The Accounting ProfessionThe Accounting Profession

What It IsWhat It Is

Accounting is a ProfessionAccounting is a Profession

Commercial/FinancialCommercial/FinancialCostCostTaxTaxAuditingAuditingBudgetingBudgetingGovernmentGovernment

Users of Financial Users of Financial InformationInformation

OwnerOwnerCreditorCreditorManagerManagerGovernmentGovernmentPublicPublic

End ProductsEnd Products

Balance Sheet (Ch 2)Balance Sheet (Ch 2) Income Statement (Ch 3)Income Statement (Ch 3)Statement of Cash Flows (Ch 4)Statement of Cash Flows (Ch 4)

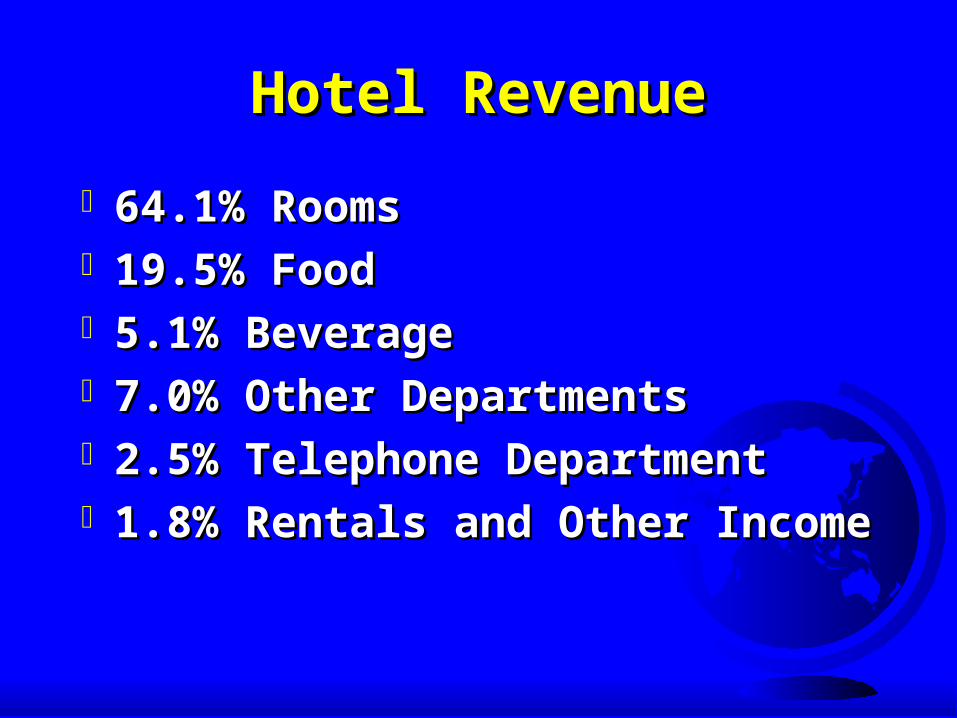

Hotel RevenueHotel Revenue

64.1% Rooms64.1% Rooms19.5% Food19.5% Food5.1% Beverage5.1% Beverage7.0% Other Departments7.0% Other Departments2.5% Telephone Department2.5% Telephone Department1.8% Rentals and Other Income1.8% Rentals and Other Income

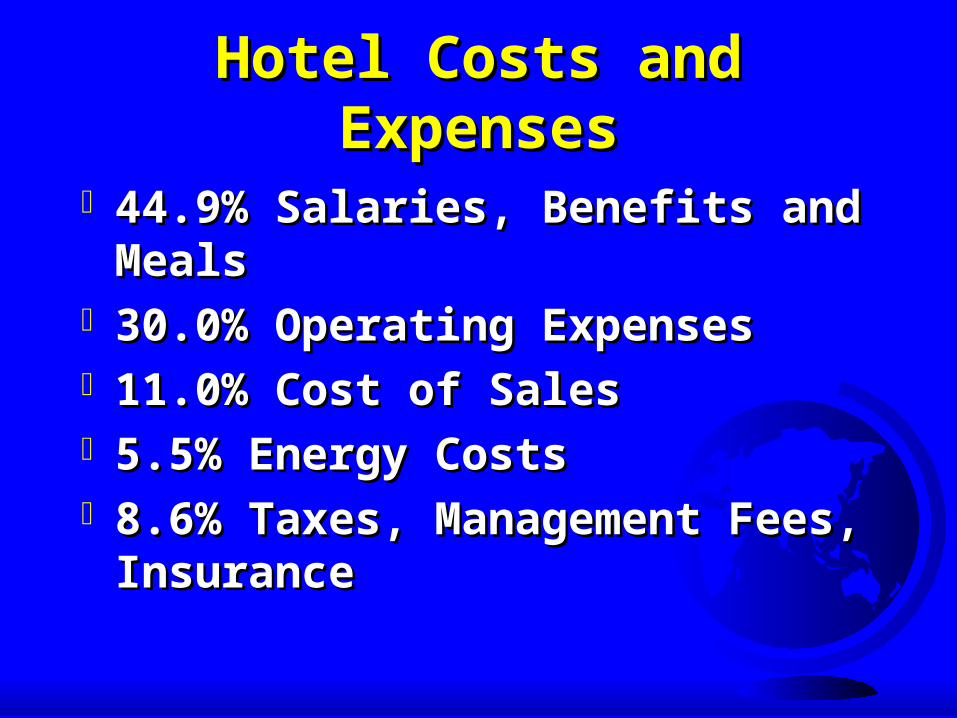

Hotel Costs and ExpensesHotel Costs and Expenses

44.9% Salaries, Benefits and 44.9% Salaries, Benefits and MealsMeals

30.0% Operating Expenses30.0% Operating Expenses 11.0% Cost of Sales11.0% Cost of Sales 5.5% Energy Costs5.5% Energy Costs 8.6% Taxes, Management Fees, 8.6% Taxes, Management Fees,

InsuranceInsurance

The Hospitality BusinessThe Hospitality Business

Seasonal BusinessSeasonal Business Fluctuating DemandFluctuating Demand Short Conversion Time - FoodShort Conversion Time - Food Selling Space - Now or NeverSelling Space - Now or Never Labor IntensiveLabor Intensive Intensive Fixed Asset InvestmentIntensive Fixed Asset Investment

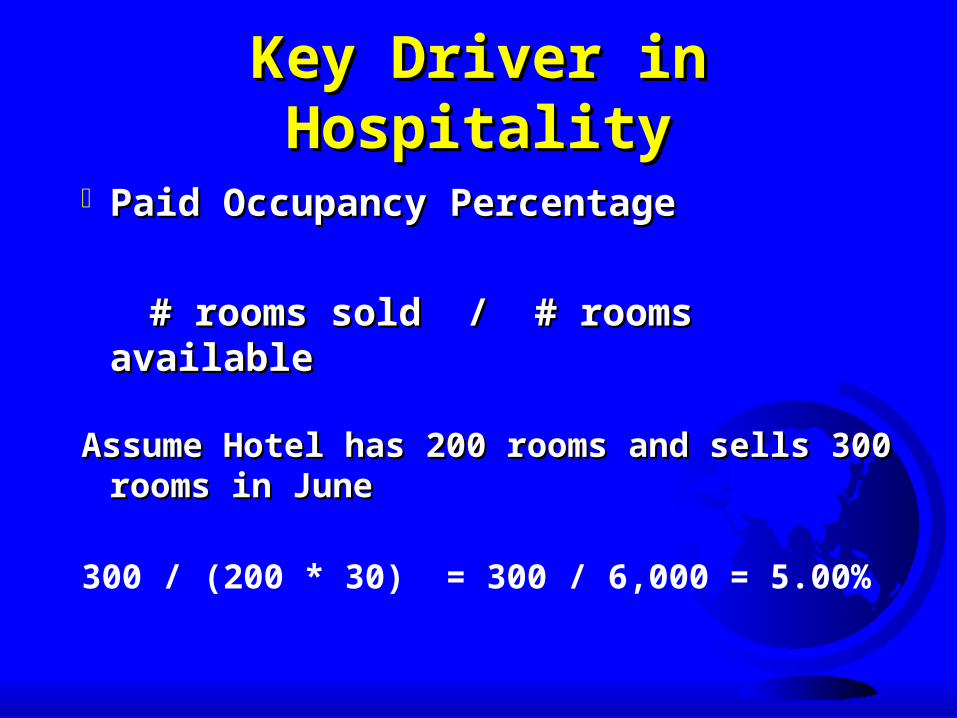

Key Driver in HospitalityKey Driver in Hospitality

Paid Occupancy PercentagePaid Occupancy Percentage

# rooms sold / # rooms available# rooms sold / # rooms available

Assume Hotel has 200 rooms and sells 300 Assume Hotel has 200 rooms and sells 300 rooms in Junerooms in June

300 / (200 * 30) = 300 / 6,000 = 5.00%

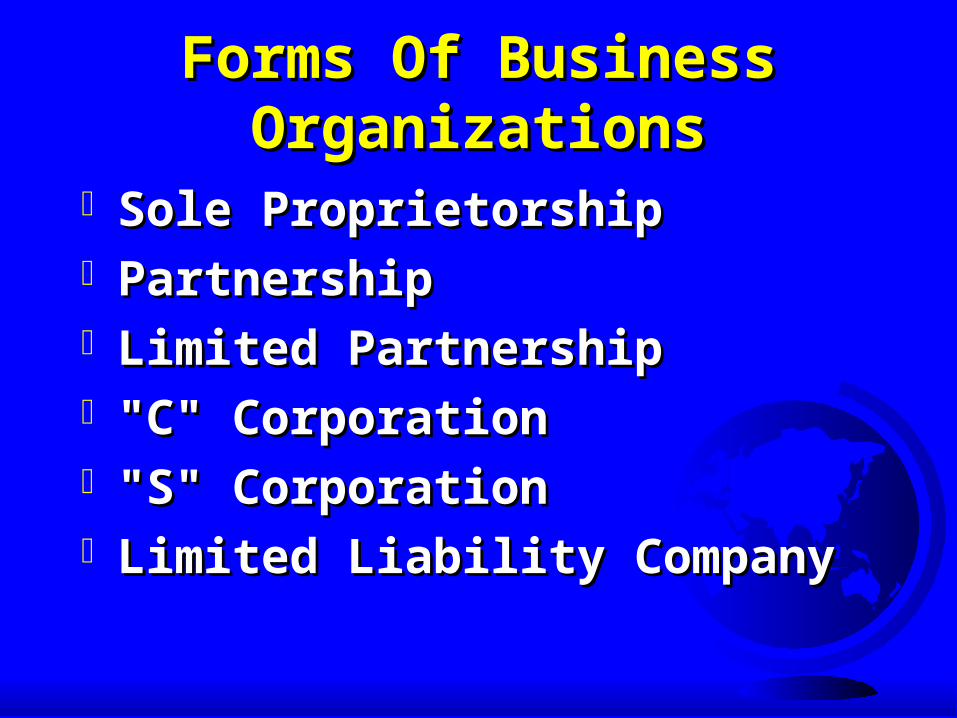

Forms Of Business Forms Of Business OrganizationsOrganizations

Sole ProprietorshipSole ProprietorshipPartnershipPartnershipLimited PartnershipLimited Partnership "C" Corporation"C" Corporation "S" Corporation"S" CorporationLimited Liability CompanyLimited Liability Company

A Review of AccountingA Review of Accounting

A Quick SummaryA Quick Summary

Uniform System of Uniform System of AccountsAccounts

Industry Uses a Uniform System Industry Uses a Uniform System of Accountingof Accounting

Lodging Operations, Lodging Operations, Restaurants, ClubsRestaurants, Clubs

Generally Accepted Generally Accepted Accounting PrinciplesAccounting Principles

Provide Uniform Basis For Provide Uniform Basis For Preparing Financial StatementsPreparing Financial Statements

AICPAAICPAFASBFASBGAAPGAAP

Principles of AccountingPrinciples of Accounting

Cost PrincipleCost PrincipleBusiness EntityBusiness EntityContinuity of the Business UnitContinuity of the Business UnitUnit of MeasurementUnit of Measurement

Principles of AccountingPrinciples of Accounting

Objective EvidenceObjective EvidenceFull DisclosureFull DisclosureConsistencyConsistencyMatchingMatching

Principles of AccountingPrinciples of Accounting

ConservatismConservatismMaterialityMaterialityCash Basis AccountingCash Basis AccountingAccrual Basis AccountingAccrual Basis Accounting

Cash vs AccrualCash vs Accrual

Cash Basis AccountingCash Basis Accounting

–Recognize revenue or expense Recognize revenue or expense when cash receivedwhen cash received

Accrual Basis AccountingAccrual Basis Accounting

–Recognize revenue when earnedRecognize revenue when earned

–Recognize expense when incurredRecognize expense when incurred

Fundamental EquationFundamental Equation

Assets = Liabilities + Owners EquityAssets = Liabilities + Owners Equity Assets = LiabilitiesAssets = Liabilities

+ Permanent OE+ Permanent OE + Temporary OE+ Temporary OE

Assets = LiabilitiesAssets = Liabilities + Permanent OE+ Permanent OE

+ Revenue+ Revenue - Expenses- Expenses

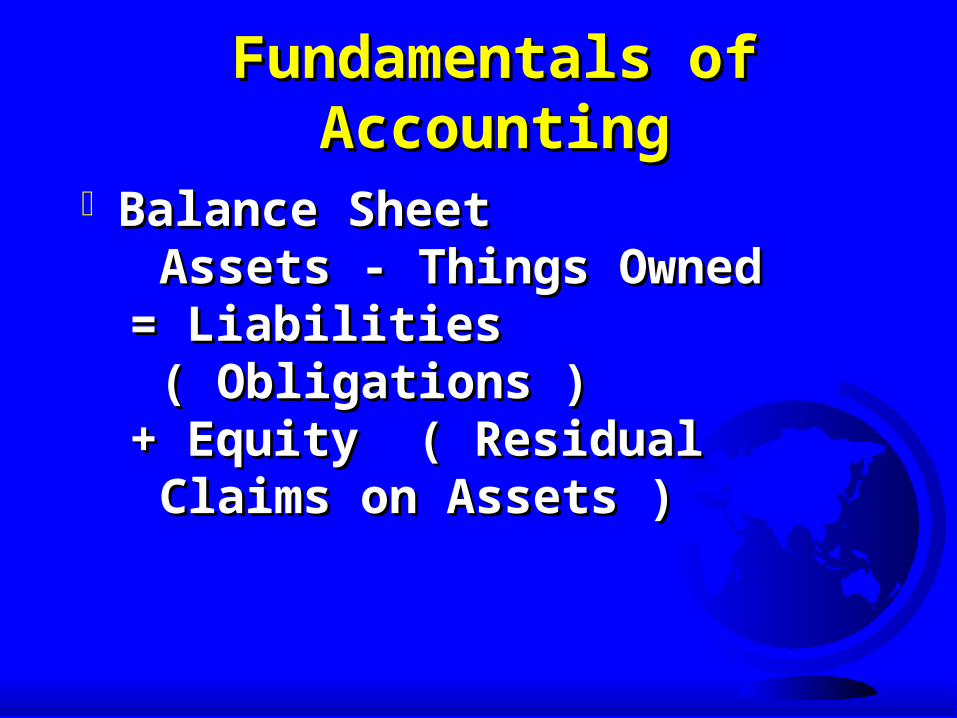

Fundamentals of AccountingFundamentals of Accounting

Balance Sheet Balance Sheet Assets - Things OwnedAssets - Things Owned

= Liabilities ( Obligations )= Liabilities ( Obligations )+ Equity ( Residual Claims on + Equity ( Residual Claims on

Assets )Assets )

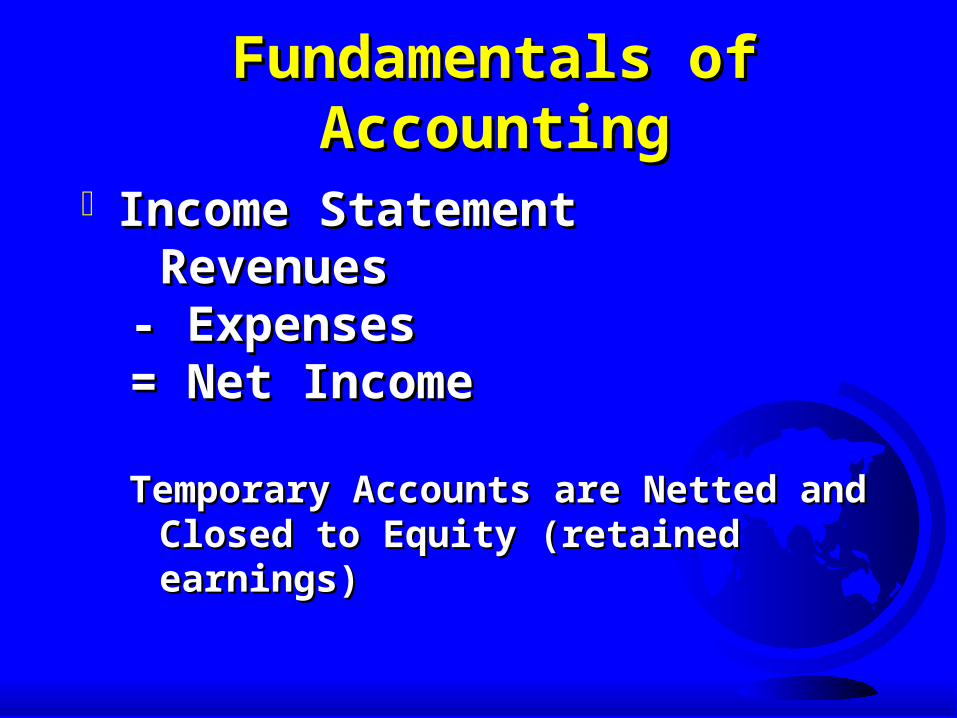

Fundamentals of AccountingFundamentals of Accounting

Income StatementIncome StatementRevenuesRevenues

- Expenses- Expenses= Net Income= Net Income

Temporary Accounts are Netted and Temporary Accounts are Netted and Closed to Equity (retained earnings)Closed to Equity (retained earnings)

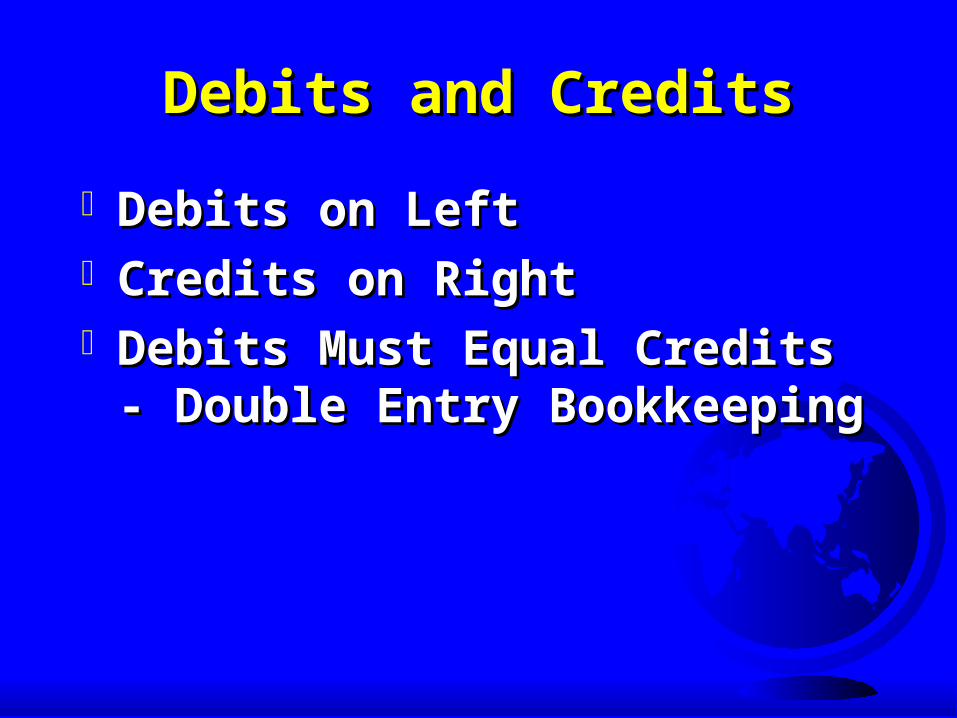

Debits and CreditsDebits and Credits

Debits on LeftDebits on LeftCredits on RightCredits on RightDebits Must Equal Credits - Debits Must Equal Credits -

Double Entry BookkeepingDouble Entry Bookkeeping

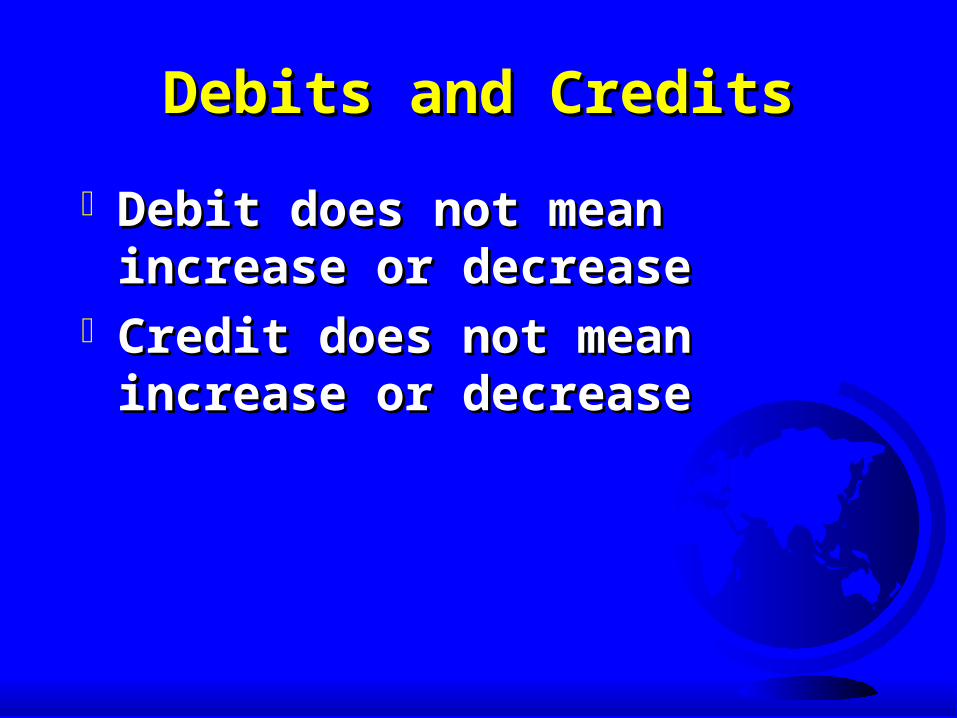

Debits and CreditsDebits and Credits

Debit does not mean increase or Debit does not mean increase or decreasedecrease

Credit does not mean increase or Credit does not mean increase or decreasedecrease

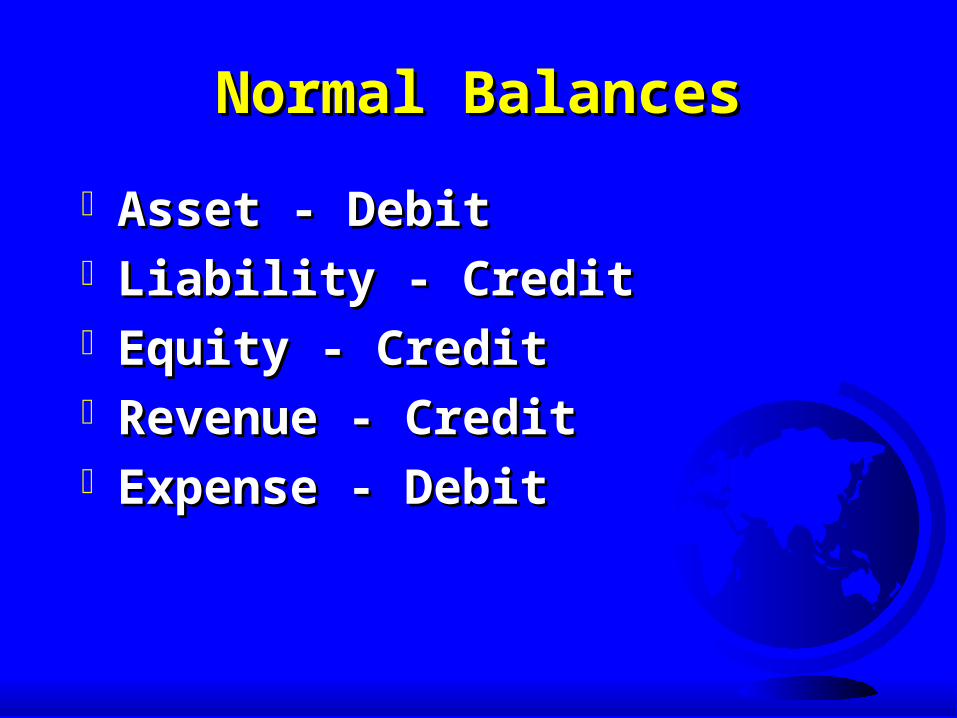

Normal BalancesNormal Balances

Asset - DebitAsset - DebitLiability - CreditLiability - CreditEquity - CreditEquity - CreditRevenue - CreditRevenue - CreditExpense - Debit Expense - Debit

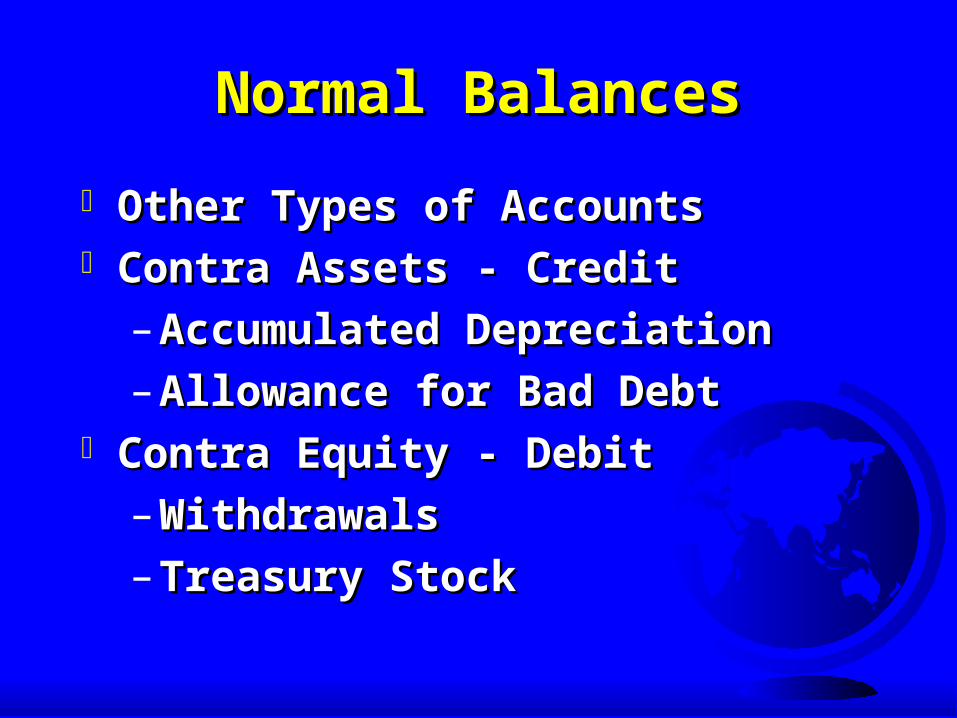

Normal BalancesNormal Balances

Other Types of AccountsOther Types of Accounts Contra Assets - CreditContra Assets - Credit

–Accumulated DepreciationAccumulated Depreciation

–Allowance for Bad DebtAllowance for Bad Debt Contra Equity - DebitContra Equity - Debit

–WithdrawalsWithdrawals

– Treasury StockTreasury Stock

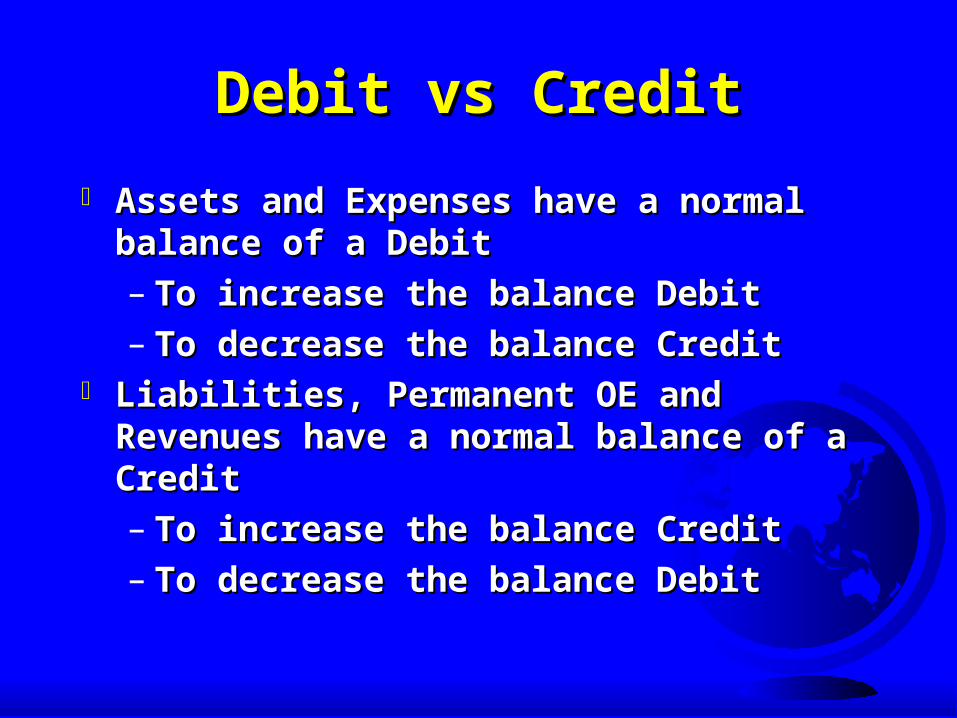

Debit vs CreditDebit vs Credit

Assets and Expenses have a normal Assets and Expenses have a normal balance of a Debitbalance of a Debit– To increase the balance DebitTo increase the balance Debit– To decrease the balance CreditTo decrease the balance Credit

Liabilities, Permanent OE and Revenues Liabilities, Permanent OE and Revenues have a normal balance of a Credithave a normal balance of a Credit– To increase the balance CreditTo increase the balance Credit– To decrease the balance DebitTo decrease the balance Debit

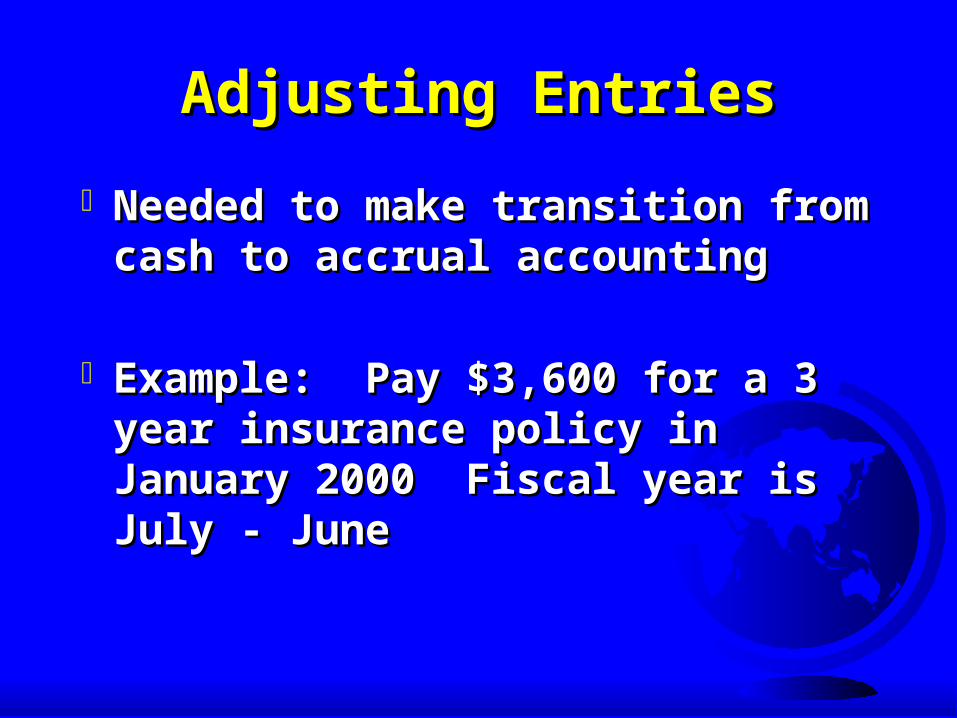

Adjusting EntriesAdjusting Entries

Needed to make transition from Needed to make transition from cash to accrual accountingcash to accrual accounting

Example: Pay $3,600 for a 3 year Example: Pay $3,600 for a 3 year insurance policy in January 2000 insurance policy in January 2000 Fiscal year is July - June Fiscal year is July - June

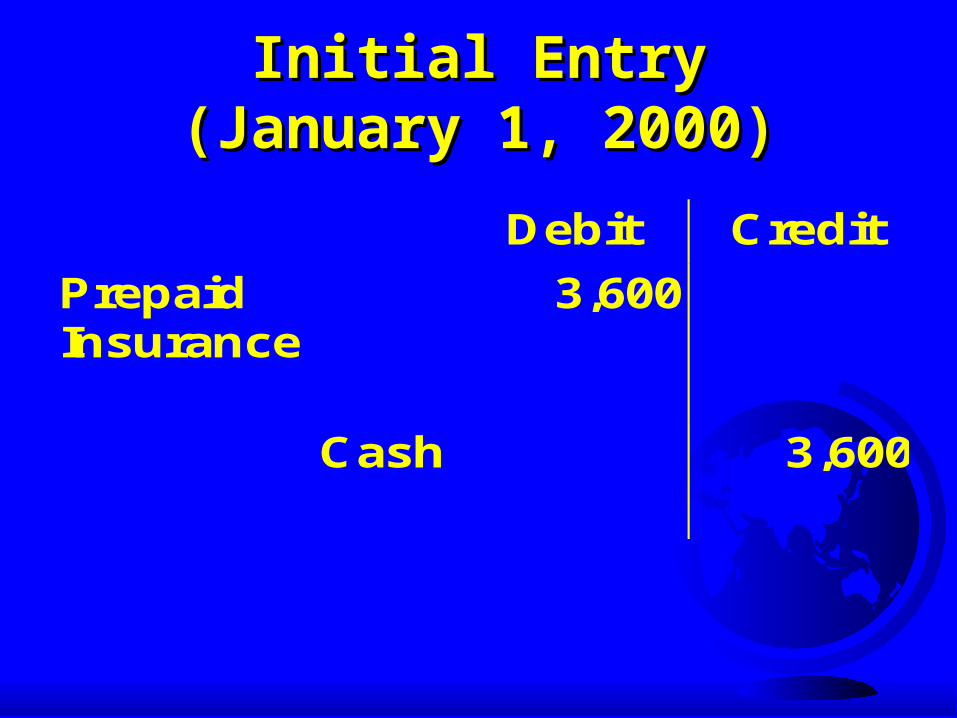

Initial EntryInitial Entry(January 1, 2000)(January 1, 2000)

Debit Credit

PrepaidInsurance

3,600

Cash 3,600

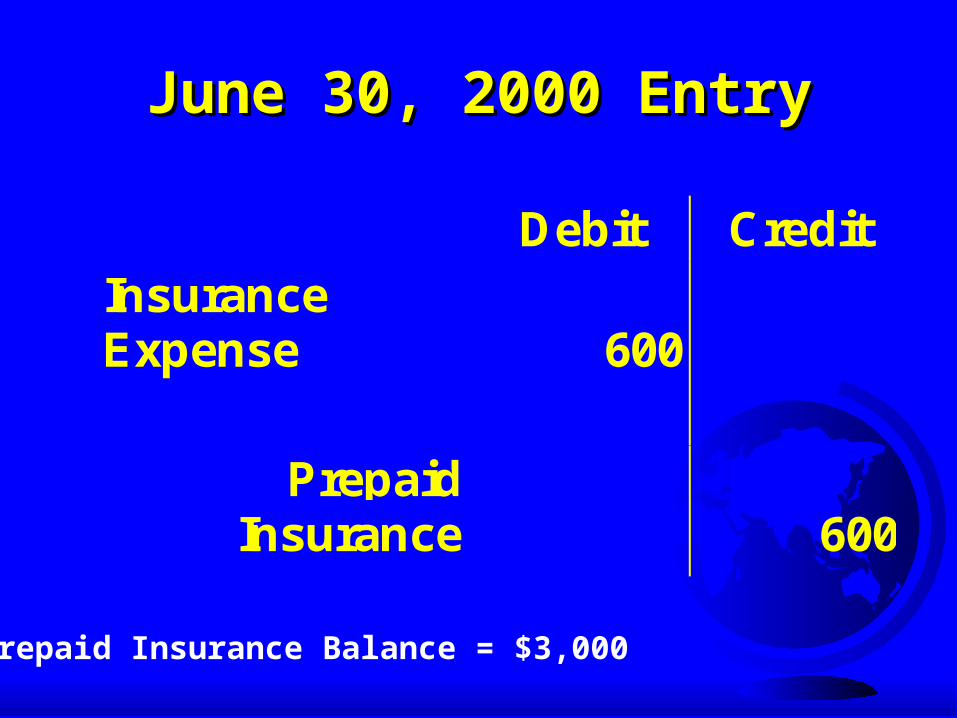

June 30, 2000 EntryJune 30, 2000 Entry

Debit CreditInsuranceExpense 600

PrepaidInsurance 600

Prepaid Insurance Balance = $3,000

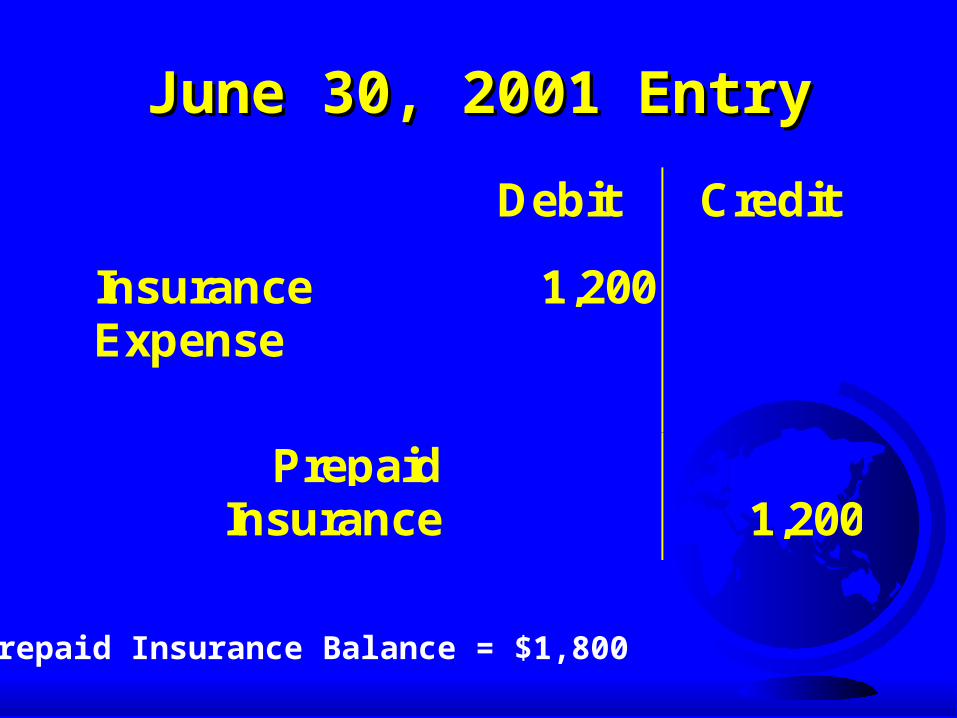

June 30, 2001 EntryJune 30, 2001 Entry

Debit Credit

InsuranceExpense

1,200

PrepaidInsurance 1,200

Prepaid Insurance Balance = $1,800

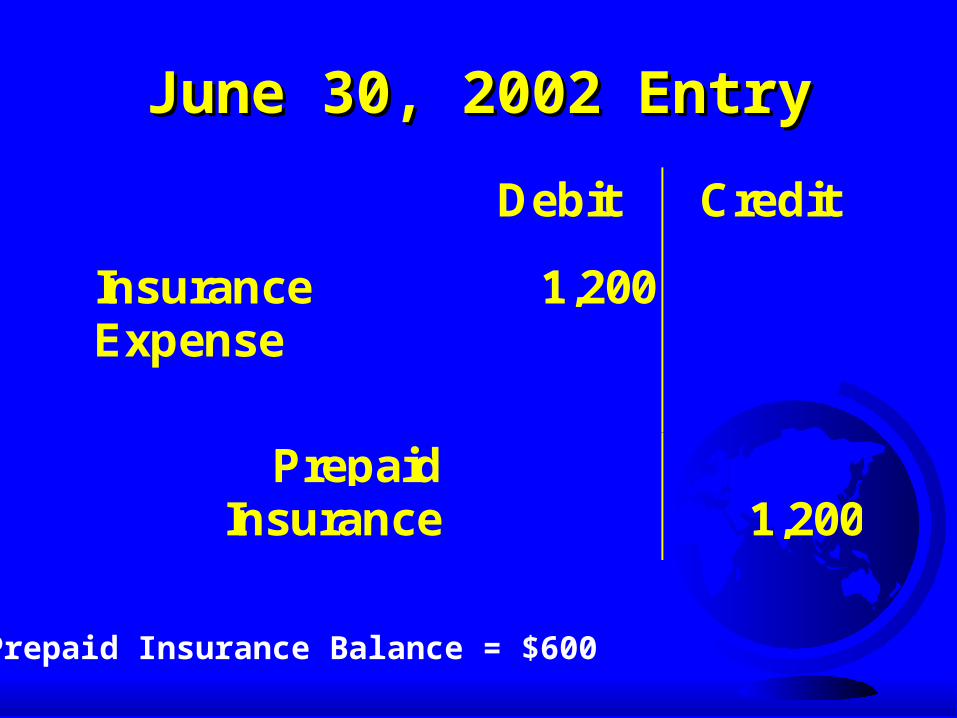

June 30, 2002 EntryJune 30, 2002 Entry

Debit Credit

InsuranceExpense

1,200

PrepaidInsurance 1,200

Prepaid Insurance Balance = $600

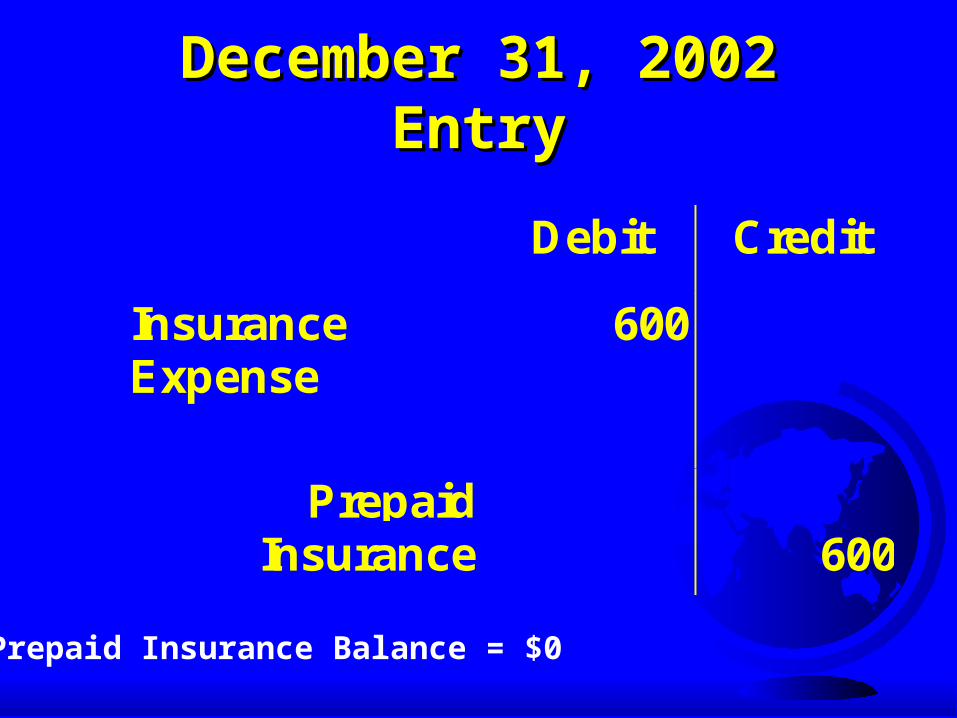

December 31, 2002 EntryDecember 31, 2002 Entry

Debit Credit

InsuranceExpense

600

PrepaidInsurance 600

Prepaid Insurance Balance = $0

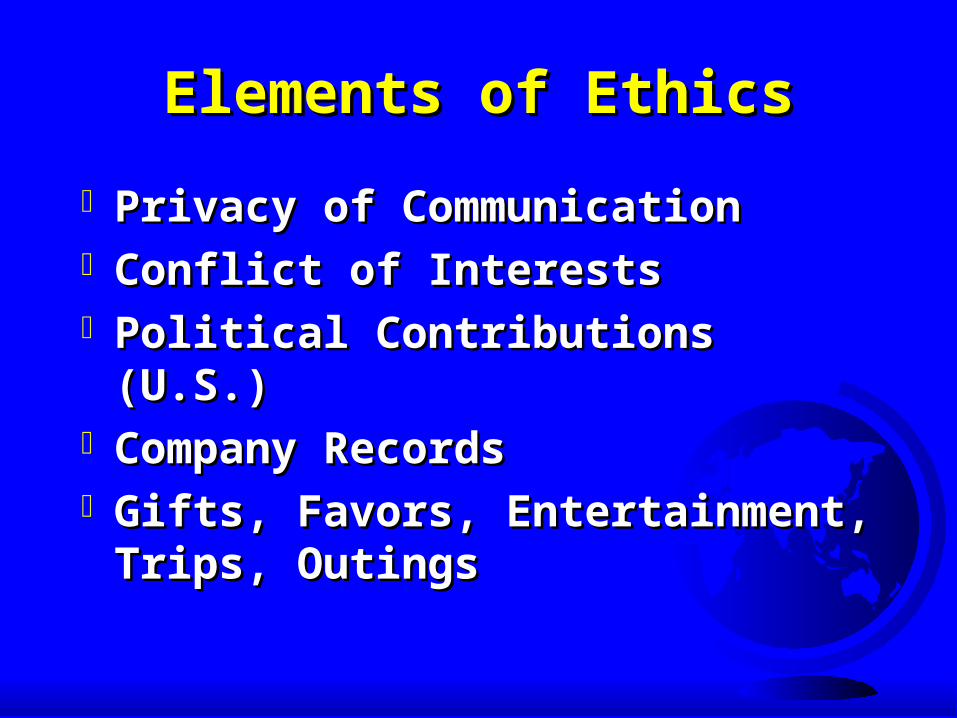

Elements of EthicsElements of Ethics

Privacy of CommunicationPrivacy of CommunicationConflict of InterestsConflict of InterestsPolitical Contributions (U.S.)Political Contributions (U.S.)Company RecordsCompany RecordsGifts, Favors, Entertainment, Gifts, Favors, Entertainment,

Trips, OutingsTrips, Outings

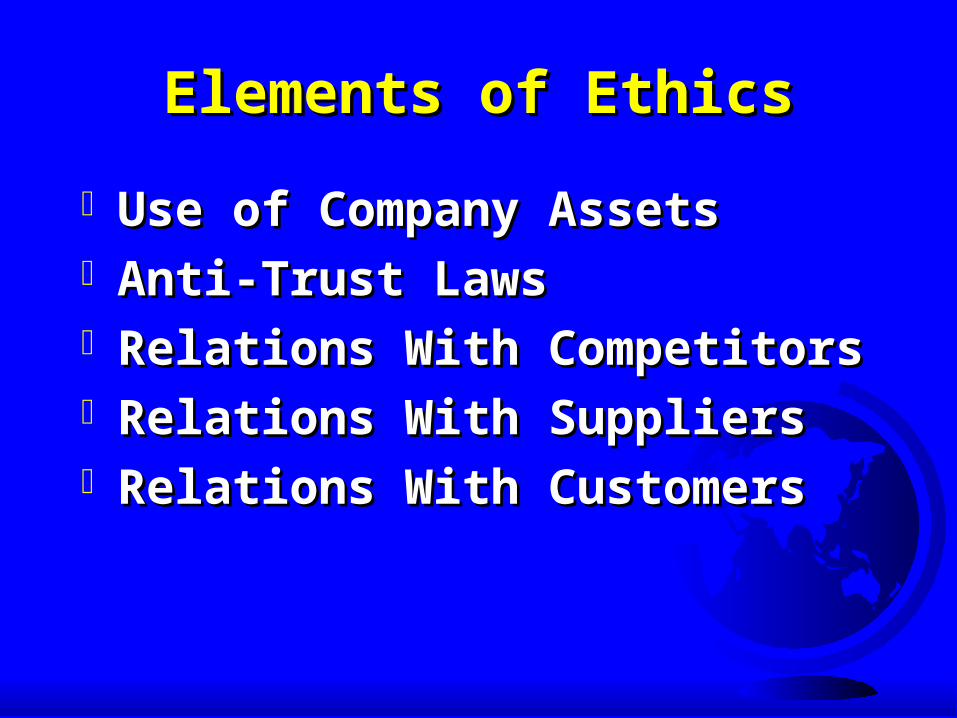

Elements of EthicsElements of Ethics

Use of Company AssetsUse of Company AssetsAnti-Trust LawsAnti-Trust LawsRelations With CompetitorsRelations With CompetitorsRelations With SuppliersRelations With SuppliersRelations With CustomersRelations With Customers

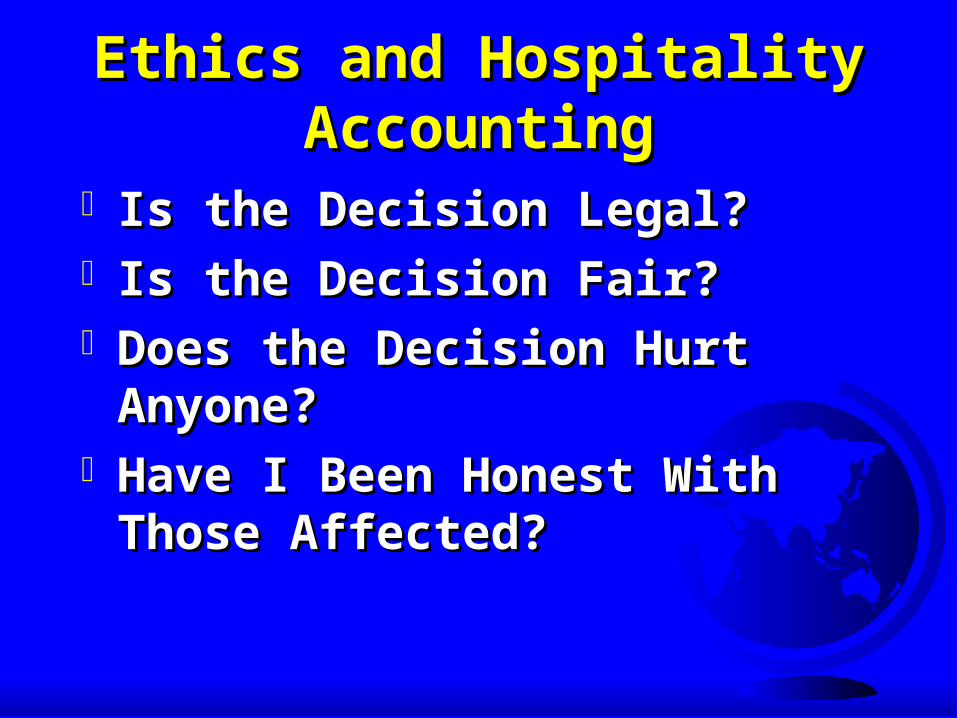

Ethics and Hospitality Ethics and Hospitality AccountingAccounting

Is the Decision Legal?Is the Decision Legal? Is the Decision Fair?Is the Decision Fair?Does the Decision Hurt Anyone?Does the Decision Hurt Anyone?Have I Been Honest With Those Have I Been Honest With Those

Affected?Affected?

Ethics and Hospitality Ethics and Hospitality AccountingAccounting

Can I Live With My Decision?Can I Live With My Decision?Am I Willing to Publicize My Am I Willing to Publicize My

Decision?Decision?What If Everyone Did What I Did?What If Everyone Did What I Did?

Recommended