Embed Size (px)

Citation preview

Urban infrastructure in Sub-Saharan Africa

Harnessing land values, housing and transport

Presented by Brendon van Niekerk, PDG

Research by Brendon van Niekerk and Ian Palmer

20 July 2015

Reaching a balance in financing urban infrastructure

Structure of presentation

• Conceptual framework (recap from earlier presentation).

• Overview of infrastructure finance (Ian new piece).

• Land-based financing instuments

• Current practice with land-based financing.

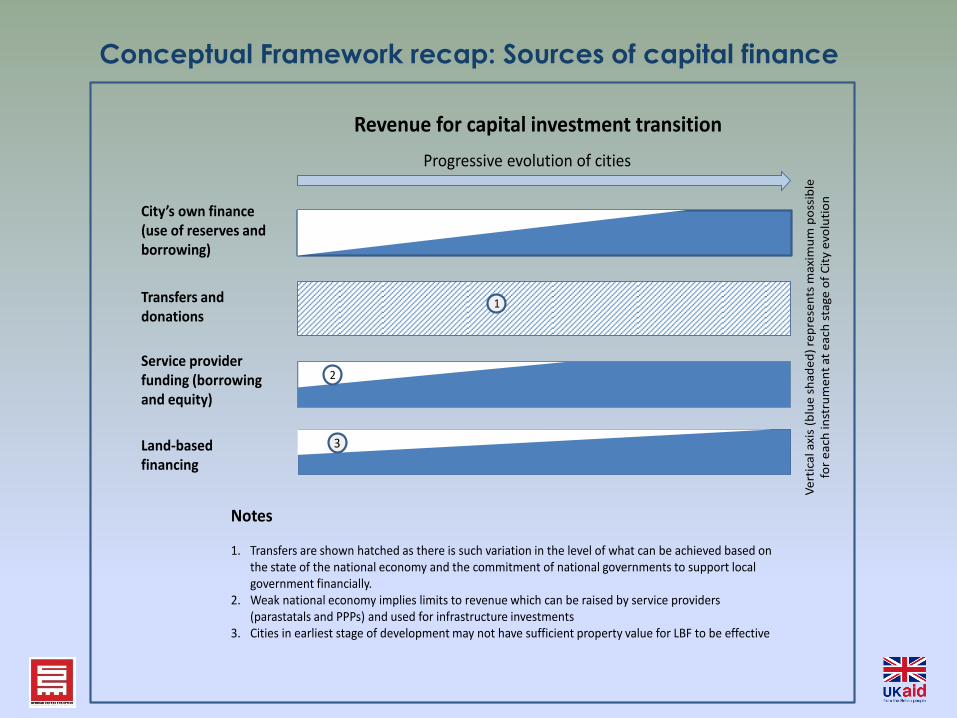

Revenue for capital investment transition

Land-based financing

City’s own finance (use of reserves and borrowing)

Service provider funding (borrowing and equity)

Progressive evolution of cities

1. Transfers are shown hatched as there is such variation in the level of what can be achieved based on the state of the national economy and the commitment of national governments to support local government financially.

2. Weak national economy implies limits to revenue which can be raised by service providers (parastatals and PPPs) and used for infrastructure investments

3. Cities in earliest stage of development may not have sufficient property value for LBF to be effective

Notes

2

Ve

rtic

al a

xis

(blu

e s

ha

de

d)

rep

rese

nts

ma

xim

um

po

ssib

le

for

ea

ch in

stru

me

nt

at

ea

ch s

tage

of

Cit

y e

volu

tio

n

Transfers and donations

3

1

Conceptual Framework recap: Sources of capital finance

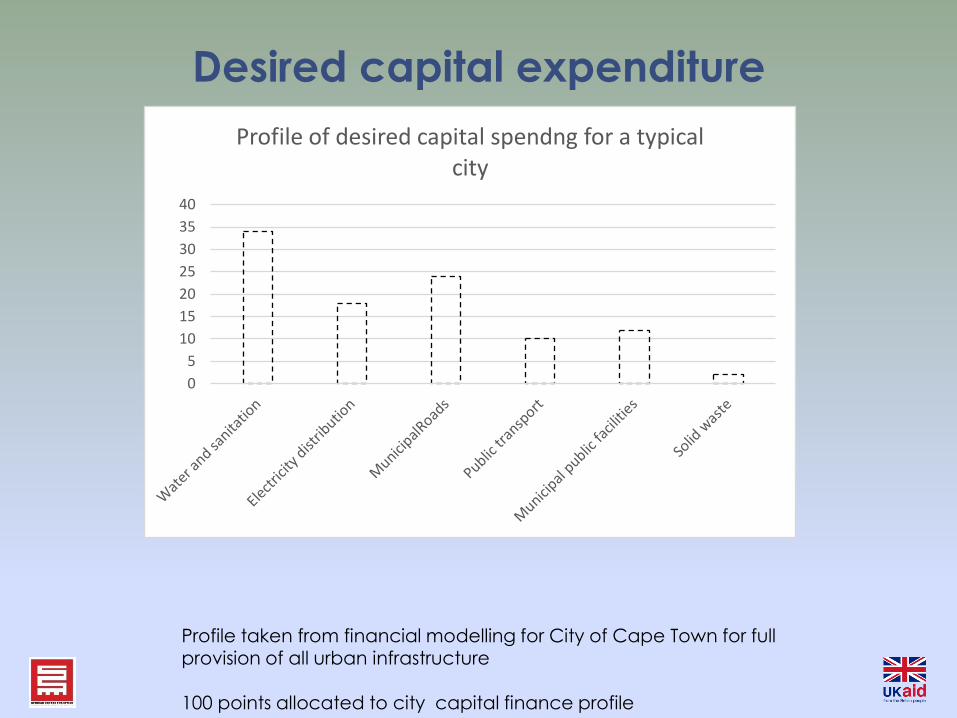

Desired capital expenditure

0

5

10

15

20

25

30

35

40

Profile of desired capital spendng for a typical city

Profile taken from financial modelling for City of Cape Town for full provision of all urban infrastructure

100 points allocated to city capital finance profile

0

5

10

15

20

25

30

35

40P

oin

ts

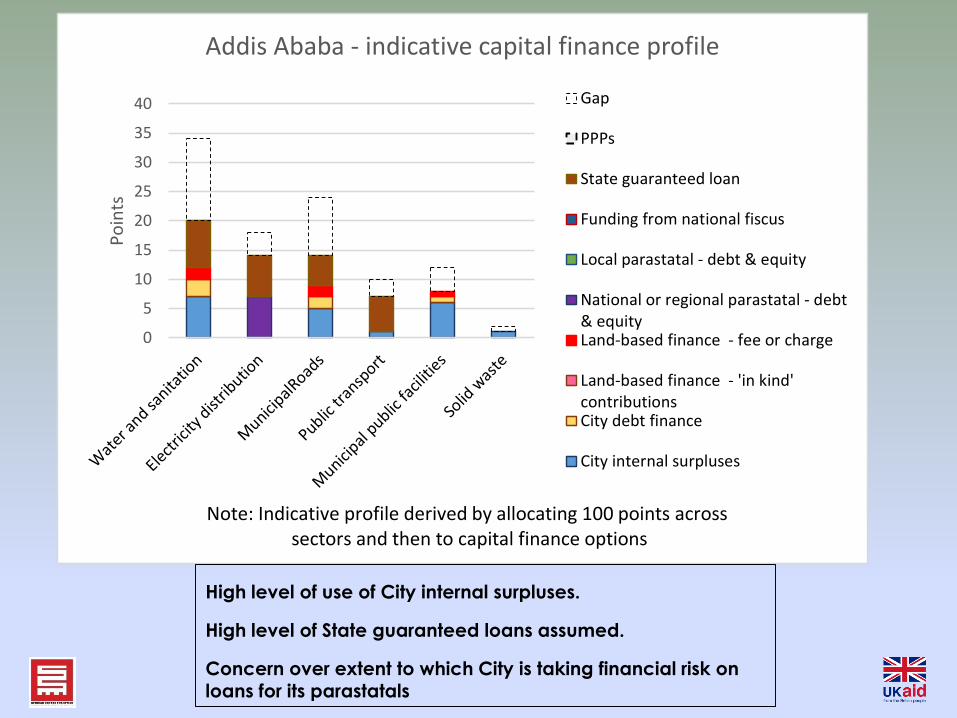

Addis Ababa - indicative capital finance profile

Gap

PPPs

State guaranteed loan

Funding from national fiscus

Local parastatal - debt & equity

National or regional parastatal - debt& equityLand-based finance - fee or charge

Land-based finance - 'in kind'contributionsCity debt finance

City internal surpluses

Note: Indicative profile derived by allocating 100 points across sectors and then to capital finance options

High level of use of City internal surpluses.

High level of State guaranteed loans assumed.

Concern over extent to which City is taking financial risk on loans for its parastatals

0

5

10

15

20

25

30

35

40P

oin

ts

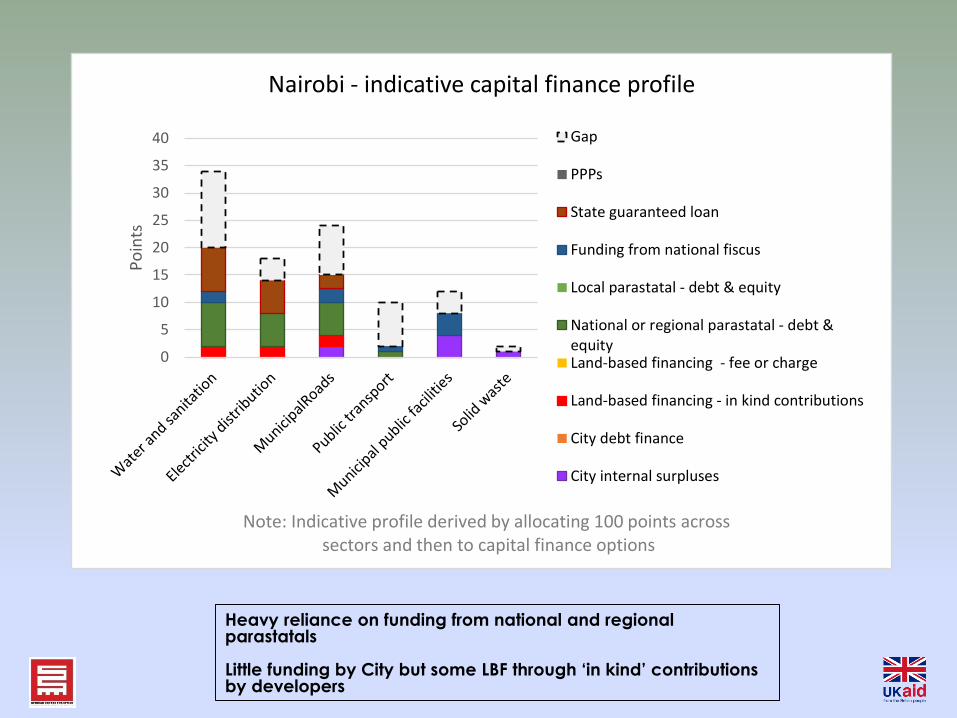

Nairobi - indicative capital finance profile

Gap

PPPs

State guaranteed loan

Funding from national fiscus

Local parastatal - debt & equity

National or regional parastatal - debt &equityLand-based financing - fee or charge

Land-based financing - in kind contributions

City debt finance

City internal surpluses

Note: Indicative profile derived by allocating 100 points across sectors and then to capital finance options

Heavy reliance on funding from national and regional parastatals

Little funding by City but some LBF through ‘in kind’ contributions by developers

0

5

10

15

20

25

30

35

40P

oin

ts

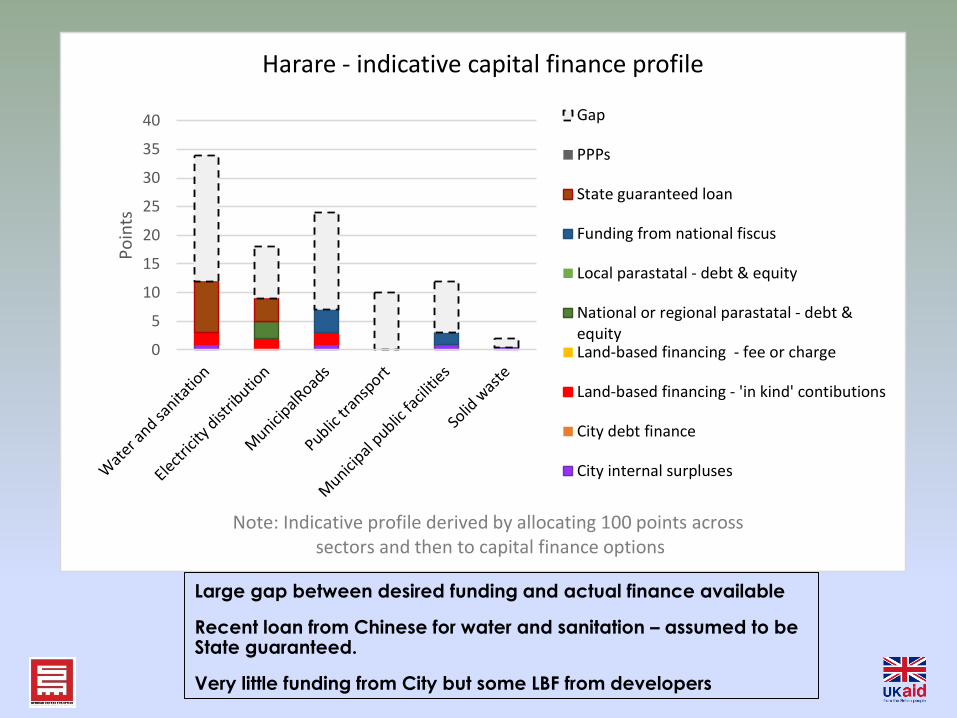

Harare - indicative capital finance profile

Gap

PPPs

State guaranteed loan

Funding from national fiscus

Local parastatal - debt & equity

National or regional parastatal - debt &equityLand-based financing - fee or charge

Land-based financing - 'in kind' contibutions

City debt finance

City internal surpluses

Note: Indicative profile derived by allocating 100 points across sectors and then to capital finance options

Large gap between desired funding and actual finance available

Recent loan from Chinese for water and sanitation – assumed to be State guaranteed.

Very little funding from City but some LBF from developers

Land-based financing

Land-Based Financing Instruments

Progressive evolution of cities

Undeveloped

propertyDeveloped property

with basic services

Increased building

height and floor

area ratios

Developer ‘in

kind’

contribution

Impact fees;

development

charges

Land sale,

land lease,

sale of

development

rights

Betterment

tax/levy

Property

tax, tax

surcharge

etc

Tax

Increment

Finance

(TIF)

City capital account

City operating account

Basic

infrastructure

serving individual

property

developments

Improved service

levels; higher

capacity

infrastructure

systems

Infrastructure

focused on

improved quality

of life

Advanced

infrastructure:

mass transit; CBD

upgrades; parks

etc

Focus on building

performance, green

space; recreation

City capital account

Negotiated

‘once off’

payments for

infrastructure

Dedicated investment account

Specific

infrastructure for

identified

properties

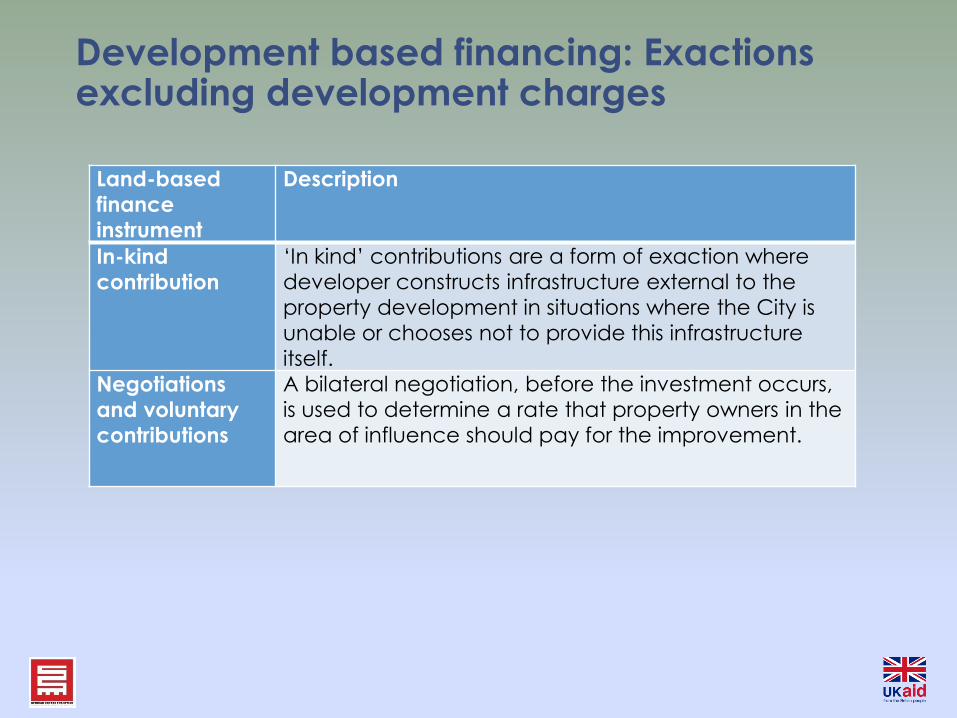

Development based financing: Exactions excluding development charges

Land-based

finance

instrument

Description

In-kind

contribution

‘In kind’ contributions are a form of exaction where

developer constructs infrastructure external to the

property development in situations where the City is

unable or chooses not to provide this infrastructure

itself.

Negotiations

and voluntary

contributions

A bilateral negotiation, before the investment occurs,

is used to determine a rate that property owners in the

area of influence should pay for the improvement.

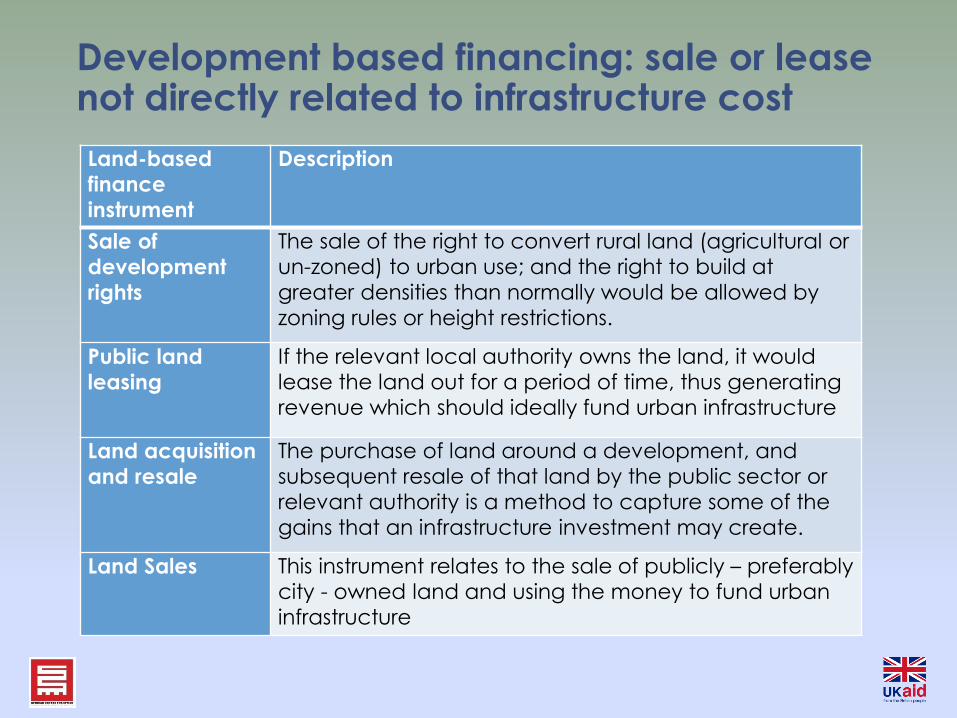

Development based financing: sale or lease not directly related to infrastructure cost

Land-based

finance

instrument

Description

Sale of

development

rights

The sale of the right to convert rural land (agricultural or

un-zoned) to urban use; and the right to build at

greater densities than normally would be allowed by

zoning rules or height restrictions.

Public land

leasing

If the relevant local authority owns the land, it would

lease the land out for a period of time, thus generating

revenue which should ideally fund urban infrastructure

Land acquisition

and resale

The purchase of land around a development, and

subsequent resale of that land by the public sector or

relevant authority is a method to capture some of the

gains that an infrastructure investment may create.

Land Sales This instrument relates to the sale of publicly – preferably

city - owned land and using the money to fund urban

infrastructure

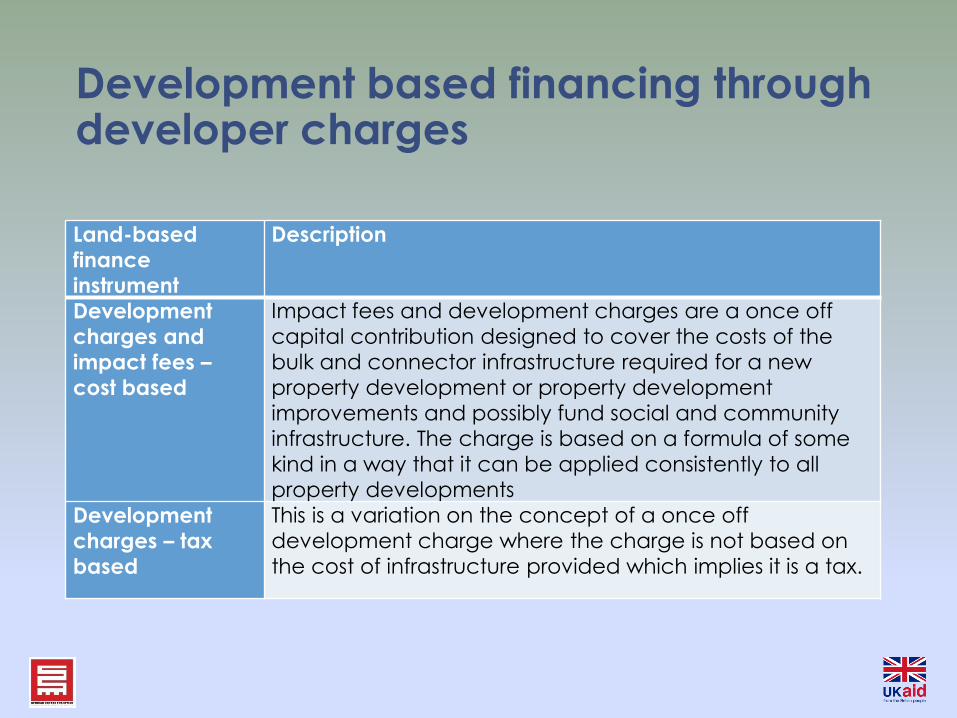

Development based financing through developer charges

Land-based

finance

instrument

Description

Development

charges and

impact fees –

cost based

Impact fees and development charges are a once off

capital contribution designed to cover the costs of the

bulk and connector infrastructure required for a new

property development or property development

improvements and possibly fund social and community

infrastructure. The charge is based on a formula of some

kind in a way that it can be applied consistently to all

property developments

Development

charges – tax

based

This is a variation on the concept of a once off

development charge where the charge is not based on

the cost of infrastructure provided which implies it is a tax.

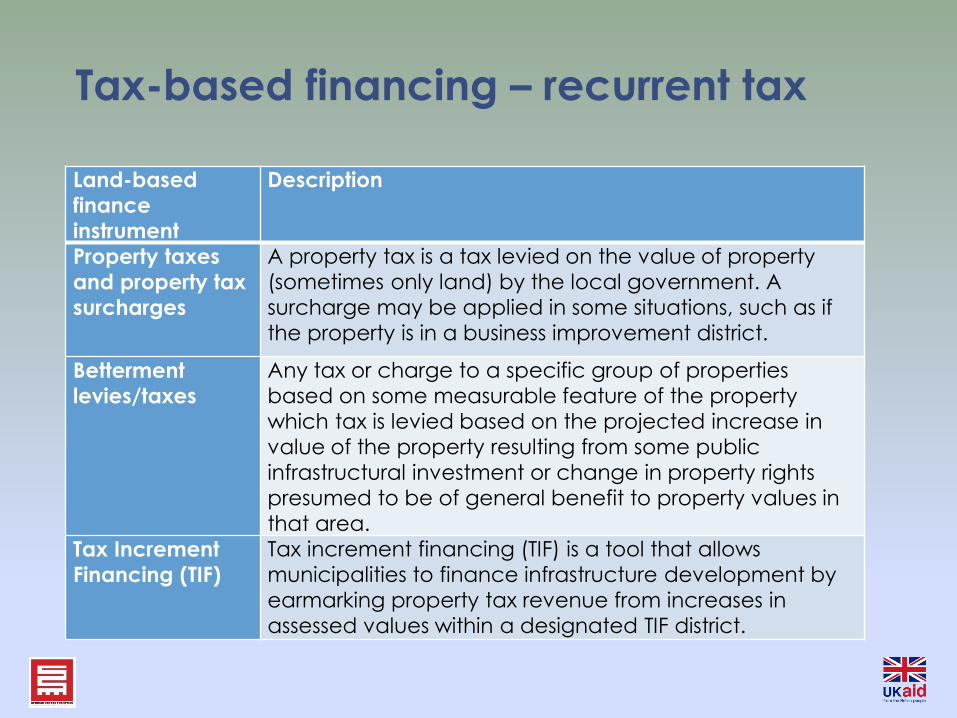

Tax-based financing – recurrent tax

Land-based

finance

instrument

Description

Property taxes

and property tax

surcharges

A property tax is a tax levied on the value of property

(sometimes only land) by the local government. A

surcharge may be applied in some situations, such as if

the property is in a business improvement district.

Betterment

levies/taxes

Any tax or charge to a specific group of properties

based on some measurable feature of the property

which tax is levied based on the projected increase in

value of the property resulting from some public

infrastructural investment or change in property rights

presumed to be of general benefit to property values in

that area.

Tax Increment

Financing (TIF)

Tax increment financing (TIF) is a tool that allows

municipalities to finance infrastructure development by

earmarking property tax revenue from increases in

assessed values within a designated TIF district.

Extent of contributions by developers

Building

Internal infrastructure

Connector infrastructure

Bulk infrastructure

Social & community infrastructure

Cross subsidise infrastructure for poor households

Land

No land-based

financing

Extreme where all building is subsidised

Land and/or internal

infrastructure subsidised

Full

cost

of

pro

per

ty d

evel

op

men

t

Maximum land based financing

including infrastructure

for poor households

Land based financing for

connector infrastructure, possibly other components

DIAGRAMATIC ILLUSTRATION OF LAND BASED FINANCE SPECTRUM FOR MIDDLE TO HIGH INCOME RESIDENTAL AND COMMERCIAL PROPERTY DEVELOPMENTS

City contributes to developer costs Developer contributes to City costs

-5 5

Rating0

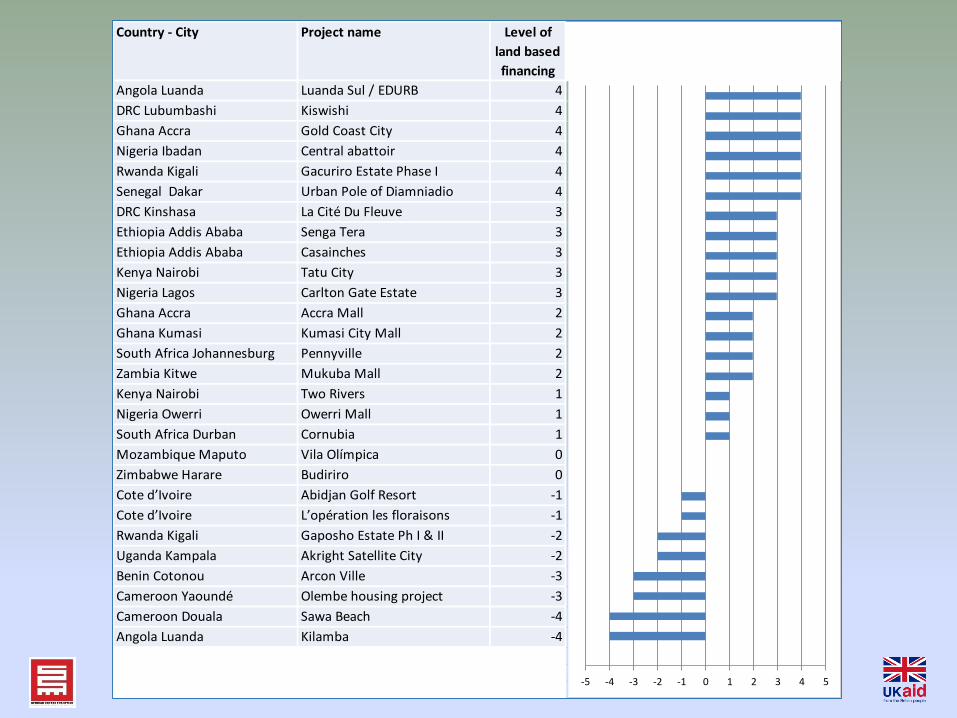

Country - City Project name Level of

land based

financing

Angola Luanda Luanda Sul / EDURB 4 -4

DRC Lubumbashi Kiswishi 4 -4

Ghana Accra Gold Coast City 4 -3

Nigeria Ibadan Central abattoir 4 -3

Rwanda Kigali Gacuriro Estate Phase I 4 -2

Senegal Dakar Urban Pole of Diamniadio 4 -2

DRC Kinshasa La Cité Du Fleuve 3 -1

Ethiopia Addis Ababa Senga Tera 3 -1

Ethiopia Addis Ababa Casainches 3 0

Kenya Nairobi Tatu City 3 0

Nigeria Lagos Carlton Gate Estate 3 1

Ghana Accra Accra Mall 2 1

Ghana Kumasi Kumasi City Mall 2 1

South Africa Johannesburg Pennyville 2 2

Zambia Kitwe Mukuba Mall 2 2

Kenya Nairobi Two Rivers 1 2

Nigeria Owerri Owerri Mall 1 2

South Africa Durban Cornubia 1 3

Mozambique Maputo Vila Olímpica 0 3

Zimbabwe Harare Budiriro 0 3

Cote d’Ivoire Abidjan Golf Resort -1 3

Cote d’Ivoire L’opération les floraisons -1 3

Rwanda Kigali Gaposho Estate Ph I & II -2 4

Uganda Kampala Akright Satellite City -2 4

Benin Cotonou Arcon Ville -3 4

Cameroon Yaoundé Olembe housing project -3 4

Cameroon Douala Sawa Beach -4 4

Angola Luanda Kilamba -4 4

-5 -4 -3 -2 -1 0 1 2 3 4 5

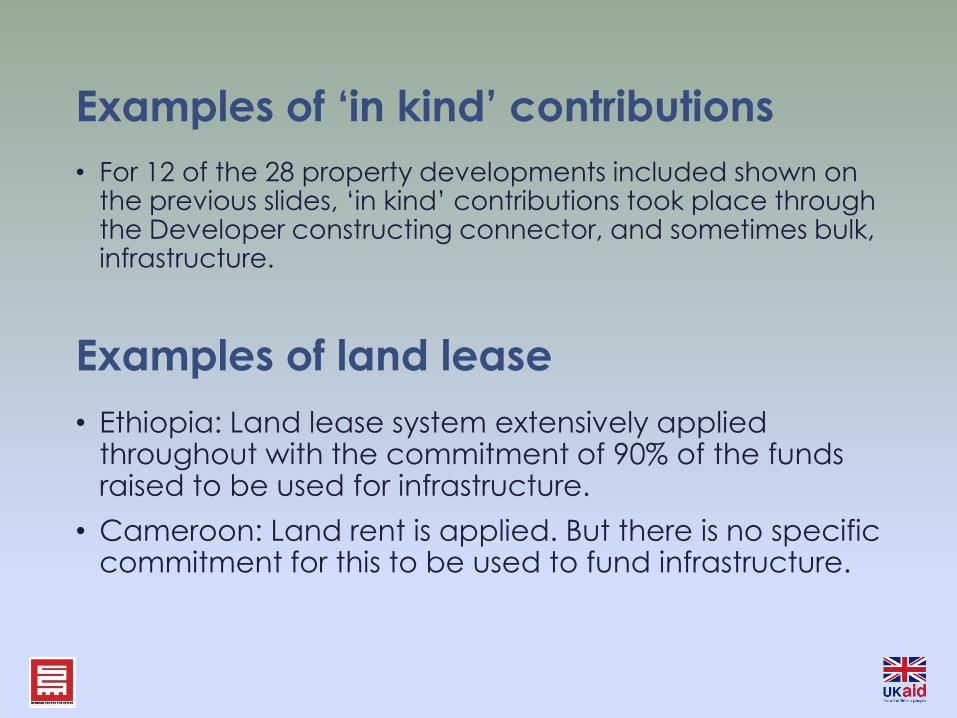

Examples of ‘in kind’ contributions

• For 12 of the 28 property developments included shown on the previous slides, ‘in kind’ contributions took place through the Developer constructing connector, and sometimes bulk, infrastructure.

Examples of land lease

• Ethiopia: Land lease system extensively applied throughout with the commitment of 90% of the funds raised to be used for infrastructure.

• Cameroon: Land rent is applied. But there is no specific commitment for this to be used to fund infrastructure.

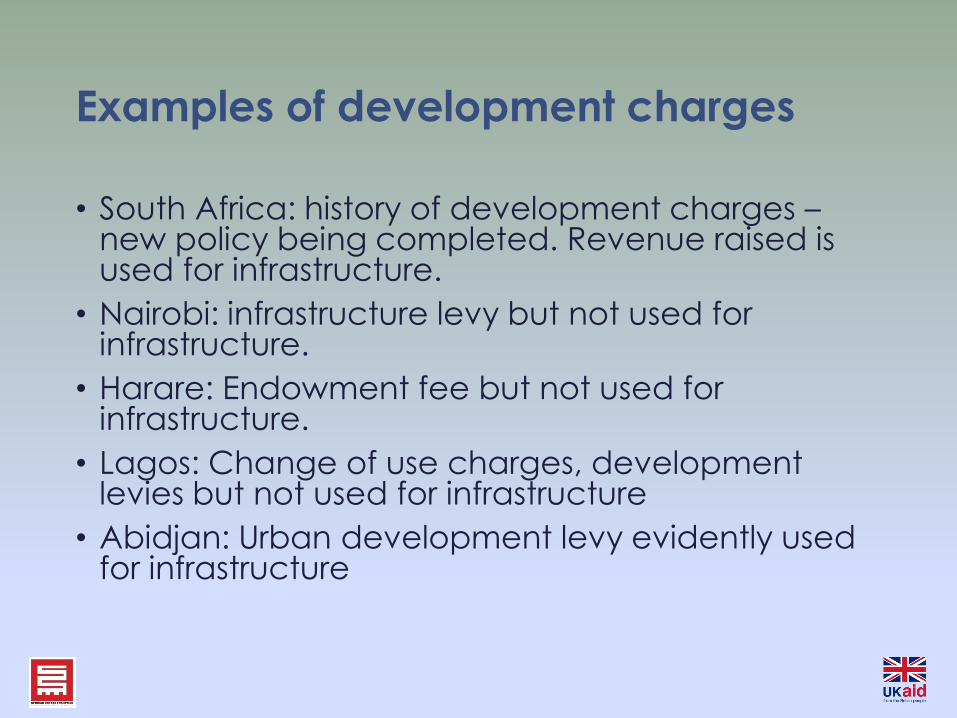

Examples of development charges

• South Africa: history of development charges –new policy being completed. Revenue raised is used for infrastructure.

• Nairobi: infrastructure levy but not used for infrastructure.

• Harare: Endowment fee but not used for infrastructure.

• Lagos: Change of use charges, development levies but not used for infrastructure

• Abidjan: Urban development levy evidently used for infrastructure

Conclusion• Land-based financing makes a relatively small contribution

to infrastructure finance in SSA.

• Evidence from this study is that most of this is through ‘in-kind’ contributions by developers.

• There are examples of development charges but in three of five countries where these are used the revenue does not do towards infrastructure investments.

• Land leasing occurs in Ethiopia and Cameroon but only contributes a modest amount to the total required to finance infrastructure.

• There are opportunities to raise substantial contributions through improved practice with development charges having the greatest promise

End

Urban infrastructure in Sub-Saharan Africa – harnessing land

values, housing and transport

Brendon van Niekerk, PDG

20 July 2015