Embed Size (px)

Citation preview

• Oriental Life Insurance Company,1818

• 1870, Bombay Mutual Life Assurance Society became the first Indian insurer.

• 1956, Life Insurance sector and Life Insurance Corporation came into existence

• 1971,General Insurance Corporation Of India

• Late 90’s Insurance sector was reopened to the private sector

• To give individual & corporate a competitive environment that can deliver products & services in tune with their requirements.

• Industry to benefit from technology transfer & capital from global insurance players.

• India is a signatory to WTO committed to open insurance & banking.

• Ensure their stability, transparency and financial strength, newentrants

• Guidelines that limit exposure in certain class of assets and also setsthreshold limits for some assets

• To ensure an orderly transition towards a deregulated insurancemarket and risk-based pricing

• Guidelines to de-tariff various segments.

• 1994 -- marine cargo, personal accident, health, banker liability and aviation

• 2005-06 -- marine hull segment

• 2007 - fire, engineering and motor own damage (OD)

The only segment that remains under a tariff regime is the third party motor business

• Sep 2013,IRDA launches 'Insurance Repository' services

• Enables policy holders to buy and keep insurance policies in dematerialized or electronic form

• Single account called electronic insurance account for policy holders.

• NSDL, Central Insurance Repository Limited , SHCIL Projects Limited, Karvy Insurance repository Limited, CAMS Repository Services Limited

• “unproven/experimental treatment”->"Treatment including drug experimental therapy which is not based on established medical practice in India, is treatment experimental or unproven.“

• “in-patient bed requirement”

• Relaxations made for maternity expenses or treatment.

Growth DriversDemand Growth for Insurance products set to accelerate:

India’s robust economy expected to sustain growth in insurance premiums underwritten

Higher personal disposable incomes higher household savings and financial savings

Emergence of affluent middle class increased demand for life and non-life insurance

Growing number of young professionals health and motor insurance

Growth of specific insurance segments such asmotor insurance and marine insurance

Favorable Policy Measures

• Covered under EEE method

• Tax benefit of approximately 30 % on select investments

Tax Incentives

• Insurance (Amendment) Bill

• Rashtriya Swasthya Bima Yojana (RSBY)Union Budget 2013-

14

• Insurance companies that have completed 10 years

of operations can raise capital through IPOs

• Need to have embedded value of twice the paid up equity capital

Life Insurance companies allowed to

go public

• Increase in FDI limit

• Revival package by government

Approval of Increase in FDI limit

Indian Insurance Industry

Strong demand •Growing interest in insurance among

people; innovative products and distribution channels aiding growth •Increasing demand for insurance offshoring•Growing use of internet has started increasing demand

Attractive opportunities •Life insurance in low-income urban areas

•Health insurance, pension segment •Strong growth potential for microinsurance, especially from

rural areas

Increasing investments •Rising participation by private players

has increased their market share in the life insurance market to 27.3 per cent in FY13 from 2 per cent in FY03 •Increase in FDI limit to 49 per cent from 26 per cent, as proposed in 2012, will further fuel investments

Policy support •Tax incentives on insurance products

•Passing of Insurance Bill gives IRDA flexibility to frame regulations •Clarity on rules for insurance IPOs would infuse liquidity in the industry •Repeated attempts to make the sector more lucrative for foreign participants

Advantage India

Current Scenario

Source:http://www.ibef.org/industry/insurance-sector-india.aspx

• In FY 2013, India stood 10th among 147 countries in life insurance

• Growth in non-life insurance outperformed average global growth

• Total Insurance market expanded from USD 14.7 in FY03 billion to USD 64.5 billion in FY13

• Total gross written premiums increased at a CAGR of 16%

• Crop insurance market in India is the largest in the world and covers around 30 million farmers

•Strong growth in the automotive industry over the next decade to be a key driver of motor insurance

•Health insurance continues to be one of the most rapidly growing sectors in the Indian insurance industry, and reported 18.66 per cent growth in gross premiums in FY13

Currently, the life insurance sector has 23 private players compared to only four in FY02

LIC is still the market leader, with 72.7 per cent share in FY13, followed by ICICI Prudential, with 4.7 per cent share

The industry is witnessing a shift towards the traditional non-linked insurance plans

The non-life insurance market grew from USD3.4 billion in FY04 to USD11.6 billion in FY13

Motor insurance forms the largest non-life segment

The market share of private sector companies rose from 14.5 per cent in FY04 to 44.4 per cent in FY13

New India leads the market with 15.9 per cent market share. Private players are not far behind and compete better in the non-life insurance segment

Indian Insurance Market

Trends

Multi-distribution i.e. increasing penetration through new modes of distribution such as the internet, direct and telemarketing and NGOs

Product innovation i.e. increased levels of customization through product innovation

Claims management i.e. timely and efficient management of claims to prevent delays which can increase the claims cost

Profitable growth i.e. expanding product range, developing innovative products and expanding distribution channels

Regulatory trends i.e. mandated regulatory changes by the IRDA to promote a competitive environment in both the life and non-life insurance sectors

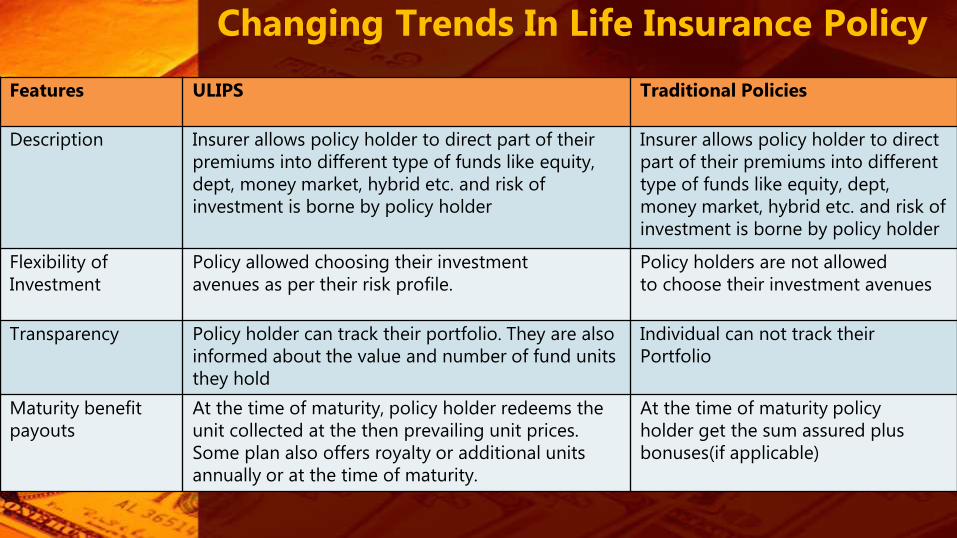

Changing Trends In Life Insurance Policy

Features ULIPS Traditional Policies

Description Insurer allows policy holder to direct part of their premiums into different type of funds like equity, dept, money market, hybrid etc. and risk ofinvestment is borne by policy holder

Insurer allows policy holder to direct part of their premiums into different type of funds like equity, dept, money market, hybrid etc. and risk of investment is borne by policy holder

Flexibility of Investment

Policy allowed choosing their investment avenues as per their risk profile.

Policy holders are not allowed to choose their investment avenues

Transparency Policy holder can track their portfolio. They are also informed about the value and number of fund units they hold

Individual can not track their Portfolio

Maturity benefit payouts

At the time of maturity, policy holder redeems the unit collected at the then prevailing unit prices. Some plan also offers royalty or additional units annually or at the time of maturity.

At the time of maturity policy holder get the sum assured plus bonuses(if applicable)

Insurance Challenges that a Business faces

Needing a trusted advisor •Are you receiving valuable advice through a consultative approach?•Is your broker proactive in addressing your insurance needs?•Do you have a “true business partner” in your insurance broker?

Finding the proper insurance program •Is your current insurance program competitively priced in the current market environment?•Has a risk management analysis been conducted recently on your insurance exposures?•Does your broker offer coverage options and recommendations?

Managing risk •How competitive is your Risk Management Program?•How are you controlling your exposure to loss sources?•Do you have a Contractual Risk Transfer Program in place to limit potential lawsuits?

Choosing a strong insurance company•Does your insurance company have financial strength and strong claims paying ability?•Is your insurance company a leader in your industry?•Does your insurance carrier provide consistent delivery of valued services?

Delivering customized employee benefits •Is your Employee Benefits Program cost-effective?•Are you able to attract and retain employees with a benefits program that is competitive within your industry?

Protecting personal assets •Are you taking advantage of recent competitive rating reforms to automobile insurance?•Do you have personal property and liability limits to protect your assets from loss?•Do you regularly review your life insurance benefits following life cycle events?

Life Insurance : Challenges

In FY12, the life insurance industry witnessed a decline in the first year premium collected which dropped from INR1, 258 billion in FY11 to INR1, 142 billion, a drop of approximately 10%. This was owing to the following challenges that the industry faced in

Product strategy and design

Cost

Taxation

Distribution

Prospects and challenges of various channels

Compensation

Customer service

Governance and regulatory issues

Health Insurance : Challenges before the insurers

Low awareness among the population about the benefits of health insurance

Trust-deficit in the customer/consumers which needs to be immediately closed out

High incidence of doubtful/suspect claims: According to a McKinsey report(2010), at least 20% of health claims in India are suspected or doubtful

Rise in moral hazard among all the stake holders in the insurance – treatment value chain resulting in large variations in healthcare costs for the same ailment/treatment

Limited product range in coverage resulting in mismatch between demand and supply of insurance

¤ LIC services less than 100 million policies, only 65 million Indians have been introduced to insurance which is a penetration of just 6%.

¤ Only about 60% of motor vehicles and only 46% of two-wheelers are insured.

¤ The future of Indian insurance sector looks bright. The sector which stood at a strong US$72 billion a few years back has the potential to grow to US$280 billion by 2020.

¤ Health insurance currently caters for 10% of the overall US$30 billion expenditure in India. The life insurance segment contributes about 4% to India’s GDP in terms of total premiums annually.

¤ The general insurance industry grew by 19.6% in April-May period of FY 13-14.

¤ The current size of aviation insurance hovers around US$78.86 million.

¤ It is anticipated that 60% of non-life insurance companies to record an average growth of more than 10%. The raising FDI limit from 26% to 49% in the sector has been viewed as key element to promote the insurance industry in India.

Indian insurance market is poised for strong growth in the long run delivering “stable profitable growth”

× Significant latent market - Expected to do well in the coming decades leading to increase in per capita incomes and awareness

× Channelizing industry focus - Three areas of focus could be

+ product innovation + reengineering the distribution

+ making sales and marketing more responsible

× Distribution - Distribution channels evolved in response to market dynamics and changing consumer preferences

× Regulation - Regulations need to drive transparency and simplification of products and services

• Multi-channel distribution footprint - Managing the expectations of channel partners, viz., banks, corporate agents, brokers, and advisory force, and keeping the acquisition costs at manageable proportions at the same time will help the new players reach break-even relatively sooner

• Technological advancement - technological advancement will be critical to functions like data management, underwriting, fund management, actuarial efficiency, and the end-to-end service delivery process.

• Quality of manpower - The quality of manpower attracted and retained by insurers and how their abilities and ambitions are harnessed would be the litmus test for the industry.

• Investment strategy and fund management - Expertise in fund management is the value proposition that any insurance company offers and the quality of asset-liability management (ALM) in a falling or stable interest rate regime will thus be a key challenge.

• Acquisition costs - Acquisition costs which is a sum total of technological, operational, and distribution costs, will be the key differentiating factor in the initial years. While the initial hits on the technology and process costs have already been absorbed by a majority of the new insurers, intermediary costs of distribution is a critical variable.

In medium & long term, growth trend in automobiles sales, emergence of large organized collaborators are expected to provide the growth momentum for this segment

Expected to grow at a robust pace driven by increased penetration in tier II and III cities increasing urbanization, demographic shifts and medical Inflation

The growth in gross capital formation, including in the infrastructure sector, would continue to drive growth in this segment in the long term

Drivers for the marine segment would continue to be the growth in GDP leading to increased international trade

expected to grow in the near term on the back of increased penetration, especially in non-metro markets, and growth in the gross capital formation of the country

• The leaps in technology helps to track relationship with the customer & give information to analyze the changing needs/profile of the consumer

• Reduction in turnaround time as well as multiple interaction points with the customer through emails, websites, and ATMs, etc.

Improved disclosure to policy holders

Resulted in

Increase in pure protection products, a refreshing look at unit-linked plans with rising protection components, launch of customized plans to suit niche requirements, improved positioning and market communication by players, and last but not the least, improved service levels which will get redefined

with every passing day

Future of Insurance is defined as

† The future in life insurance will be determined by the increase in pure protection products, a refreshing look at unit-linked plans, launch of customized plans, and improved service levels

† The insurance sector will grow steadily rather than rapidly, the regulator’s challenge lies in monitoring compliance

† The opportunity for financial services is increasing all over the world. Big domestic companies with significant market shares have opportunities to commence business in other markets

† Keeping in mind the complexities of the industry, multi-product, multi-channel, and multi-segment route needs to be followed for growth

† The challenge of successfully implementing bancassurance lies in training the staff, integrating the insurance products, and ensuring best quality service

† Agents in the insurance sector are critical for its success and, in order to gain competitive advantage, quality people are needed but attracting and retaining agents is a challenge