valuation in the wake of the capital controls and the forthcoming recapitalizations.

GGB & ATHEX swings | start 2008-now

time length (months) GGB yield

change ATHEX GI performance ATHEX ex-banks performace -

average per month spot P/E total

market ex banks

4 26.7% -14.8% -17.3% 13.2

4 -13.0% -29.4% -37.1% 9.8

3 34.1% -37.0% -9.2% 6.9

12 -9.8% 32.1% 9.5% 9.8

26 490.0% -65.9% -53.2% 7.2

30 -83.3% 60.0% 72.7% 20.7

8 93.5% -33.3% -22.1% 11.8

2 -28.7% -14.8% -0.4% 14.7

8

Top down, the Greek market does not seem to be attractive

5 10 15 20 25 30

US

Japan

Developed Markets

Australia

Asia ex Japan

Europe ex UK

EM

UK

Emerging Europe

Greece

Schiller P/E: Greek market vs peers*

01020304050

US

Japan

Developed Markets

Australia

Asia ex Japan

Europe ex UK

EM

UK

CEEMEA

Greece

Median Historical Schiller P/E: Greek market vs peers*

*Greek Schiller P/E does not include financials

9

Our non financial universe has derated substantially in 2015 and especially over the summer. Right now 12M fwd P/E stands c11% below the end-2014 print, which means that the market has already incorporated some EPS downgrades.

Much better picture for our non-financials universe #1

0

5

10

15

20

25

1/3

1/20

00

7/3

1/20

00

1/3

1/20

01

7/3

1/20

01

1/3

1/20

02

7/3

1/20

02

1/3

1/20

03

7/3

1/20

03

1/3

0/20

04

7/3

0/20

04

1/3

1/20

05

7/2

9/20

05

1/3

1/20

06

7/3

1/20

06

1/3

1/20

07

7/3

1/20

07

1/3

1/20

08

7/3

1/20

08

1/3

0/20

09

7/3

1/20

09

1/2

9/20

10

7/3

0/20

10

1/3

1/20

11

7/2

9/20

11

1/3

1/20

12

7/3

1/20

12

1/3

1/20

13

7/3

1/20

13

1/3

1/20

14

7/3

1/20

14

1/3

0/20

15

7/3

1/20

15

12m Fwd P/E- PS non financials universe

0

2

4

6

8

10

12

2/2

9/2

000

8/3

1/2

000

2/2

8/2

001

8/3

1/2

001

2/2

8/2

002

8/3

0/2

002

2/2

8/2

003

8/2

9/2

003

2/2

7/2

004

8/3

1/2

004

2/2

8/2

005

8/3

1/2

005

2/2

8/2

006

8/3

1/2

006

2/2

8/2

007

8/3

1/2

007

2/2

9/2

008

8/2

9/2

008

2/2

7/2

009

8/3

1/2

009

2/2

6/2

010

8/3

1/2

010

2/2

8/2

011

8/3

1/2

011

2/2

9/2

012

8/3

1/2

012

2/2

8/2

013

8/3

0/2

013

2/2

8/2

014

8/2

9/2

014

2/2

7/2

015

8/3

1/2

015

12M Fwd EV/EBITDA-PS non financials universe

10

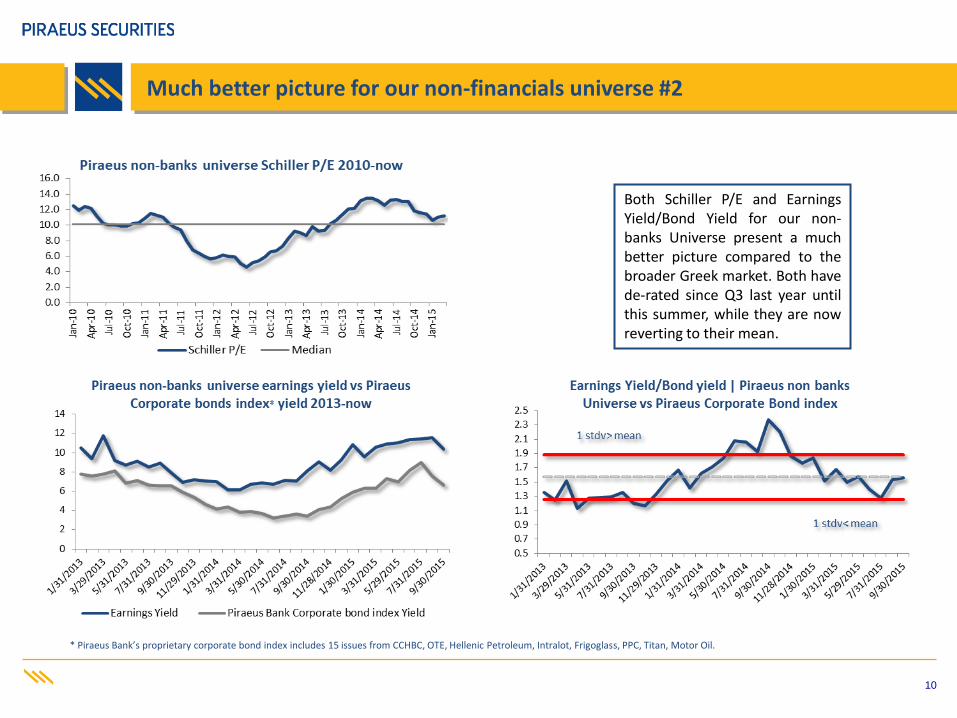

Both Schiller P/E and Earnings Yield/Bond Yield for our non-banks Universe present a much better picture compared to the broader Greek market. Both have de-rated since Q3 last year until this summer, while they are now reverting to their mean.

Much better picture for our non-financials universe #2

* Piraeus Bank’s proprietary corporate bond index includes 15 issues from CCHBC, OTE, Hellenic Petroleum, Intralot, Frigoglass, PPC, Titan, Motor Oil.

11

Our Non-Banks Universe has outperformed MoM

Our two top picks, Motor Oil and Opap are up 14.3% and 15% respectively since our last strategy report. FFGROUP is the outlier here, having a negative performance over the same period due to concerns about the Chinese economic dynamics.

12

Piraeus Securities Universe valuation (non-financials)

current price (COB

15-Oct-2015) Market cap. PT number of

shares Target Market

cap.

Total Expected

return

Aegean 7.25 517.8 7.80 71.4 557.1 13.2%

ATHEX 5.18 338.6 5.70 65.4 372.6 18.7%

Autohellas 10.55 128.3 10.00 12.2 121.6 1.4%

CCHBC 20.70 7,613.5 17.00 367.8 6,252.6 -16.0%

Frigoglass 2.23 112.8 3.00 50.6 151.8 34.5%

Fourlis 2.80 142.8 4.30 51.0 219.3 53.6%

FFGROUP 18.02 1,206.4 28.70 66.9 1,921.4 60.1%

Jumbo 8.27 1,125.2 9.80 136.1 1,333.4 21.0%

Motor Oil 10.30 1,141.1 12.00 110.8 1,329.4 25.7%

OTE 8.85 4,337.8 9.00 490.2 4,411.4 2.6%

OPAP 8.43 2,689.2 10.80 319.0 3,445.2 38.2%

PPC 5.17 1,199.4 4.00 232.0 928.0 -18.2%

Total (including dividend) 20,552.8 21,758.2 5.9%

Source: Piraeus Securities, Greek Equity Research

The total upside of our universe has been trimmed to 5.9%. We highlight two stocks that stand well above our current target prices. We think CCHBC (CCH LN) trades at stretched valuation metrics. Current price levels are not supported by fundamentals in our view, while we do not see positive developments in key markets like Russia or Italy that warrant a significant pick up in profitability. Moreover, the outlook for sugar is also negative. In this context we downgrade CCHBC to Underperform from Neutral. On the other hand, PPC (PPC GA) is a binary investment case in our view. We think that should the measures stipulated by the MoU regarding the liberalization of the electricity market are implemented, PPC will be able to crystalize some of its hidden value. However given there are many uncertainties we prefer to remain on the sidelines for the time being.

Our Non-Banks Universe offers an upside of 5.9%

13

Universe | PT and recommendation changes

We made some fine-tuning in our estimates in Jumbo (BELA GA) due to slightly worse outlook in the Greek operations. We therefore trimmed out valuation on the stock to EUR 9.80 from EUR 10.0 previously. We remain Buyers on the stock. From our Outperform list, we would also highlight Frigoglass (FRIGO GA) as our best bet to beat the market and our universe in the following weeks. The group is about to complete the sale of the glass business in Q4 and receive USD 200mn. This is of course an opportunistic call and dependent on the positive outcome of the sale, hence we refrain from giving the stock a top pick status. On Folli Follie (FFGRP GA) and despite the weakness y-t-d due to the Chinese softness, we could see a strong rebound in the case of positive newsflow on Chinese macros.

Piraeus Securities | Universe; changes in ratings and PTs

Target Price Old Target

Price Rating Previous

Rating Aegean 7.80 7.80 Outperform Outperform

Autohellas 10.00 10.00 Neutral Neutral

Coca Cola HLB AG 17.00 17.00 Underperform Neutral

Folli Follie Group 28.70 28.70 Outperform Outperform

Fourlis 4.30 4.30 Outperform Outperform

Frigoglass 3.00 3.00 Outperform Outperform

Hellenic Exchanges 5.70 5.70 Outperform Outperform

Jumbo 9.80 10.00 Outperform Outperform

Motor Oil* 12.00 12.00 Outperform Outperform

OPAP* 10.80 10.80 Outperform Outperform

OTE 9.00 9.00 Neutral Neutral

PPC 4.00 4.00 Neutral Neutral

Metka U/R U/R U/R U/R

NBG U/R U/R U/R U/R

Alpha Bank U/R U/R U/R U/R

Eurobank U/R U/R U/R U/R

Titan U/R U/R U/R U/R

Sarantis U/R U/R U/R U/R

* top picks

14

We lie below 2015 and 2016 consensus

We stand 6.8% and 1.9% below 2015 and 2016 consensus respectively although we see downside risks in 2016 estimates.

15

Appendix

16

Piraeus Securities Universe | statistics, financials, valuation

Prices as of COB, 15 October 2015

Reuters Last Daily Chg Target Mcap Ytd Perf Ytd Rel Div.Yield P/E P/BV EV/EBITDA

Outperform Code Price € (%) Price € T.Ε.R. € mn (%) (%) 2014 2015E 2014 2015E 2016E 2015E 2014 2015E 2016E

Aegean Airlines AGNr.AT 7.250 2.7% 7.80 13.2% 517.77 5.1% 25.0% 8.1% 5.7% 7.4x 8.8x 7.5x 3.0x 3.0x 3.9x 3.0x

Folli Follie Group HDFr.AT 18.020 0.6% 28.70 60.1% 1,206.41 -31.7% -18.8% 4.2% 0.8% 8.5x 8.1x 6.8x 0.8x 5.7x 5.4x 4.8x

Fourlis FRLr.AT 2.800 1.8% 4.30 53.6% 142.78 -13.0% 3.4% 0.0% 0.0% <0 <0 35.3x 0.9x 10.7x 9.0x 7.9x

Frigoglass FRIr.AT 2.230 -3.0% 3.00 34.5% 112.82 33.5% 58.9% 0.0% 0.0% <0 <0 52.7x 1.2x 13.5x 7.3x 6.0x

Hellenic Exchanges EXCr.AT 5.180 4.2% 5.70 10.0% 338.61 11.4% 32.5% 6.2% 8.7% 18.4x 31.6x 24.0x 1.7x 7.1x 9.7x 8.5x

Jumbo BABr.AT 8.270 1.5% 10.00 20.9% 1,125.21 -2.4% 16.2% 4.4% 0.0% 11.1x 10.7x 10.5x 1.4x 6.8x 6.1x 5.6x

Motor Oil Hellas MORr.AT 10.300 2.1% 12.00 25.7% 1,141.06 58.5% 88.5% 0.0% 9.2% 10.8x 4.5x 4.8x 1.7x 39.5x 3.4x 3.3x

Opap OPAr.AT 8.430 2.9% 10.80 38.2% 2,689.17 -5.3% 12.7% 8.3% 10.1% 13.8x 13.8x 12.9x 2.4x 6.9x 7.2x 5.9x

Neutral

Autohellas AUTr.AT 10.550 -0.5% 10.00 0.7% 128.26 13.7% 35.2% 7.6% 5.9% 8.0x 8.6x 7.6x 0.7x 3.3x 3.1x 3.0x

OTE OTEr.AT 8.850 2.3% 9.00 2.6% 4,337.83 -2.7% 15.7% 0.9% 0.9% 13.7x 14.6x 16.1x 1.9x 3.9x 4.2x 3.7x

PPC DEHr.AT 5.170 3.4% 4.00 -18.2% 1,199.44 -4.3% 13.9% 1.0% 4.4% 11.1x 7.8x 7.2x 0.2x 6.2x 5.5x 5.1x

Under Perform

Coca Cola HBC AG EEEr.AT 20.700 2.6% 17.00 -16.0% 7,614.25 32.0% 57.1% 1.7% 1.8% 27.4x 26.2x 24.7x 2.6x 12.2x 11.5x 10.3x

Under Review

Alpha Bank ACBr.AT 0.135 27.4% U/R n/a 1,723.82 -71.2% -65.7% 0.0% 0.0% <0 U/R U/R U/R n/a U/R U/R

Eurobank EURBr.AT 0.025 25.0% U/R n/a 367.70 -86.6% -84.1% 0.0% 0.0% <0 U/R U/R U/R n/a U/R U/R

Metka MTKr.AT 8.230 1.6% U/R n/a 427.55 -2.6% 15.9% 3.0% 2.3% 4.7x U/R U/R U/R 1.4x U/R U/R

National Bank NBGr.AT 0.571 4.0% U/R n/a 2,017.43 -61.2% -53.8% 0.0% 0.0% <0 U/R U/R U/R n/a U/R U/R

Sarantis SRSr.AT 7.300 0.7% U/R n/a 253.83 -3.9% 14.3% 2.1% 2.2% 14.8x 13.8x 12.1x 1.5x 9.8x 8.6x 7.1x

Titan TTNr.AT 21.300 0.1% U/R n/a 1,641.45 11.1% 32.2% 1.4% 1.4% <0 53.0x 25.4x 1.1x 11.1x 12.0x 9.4x

Restricted

Piraeus Bank BOPr.AT 0.086 22.9% Restricted n/a 524.77 -90.5% -88.8% 0.0% 0.0% <0 n/a ###### n/a n/a n/a #VALUE!

Reuters Last Daily Chg Value Volume

Warrants Code Price € (%) € mn mn

Alpha Bank GRALFAw.AT 0.020 42.9% 0.13 7.74

National Bank GRETEw.AT 0.034 30.8% 0.02 0.65

Piraeus Bank GRTPEIw.AT 0.010 25.0% 0.07 7.91

17

Piraeus Securities Universe & Radar| Price performance

Sources for this report: Piraeus Securities Greek Equity Research, Piraeus Bank Research, Bloomberg, Reuters, Factset, Effect, ATHEX, PDMA.

Prices Prices Prices Prices

31/05/12 26/06/15 chg % 04/09/15 chg % 15/10/15 chg %

General Index 525.45 797.52 51.78% 646.62 -18.92% 694.48 7.40%

PS Universe-Banks

Alpha Bank 0.159 0.094 -40.9% 0.119 26.6% 0.135 13.4%

Eurobank 4.155 0.144 -96.5% 0.038 -73.6% 0.025 -34.2%

National Bank 5.085 1.200 -76.4% 0.540 -55.0% 0.571 5.7%

Piraeus Bank 1.819 0.400 -78.0% 0.094 -76.5% 0.086 -8.5%

PS Universe-Non financials

Aegean 1.18 6.18 423.7% 6.49 5.0% 7.25 11.7%

Autohellas 2.27 11.50 405.5% 9.75 -15.2% 10.55 8.2%

Coca Cola HLB AG 18.38 20.01 8.9% 17.97 -10.2% 20.70 15.2%

Folli Follie Group 4.38 24.20 452.5% 19.89 -17.8% 18.02 -9.4%

Fourlis 0.65 3.00 360.8% 2.38 -20.7% 2.80 17.6%

Frigoglass 3.32 2.10 -36.7% 2.00 -4.8% 2.23 11.5%

Hellenic Exchanges 2.05 4.64 125.8% 4.63 -0.2% 5.18 11.9%

Jumbo 2.42 7.42 206.6% 7.37 -0.7% 8.27 12.2%

Metka 5.85 7.79 33.2% 7.12 -8.6% 8.23 15.6%

Motor Oil 4.60 8.50 84.8% 9.01 6.0% 10.30 14.3%

OPAP 4.30 7.81 81.6% 7.33 -6.1% 8.43 15.0%

OTE 1.30 8.20 530.8% 8.00 -2.4% 8.85 10.6%

PPC 1.32 4.71 256.8% 4.74 0.6% 5.17 9.1%

Sarantis 1.35 7.58 459.8% 7.23 -4.6% 7.30 1.0%

ON THE RADAR

Athens Water 2.58 5.84 126.4% 5.20 -11.0% 5.62 8.1%

Corinth Pipeworks 0.51 1.08 111.8% 1.01 -6.5% 1.14 12.9%

Ellaktor 0.67 1.87 177.4% 1.41 -24.6% 1.78 26.2%

Elval 0.79 1.49 89.1% 1.73 16.1% 1.66 -4.0%

Grivalia Properties 2.02 7.36 264.4% 7.93 7.7% 8.43 6.3%

GEK-Terna 0.52 1.79 247.3% 1.56 -12.8% 1.78 14.1%

Hellenic Petroleum 4.76 4.68 -1.7% 4.61 -1.5% 5.42 17.6%

Intralot 0.69 1.70 146.4% 1.48 -12.9% 1.60 8.1%

Karatzis 1.90 3.58 88.4% 3.68 2.8% 3.30 -10.3%

Kleemann 0.62 1.79 187.3% 1.76 -1.7% 1.72 -2.3%

Kloukinas 0.24 0.36 50.8% 0.36 -0.3% 0.35 -3.6%

Korres 3.27 3.80 16.3% 3.70 -2.6% 3.70 0.0%

Kri-Kri 0.71 1.80 152.2% 1.80 0.0% 1.80 0.0%

Mytilineos 1.66 5.79 248.8% 4.63 -20.0% 4.93 6.5%

Piraeus Port 7.90 13.31 68.5% 14.71 10.5% 16.29 10.7%

Terna Energy 0.92 3.07 235.2% 2.57 -16.3% 2.79 8.6%

Thessaloniki Port 10.23 19.80 93.5% 21.89 10.6% 24.64 12.6%

Thessaloniki Water 2.96 2.66 -10.1% 2.80 5.3% 3.26 16.4%

Thrace Plastics 0.47 1.41 200.0% 1.40 -0.7% 1.35 -3.6%

Titan 10.87 21.40 96.9% 20.24 -5.4% 21.30 5.2%

Source: Piraeus Securities Greek Equity Research

18

IMPORTANT DISCLOSURES Piraeus Securities S.A. is the brokerage division of Piraeus Bank (‘The Firm’), which does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Piraeus Securities S.A. certifies that the current organizational and administrative structure is proof of conflicts of interest and dissemination of any kind of information between the departments and also certifies that it does not relate to any kind of interest or conflict of interest with a) any other legal entity or person that might participate in the preparation of this research report and b) with any other legal entity or person that might not participate in the preparation of this research report but had access to the research report before its publication. Piraeus Securities seeks to update covered companies on a quarterly basis or else on any material upcoming events. ANALYST CERTIFICATION: The analyst identified in this report certifies that his/her views about the company/ies and securities analysed in this report a) accurately reflect his/her personal views and b) do not directly or indirectly relate to any kind of compensation in exchange for specific recommendations or views.

Coverage Universe

Piraeus Securities Research Stock Ratings

Weighted on Mcap

Un-weighted Rating Definitions Investment Banking Activities within

12-month period

Outperform : 34.2% 42.1% Total return (*) expected to be greater than 10% compared to the market’s return (**) over a 12-month period

-

Neutral: 54.6% 15.8% Total return (*) expected to be between -10%/+10% compared to the market’s return (**) over a 12-month period

-

Underperform: 0.0% 5.3% Total return (*) expected to be below -10% compared to the market’s return (**)over a 12-month period

-

Restricted: 0.4% 5.3%

In certain circumstances that Piraeus Securities S.A. policy or applicable law / regulations preclude certain types of communication and investment recommendations

-

Under Review: 10.9% 31.6% Rating/TP may be subject to future revision - (*) Total return = Price appreciation + Dividend (**) Market return = Risk free rate + 5% (an approximation of equity risk premium) Investment ratings are determined by the ranges described above at the time of initiation of coverage, a change in rating, or a change in target price. At other times, the expected total returns may fall outside of these ranges because of price movement and/or volatility. Such interim deviations from specified ranges will be permitted but will become subject to review by Research Management.

CAUTION - DISCLAIMER This document has been issued by Piraeus Securities S.A. (“The Firm”), a member of the Athens Exchange supervised by the Hellenic Capital Market Committee. Piraeus Securities has based this document on information obtained from sources it believes to be reliable, but it has not independently verified all the information presented in this document. Accordingly, no representation or warranty, express or otherwise implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained in this document, or otherwise arising in connection therewith. Expressions of opinion herein are those of the Research Department only, reflect our judgment at this date and are subject to change without notice. This document does not constitute or form part of any offer for sale or subscription, or solicitation to buy or subscribe to any securities, nor shall it or any part of it form the basis of, in part or in whole, any contract or commitment whatsoever. This document was produced by the Research Department of Piraeus Securities and is for distribution only to persons who (i) have professional experience in matters relating to investments or (ii) are persons falling within Article 49(2) (a) to (d) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or to whom it may otherwise lawfully be passed on (all such persons being referred to as “relevant persons”). This report is directed only to relevant persons and must not be acted on or relied on by persons who are no relevant persons. Any investment or investment activity to which this report relates is available to relevant persons and will be engaged in only with relevant persons. This notice will not affect your rights under the Financial Services and Markets Act 2000 or the regulatory system. The opinions and recommendations herein do not take into account individual client circumstances, objectives or needs. This report is addressed to professional investors only and is being supplied to you solely for your information, and may not be reproduced, redistributed or passed on to any other person, or published, in whole or in part, for any purpose without prior written permission of Piraeus Securities S.A. and Piraeus Securities S.A. accepts no liability whatsoever for the actions of third parties in this respect. Additional note to our U.S. readers: This document may be distributed in the United States solely to “major US institutional investors” as defined in Rule 15a-6 under the US Securities Exchange Act of 1934. Each person that receives a copy, by acceptance thereof, represents and agrees that he/she will not distribute or otherwise make available this document to any other person. The distribution of this document in other jurisdictions may be restricted by law, and persons who come into possession of this document should inform themselves about and observe any such restrictions.

RESEARCH SALES/ TRADING Natasha Roumantzi

George Doukas

Iakovos Kourtesis

+30 210 3354065

+30 210 3354093

+30 210 3354083

Constantinos Xenos

Dimitris Dardanis

Yorgi Papazisis

Alexandros Malamas

+30 210 3354087

+30 210 3354043

+30 210 3354063

+30 210 3354041