© Woodhead Publishing Limited, 2013

497

18 Future directions toward more efficient and

cleaner use of coal

D. G. OSBORNE and M. SHARPLES, Xstrata Technology,

Australia , L. LIEN, United Finance and Management Services, USA ,

G. SCHUMACHER, NRG Gladstone Operating Services, Australia ,

A. BABICH, RWTH Aachen University, Germany , D. HARRIS and

J. CARRAS, CSIRO Energy Technology, Australia

DOI : 10.1533/9781782421177.3.497

Abstracts : Many eminent coal technologists perceive a shift towards integrated coal utilisation complexes that could one day convert coal into clean, ready to use energy, produce cost-effective reductants for steelmaking, and simultaneously generate an array of useful chemical feed-stocks or products, whilst still achieving environmental compliance. Is this feasible of just a pipedream? The chapter explores this and covers the future trend as it is perceived refl ecting on the changing energy scene and considering all energy sources. Current practices involve a series of distinct supply chains that lead to designated coal brands being passed from the supplier (producer) to the buyer (user) with very little collaboration or cooperation. Such practices minimise the potential for optimisation of the outcome and/or sustainability of the resource. An optimisation approach is important in order to set the scene for innovative concepts such as the “modifi ed” supply chain with the shift towards gasifi cation and transportation as SNG/LNG cargoes instead of bulk shipment including water and waste that are becoming increasing controversial, particularly in terms of regulatory controls and waste disposal. The ultimate outcome could be a move towards poly-generation, the integrated “coal driven factory/refi nery” that produces power, chemicals, steel, ash-based by-products, refractories, etc., all on one site.

Key words : coal utilisation, supply chain, integration, optimisation, poly-generation, emerging coal technologies.

18.1 Introduction

In this fi nal chapter several expert authors come together to describe a per-

ceived shift towards new, integrated coal utilisation complexes that could one

day convert coal into clean energy, produce cost-effective reductants for steel-

making, and simultaneously produce an array of useful chemical feed-stocks

or products, whilst still achieving environmental compliance. Is this feasible

or just a pipedream? The chapter explores this and covers the future trend

as we see it and initially refl ects on the changing energy scene considering all

energy sources. Current practices involve a series of distinct endeavours that

498 The coal handbook

© Woodhead Publishing Limited, 2013

lead to designated coal brands being passed from the supplier (producer) to

the buyer (user) with very little collaboration or cooperation. Such practices

minimise the potential for optimisation of the outcome and/or sustainabil-

ity of the resource. This ‘optimisation’ approach is important in order to set

the scene for innovative concepts like the ‘modifi ed’ supply chain with the

shift towards gasifi cation and transportation as SNG/LNG cargoes instead

of bulk shipment including water and waste that are becoming increasingly

controversial, particularly in terms of permitting and disposal. The ultimate

outcome should perhaps be a move towards polygeneration, the integrated

‘coal driven factory/refi nery’ that produces power, chemicals, steel, ash-based

by-products, refractories, etc., all on one site.

One of the greatest uncertainties in climate prediction is the amount of

CO 2 that will ultimately be released into the atmosphere. Ken Caldeira, a

climate scientist at Stanford University, asks how much CO 2 will be released

into the atmosphere if we assume that industrial civilisation will continue to

do what it has been doing for the past 200 years, namely burn fossil fuels at

an accelerating rate until we can no longer afford to extract them. 1 Current

predictions suggest over one quadrillion tonnes of carbon is currently locked

up in the Earth’s sedimentary deposits. So far, we have used only about

0.05% of this which has produced about 2000 billion tonnes of CO 2, so real-

istically that we will never run out of fossil fuels or use up all of the carbon

in the Earth’s crust. In addition to coal, oil and gas, we are also extracting oil

from tar sands and gas from fractured (fracked) oil shales; both resources

were once considered economically and technologically inaccessible. It is

therefore hard to imagine how far technology might take us, but it is prob-

ably fair to assume that coal will remain the most competitive option and

will continue to be used until the cost of extraction and processing become

uneconomical compared to other energy options. By this time, perhaps

more than 100 years from now, climate conditions will have changed sig-

nifi cantly even if the majority of the CO 2 is eventually successfully seques-

tered. Already, global temperatures have risen by almost 1°C and average

temperatures could conceivably continue to rise by 10°C, more than enough

to melt the ice in the glaciers of Greenland and at the polar icecaps. This

would cause water levels to be raised by 120 m and atmospheric concen-

trations would reach levels last reached somewhere in the mid-Cretaceous

period (~100 million years ago). Perhaps this transition will occur again and

mankind will gradually adapt to it. There is a very clear and strong tendency

to fi nd alternative solutions involving ‘coal free’ and ‘carbon lean’ technolo-

gies, especially in Europe. Therefore the main objective for this outlook,

from the point of view of the contributing authors, is to provide analysis and

discussion as to where, why and to what extent coal will be irreplaceable in

the future and how coal should be used in more environmentally friendly or

carbon conscious ways.

Future directions toward more effi cient and cleaner use of coal 499

© Woodhead Publishing Limited, 2013

18.1.1 Current coal reserves, resources and consumption

Globally, coal is the most abundant fossil fuel, with total reserves over 1 trillion

tonnes – in energy terms, approximately 3.2 and 2.5 times larger than those of

natural gas and oil. The coal resources are signifi cantly larger and more geo-

graphically diverse than the current reserve base, and as market conditions

change and technology advances more of the coal resources are converted into

reserves. Even though there has been a signifi cant increase in international

coal prices since 2005, continued depletion of lower cost mining seams and the

need to move towards deposits which are more challenging or more distant

from existing infrastructure has led to a signifi cant increase in overall mining

costs, since from 2005 the weighted-average coal mining costs has increased by

around 12% per annum. This balance between mining investment/operational

costs and international coal prices will be the ultimate driving factor in deter-

mining which resources are eventually converted into reserves and the cost

effectiveness of coal compared to alternative sources of primary energy.

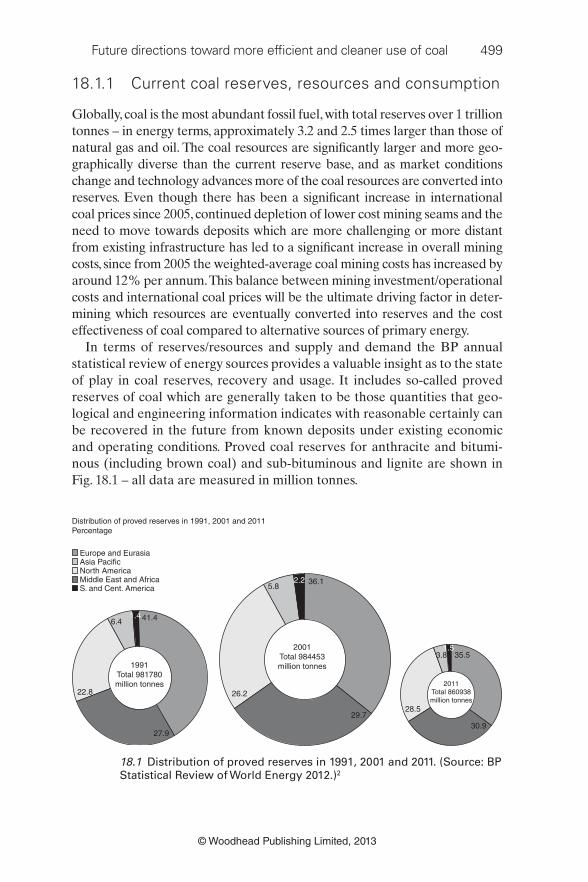

In terms of reserves/resources and supply and demand the BP annual

statistical review of energy sources provides a valuable insight as to the state

of play in coal reserves, recovery and usage. It includes so-called proved

reserves of coal which are generally taken to be those quantities that geo-

logical and engineering information indicates with reasonable certainly can

be recovered in the future from known deposits under existing economic

and operating conditions. Proved coal reserves for anthracite and bitumi-

nous (including brown coal) and sub-bituminous and lignite are shown in

Fig. 18.1 – all data are measured in million tonnes.

6.41.4 41.4

22.8

27.9

26.2

28.5

3.81.5

35.5

30.9

5.82.2 36.1

2001Total 984453million tonnes

Distribution of proved reserves in 1991, 2001 and 2011Percentage

2011Total 860938million tonnes

29.7

1991Total 981780million tonnes

Europe and EurasiaAsia PacificNorth AmericaMiddle East and AfricaS. and Cent. America

18.1 Distribution of proved reserves in 1991, 2001 and 2011. ( Source : BP

Statistical Review of World Energy 2012.) 2

500 The coal handbook

© Woodhead Publishing Limited, 2013

300

250

200

150

100

50

NorthAmerica

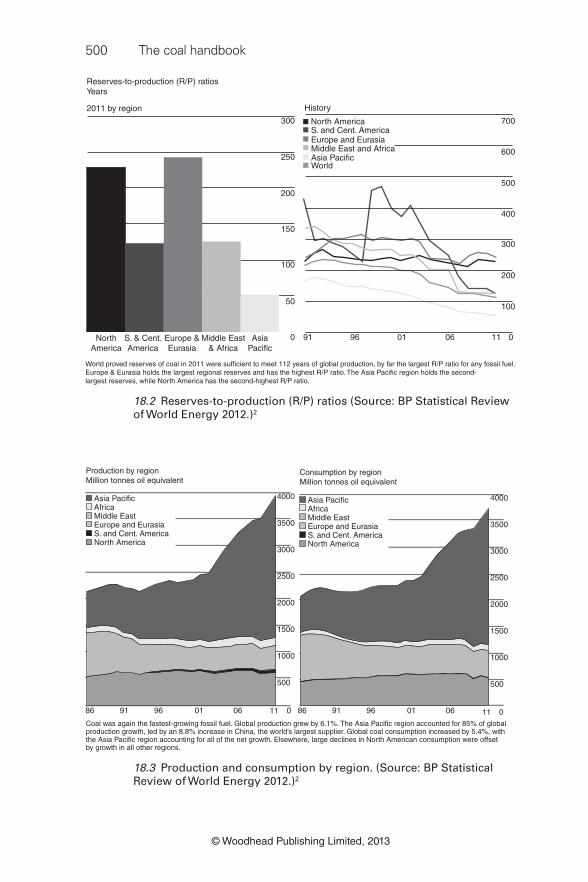

World proved reserves of coal in 2011 were sufficient to meet 112 years of global production, by far the largest R/P ratio for any fossil fuel.Europe & Eurasia holds the largest regional reserves and has the highest R/P ratio. The Asia Pacific region holds the second-largest reserves, while North America has the second-highest R/P ratio.

S. & Cent.America

Europe &Eurasia

Middle East& Africa

AsiaPacific

0 91 96 01 06 11 0

100

200

300

400

500

600

700

Reserves-to-production (R/P) ratiosYears

2011 by region History

North AmericaS. and Cent. AmericaEurope and EurasiaMiddle East and AfricaAsia PacificWorld

18.2 Reserves-to-production (R/P) ratios ( Source : BP Statistical Review

of World Energy 2012.)2

Production by regionMillion tonnes oil equivalent

Consumption by regionMillion tonnes oil equivalent

Asia PacificAfricaMiddle EastEurope and EurasiaS. and Cent. AmericaNorth America

Asia PacificAfricaMiddle EastEurope and EurasiaS. and Cent. AmericaNorth America

4000

3500

3000

2500

2000

1500

1000

500

4000

3500

3000

2500

2000

1500

1000

500

86

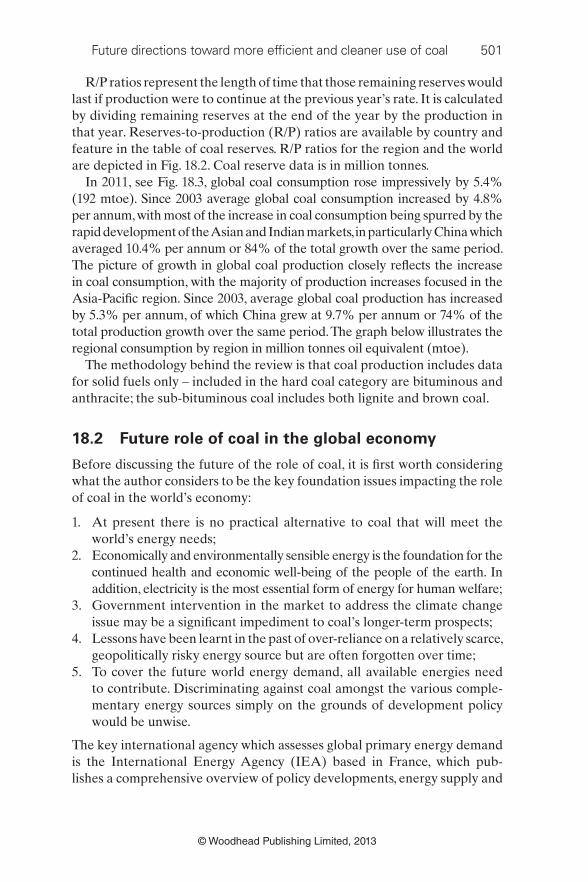

Coal was again the fastest-growing fossil fuel. Global production grew by 6.1%. The Asia Pacific region accounted for 85% of globalproduction growth, led by an 8.8% increase in China, the world’s largest supplier. Global coal consumption increased by 5.4%, withthe Asia Pacific region accounting for all of the net growth. Elsewhere, large declines in North American consumption were offsetby growth in all other regions.

91 96 01 06 11 0 86 91 96 01 06 11 0

18.3 Production and consumption by region. ( Source : BP Statistical

Review of World Energy 2012.)2

Future directions toward more effi cient and cleaner use of coal 501

© Woodhead Publishing Limited, 2013

R/P ratios represent the length of time that those remaining reserves would

last if production were to continue at the previous year’s rate. It is calculated

by dividing remaining reserves at the end of the year by the production in

that year. Reserves-to-production (R/P) ratios are available by country and

feature in the table of coal reserves. R/P ratios for the region and the world

are depicted in Fig. 18.2. Coal reserve data is in million tonnes.

In 2011, see Fig. 18.3, global coal consumption rose impressively by 5.4%

(192 mtoe). Since 2003 average global coal consumption increased by 4.8%

per annum, with most of the increase in coal consumption being spurred by the

rapid development of the Asian and Indian markets, in particularly China which

averaged 10.4% per annum or 84% of the total growth over the same period.

The picture of growth in global coal production closely refl ects the increase

in coal consumption, with the majority of production increases focused in the

Asia-Pacifi c region. Since 2003, average global coal production has increased

by 5.3% per annum, of which China grew at 9.7% per annum or 74% of the

total production growth over the same period. The graph below illustrates the

regional consumption by region in million tonnes oil equivalent (mtoe).

The methodology behind the review is that coal production includes data

for solid fuels only – included in the hard coal category are bituminous and

anthracite; the sub-bituminous coal includes both lignite and brown coal.

18.2 Future role of coal in the global economy

Before discussing the future of the role of coal, it is fi rst worth considering

what the author considers to be the key foundation issues impacting the role

of coal in the world’s economy:

1. At present there is no practical alternative to coal that will meet the

world’s energy needs;

2. Economically and environmentally sensible energy is the foundation for the

continued health and economic well-being of the people of the earth. In

addition, electricity is the most essential form of energy for human welfare;

3. Government intervention in the market to address the climate change

issue may be a signifi cant impediment to coal’s longer-term prospects;

4. Lessons have been learnt in the past of over-reliance on a relatively scarce,

geopolitically risky energy source but are often forgotten over time;

5. To cover the future world energy demand, all available energies need

to contribute. Discriminating against coal amongst the various comple-

mentary energy sources simply on the grounds of development policy

would be unwise.

The key international agency which assesses global primary energy demand

is the International Energy Agency (IEA) based in France, which pub-

lishes a comprehensive overview of policy developments, energy supply and

502 The coal handbook

© Woodhead Publishing Limited, 2013

demand balances and a primary energy outlook for the next 25 years. The

IEA is primarily funded by OECD governments to assess energy demand

in conjunction with pricing scenarios and resources availability. They assess

the threats and opportunities facing the global energy system based on

quantitative analysis of energy and climatic trends to create three global

energy demand scenarios: Current Policies, New Policies and 450 Scenario.

These scenarios are constructed in order to assess potential economic and

energy pathways which can therefore be used in setting government policies

to manage growth and environmental outcomes.

1. Current Policies – Status quo – assumes no new policies are added to the

current ones in place (mid-2011 at the time of writing).

2. New Policies – Partial reform – assumes recent government policy com-

mitments (i.e. Kyoto agreement and other global/country greenhouse

gas commitments) are implemented in a ‘cautious’ manner.

3. 450 Scenario – Full reform – assumes global compliance to the target to

limit long-term increase in the global mean temperature to two degrees

Celsius above pre-industrial levels.

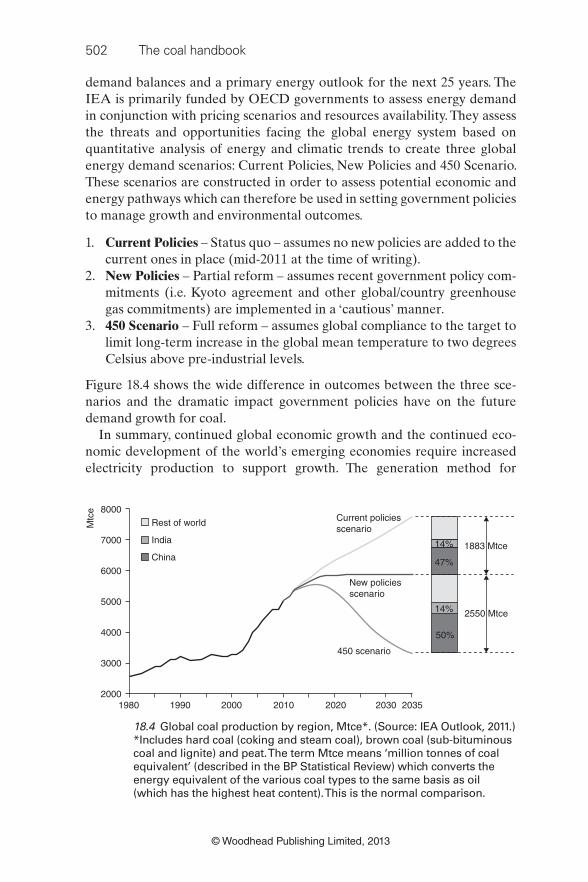

Figure 18.4 shows the wide difference in outcomes between the three sce-

narios and the dramatic impact government policies have on the future

demand growth for coal.

In summary, continued global economic growth and the continued eco-

nomic development of the world’s emerging economies require increased

electricity production to support growth. The generation method for

8000

Mtc

e

Rest of world Current policiesscenario

14%

47%

14%

50%

1883 Mtce

2550 Mtce

New policiesscenario

450 scenario

India

China

7000

6000

5000

4000

3000

20001980 1990 2000 2010 2020 2030 2035

18.4 Global coal production by region, Mtce*. ( Source : IEA Outlook, 2011 .)

*Includes hard coal (coking and steam coal), brown coal (sub-bituminous

coal and lignite) and peat. The term Mtce means ‘million tonnes of coal

equivalent’ (described in the BP Statistical Review) which converts the

energy equivalent of the various coal types to the same basis as oil

(which has the highest heat content). This is the normal comparison.

Future directions toward more effi cient and cleaner use of coal 503

© Woodhead Publishing Limited, 2013

electricity in all countries will be dependent upon the availability of fuel,

generation cost and reliability of electricity supply.

Under the Current Policies scenario the IEA predicts that global coal

production will increase by 1603 Mtce and 3037 Mtce by 2020 and 2035

respectively above the 2009 global coal consumption level of 4705 Mtce

(IEA, 2011). 3 To put this in perspective, global coal production increased by

5.3% per annum between 2003 and 2011, compared to the IEA’s Current

Policies scenario of 3.6% per annum growth between 2009 and 2035. Under

the Current Policies scenario the largest growth sector is steaming or thermal

coal due to increased demand from the power sector, particularly in India

and China. In the IEA’s New Policies scenario they still predict a signifi cant

increase in global coal consumption, increasing by 1128 Mtce and 1154 Mtce

by 2020 and 2035, respectively, above the 2009 levels. Regardless of which

IEA scenario, China and India represent the main areas for growth in coal

consumption accounting for 47% and 14% of the incremental demand.

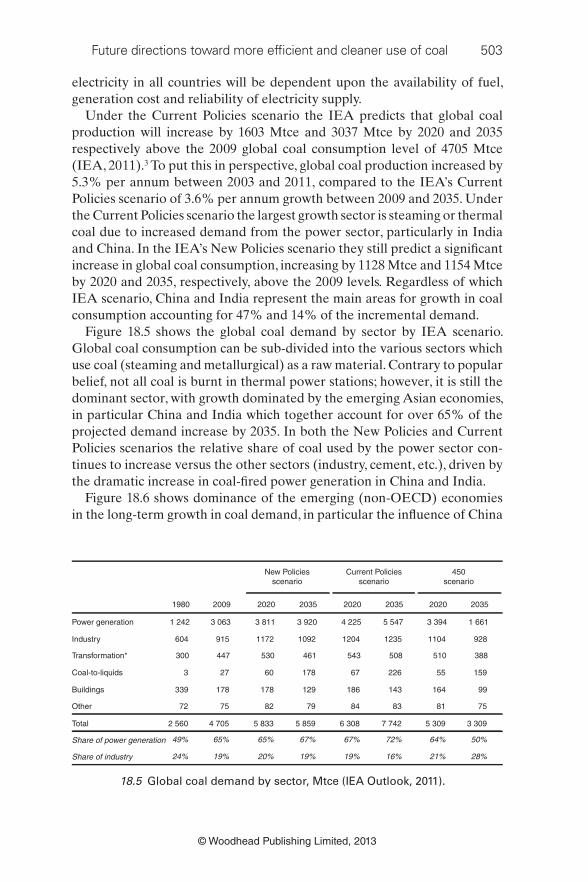

Figure 18.5 shows the global coal demand by sector by IEA scenario.

Global coal consumption can be sub-divided into the various sectors which

use coal (steaming and metallurgical) as a raw material. Contrary to popular

belief, not all coal is burnt in thermal power stations; however, it is still the

dominant sector, with growth dominated by the emerging Asian economies,

in particular China and India which together account for over 65% of the

projected demand increase by 2035. In both the New Policies and Current

Policies scenarios the relative share of coal used by the power sector con-

tinues to increase versus the other sectors (industry, cement, etc.), driven by

the dramatic increase in coal-fi red power generation in China and India.

Figure 18.6 shows dominance of the emerging (non-OECD) economies

in the long-term growth in coal demand, in particular the infl uence of China

Power generation 1 242

1980

Industry 604

Transformation* 300

Coal-to-liquids 3

Buildings 339

Other 72

3 063

2009

915

447

27

178

75

3 811

2020

New Policiesscenario

Current Policiesscenario

450scenario

1172

530

60

178

82

3 920

2035

1092

461

178

129

79

4 225

2020

1204

543

67

186

84

5 547

2035

1235

508

226

143

83

3 394

2020

1104

510

55

164

81

1 661

2035

928

388

159

99

75

Total 2 560

49%

4 705

65%

5 833

65%

5 859

67%

6 308

67%

7 742

72%

5 309

64%

3 309

50%Share of power generation

Share of industry 24% 19% 20% 19% 19% 16% 21% 28%

18.5 Global coal demand by sector, Mtce (IEA Outlook, 2011).

504 The coal handbook

© Woodhead Publishing Limited, 2013

and India. In comparison, in OECD countries the IEA predicts a slight

increase in the Current Polices and slight decrease in the New Policies sce-

narios as coal-fi red power generation is partially substituted by gas-fi red

and renewable (wind, solar) power generation.

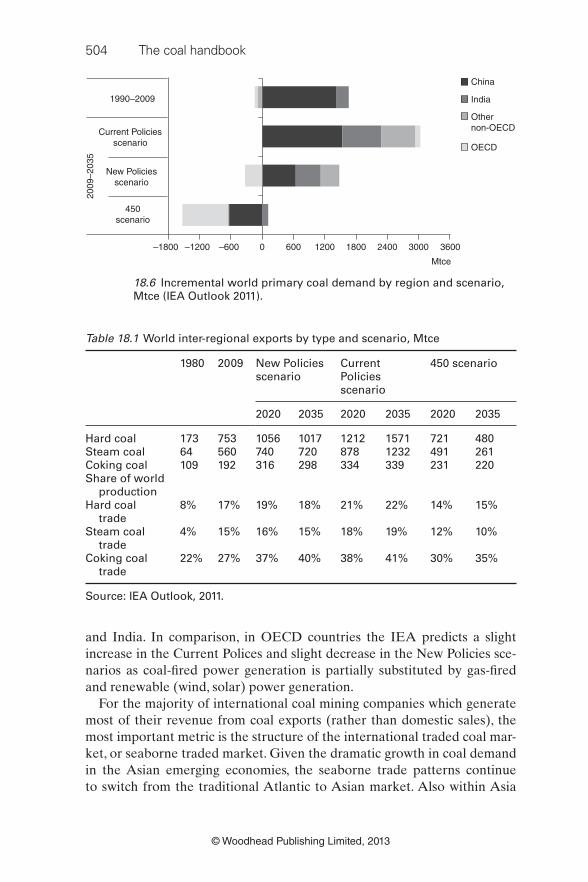

For the majority of international coal mining companies which generate

most of their revenue from coal exports (rather than domestic sales), the

most important metric is the structure of the international traded coal mar-

ket, or seaborne traded market. Given the dramatic growth in coal demand

in the Asian emerging economies, the seaborne trade patterns continue

to switch from the traditional Atlantic to Asian market. Also within Asia

Table 18.1 World inter-regional exports by type and scenario, Mtce

1980 2009 New Policies

scenario

Current

Policies

scenario

450 scenario

2020 2035 2020 2035 2020 2035

Hard coal 173 753 1056 1017 1212 1571 721 480

Steam coal 64 560 740 720 878 1232 491 261

Coking coal 109 192 316 298 334 339 231 220

Share of world

production

Hard coal

trade

8% 17% 19% 18% 21% 22% 14% 15%

Steam coal

trade

4% 15% 16% 15% 18% 19% 12% 10%

Coking coal

trade

22% 27% 37% 40% 38% 41% 30% 35%

Source : IEA Outlook, 2011.

1990–2009

Current Policiesscenario

New Policiesscenario

450scenario

–1800 –1200 –600 0 600 1200 1800 2400 3000 3600

Mtce

2009

–203

5China

India

Othernon-OECD

OECD

18.6 Incremental world primary coal demand by region and scenario,

Mtce (IEA Outlook 2011).

Future directions toward more effi cient and cleaner use of coal 505

© Woodhead Publishing Limited, 2013

the seaborne traded market continues to evolve from the traditional coal

import economies – Japan, Korea and Taiwan – towards China and India.

It is worth noting the Chinese net trade position has a signifi cant impact

on the global seaborne traded market, and minor changes in its domestic

coal production and consumption could have profound implications on the

international traded market – causing international coal prices to rally or

crash depending upon small changes in overall domestic consumption (in

2011 China imported 174 Mt of thermal/steaming coal, accounting for 22%

of the total thermal seaborne traded market). Table 18.1 shows the world’s

international coals traded by type and scenario.

18.3 Collaboration along the coal supply chain

There is little doubt that success and future growth in coal use will increas-

ingly depend upon the interaction of all participants in the coal supply chain

from resource to end user, including dealing with secondary ‘products’ gen-

erated from the main utilisation avenue, for example ash and slag products

that are still commonly regarded as waste or discards and also the asso-

ciated environmental management. This collaboration must also include

R&D, implementation and commercialisation.

The book ‘Clockspeed’ by Charles Fine, 4 introduces a unique combina-

tion of an analysis of the development speed of different industries, with

a ‘double helix’ description of the industry which trends toward vertical

H3

H2

Tim

e of

impl

emen

tatio

n

Low

(<

1 ye

ar)

Hig

h (>

10 y

ears

)

H1

S1Low (<$1M) Mid (>$20M) High (> $200M)

S2

Estimated return or ‘Leverage’ $M NPV

S3(Level of innovation)

Strategic Challenging

Cooperativeresearch centrese.g., AMIRA, etc

Short-term cooperativeResearch, ACARP (Australia)

CCRA (Canada) etc

Problem solving Core development

Collaborative researche.g. Major new process.Co-development

Competitive researche.g. specific company funded

strategic projectsUniversities, Institutes, e.g., CSIRO

18.7 Potential leverage from integrated R&D (an Australian example).

506 The coal handbook

© Woodhead Publishing Limited, 2013

integration, or its opposite. Understanding these trends and the pace of the

evolution of their ‘technological habitat’, and gaining value chain advantage

in their chosen niche, is vitally important to high technology start-ups in par-

ticular where success depends on operating at maximum ‘speed’. Applying

this analogy to the coal industry translates to the fact that successful imple-

mentation fi rst time around can provide an advantage over main competi-

tors. Failing to do so could switch this advantage from the particular coal

user to one of its main competitors, or even to a rival energy source.

An example of this is the Australian model shown in Fig 18.7. Valuable

short-term cooperative research and development, i.e., 1-3 years, is deliv-

ered through a so-called ACARP program (Australian Coal Association

Research Program) which is funded by a 5c/tonne levy on black coal exports.

Participating coal companies drive the research and the fund value is further

expanded by in-kind contributions from coal producers, research organisa-

tions and industry stakeholders which probably more than trebles the levy

value. Longer term R&D can also be collaborative via cooperative research

centres (CRCs) which draw together several research providers to take on

more challenging and higher cost projects. The direction of these is often

driven by industry-wide priorities, for example safety driven major projects

such as long-wall face automation, together with prioritised research follow-

ing a strategic direction of the individual participating companies. This latter

infl uence will have generated some competitive research projects; as well as

larger-scale high cost, high leverage collaborative projects many as joint ven-

tures with other non-competing organisations.

A recent article by Henry Chesbrough and Andrew Garman 5 explains a

strategic concept that can potentially reduce the costs of R&D to coal industry

participants without sacrifi cing tomorrow’s projected growth. The argument is

raised that companies which invest in their innovative capabilities during tough

economic times are those that fare best when growth returns. This concept would

be well suited to the major coal industry players because of their R&D invest-

ment already made both internally externally and the strong, albeit often poorly

coordinated, R&D network currently in place. The main challenge is how to

ensure this has the right impact throughout the whole of the value chain.

The authors call the concept the ‘Inside-out’ process and it involves placing

some of the ongoing internal projects outside the company, thereby reducing

R&D costs without relinquishing related growth opportunities. Each project

will then take a unique pathway to its most strategically valuable outcome. The

process also facilitates decision-making as to which projects should remain

internal, which should be outsourced and which could be converted into

‘spin-off’ ventures whereby a company retains or acquires an equity position.

Translated into supply chain terms, this could mean that resource companies

with the common goal of maintaining a leading position will continuously seek

solutions to integrate their operations with those of their stakeholders and cus-

tomers and reduce their dependence on line managers along the chain.

© W

oodhead P

ublis

hin

g L

imite

d, 2

013

18.8 The value chain approach to integrated R&D.

© W

oodhead P

ublis

hin

g L

imite

d, 2

013

18.9 Looking for ‘Green Opportunities’ in collaboration with a customer.

© W

oodhead P

ublis

hin

g L

imite

d, 2

013

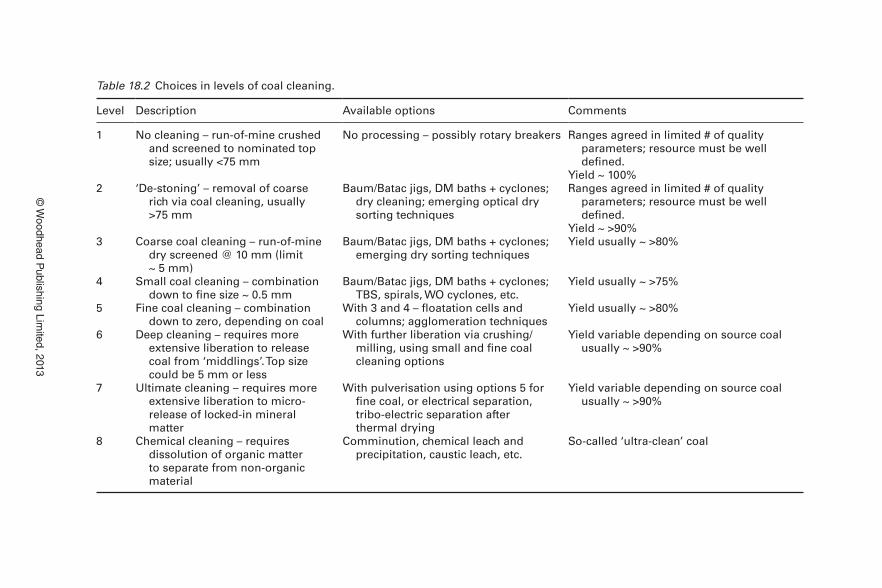

Table 18.2 Choices in levels of coal cleaning.

Level Description Available options Comments

1 No cleaning – run-of-mine crushed

and screened to nominated top

size; usually <75 mm

No processing – possibly rotary breakers Ranges agreed in limited # of quality

parameters; resource must be well

defi ned.

Yield ~ 100%

2 ‘De-stoning’ – removal of coarse

rich via coal cleaning, usually

>75 mm

Baum/Batac jigs, DM baths + cyclones;

dry cleaning; emerging optical dry

sorting techniques

Ranges agreed in limited # of quality

parameters; resource must be well

defi ned.

Yield ~ >90%

3 Coarse coal cleaning – run-of-mine

dry screened @ 10 mm (limit

~ 5 mm)

Baum/Batac jigs, DM baths + cyclones;

emerging dry sorting techniques

Yield usually ~ >80%

4 Small coal cleaning – combination

down to fi ne size ~ 0.5 mm

Baum/Batac jigs, DM baths + cyclones;

TBS, spirals, WO cyclones, etc.

Yield usually ~ >75%

5 Fine coal cleaning – combination

down to zero, depending on coal

With 3 and 4 – fl oatation cells and

columns; agglomeration techniques

Yield usually ~ >80%

6 Deep cleaning – requires more

extensive liberation to release

coal from ‘middlings’. Top size

could be 5 mm or less

With further liberation via crushing/

milling, using small and fi ne coal

cleaning options

Yield variable depending on source coal

usually ~ >90%

7 Ultimate cleaning – requires more

extensive liberation to micro-

release of locked-in mineral

matter

With pulverisation using options 5 for

fi ne coal, or electrical separation,

tribo-electric separation after

thermal drying

Yield variable depending on source coal

usually ~ >90%

8 Chemical cleaning – requires

dissolution of organic matter

to separate from non-organic

material

Comminution, chemical leach and

precipitation, caustic leach, etc.

So-called ‘ultra-clean’ coal

510 The coal handbook

© Woodhead Publishing Limited, 2013

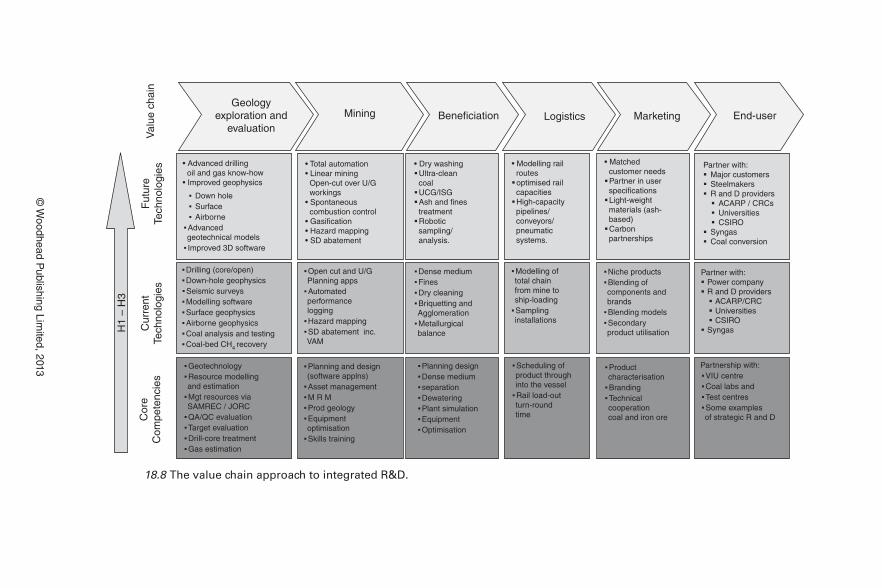

Figure 18.8 illustrates the supply chain linkages between current tech-

nologies, aligned with current competencies and thus available to a com-

pany, and the future technologies identifi ed as being the strategic direction.

The future promises greater cooperation whereby the mining approach and

degree of benefi ciation are determined by the best outcome for the entire

supply chain, i.e., selective mining and/or coal cleaning involving the removal

of entities not regarded as useful by the user are optimised; and utilisation

considers all potential value elements of the coal as supplied.

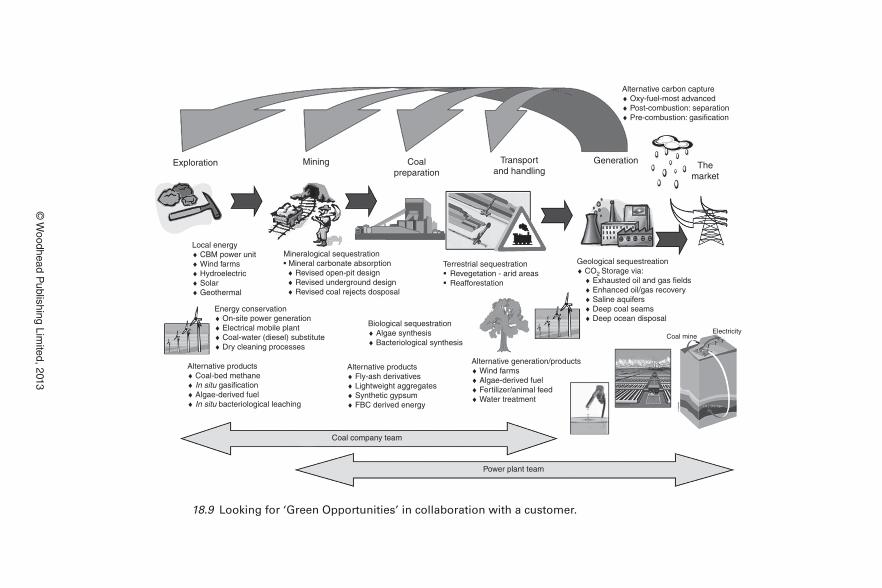

Figure 18.9 illustrates some examples where coal producer and power

producer could collaborate to progress on carbon issues, but also improve

the cost and overall performance with the coal source. An ultimate solution

might be to conduct all the steps leading to a value product in situ, such as

integrated mining and benefi ciation, or even underground coal seam gas-

ifi cation; and perhaps later along the chain creating a ‘carbon concentrate’

such as micronised, refi ned coal; or processes for removing non-coal par-

ticles from pulverised fuel at a power plant using tribo-electric separation.

18.4 Developments in mining and processing technologies

Mining companies are going to continue to explore all economical coal

resources. As technology progresses, coal resources hitherto regarded as

being un-minable or uneconomic could become feasible candidates for

development. At some future date, concepts like below sea-level mining of

coal, deep coal seams and sub-zero temperature mining at the poles may

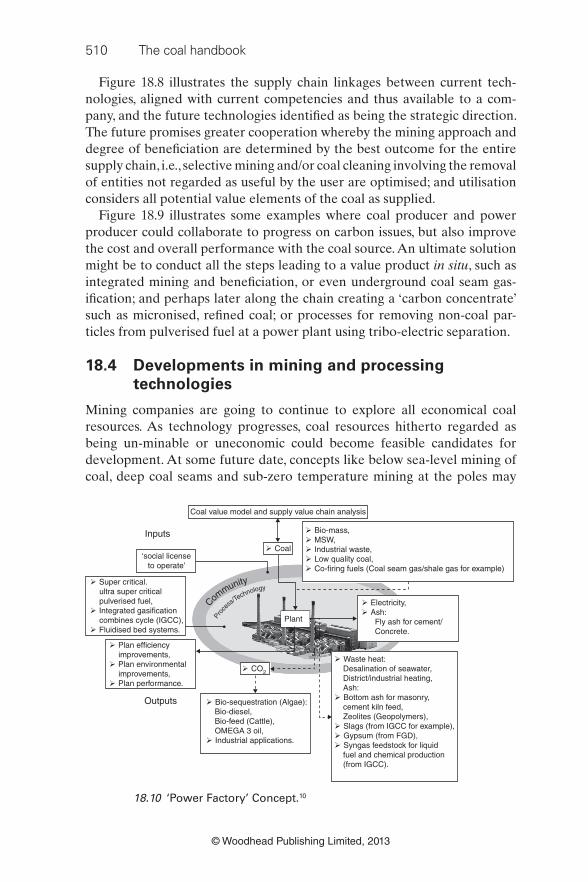

18.10 ‘Power Factory’ Concept. 10

Future directions toward more effi cient and cleaner use of coal 511

© Woodhead Publishing Limited, 2013

come to fruition if technologies are developed to include things like in situ gasifi cation and/or liquefaction of coal, i.e., ‘ in situ ’ extraction becomes prac-

tical. On the other hand, without expansion of these technologies, the coal

mining industry as we now know it may have only another century of life.

Then what is next? Factory mining: bigger machines, fewer people, more

automation? Over the next 10–20 years machines will undoubtedly continue

to become larger; more coal will be mined from the surface, processing and

handling units will get even larger. Individual coal mines will produce between

10 and 30 million tonnes per annum. Small coal mines (<5 Mt/a) will no lon-

ger be economically or technologically feasible. Safety and economics will still

drive the market but environmental constraints will need to be fully met.

Research will probably be driven by organisations such a CSIRO,

(Commonwealth Scientifi c and Industrial Research Organization), Australia’s

national science agency, which has led the way to the advancement of mining

and benefi ciation technology. Researchers at CSIRO are developing state-of-

the-art sensing, control, and planning systems that will enable the automation

of mining activities – primarily excavation, coal benefi ciation and material

handling. Successful development and deployment of such new technology

will allow surface and underground mining to be carried out more effi ciently,

far more safely, and with less human intervention than is currently required.

Automation will ultimately enable mining operations to proceed in

remote and harsh environments. The same is true for the preparation of the

coal for the various market users. 6 Artifi cial intelligence is being built into

coal processing plants, giving controlling systems the capacity to monitor

and adjust operations ‘intuitively’ to improve operational effi ciencies. The

technology, still under development, will allow all computer-controlled

functions in a processing plant to measure, in real time, operating perfor-

mance against predetermined optimums. 7 The extent to which the coal can

be cleaned has always been subjected to economics and effi ciency.

Manufacturers of equipment will continue to develop robust control systems

that will both enhance and in some cases eliminate the need for human opera-

tors. The relative price of coal as a fuel has not changed for 30 years. The issue of

it being a climate change fuel will continue to grow as an issue. But the reality is

that coal, as a fuel, is very abundant, available and relatively inexpensive and it

will almost certainly be used as a major fuel source for the next century.

18.5 Developments in coal utilisation for electricity generation

So how do we think about electricity generation differently? It is arguable

that since the inception of the Electricity Generation and Supply Industry

in 1881, 8 this industry has been very staid and on the whole very focused on

individual plants that saw electricity as a sole output from a single or at worst

two fuels (usually a primary fuel and a secondary fuel) as inputs. The aim was

512 The coal handbook

© Woodhead Publishing Limited, 2013

to keep the plants as simple as possible; however, environmental concerns

have driven some signifi cant changes in the nature of the plants and also

changes in some fuel inputs such as co-fi ring with fuels such as biomass.

The focus on keeping plants simple whilst growing in size has been driven

by the nature of the product. Electricity can be considered the ultimate ‘just-

in-time’ product that cannot be stored, and yet the majority of end users

expect it to be available at the fl ick of a switch. The fact is that this clean,

safe and cheap source of effi cient and fl exible energy has become the basis

of human development over the twentieth century and probably will be for

many years into the future.

At least in the Western world and now in the developing world, electric-

ity is seen as a fundamental element of modern life. This critical role has on

the one hand made electricity both an unseen staple of life and also a very

politically sensitive matter. When electricity goes out, governments react. This

unique place of electricity in the developed world poses a dichotomy when

issues such as climate change come into play. Concern over climate change has

driven objection specifi cally to coal-fi red electricity generation whilst at the

same time the electricity produced from coal is considered essential. The fact

remains that coal fuels 40.33% 9 of the world’s electricity and will continue to

play a signifi cant role in electricity generation for the foreseeable future.

So, the real issue is how we can better utilise the great energy resource

that coal represents to cost effectively and responsibly generate electricity

for the duration. Putting aside the issue of climate change, there are other

issues that will drive changes in coal utilisation for the generation of electric-

ity. Such issues include the disposal of ash, increasing need to utilise lower

quality coals, improving effi ciency of coal utilisation not only in the plant

but across the coal supply chain and improvements in the size and nature

of the environmental ‘footprint’ also right across the supply chain. In addi-

tion, the issue of energy sustainability should drive the maximisation of the

valuation of the coal resource in terms of not only electricity generation, but

what range of products can be derived from coal along with electricity.

One concept that may illustrate how we can think about coal utilisation

in electricity generation in a different manner is to consider electricity gen-

eration in manufacturing terms and this is refl ected in the ‘Power Factory’

concept. In this model, we consider Inputs, Process (the power plant) and

Outputs. The ‘Power Factory’ concept leads to considering the whole supply

chain both upstream of the power plant and downstream of the plant. The

concept naturally requires that the power plant can no longer be considered

in isolation; rather the generation of electricity must be considered in asso-

ciation with other ‘processes’ that can add value to both the generation of

electricity but may also maximise the value in the original energy sources

such as coal as well as offer other benefi ts such as combustion product utili-

sation and general environmental improvements.

Future directions toward more effi cient and cleaner use of coal 513

© Woodhead Publishing Limited, 2013

So, if we are to ensure a future for coal in the generation of electricity whilst

at the same time playing a key role in meeting the world’s ever-growing need for

energy, we must think about how we use coal to gain the best overall outcomes.

In addition, taking new approaches to coal utilisation in power genera-

tion also offers an opportunity to successfully make use of lower grade or

diffi cult coals thus adding value to the world’s coal resources.

18.6 Developments in coal utilisation for iron ore reduction

Forecasts for long-term use of coal in the steel industry are extremely diffi cult

because the combination of several uncertain factors, such as growth of popu-

lation, development and use of new/alternative materials and energy sources,

development of existing and new metallurgical technologies and, last but not

least, political and social changes, will strongly affect the picture of the future.

Growth in demand for steel from about 1.4 billion tons in 2011 to 2.3–2.7

billion tons by 2050 is expected. 11 The ratio of oxygen/electric steel (it means

BF-BOF and scrap-EAF routes, see chapter 12) is assumed to switch from

70:30 today to 40:60% in 2050 . 12 That would mean that the oxygen steel pro-

duction mainly using blast furnace iron-making remains more or less at the

same level. The amount and structure/types of energy and reducing agents

for iron ore reduction are key factors that will shape the future of the steel

industry. The dominant energy inputs in an integrated steelworks today are

coal/coke and some heavy oil, natural gas and other hydrocarbons.

A current modern steelworks is a highly optimised system in terms of con-

sumption of energy and reducing agents. The blast furnace operates 5% away

from the thermodynamics limit and the whole mill has a potential of energy

savings of only about 10%. 13 Energy consumption of best performing inte-

grated steel works (BF-BOF route) makes up 17 GJ/t crude steel, 16 GJ/t of

which is related to coal and 0.9 GJ/t to electricity. In a scrap-EAF route, the

best results correspond to 3.5 GJ/t of hot rolled product, of which 1.6 GJ/t is

related to electricity consumption, 0.6 GJ/t of fossil energy (coal and natu-

ral gas) and 0.3 GJ/t of energy for hot rolling and 1 GJ/t natural gas for the

reheating furnace. 14 At the same time, the worst performers are at the level of

50 and 30 GJ/t crude steel for the BF-BOF and the EAF routes respectively. 7

Improvement of performance of all the other steelworks to the level of the

current best performing ones offers an enormous potential for energy saving.

Environmental challenges facing the steel industry require very large cuts

in CO 2 emissions; even today’s best metallurgical technologies are not ‘clean’

enough and radical improvement will be required to meet emerging mandatory

targets. CCS as a tool for mitigation CO 2 emissions in the steel industry could be

deployed in the future for existing and new iron-making processes, if still open,

technical, economic and social problems related to the CCS will be solved.

514 The coal handbook

© Woodhead Publishing Limited, 2013

Another way to reduce the CO 2 emissions is related to a change in the struc-

ture of energy sources. Coal used for iron ore reduction can be replaced by

hydrogen, electricity or biomass. Industrial implementation of these energy

sources depends on their sustainability, availability and costs, i.e. sustainable

plantations, processing and use of biomass, avoiding confl icts between energetic

use of biomass and food security, use of CO 2 -lean electricity, development of

technically and cost-acceptable methods of electrolysis, etc. On the other hand,

new iron-making technologies still have to be developed; existing ones enable

only partial replacement of coal/coke by the above-mentioned sources.

Looking at the existing coke, iron and steel making technologies, further

increase in carbon use effi ciency and cost optimisation is needed. It is com-

monly recognised that until now, coke quality produced from coking coals

with well-defi ned properties has been a prerequisite for high effi ciency blast

furnace operation. An increasing demand on coke (nearly 600 Mt of coke on

dry basis was produced in 2010) and depletion of resources of high quality

coals leads to frequently changing coal blends and drives up the price.

The strategy on coke quality should be shifted from maximising to optimis-

ing its properties. Optimum quality in general means coke that is adequate for

needs considering both costs and availability. Furthermore, blast furnace oper-

ation with low coke rate, high PCI rate (>250 kg/THM) and other injectants

causes a change in coke quality requirements; some of its functions become

less important (heat source, reducing agent), other tasks (maintenance of gas

permeability) become decisive. Solution loss reaction, alkali and high tem-

perature attack infl uence the coke degradation behaviour strongly. 15

Standard characteristics of coke quality and test methods are therefore

not suffi cient to simulate real conditions in a modern blast furnace. They

provide limited assessment of coke properties under limited reacting condi-

tions and should be complemented with new ones.

Iron ore – carbon agglomerates (self-reducing pellets, briquettes or com-

posites) with embedded coal or other carbonaceous materials might be used

in the blast furnace for decreasing the carbon consumption and in direct

reduction processes for improving their performance and productivity.

Use of a broader palette of coals and cokes enables the further reduction

of costs. Examples include the effi cient use of nut coke and anthracite in

the blast furnace, the briquetting and hence use of fi ne coals for injection in

Corex/Finex smelting reduction technologies.

18.7 Development of low emissions coal-based power generation technologies

World coal consumption is projected to grow by approximately 55% between

2007 and 2035. 16 The non-OECD Asian nations (predominantly China and

India) are expected to account for 95% of this projected growth, with China

Future directions toward more effi cient and cleaner use of coal 515

© Woodhead Publishing Limited, 2013

to increase its coal-fi red electricity generation capacity from approximately

500 GW (2007) to approximately 1250 GW by 2035.

An important factor in some OECD countries (particularly the US and

Australia) is the need for new plant to replace ageing installations which

have relatively low effi ciencies and are expected to be unattractive for ret-

rofi t of CO 2 capture technologies to meet likely future greenhouse-gas emis-

sions requirements.

The research challenges needed to advance the development of low emis-

sions coal-based power generation technologies are clearly associated with

increasing effi ciencies and reducing greenhouse gas emissions at large scale

and low cost. In the face of strongly increasing world coal use, new tech-

nologies will be needed in the future to increase the effi ciency of coal-fi red

power generation signifi cantly above the levels of current best practice and

to facilitate the capture of CO 2 for long-term storage.

18.7.1 Effi ciency of coal-fi red power plants

The average effi ciency of coal-fi red plants globally is currently only about

28% (higher heating value, HHV ) with the most effi cient ultra-supercritical

steam plants and new integrated gasifi cation combined cycle (IGCC) dem-

onstration technologies achieving about 45%. 17 The current large worldwide

growth in new power generation capacity provides an important opportunity

in both developing and developed nations for development and deployment

of advanced, high effi ciency power generation technologies which can provide

a suitable technology platform for further effi ciency and cost improvements

to meet the requirements for increasing levels of CO 2 emissions abatement.

Repowering existing coal-fi red plants, where possible, to improve their

effi ciency, as well as installation of new and more effi cient plant, will pro-

vide signifi cant reductions in CO 2 emissions. However, to achieve very high

levels of CO 2 emissions reduction from fossil fuel-based power generation

technologies, it will be increasingly important to have in place conversion

technologies with the highest possible effi ciencies capable of reducing the

amount of CO 2 that must eventually be captured and stored. Due to the sig-

nifi cant energy demands and costs associated with CO 2 capture and storage

(CCS), deploying the most effi cient plant possible is a critical prerequisite to

enable these plants to be capable of being fi tted with CO 2 capture technolo-

gies, either from new or as a staged retrofi t in the future.

There are several key research areas associated with coal utilisation per-

formance and gas processing and separation which will need to be pursued to

support some of the most promising technology development pathways in the

areas of high effi ciency, low emissions coal technologies. Particular emphasis is

required on coal gasifi cation performance issues affecting coal selection, gas-

ifi er design and reliability and important downstream syngas conversion and

516 The coal handbook

© Woodhead Publishing Limited, 2013

gas separation technologies necessary to facilitate CO 2 capture and hydrogen

production at a scale and cost acceptable to the power industry.

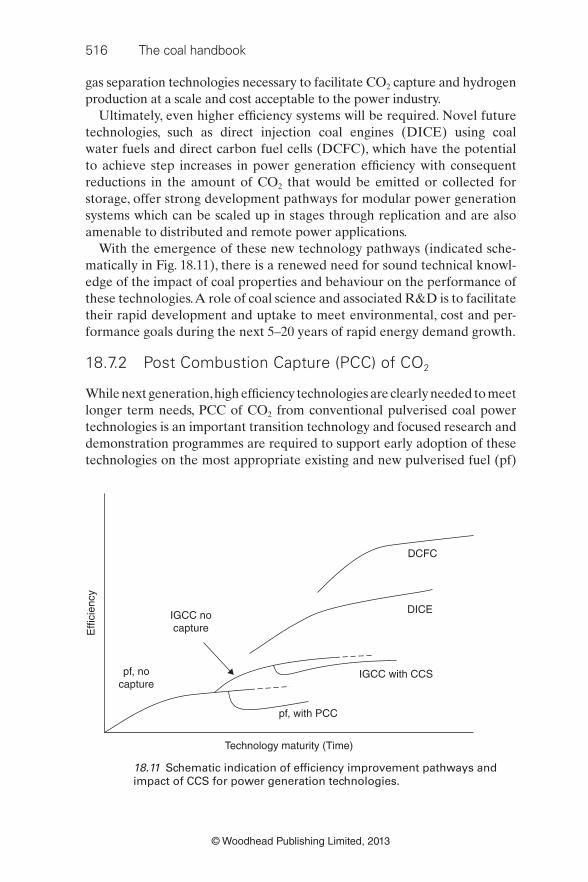

Ultimately, even higher effi ciency systems will be required. Novel future

technologies, such as direct injection coal engines (DICE) using coal

water fuels and direct carbon fuel cells (DCFC), which have the potential

to achieve step increases in power generation effi ciency with consequent

reductions in the amount of CO 2 that would be emitted or collected for

storage, offer strong development pathways for modular power generation

systems which can be scaled up in stages through replication and are also

amenable to distributed and remote power applications.

With the emergence of these new technology pathways (indicated sche-

matically in Fig. 18.11), there is a renewed need for sound technical knowl-

edge of the impact of coal properties and behaviour on the performance of

these technologies. A role of coal science and associated R&D is to facilitate

their rapid development and uptake to meet environmental, cost and per-

formance goals during the next 5–20 years of rapid energy demand growth.

18.7.2 Post Combustion Capture (PCC) of CO 2

While next generation, high effi ciency technologies are clearly needed to meet

longer term needs, PCC of CO 2 from conventional pulverised coal power

technologies is an important transition technology and focused research and

demonstration programmes are required to support early adoption of these

technologies on the most appropriate existing and new pulverised fuel (pf)

IGCC nocapture

IGCC with CCS

DICE

DCFC

pf, nocapture

pf, with PCC

Technology maturity (Time)

Effi

cien

cy

18.11 Schematic indication of effi ciency improvement pathways and

impact of CCS for power generation technologies.

Future directions toward more effi cient and cleaner use of coal 517

© Woodhead Publishing Limited, 2013

plant. While solvent-based technologies for CO 2 capture are well established

in the chemical and process industries, the key challenges associated with PCC

technology are associated with reducing the capital cost, energy effi ciency

penalties and potential environmental impacts of these large-scale solvent

based systems. For current systems, the effi ciency penalties associated with

PCC on conventional plant can be up to 10 percentage points and this major

loss of effi ciency (and capacity) represents the most challenging aspect for

retrofi t and new build applications of this technology. On the most modern

pf plants, which already have high levels of fl ue gas treatment, coal property

impacts on PCC systems are relatively minor and much of the required R&D

is focused on developing improved solvents and reducing the energy require-

ments of CO 2 recovery. However, many existing coal-fi red plants, with little

or no fl ue gas treatment, face additional constraints as coal specifi c contami-

nants can interact deleteriously with the most common solvents, and further

work is required to develop alternative materials and processes.

18.7.3 Integrated gasifi cation combined cycle (IGCC): A high-effi ciency platform for carbon capture and storage (CCS)

IGCC technology presently achieves similar effi ciency to latest PC technol-

ogy (~40–45% HHV basis) but at a slightly higher capital cost. However,

substantial improvements in IGCC effi ciency (~ + 8 percentage points)

along with signifi cant reductions in capital cost are projected through new

and improved process blocks now under development internationally.

As for all power technologies, the introduction of CCS decreases the

overall effi ciency and increases costs of power generation. For IGCC sys-

tems, effi ciency losses with currently-available (pre-combustion) CO 2 cap-

ture technologies are expected to be approximately 6–8% points and capital

costs are likely to increase by up to 40%. Carbon capture technologies for

IGCC applications are still early in their learning curve; therefore, as with

the main IGCC plant, signifi cant improvements to the process components

can be envisaged and development of these will substantially reduce the

cost and effi ciency penalties associated with CCS.

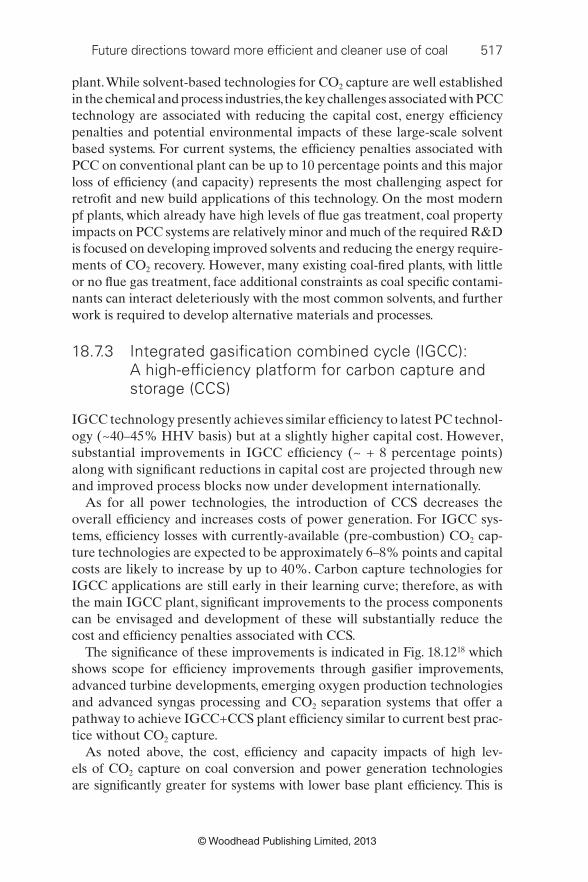

The signifi cance of these improvements is indicated in Fig. 18.12 18 which

shows scope for effi ciency improvements through gasifi er improvements,

advanced turbine developments, emerging oxygen production technologies

and advanced syngas processing and CO 2 separation systems that offer a

pathway to achieve IGCC+CCS plant effi ciency similar to current best prac-

tice without CO 2 capture.

As noted above, the cost, effi ciency and capacity impacts of high lev-

els of CO 2 capture on coal conversion and power generation technologies

are signifi cantly greater for systems with lower base plant effi ciency. This is

518 The coal handbook

© Woodhead Publishing Limited, 2013

essentially because for a lower effi ciency plant, a greater amount of CO 2 must

be captured and stored per unit of coal consumed, or per MWh of electricity

produced. It will therefore become increasingly important that technology

improvements such as those indicated in Fig. 18.12, and which are the subject

of current R&D programmes around the world, are available as soon as possi-

ble to support the deployment of viable low emissions coal technologies capa-

ble of operating within practical commercial and environment constraints.

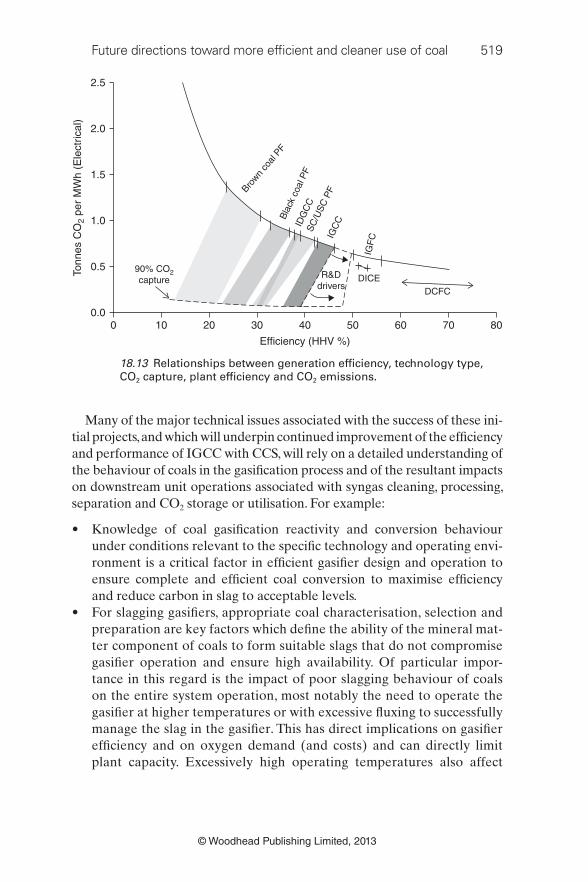

The schematic diagram shown in Fig. 18.13 provides an illustration of the

impact of CO 2 capture on the effi ciency and capacity of combustion and IGCC-

based power generation technologies. The upper line represents the CO 2 emis-

sions as a function of effi ciency for a reference coal composition for a range of

technologies. This diagram illustrates very clearly the strong drivers for a high

effi ciency underpinning technology base and also the value of R&D to decrease

the effi ciency penalty associated with CO 2 capture from these systems.

As IGCC and IGCC-CCS technologies begin to be implemented, initially

at the commercial demonstration scale, a critical factor in the success of these

projects, and in the subsequent wider deployment, will be stakeholder con-

fi dence. It is important that governments, technology developers, vendors,

operators and the community can see that such technologies can operate

reliably at the required scale with high availability, safety and environmen-

tal performance while meeting the necessary CO 2 emissions requirements.

Ongoing research is therefore required to continue to support development

and deployment of large-scale IGCC and IGCC-CCS systems.

Baseline(no CCS)

30

32

34

Net

pla

nt e

ffici

ency

(%

HH

V)

36

38

Full (90%capture)

AdvancedG-class GT

Cumulative efficiency improvement

ITM Oxygen CO2 slurryfeed

Advancedsyngas

processes

18.12 Examples of technology development initiatives being developed

to decrease cost and effi ciency penalties associated with CO 2 capture

from IGCC systems (after H. Jaeger, 2010).

Future directions toward more effi cient and cleaner use of coal 519

© Woodhead Publishing Limited, 2013

Many of the major technical issues associated with the success of these ini-

tial projects, and which will underpin continued improvement of the effi ciency

and performance of IGCC with CCS, will rely on a detailed understanding of

the behaviour of coals in the gasifi cation process and of the resultant impacts

on downstream unit operations associated with syngas cleaning, processing,

separation and CO 2 storage or utilisation. For example:

Knowledge of coal gasifi cation reactivity and conversion behaviour •

under conditions relevant to the specifi c technology and operating envi-

ronment is a critical factor in effi cient gasifi er design and operation to

ensure complete and effi cient coal conversion to maximise effi ciency

and reduce carbon in slag to acceptable levels.

For slagging gasifi ers, appropriate coal characterisation, selection and •

preparation are key factors which defi ne the ability of the mineral mat-

ter component of coals to form suitable slags that do not compromise

gasifi er operation and ensure high availability. Of particular impor-

tance in this regard is the impact of poor slagging behaviour of coals

on the entire system operation, most notably the need to operate the

gasifi er at higher temperatures or with excessive fl uxing to successfully

manage the slag in the gasifi er. This has direct implications on gasifi er

effi ciency and on oxygen demand (and costs) and can directly limit

plant capacity. Excessively high operating temperatures also affect

00.0

0.5 90% CO2capture

DCFCDICER&D

drivers

IGF

CIGC

CIDG

CC

Bla

ck c

oal P

F

Brown

coal

PF

SC

/US

C P

F

1.0

1.5

Tonn

es C

O2

per

MW

h (E

lect

rical

)

2.0

2.5

10 20 30 40

Efficiency (HHV %)

50 60 70 80

18.13 Relationships between generation effi ciency, technology type,

CO 2 capture, plant effi ciency and CO 2 emissions.

520 The coal handbook

© Woodhead Publishing Limited, 2013

plant life and maintenance requirements – both within the gasifi er and

in downstream gas cooling and cleaning systems.

In any system where coal-derived syngas is used as the basis for power •

generation, chemicals production, or in the manufacture of liquid fuels, the

syngas must be cleaned to standards acceptable by the downstream plant.

In coal gasifi cation derived systems the contaminants include fi ne parti-

cles of fl y ash, gaseous species containing sulphur, chlorine, fl uorine, alkali

metals and trace elements. Coal properties and gasifi cation behaviour

under the relevant process conditions profoundly affect syngas composi-

tion which specifi es development criteria for improved and breakthrough

technologies to reduce the costs and energy penalties associated with syn-

gas cleaning and processing, gas separation and CO 2 capture systems.

Coal impacts on gasifi cation performance

Conditions inside an entrained fl ow gasifi er are extreme: pressures are high

(20–40 bar or sometimes greater) and temperatures are high (fl ame temper-

atures often over 1800 K). The ratio of oxygen to fuel is signifi cantly lower

than those used in coal combustion technologies, and the mineral matter in

the coal is required to melt and fl ow out of the gasifi er continuously. Steam

is sometimes included in the feed streams to the gasifi er, and some gasifi ers

are designed to feed coal as a coal-water slurry.

These aspects of gasifi cation mean that the extensive literature and under-

standing of coal performance in pf boilers has little direct application to

understanding and predicting coal performance under gasifi cation conditions.

Results of ‘standard’ combustion tests do not translate to gasifi cation perfor-

mance – new approaches, facilities, techniques, and knowledge are required.

A striking point to emerge from analysis of coal performance in the com-

plex environment in these high pressure, high temperature reaction systems

is the potential impact of relatively fundamental coal properties on many

of the process operations comprising the IGCC system. Even seemingly

simple factors such as inherent moisture, mineral matter composition, high

temperature volatile yield, char reactivity and structure, grinding behav-

iour, slurrying characteristics, sulphur content, etc. can become particularly

important as they may create issues that cannot be accommodated through

simple changes to operating conditions. Such issues therefore become lim-

iting factors for the fi xed plant design (e.g. size of oxygen plant, gasifi er,

syngas cooler, etc.). Managing these and other coal-related issues can incur

signifi cant costs and/or operating boundaries that can seriously affect plant

capacity, effi ciency and performance.

To allow practical and reliable application of a sound fundamental under-

standing of gasifi cation science to the solving of real industrial problems,

knowledge of coal pyrolysis, char formation, char reactivity, slag formation

Future directions toward more effi cient and cleaner use of coal 521

© Woodhead Publishing Limited, 2013

and fl ow, and coal gasifi cation behaviour needs to be integrated in a form that

is applicable to a range of gasifi cation technologies and, eventually, gasifi ca-

tion-based energy systems. Fundamental, experimental gasifi cation research

needs to be undertaken in parallel with the development of detailed coal reac-

tion and conversion models designed to allow more widespread application

of the outcomes through, for example, relevant gasifer and integrated process

models of the entire coal conversion, slag handling, syngas processing and gas

separation systems. This can be done effectively only through close collabora-

tion of researchers, industrial technology developers, vendors and operators.

From refi neries to power generation: advanced syngas processing for high effi ciency CCS

In the chemicals and refi nery industries, coal gasifi cation, and capture of

CO 2 from syngas is commercially mature. R&D strategies to support the

rapid development and application of advanced syngas processing and gas

separation technologies in the power sector will require a combination of

fundamental materials development and testing programmes, laboratory

scale experiments, modelling projects, larger ‘research gasifi er’ scale mea-

surements and screening tests. This work would be complemented with

appropriately targeted pilot plant and slipstream tests utilising syngas slip-

streams such as those available from a number of international IGCC com-

mercial, demonstration and research projects. An example of a commercial

facility that currently operates in this way is the Puertollano demonstration

IGCC project in Spain which has a slipstream of up to approximately 2% of

the syngas available for advanced technology development projects such as

gas cleaning, shift and gas separation concept development, materials test-

ing, etc. The Polk Power IGCC plant in Tampa USA is also fi tting a major

syngas treatment and CO 2 capture system to support R&D programmes

aimed at reducing the costs and improving the effi ciency and reliability of

IGCC-CCS technologies. The US Department of Energy’s National Carbon

Capture Center has established a syngas slipstream facility to perform

extended testing of a range of pre-combustion CO 2 capture technologies

using commercially realistic coal-derived syngas streams. 19

Improved technology components and concepts fi tting within the IGCC

process fl ow sheet that have been identifi ed to date, and in some cases tested

using simulated syngas environments at laboratory scale, include:

new water gas shift catalysts optimised for coal syngas and suitable for use •

with membrane reactor systems at higher temperatures (up to 600°C);

integrated high temperature (~ 600°C) dry syngas cleaning systems; •

trace element capture integrated with high temperature syngas cleaning; •

metal and ceramic membrane based hydrogen/CO • 2 separation

technologies;

522 The coal handbook

© Woodhead Publishing Limited, 2013

integrated water gas-shift/metal membrane catalytic reactor concepts •

capable of enhancing hydrogen production and separation at high

temperatures;

ion transport membrane air separation technologies have been in devel-•

opment for almost two decades and are now nearing commercial avail-

ability at tonnage scales.

Further opportunities to signifi cantly increase effi ciencies are expected as

syngas and hydrogen-based fuel cells reach commercial availability. While

these are unlikely to be available at the scale and reliability required for

large-scale power generation within the next 10–15 years they provide an

attractive development pathway for the core, high effi ciency technology

platforms that are being developed and demonstrated today.

18.8 Integrated coal complexes and polygeneration

This section introduces the idea of an integrated coal complex, a concept

which many believe has great potential especially in the growth areas of

China and India. This is a subject that has over the years captured the

imagination of many coal technologists, including Professor David Horsfall.

Originally from the UK, David moved to South Africa in the late 1960s and

became very infl uential in the development of the coal export business that

added enormous value to the country’s economy. David fi rst introduced a

concept which he called COALCOM (an acronym for coal, coke, oil and

megawatts) in the mid-1970s. At the time, South Africa was striving to over-

come the threat of oil import sanctions and the Sasol Company was produc-

ing oil and chemicals from coal via a combination of Lurgi gasifi ers and the

Fischer Tropsch process. He proposed taking this one step further and incor-

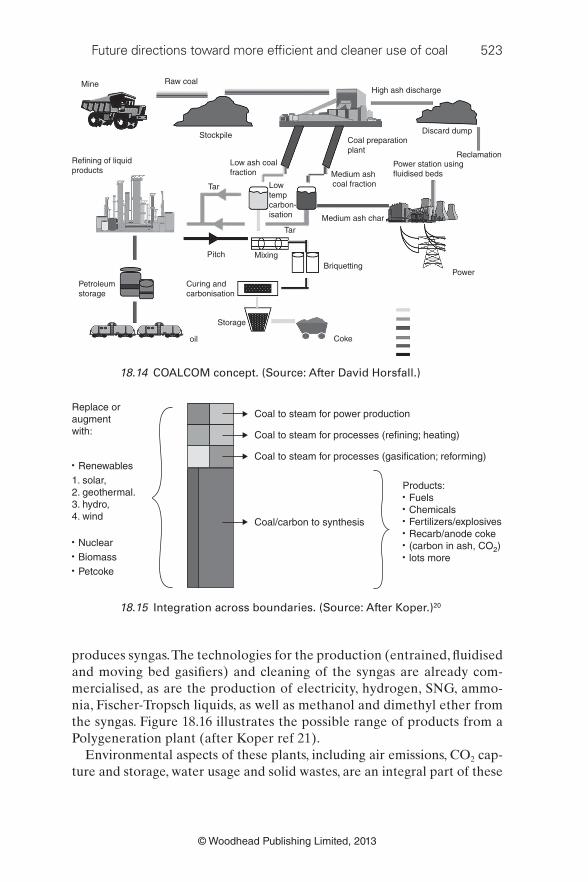

porating a metallurgical element to the complex. The diagram in Fig. 18.14

illustrates his thinking and many subsequent schemes have emerged that

suggest similar direction including the polygeneration concept.

Integration across boundaries – outside a complex – is summarised in

Fig. 18.15 whereby coal utilisation takes place via a number of avenues by

conversion to steam for power generation, refi ning and heating as well as

gasifi cation to reforming and synthesis. In the modern idiom, replacement

or augmentation with renewables, including biomass or nuclear supplement-

ing carbon and energy from coal with these alternatives, can create energy

optimisation and lower the carbon footprint.

A polygeneration plant is defi ned as one that exports electricity and at

least one other product. 18 Manufacturing two or more products can exploit

synergies between the constituent processes (thereby increasing overall

plant effi ciency), increase operational fl exibility, and offer signifi cant eco-

nomic advantages. Polygeneration is achieved via coal gasifi cation that

Future directions toward more effi cient and cleaner use of coal 523

© Woodhead Publishing Limited, 2013

Mine Raw coal

Stockpile

Refining of liquidproducts

Tar

Low ash coalfraction

Petroleumstorage

Pitch

Curing andcarbonisation

Storage

oil Coke

BriquettingMixing

Tar

Lowtempcarbon-isation Medium ash char

Medium ash coal fraction

Coal preparationplant

High ash discharge

Discard dump

ReclamationPower station usingfluidised beds

Power

18.14 COALCOM concept. ( Source : After David Horsfall.)

Coal to steam for power productionReplace oraugmentwith:

• Renewables1. solar,2. geothermal.3. hydro,4. wind

• Nuclear• Biomass• Petcoke

Coal to steam for processes (refining; heating)

Coal to steam for processes (gasification; reforming)

Coal/carbon to synthesis

Products:• Fuels• Chemicals• Fertilizers/explosives• Recarb/anode coke• (carbon in ash, CO2)• lots more

18.15 Integration across boundaries. ( Source : After Koper.) 20

produces syngas. The technologies for the production (entrained, fl uidised

and moving bed gasifi ers) and cleaning of the syngas are already com-

mercialised, as are the production of electricity, hydrogen, SNG, ammo-

nia, Fischer-Tropsch liquids, as well as methanol and dimethyl ether from

the syngas. Figure 18.16 illustrates the possible range of products from a

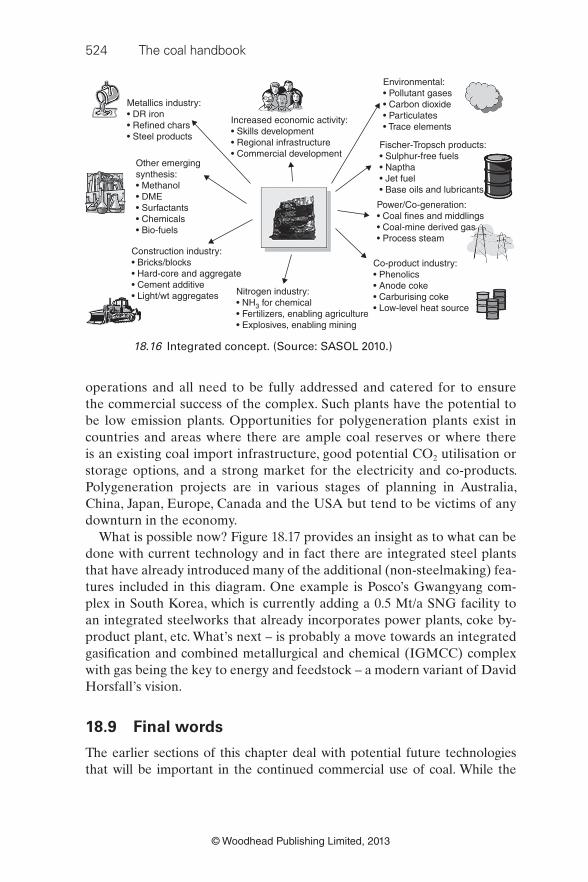

Polygeneration plant (after Koper ref 21).

Environmental aspects of these plants, including air emissions, CO 2 cap-

ture and storage, water usage and solid wastes, are an integral part of these

524 The coal handbook

© Woodhead Publishing Limited, 2013

operations and all need to be fully addressed and catered for to ensure

the commercial success of the complex. Such plants have the potential to

be low emission plants. Opportunities for polygeneration plants exist in

countries and areas where there are ample coal reserves or where there

is an existing coal import infrastructure, good potential CO 2 utilisation or

storage options, and a strong market for the electricity and co-products.

Polygeneration projects are in various stages of planning in Australia,

China, Japan, Europe, Canada and the USA but tend to be victims of any

downturn in the economy.

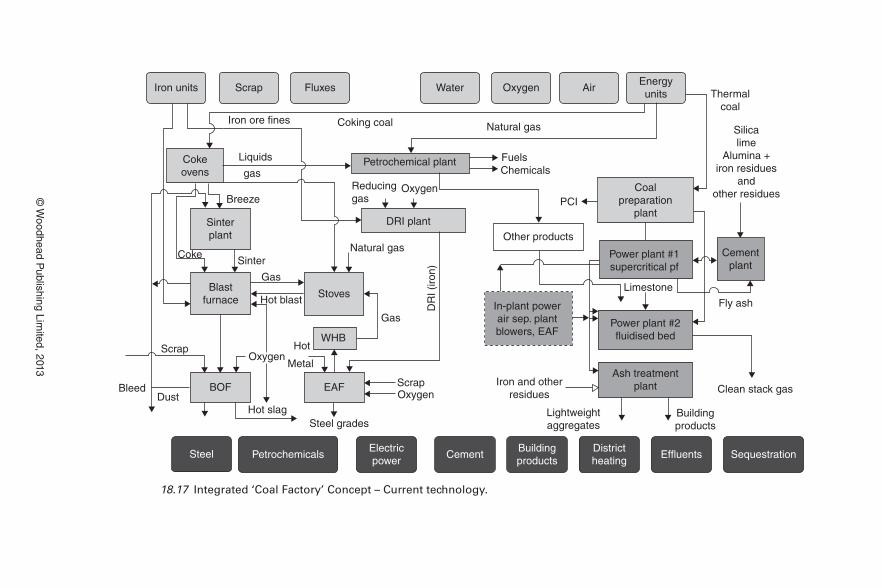

What is possible now? Figure 18.17 provides an insight as to what can be

done with current technology and in fact there are integrated steel plants

that have already introduced many of the additional (non-steelmaking) fea-

tures included in this diagram. One example is Posco’s Gwangyang com-

plex in South Korea, which is currently adding a 0.5 Mt/a SNG facility to

an integrated steelworks that already incorporates power plants, coke by-

product plant, etc. What’s next – is probably a move towards an integrated

gasifi cation and combined metallurgical and chemical (IGMCC) complex

with gas being the key to energy and feedstock – a modern variant of David

Horsfall’s vision.

18.9 Final words

The earlier sections of this chapter deal with potential future technologies

that will be important in the continued commercial use of coal. While the

Metallics industry:• DR iron• Refined chars• Steel products

Other emergingsynthesis:• Methanol• DME• Surfactants• Chemicals• Bio-fuels

Construction industry:• Bricks/blocks• Hard-core and aggregate• Cement additive• Light/wt aggregates Nitrogen industry:

• NH3 for chemical• Fertilizers, enabling agriculture• Explosives, enabling mining

Co-product industry:• Phenolics• Anode coke• Carburising coke• Low-level heat source

Environmental:• Pollutant gases• Carbon dioxide• Particulates• Trace elements

Fischer-Tropsch products:• Sulphur-free fuels• Naptha• Jet fuel• Base oils and lubricants

Power/Co-generation:• Coal fines and middlings• Coal-mine derived gas• Process steam

Increased economic activity:• Skills development• Regional infrastructure• Commercial development

18.16 Integrated concept. ( Source : SASOL 2010.)

© W

oodhead P

ublis

hin

g L

imite

d, 2

013

Iron units Scrap

Iron ore fines

Liquids

gasCokeovens

Breeze

Sinterplant

CokeSinter

GasBlast

furnaceStoves

Gas

Natural gas

Scrap

BleedDust

BOF

Hot slag

Steel PetrochemicalsElectricpower

CementBuildingproducts

Districtheating

Effluents Sequestration

Clean stack gas

Fly ash

Cementplant

Buildingproducts

Lightweightaggregates

Iron and otherresidues

ScrapOxygen

Steel grades

EAF

WHBHot

Hot blast

Metal

Fluxes

Coking coal Natural gas

FuelsPetrochemical plant

Coalpreparation

plantPCI

Other products

In-plant powerair sep. plantblowers, EAF

Power plant #1supercritical pf

Limestone

Power plant #2fluidised bed

Ash treatmentplant

DRI plant

Reducinggas

Oxygen

DR

I (iro

n)

Chemicals

Water Oxygen AirEnergyunits Thermal

coal

Silicalime

Alumina +iron residues

andother residues

Oxygen

18.17 Integrated ‘Coal Factory’ Concept – Current technology.

526 The coal handbook

© Woodhead Publishing Limited, 2013

use of coal as a feedstock to produce chemicals and as a reductant in iron

ore smelting seems assured, this is not clearly the case for coal in the electric-

ity generation industry. For this reason these ‘fi nal words’ focus on coal and

electricity.

Two of the great benefi ts of coal as a fuel for electricity are the rela-

tively high energy density (~30 MJ/kg) and the relatively low price. The

former is due to the chemical and physical processes that have trans-

formed vegetation into coal by the coalifi cation process while the latter

is also due to the maturity of the industry where engineering practice has

streamlined the processes involved in the winning, transport and utilisa-

tion of coal and has led to reduced costs accordingly. This latter point

is quite remarkable when one considers the whole coal value chain and

the effort required at each stage to mine, transport, prepare, combust

coal and to deal with the waste streams generated along the way. Over

the past century, industries and economies have developed along these

known cost structures, and coal currently plays a centrally important role

in the global economy.

However, coal is not without its challenges. It became apparent in the

1950s and 1960s that the particles released into the atmosphere by the then

coal combustion technology were creating signifi cant impacts including visi-

bility degradation and, in extreme cases, deleterious effects on human health.

These matters were addressed by the introduction initially of electrostatic

precipitator technology followed later, as the size of installations increased,

by fi ltration of the fl ue gas by use of solid fi lters housed in large bag houses.

From about the 1970s the issues associated with sulphur and nitrogen

deposition resulting from the emitted sulphur and nitrogen oxides demanded

attention and these saw the introduction of sulphur and nitrogen mitiga-

tion technologies to clean fl ue gases further, prior to their emission into the

atmosphere. These trends have continued, and over the past decade or so

the emission of trace elements has also come strongly into focus.

Similarly, the issues around the disposal of the solid waste (or ash) have

also been studied extensively with many studies investigating uses for ash

apart from storage in large ash disposal dams.

While the coal and power generation industries have been able to meet

each of these environmental challenges through the development and

deployment of new technologies, the current range of challenges raised by

the issue of climate change are more substantial. This is due to the larger

mass of CO 2 produced compared with the other waste streams and the fact

that the impacts of climate change are global rather than the more localized

impacts as has been the case in the past.

As all fossil energy use in future decades will have to deal with the issue of

greenhouse gas emissions, it is important that this be addressed in a system-

atic manner through the coal value chain. The fi rst step in this process is to

Future directions toward more effi cient and cleaner use of coal 527

© Woodhead Publishing Limited, 2013

decrease any fugitive emissions of methane arising from mining and transport.

The second step in this process is to increase the effi ciency of coal utilisation.

Here technologies such as Ultra Super Critical pf (USC), IGCC, the direct

injection coal engine (DICE) and the direct carbon fuel cell (DCFC) show

increasing effi ciency with corresponding decrease in CO 2 per unit of electric-

ity produced. However, each of these technologies is at a different stage of

development. For instance, USC is a more mature technology while DCFC is

presently a laboratory-based research activity. While DICE is further devel-

oped than DCFC it is not as far along the development curve as IGCC.

In any event, even with these new higher effi ciency processes carbon diox-

ide capture and storage will still be required for global emissions to be cut

by the amounts required to stabilise the global temperature at an acceptable

level as described by the climate change science community.

While the technology pathways described in this document will be able

to address the CO 2 emissions, major questions still exist concerning cost of

the technologies and whether there will be suffi cient public acceptance for

these technologies to be deployed. At present the projections for the costs

of the low emissions coal technologies are comparable with the alternatives.

An important aspect in determining the deployment of future technologies

will be the suitability of the technology with regard to the electricity demand

curves as well as the presence of a cost on the carbon dioxide emitted.