Initial Margin for Non-CentrallyCleared OTC DerivativesOverview, Modelling and Calibration

June 2016

Institute

Dominic O'KaneAffiliate Professor of Finance, EDHEC Business School

2

Table of Acronyms

Acronym Meaning

BCBS Basel Committee on Banking Supervision

BIS Bank for International Settlements

CCP Central Counterparties

CFTC Commodity Futures Trading Commission

DTCC Depository Trust Company

DV01 Dollar Change for a 1bp increase in interest rates

EBA European Banking Authority

EIOPA European Insurance and Occupational Pensions Authority

EMIR European Market Infrastructure Regulation

ESMA European Securities and Markets Authority

FC Financial Counterparties

FRTB Fundamental Review of the Trading Book

GFC Global Financial Crisis of 2007-2009

IM Initial Margin

ISDA International Swaps and Derivatives Association

IOSCO International Organization of Securities Commissions

MPR Margin Period of Risk

NFC Non-Financial Counterparties

OTC Over the counter

RTS Regulatory Technical Standards

VM Variation Margin

WGMR Working Group on Margin Requirements

I would like to thank Jon Gregory, George Handjinicolauou, Lionel Martellini and David Murphy for their comments. Dominic O'Kane benefited from the support of the French Banking Federation (FBF) Chair on Banking regulation and innovation under the aegis of the Louis Bachelier laboratory in collaboration with the Fondation Institut Europlace de Finance (IEF) and EDHEC.

The work presented herein is a detailed summary of academic research conducted by EDHEC-Risk Institute. The opinions expressed are those of the authors. EDHEC-Risk Institute declines all reponsibility for any errors or omissions.

Dominic O'Kane is a specialist in credit modelling, derivative pricing and risk-management. He spent over 12 years working in the finance industry first at Salomon Brothers and then Lehman Brothers. When he left in 2006 he was head of quantitative research and led the team of over 20 Ph.D. researchers. He has taught at the London Business School and the University of Oxford. He wrote Modelling Single-Name and Multi-name Credit Derivatives (published in 2008 by Wiley Finance) and has contributed to several major industry texts including the Handbook of Fixed Income Securities. He also publishes in international finance journals. He has a doctorate in theoretical physics from the University of Oxford.

About the Author

3

Table of Contents

4

Executive Summary ............................................................................................................................... 5

1. Introduction ...................................................................................................................................... 8

2. The Non-Cleared OTC Derivatives Market ............................................................................... 12

3. Margin and Counterparty Risk .................................................................................................... 15

4. The Regulatory Framework .......................................................................................................... 25

5. Regulations for Calculating Initial Margin .............................................................................. 31

6. Calibration of Asset Classes ......................................................................................................... 47

7. The ISDA Standard Initial Margin Model (SIMM) ................................................................... 56

8. Discussion ........................................................................................................................................ 61

References ............................................................................................................................................. 63

EDHEC-Risk Institute Position Papers and Publications (2009-2012) .................................... 64

5

This report provides a detailed overview and analysis of the forthcoming new framework to be used by large financial institutions to determine initial margin (IM) and variation margin (VM) payments when trading non-cleared over-the-counter (OTC) derivatives. Coming into effect in September 2016, this new framework is based on the recommendations of the BCBS/IOSCO Working Group on Margin Requirements (WGMR)1 which has been set out in [BIS2015].

This framework has been in development since it was first proposed following the Pittsburgh G20 meeting in 2009. It was a response to the events of September 2008 which saw the bankruptcy of Lehman Brothers, the bailout of AIG and the federal takeover of Fannie Mae and Freddie Mac, all of whom had large exposures to the OTC derivatives market. In the US, the framework has been implemented by the Commodities Futures Trading Commission (CFTC) within the framework of the Dodd-Frank Act Title VII. In Europe the rules willbe implemented within the new EMIR directive of the EU.

Since Pittsburgh, new regulations have accelerated the separation of the OTC derivatives market into a cleared and non-cleared market, with the former focusing on the `standard' OTC derivatives. As of the end of 2013, the size of the non-cleared segment of the interest rate derivatives market alone was approximately $123-$141trillion.2 The new margining regulations for the non-cleared OTC derivatives are the main subject of this report. Their purpose is to reduce systemic risk across financial markets. In this report we have provided an overview of these new regulations and summarise our observations as follows:1. The significant growth in the use of central clearing via CCPs has reduced

the non-cleared market to less standard, more exotic products or products in illiquid currencies. It also means that price discovery is not centralised and trade valuation is model-based. A framework for VM and IM needs to take these factors into account.2. The role of ISDA3 in creating a standard framework, the ISDA Master Agreement, for trading OTC derivatives, plus inclusion of the close-out netting mechanics, has been key in reducing and simplifying counterparty risk.3. The new framework will enforce the universal use of variation margin (VM). Although VM has been fairly widely used, especially following the Global Financial Crisis (GFC) of 2007-2009, its use has not been universal. This regulation will mainly impact smaller counterparties as most large counterparties already post VM.4. The use of collateral for VM is one-way (towards the in-the-money counterparty). Both cash and non-cash collateral can be used, although cash is preferred as it is faster to move. VM collateral can be reused, rehypothecated and does not need to be segregated. This means that the requirement to post VM collateral does not reduce overall market liquidity.5. Initial Margin (IM) is intended to protect the non-defaulting party to a non-centrally cleared OTC trade from a loss incurred when replacing the trades due to market movements after the other party defaults, including bid-offer increases. The new framework mandates the use of IM for all non-cleared OTC derivatives. Although the concept of IM under the name ̀ independent amount' (IA) had existed previously under ISDA, its usage was not widespread.6. IM requires a two-way posting of collateral, a change in rules since current market practice has been for one-way (IA). In the event of default, the non-defaulting counterparty keeps enough of

Executive Summary

1 - The BCBS is the Basel Committee on Banking Supervision and IOSCO is the International Organization of Securities Commissions. The group responsible for the framework is the Working Group on Margin Requirements (WGMR).2 - See [ISDA(2014b)].3 - The International Swap and Derivatives Association (ISDA) is a trade association for OTC derivatives and their users.

6

the IM collateral posted by the defaulting counterparty to cover any costs involved in replacing its trades. This is the `defaulter pays' principle. It means that the amount of collateral held will exceed the potential loss to the financial system of a single counterparty default.7. IM margin collateral, which may be cash or non-cash, must be held in such a way that it would provide the non-defaulting counterparty immediate access. The WGMR defines how this collateral is to be segregated and stipulate that it cannot be rehypothecated or reused, except for strictly defined hedging purposes.8. The first approach for calculating IM is the standard schedule approach. This based on a schedule of `add-ons' - notional weights linked to the type, and maturity of each asset. Based on historical prices, we find that the add-on weights are consistent with a 10-day 99th percentile loss. However the approach is compromised by its treatment of portfolio effects which rely on the net-to-gross ratio (NGR). We examine the NGR and and conclude that it does not capture diversification in the netting set. Nor does this approach take into account the moneyness of options. For this reason we find the standard schedule approach significantly overestimates the IM amount, and is misaligned to the actual risk. We cannot recommend it.9. The second WGMR approach to calculating IM is based on the use of an internal model where the IM should be the 99th percentile of the 10-day potential future exposure of the netting set. Although not a coherent risk measure, we do not consider this to be a serious criticism provided the risk-factors are Gaussian-like, which we show is the case for most of the markets covered.10. The calibration period for the IM model must be 3 to 5 years (this may differ between the EU and US regulations) and

must include a period of financial stress. We believe that this may pin the period to include the GFC of 2007-2009. This may narrow the scope of calibration parameters and so remove issues of pro-cyclicality that a shorter and changing calibration period could create.11. The choice of a 99th percentile embeds an estimate about the size of market movements expected following a counterparty default, and the probability the IM will cover the realised loss. We note that determining the size of the IM is difficult as there is very little empirical data for such events. We describe the events following the Lehman Brothers bankruptcyto give one example.12. We find that the WGMR modelling requirement to split the netting set by principal asset type fails to recognise the fact that many OTC derivatives have exposures to different risk types. Hence splitting by principal risk factor can penalise sensible hedging. It could be avoided by calculating the portfolio-wide IM for each risk type and summing the resulting risk type IMs.13. Two approaches to calculating the tail risk are possible. One is to assume some joint distribution whose 99th percentile can be calculated analytically. This may restrict the choice of risk factor dynamics. A more commonly used approach is to use either historical or Monte Carlo simulation. A delta-approach may be used to speed up the calculation of IM. However given the high likelihood of non-linear products, a delta-gamma approach may be required. This may need to be checked on a case-by-case basis.14. The variety of products and pay-offs, the lack of a central price discovery venue and the need for valuation models means that disputes are likely. To minimise such occurrences we argue that as much of the model as possible should be developed via a shared industry-wide effort.

Executive Summary

7

Executive Summary

15. ISDA has developed a Standard Initial Margin Model (SIMM) that is very likely to become the market standard. The ISDA SIMM model is based on the Sensitivity Based Approach which has been described by the Bank for International Settlements (BIS), a fact which may assist its regulatory approval. It avoids a Monte Carlo framework, instead applying a set of asset specific risk weights and correlations.16. The WGMR does not permit the inclusion of the modelling of both netting set and collateral in the IM calculation. In fact, EU regulations4 state that the value of the collateral should not have any correlation with the netting set of derivatives. We think that this could restrict flexibility. It would perhaps make sense to incorporate collateral into the IM model as it would permit any correlations (positive or negative) between the two to be recognised.17. Differences in the implementation of the law between the US and Europe exist but do not appear to be so different that they would skew the playing field in either direction. The main difference is the exclusion of non-financial entities from the list of covered entities, and options on securities from the covered products in the US framework.18. We caveat this report with the comment that some of these regulations may be subject to change and interpretation. Readers must not rely upon this report for regulatory guidance and must consult legal and regulatory professionals.

4 - The EU Law Supplementing Regulation No. 648/2012 on OTC derivatives...

8

1. Introduction

5 - See http://www.fanniemae.com/resources/file/ir/pdf/quarterly-annual-results/2008/form10k_022609.pdf6 - See http://www.freddiemac.com/investors/er/pdf/10k_031109.pdf7 - ISDA stands for the International Swap and Derivatives Association and is the trade body for users of OTC derivatives. It has been instrumental in creating the legal framework, known as the ISDA Master Agreement, to assist the trading of OTC derivatives.8 - https://g20.org/wp-content/uploads/2014/12/Pittsburgh_Declaration_0.pdf

The global financial crisis of 2007-2009 alerted political leaders to the risks posed by the existence of the over-the-counter (OTC) derivatives market. This market connects the major dealer banks via hundreds of thousands of individual contracts. The scenario which political leaders feared was one in which the default of a major dealer could, via this web of contracts, create a cascade of defaults across the financial system. The events of September 2008 created a severe test for the OTC derivatives market. First there was the federal takeover of Fannie Mae and Freddie Mac on 7 September, followed by the bankruptcy of Lehman Brothers on 15 September. And one day later there was the bailout of AIG and the federal takeover of Fannie Mae and Freddie Mac. All four of these institutions had large exposures to the OTC derivatives market. For example, Fannie Mae and Freddie Mac had total derivative notional positions of $1.2 trillion5 and $1.3 trillion6 respectively, AIG had sold protection in Credit Default Swap form on $440bn of mortgage-backed securities, and Lehman had derivative contracts with a total notional of $35 trillion.

Clearly Lehman presented the biggest risk. However, for a number of reasons, the `cascade' scenario was not realised. These reasons included the fact that many of Lehman's counterparties were shielded from Lehman's default by the collateral that Lehman had posted within the framework of their ISDA7 Master Agreements. Second, the ISDA framework provides for the ability to set-off exposures (discussed in detail below) and this reduces counterparty risk and simplifies the bankruptcy process. A third mitigating factor was that some 66,000 OTC contracts, with a total notional exposure of $9 trillion, were interest rate swaps Lehman Brothers had cleared at LCH.Clearnet. For these, initial margin and

variation margin had been posted such that replacement costs were below the value of margin that had been posted, resulting in no losses to market participants. A fourth reason was that the OTC derivatives market had begun in 2005 to reduce its backlog of unconfirmed CDS trades and to process them via the NY-based DTCC trade repository, thereby creating a central source of market position information and eliminating a source of uncertainty.

Once the potential for systemic risk created by the OTC derivatives market became apparent to legislators, it was inevitable that some form of regulation would ensue. This process began when the G20 Leaders met one year later in Pittsburgh where they agreed that:All standardised OTC derivative contracts should be traded on exchanges or electronictrading platforms, where appropriate, and cleared through central counter-parties by end-2012 at the latest. OTC derivative contracts should be reported to trade repositories. Non-centrally cleared contracts should be subject to higher capital requirements.8

Since then, regulators have imposed two general requirements on OTC derivatives markets. The first has been to push as much of the OTC derivatives market onto central counterparties (CCPs) as possible. Using a CCP means that a trade initially conducted OTC between two market participants is immediately split into two trades, each facing the same CCP. The CCP then manages payments between parties and also performs netting of exposures. The intermediation of the CCP is intended to create a more robust counterparty than a typical dealer as the CCP is required to be well capitalised. It is also argued that the CCP should be able to benefit from the income and diversification effects of a

9

1. Introduction

large number of offsetting trades. The CCP is capitalised by its members and much of this capital is provided through the use of initial and variation margin. The second requirement pushed by regulators has been to require non-cleared OTC derivatives to also post variation and initial margin.

Over the past three years the Basel Committee on Banking Supervision (BCBS) and the International Organization of Securities Commissions (IOSCO9) have worked on developing a framework for the margin requirements of non-centrally cleared derivatives through the Working Group on Margin Requirements (WGMR). The purpose of this exercise has been to establish minimum global standards that legislators can then translate into law. In the US, the rules on VM and IM for non-cleared OTC derivatives fall under the Dodd-Frank Act Title VII, and are to be established by the U.S. Commodity Futures Trading Commission (CFTC). Indeed they very recently approved the final rules on margin for uncleared swaps.10 In Europe, the rules governing non-cleared OTC derivatives fall under the framework of the European Market Infrastructure Regulation (EMIR). These rules take the form of Regulatory Technical Standards (RTS) and the European Market regulator ESMA, the European Banking Authority (EBA), and the insurance company regulator EIOPA have been consulting on the latest version of these with the latest publication11 being released in June 2015.

As with CCPs, margin for non-cleared OTC derivatives will consist of initial margin (IM)and variation margin (VM). We note that there is already an initial margin provision built into the ISDA credit support annnex (CSA) known as the independent amount or IA which has been in existence since the 1980s. However, the failure of

Lehman Brothers highlighted that one problem with this was that the collateral could be rehypothecated and so was not segregated from other assets. Following Lehman's bankruptcy filing, those who had overcollateralised their exposures at Lehman then became general unsecured creditors and were not able to recover their assets in full. The new regulations on IM correct for this shortcoming by imposing stringent limits on the segregation and rehypothecation of initial margin collateral.

Unlike initial margin, variation margin has been a risk-mitigation technique used by the OTC derivatives market since its inception. Through the work of ISDA, the market has established common standards for legal documentation and dispute resolution in the form of the ISDA Master Agreement and its various annexes. Of these, the most important is the aforementioned CSA, which determines the conditions under which initial and variation margin is posted between counterparties. It also specifies the `close-out' procedures to be followed in the event of a counterparty default. It is periodically updated so that some legacy contracts have been created under the 1992 Master Agreement and others under the updated 2002 Master Agreement. The ISDA Master Agreement also establishes a legal framework for the set-off of derivative contracts. This reduces the claim on the non-defaulting counterparty to the net value of all derivative trades between each pair of counterparties. From this we get the concept of a `netting set' of derivative contracts.

The purpose of variation margin (VM) is to ensure that when a counterparty defaults, the in-the-money counterparty is holding an amount of collateral sufficient to cover their maximum loss assuming a recovery rate of zero. Because of this, VM collateral

9 - Based in Madrid, Spain, IOSCO is the international body for the world's securities regulators.10 - On December 16, 2015.11 - https://www.eba.europa.eu/documents/10180/1106136/JC-CP-2015-002+JC+CP+on+Risk+Management+Techniques+for+OTC+derivatives+.pdf

10

posting is one-way, from the party that is out of the money to the party that is in the money. The amount of VM is given by the market value of the set of trades from the perspective of the in-the-money party. This is not always easy to determine and agree between counterparties as it will depend on factors such as whether OIS discounting is used, and the impact of CVA charges. At any time only the in-the-money party to a set of trades will be holding any collateralfor those trades.

Initial margin (IM) serves a different purpose. It is to protect the non-defaulting counterparty against the risk that the mutual contracts cannot be replaced at their latest valuation amount after the default of the counterparty. The risk is that the value of the netting set of derivativeshas time to increase due to a delay. This delay can be due to a sudden lack of liquidity or other market disruption. Because this loss can impact the non-defaulting party whether they are in-the-money or out-of-the-money, initial margin collateral posting is two-way. Both parties will therefore hold IM collateral.

The WGMR has taken the view that IM should follow a `defaulter pays' principle. This means that any loss to the non-defaulting counterparty should be compensated by them keeping the collateral they have received. At the same time the defaulting party must return the collateral they hold. If the replacement loss happens to the defaulted counterparty (which impacts the value of the bankruptcy estate) then both parties must receive back their deposited collateral. The loss incurred by the defaulting counterparty must be borne by the bankruptcy estate.

The last sentence of the G20 Pittsburgh statement quoted above states that non-

centrally cleared contracts should be subject to higher capital requirements, both higher than before and higher than for cleared swaps. Nevertheless, it should be stated that the imposition of overly high charges could damage the OTC derivatives market, which would not be desirable since OTC derivatives permit various parties to create, value and risk-manage certain risks. An exchange-based market, which must focus on maximising liquidity and hence standardisation, cannot perform such a function.

The imposition of margin requirements on OTC derivatives presents a number of difficulties that do not exist in exchange-traded derivatives markets. First, there is the very great variety in OTC derivative trade types. Second, price discovery in the OTC derivatives market does not happen in one public venue. It happens in private, bilateral negotiations between parties. Third, product innovation in the OTC derivatives market is an ongoing process with new products becoming more attractive and other products less so as the market environment changes. Fourth and final, as there is no central third party like an exchange to perform the calculation of variation and initial margin, this task will have to be performed by the counterparties themselves. It is therefore important that the calculation methodology be reasonably simple, transparent, easily implementable and truly reflective of the actual risk.

Although we will discuss VM, our main focus in the rest of this report will be on the definition, mechanics, calibration and calculation of IM. In Section 2 we continue with a brief survey of the OTC derivatives market. In Section 3 we discuss the mechanics of the ISDA close-out and explain in detail the precise risks VM and IM are intended to neutralise. In

1. Introduction

Section 4 we discuss the new regulatory framework. Section 5 focuses on the two main approaches to determining the initial margin amount. Section 6 presents some calibration results for an initial margin model which follows the prescription set out by the WGMR. In Section 7 we present an overview of the ISDA SIMM approach. In Section 8 we discuss our observations.

1. Introduction

11

12

2. The Non-Cleared OTC Derivatives Market

12 - http://www.bis.org/publ/qtrpdf/r_qt1312h.pdf13 - See http://www.bis.org/publ/otc_hy1504.pdf14 - http://www.lchclearnet.com/asset-classes/otc-interest-rate-derivatives/volumes15 - The CME Group has stated that it intends to add USD swaptions to central clearing.

Over-the-counter (OTC) derivatives aretrades that are executed bilaterally between two parties rather than with a central exchange. Most trades are executed between dealers. A smaller percentage of trades are executed between dealers and non-dealers (also known as `end-users' or `customers'). Most trading in the OTC market is via telephone with an increasing amount via electronic platforms. In many cases brokers will intermediate between dealers.

Over recent years, the OTC derivatives market has split into two different sections. These are cleared and non-cleared OTC derivatives. Both are discussed below, and a more detailed description of the evolving structure of the market may be found in [Murphy (2013)]. However our focus in this report is on non-cleared OTC derivatives. We first consider the size and structure of the entire OTC derivatives market using data gathered by the Bank for International Settlements shown in Table 1. It shows the changing total notional outstanding of OTC derivative contracts every two years from 2008 to 2014 broken down by asset class. The numbers combine cleared and non-cleared contracts. It is clear that the OTC market is extremely large with a gross notional outstanding of $630 trillion in December 2014. As a reference, note that this is about ten times the amount of open interest on international derivative exchanges which in mid-2013 was estimated to be $62 trillion.12

Another important metric that indicates the size of the OTC derivatives market is the gross market value. This is the sum of the absolute value of every position across all trades without any netting. In the second half of 2014, the gross notional value was equal to $20.9 trillion.13 This is 3.2% of the gross market notional. Furthermore, as it

ignores netting, it is an upper bound on the size of counterparty exposure across the OTC derivatives market. In addition, as a measure of counterparty default exposure, it is also an over-estimate as it does not take into account the collateral that has been exchanged between counterparties.

Over the past few years, the OTC derivatives market has been transformed by the rapidincrease in usage of CCPs, mainly due to regulatory pressure from US and European lawmakers. Using a CCP means that a trade initially transacted between two dealers is immediately split so that both parties face a CCP. The payments between the counterparties are then `cleared' via the CCP. To be cleared, a derivative must be highly liquid and conform to a market-wide standard. Examples include interest rate swaps in the major currencies. A list of products mandated for clearing at LCH.Clearnet is given in Table 2. Currently LCH.Clearnet clears over 50% of the global interest rate swap market14 and over 90% of all cleared interest rate swaps. A simplified schematic is shown in Figure 1.

The dominating asset class in the OTC market is the interest rate market with a total gross notional of $505 trillion. Table 1 presents a breakdown of this market by product. In 2014, around 79% of the market was made up by interest rate swaps and these are mostly cleared. Interest rate options, consisting of caps and floors and swaptions, make up around $43 trillion and are not generally cleared.15 In terms of size, the next asset class is the FX market of which about $10.6 trillion are options which are not centrally cleared. The credit derivative market comes next. In this market the CDS indices are cleared but only a limited fraction of $25.7 trillion in single-name CDS are cleared. The equity options market then makes up $4.8 trillion

2. The Non-Cleared OTC Derivatives Market

13

Table 1: Gross notional outstanding of OTC derivatives by risk category and instrument in $bn at the end of 2008, 2010, 2012 and 2014. For each asset class of derivatives, a breakdown is provided of the main product types. Source: Bank for International Settlements (BIS).

Dec 2008 Dec 2010 Dec 2012 Dec 2014

Total contracts 598,147 601,046 635,685 630,150

Foreign exchange contracts 50,042 57,796 67,358 75,879

Outright forwards and fx swaps 24,494 28,433 31,718 37,076

Currency swaps 14,941 19,271 25,420 24,204

Options 10,608 10,092 10,220 14,600

Interest rate contracts 432,657 465,260 492,605 505,454

Forward rate agreements 41,561 51,587 71,960 80,836

Interest rate swaps 341,128 364,377 372,293 381,028

Options 49,968 49,295 48,351 43,591

Equity-linked contracts 6,471 5,635 6,251 7,941

Forwards and swaps 1,627 1,828 2,045 2,495

Options 4,844 3,807 4,207 5,446

Commodity contracts 4,427 2,922 2,587 1,868

Gold 395 397 486 300

Other commodities 4,032 2,525 2,101 1,568

Forwards and swaps 2,471 1,781 1,363 1,053

Options 1,561 744 739 515

Credit default swaps 41,883 29,898 25,068 16,399

Single-name instruments 25,740 18,145 14,309 9,041

Multi-name instruments 16,143 11,753 10,760 7,358

of which index products ... 7,476 9,656 6,747

Unallocated 62,667 39,536 41,815 22,609

Table 2: The list of standard fixed for floating interest rate products mandated for central clearing at LCH Clearnet.

Currency Index Term

EUR Euribor 28 days to 50 years

JPY LIBOR Up to 40 years

GBP LIBOR Between 28 days and 50 years

USD LIBOR Up to 50 years

Figure 1: A trade executed in the OTC derivatives market may be cleared bilaterally, in which case margining will be governed by the new regulations on VM and IM based on the WGMR rules. A cleared OTC derivative will face a CCP for which initial and variation margin will be determined by the CCP's rules.

14

and commodity options around $1.6 trillion. So while the non-cleared credit and equity derivatives markets may appear small in relative terms, they are still large in absolute terms.

We will not say more about the cleared OTC derivatives market as our focus is on the treatment of the non-cleared portion of the market, on which the new initial margin and variation margin regulations are targetted. As the cleared market has a focus on the more standard contracts, the non-cleared OTC derivatives market consists of non-standard trades in terms of currency, maturity and pay-off. This is made clear by Table 3, which is based on recent data from the DTCC trade repository. This shows that the majority of interest rate swaps are cleared whereas the swaption market is almost equally split between dealer vs dealer trades and dealer vs non-dealer trades. There is no clearing for this less standard derivative type.

Establishing the valuation of a derivative in the OTC derivatives market can be difficultas they do not trade on an exchange. Price information is however disseminated via regular communication flows between dealers, brokers and their customers. For standard cleared OTC derivatives, the variation in model valuations is typically small as brokers provide real-time swap market rates and the valuation models are fairly standard. Differences may arise due to differing valuation assumptions around CVA, OIS discounting and bid-ask spreads. For non-cleared OTC derivatives

the underlying risk inputs, such as volatility surfaces, may be harder to ascertain and the models are more complex.

2. The Non-Cleared OTC Derivatives Market

Table 3: Breakdown of counterparty types for cleared and non-cleared OTC derivatives. Numbers are gross notional in dollar equiva-lents as of December 2015. Source: DTCC.

Counterparties Swaps ($bn) Swaptions ($bn)

Dealer vs Dealer 33,011,238 12,755,918

Dealer vs Non-Dealer 84,854,728 12,226,197

Dealer vs CCP 261,333,661 0

Total 379,199,628 24,982,116

In this section we consider in detail the impact of a counterparty default between parties with non-cleared OTC derivative contracts. We do this on the assumption that the contracts have been traded under an ISDA Master Agreement. As discussed earlier, this agreement is the legal foundation of the OTC derivatives market. It is a document to which all OTC derivative counterparties sign up. Among other things, it specifies that all transactions between a pair of parties conducted within the ISDA master agreement should be considered to be a single agreement.

The treatment of counterparty default is dealt with under the category of events of default. A key feature of the ISDA Master Agreement is close-out netting. This is the fact that the claim of the non-defaulting counterparty on the bankruptcy estate of the defaulting counterparty is based on the net value of all the trades rather than being composed of a set of separate claims,with one for each trade. This is a consequence of the single agreement clause mentioned above which can be found in section 1(c) of the 2002 ISDA Master Agreement. Because all of the trades are considered as a single claim based on their net value, they are known as a netting set. The WGMR defines a netting set as a group of transactions with a single counterparty that are subject to a legally enforceable bilateral netting arrangement16 as shown in Figure 2. To understand the benefits of close-out netting, consider the following example.

Example: Suppose that there are two trades between counterparties A and B when B defaults. Trade one has value e+10m and trade two has value -e3m. Both values are from A's perspective. Treating the trades individually would result in a claim by A for e10m on the bankruptcy estate of B, receiving some recovery amount. There would also be a claim of e3m from B on A which would have to be paid in full. Assuming a 40% recovery rate, the net income for A would be e10m x 40% m — e3m = e1m. However, with netting, A's claim would be equal to e10m — e3m = e7m from which they would recover 40% giving e2.8m. This is greater than the value without netting.

A recent ISDA survey17 shown in Table 4 provides some information on the distribution of sizes of netting sets. It finds that there were 133,155 collateral agreements at the end of 2013. Of these, 87% of relate to portfolios of less than 100 trades, and 11% of agreements refer to portfolios of 100-499 trades. We would expect the benefits of netting to be greater for the larger portfolios.

The value of the netting set is calculated by summing the mark-to-market value of each trade. The mark-to-market value of a trade is the cost of replacing that trade at current market prices. Internal valuation models calculate the mark-to-market value using mid-market values. However the true replacement cost will necessarily involve trading at either the bid or ask price depending on the direction

3. Margin and Counterparty Risk

1516 - See www:bis.org/publ/bcbs128d.pdf page 255 section C.17 - See https://www2.isda.org/attachment/Njc3NQ==/2014%20ISDA%20Margin%20Survey.pdf.

Figure 2: Two parties with a netting set of N bilateral OTC derivative positions traded under an ISDA Master Agreement. In the following we will consider a scenario in which counterparty B defaults.

16

of the initial trade. We typically assume that the bid-ask price is small, although in times of market distress it may become material. The value of the netting set can be positive or negative. If positive, replacing the trades will involve paying the value of the netting set upfront in cash. If negative, replacing the trades will involve receiving the positive value of the netting set of trades upfront in cash.

In the following we will see that collateral plays a key role in reducing counterparty risk when trading non-cleared OTC derivatives. The posting of collateral as variation margin has become widespread since the GFC. A recent survey18 by ISDA shows that in 2013, 90% of non-cleared OTC transactions were subject to collateral agreements, of which 87% were ISDA CSAs. The percentage of ISDA CSA's rises to 97% and 86% for the credit and interest rate derivatives respectively. The same survey also estimated that the value of collateral in use at the end of 2013 was $3.7 trillion, of which around 75% was made up from cash and 15% government securities. The remaining collateral was mostly split across equities, corporate bonds, government agencies/GSEs and others.

Most OTC derivative contracts have been traded under either the 1992 ISDA Master Agreement or the ISDA 2002 Master Agreement. There are some differences between these two agreements when it comes to the close-out procedure. Under the ISDA 92 Master Netting Agreement (MNA), there are two decisions that must be taken.

First, the parties must choose between the `first method' in which the non-defaulting party A does not have to pay, and the ̀ second method' in which the non-defaulting party does have to pay. In most cases the second method is chosen. The second decision is whether the replacement values should be based on `market quotations' or `loss'. If `market quotations' are chosen then quotes must be requested as soon as is practicable (some leeway is provided) after the default from up to four other dealers. These are then averaged. If the `loss' approach is chosen then the non-defaulting party A needs to determine in good faith its loss as a result of the default of B.

The subsequent ISDA 2002 Master Agreement simplified matters by having only one approach, corresponding to the second method of ISDA 92. In this approach the determining party (normally the non-defaulting counterparty) calculates the close-out amount, defined as the amount of losses or costs to the determining party of replacing the initial economic exposureof the netting set. The close-out amount must be determined in good faith using commercially reasonable procedures. Relevant information including quotations, market data or other may be considered. Each party must produce a statement detailing the approach used and the marketquotes or other data on which the amount was based.

The initial margin rules described in this report are only one of the myriad of new regulations that concern derivative

3. Margin and Counterparty Risk

18 - ISDA Margin Survey 2014.

Table 4: Percentage of active non-cleared OTC collateral agreements by portfolio size as of 31 December 2013. Source: ISDA.

Number of Trades in Netting Set 2014 2013

Greater than 5,000 trades 0.3% 0.4%

Between 2,500 and 5,000 trades 0.3% 4.3%

Between 500 and 2,499 trades 1.6% 2.4%

Between 100 and 499 trades 11.0% 5.6%

Less than 100 trades 86.8% 87.4%

counterparty risk that have impacted banks since the GFC. These rules include new ways to compute counterparty-related capital charges and credit valuation adjustments (CVA). Many of these, along with variation and initial margin, are discussed in depth in [Gregory(2015)].

In the following we discuss the mechanics of close-out of a netting set after a counterparty defaults. We state that the complexities of this process are necessarily simplied as the mechanics of close-out are detailed and quite complex, and are also subject to legal interpretation. For this reason, we ask the reader to consider them as broadly correct. A full description of the legal technicalities of the ISDA Master Agreement in the close-out scenario is well beyond the scope of this report and interested readers should consult a lawyer to know precisely how a given scenario will be treated.

3.1 Risk FrameworkTo set up a framework for thinking about counterparty risk, we consider two counterparties A and B which have between them N non-centrally cleared derivative trades which form a netting set under an ISDA Master Agreement. This is shown in Figure 3.

The value of the netting set of contracts from the perspective of party A is given by VA. We can write where Vt,A is the mark-to-market value of trade t from the perspective of A. The value of the netting set of contracts from the perspective of party B is VB. This value is also known as the mark-to-market value of the contracts since it is what a counterparty would have to pay (if V > 0) or receive (if V < 0) if they had to (assuming it was possible) replace the contracts in the market immediately. We assume that A and B agree on the market valuation of their mutual netting set of trades so that VA = —VB. In practice differences may arise between counterparties due to factors including different market quotes, different valuation models and different CVA charges. If they are small then these differences may be ignored for reasons of collateral posting. If they are large then some negotiated value needs to be found.

3.2 Variation MarginThe purpose of variation margin (VM) is to protect the in-the-money counterparty against a sudden default of the other party. The amount of VM collateral needed to protect against default is simply the amount of the loss that would occur,

17

3. Margin and Counterparty Risk

Figure 3: Two parties with a netting set of N bilateral OTC derivative positions where VA is the mark- to-market value of the netting set from the perspective of party A and VB is the mark-to-market value of the netting set from the perspective of party B.

Figure 4: Timeline of default as it affects VM. The last posting of collateral is at time tL. Default occurs at time tD.

18

before recovery. Hence it equals the mark-to-market replacement value of the netting set, but only if this value is positive. VM allows the non-defaulting counterparty to replace its positions without any loss.

To see why the variation margin must be posted only to the in-the-money counterparty, consider the case of an in-the-money and out-of-the-money counterparty A when counterparty B defaults where we set V = VA for notational simplicity:1. Counterparty A is in-the-money V >0:The default of B will result in an unexpected loss for A, since a netting set of trades that had a value of V immediately prior to the default will only recover R.V, as they will become an unsecured claim on the bankruptcy estate of B where R is the fractional recovery on notional claims by unsecured creditors. Assuming that the netting set can be immediately replaced at the market value of V , there is an unexpected loss of (1—R) .V.2. Counterparty A is out-of-the-money V < 0:Positions which had a negative value at the time of default of B mean that B will have a claim on A for —V . This has to be paid in full by A. Party A is simply realising its mark-to-market loss. Economically nothing has changed from the pre-default situation provided A can immediately replace the netting set of trades at the market value of —V.

The purpose of variation margin (VM) is to protect A from the loss in the case that thevalue of its netting set is positive. This is done by B posting collateral to A. The CSA is an extension of the ISDA Master Agreement that sets out the rules governing such contractual terms as the threshold exposure for paying VM collateral, the payment frequency for posting collateral, rating triggers that may require additional

collateral to be posted and the different forms of eligible collateral.

According to the new regulations, the eligible collateral for VM includes cash, government bonds, corporate bonds, equities and gold. This is broader than some of the other proposals considered by the WGMR which included restricting VM collateral to cash only. Each type of asset is subject to a haircut as shown in Table 9. The purpose of the haircut is to protect against a fall in the value of the collateral following a counterparty default.

The new VM regulations require the daily posting of VM and the amount that has to be posted equals the difference between the mark-to-market value of the netting set adjusted by the collateral haircut, and the value of the collateral already posted. This is subject to some minimum transfer amount which has been set equal to $500,000 in the EU and $500,000 in the US.

Consider the case where A is out-of-the-money (V < 0) and has been required to post collateral to B (C < 0). In the case that A has over-collateralised their netting set with B such that the value of the collateral held by B is greater than the value of B's position, A will not automatically receive back the excess collateral if B defaults. Instead the difference (V (tD) — C(tD)), which is a positive amount as C(tD) < V (tD),will become part of A's claim on B's bankruptcy estate and only a fraction will be recovered.

3.2.1 Default ScenariosLet us consider a number of examples in which we calculate the loss when counterparty B defaults. We start with the case when A is holding excess VM collateral thanks to a haircut H. There is no

3. Margin and Counterparty Risk

IM collateral being held in these examples. It is only VM, which is not segregated such that in the event of B's default, any collateral that is held by B will become mixed in with B's estate and so will have to be claimed back by A. As ISDA claims are senior unsecured, they will obtain the corresponding recovery rate.

Example 1: The mark-to-market value to A of the netting set of trades between A and B is $320m, and due to a haircut, the amount of VM held by A is worth $335m. B suddenly defaults. A and B close out the netting set for $320m. A sells collateral worth $320m which is then used to enter into new replacement trades by transacting with other counterparties. The excess VM collateral of $(335—320) = $15m is returned from A to B. A has no loss.

Now consider the same example but with A holding insufficient VM collateral.

Example 2: The amount of VM held by A is only worth $305m. B suddenly defaults. A and B close out the netting set for $320m. A sells VM collateral worth $305m. However they need another $15m to replace the trades. A makes a claim for $15m on B, of which only 40% can be recovered. The loss to A is $(1—0.40)15= $9m.

Now consider an example in which V is negative and B defaults. This example is different because A does not hold any variation margin and would receive money if it were to enter into the replacement OTC derivative. As we will see, A loses because it has over-collateralised its trade with B.

Example 3: The value to A of the netting set of trades between A and B is -$120m.

Due to a haircut, B holds VM collateral worth $130m. B suddenly defaults. A terminates the trade and wishes to replace it at -$120m, receiving $120m. B keeps enough of A's VM collateral to cover its claim. A must then make a claim on A for the excess VM collateral worth e10m in order to replace its position. Because this is VM collateral that has not been segregated, it involves a claim on B's bankruptcy estate. Assuming a 40% recovery rate, this is a loss of $6m.

We do not consider the case when the amount of collateral posted by A to B is insufficient to cover A's claim. In this case A simply pays the difference and neither A or B incur a loss. A loss only occurs to A if it has insufficient collateral or it has posted too much VM collateral. We can therefore generalise the loss to A using the following formula

If A has posted collateral to B then CA < 0.It is simple enough to confirm this formula by considering each of the above examples. We note that between tL and tD the value of either the trade or the collateral can change.

To summarise, VM protects the non-defaulting counterparty from incurring a loss provided the VM collateral held is sufficient, and any collateral posted is not excessive. In the following section we examine what happens if the value of the netting set V and C, the value of the collateral held, change between the last collateral posting and the close-out of the derivative trades.

3. Margin and Counterparty Risk

19

20

3.3 Initial MarginInitial margin (IM) is intended to protect the non-defaulting counterparty against the loss that occurs if the cost of replacing (or closing out) the netting set of trades exceeds the amount of variation margin (VM) held. This can happen if the mark-to-market value of the netting set to the non-defaulting counterparty has increased since the last variation margin payment was made. Such a scenario is most likely to occur if counterparties are unable to replace their positions quickly due to a drop in market liquidity, thereby providing more time for market movements, or if there are very sudden price movements in the period following the default.

A full timeline of the events leading to a need for initial margin could be fairly complex. Consider this from the perspective of an in-the-money counterparty A. Assume that the last posting of collateral was at time tL so that the amount of VM collateral held is C(tL). Another VM posting is now due on date tC. A calculates the mark to market value of the netting set to give V (tC). The value of V (tC) is then communicated to counterparty B on the following day. Provided there is no dispute regarding this amount, and assuming that V (tC) — C(tC) > θ, where is the minimum transfer amount19, collateral equal in value to V (tC) — C(tC) is then posted from B to A. This may not happen until the following day.

Suppose B is in financial difficulty, but not yet in default. In this case, the collateral may not be paid immediately as B may wish to hold on to its liquid assets in an attempt to stave off default. B may do this by contesting the valuation and this dispute could last days, and potentially longer. There is also a question of whether other contractual payments such as swap

fixed or floating payments would be made during this period, and also whether collateral held by A would be returned. Eventually B defaults, but the time delay between the last posting of collateral at tL and the default time could easily add up to a week or more.

Now we consider the situation at time tD immediately after B announces that it is entering bankruptcy proceedings. In some jurisdictions, an immediate stay on the actions of creditors comes into effect immediately after a bankruptcy filing. Normally this would block an immediate close-out and possibly make it subject to the decision of the bankruptcy court. However some bankruptcy codes, most notably in the US, have carved out a `safe harbour' exception for OTC derivatives20 meaning that they are excluded from the stay and so trades may be closed out immediately.

Market volatility is likely to increase in the aftermath of the bankruptcy of B and this can cause the value of the netting set of trades to become more volatile than usual. If the value of the netting set increases, then it will cost A more to replace the defaulted trades than before, and given that the increase has not been collateralised with VM, A has an increased loss. If the value of the netting set falls then A will use the VM collateral to cover the replacement cost and will suffer no loss.

Note that in some actual cases one party has intentionally delayed the process of closing-out the netting set under the safe harbour provision.21 One possible motive for doing this may be if he or she believes that the value of the netting set is moving in his or her favour. This is generally not permitted and if such tactics become

3. Margin and Counterparty Risk

19 - $500,000 in US and e500,000 in EU.20 - See Page 36 of [Murphy(2013)].21 - See for example http://www.cadwalader.com/resources/clients-friends-memos/lehman-bankruptcy-court-holds-isda-swap-counterparty-in-violation-of-automatic-stay-counterparty-seeks-modification.

apparent, they will typically be ruled against by the bankruptcy court.

Figure 5 depicts the timing delay that leads to the need for initial margin. As before we have a trade between parties A and B where the last posting of VM was at time tL. Counterparty B defaults at time tD. We assume that following B's default, a lack of liquidity and other restrictions mean that party A can then only replace the positions at a later time tU and at a price VA(tU). The time between the last posting of collateral tL and replacement of the positions is called the margin period of risk (MPR).

3.3.1 Post-Default Close-Out Scenarios with VM onlyTo understand the mechanics of VM when there is a delayed close-out, and to quantify the loss that the initial margin amount is intended to cover, we consider a series of examples, all from the perspective of the non-defaulting counterparty A. In the first, we consider what happens if A is in-the-money and B defaults.

Example 1: Party A has a netting set of derivatives with B worth e135m. Due to a haircut, B has posted VM to A with a value of e138m. B defaults and the VM

collateral is sold immediately. Market events lead to a delay in agreeing a close-out price until six days later. On this date the cost of replacing the defaulted trades is agreed to be e145m. But A only has collateral worth e138m, so A claims e7m from B. Assuming a 40% recovery they get e2.8m and lose Loss to A = (1—R) Max[VA(tU)—CA(tU), 0] = 0,6 . Max[145—138, 0] = e4.2m.

In this example, A was partly protected by the over-collateralisation of the VM. Now we consider a scenario in which party A is out-of-the-money. This scenario is different because A has posted VM collateral to B and this must be accounted for when considering any extra cost incurred in replacing the netting set.

Example 2: Party A has a netting set of derivatives with B with a mark-to-market value of -e135m. It is holding no collateral but has posted VM to B with a value of e145m. B defaults and sells the collateral immediately for cash. A is unable to replace its trades until six days later by which time the netting set has increased in value to -e120m. A closes out the trade with B at this value. The e25m of excess collateral becomes the

3. Margin and Counterparty Risk

21

Figure 5: Timeline of default as it affects IM. The last posting of collateral is at time tL. Collateral disputes delay subsequent collateral postings between tL and the time of default tD of counterparty B. Market disruptions mean that the netting set is not closed out until time tU. The time tU —tL is called the margin period of risk (MPR).

22

subject of an unsecured claim on B from A. Assuming a 40% recovery, A loses e15m. Once again the loss formula is given by Loss to A = (1—R) Max[VA(tU)—CA(tU), 0] = 0.60 . Max[—120—(—145), 0] = e15m.

Finally we consider an example in which the sign of the value of the netting set flips between default and close-out.

Example 3: Party A has a netting set of derivatives with B worth -e15m. A has posted VM to B with a value of e18m. B defaults. Market events lead to a delay in agreeing a close-out price until six days later. On this date the cost of replacing the defaulted trades has become +e10m. B no longer has a claim on A but A has a claim on B of e10m. It also requires e18m of collateral to be repaid so A has a total claim of e28m. With a recovery rate of 40%, A loses Loss to A = (1—R) Max[VA(tU)—CA(tU), 0] = 0.60 . Max[10—(—18), 0] = e16.8m.

What is common to all of these scenarios is an increase in the value of the trade over the value of the collateral at the default time from the perspective of the non-defaulting counterparty. The loss formula is the same whether VA > 0 or VA < 0. The IM is set so that it can cover this loss to a high confidence. We see from this formula that IM will be needed by either of the twocounterparties to a netting set, although only the non-defaulting party is permitted to use it. The loss for party A if B defaults is given by IM Loss to A = (1—RB) Max[VA(tU)—CA(tU), 0] and for party B if A defaults is IM Loss to B = (1—RA) Max[—VA(tU)—CA(tU), 0].

where RA and RB are the respective recovery rates of party A and party B following their default. These loss amounts depend on the change in the value of both the netting set

and the collateral between tL and tU. If we are being conservative then we can assume that RA = RB = 0. In both cases we know that CA(tL) = V (tL) / (1—H) at the last time of collateral posting tL Unless in cash, the value of this collateral will almost change between tLand close-out time tU.

3.3.2 Default Scenarios with IMNow reconsider an examples from the perspective of the non-defaulting counterparty A. In this case both parties have posted initial margin.

Example 1: Party A has a netting set of derivatives with B worth e135m. Due to a haircut, B has posted VM to A with a value of e138m. A and B have both calculated and exchanged IM worth $10m. B defaults and A is unable to replace the trades until six days later. On this date the cost of replacing the defaulted trades is agreed to be e145m. Also, A has VM collateral now worth e138m. The cost to A of closing out the trades has led to a loss of e145—e138 =e7m. Party A simply uses the $10m of IM that B deposited to cover this loss. The remaining e3m is returned to B. A receives back his $10m in IM collateral from B as it has been segregated.

The loss is now completely covered by the IM. If the loss had exceeded the IM then A would have had a claim on the bankruptcy estate of B, and so would have incurred a loss on the unrecovered fraction of this amount.

3.4 The Distribution of LossesThe risk covered by IM is a future loss conditional on an increase in the value of the netting set (or a decline in the value of the collateral, or both) following the default of the other counterparty. So any

3. Margin and Counterparty Risk

attempt to model the loss amount for party A has to simulate the change in the value of the netting set ∆VA from time tL to tU and so needs to reflect the market environment following the default of a major derivatives dealer. Model calibration presents a problem as we do not have many examples in which large derivatives counterparties have defaulted, allowing usto empirically estimate the typical market adjustment.

A full model-based calculation of IM would need to take into account the volatility of the value of the position, the impact of the default of the counterparty on market liquidity, and the impact of the default on any tendency for the value of the position to increase before it can be re-established. If we wish to take into account the effect of collateral, we would then need to add that to the netting set portfolio and to take into account the effect of any correlations.

The output of the model needs to be a distribution of the loss due to future value changes of the netting set (including collateral) between time tL and time tU. We therefore define ∆V = V(tU)—C(tU) where C(tU) is the value at time tU of the collateral that has been posted. There will be two values of IM, one for counterparty A and one for counterparty B. These can be written as

IM Loss to A = Max[VA(tU)—CA(tU). 0]

IM Losst to B = Max[CA(tU)—VA(tU). 0].

For this reason, whether V refers to VA or VB depends on which counterparty we are considering. We also define ρ(∆V) to be the probability density function of ∆V. We note that this distribution of losses is almost certainly not symmetric about ∆V = 0. Its shape is driven by the pay-off

of the derivative trades in the netting set portfolio and the form of the distribution assumed for the underlying risk factors.

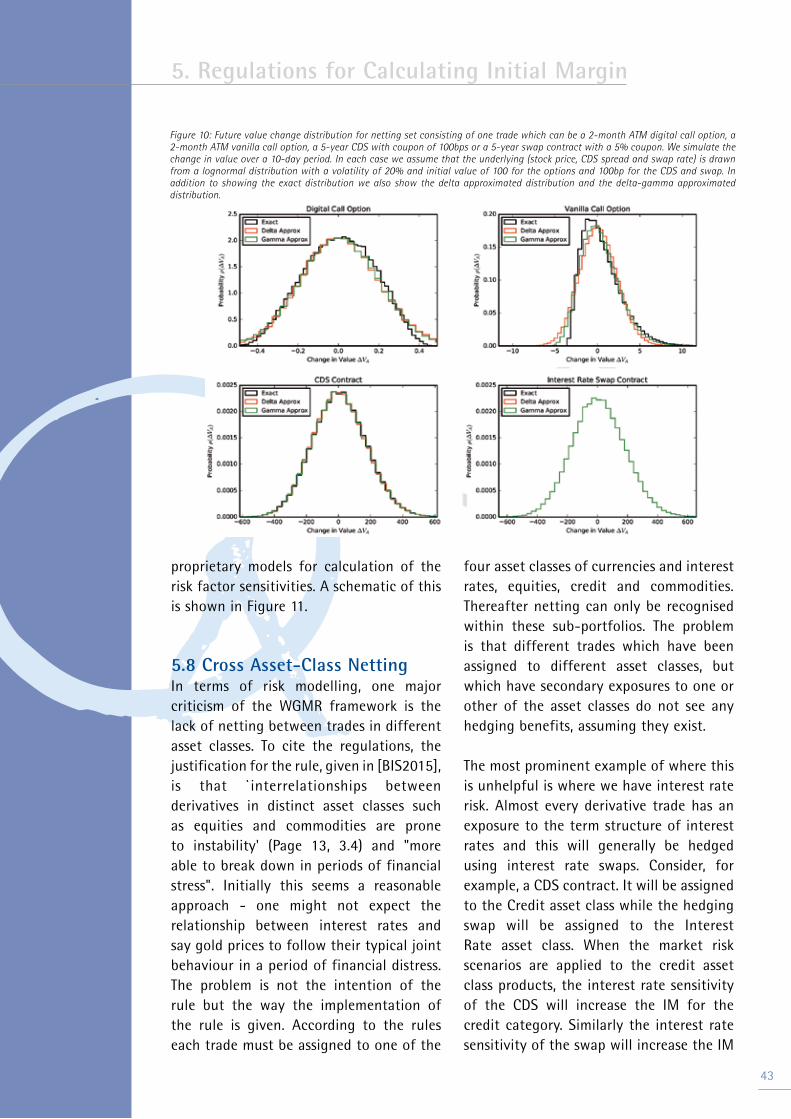

Figure 6: Future value change distribution for a digital call option and a vanilla call option both with K = 100, S = 100 and T = 2 months to expiry. We set σ = 20% and simulate the change in value over a 10-day period. We centre the distribution at the zero loss to emphasis the extent to which the distribution is not symmetric about zero.

An example of this asymmetry can be seen in Figure 6 where we plot the value changedistribution for a netting set consisting of a simple short-dated at-the-money call option from the perspective of counterparty A. The risk factor is the stock price which is assumed to obey a lognormal distribution with a volatility of 20%. The MPR is assumed to be 10 days.

This asymmetry, which was not present in the standardised approach, means that the probability that A sees his netting set increase in value by $5m is not the same as the probability that B sees his netting set increase in value by $5m. The implication of this is that the amount of initial margin

3. Margin and Counterparty Risk

23

24

that A must post to B is not the same as the amount that B must post to A. This adds a certain amount of additional negotiation to the IM posting as it means that both parties must be able to agree on two values rather than just one.

3. Margin and Counterparty Risk

Following the Pittsburgh declaration, the body charged with drawing up the detailed regulations for the non-cleared derivatives market has been the Basel Committee on Banking Supervision (BCBS) and the Board of the International Organization of Securities Commissions (IOSCO). In this section we provide an overview of the new VM and IM regulations put forward by theWGMR. These can be found in the March 2015 version of Margin requirements for non-centrally cleared derivatives22.

4.1 Variation Margin RegulationsWhile VM has been an aspect of OTC derivatives markets since their inception, and is documented by the ISDA CSA, it has not always been universally applied. Under the new regulations the scope of market participants who are subject to VM has been defined explicitly. One of the key principals of the new regulations states that all financial firms and systemically important non-financial entities (`covered entities') that engage in non-centrally cleared derivatives must exchange initial and variation margin as appropriate to the counterparty risks posed by such transactions'. The range of covered entities includes financial firms and those non-financial firms deemed to be systemically important. However, it does not include central banks, development banks and sovereign issuers.

The new regulations note that VM should be posted with `sufficient frequency (e.g. daily)'. This is subject to a minimum transfer amount of e500,000 in the EU and $500,000 in US. The size of the VM that needs to be held is the market value of the netting set of derivatives (which will be positive for the party receiving VM). As some of the products in the netting set may be exotic or illiquid,

determination of their market value may be partly subjective and subjectto dispute between both parties. For this reason, the BCBS/IOSCO has insisted that `robust' dispute resolution procedures need to be put in place before such trades are executed.

The form of collateral permitted for VM is quite broad as we discuss below. There are no restrictions on what the party receiving the collateral can do with it. It does not need to be segregated and can be rehypothecated. Clearly, if the counterparty defaults and the non-defaulting counterparty is in-the-money but has rehypothecated the collateral it has received, it is very much in their interest to make sure that they can have this collateral returned. Unfortunately this mixing of assets means that a non-defaulting counterparty that has posted variation margin worth more than the value of the netting set will not have its excess collateral returned automatically following a default. Instead they will need to enter a claim in the bankruptcy process.

In terms of liquidity, the posting of VM does transfer liquidity from the poster to the receiver and so the poster loses use of the collateral. It is a gain in liquidity for the receiver of the collateral. Therefore, the effect on the overall liquidity of the market is unchanged. This is one feature in which VM is very different from IM.

A timetable for the implementation of the new VM regulations is shown in Table 5. This shows that it is expected that there will be a universal application of VM after early 2017. For large entities which have a monthly notional of non-centrally cleared derivatives in excess of e3 trillion, the range of contracts subject to the new rules are those transacted after 1 September

4. The Regulatory Framework

2522 - See http://www.bis.org/bcbs/publ/d317:pdf

26

2016. For the remaining parties it only applies to contracts transacted after 1 March 2017.

4.2 Initial Margin RegulationsAssuming that the default of a financial institution is sudden and unpredictable, the loss event which IM is intended to cover can potentially cause either of the two parties to incur a loss. However, IM only protects the non-defaulting party. For this reason, the regulations around IM differ in a number of fundamental ways from those governing variation margin.

In terms of product coverage, the new IM requirements are very broad as they apply to all non-centrally cleared derivatives, except physically settled currency forwards and swaps. For cross-currency swaps they do not apply to the fixed physically settled FX transactions associated with the exchange of principal.

The WGMR has stated as a principle that IM should be based on a `defaulter pays' approach. Since the loss that IM covers can impact either party, the regulations require an exchange of margin by both parties. In order that the margin posted by the defaulting counterparty is immediately available to the non-defaulting counterparty at the time of default, and additionally that the margin posted by the non-defaulting counterparty is returned. Because of this requirement, the IM cannot be reused, repledged or rehypothecated (except for very specific hedging purposes described in the WGMR framework document). It is key that the margin amounts are held in a ring-fenced segregated account. This suggests the use of a third-party custodian account.

The overall result is that summed across the financial system, the amount of IM collateral posted will greatly exceed the likely realised losses that might occur following a counterparty default. Consider, for example, a world of N counterparties,

4. The Regulatory Framework

Table 5: The implementation timetable for Variation Margin. The regulations are expected to be fully implemented by 1 March 2017.

Implementation Date Who pays Variation Margin and When

1 September 2016 After this date any covered entity with monthly notional non-centrally cleared in excess of e3 trillion across March, April and May 2016 will be required to exchange VM for contracts traded after 1 September 2016

1 March 2017 After this date all covered entities will be required to exchange VM

Figure 7: Two parties A and B depositing IM with a third-party custodian. The amounts IMA and IMB can be different and are held in segregated accounts.

and suppose they all face identical and symmetric risks resulting in an initial margin for each counterparty equal to G. In this case the total amount of initial margin posted will be N(N—1)G. We would not expect secondary defaults due to the use of VM and IM. However, if one counterparty defaults, the total losses will, with high confidence, be less than (N—1)G. So the system is effectively putting aside N times as much collateral as is needed to protect against a default.

Collateral that has been provided as initial margin from a customer (buy-side financial firm or non-financial company) can be rehypothecated for the purpose of hedging the derivative positions of the receiver of the collateral only if permission has been given by the provider. The collateral must also be held in a form that protects the rights of the customer. If the customer has agreed to allow rehypothecation, then they have to be informed of this and how much has been rehypothecated.

As with the VM, the form of collateral used for IM must be accessible when needed and be provided in a form that can be `liquidated rapidly and at a predictable price even in a time of financial stress'. In order to mitigate this loss of liquidity, the rules allow a fairly broad range of assets to be used, albeit subject to a haircut. These haircuts are the same as those used for VM.

To restrict the imposition of IM to counterparties with large derivatives exposures, regulators have imposed an IM threshold. This states that no IM has to be posted until the amount of IM exceeds e50m. Beyond this threshold, the amount of collateral to be posted is the differencebetween the IM amount and the threshold. To prevent companies from creating new entities in a group structure in order to reuse the threshold, the threshold can only be applied on a consolidated group basis.

The timetable for the introduction of IM is given in Table 6. There is a gradual ramp-up phase in terms of counterparty size, as determined by the monthly notional of non-centrally cleared OTC derivatives traded by that party. It is envisaged that the IM arrangements will be fully operational by the end of August 2020.

4.3 Collateral HaircutsBoth VM and IM require the posting of collateral. Because this collateral is needed to protect against losses in the scenario in which one counterparty defaults, it is essential that the collateral is able to hold its value in times of financial stress. One concern is that the collateral value could be correlated to the event of a bank default and this, according to the regulations, should be avoided.

4. The Regulatory Framework

27

Table 6: The implementation timeline for Initial Margin. The first implementation deadline for the largest parties will be in September 2016. All covered entities will be subject to the IM rules by 1 September 2019.

Implementation Date Who pays Initial Margin and When

1 September 2016to 31 August 2017

Any covered entity with monthly notional non-centrally cleared in excess of e3 trillion will be required to exchange IM

1 September 2017 to 31 August 2018

Any covered entity with monthly notional non-centrally cleared in excess of e2.25 trillion will be required to exchange IM

1 September 2018 to 31 August 2019

Any covered entity with monthly notional non-centrally cleared in excess of e1.5 trillion will be required to exchange IM

1 September 2019 to 31 August 2020

Any covered entity with monthly notional non-centrally cleared in excess of e0.75 trillion will be required to exchange IM

1 September 2019 to 31 August 2020

Any covered entity with monthly notional non-centrally cleared in excess of e8 billion will be required to exchange IM

28

One way to reduce this risk would be to limit the range of collateral to only the safest form of assets, e.g. cash or short-term Treasury bills. However, this could have a negative impact on market liquidity, especially as this IM collateral cannot be re-used or re-hypothecated. For this reason, the WGMR has widened the range of eligible collateral to include cash, high quality government bonds and central bank securities, high-quality corporate bonds, high-quality covered bonds, equities in major stock indices and gold.

To adjust for the riskiness of these assets, a table of haircuts has been provided and this is shown in Figure 7. The eligible collateral can also be in any currency, and this explains the last row of the haircut table which imposes an 8% haircut on collateral if it is denominated in a different currency from that of the netting set derivatives.

Because of the limits on re-use and re-hypothecation, one of the major concern across banks is the impact of initial margin on market liquidity. An analysis of the expected liquidity impact of IM has been performed by the WGMR. Known as the Quantitative Impact Study, this was carried

during 2012 and 2013 and shows23 that if a threshold for IM of e50m ($65m in US) is used, the amount of IM required would be around e558 billion. This is a substantial amount of collateral, especially as it cannot be rehypothecated. A 2014 report by the European Central Bank (ECB) estimates24 that the overall supply of high quality assets at a global level is around e41 trillion. If we restrict collateral to those eligible for CCPs, the number drops to a range of between e2 and e14 trillion. And if we just consider margin eligible for initial margin, we get e5 to e28 trillion. This seems to be well in excess of the e558 billion mentioned above. But we should be aware that this is in the context of additional liquidity requirements that are being applied to banks such as the Liquidity Coverage Ratio25 and Net Stable Funding Ratio26. So while sufficient collateral does exist, demand for high-quality collateral is growing.

4.4 Comparison of US and European RegulationsWe have already mentioned that the WGMR framework is to establish minimum global standards that legislators can then translate into law. In the US, the rules have

4. The Regulatory Framework

23 - See http://www.bis.org/publ/bcbs242:pdf24 - See https://www.ecb.europa.eu/pub/pdf/other/cea201407en.pdf?c5856909bbcb7b0ed884be5b281ddc24.25 - See http://www.bis.org/publ/bcbs238:pdf26 - See http://www.bis.org/publ/bcbs271:pdf

Table 7: The schedule of standardised haircuts as they apply to derivatives for which the asset class is the primary one for that derivative. See Appendix B of www:bis:org/publ/bcbs261:pdf

Asset Class Collateral Haircut (% of value)

Cash in same currency High quality government bonds and central central bank securities

0

Under 1 year 0.5

1-5 years 2

Over 5 years 4

High quality corporate/covered bonds

Under 1 year 1

1-5 years 4

Over 5 years 8

Equities in major stock indices 15

Gold 15

Currency mismatch 8

4. The Regulatory Framework

29

been set by the CFTC27 and in Europe they are being set by ESMA, the EBA, and EIOPA. We now wish to discuss the main regional differences between the US and Europe.

In the US, the new VM and IM rules apply to any `covered swap entity' (CSE) which is a CFTC-registered swap dealer or major swap participant. It exempts those parties that deal with less than $8 billion of notional a year and those who are declared to be non-financial end users. VM will be required for all financial end users and for swap entities who trade with CSEs. A CSE must post or collect IM within one business day after a swap is executed subject to a minimum transfer amount of $500,000 and a threshold value for IM of $65m. The daily posting of VM collateral is also required and has the same minimum transfer amount. The IM amount can be calculated using a model or use the standard table of add-ons shown in Table 9. The US rules recognise an additional number of asset categories that may be used in an initial margin model with the set of risk categories and these include agriculture, energy, metals, and other commodities. The US law also exempts certain products from the margining requirement. It also broadens the range of the calibration period to 1-5 years. It also requires collateral to be segregated at third-party custodians.

The EU rules have fewer changes with respect to the WGMR framework. The covered entities are financial counterparties (FC), non-financial counterparties (NFCs) as classified under EMIR, and those above the EMIR clearing threshold (NFC+). While any covered entity must exchange VM, only those with an aggregate month-end notional amount of non-centrally cleared derivatives of over e8 billion have to exchange IM. All OTC derivatives that have not been cleared by a CCP are subject to the new margin rules. The minimum transfer amount under EMIR is e500,000. The threshold for posting IM is e50m. A summary of the differences can be found in Table 8.

27 - See Federal Register at http://www.cftc.gov/idc/groups/public/@lrfederalregister/documents/file/2015-32320a.pdf.

Table 8: A list of the main differences between US and EU implementations of their regulations on margin for non-cleared OTC derivatives.

Regulation EU Treatment US Treatment

Covered Entities Financial and Non-Financial Exempts Non-Financial Entities

Minimum Transfer Amount e500,000 $500,000

IM Threshold e50m $65m

Covered Transactions Exempts options on certain securities

Eligible Collateral An 8% charge when currencies of collateral and derivative differs

Requires collateral to be in USDor currency of swap

IM Model Categories 4 in Europe 4+ in US

Calibration Period 3-5 years 1-5 years

IM Segregation US requires segregation at3rd party custodians

30

4. The Regulatory Framework

The IM charge is designed to be a protection against a potential future exposure (PFE) in which the cost of closing out a netting set of trades exceeds the amount of VM held. This potential loss cannot therefore be known either now, or even at the time of the counterparty default. The most we can do is to construct a model which can quantify the possible distribution of lossesand to extract from that a tail risk amount with some defined confidence level.

To achieve its aim, the modelling approach must be conservative such that to some high level of confidence, the amount of posted IM will be sufficient to cover any loss in most scenarios. Equally it must be reasonable. A charge that has been set too high could damage the non-cleared derivatives market. Also, the amount of IM required should be aligned with the risk that it is intended to hedge. If this is not the case then behaviours could develop which would be counter to the objectives of IM.