Embed Size (px)

Citation preview

Sales Finance Bulk Purchases with Credit Insurance

Getting Started

• Read the entire Sales Contract

• Ask for All Insurance Forms

• Determine if there is a “Master Policy”

or Group Policy

Agenda or Summary Layout A second line of text could go here

Discussion Item One – A Placeholder for text Add a second line of text here

Discussion Item Two – A Placeholder for text Add a second line of text here

Discussion Item Four – A Placeholder for text Add a second line of text here

Discussion Item Five – A Placeholder for text Add a second line of text here

Discussion Item Six – A Placeholder Add a second line of text here

General Rules

Discussion Item Three – A Placeholder for text Add a second line of text here

Item 2

Item 3

Item 4

Item 5

Item 6

General Rules

LICENSED AGENTS

Licensed Agents

• Insurance can only be offered through a licensed agent.

• Request a copy of license to be sure that it is current.

• All states require that a copy of the agent’s license be posted in the office.

• There are requirements for agent involvement in the offering of insurance.

• Vary by state.

• Verify laws are being followed by asking for a copy of the license.

• Verify that an agent signature is found

on insurance forms.

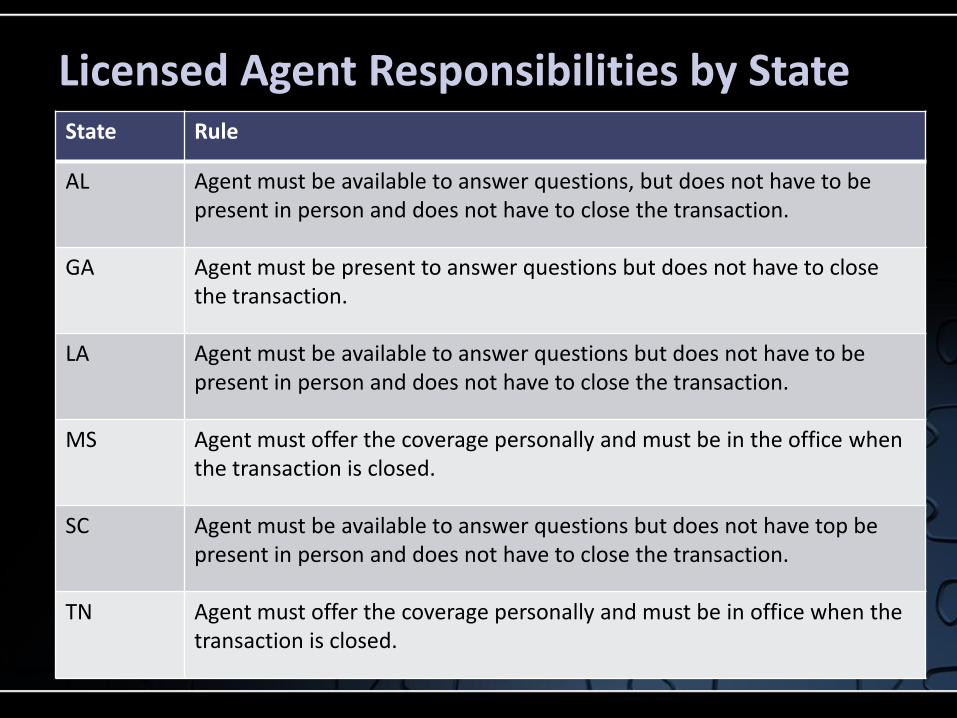

Licensed Agent Responsibilities by State State Rule

AL Agent must be available to answer questions, but does not have to be present in person and does not have to close the transaction.

GA Agent must be present to answer questions but does not have to close the transaction.

LA Agent must be available to answer questions but does not have to be present in person and does not have to close the transaction.

MS Agent must offer the coverage personally and must be in the office when the transaction is closed.

SC Agent must be available to answer questions but does not have top be present in person and does not have to close the transaction.

TN Agent must offer the coverage personally and must be in office when the transaction is closed.

Insurance Certificates

• The insured must receive a copy of the certificate of insurance or the policy.

• Closing of the transaction

• By mail within 30 days of the closing.

• A copy must be placed in the customer’s file.

• Missing documents may indicate:

• (1) a copy is not being given to the insured,

• (2) a copy is not being mailed to the insured,

• (3) the Seller is not maintaining his files properly, or

• (4) the insurance premiums are being collected

but not remitted to the carrier.

SCHEDULE OF INSURANCE VS CERTIFICATE OR POLICY

• A Schedule of Insurance contain the basic

information related to the insurance such as effective date, term of coverage, expiration date, premium amount, and coverage amount. It may or may not contain some of the additional policy language. A Schedule when given to the insured does not satisfy the requirement to provide a certificate or policy within 30 days. It also does not satisfy the requirement to retain a copy of the certificate or policy in the customer’s file. When you see only a Schedule in the customer’s file, you must (1) confirm that an Individual Policy has been issued and mailed to the insured and ask why there is no copy in file, or (2) confirm that a Certificate has been issued and mailed to the insured and ask why there is no copy in file. Also request a copy of the Group Policy.

• A Group Policy (sometimes called a Master Policy or Control Policy) multiple insured individuals are covered under one policy. Certificates are issued to the individuals.

• A Certificate of Insurance is issued only in connection with a Group Policy (sometimes called Master Policy or Control Policy). A Certificate will contain at least a portion of the terms of the Group Policy and sometimes will contain all of the terms. The Certificate should always refer to the Group Policy, and the Seller should have a copy of the Group Policy. When you see a certificate instead of a policy, you must obtain a copy of the group policy from the Seller.

• An Individual Policy stands alone. It is not group coverage, so there is no certificate.

General Rules

General Rules

• Population will depend on the type insurance offered and authorized by the customer. The type insurance written will also affect how refunds are handled. See # 11 below.

• Disability insurance

• 3, 7, 14, or 30 day non-retro

or

• 3, 7, 14, or 30 day retro.

•Life insurance • Level-term • Gross decreasing term

• Net decreasing term

• Net decreasing term + XX payments

Insurance Options

Either single or joint coverage can be offered.

Either single or joint coverage can be offered.

•Coverage on Consumer Goods

•Single interest

•Dual interest

General Rules • Credit insurance products - A&H, Life and IUI coverage may be optional

or required.

• If coverage is required, you should determine that the premiums have been

included in the finance charge and reflected in the APR.

• If the coverage is optional, the premiums for coverage and other related

information must be disclosed in writing.

• The insured must indicate their choice of coverage in writing by signing or

initialing.

• Required disclosures and signature (or initials) may be found in the seller’s

documents or the insurance forms.

• Use of model disclosures provides a TILA safe harbor.

• We offer these products as optional coverage using

the model disclosure format.

• A seller who requires the products should clearly

state that they do so.

General Rules

• Coverage on consumer goods or motor vehicles may be required. However, the seller can not require that the buyer purchase credit insurance.

• This coverage may be provided in one of three ways:

• (1) an existing outside policy that the buyer holds (by endorsement),

• (2) a new policy purchased outside by the buyer (by endorsement),

• (3) credit insurance that the seller offers.

• Required disclosures may be in the seller’s documents or the insurance

forms.

• Use of model disclosures provides a TILA safe harbor.

General Rules • It is important to confirm that the seller is promptly remitting

net premiums to the insurance carrier.

• Obtain insurance company name, contact person, and telephone

number.

• Confirmation may be one of two ways:

• Request to see a copy of a monthly remittance check. The check should be

for the premium written less refunds made less commission. The

remittance should occur within the month following the activity which it

represents.

• Contact the carrier to confirm that the seller is remitting

net premiums promptly and is in good standing.

General Rules

• Separate from the Compliance review is a discussion of how the existing insurance policies will be handled if we purchase the accounts.

• Will we report refunds direct to the carrier and receive refund checks

direct from the carrier?

• Will we report refunds to the seller and receive reimbursement from

the seller?

• How often will we report refunds, and what information is required for

this reporting?

• How will claims be handled?

General Rules

• Account servicing rules must be reviewed prior to purchasing the accounts. For each insurance type, you must identify and document the following:

• Refund method

• Number of days elapsed for earning each month’s premium

• Whether months are counted by loan months or payment periods

• Minimum refund provisions

• Time period during which 100% refund must be given

• Special refund rules in the event of a claim

Special State Rules

• Alabama can offer only net decreasing or net + 1 decreasing life insurance.

• South Carolina can offer level-term life insurance only on single-payment accounts.

• Pro rata refunding is required for level-term life insurance in all of the States in which we operate.