1

Li & Fung Research Centre

Member of the Li & Fung Group

China Distribution & Trading Issue 48 November 2007

IN THIS ISSUE :

Li & Fung Research Centre

13/F, LiFung Centre

2 On Ping Street

Shatin, Hong Kong

Tel: (852) 2635 5563

Fax: (852) 2635 1598

E-mail: [email protected]

http://www.lifunggroup.com/

Chinese Consumer Behaviour Revisited

Today, the allure of China’s consumer market is undeniably stronger than

before. With impressive economic growth, strong retail performance, rising

wealth levels and government initiatives to boost domestic consumption,

China’s consumer market presents rosy development prospects.

Eyeing this huge market, both international and local brand owners and

retailers are striving their best to understand the preferences of different groups

of Chinese consumers so as to grab a firm share in the market.

In this issue, we will first have a quick look on the growth drivers of the

consumer market of China. We will then discuss the behaviour of the Chinese

consumers. A brief description of the emerging groups of consumers in China

will follow and selected consumption hotspots in China will be presented at the

end of this issue.

I. Growth drivers of China’s consumer market

1. Growing economy and booming retail sector

After many years of rapid development, China is now the fourth largest

economy in the world after the United States, Japan and Germany. In 2006,

China’s GDP continued to grow by 11.1% based on constant price to reach

21.1 trillion yuan (approximately USD 2.8 trillion). The total retail sales

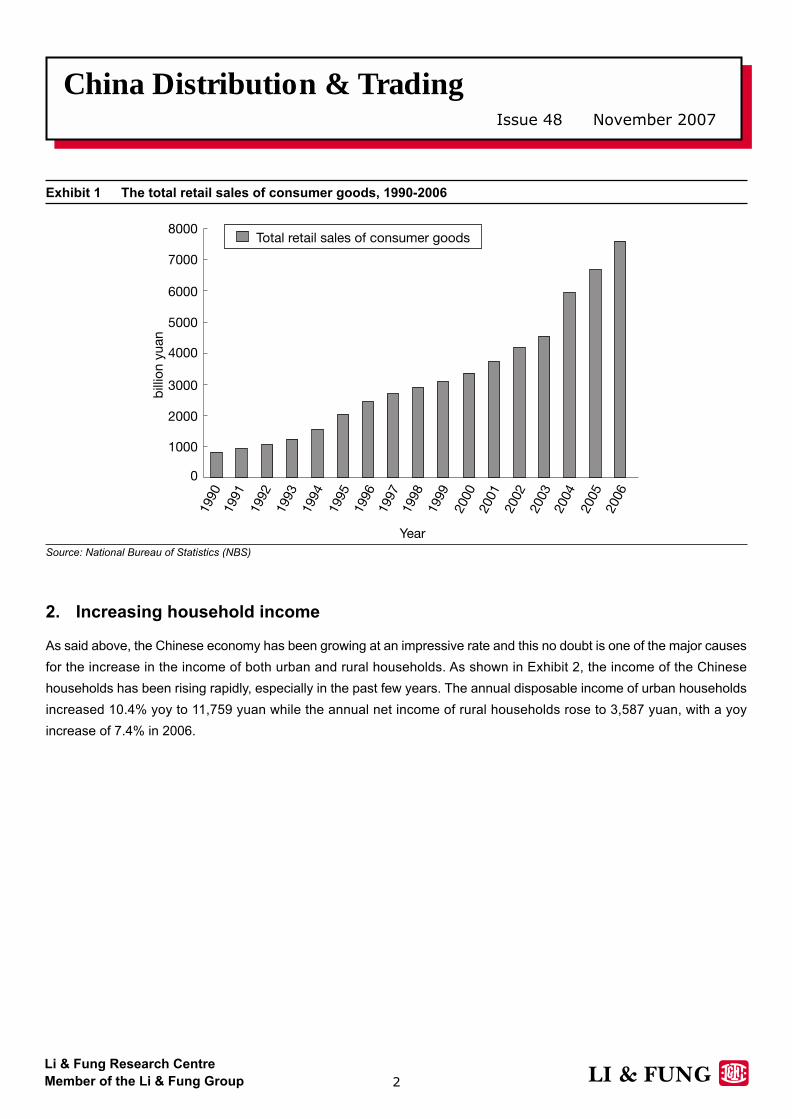

of consumer goods in China, rising along with the growing economy,

reached 7,641.0 billion yuan, with a year-on-year (yoy) increase of 13.7%.

(see Exhibit 1). Considering one of the major 11th Five-Year Program initiatives

is to promote private consumption and development of the service sector to

shift the economic growth model from investment-driven to consumption-led,

the growth potential of retail sector is anticipated to be huge.

I. Growth drivers of 1

China’s consumer market

II. Consumer behaviour 5

in China

III. Emerging consumer 13

groups

IV. Selected consumption 14

hotspots

LI & FUNG RESEARCH CENTRE

China Distribution & TradingIssue 48 November 2007

2

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 1 The total retail sales of consumer goods, 1990-2006

Source: National Bureau of Statistics (NBS)

2. Increasing household income

As said above, the Chinese economy has been growing at an impressive rate and this no doubt is one of the major causes

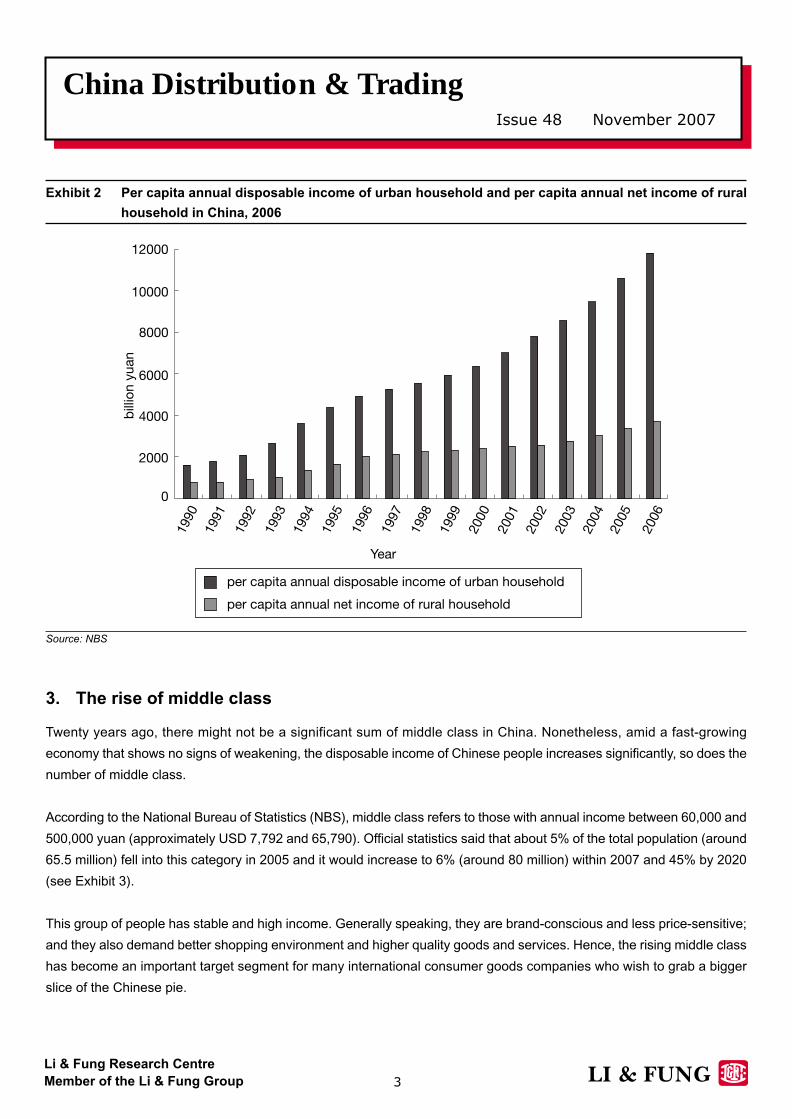

for the increase in the income of both urban and rural households. As shown in Exhibit 2, the income of the Chinese

households has been rising rapidly, especially in the past few years. The annual disposable income of urban households

increased 10.4% yoy to 11,759 yuan while the annual net income of rural households rose to 3,587 yuan, with a yoy

increase of 7.4% in 2006.

China Distribution & TradingIssue 48 November 2007

3

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 2 Per capita annual disposable income of urban household and per capita annual net income of rural

household in China, 2006

Source: NBS

3. The rise of middle class

Twenty years ago, there might not be a significant sum of middle class in China. Nonetheless, amid a fast-growing

economy that shows no signs of weakening, the disposable income of Chinese people increases significantly, so does the

number of middle class.

According to the National Bureau of Statistics (NBS), middle class refers to those with annual income between 60,000 and

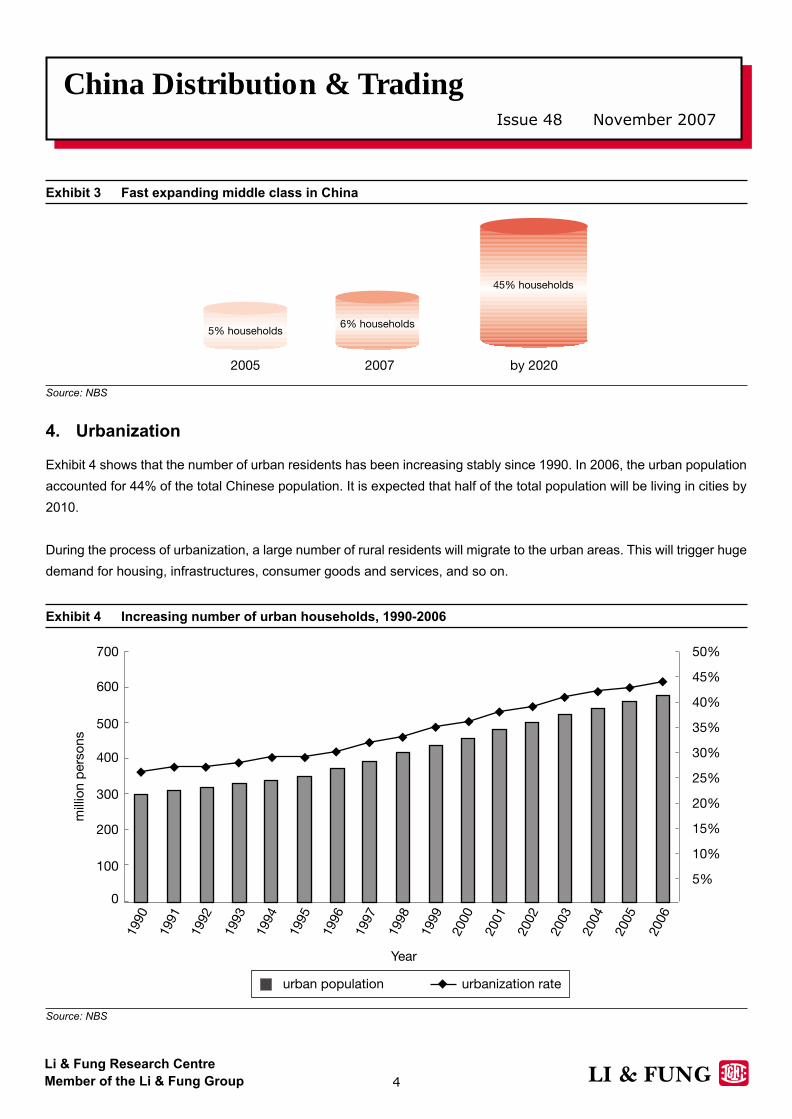

500,000 yuan (approximately USD 7,792 and 65,790). Official statistics said that about 5% of the total population (around

65.5 million) fell into this category in 2005 and it would increase to 6% (around 80 million) within 2007 and 45% by 2020

(see Exhibit 3).

This group of people has stable and high income. Generally speaking, they are brand-conscious and less price-sensitive;

and they also demand better shopping environment and higher quality goods and services. Hence, the rising middle class

has become an important target segment for many international consumer goods companies who wish to grab a bigger

slice of the Chinese pie.

China Distribution & TradingIssue 48 November 2007

4

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 3 Fast expanding middle class in China

Source: NBS

4. Urbanization

Exhibit 4 shows that the number of urban residents has been increasing stably since 1990. In 2006, the urban population

accounted for 44% of the total Chinese population. It is expected that half of the total population will be living in cities by

2010.

During the process of urbanization, a large number of rural residents will migrate to the urban areas. This will trigger huge

demand for housing, infrastructures, consumer goods and services, and so on.

Exhibit 4 Increasing number of urban households, 1990-2006

Source: NBS

China Distribution & TradingIssue 48 November 2007

5

Li & Fung Research Centre

Member of the Li & Fung Group

II. Consumer behaviour in China

1. Consumption structure upgrade

(1) Spending more on discretionary items

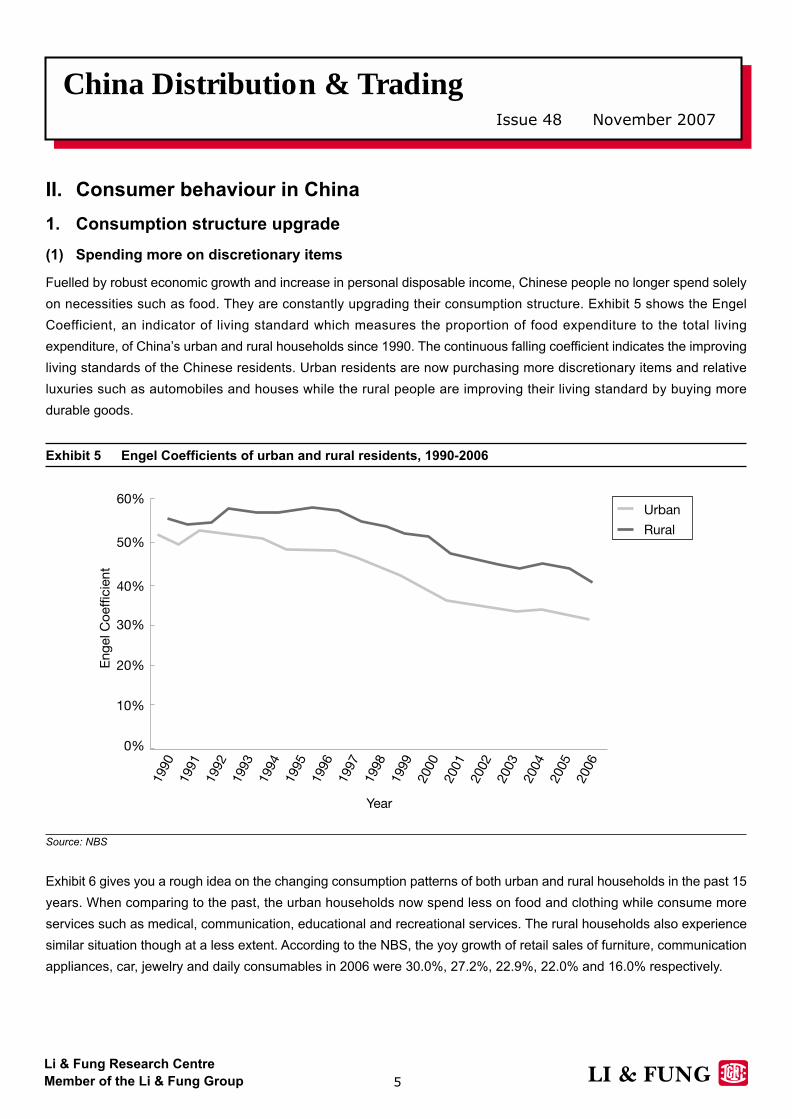

Fuelled by robust economic growth and increase in personal disposable income, Chinese people no longer spend solely

on necessities such as food. They are constantly upgrading their consumption structure. Exhibit 5 shows the Engel

Coefficient, an indicator of living standard which measures the proportion of food expenditure to the total living

expenditure, of China’s urban and rural households since 1990. The continuous falling coefficient indicates the improving

living standards of the Chinese residents. Urban residents are now purchasing more discretionary items and relative

luxuries such as automobiles and houses while the rural people are improving their living standard by buying more

durable goods.

Exhibit 5 Engel Coefficients of urban and rural residents, 1990-2006

Source: NBS

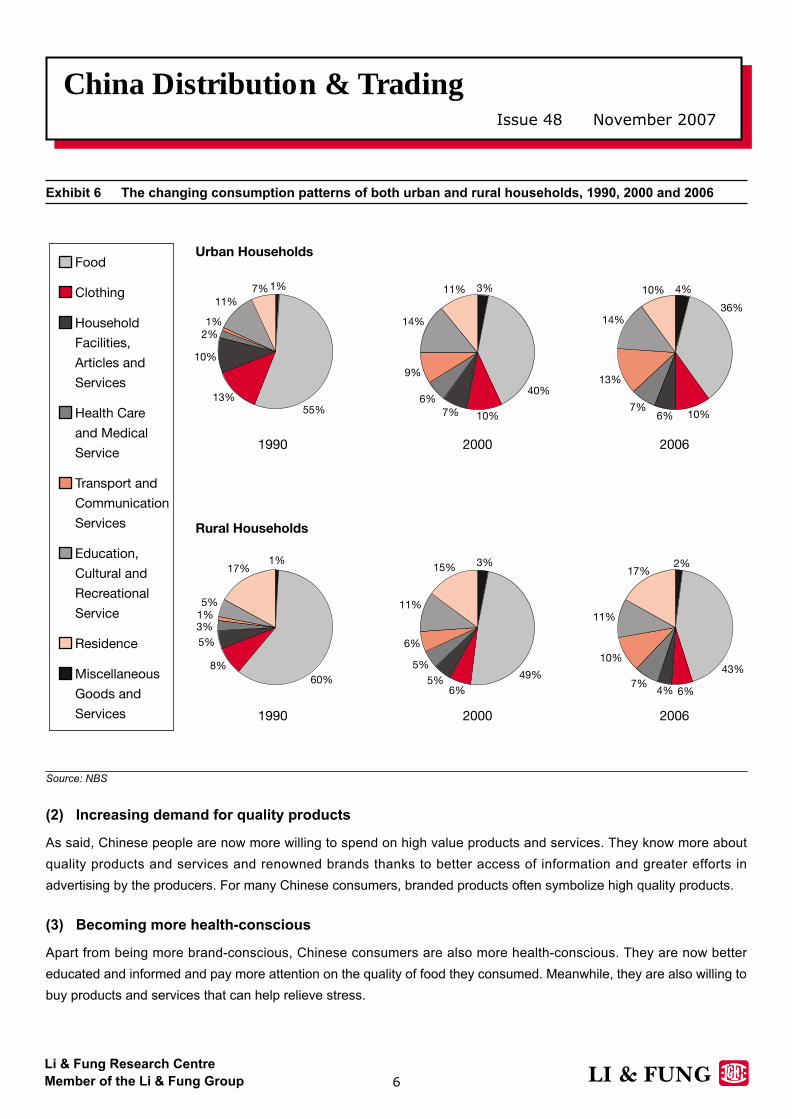

Exhibit 6 gives you a rough idea on the changing consumption patterns of both urban and rural households in the past 15

years. When comparing to the past, the urban households now spend less on food and clothing while consume more

services such as medical, communication, educational and recreational services. The rural households also experience

similar situation though at a less extent. According to the NBS, the yoy growth of retail sales of furniture, communication

appliances, car, jewelry and daily consumables in 2006 were 30.0%, 27.2%, 22.9%, 22.0% and 16.0% respectively.

China Distribution & TradingIssue 48 November 2007

6

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 6 The changing consumption patterns of both urban and rural households, 1990, 2000 and 2006

Source: NBS

(2) Increasing demand for quality products

As said, Chinese people are now more willing to spend on high value products and services. They know more about

quality products and services and renowned brands thanks to better access of information and greater efforts in

advertising by the producers. For many Chinese consumers, branded products often symbolize high quality products.

(3) Becoming more health-conscious

Apart from being more brand-conscious, Chinese consumers are also more health-conscious. They are now better

educated and informed and pay more attention on the quality of food they consumed. Meanwhile, they are also willing to

buy products and services that can help relieve stress.

China Distribution & TradingIssue 48 November 2007

7

Li & Fung Research Centre

Member of the Li & Fung Group

2. New ways of spending

(1) Use of credit card

Today, China is by and large a cash-based society. For many Chinese, making payments by credit cards or debit cards is

still a new way of spending. According to a recent survey by the Economist Intelligence Unit, among some one billion

active cards (including credit and debit cards) being issued in China, only 50 million of them are credit cards. On average,

Chinese card users make only one transaction each month; and about 80% of them pay off their entire balance.

According to a survey by Credit Suisse, credit card ownership is most popular among the younger generation who

generally is less conservative about money. Multi-card ownership is also observed among this age group.

With the rise of the middle class, which pocesses higher purchasing power, credit card usage in China is expected to see

a boom in the coming years.

(2) Online shopping

According to a recent national survey by the quasi-governmental China Internet Network Information Centre (CNNIC), the

number of Internet users in China soared from 123 million as of June 2006 to 162 million as of June 2007; the number was

second highest in the world, only after the United States. Among the surveyed users, more than 80% aged 35 or below.

This reflects that Internet users in China are relatively young.

The survey also stated that around 26% of Chinese Internet users (or 40 million people) engaged in online shopping as of

June 2007. Considering the fact that more than 70% of American Internet users regularly shop online, online shopping is

still not very popular in China. This indicates that the growth potential for this alternative way of spending for Chinese

customers is huge.

In recent years, a growing number of Chinese Internet users has engaged in customer to customer (C2C) online

shopping, especially those in richer cities. According to the China Online Shopping Market Survey 2006 conducted by

CNNIC, around 2 million residents of Beijing, Shanghai and Guangzhou shopped on C2C auction websites in 2005. The

most prominent ones were Taobao ( ) and eBay ( ); and their market share was 67.3% and 29.1% respectively

in 2005. CNNIC estimated that the total number of C2C shoppers in China has exceeded 10 million. The top-five popular

categories in C2C market were clothing, shoes & accessories, cosmetics & jewelry, computers & networking, prepaid

phones/game cards and books.

China Distribution & TradingIssue 48 November 2007

8

Li & Fung Research Centre

Member of the Li & Fung Group

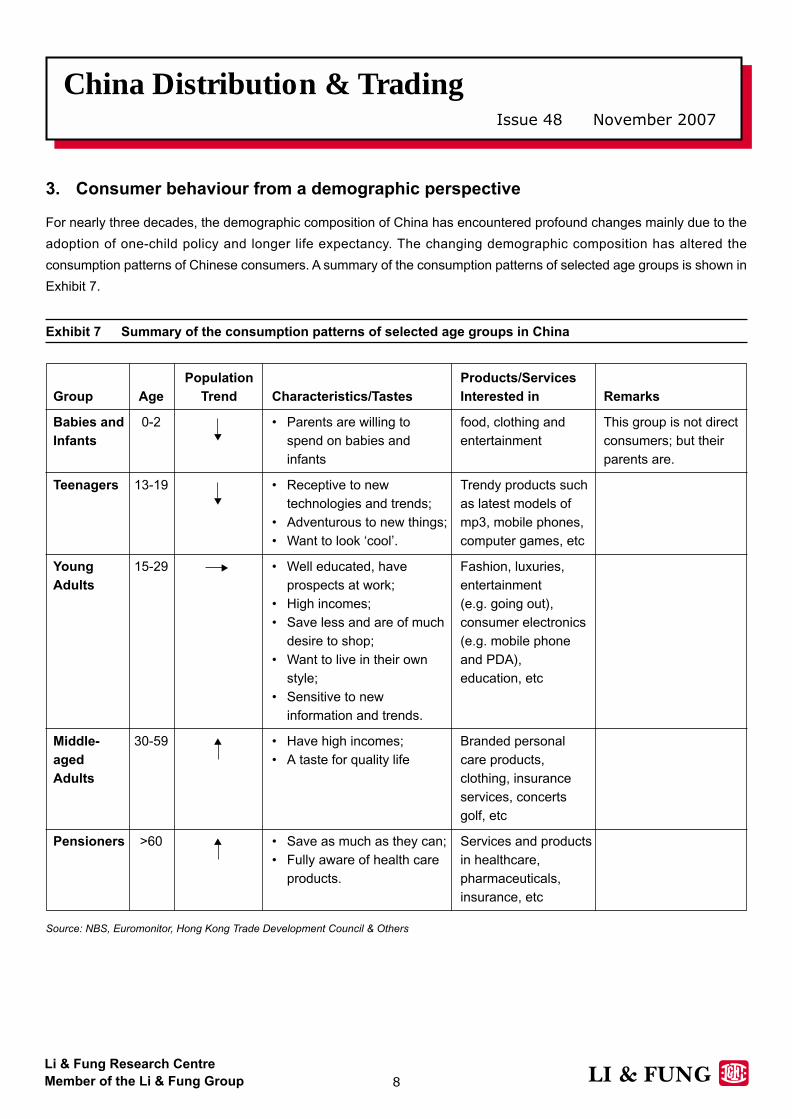

3. Consumer behaviour from a demographic perspective

For nearly three decades, the demographic composition of China has encountered profound changes mainly due to the

adoption of one-child policy and longer life expectancy. The changing demographic composition has altered the

consumption patterns of Chinese consumers. A summary of the consumption patterns of selected age groups is shown in

Exhibit 7.

Exhibit 7 Summary of the consumption patterns of selected age groups in China

Population Products/Services

Group Age Trend Characteristics/Tastes Interested in Remarks

Babies and 0-2 • Parents are willing to food, clothing and This group is not direct

Infants spend on babies and entertainment consumers; but their

infants parents are.

Teenagers 13-19 • Receptive to new Trendy products such

technologies and trends; as latest models of

• Adventurous to new things; mp3, mobile phones,

• Want to look ‘cool’. computer games, etc

Young 15-29 • Well educated, have Fashion, luxuries,

Adults prospects at work; entertainment

• High incomes; (e.g. going out),

• Save less and are of much consumer electronics

desire to shop; (e.g. mobile phone

• Want to live in their own and PDA),

style; education, etc

• Sensitive to new

information and trends.

Middle- 30-59 • Have high incomes; Branded personal

aged • A taste for quality life care products,

Adults clothing, insurance

services, concerts

golf, etc

Pensioners >60 • Save as much as they can; Services and products

• Fully aware of health care in healthcare,

products. pharmaceuticals,

insurance, etc

Source: NBS, Euromonitor, Hong Kong Trade Development Council & Others

China Distribution & TradingIssue 48 November 2007

9

Li & Fung Research Centre

Member of the Li & Fung Group

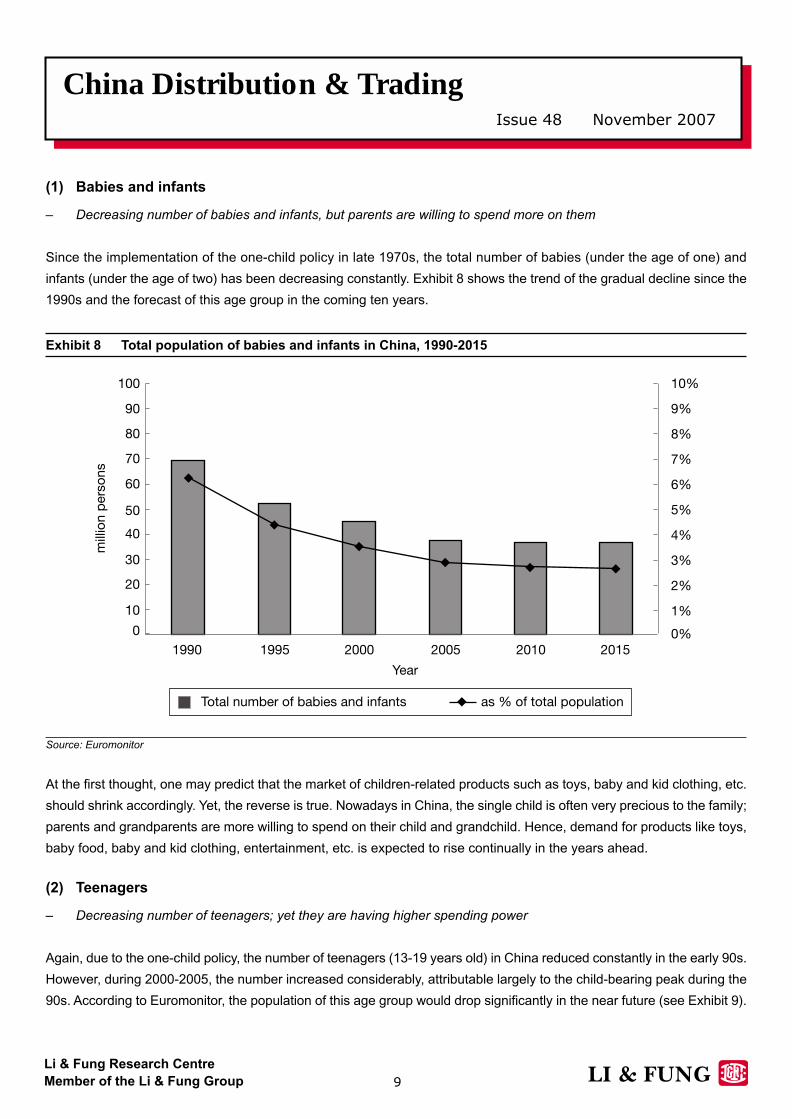

(1) Babies and infants

– Decreasing number of babies and infants, but parents are willing to spend more on them

Since the implementation of the one-child policy in late 1970s, the total number of babies (under the age of one) and

infants (under the age of two) has been decreasing constantly. Exhibit 8 shows the trend of the gradual decline since the

1990s and the forecast of this age group in the coming ten years.

Exhibit 8 Total population of babies and infants in China, 1990-2015

Source: Euromonitor

At the first thought, one may predict that the market of children-related products such as toys, baby and kid clothing, etc.

should shrink accordingly. Yet, the reverse is true. Nowadays in China, the single child is often very precious to the family;

parents and grandparents are more willing to spend on their child and grandchild. Hence, demand for products like toys,

baby food, baby and kid clothing, entertainment, etc. is expected to rise continually in the years ahead.

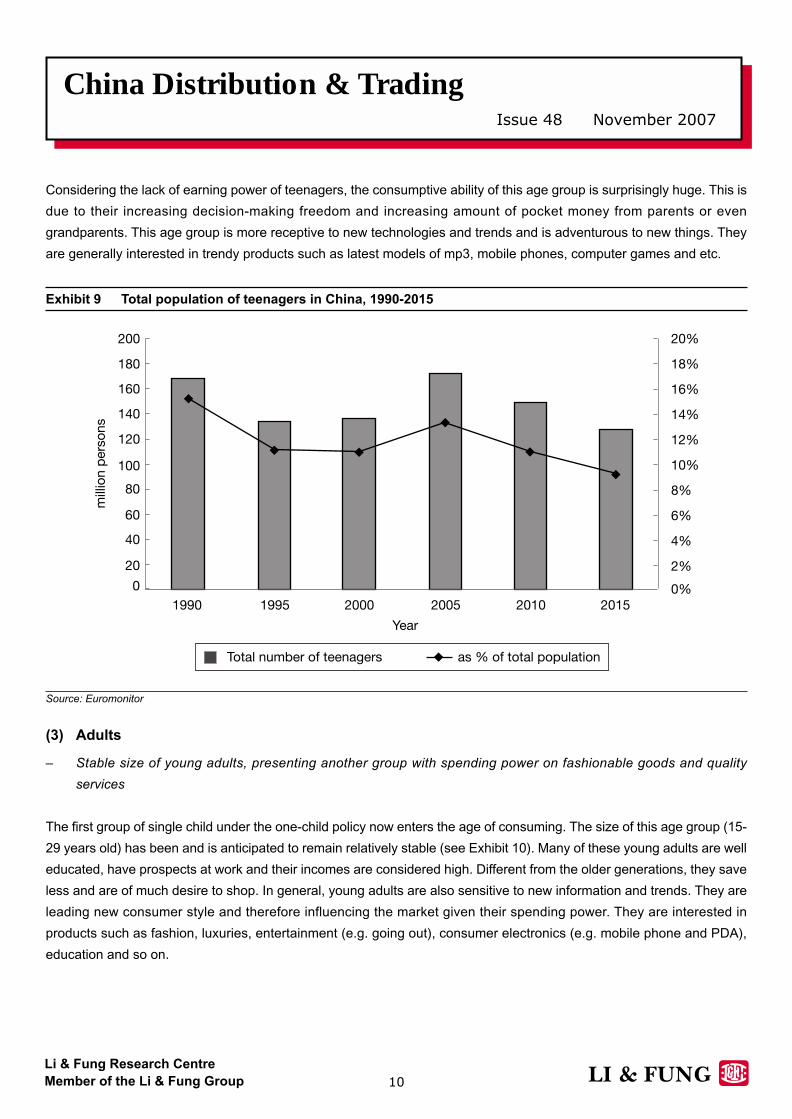

(2) Teenagers

– Decreasing number of teenagers; yet they are having higher spending power

Again, due to the one-child policy, the number of teenagers (13-19 years old) in China reduced constantly in the early 90s.

However, during 2000-2005, the number increased considerably, attributable largely to the child-bearing peak during the

90s. According to Euromonitor, the population of this age group would drop significantly in the near future (see Exhibit 9).

China Distribution & TradingIssue 48 November 2007

10

Li & Fung Research Centre

Member of the Li & Fung Group

Considering the lack of earning power of teenagers, the consumptive ability of this age group is surprisingly huge. This is

due to their increasing decision-making freedom and increasing amount of pocket money from parents or even

grandparents. This age group is more receptive to new technologies and trends and is adventurous to new things. They

are generally interested in trendy products such as latest models of mp3, mobile phones, computer games and etc.

Exhibit 9 Total population of teenagers in China, 1990-2015

Source: Euromonitor

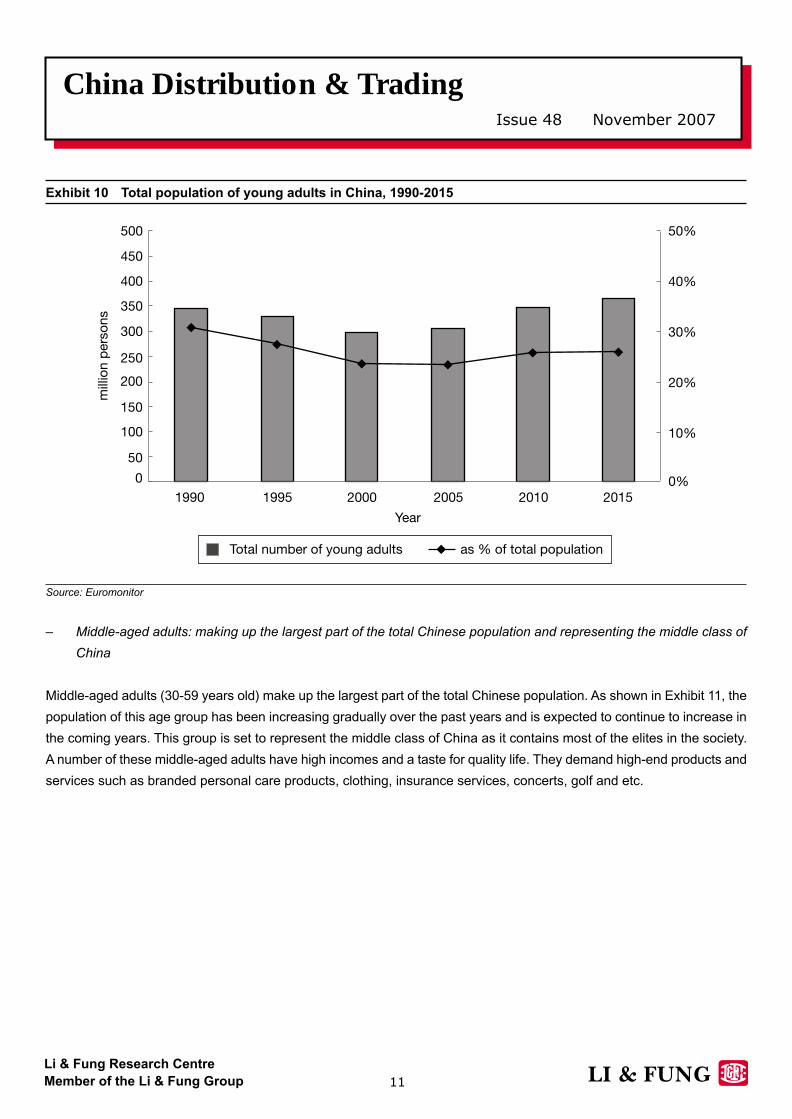

(3) Adults

– Stable size of young adults, presenting another group with spending power on fashionable goods and quality

services

The first group of single child under the one-child policy now enters the age of consuming. The size of this age group (15-

29 years old) has been and is anticipated to remain relatively stable (see Exhibit 10). Many of these young adults are well

educated, have prospects at work and their incomes are considered high. Different from the older generations, they save

less and are of much desire to shop. In general, young adults are also sensitive to new information and trends. They are

leading new consumer style and therefore influencing the market given their spending power. They are interested in

products such as fashion, luxuries, entertainment (e.g. going out), consumer electronics (e.g. mobile phone and PDA),

education and so on.

China Distribution & TradingIssue 48 November 2007

11

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 10 Total population of young adults in China, 1990-2015

Source: Euromonitor

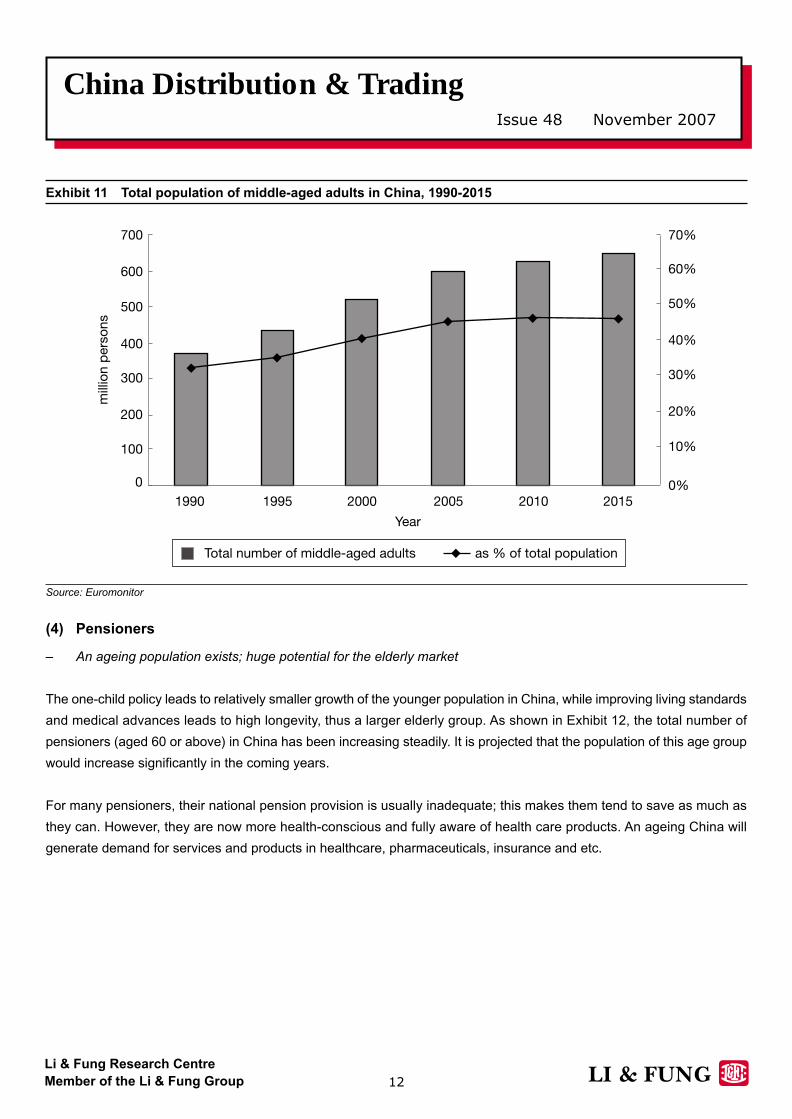

– Middle-aged adults: making up the largest part of the total Chinese population and representing the middle class of

China

Middle-aged adults (30-59 years old) make up the largest part of the total Chinese population. As shown in Exhibit 11, the

population of this age group has been increasing gradually over the past years and is expected to continue to increase in

the coming years. This group is set to represent the middle class of China as it contains most of the elites in the society.

A number of these middle-aged adults have high incomes and a taste for quality life. They demand high-end products and

services such as branded personal care products, clothing, insurance services, concerts, golf and etc.

China Distribution & TradingIssue 48 November 2007

12

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 11 Total population of middle-aged adults in China, 1990-2015

Source: Euromonitor

(4) Pensioners

– An ageing population exists; huge potential for the elderly market

The one-child policy leads to relatively smaller growth of the younger population in China, while improving living standards

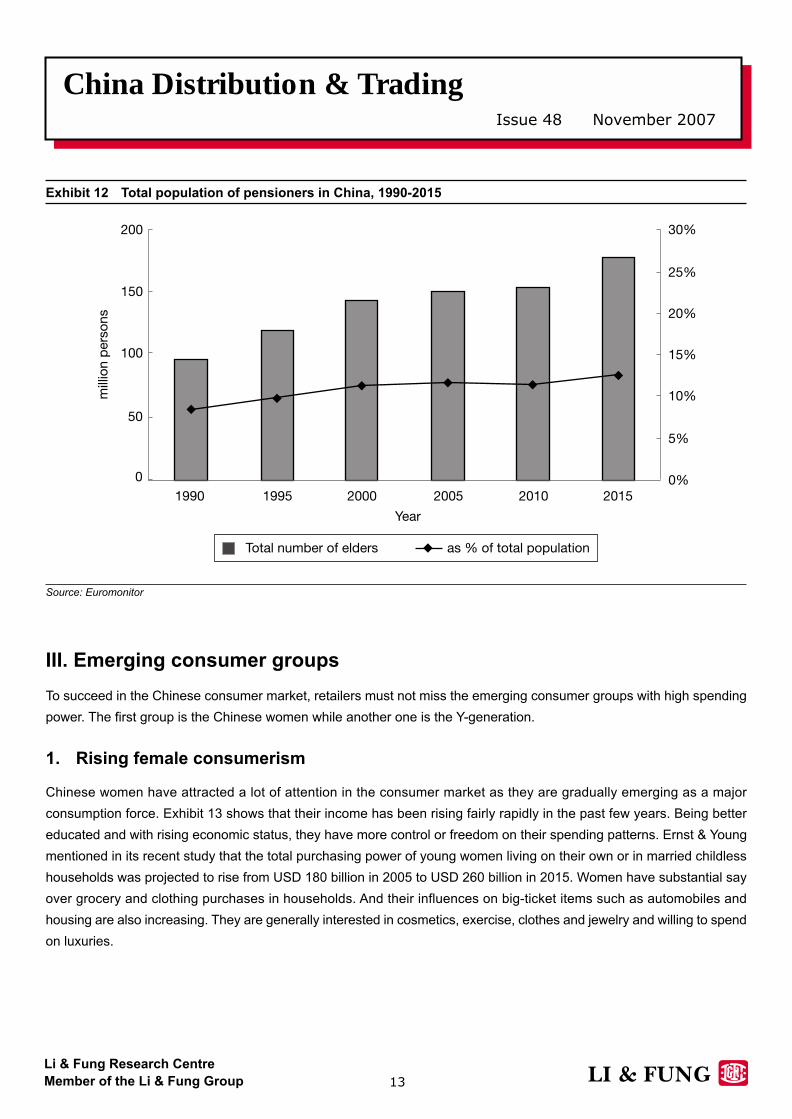

and medical advances leads to high longevity, thus a larger elderly group. As shown in Exhibit 12, the total number of

pensioners (aged 60 or above) in China has been increasing steadily. It is projected that the population of this age group

would increase significantly in the coming years.

For many pensioners, their national pension provision is usually inadequate; this makes them tend to save as much as

they can. However, they are now more health-conscious and fully aware of health care products. An ageing China will

generate demand for services and products in healthcare, pharmaceuticals, insurance and etc.

China Distribution & TradingIssue 48 November 2007

13

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 12 Total population of pensioners in China, 1990-2015

Source: Euromonitor

III. Emerging consumer groups

To succeed in the Chinese consumer market, retailers must not miss the emerging consumer groups with high spending

power. The first group is the Chinese women while another one is the Y-generation.

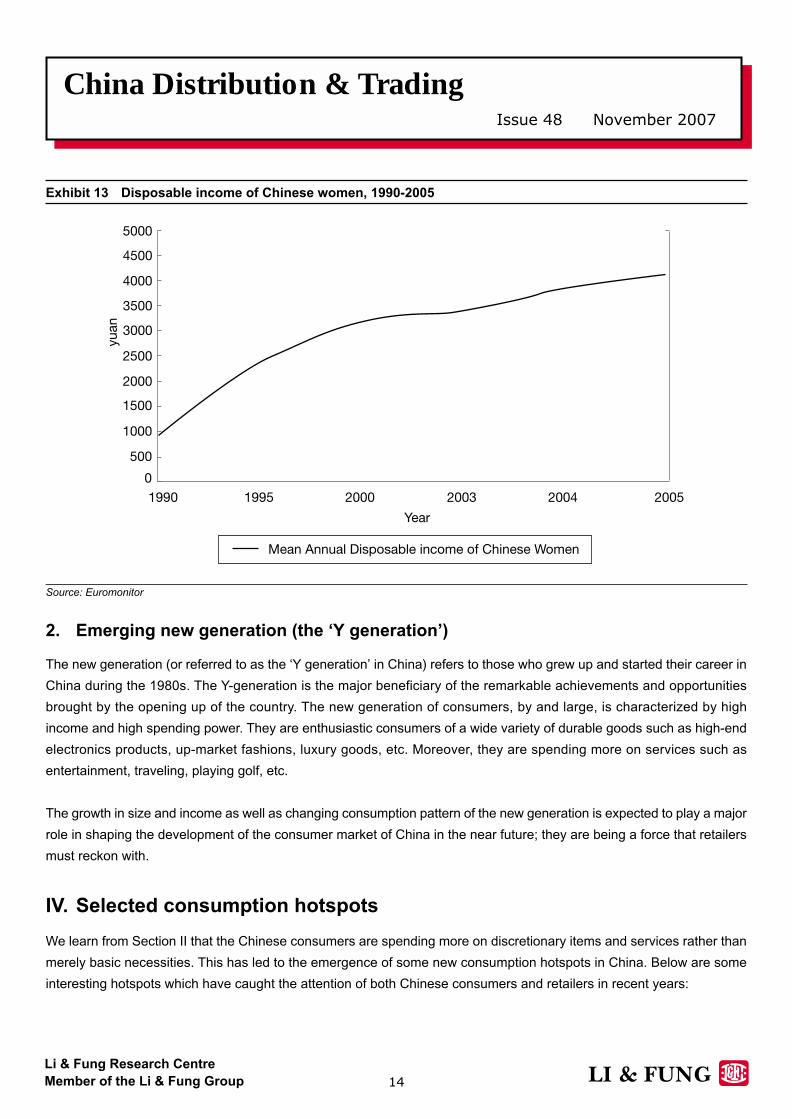

1. Rising female consumerism

Chinese women have attracted a lot of attention in the consumer market as they are gradually emerging as a major

consumption force. Exhibit 13 shows that their income has been rising fairly rapidly in the past few years. Being better

educated and with rising economic status, they have more control or freedom on their spending patterns. Ernst & Young

mentioned in its recent study that the total purchasing power of young women living on their own or in married childless

households was projected to rise from USD 180 billion in 2005 to USD 260 billion in 2015. Women have substantial say

over grocery and clothing purchases in households. And their influences on big-ticket items such as automobiles and

housing are also increasing. They are generally interested in cosmetics, exercise, clothes and jewelry and willing to spend

on luxuries.

China Distribution & TradingIssue 48 November 2007

14

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 13 Disposable income of Chinese women, 1990-2005

Source: Euromonitor

2. Emerging new generation (the ‘Y generation’)

The new generation (or referred to as the ‘Y generation’ in China) refers to those who grew up and started their career in

China during the 1980s. The Y-generation is the major beneficiary of the remarkable achievements and opportunities

brought by the opening up of the country. The new generation of consumers, by and large, is characterized by high

income and high spending power. They are enthusiastic consumers of a wide variety of durable goods such as high-end

electronics products, up-market fashions, luxury goods, etc. Moreover, they are spending more on services such as

entertainment, traveling, playing golf, etc.

The growth in size and income as well as changing consumption pattern of the new generation is expected to play a major

role in shaping the development of the consumer market of China in the near future; they are being a force that retailers

must reckon with.

IV. Selected consumption hotspots

We learn from Section II that the Chinese consumers are spending more on discretionary items and services rather than

merely basic necessities. This has led to the emergence of some new consumption hotspots in China. Below are some

interesting hotspots which have caught the attention of both Chinese consumers and retailers in recent years:

China Distribution & TradingIssue 48 November 2007

15

Li & Fung Research Centre

Member of the Li & Fung Group

1. Luxuries

Luxury products broadly refer to items bringing an elegant lifestyle, taste and quality. For Chinese consumers, it may

further represent indulgence, exclusiveness and a symbol of elevated social status. Some popular luxury items for

Chinese consumers include clothes, bags & footwear, watches, pens, cosmetics & perfumes and jewelry. According to

Ernst & Young, China is the world’s third largest consumer of high-end fashions, accessories and other luxury products,

with sales value of more than USD 2 billion a year. It is estimated that the sales value will exceed USD 11.5 billion,

accounting for 29% of the total world sales by 2015.

According to China Association of Branding Strategy, the luxury products market of China has approximately 170 million

potential consumers, or 13.5% of the total population. Of which, 10 to 13 million are active purchasers. The number of

potential customers is projected to reach 250 million by 2010.

There are two major luxuries consumer groups in China. One group comprises wealthy consumers, mostly ‘tai-tais’, who

are crowd-averse, seek personalized services and frequently visit luxury retail stores for the newest and most fashionable

products offerings. Another group consists of white-collar employees, usually employed by foreign companies, who are

willing to spend an entire month’s salary on a single purchase.

According to KPMG, many of these purchasers buy luxuries within Mainland China; quite a number of them made their

purchases in Hong Kong, Macau and Taiwan. For most luxury products such as cosmetics and perfume, bags & footwear,

watches and jewelry, about 40% of the Mainland consumers bought the items in Hong Kong, Macau and Taiwan in 2005.

And some reports pointed out that Chinese customers spend a lot on premium brands when they travel overseas,

especially in European countries such as France and Italy.

The premium brands, not daring missing this huge market, are investing a lot to lure more Chinese customers, especially

after the full opening-up of China’s retail sector to foreign investors in December 2004. And the trend is, they do not only

set foot in first-tier cities such as Beijing, Shanghai and Guangzhou, but are increasingly marching into second- and third-

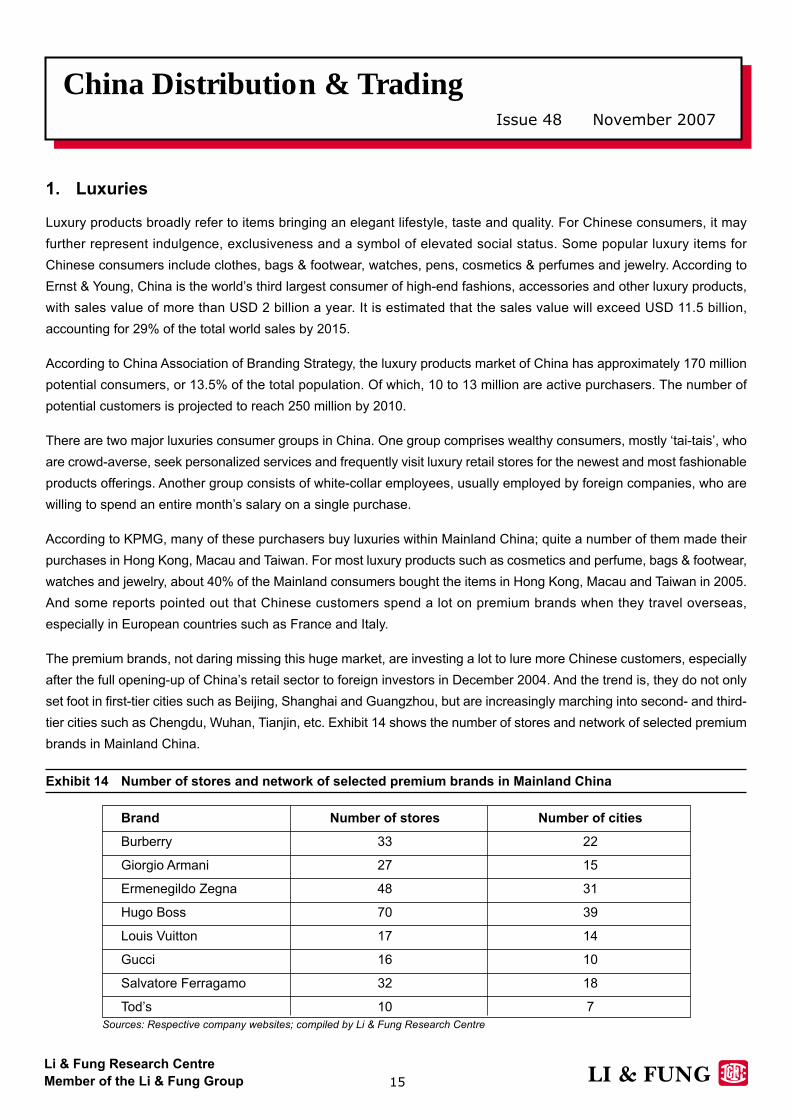

tier cities such as Chengdu, Wuhan, Tianjin, etc. Exhibit 14 shows the number of stores and network of selected premium

brands in Mainland China.

Exhibit 14 Number of stores and network of selected premium brands in Mainland China

Brand Number of stores Number of cities

Burberry 33 22

Giorgio Armani 27 15

Ermenegildo Zegna 48 31

Hugo Boss 70 39

Louis Vuitton 17 14

Gucci 16 10

Salvatore Ferragamo 32 18

Tod’s 10 7

Sources: Respective company websites; compiled by Li & Fung Research Centre

China Distribution & TradingIssue 48 November 2007

16

Li & Fung Research Centre

Member of the Li & Fung Group

2. Financial services

Financial service and product market is another emerging consumption hotspot in China. As a result of the influx of the

foreign banks and financial institutions into China after the deregulation of the banking sector in 2006, more financial

products and services are available for Chinese customers. They can consider investing in different types of financial

products or services rather than putting all their money into the saving accounts.

No doubt that credit card service is always a hot field banks wish to grab. However, Chinese customers have other new

financial needs such as mortgage, car loan and insurance. Bain & Company estimated that the total value of mortgage

loans would jump to some USD 725 billion and generate over USD 3 billion in banks’ after-tax profits by 2010. It also

anticipated that the total value of car loans would surge to around USD 50 billion by 2010.

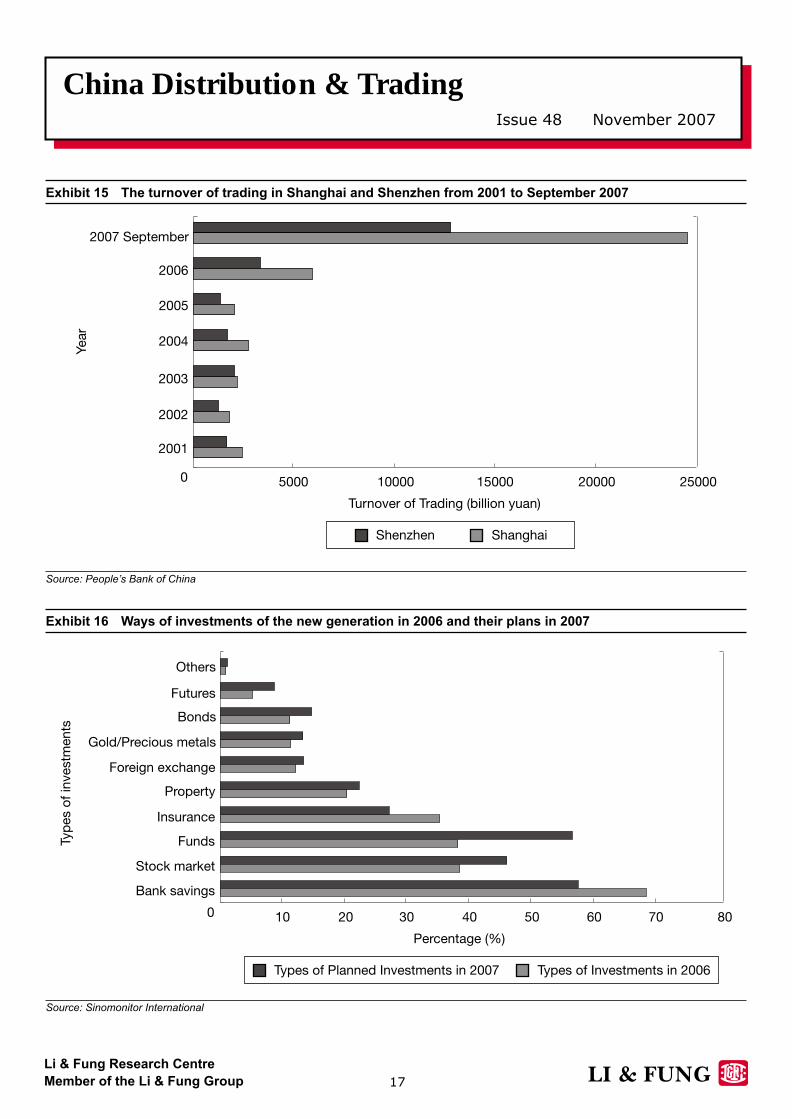

On the other hand, the red-hot stock market has brought huge opportunities for these financial institutions lately. The

turnover of trading in Shanghai and Shenzhen stock exchanges has been increasing enormously over the past two years

(see Exhibit 15). Many Chinese people have rushed to open trading accounts to bet on the stock market. According to the

China Securities Depository and Clearing Corporation, as of September 2007, the number of trading accounts has soared

to over 126 million, up by 65.6% yoy.

According to a survey conducted by Sinomonitor International, young adults with higher incomes have a more

adventurous attitude towards wealth management. Unlike the traditional Chinese who use only a very limited range of

financial services such as cash withdrawal or bank deposits, the younger generation tends to consume more types of

financial products/services such as stocks, funds and bonds rather than merely putting the money in their saving accounts

(see Exhibit 16).

Apart from consuming the services at the banks or other financial institutions, Chinese customers growingly prefer online

financial management, especially for those who are young and computer literate. According to CNNIC, among the 162

million of Internet users in China, about 20% of them managed their money via Internet. Bain & Company also predicted

that the penetration of Internet banking services in China would reach 30% of all computer users by next year.

China Distribution & TradingIssue 48 November 2007

17

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 15 The turnover of trading in Shanghai and Shenzhen from 2001 to September 2007

Source: People’s Bank of China

Exhibit 16 Ways of investments of the new generation in 2006 and their plans in 2007

Source: Sinomonitor International

China Distribution & TradingIssue 48 November 2007

18

Li & Fung Research Centre

Member of the Li & Fung Group

3. Vacation

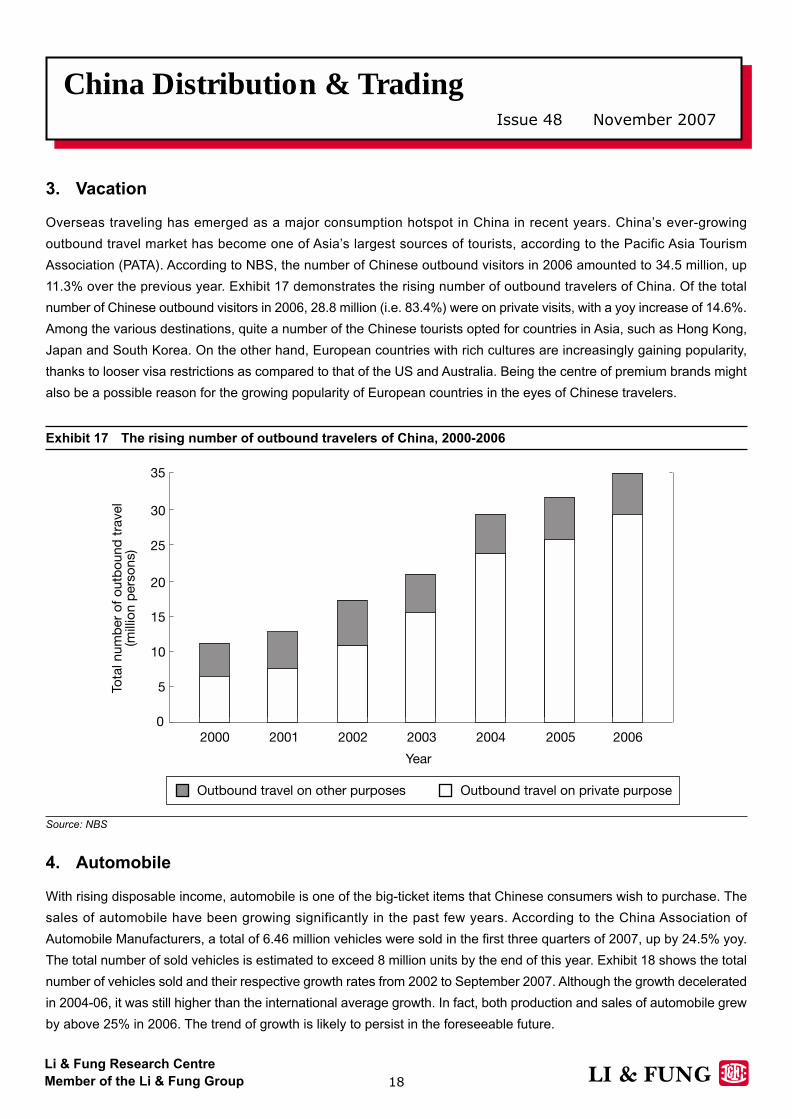

Overseas traveling has emerged as a major consumption hotspot in China in recent years. China’s ever-growing

outbound travel market has become one of Asia’s largest sources of tourists, according to the Pacific Asia Tourism

Association (PATA). According to NBS, the number of Chinese outbound visitors in 2006 amounted to 34.5 million, up

11.3% over the previous year. Exhibit 17 demonstrates the rising number of outbound travelers of China. Of the total

number of Chinese outbound visitors in 2006, 28.8 million (i.e. 83.4%) were on private visits, with a yoy increase of 14.6%.

Among the various destinations, quite a number of the Chinese tourists opted for countries in Asia, such as Hong Kong,

Japan and South Korea. On the other hand, European countries with rich cultures are increasingly gaining popularity,

thanks to looser visa restrictions as compared to that of the US and Australia. Being the centre of premium brands might

also be a possible reason for the growing popularity of European countries in the eyes of Chinese travelers.

Exhibit 17 The rising number of outbound travelers of China, 2000-2006

Source: NBS

4. Automobile

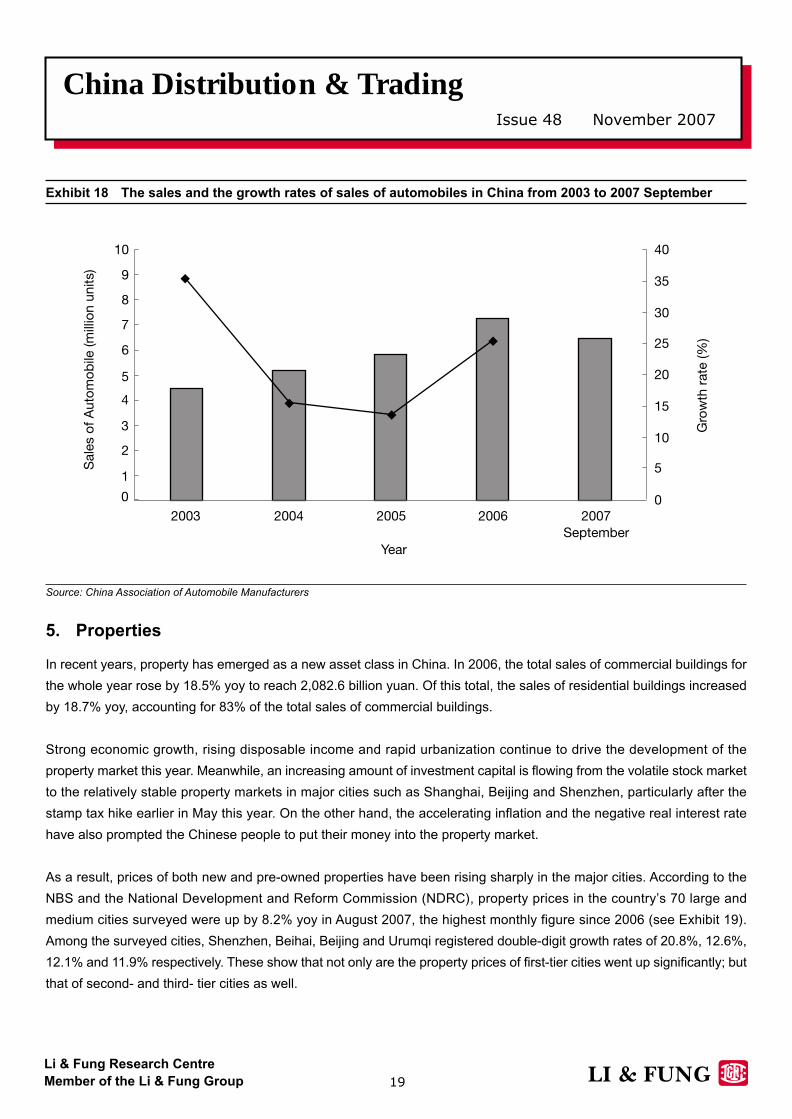

With rising disposable income, automobile is one of the big-ticket items that Chinese consumers wish to purchase. The

sales of automobile have been growing significantly in the past few years. According to the China Association of

Automobile Manufacturers, a total of 6.46 million vehicles were sold in the first three quarters of 2007, up by 24.5% yoy.

The total number of sold vehicles is estimated to exceed 8 million units by the end of this year. Exhibit 18 shows the total

number of vehicles sold and their respective growth rates from 2002 to September 2007. Although the growth decelerated

in 2004-06, it was still higher than the international average growth. In fact, both production and sales of automobile grew

by above 25% in 2006. The trend of growth is likely to persist in the foreseeable future.

China Distribution & TradingIssue 48 November 2007

19

Li & Fung Research Centre

Member of the Li & Fung Group

Exhibit 18 The sales and the growth rates of sales of automobiles in China from 2003 to 2007 September

Source: China Association of Automobile Manufacturers

5. Properties

In recent years, property has emerged as a new asset class in China. In 2006, the total sales of commercial buildings for

the whole year rose by 18.5% yoy to reach 2,082.6 billion yuan. Of this total, the sales of residential buildings increased

by 18.7% yoy, accounting for 83% of the total sales of commercial buildings.

Strong economic growth, rising disposable income and rapid urbanization continue to drive the development of the

property market this year. Meanwhile, an increasing amount of investment capital is flowing from the volatile stock market

to the relatively stable property markets in major cities such as Shanghai, Beijing and Shenzhen, particularly after the

stamp tax hike earlier in May this year. On the other hand, the accelerating inflation and the negative real interest rate

have also prompted the Chinese people to put their money into the property market.

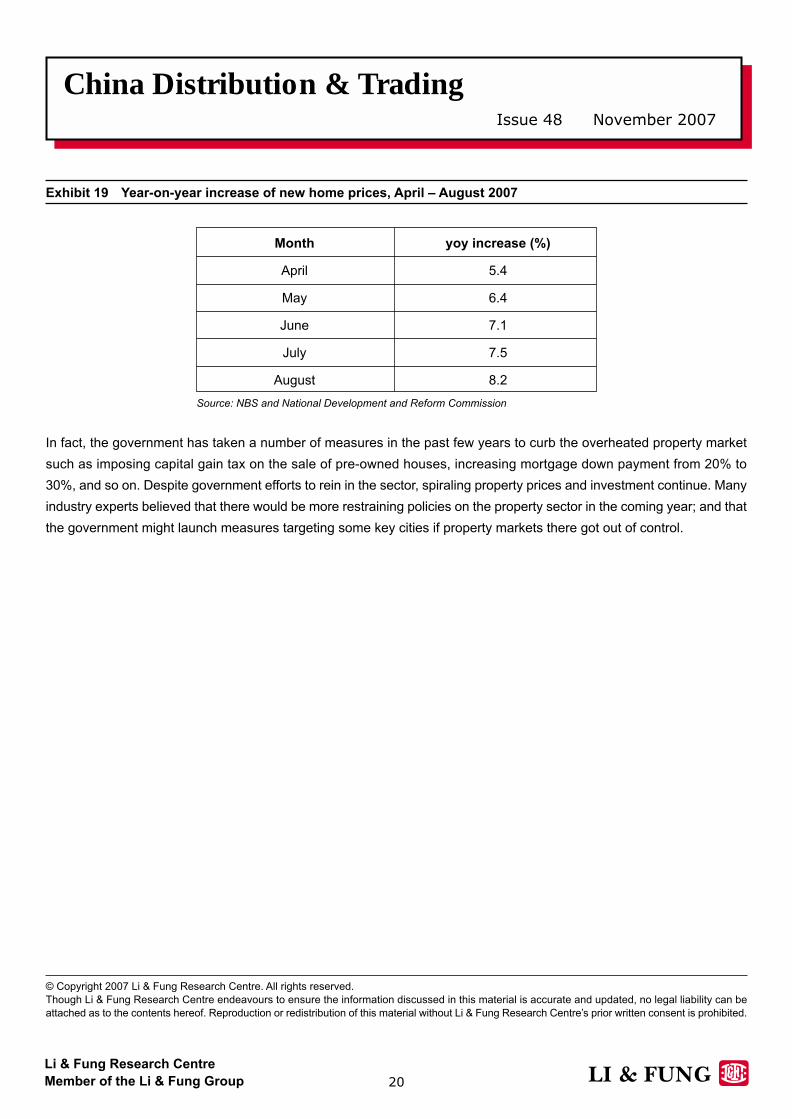

As a result, prices of both new and pre-owned properties have been rising sharply in the major cities. According to the

NBS and the National Development and Reform Commission (NDRC), property prices in the country’s 70 large and

medium cities surveyed were up by 8.2% yoy in August 2007, the highest monthly figure since 2006 (see Exhibit 19).

Among the surveyed cities, Shenzhen, Beihai, Beijing and Urumqi registered double-digit growth rates of 20.8%, 12.6%,

12.1% and 11.9% respectively. These show that not only are the property prices of first-tier cities went up significantly; but

that of second- and third- tier cities as well.

China Distribution & TradingIssue 48 November 2007

20

Li & Fung Research Centre

Member of the Li & Fung Group

© Copyright 2007 Li & Fung Research Centre. All rights reserved.

Though Li & Fung Research Centre endeavours to ensure the information discussed in this material is accurate and updated, no legal liability can be

attached as to the contents hereof. Reproduction or redistribution of this material without Li & Fung Research Centre’s prior written consent is prohibited.

Exhibit 19 Year-on-year increase of new home prices, April – August 2007

Month yoy increase (%)

April 5.4

May 6.4

June 7.1

July 7.5

August 8.2

Source: NBS and National Development and Reform Commission

In fact, the government has taken a number of measures in the past few years to curb the overheated property market

such as imposing capital gain tax on the sale of pre-owned houses, increasing mortgage down payment from 20% to

30%, and so on. Despite government efforts to rein in the sector, spiraling property prices and investment continue. Many

industry experts believed that there would be more restraining policies on the property sector in the coming year; and that

the government might launch measures targeting some key cities if property markets there got out of control.

Recommended