INDUSTRY PAPER:

THE LEATHER GOODS SECTOR (NON FOOTWEAR) OF

BANGLADESH

INDUSTRY PAPER:

THE LEATHER GOODS SECTOR (NON FOOTWEAR) OF

BANGLADESH

Prepared for:

Mohammad Saif Noman Khan

Assistant Professor

Prepared by:

Amreen Akhtar ID: 24

Md. Mushfiq Alam Arko ID: 34 (Group Leader)

01703803619

Nisa Nur Majumder ID: 36

Tapas Debnath ID: 40

Syeda Nawrin Huq ID: 41

Batch: MBA 52-D

Institute of Business Administration

University of Dhaka

January 2, 2015

iii

Contents

Executive Summary .............................................................................................................................. viii

1.0 INTRODUCTION ............................................................................................................................ 1

1.1 Origin of the Report ...................................................................................................................... 1

1.2 Objective of the Study .................................................................................................................. 1

1.3 Scope ................................................................................................................................................ 1

1.4 Methodology ................................................................................................................................... 2

1.5 Location of the Industry .............................................................................................................. 2

2.0 LEATHER INDUSTRY .................................................................................................................. 3

2.1 Global Market in Brief ................................................................................................................... 3

2.2 Global Leather Goods Market .................................................................................................... 3

2.2.1 Worldwide Leather Export and Import ............................................................................. 4

2.2.2 Recent Development ............................................................................................................. 6

2.2.3 Product Groups ...................................................................................................................... 8

3.0 BANGLADESH LEATHER INDUSTRY ........................................................................................ 11

3.1. History of Leather Industry in Bangladesh ......................................................................... 11

3.2. Leather Industry in Brief ........................................................................................................... 12

3.3 Market Structure .......................................................................................................................... 16

3.3.1 Demographic Concentration ............................................................................................. 16

3.3.2 Leather Goods Market Size in Bangladesh 2013 ......................................................... 16

3.4 Major Institutions involved in leather sector ....................................................................... 20

3.4.1 Leather Associations of Bangladesh .............................................................................. 20

3.4.2 Leather Institutions.............................................................................................................. 25

3.4.3 Leather Research Institutes .............................................................................................. 26

3.4.4 Government Bodies ............................................................................................................. 27

3.4.5 Private Organizations.......................................................................................................... 30

3.5 Leather Products in Bangladesh ....................................................................................... 30

3.5.1. Small Leather products ..................................................................................................... 31

3.5.2. Medium Leather Goods ..................................................................................................... 31

3.5.3 Heavy Leather Goods.......................................................................................................... 31

3.6 Marketing Leather goods .......................................................................................................... 32

3.6.1 Research ................................................................................................................................. 32

3.6.2 Strategies for Selling Products ................................................................................. 33

iv

3.6.3 Parameters ............................................................................................................................. 34

3.6.4 Marketing Tools .................................................................................................................... 34

3.7 Distribution Channel ................................................................................................................... 35

3.7.1 Raw Hide and Skin Collectors and Suppliers ............................................................... 35

3.7.2 Importers of Chemicals ...................................................................................................... 35

3.7.3 Leather Processing Units or Tanneries ......................................................................... 36

3.7.4 Wholesaler of Leather and Accessories ........................................................................ 37

3.7.5 Handmade Footwear Manufacturers ............................................................................... 37

3.7.6 Industrial Footwear Manufacturers ................................................................................. 38

3.7.7 Semi-industrial Footwear Manufacturers ...................................................................... 38

3.7.8 Handmade Leather Goods/Crafts Manufacturers ........................................................ 38

3.7.9 Industrial Leather Goods Manufacturers ....................................................................... 39

3.7.10 Semi-industrial Leather Goods Manufacturers .......................................................... 39

3.7.11 Wholesaler of Footwear ................................................................................................... 40

3.7.12 Retailers of Footwear, Leather Goods, and Leather Garments ............................. 40

3.7.13 Export Agent ....................................................................................................................... 40

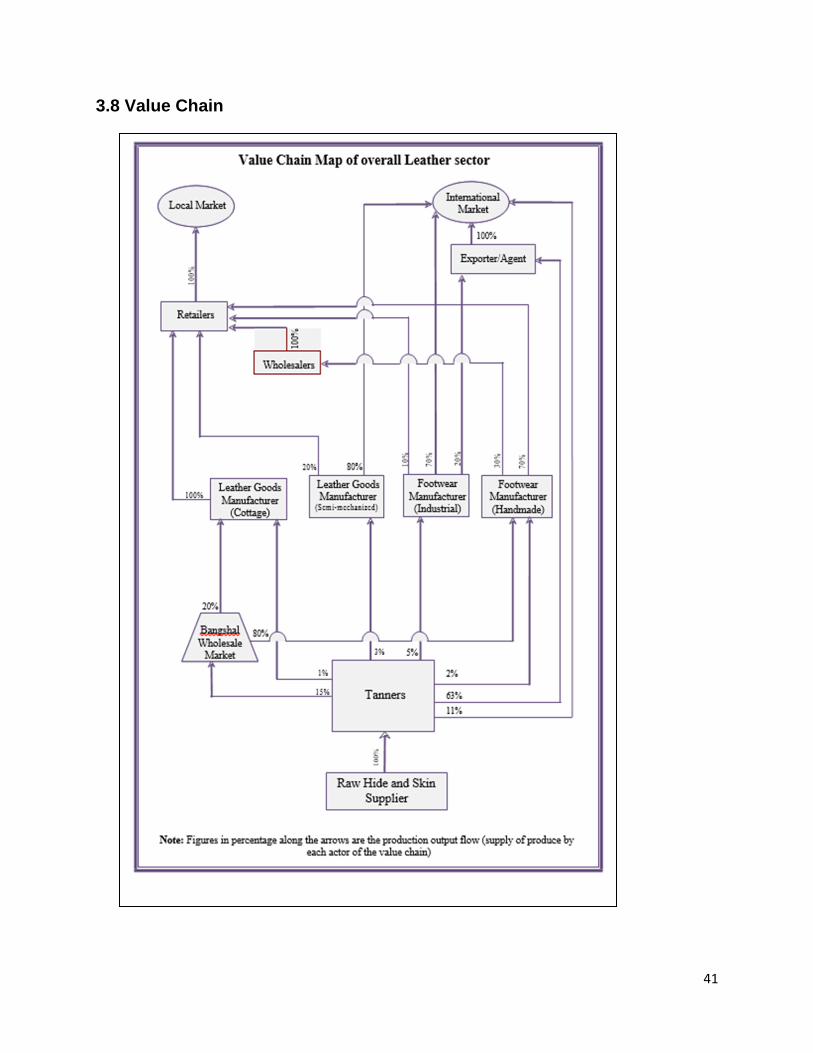

3.8 Value Chain ................................................................................................................................... 41

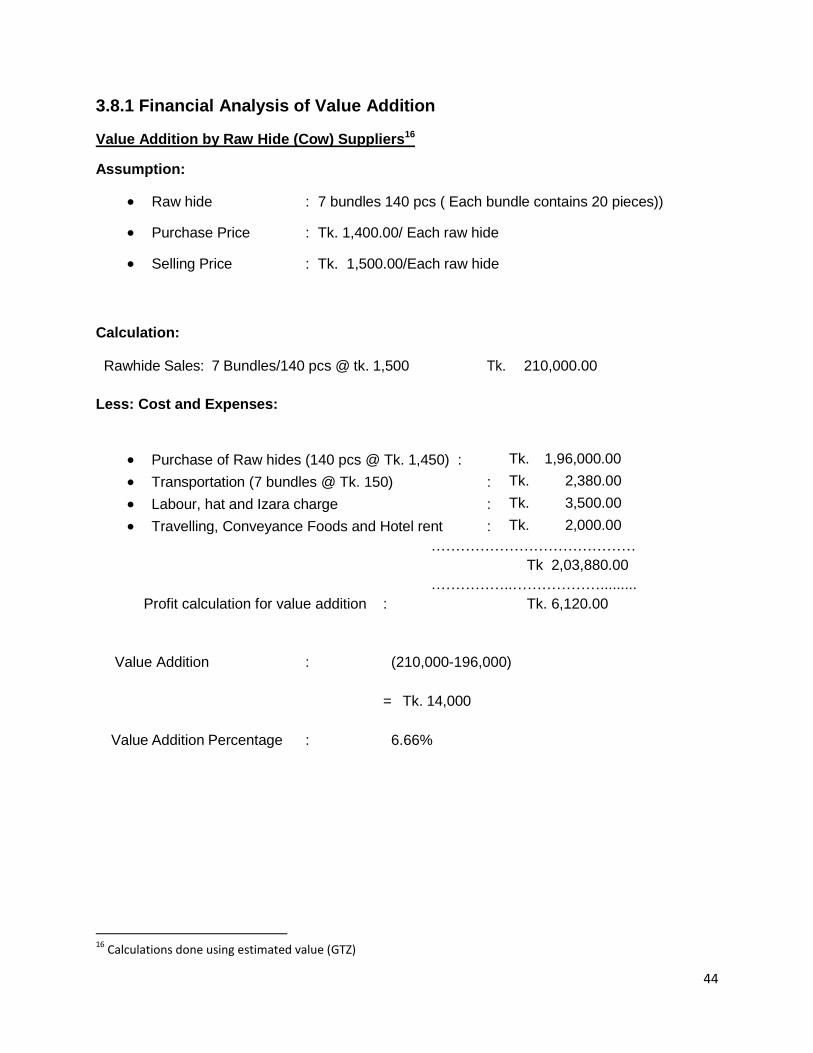

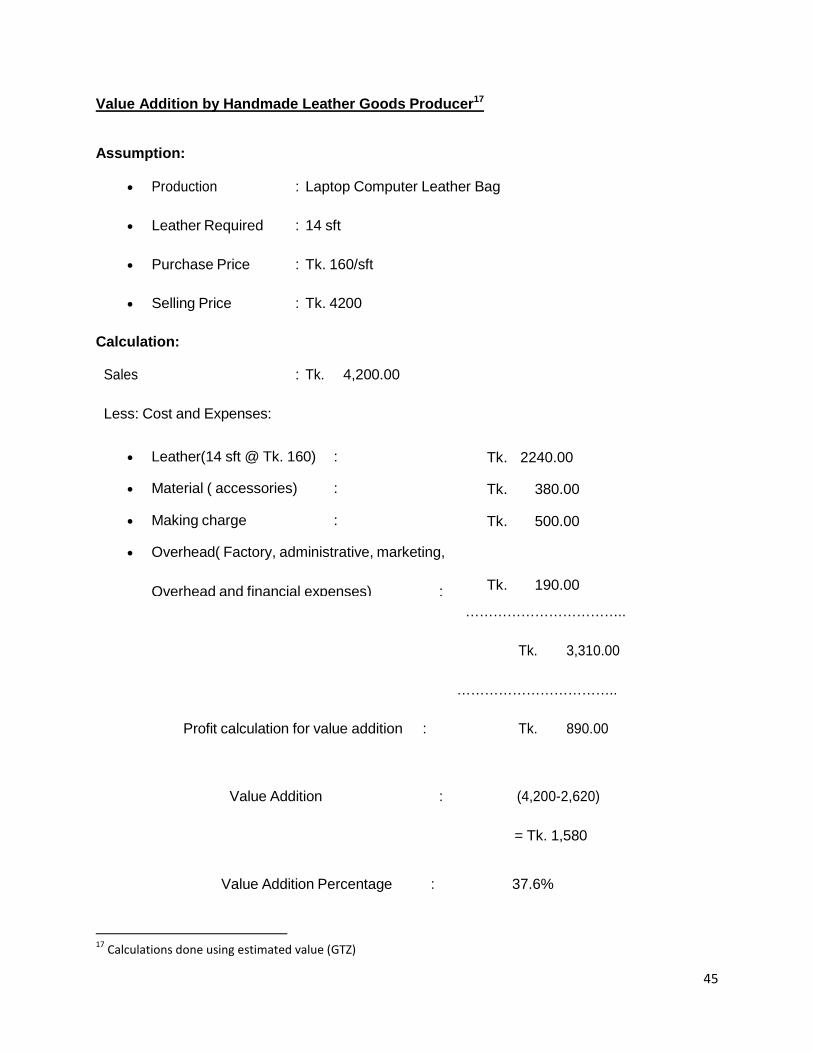

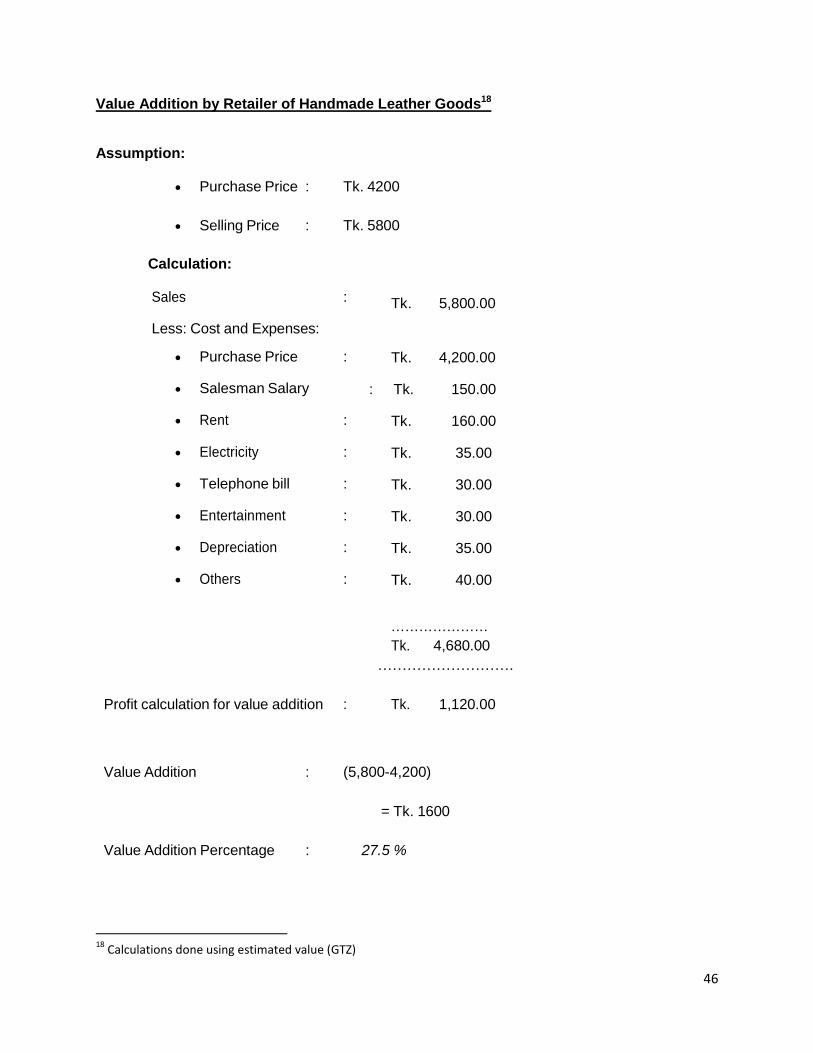

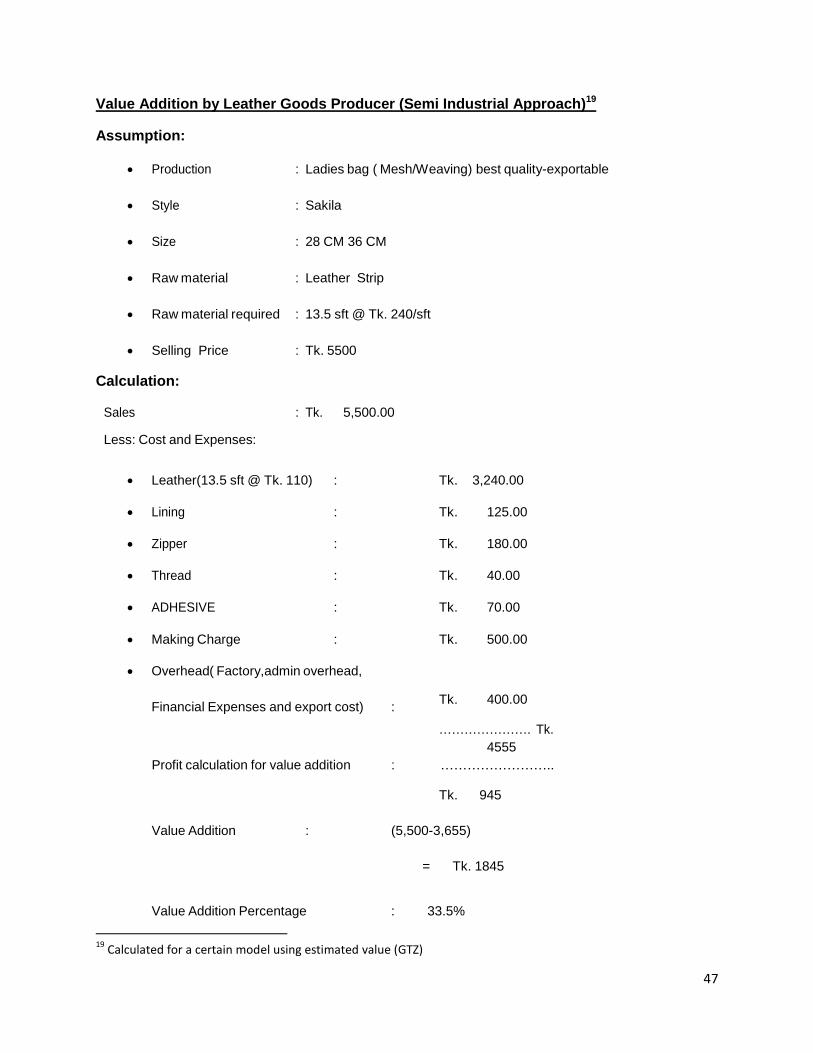

3.8.1 Financial Analysis of Value Addition .................................................................................. 44

3.9 Brief of Top Industry Players ................................................................................................... 48

3.9.1 APEX Leather ........................................................................................................................ 48

3.9.2 Bata Shoe Company (Bangladesh) Ltd. ......................................................................... 49

3.9.3 Leatherex Footwear Industry ............................................................................................ 50

3.9.4 Picard Bangladesh Limited ............................................................................................... 51

3.9.5 Ramim Leather & Finished Goods Corporation ........................................................... 51

3.9.6 Fortuna Bangladesh ............................................................................................................ 52

3.10 Legal Environment .................................................................................................................... 52

3.10.1 Bangladesh Environment Conservation Act, 1995 ................................................... 52

3.10.2 Relocation of Tanneries ............................................................................................... 53

3.10.3 Related Tax and other issues ..................................................................................... 54

3.10.4 Price Control ................................................................................................................... 54

4.0 INDUSTRY RISKS ............................................................................................................................ 55

4.1 Political Situation ........................................................................................................................ 55

4.2 Diseases and accidents ............................................................................................................. 55

v

4.3 Cheap Chinese Products (Dumping) ...................................................................................... 56

4.4 Smuggling of Leather ................................................................................................................. 56

4.5 Lack of Technical Knowhow in Designing ........................................................................... 56

4.6 Low investment in R&D ............................................................................................................. 56

4.7 Foreign Currency Fluctuation .................................................................................................. 56

4.8 Small Market ................................................................................................................................. 57

5.0 CRITICAL SUCCESS FACTORS .................................................................................................. 58

5.1 Competitive Pricing .................................................................................................................... 58

5.2 Quality of Products ..................................................................................................................... 58

5.3 Strong Distribution Channel ..................................................................................................... 58

5.4 Cost Control .................................................................................................................................. 58

5.5 Meeting Ecological Standards ................................................................................................. 59

5.6 Ensuring Government Support ................................................................................................ 59

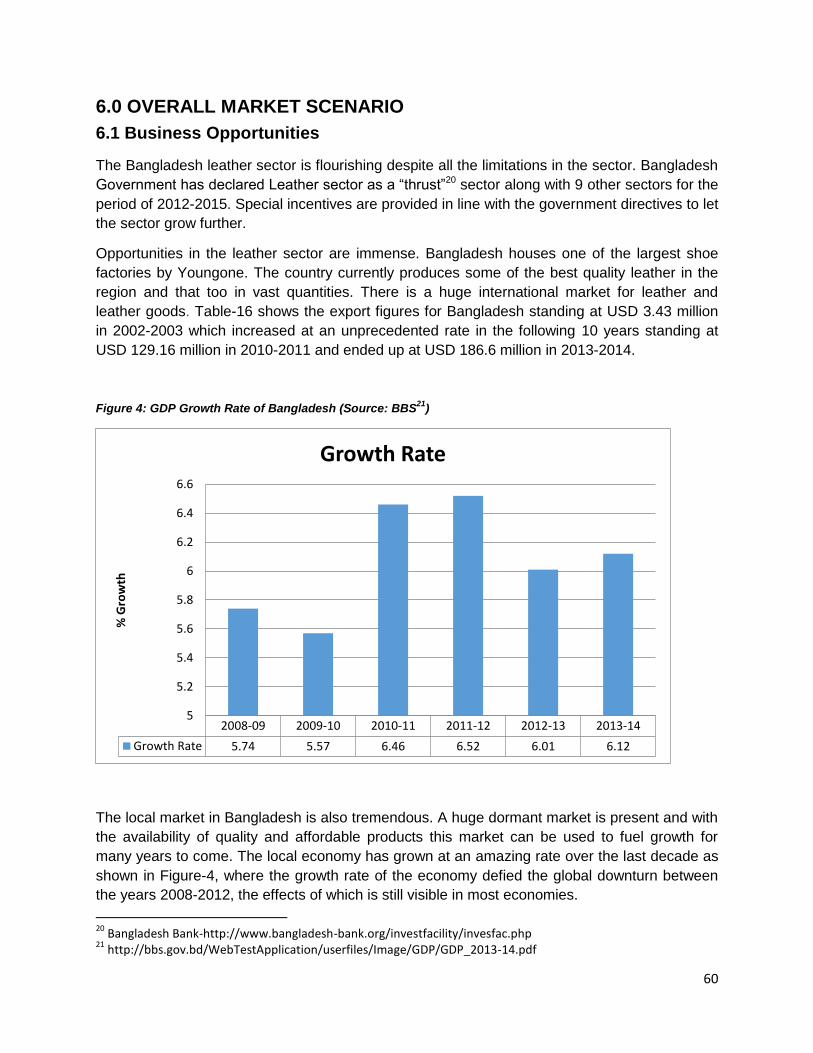

6.0 OVERALL MARKET SCENARIO .................................................................................................. 60

6.1 Business Opportunities ............................................................................................................. 60

6.2 PESTEL Analysis ......................................................................................................................... 66

6.3 SWOT Analysis ............................................................................................................................ 68

6.4 Limitations Faced by the Industry .......................................................................................... 70

7.0 SUMMARY OF THE FINDINGS ..................................................................................................... 72

BIBLIOGRAPHY ...................................................................................................................................... 73

APPENDICES........................................................................................................................................... 74

vi

List of Figures

Figure 1: Export trends of countries in 2012 .................................................................................... 5

Figure 2: % Contribution to GDP ....................................................................................................... 13

Figure 3: Export Growth Rates of Leather and Leather Goods for the Years 1998-2005

(Source: Bangladesh Bureau of Statistics and Export Promotion Bureau) ........................... 14

Figure 4: GDP Growth Rate of Bangladesh (Source: BBS) ........................................................ 60

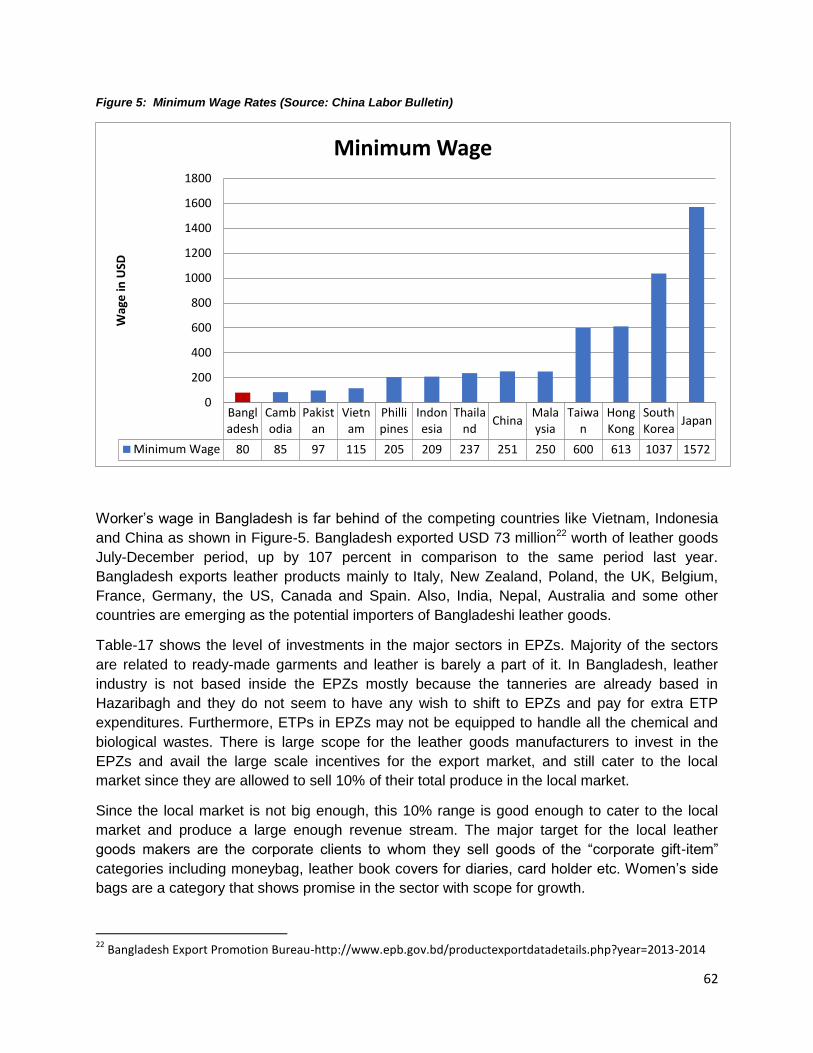

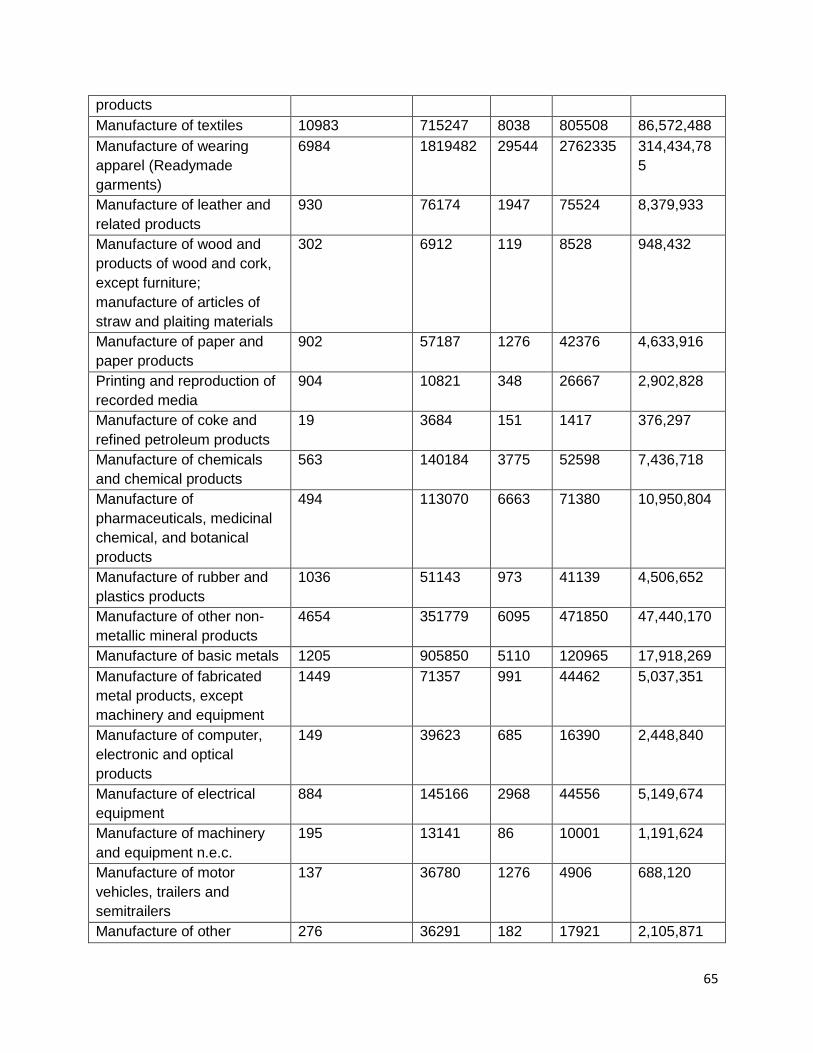

Figure 5: Minimum Wage Rates (Source: China Labor Bulletin).............................................. 62

Figure 6: Leather Goods Manufacturers in Bangladesh (Source: Bangladesh Bureau of

Statistics) ................................................................................................................................................. 64

vii

List of Tables

Table 1: Imports and Exports of Leather and Leather Goods Worldwide (Source: UN

Comtrade)................................................................................................................................................... 4

Table 2: Major Exporting Countries in 2012 (Source: UN Comtrade) ........................................ 5

Table 3: Importing countries 2012 (Source: UN Comtrade) .......................................................... 6

Table 4: List of Leather Product Groups and Products ................................................................. 8

Table 5: List of Leather Goods Produced in Bangladesh ........................................................... 15

Table 6: Footwear Sector Growth (Source: Bangladesh Bureau of Statistics) ..................... 18

Table 7: Leather Goods Subsector Growth (Source: Bangladesh Bureau of Statistics) .... 18

Table 8: Employment in the Leather Sector Value Chain (Source: GTZ) ................................ 19

Table 9: Distribution of Value Addition across all Value Chain (Source: GTZ) ..................... 19

Table 10: Major Associations in the Leather Sector (Source: GTZ) ......................................... 20

Table 11: List of Major Leather Institutes (Source: GTZ) ............................................................ 25

Table 12: List of Major Leather Research Institutes (Source: GTZ) ......................................... 26

Table 13: List of Government Bodies Working in the Leather Sector (Source: GTZ) .......... 27

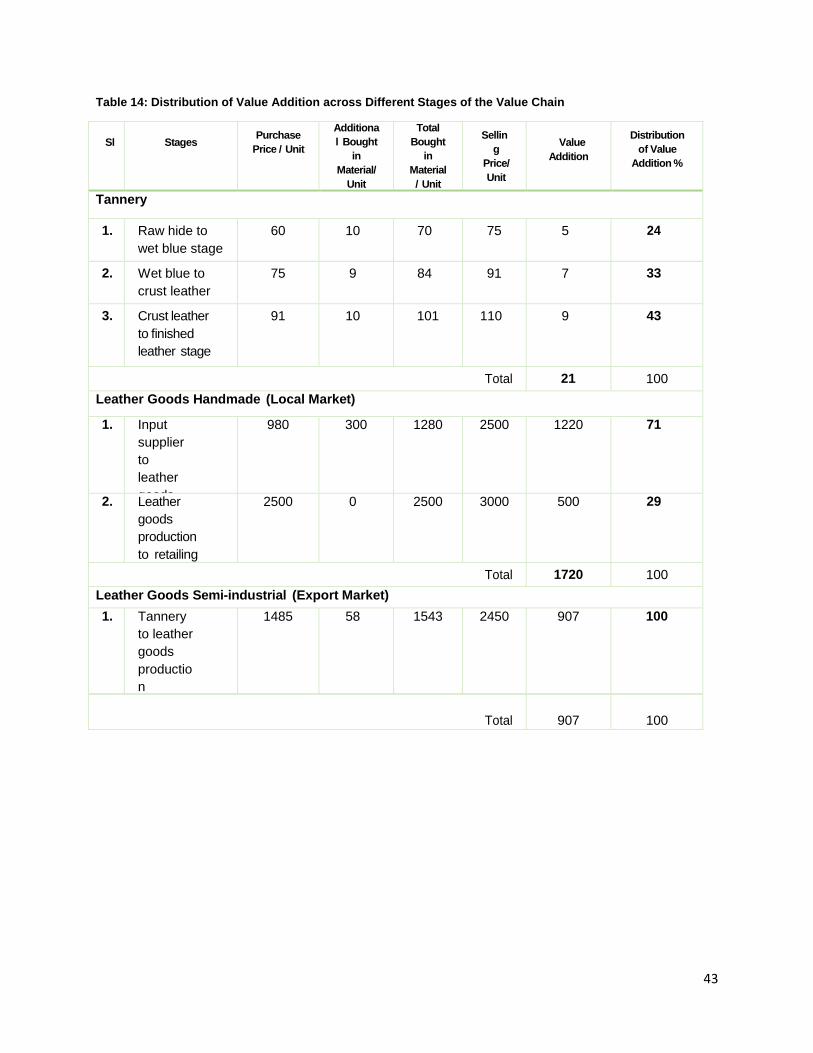

Table 14: Distribution of Value Addition across Different Stages of the Value Chain ........ 43

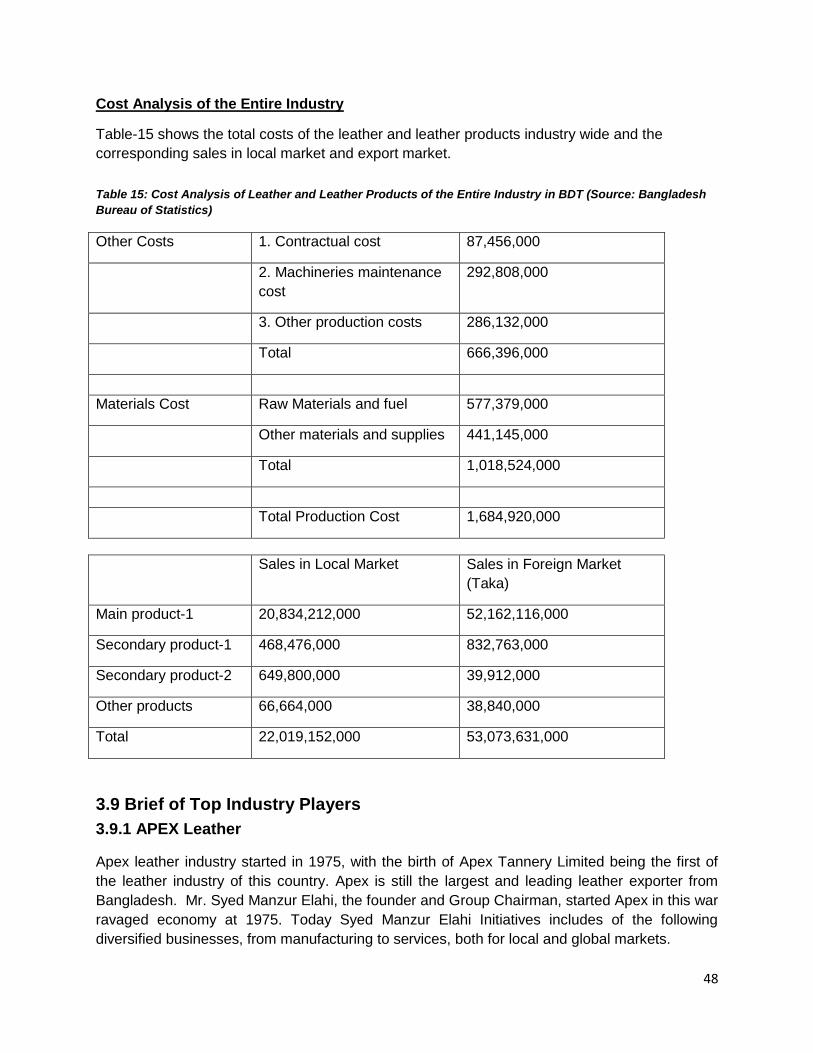

Table 15: Cost Analysis of Leather and Leather Products of the Entire Industry in BDT

(Source: Bangladesh Bureau of Statistics) ..................................................................................... 48

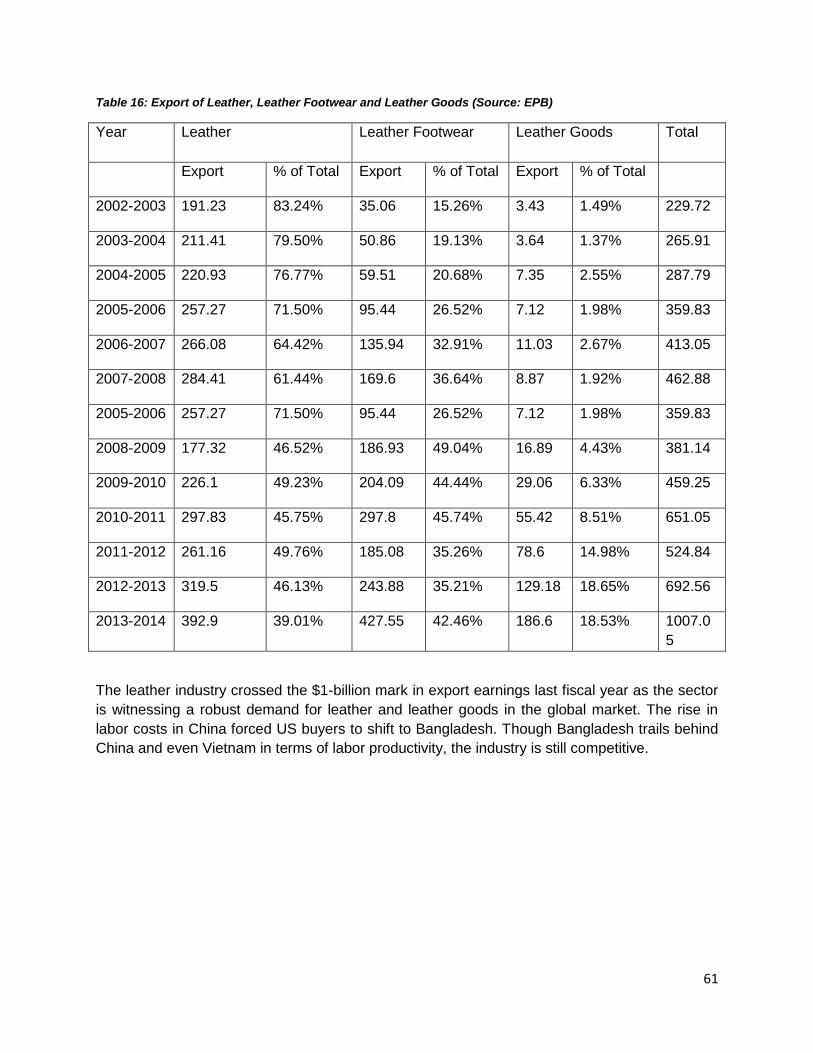

Table 16: Export of Leather, Leather Footwear and Leather Goods (Source: EPB) ............ 61

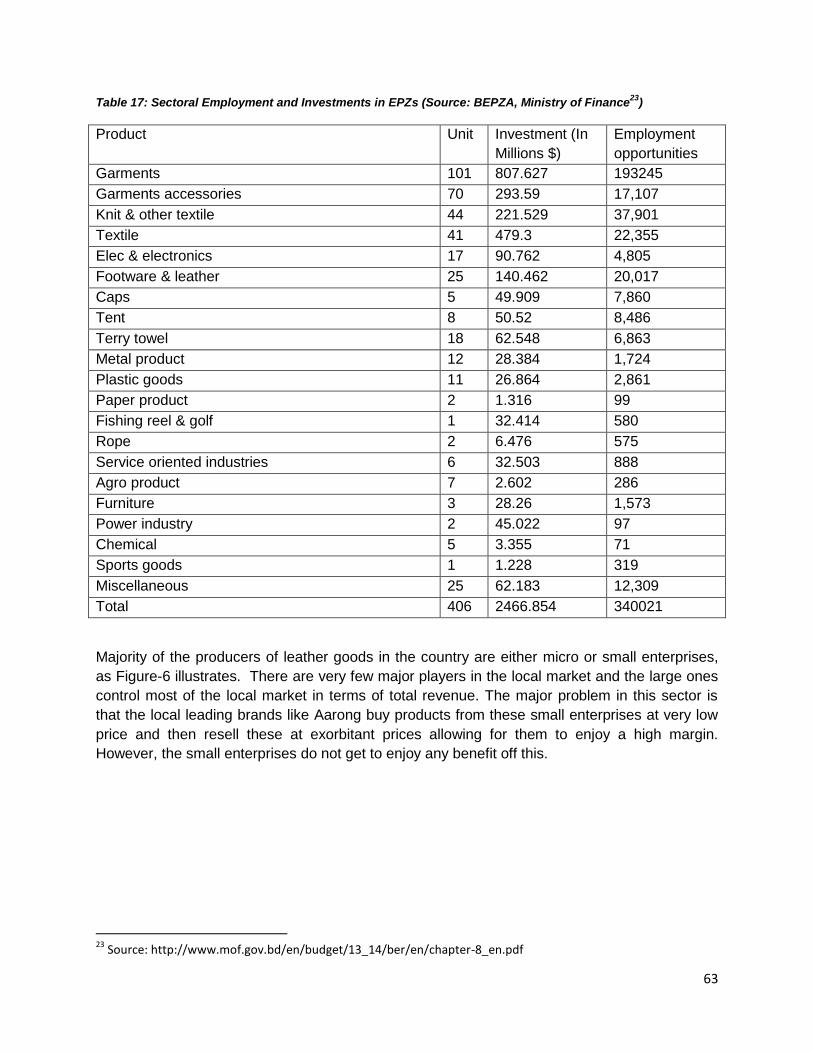

Table 17: Sectoral Employment and Investments in EPZs (Source: BEPZA, Ministry of

Finance) .................................................................................................................................................... 63

Table 18: Employment, Output, Tax and Salaries Provided by Leading Industries (Source:

Bangladesh Bureau of Statistics) ...................................................................................................... 64

viii

Executive Summary

This report collected all the information available of the leather industry, concentrating upon the

non-footwear product segment that is important for all the stakeholders of the industry. The

leather sector has been declared a “thrust” sector by the government which lead to a number of

incentives provided by the government along with the regular incentives provided for the

industries, including:

7% interest rate for commercial loans as declared by the central bank.

15% cash incentives for exports.

Full repatriation of profits for foreign investors, and that too without prior permission from

the central bank.

Duty free import of capital machineries during primary set up.

Relief from double taxation.

GSP facilities

Furthermore, EPZs in the country provide the following major incentives:

10 years of tax holiday for industries set up before 1st Jan, 2012.

For those set up after 31st Dec 2011:

Tax Exemption Period Rate of Tax Exemption

First 2 years 100%

Next 2 years 50%

Next 1 year 25%

Duty free import of construction materials, machineries, office equipment, spare parts,

raw materials and finished goods.

Relief from dividend tax.

Duty and quota free access to EU, Canada, Norway and Australia.

The leather industry in the country starts with the collection of raw hides by the tanneries that

process it using mostly imported chemicals and machineries into finished leather. Currently

there are restrictions upon export of unprocessed or semi-processed hides. Major portion of the

finished leather is exported to EU countries, while the remaining are used to produce leather

footwear and leather goods majority of which is exported as well.

Leather goods market is very minimal in the country, most of which is comprised of corporate

gift items like leather book cover for diaries, cardholders, wallet etc. Consumer items include

wallet, side bags for women, belts etc. Major segment of the leather market consists of micro

and small enterprises at 54% of the total number. These enterprises mostly sell directly to

corporate clients and to major consumer brand shops like Aarong, Deshal, Jatra etc. The major

brands then sell these products to the consumers under their name. To increase the profit

margin and cut off the intermediaries, some small business set up a brand, Leather Cave,

together and sells all their products under the same brand name directly to consumers.

The country has seen strong growth at over 5% over the last decade and enjoyed strong growth

in the exports of leather, leather footwear, and leather goods. Exports of leather goods

increased from USD 3.43 million in 2002-2003 to USD 129.16 million in 2010-2011 and ended

ix

up at USD 186.6 million in 2013-2014 despite high political turmoil, natural disasters, global

recession in the recent past.

The country enjoys major advantage in this labor-intensive segment, as the wage rate of

Bangladeshi workers at about 85 USD is far lower than that of the Chinese, Vietnamese and

Indian competitors. Furthermore, the leather from Bangladeshi hides is of superior quality due to

environmental factors like humidity. This allows for the products to be priced at higher rates,

bringing in extra revenues.

There are a lack of ETP usage and control in the leather industry. As a result, the pricing of

leather goods get affected. The government is working on the shifting of the tanneries to Savar,

from Hazaribagh. This will allow for the products being marked as more eco-friendly, leading to

them being priced much higher. However, the shifting of the tanneries will affect the micro and

small enterprises producing leather goods as they will not be accommodated in the government-

sanctioned land and will have to avail expensive lands outside the tannery region.

1

1.0 INTRODUCTION

As a developing country in the third world nation, Bangladesh has a steady GDP growth at a

significant rate of 6 percent in the last five years. The leather industry is one of the driving forces

for the GDP growth rate of Bangladesh, ranking 4th largest export earnings in 20131

contributing about 6% of total export earnings last year.

Bangladesh has a long established tanning industry producing around 2-3% of the world`s

leather from a ready supply of raw materials, the leather is widely known around the world for its

high quality of the fine grain pattern uniform fiber structure, smooth feel with natural fine texture.

About 95% of leather and leather products of Bangladesh are marketed abroad, mostly in the

form of crushed leather, finished leather, leather garments, and footwear. Most leather and

leather goods are exported to Germany, Italy, France, Netherlands, Spain, Russia, Brazil,

Japan, China, Singapore and Taiwan.

The leather industry is perfectly suitable to Bangladesh with its abundance of labor and natural

resources at internationally competitive rates; the leather industry of this country provides a

strong stream of good quality leather and has all the potential to be one of the significant export

earners in the global leather sector.

1.1 Origin of the Report

The report “THE LEATHER GOODS SECTOR (NON FOOTWEAR) OF BANGLADESH” was

commissioned by Mohammad Saif Noman Khan, Assistant Professor, Institute of Business

Administration, University of Dhaka as a term paper for the course Financial Managerial

Communication (C-501). This report was written by, Amreen Akhtar (ID-24), Md. Mushfiq Alam

Arko (ID-34), Nisa Nur Majumder (ID-36), Tapas Debnath (ID-40) and Syeda Nawrin Huq (ID-

41) of the MBA batch of 52D of Institute of Business Administration, University of Dhaka.

1.2 Objective of the Study

This report will act as an industry paper, gathering all necessary information concerning all the

stakeholders of the industry.

1.3 Scope

This report has concentrated mostly upon the “non-footwear leather goods industry”.

1 (Technical Report: Leather Sector Includes a Value Chain Analysis and Proposed actions)

2

1.4 Methodology

The data illustrated in this report are both from secondary and tertiary sources and have been

cited where appropriate. Secondary data has been collected from UN Comtrade, World

Statistics Compendium from FAO, Future Trends of the World from UNIDO, Bangladesh Bureau

of Statistics, Bangladesh Bank, Ministry of Finance and the Ministry of Industries of the

Government of Bangladesh. Tertiary data has been collected from reports published by GTZ.

1.5 Location of the Industry

Bangladesh, with a population of about 152.5 million in a total area of 147,570 square kilometer,

is heavily populated country. The leather industry is concentrated at Hazaribagh in Dhaka, with

186 tanneries out of 207 is located in Hazaribagh. In an area of only 70 acres land, Hazaribagh

produces about 84% of the total supply of the processed leather.

Even though the accommodation of the tanneries provides many benefits such as raw

materials, sharing knowledge, spare parts by the investors, along with development of vertical

and horizontal integrations of the industry.

Apart from only these few benefits Hazaribagh is a not the perfect place for the leather industry,

as the area lacks of proper sewerage facilities as it was previously built for residential area and

the number of Tanneries are increasingly exponential, this causes the land area to be limited,

making it not possible for effluent treatment2.

2 H. L. PAUL

3

2.0 LEATHER INDUSTRY

2.1 Global Market in Brief

Global Leather industry dealing with raw leather, finished leather and leather products is

flourishing. Leather and leather products are widely traded globally and used universally.

Playing a prominent role in the world economy, the leather and leather goods industry chalks up

approximately USD 100 Billion3 trade per year (UNIDO, 2010).

With the world population increasing dramatically in the 20th century and the current economic

and population growth trend of developing countries will ensure the increase in the growing use

of leather and leather products (FAO, 2013). The growing population and the overall increase in

wealth leads to the increase in the consumption of meat and hence kept the supply of raw

material fairly constant4 . Predictions indicate that the supply of raw material will continue to

grow following the trend of population growth, though higher costs and decreasing pasturing

land and higher consumption of poultry and pork in Asia and Africa seem to exist.

These might eventually lead to sourcing of raw materials from alternate markets and animals

like camel, deer, kangaroo etc. (UNIDO, 2010). Globally, the supply of leather has increased by

0.8% per year between the years 1986-2003 from bovine, 0.3% from sheep and 3.6% from goat

and 38% of output of raw lather was traded globally in 2001-035 which exceed by over a third of

the figure in 1980s. However, goatskin exports have decreased as countries are holding on to

their raw materials for local industries for processing and production of finished goods (FAO,

2013).

2.2 Global Leather Goods Market

In the professional jargon of the leather industries, the term “leather goods” covers a wide range

of Items such as all kinds of handbags, attaché cases, luggage and other travel goods, flat or

small items(e.g., purses, wallets), belts, etc., but excludes other leather products, such as

leather upholstery and Leather clothing (UNIDO, 2010).

In most languages, this term simply means “items made of leather”, e.g., Indonesian,

“barangkulit,” in Arabic, “mewed min Jeld,” in German, “Lederwaren,” and in the French term

“maroquinerie” since it comes from the word “Maroc” (Morocco), where quality goats were

reared and source of the marvelous quality leather called “le maroquin.”

The history of leather industry is distinctive with the regular shifts in end uses and materials,

from the age of horse and foot transport to the automobile era, from the use of leather products

for specific functional purposes in the current market of luxury goods. Large amounts of leather

goods have been and are still made in small craft shops. Therefore, statistics are scarce, not

always reliable, or based on informal communications. Due to the wide variety of products, with

3 Future Trends in the World Leather and Leather Products Industry and Trade, UNIDO, 2010

4 World Statistical Compendium for raw hides and skins, leather and leather footwear, FAO 1993-2012

5 FAO

4

different functions, sizes, constructions, and material structures, available production and trade

statistics are expressed in value rather than in natural (volume) terms (UNIDO, 2010).

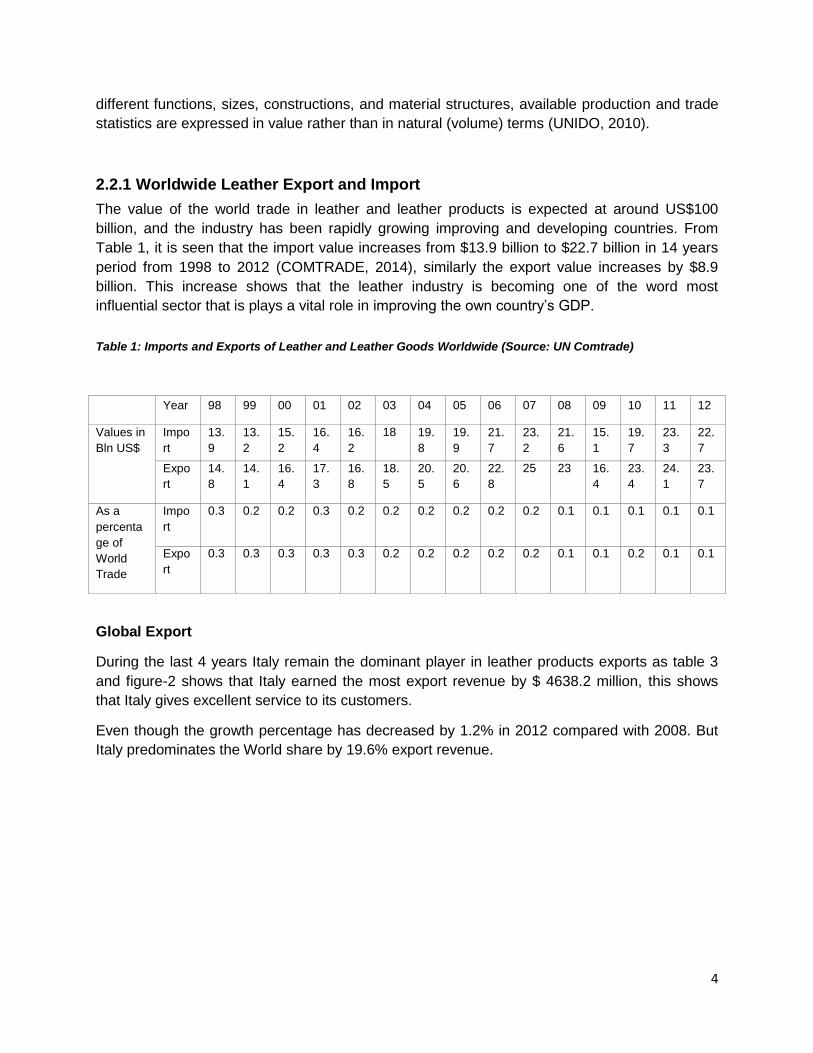

2.2.1 Worldwide Leather Export and Import

The value of the world trade in leather and leather products is expected at around US$100

billion, and the industry has been rapidly growing improving and developing countries. From

Table 1, it is seen that the import value increases from $13.9 billion to $22.7 billion in 14 years

period from 1998 to 2012 (COMTRADE, 2014), similarly the export value increases by $8.9

billion. This increase shows that the leather industry is becoming one of the word most

influential sector that is plays a vital role in improving the own country’s GDP.

Table 1: Imports and Exports of Leather and Leather Goods Worldwide (Source: UN Comtrade)

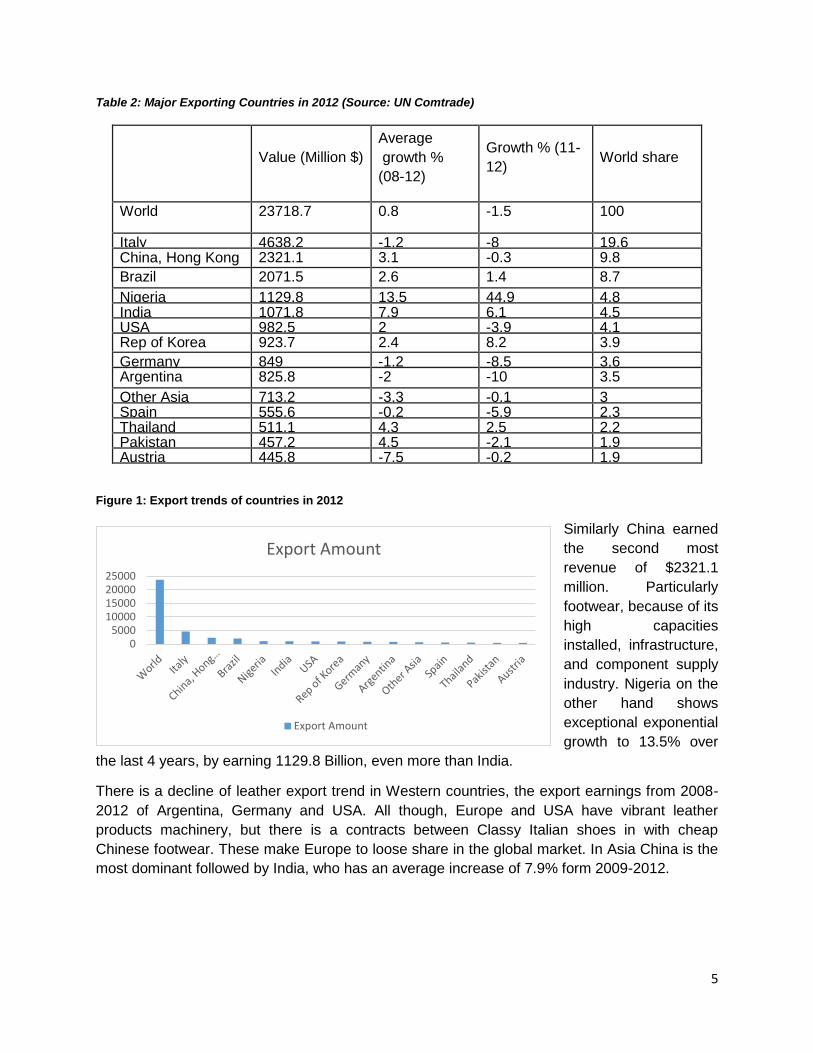

Global Export

During the last 4 years Italy remain the dominant player in leather products exports as table 3

and figure-2 shows that Italy earned the most export revenue by $ 4638.2 million, this shows

that Italy gives excellent service to its customers.

Even though the growth percentage has decreased by 1.2% in 2012 compared with 2008. But

Italy predominates the World share by 19.6% export revenue.

Year 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Values in

Bln US$

Impo

rt

13.

9

13.

2

15.

2

16.

4

16.

2

18 19.

8

19.

9

21.

7

23.

2

21.

6

15.

1

19.

7

23.

3

22.

7

Expo

rt

14.

8

14.

1

16.

4

17.

3

16.

8

18.

5

20.

5

20.

6

22.

8

25 23 16.

4

23.

4

24.

1

23.

7

As a

percenta

ge of

World

Trade

Impo

rt

0.3 0.2 0.2 0.3 0.2 0.2 0.2 0.2 0.2 0.2 0.1 0.1 0.1 0.1 0.1

Expo

rt

0.3 0.3 0.3 0.3 0.3 0.2 0.2 0.2 0.2 0.2 0.1 0.1 0.2 0.1 0.1

5

Table 2: Major Exporting Countries in 2012 (Source: UN Comtrade)

Value (Million $)

Average

growth %

(08-12)

Growth % (11-

12) World share

World 23718.7 0.8 -1.5 100

Italy 4638.2 -1.2 -8 19.6 China, Hong Kong

SAR

2321.1 3.1 -0.3 9.8

Brazil 2071.5 2.6 1.4 8.7

Nigeria 1129.8 13.5 44.9 4.8 India 1071.8 7.9 6.1 4.5 USA 982.5 2 -3.9 4.1 Rep of Korea 923.7 2.4 8.2 3.9

Germany 849 -1.2 -8.5 3.6 Argentina 825.8 -2 -10 3.5

Other Asia 713.2 -3.3 -0.1 3 Spain 555.6 -0.2 -5.9 2.3 Thailand 511.1 4.3 2.5 2.2 Pakistan 457.2 4.5 -2.1 1.9 Austria 445.8 -7.5 -0.2 1.9

Figure 1: Export trends of countries in 2012

Similarly China earned

the second most

revenue of $2321.1

million. Particularly

footwear, because of its

high capacities

installed, infrastructure,

and component supply

industry. Nigeria on the

other hand shows

exceptional exponential

growth to 13.5% over

the last 4 years, by earning 1129.8 Billion, even more than India.

There is a decline of leather export trend in Western countries, the export earnings from 2008-

2012 of Argentina, Germany and USA. All though, Europe and USA have vibrant leather

products machinery, but there is a contracts between Classy Italian shoes in with cheap

Chinese footwear. These make Europe to loose share in the global market. In Asia China is the

most dominant followed by India, who has an average increase of 7.9% form 2009-2012.

05000

10000150002000025000

Export Amount

Export Amount

6

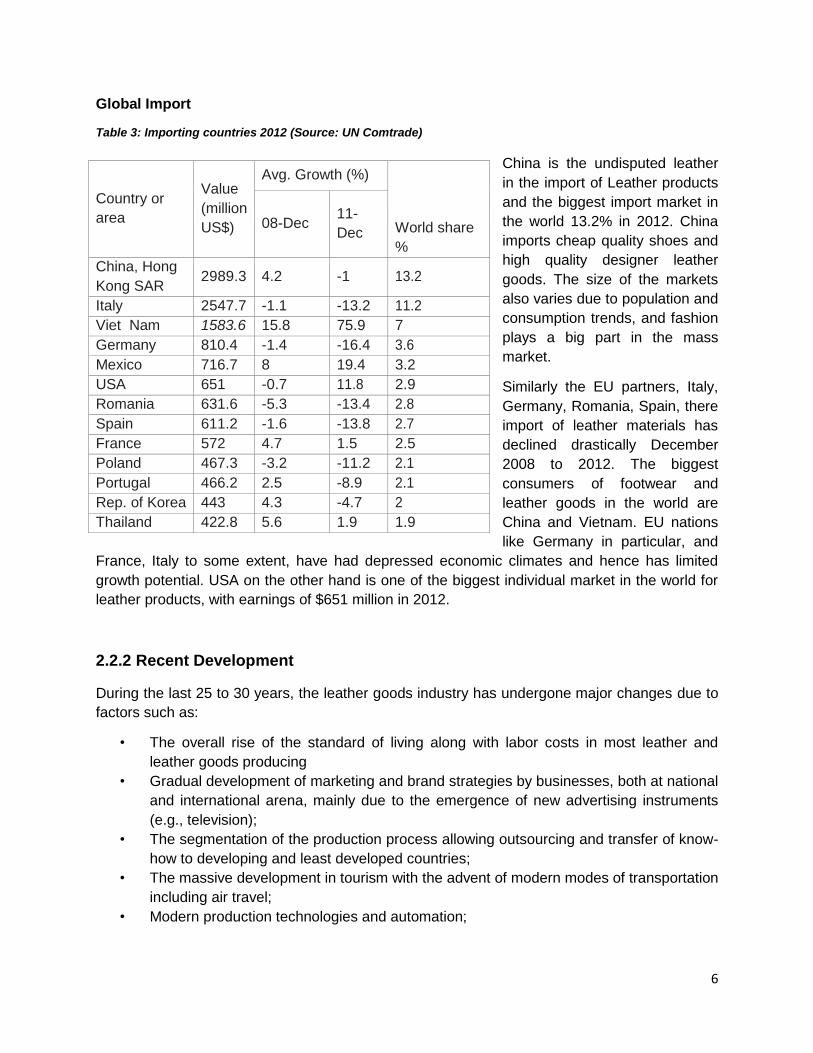

Global Import

Table 3: Importing countries 2012 (Source: UN Comtrade)

China is the undisputed leather

in the import of Leather products

and the biggest import market in

the world 13.2% in 2012. China

imports cheap quality shoes and

high quality designer leather

goods. The size of the markets

also varies due to population and

consumption trends, and fashion

plays a big part in the mass

market.

Similarly the EU partners, Italy,

Germany, Romania, Spain, there

import of leather materials has

declined drastically December

2008 to 2012. The biggest

consumers of footwear and

leather goods in the world are

China and Vietnam. EU nations

like Germany in particular, and

France, Italy to some extent, have had depressed economic climates and hence has limited

growth potential. USA on the other hand is one of the biggest individual market in the world for

leather products, with earnings of $651 million in 2012.

2.2.2 Recent Development

During the last 25 to 30 years, the leather goods industry has undergone major changes due to

factors such as:

• The overall rise of the standard of living along with labor costs in most leather and

leather goods producing

• Gradual development of marketing and brand strategies by businesses, both at national

and international arena, mainly due to the emergence of new advertising instruments

(e.g., television);

• The segmentation of the production process allowing outsourcing and transfer of know-

how to developing and least developed countries;

• The massive development in tourism with the advent of modern modes of transportation

including air travel;

• Modern production technologies and automation;

Country or

area

Value

(million

US$)

Avg. Growth (%)

World share

%

08-Dec 11-

Dec

China, Hong

Kong SAR 2989.3 4.2 -1 13.2

Italy 2547.7 -1.1 -13.2 11.2

Viet Nam 1583.6 15.8 75.9 7

Germany 810.4 -1.4 -16.4 3.6

Mexico 716.7 8 19.4 3.2

USA 651 -0.7 11.8 2.9

Romania 631.6 -5.3 -13.4 2.8

Spain 611.2 -1.6 -13.8 2.7

France 572 4.7 1.5 2.5

Poland 467.3 -3.2 -11.2 2.1

Portugal 466.2 2.5 -8.9 2.1

Rep. of Korea 443 4.3 -4.7 2

Thailand 422.8 5.6 1.9 1.9

7

• High quality production and efficiency with an overall increase in productivity with the

advent of modern high-tech machineries;

• The use of leather and leather goods in the automotive industry.

In this context, in order to survive in the competitive market and ever changing industry, it was

necessary to look for lower production costs in labor-intensive industries such as textiles,

footwear and leather goods. Moreover, and forced by competition, a great number of companies

started to brand themselves in order to make them better known by customers, requiring

massive expenditure on marketing along with even lower production costs to cope up. A Major

portion of the production companies shifted their production base to countries offering lower

labor costs and cheaper raw materials (UNIDO, 2010).

Destination countries were selected by assessing certain set criteria: proximity to market and

raw material, economic and political, efficient and highly productive labor and their

corresponding costs, the official language of the locality or destination country, quality of life and

living conditions (for expatriate production supervisors).

EU countries, mostly chose North Africa while North Americans, favored neighboring countries

in Latin America (Mexico, Brazil, Nicaragua, Colombia, etc.). However, some did not hesitate to

go further – to Mauritius, for example, where a major French company moved its production

facility of wrist-watch straps long before 1980s. Early in the 20th century, long before all these,

the US glove business had shifted first to Puerto Rico and later on to the Philippines.

Analyzing this gradual transition, we can come up with the following features:

• In the early stages, these transitions were not always successful and yet the relocation

trend continued; continually expanding due to faster transportation at lower costs for

raw materials as well as finished products;

• The modern and efficient mode of communication let to lower costs;

• Industrial cooperation (e.g., through UNIDO, ILO, and bilateral technical assistance

programs) made possible the transfer of technologies and know-how to developing

countries;

• Lucrative incentives granted by some countries to lure in foreign investors, in the form

of bonded warehouses, tax exemptions, and the export of 100% profits to the home

country in foreign currencies achieved their objectives.

In the last 20-30 years, production bases of most of the leather goods companies moved out of

industrialized countries, resulting in the closure of a great number of factories, inducing jobs loss

and the gradual disappearance of know-how, disappearance of know-how and the diminishing

significance or shutting down of some vocational training centers are complemented by the

emergence of local manufacturers and induction of foreign direct investments in the leather

sector with modern institutes dedicated to the development of trained personnel for this sector.

8

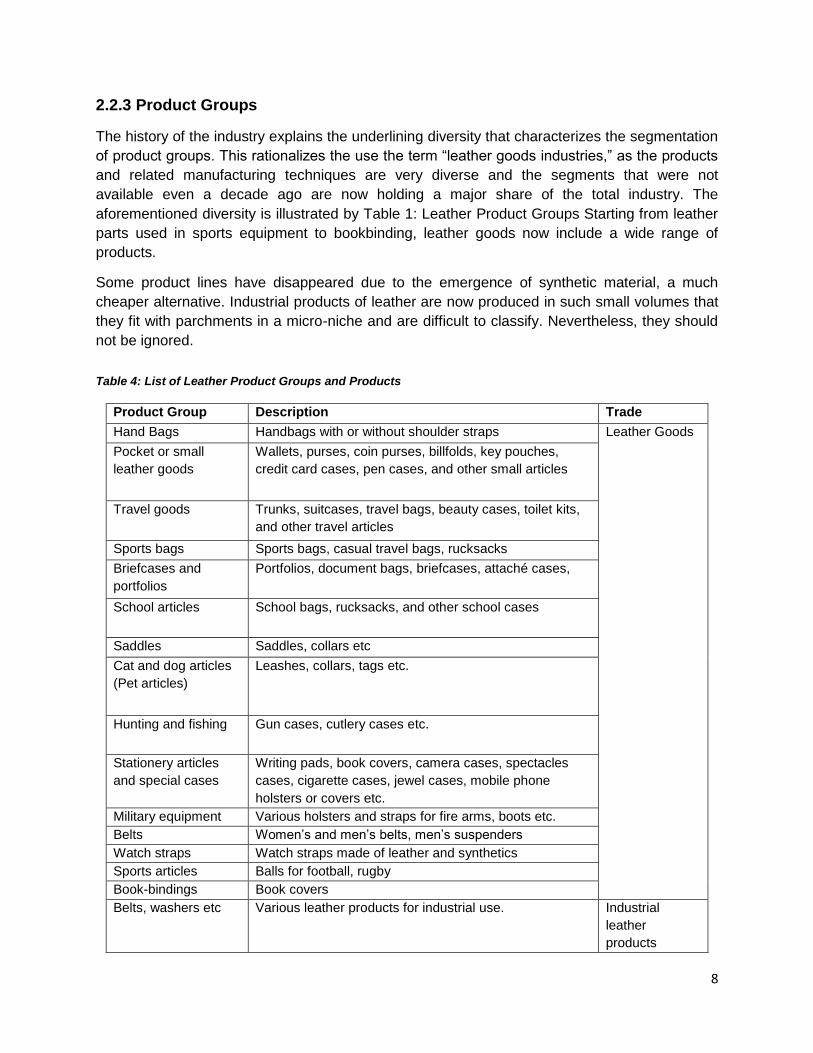

2.2.3 Product Groups

The history of the industry explains the underlining diversity that characterizes the segmentation

of product groups. This rationalizes the use the term “leather goods industries,” as the products

and related manufacturing techniques are very diverse and the segments that were not

available even a decade ago are now holding a major share of the total industry. The

aforementioned diversity is illustrated by Table 1: Leather Product Groups Starting from leather

parts used in sports equipment to bookbinding, leather goods now include a wide range of

products.

Some product lines have disappeared due to the emergence of synthetic material, a much

cheaper alternative. Industrial products of leather are now produced in such small volumes that

they fit with parchments in a micro-niche and are difficult to classify. Nevertheless, they should

not be ignored.

Table 4: List of Leather Product Groups and Products

Product Group Description Trade

Hand Bags Handbags with or without shoulder straps Leather Goods

Pocket or small

leather goods

Wallets, purses, coin purses, billfolds, key pouches,

credit card cases, pen cases, and other small articles

Travel goods Trunks, suitcases, travel bags, beauty cases, toilet kits,

and other travel articles

Sports bags Sports bags, casual travel bags, rucksacks

Briefcases and

portfolios

Portfolios, document bags, briefcases, attaché cases,

School articles School bags, rucksacks, and other school cases

Saddles Saddles, collars etc

Cat and dog articles

(Pet articles)

Leashes, collars, tags etc.

Hunting and fishing Gun cases, cutlery cases etc.

Stationery articles

and special cases

Writing pads, book covers, camera cases, spectacles

cases, cigarette cases, jewel cases, mobile phone

holsters or covers etc.

Military equipment Various holsters and straps for fire arms, boots etc.

Belts Women’s and men’s belts, men’s suspenders

Watch straps Watch straps made of leather and synthetics

Sports articles Balls for football, rugby

Book-bindings Book covers

Belts, washers etc Various leather products for industrial use. Industrial

leather

products

9

Handbags: Women’s handbags represent a huge leather goods market. Bags are not only a

useful accessory; they are also a sign of social rank. The use of bags is very much influenced

by fashion and culture, which themselves vary from one country to another. There are many

price segments in the market and a wide variety of styles and designs. Consequently, the

market for handbags retailing at US$1,000 and above has been growing quite rapidly in the past

five years.

Small leather goods: These are less dependent on fashion. Pocket leather goods, which are

mainly made of genuine leather, follow societal trends and utilizations, such as size of

banknotes or credit cards. The last ten years have seen the rise in importance of holsters for

mobile phones, MP3 players, and iPods. The super-luxury leather goods related to electronic

equipment is a segment that is expected to grow.

Travel goods: This category constitutes a large market that has developed in step with

travelling and tourism. The emphasis is basically on usefulness and ergonomics. The major

trends over the last years have been the introduction of wheels to all kinds of luggage and the

search for lightness. This has worked against leather. There have been considerable changes in

the last decade with the arrival of budget airlines and continuously changing security rules.

Short-haul passengers not wishing to check in luggage have created a market for maximum-

size hand/cabin luggage of high quality.

Briefcases and portfolios: This market is linked to travel and business. Laptops have created

a great need for cases with a specific design – they are mostly made from high-performance

textiles and synthetic materials. Similarly, women’s and men’s briefcases made of genuine

leather and synthetic materials hold an important place in the market. Changes in travel are

affecting this market in the same way as they do travel goods.

School articles: This category corresponds to that of the old “leather satchels.” Trends

changed in 1980 with the appearance of new and fashionable lines of school bags in France

and Germany. Today, the trend is the rucksack made of canvas and printed with various logos

and brand names. A number of the better-known brands today were initially military packs and

evolved into school bags made of materials such as corduroy.

Saddlery: This is a specialized market with a very specific clientele. Saddles and harness items

belong to the luxury segment due to their time-consuming manufacturing process. They are

hardly affected by fashion, so they can easily be made in countries with low labor costs. There

is still a premium market for superior quality saddles, especially the “English” saddle; most

manufacturers of high-quality saddles are in France, Germany and the UK. Argentina, Pakistan

and Morocco are now important suppliers of saddles, and India is also making efforts to get a

share of this specialty market.

Cat and dog articles: A fast growing market in industrialized countries (USA, Europe), where

people are increasingly fond of pets. Many of these products (e.g., collars, leashes, muzzles)

are made predominantly in developing countries. The pet-food sector, which uses raw hides, is

a separate, but important market.

10

Hunting and fishing articles: This is a specific market that is not really influenced by fashion.

These products are generally purchased by well-to-do people with a wide variety of

backgrounds. Stationery articles and special cases articles such as desk pads and note-pad

covers are today in decline due to the use of computers. But other articles, such as mobile-

phone holsters, are booming. The fountain pen has made a comeback and, with it, the demand

for protective carrying cases has re-emerged. Some evolution at the luxury end of this market

can be expected, as the balance between paper and the computer continues to change.

Military equipment: Historically, leather and the military have been of great importance to each

other in terms of saddles, harness, belting, holsters, footwear, and at one time armor. Today,

this is a very specific market, which has been growing considerably in the last ten years. The

main products are footwear and gloves (as personal protective equipment), which are now

usually made of highly technical leathers.

Belts: This is a steady and relatively large market especially in the traditional men’s belts

segment. Belts are not much influenced by fashion, since changes occur mostly in buckle

designs. The manufacturing process of such items has become highly mechanized.

Watch straps: This also constitutes a relatively large market that has only been slightly

threatened by metal or synthetic straps since it stabilized some years ago. The manufacturing

process, as in the case of belts, is highly mechanized, except for top luxury products (hand-

stitched straps made of exotic skins). Leather for watch straps has to be anti-allergic and to

have good levels of sweat resistance.

Overall, the leather goods industry is characterized by the diversity of its products. These items

are constantly developing according to consumer needs and, for certain articles, to fashion

trends.

11

3.0 BANGLADESH LEATHER INDUSTRY

3.1. History of Leather Industry in Bangladesh

Leather sector is a mature manufacturing sector in Bangladesh with an extensive heritage of

over 606 years. This is a bi-product industry which is agro based integrated with locally

sourced original raw materials (hides and skins) having incredible potentials for sustained

growth and export development along a noticeably long duration of time length.

Indian vegetable-tanned crust was being developed by the Indian- subcontinent small leather

industry over a hundred years ago to safeguard the hide in the safest way to suit Indian weather

conditions. The leather industry was subjugated by vegetable-tanned until mid-1960’s.

Bangladesh’s expansion of leather processing industry started in the later part of1940s. East

Bengal, the first tannery of the country, was set up by RP Sahaat Narayanganj in the 1940s7 .

It was afterward moved to Hazaribagh area of Dhaka, which evolved into the major mover of

tannery units through the installation of a large number of tannery units in the past years. Before

the Partition of Bengal (1947), hides and skins available in the former East Bengal, almost all

were exported to West Bengal, erstwhile West Pakistan, Iran and Turkey. During that time it

was mostly the non-Bengali tradesmen and traders scheme the tanning industry in East

Pakistan and export of leather. Nevertheless, a few small tanning units which were mostly

cottage type and used to process leather mainly for the domestic markets, belonged to Bengali

entrepreneurs.

Non-Bengali tanners processed wet-blue and for further processing and finishing for producing

different consumer goods sent them to erstwhile West Pakistan. Till1960, tanneries of erstwhile

East Pakistan used to process raw hides and cattle skins by applying salt and then freshening

them in the sun and the substance thus developed were known as shaltu8 .

In 1971, during the war of liberation, abandoning about 30 tannery units owned by them, the

non-Bengali tanners of Bangladesh left the country. After the war, the new government of

Bangladesh with a newly formed Tannery Corporation vested the management of these units,

addressing an indirect expectation to change the units into finished leather manufacture units.

Regrettably, because of lack of experience and corrupt practices the corporation could not serve

the purpose.

Later, the government closed down the Tannery Corporation and transferred the management

of most of these tanneries to Bangladesh Chemical Industries Corporation (BCIC) and three

of them to Bangladesh Freedom Fighters Welfare Trust. Both the authorities had miserably

failed to bring success in the tannery industry9 .The Government of Bangladesh forced export

duty on wet-blue leather in 1977 to encourage the production of crust and finished leather.

6 Banglapedia

7 Banglapedia

8 Ancient way of preserving raw cattle leather

9 www.sos-arsenic.net

12

The export from leather sector was almost 100% in the form of wet-blue, the chrome tanned and

semi-processed leather until 1980-85. Improvement of major policies took place in this sector

during the period of 1980-81, which resulted in affirmative development of the sector.

Due to the veto on wet-blue export from July, 1990, the leather industry of Bangladesh had

entered into second chapter of its development. Duringthemid-90s began a new era for leather

industries in Bangladesh as the modern leather manufacturing units were set up. Till the end of

the last century, the leather sector maintained a very feeble profile. So, the growth of this

industry was always minor.

As it has neither encouraged the emergence of new entrepreneurs in this sector nor has it

helped to raise foreign buyer’s confidence to invest, this trend in management of technology has

further worsened the state of the industry. Therefore, Bangladesh still remains a source of

processed leather and to a very inadequate extent, finished leather and leather goods in the

international market.

3.2. Leather Industry in Brief

The leather industry in Bangladesh is well recognized and is a significant foreign exchange

earner. The industry is completely in the private sector, which has been proven fully capable of

handling it. Out of the total 207 tanneries of Bangladesh, 186 are located chaotically in

Hazaribagh area in Dhaka where 84 percent of the total supply of hides and skins are

processed in a highly jam-packed area of only 70 acres of land.

The unplanned tanneries at Hazaribagh do not have sustaining infrastructures. No tannery in

the area has effluent treatment facilities (ETP), which is posing a grave danger to environment.

The industry is in the process of shifting to Savar in thought of the pollution it cast upon the

Dhaka City and because of a heightened lack of space for development and modernization.

13

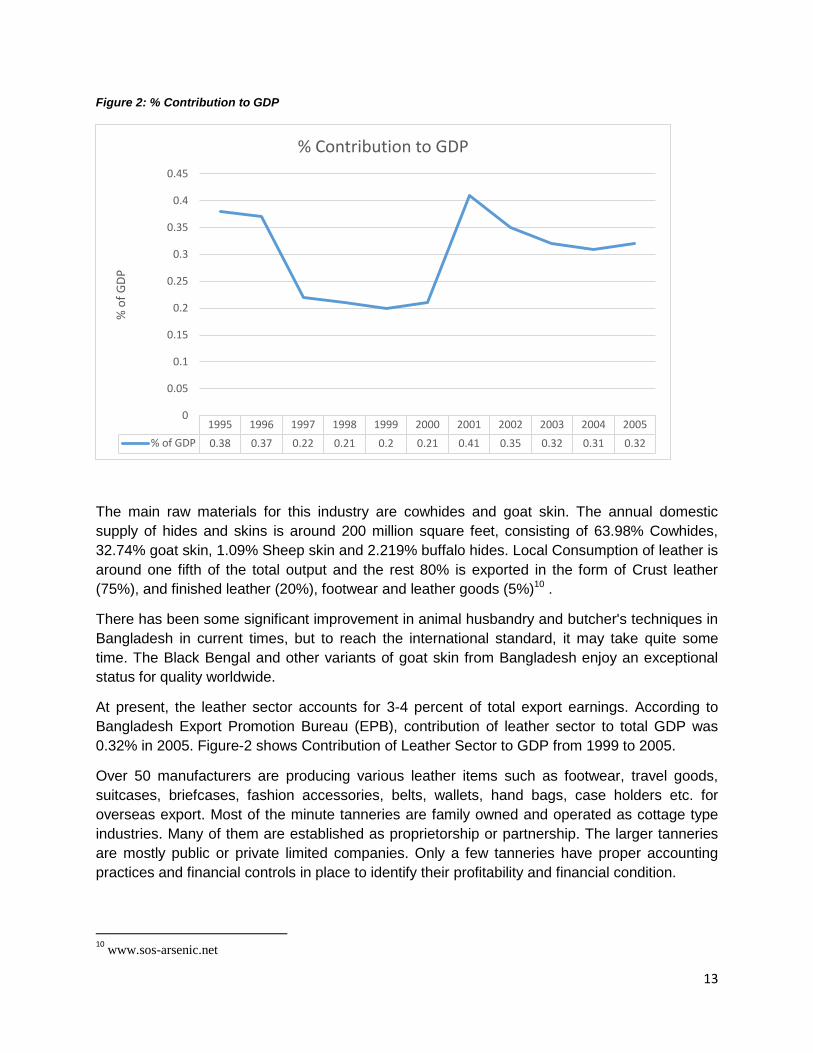

Figure 2: % Contribution to GDP

The main raw materials for this industry are cowhides and goat skin. The annual domestic

supply of hides and skins is around 200 million square feet, consisting of 63.98% Cowhides,

32.74% goat skin, 1.09% Sheep skin and 2.219% buffalo hides. Local Consumption of leather is

around one fifth of the total output and the rest 80% is exported in the form of Crust leather

(75%), and finished leather (20%), footwear and leather goods (5%)10 .

There has been some significant improvement in animal husbandry and butcher's techniques in

Bangladesh in current times, but to reach the international standard, it may take quite some

time. The Black Bengal and other variants of goat skin from Bangladesh enjoy an exceptional

status for quality worldwide.

At present, the leather sector accounts for 3-4 percent of total export earnings. According to

Bangladesh Export Promotion Bureau (EPB), contribution of leather sector to total GDP was

0.32% in 2005. Figure-2 shows Contribution of Leather Sector to GDP from 1999 to 2005.

Over 50 manufacturers are producing various leather items such as footwear, travel goods,

suitcases, briefcases, fashion accessories, belts, wallets, hand bags, case holders etc. for

overseas export. Most of the minute tanneries are family owned and operated as cottage type

industries. Many of them are established as proprietorship or partnership. The larger tanneries

are mostly public or private limited companies. Only a few tanneries have proper accounting

practices and financial controls in place to identify their profitability and financial condition.

10

www.sos-arsenic.net

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

% of GDP 0.38 0.37 0.22 0.21 0.2 0.21 0.41 0.35 0.32 0.31 0.32

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

% o

f G

DP

% Contribution to GDP

14

Now a days, leather and leather products are exported to about 53 countries of the world. The

chief importing countries are: Italy, Brazil, Germany, Singapore, China and the USA. Export

Promotion Bureau sources state that export income from leather goods was US$287.78 million

in 2004-2005, and of that, about 80% are from leather and the rest is from completed leather

goods.

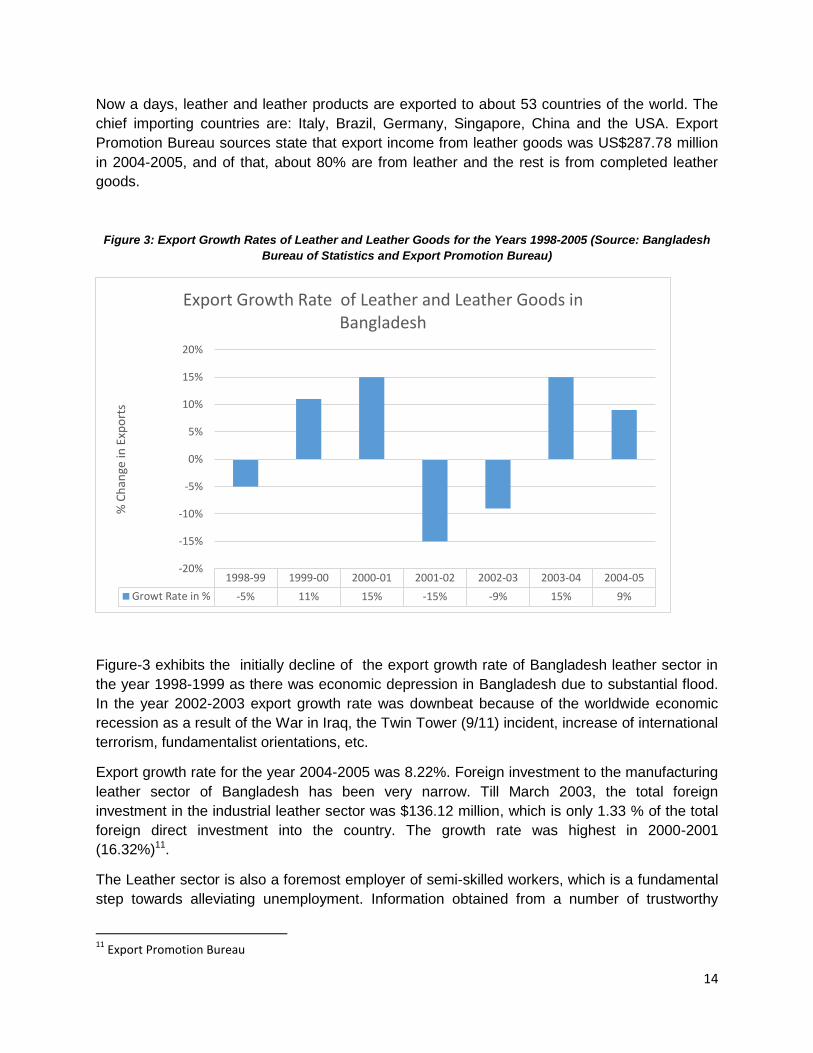

Figure 3: Export Growth Rates of Leather and Leather Goods for the Years 1998-2005 (Source: Bangladesh

Bureau of Statistics and Export Promotion Bureau)

Figure-3 exhibits the initially decline of the export growth rate of Bangladesh leather sector in

the year 1998-1999 as there was economic depression in Bangladesh due to substantial flood.

In the year 2002-2003 export growth rate was downbeat because of the worldwide economic

recession as a result of the War in Iraq, the Twin Tower (9/11) incident, increase of international

terrorism, fundamentalist orientations, etc.

Export growth rate for the year 2004-2005 was 8.22%. Foreign investment to the manufacturing

leather sector of Bangladesh has been very narrow. Till March 2003, the total foreign

investment in the industrial leather sector was $136.12 million, which is only 1.33 % of the total

foreign direct investment into the country. The growth rate was highest in 2000-2001

(16.32%)11.

The Leather sector is also a foremost employer of semi-skilled workers, which is a fundamental

step towards alleviating unemployment. Information obtained from a number of trustworthy

11

Export Promotion Bureau

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05

Growt Rate in % -5% 11% 15% -15% -9% 15% 9%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

% C

han

ge in

Exp

ort

s

Export Growth Rate of Leather and Leather Goods in Bangladesh

15

sources exhibits that in total (accumulated) 741,000 people are directly or indirectly in leather

and its sub-sectors are employed. 200,000 people are involved in rawhide collection and supply

and 50,000 are operational in tanning industry. About 300,000 workers are related to retailing of

leather.

Table 5: List of Leather Goods Produced in Bangladesh

At present it is anticipated that about

150,000 persons are employed in the

footwear industry, 30,000 persons are

in leather goods industry and another

8000 persons are involved in

exporting of leather and byproduct

processing12. In spite of having a

great prospective for growth, the

net outcome of development efforts

undertaken for the leather export

sector of Bangladesh have been far

from remarkable due to the

unfortunate quality of processing,

illegal export to India, reduced

technological base, insufficient

financing, low value addition,

requirement of marketing skill,

incorrect planning and improper

execution.

Bangladesh exports significant

amount of leather, which is used as a

go-between product for producing

special types of leather goods and

footwear by the developed countries.

Besides, Bangladesh manufactures an

extensive and diverse range of leather

goods for the export market albeit in a

restricted quantity.

12

(Source: BCLT, LSBPC, ILO, BBS, GTZ, RSMA and ITC-ATF)

Sl For Domestic

Market

Sl For International

Market

1 Ladies Shoes 1 Processed Leather

2 Leather Jacket

2 Gents Shoes 3 Leather Blazer

4 Leather Skirt

3 Sandals /Slippers 5 Leather Trouser

6 Apron

4 Belts 7 Purse

8 Money bags

5 Travel Bags 9 Belts

10 Briefcase

6 Purse 11 Travel bags

12 Office bags

7 Money Bags 13 Suitcase

14 Ladies shoes

8 Office Bags 15 Gents shoes

16 Sandals /Slippers

9 Suitcase 17 Camera case

18 Racket cover

10 Briefcases 19 Card holder

20 Pen holder

11 Gift Items 21 Passport case

22 Document case

12 Processed Leather 23 Spectacle case

24 Gift Items

16

3.3 Market Structure

3.3.1 Demographic Concentration

Traditionally, the tannery industry got intense in the Hazaribagh area of Dhaka city where

almost 90% of all tanneries are situated. This concentration happened in an unplanned style

posing severe threat to the environment. Hence, the government has taken a step to shift the

industry to a leather estate at Savar outside the city. Nearly 90% of all leather footwear making

units is located in and around Dhaka city with some leather footwear production units existing in

Khulna and Chittagong city and in Bhairab of Kishoreganj district.

Inside Dhaka city) in two areas known as Siddique Bazaar and Bongshal where concentration of

small leather footwear making units (having 10-49 workers), half of these small units are

located. Others areas of concentration of small and medium leather footwear making units in

and about Dhaka city include Lalbag, Nazirabazar, Sitpatli, Bangladuar, Alu Bazar, Dakkhin

Moishundi, Pagla and Nawabpur.

3.3.1.1. Modern Leather Industrial City-Savar

In the year 2003, the Government of Bangladesh announced that the tanneries situated in

Hazaribag will be shifted to modern and a purpose-built cluster in Savar, 10 kilometers from

Hazaribag, on the banks of the river Dhaleswari. The key emphasize of the Savar cluster was to

be the Common Effluent Treatment Plant (CETP), compliant to international environmental

standards. The Bangladesh Small and Cottage Industries Corporation (BSCIC) is the

implementing agency for the project.

It will hold up 195 tanneries with an employment probable of 100,000 people. However, transfer

and moving to designated modern tannery cite with on handout old machineries from the

existing Hazaribagh cite is a huge challenge, and a matter of big investments for the tannery

owners. The sooner it takes place the better.

3.3.2 Leather Goods Market Size in Bangladesh 2013

Other than the existing subsectors in leather sector no pioneering sub-sector is found emerging

very soon, although a few big companies from Taiwan and China beforehand invested in this

sector, and a few factories had started producing out soles which is a very significant and

welcoming start of new addition in the footwear sub-sector. The rearward linkage industries are

nearly empty, and ready for investment.

17

3.3.2.1 Tannery Subsector

Among the total 220 tanneries in Bangladesh, 187 tanneries are situated in Hazaribagh, Dhaka.

The main raw materials for

this sector are cowhides

and goatskins. 112-115 big

units have amenities for

processing only wet blue

leather. The residual 91-95

small, medium and large

units have sound facilities

to produce crust and

finished leather.

The annual domestic

supply is around 220

million square feet of hides

and skins, consisting of

63.98% cowhides, 32.74% goat skins, 1.09% sheep skin and 2.219% buffalo hides. While 50%

of this is consumed locally and rest 50% is exported to 53 countries in the form of semi-finished

leather (75%), finished leather (20%), and footwear, handbags, accessories, and other leather

goods (5%)13 .

The Hazaribagh tanneries can reportedly process 94% of the hides and skins accessible in

Bangladesh. However, free of this capacity, there are issues effecting the collection of hides and

skins before they arrive at the tanneries.

The global leather and its product market size is considered to be as ~US$ 100 billion, and the

share of Bangladesh business is 0.56% (COMTRADE, 2014) . The objective of Bangladesh is

increasing that market share to 2% by 2013 represents an striving increase in export value. This

subsector generated direct employment of about 50,000 people.

Environmental pollution is one of the major concerns of this sector, according to DOE, the

tanneries release nearly 22,000 cubic meters of unprocessed and highly toxic (contains

chromium) into the water body on a regular basis. On the other hand, it produces 100 tons of

solid waste every day in the form of trappings of finished leathers, shaving dust, hairs, trimmed

animal flesh skins/hides to infect the soil and the water.

13

Draft Leather Policy 2006-2010 by LSBPC, MoC & GoB

18

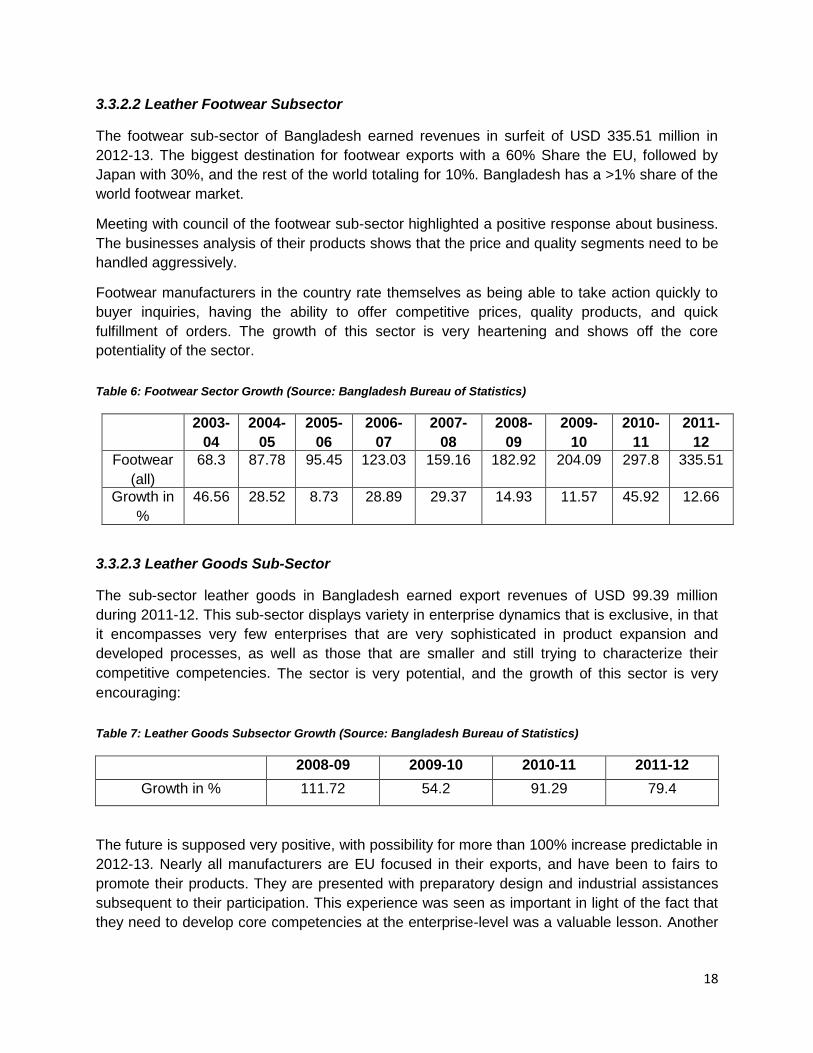

3.3.2.2 Leather Footwear Subsector

The footwear sub-sector of Bangladesh earned revenues in surfeit of USD 335.51 million in

2012-13. The biggest destination for footwear exports with a 60% Share the EU, followed by

Japan with 30%, and the rest of the world totaling for 10%. Bangladesh has a >1% share of the

world footwear market.

Meeting with council of the footwear sub-sector highlighted a positive response about business.

The businesses analysis of their products shows that the price and quality segments need to be

handled aggressively.

Footwear manufacturers in the country rate themselves as being able to take action quickly to

buyer inquiries, having the ability to offer competitive prices, quality products, and quick

fulfillment of orders. The growth of this sector is very heartening and shows off the core

potentiality of the sector.

Table 6: Footwear Sector Growth (Source: Bangladesh Bureau of Statistics)

2003-

04

2004-

05

2005-

06

2006-

07

2007-

08

2008-

09

2009-

10

2010-

11

2011-

12

Footwear

(all)

68.3 87.78 95.45 123.03 159.16 182.92 204.09 297.8 335.51

Growth in

%

46.56 28.52 8.73 28.89 29.37 14.93 11.57 45.92 12.66

3.3.2.3 Leather Goods Sub-Sector

The sub-sector leather goods in Bangladesh earned export revenues of USD 99.39 million

during 2011-12. This sub-sector displays variety in enterprise dynamics that is exclusive, in that

it encompasses very few enterprises that are very sophisticated in product expansion and

developed processes, as well as those that are smaller and still trying to characterize their

competitive competencies. The sector is very potential, and the growth of this sector is very

encouraging:

Table 7: Leather Goods Subsector Growth (Source: Bangladesh Bureau of Statistics)

2008-09 2009-10 2010-11 2011-12

Growth in % 111.72 54.2 91.29 79.4

The future is supposed very positive, with possibility for more than 100% increase predictable in

2012-13. Nearly all manufacturers are EU focused in their exports, and have been to fairs to

promote their products. They are presented with preparatory design and industrial assistances

subsequent to their participation. This experience was seen as important in light of the fact that

they need to develop core competencies at the enterprise-level was a valuable lesson. Another

19

lesson that came through to the participants was the requirement for product demarcation at the

enterprise-level.

This sub-sector is eager on developing partnership with its peers in Asia (India, China, and

Vietnam), and believes that in craftsmanship that technical assistance may be more appropriate

if sourced from the region. The representatives of leather goods firms also uttered the need to

organize fair(s) in Bangladesh regularly, and attracting buyers to visit in concurrence with the

Chennai leather fair, in India. Japan.

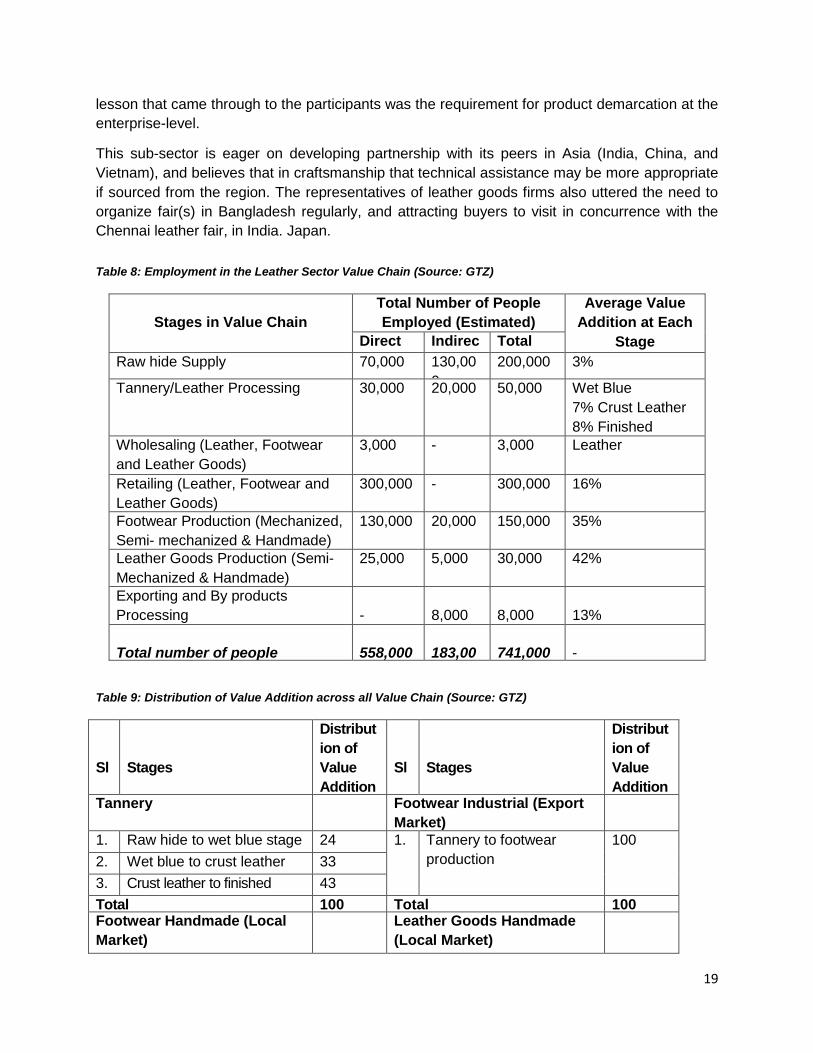

Table 8: Employment in the Leather Sector Value Chain (Source: GTZ)

Stages in Value Chain

Total Number of People

Employed (Estimated)

Average Value

Addition at Each

Stage Direct Indirec

t

Total

Raw hide Supply 70,000 130,00

0

200,000 3%

Tannery/Leather Processing 30,000 20,000 50,000 Wet Blue

7% Crust Leather

8% Finished

Leather 9% Wholesaling (Leather, Footwear

and Leather Goods)

3,000 - 3,000 Leather 29% Footwear 6%

Retailing (Leather, Footwear and

Leather Goods)

300,000 - 300,000 16%

Footwear Production (Mechanized,

Semi- mechanized & Handmade)

130,000 20,000 150,000 35%

Leather Goods Production (Semi-

Mechanized & Handmade)

25,000 5,000 30,000 42%

Exporting and By products

Processing

-

8,000

8,000

13%

Total number of people

employed

558,000

183,00

0

741,000

-

Table 9: Distribution of Value Addition across all Value Chain (Source: GTZ)

Sl

Stages

Distribut

ion of

Value

Addition

%

Sl

Stages

Distribut

ion of

Value

Addition

% Tannery Footwear Industrial (Export

Market)

1. Raw hide to wet blue stage 24 1. Tannery to footwear

production

100

2. Wet blue to crust leather

stage

33

3. Crust leather to finished

leather stage

43

Total 100 Total 100 Footwear Handmade (Local

Market)

Leather Goods Handmade

(Local Market)

20

1. Input supplier to footwear

production

58 1. Input supplier to Lather

goods

production

71

2. Footwear production to

footwear

wholesale

10 2. Leather goods production

to

retailing

29

3. Footwear wholesale to

retailing

32

Total 100 Total 100 Footwear Industrial (Local

Market)

Leather Goods Semi-

industrial

(Export Market)

1. Tannery to footwear

production

65 1. Tannery to leather goods

production

100

2. Footwear production to

wholesale

9

3. Wholesale to retailing 26

Total 100 Total 100

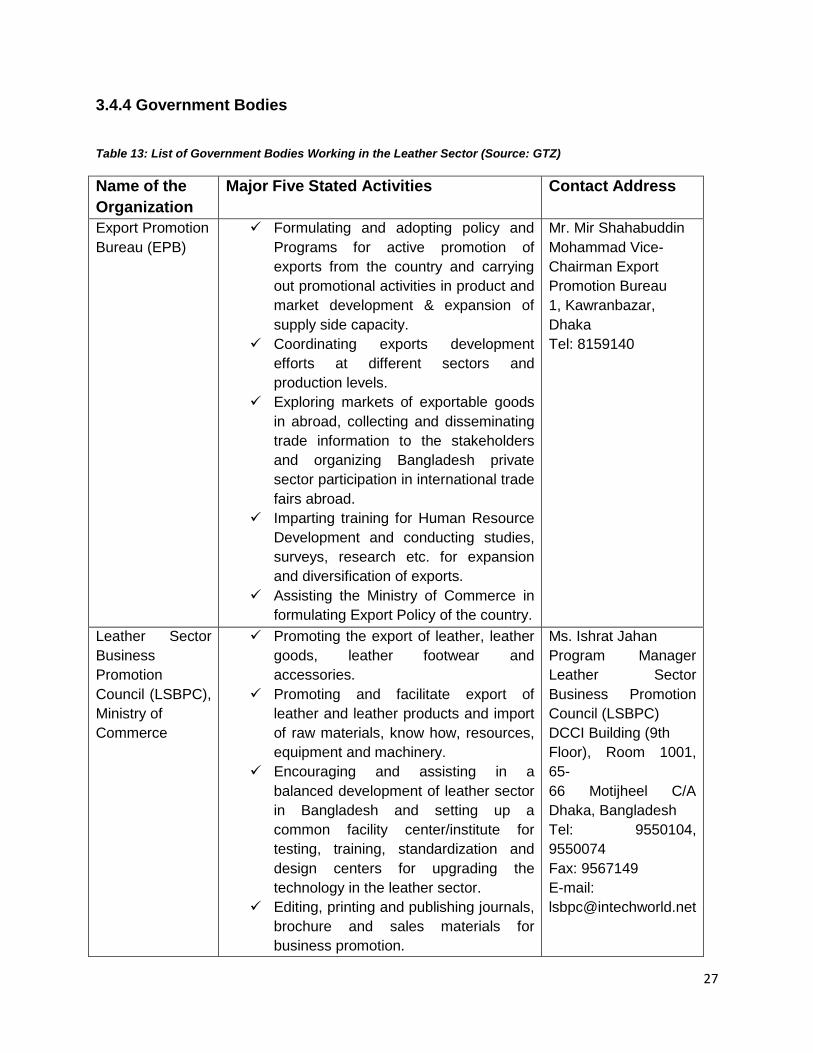

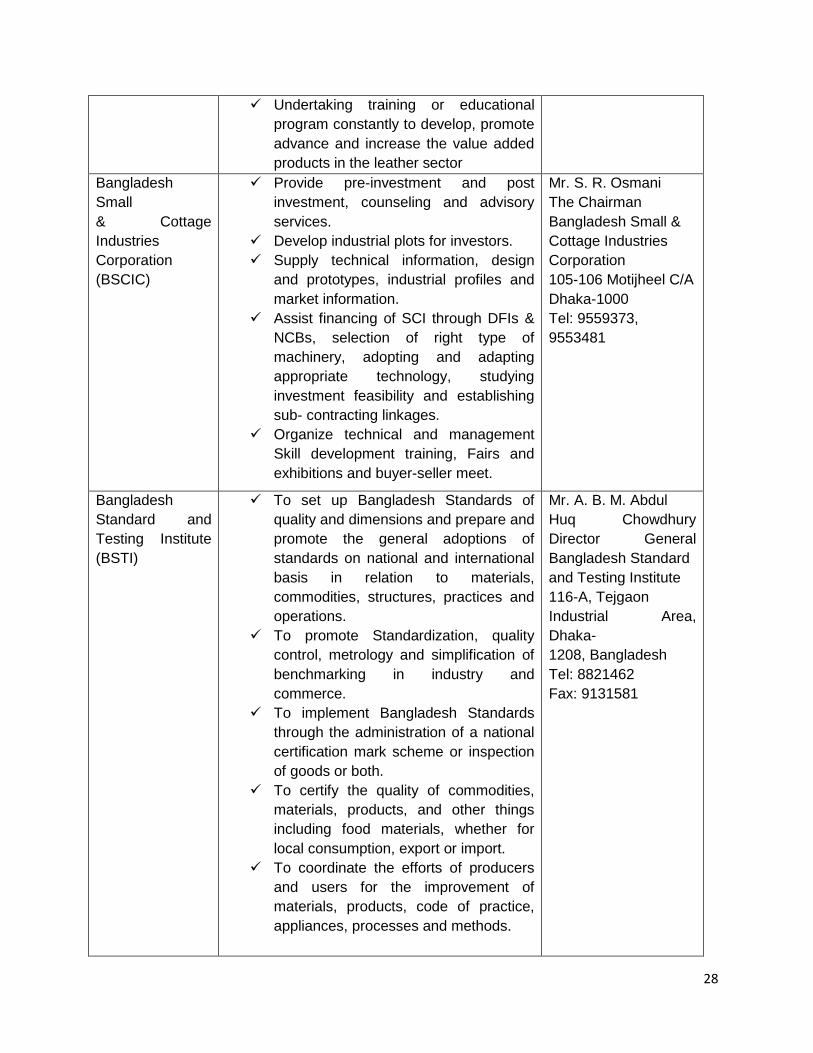

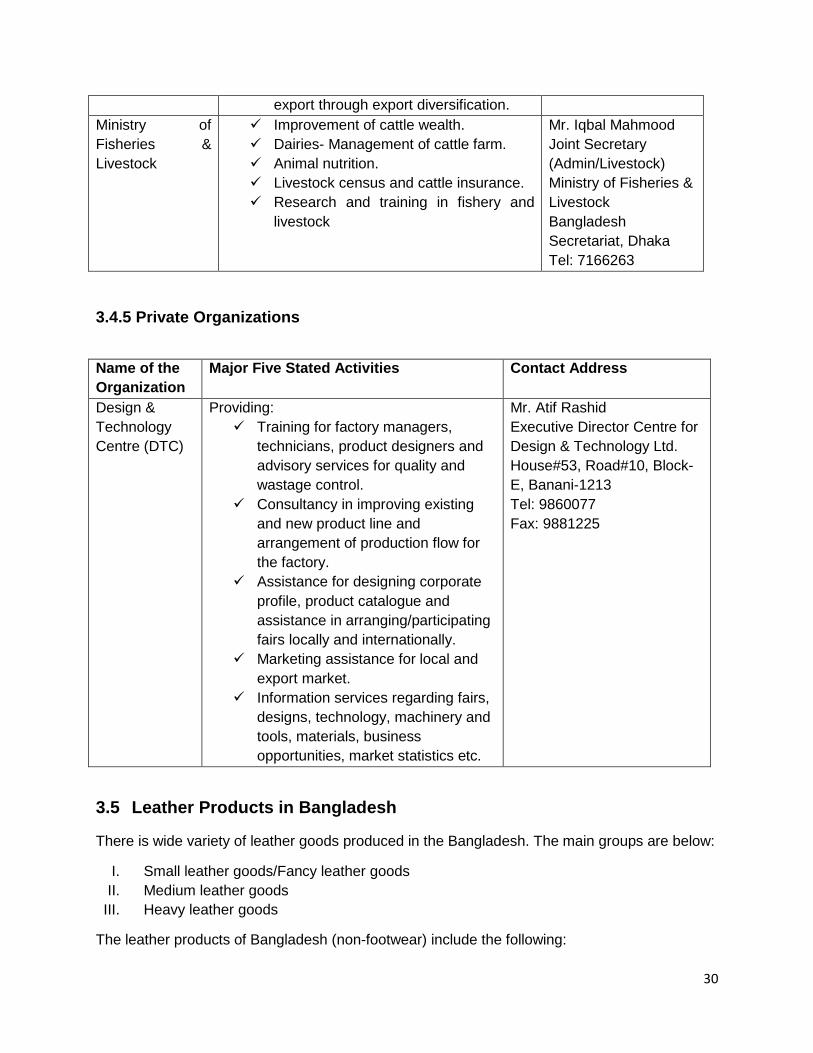

3.4 Major Institutions involved in leather sector

3.4.1 Leather Associations of Bangladesh

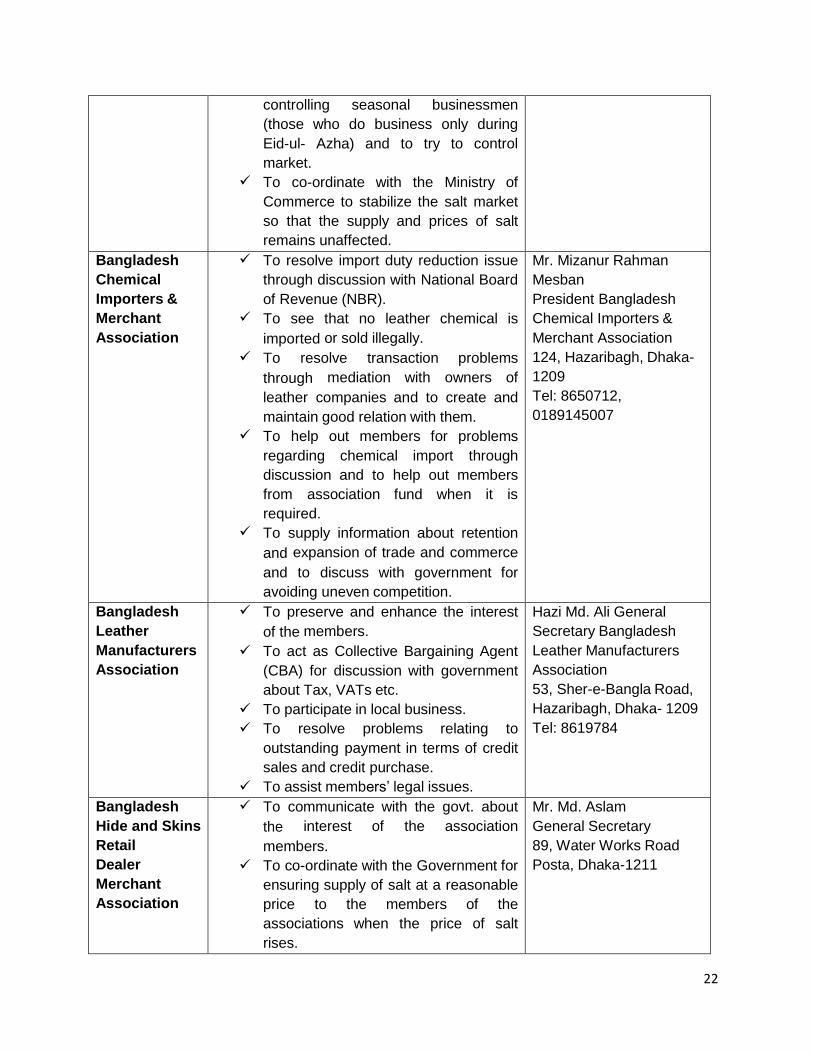

Table 10: Major Associations in the Leather Sector (Source: GTZ)

Name of the

Organization

Major Five Stated Activities Contact Address

Bangladesh

Finished

Leather,

Leather goods

and Footwear

and Exporters’

Association

(BFLLFEA)

To promote, protect and safeguard the

interest of all the members of the

association who are engaged in the

manufacture and export of crust and

finished leather and leather goods.

To keep and maintain the highest

standard of unity, mutual cooperation

and goodwill among the members of

the association in the conduct of their

business carried on by them.

To promote a cognizance of mutual

assistance and cooperation among the

members and maintain the uniformity

of rules of business and discourage

unhealthy competition among the

members of the association.

To render such assistance, cooperation

and advice to government authority or

any other public or private authority in

order to enable them to promote,

protect and safeguard the interest of

the members of the association

members and customers.

To arbitrate all disputes and differences

Mr. Md. Tipu Sultan,

Chairman Bangladesh

Finished Leather, Leather

goods and Footwear

Exporters’ Association

(BFLLFEA) House#61,

Road#2A, Dhanmondi

R/A, Dhaka-1209

Phone: +8802-8622167

Fax: +880-2-8622168

E-mail:

21

that may arise between the members

of the association and/or between the

members

Bangladesh

Tanners

Association

(BTA)

To work for over all welfare of the

members of leather industry.

To apprise the government about the

importance and contribution of leather

industry in order to raise benefits of the

members.

To popularize leather, leather goods

and footwear of Bangladesh in

international markets; marketing of the

same.

To resolve disputes related to

transactions among the members.

To perform social works for general

public in times of famine, earthquake,

storm etc.

Mr. Md. Harun

Chowdhury

Chairman Bangladesh

Tanners Association

(BTA)

99, Hazaribagh, Dhaka-

1209

Phone: +880-2-8626878,

9660754 (Off)

Fax: +880-2-8616348,

8618546

Leather Goods

and Footwear

Manufacturers’

& Exporters’

Association of

Bangladesh

(LFMEAB)

To help in gaining export market for the

members by sending delegates to

various countries, attending

international fairs, seminar etc.

To assist members get customs, bond,

and warehouse license and renew

them.

To help members in resolving various

problems and difficulties related to

customs, duties and taxes.

To authenticate GSP application and to

help out members for getting cash

incentive and other financial benefits

from government.

To maintain liaison with exporters and

to work with Export Promotion Bureau.

Mr. Saiful Islam

Vice-President Leather

Goods and Footwear

Manufacturers’ and

Exporters Association

of Bangladesh (LFMEAB)

Erectors House (9th

floor), 18, Kamal Ataturk

Avenue,

Banani C/A, Dhaka-1213,

Bangladesh

Phone: 9354993-4 (off),

01711522170

Fax: +880-2-9332569

Bangladesh

Hide and Skin

Merchants

Association

To handle tax problems for the

member.

To prevent extortion and other

problems associated with riverine

transportation as un-processed/semi-

processed hide can be considered as

perishable goods.

To resolve problems related to debt

and receipts with the tannery owners.

To organize joint committees for

Mr. Md. Aftab

Vice Chairman

Bangladesh Hide and

Skin Merchants

Association

88/A, Water Works Road,

Posta, Dhaka-1211,

Bangladesh

Phone: 9663203,

01711-523673

22

controlling seasonal businessmen

(those who do business only during

Eid-ul- Azha) and to try to control

market.

To co-ordinate with the Ministry of

Commerce to stabilize the salt market

so that the supply and prices of salt

remains unaffected.

Bangladesh

Chemical

Importers &

Merchant

Association

To resolve import duty reduction issue

through discussion with National Board

of Revenue (NBR).

To see that no leather chemical is

imported or sold illegally.

To resolve transaction problems

through mediation with owners of

leather companies and to create and

maintain good relation with them.

To help out members for problems

regarding chemical import through

discussion and to help out members

from association fund when it is

required.

To supply information about retention

and expansion of trade and commerce

and to discuss with government for

avoiding uneven competition.

Mr. Mizanur Rahman

Mesban

President Bangladesh

Chemical Importers &

Merchant Association

124, Hazaribagh, Dhaka-

1209

Tel: 8650712,

0189145007

Bangladesh

Leather

Manufacturers

Association

To preserve and enhance the interest

of the members.

To act as Collective Bargaining Agent

(CBA) for discussion with government

about Tax, VATs etc.

To participate in local business.

To resolve problems relating to

outstanding payment in terms of credit

sales and credit purchase.

To assist members’ legal issues.

Hazi Md. Ali General

Secretary Bangladesh

Leather Manufacturers

Association

53, Sher-e-Bangla Road,

Hazaribagh, Dhaka- 1209

Tel: 8619784

Bangladesh

Hide and Skins

Retail

Dealer

Merchant

Association

To communicate with the govt. about

the interest of the association

members.

To co-ordinate with the Government for

ensuring supply of salt at a reasonable

price to the members of the

associations when the price of salt

rises.

Mr. Md. Aslam

General Secretary

89, Water Works Road

Posta, Dhaka-1211

23

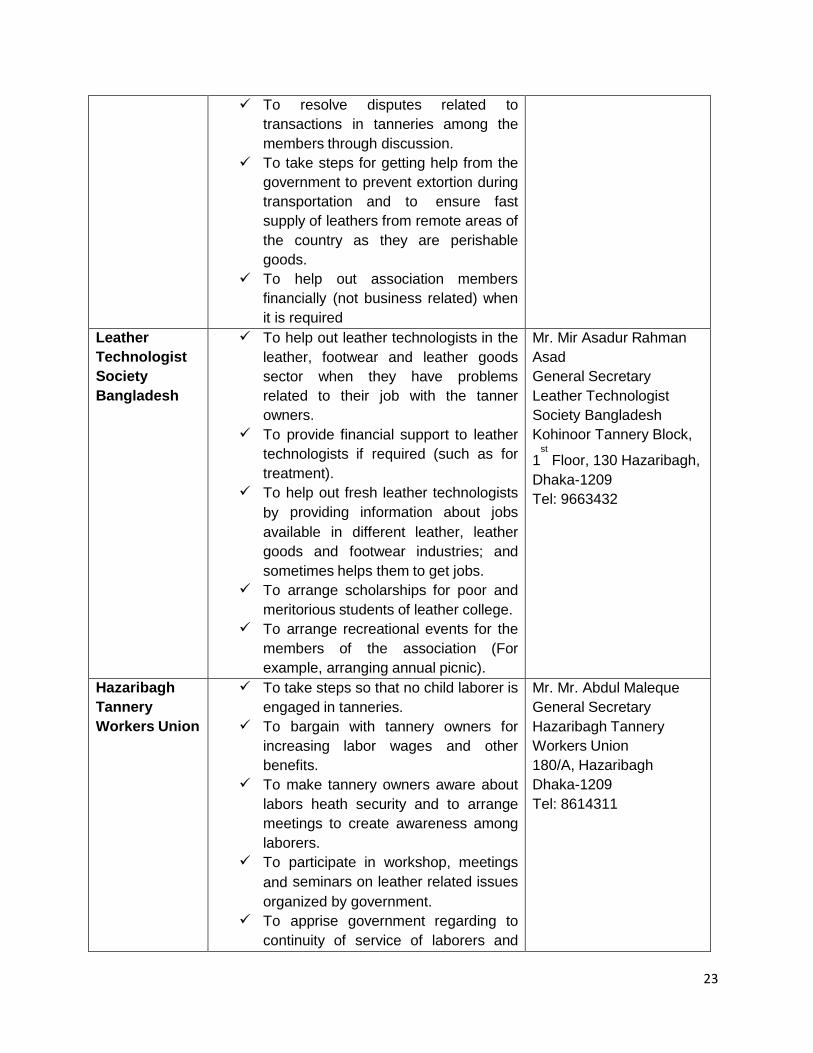

To resolve disputes related to

transactions in tanneries among the

members through discussion.

To take steps for getting help from the

government to prevent extortion during

transportation and to ensure fast

supply of leathers from remote areas of

the country as they are perishable

goods.

To help out association members

financially (not business related) when

it is required

Leather

Technologist

Society

Bangladesh

To help out leather technologists in the

leather, footwear and leather goods

sector when they have problems

related to their job with the tanner

owners.

To provide financial support to leather

technologists if required (such as for

treatment).

To help out fresh leather technologists

by providing information about jobs

available in different leather, leather

goods and footwear industries; and

sometimes helps them to get jobs.

To arrange scholarships for poor and

meritorious students of leather college.

To arrange recreational events for the

members of the association (For

example, arranging annual picnic).

Mr. Mir Asadur Rahman

Asad

General Secretary

Leather Technologist

Society Bangladesh

Kohinoor Tannery Block,

1st Floor, 130 Hazaribagh,

Dhaka-1209

Tel: 9663432

Hazaribagh

Tannery

Workers Union

To take steps so that no child laborer is

engaged in tanneries.

To bargain with tannery owners for

increasing labor wages and other

benefits.

To make tannery owners aware about

labors heath security and to arrange

meetings to create awareness among

laborers.

To participate in workshop, meetings

and seminars on leather related issues

organized by government.

To apprise government regarding to

continuity of service of laborers and

Mr. Mr. Abdul Maleque

General Secretary

Hazaribagh Tannery

Workers Union

180/A, Hazaribagh

Dhaka-1209

Tel: 8614311

24

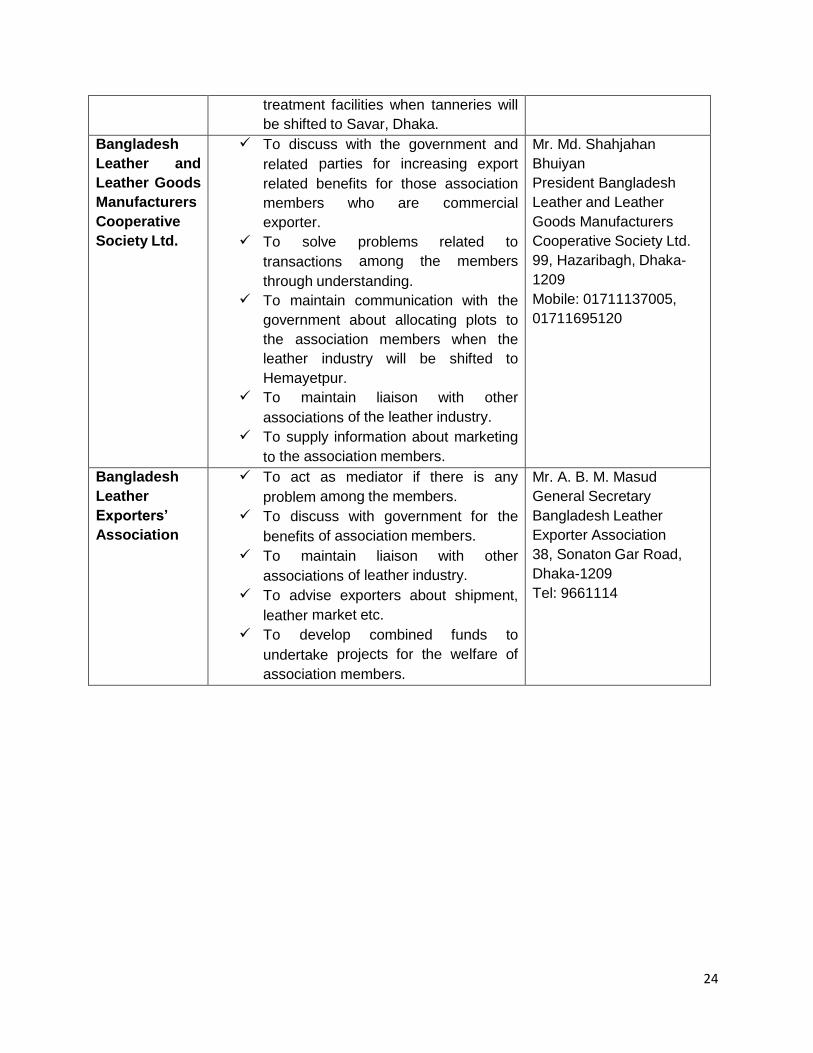

treatment facilities when tanneries will

be shifted to Savar, Dhaka.

Bangladesh

Leather and

Leather Goods

Manufacturers

Cooperative

Society Ltd.

To discuss with the government and

related parties for increasing export

related benefits for those association

members who are commercial

exporter.

To solve problems related to

transactions among the members

through understanding.

To maintain communication with the

government about allocating plots to

the association members when the

leather industry will be shifted to

Hemayetpur.

To maintain liaison with other

associations of the leather industry.

To supply information about marketing

to the association members.

Mr. Md. Shahjahan

Bhuiyan

President Bangladesh

Leather and Leather

Goods Manufacturers

Cooperative Society Ltd.

99, Hazaribagh, Dhaka-

1209

Mobile: 01711137005,

01711695120

Bangladesh

Leather

Exporters’

Association

To act as mediator if there is any

problem among the members.

To discuss with government for the

benefits of association members.

To maintain liaison with other

associations of leather industry.

To advise exporters about shipment,

leather market etc.

To develop combined funds to

undertake projects for the welfare of

association members.

Mr. A. B. M. Masud

General Secretary

Bangladesh Leather

Exporter Association

38, Sonaton Gar Road,

Dhaka-1209

Tel: 9661114

25

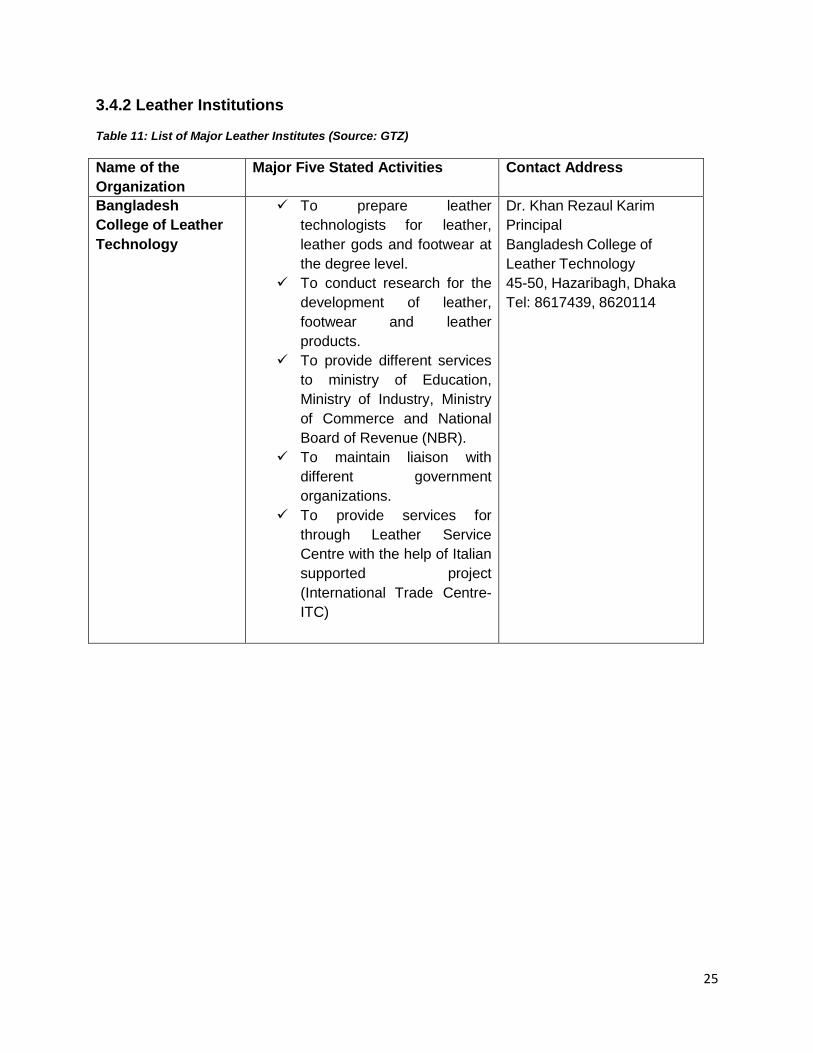

3.4.2 Leather Institutions

Table 11: List of Major Leather Institutes (Source: GTZ)

Name of the

Organization

Major Five Stated Activities Contact Address

Bangladesh

College of Leather

Technology

To prepare leather

technologists for leather,

leather gods and footwear at

the degree level.

To conduct research for the

development of leather,

footwear and leather

products.

To provide different services

to ministry of Education,

Ministry of Industry, Ministry

of Commerce and National

Board of Revenue (NBR).

To maintain liaison with

different government

organizations.

To provide services for

through Leather Service

Centre with the help of Italian

supported project

(International Trade Centre-

ITC)

Dr. Khan Rezaul Karim

Principal

Bangladesh College of

Leather Technology

45-50, Hazaribagh, Dhaka

Tel: 8617439, 8620114

26

3.4.3 Leather Research Institutes

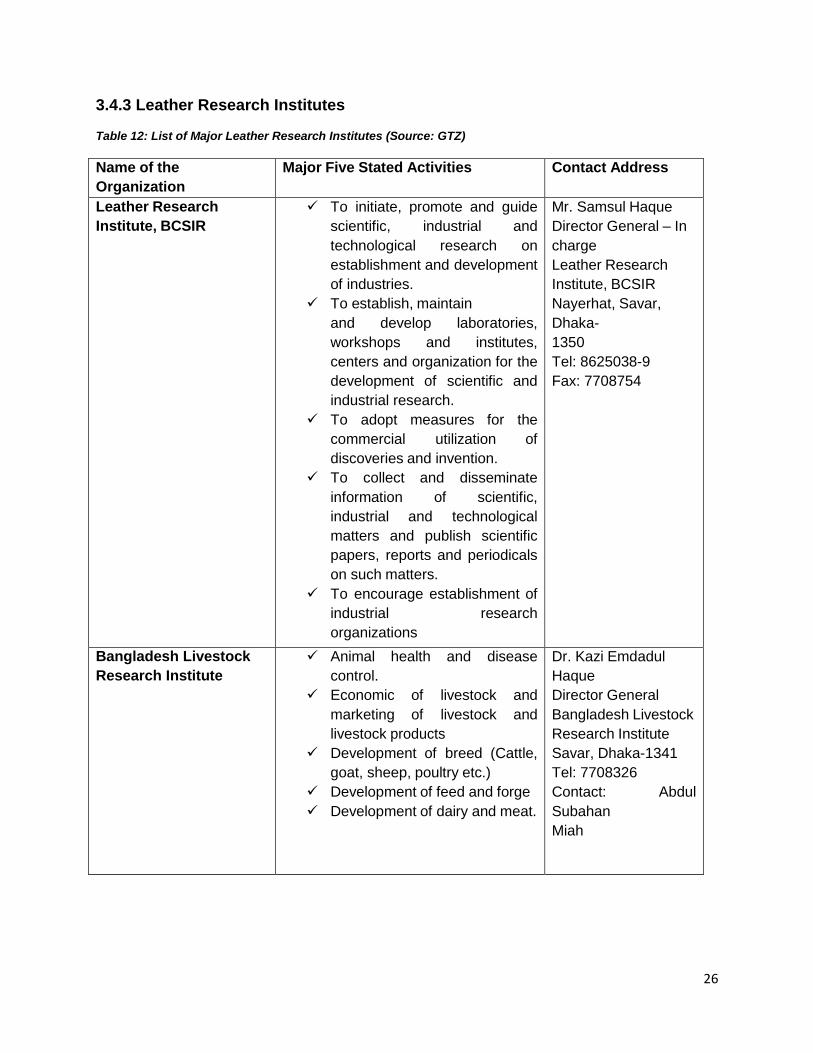

Table 12: List of Major Leather Research Institutes (Source: GTZ)

Name of the

Organization

Major Five Stated Activities Contact Address

Leather Research

Institute, BCSIR

To initiate, promote and guide

scientific, industrial and

technological research on

establishment and development

of industries.

To establish, maintain

and develop laboratories,

workshops and institutes,

centers and organization for the

development of scientific and

industrial research.

To adopt measures for the

commercial utilization of

discoveries and invention.

To collect and disseminate

information of scientific,

industrial and technological

matters and publish scientific

papers, reports and periodicals

on such matters.

To encourage establishment of

industrial research

organizations

Mr. Samsul Haque

Director General – In

charge

Leather Research

Institute, BCSIR

Nayerhat, Savar,

Dhaka-

1350

Tel: 8625038-9

Fax: 7708754

Bangladesh Livestock

Research Institute

Animal health and disease

control.

Economic of livestock and

marketing of livestock and

livestock products