EVALUATING THE IMPLEMENTATIONOF CLEANER PRODUCTION AUDITDEMONSTRATION PROJECTS

Katherine Kao CushingUniversity of California, Berkeley

Peter L. Wise and Janet Hawes-DavisIllinois Environmental Protection Agency

Cleaner production audit demonstration projects were carried out in two Chi-nese case factories as part of a project co-sponsored by the Illinois Environmen-tal Protection Agency and China’s State Environmental Protection Administra-tion. Audit results at both factories were characterized by implementation ofpredominantly low- or no-cost options, notable reductions in water pollution,and incomplete financial benefit analyses. Two reasons explain the financialbenefit analyses’ apparent weakness. First, factory audit teams were inexperi-enced in the techniques and procedures used to determine the economic benefitsof cleaner production options. Second, motivations project personnel had forparticipating in the demonstration projects were not centered on attaining themonetary benefits of implementing cleaner production. Instead, other factorsrelated to the international nature of the project, such as a high degree of statelevel oversight and prestige, were more influential in affecting the behavior ofproject personnel. 1999 Elsevier Science Inc.

Introduction

The Chinese government’s formal efforts to promote cleaner production(qingjie shengchan) began in the early 1990s. A central component of theseefforts has been implementing cleaner production audit demonstration proj-ects with the assistance of bilateral and multilateral aid agencies. Since 1992,China’s government has conducted cleaner production audit demonstrationprojects with organizations including the World Bank, the United NationsEnvironment Programme (UNEP), the Overseas Development Agency of

Address requests for reprints to: Katherine Kao Cushing, 990 Lundy Lane, Los Altos, CA 94024,USA. [email protected]

ENVIRON IMPACT ASSESS REV 1999;19:569–586 1999 Elsevier Science Inc. All rights reserved. 0195-9255/99/$–see front matter655 Avenue of the Americas, New York, NY 10010 PII S0195-9255(99)00027-X

570 KATHERINE KAO CUSHING ET AL.

Britain, and the Canadian Ministry of Foreign Affairs (NEPA and CNCPC1996). This research examines one such project—a cooperative effort be-tween the Illinois Environmental Protection Agency (IL EPA) of theUnited States and the National Environmental Protection Agency (NEPA)1

of China.This project, “International Diffusion of Pollution Prevention Technolo-

gies through Outreach, Assessments, Demonstrations, and Evaluations forthe Metal Finishing, Petrochemical, and Pharmaceutical Industries inChina,” hereafter referred to as the “IL EPA-NEPA project,” includedcarrying out cleaner production audits in six large state-owned factories.The IL EPA-NEPA project team selected two factories in each of thesesectors (i.e., metal finishing, petrochemical, and pharmaceutical) to partici-pate in the audits. This paper follows the progress of the two Chinesepharmaceutical factories, Xinhua and Huabei, that participated in the ILEPA-NEPA project through a 10-month audit implementation process. Itassesses the environmental and financial impacts of audit implementation,explains those results, and relates the study’s findings to the larger issueof promoting cleaner production via demonstration projects in China andother industrializing countries.

Definition and Process

Cleaner production is one of several terms used to describe an environmen-tal management strategy that focuses on waste minimization. Accordingto the Chinese National Cleaner Production Center (CNCPC), a leadingauthority on cleaner production in China, cleaner production in the Chinesecontext is defined as follows:

Cleaner production is the continuous application of an integrated preven-tative environmental strategy to processes and products to reduce risksto humans and the environment.

For production processes, cleaner production includes conserving rawmaterials and energy, eliminating toxic raw materials, and reducing thequantity and toxicity of all emissions and wastes before they leave aprocess.

For products, the strategy focuses on reducing impacts along the entirelife cycle of the product, from raw material extraction to the ultimatedisposal of the product. Cleaner production is achieved by applying know-how, by improving technology, and by changing attitudes (Duan 1996).

Based on this broad definition, cleaner production encompasses numer-ous activities, ranging from instituting a periodic valve maintenance system

1 Since the time of the project, NEPA has been elevated in organizational status and renamed the StateEnvironmental Protection Administration (SEPA).

CP AUDIT DEMONSTRATION PROJECTS 571

to installing equipment to recover solvents in the manufacturing process.Examples of cleaner production activities commonly used by US pharma-ceutical factories include using water-based cleaning solutions instead ofsolvent-based solutions, automating a material handling and transfer systemto reduce the likelihood of spilling raw materials, and recovering acetoneor other solvents from a wastestream for re-use in a chemical reactor (USEPA 1991).

Chinese factories can implement cleaner production in a variety of ways.For example, the study by Warren (1996) of Chinese electroplating factoriesshows how Chinese factory management may elect to adopt certain pollu-tion prevention practices in a “piecemeal” fashion, independent of conduct-ing a factorywide pollution prevention audit. Alternatively, factories mayimplement cleaner production in a more systematic, formal manner, inwhich factory teams follow detailed step-by-step procedures. The two casefactories in this study utilized the following formalized audit process devel-oped by the CNCPC.

According to the CNCPC, a formalized audit should consist of the follow-ing seven steps: (1) planning and organization, (2) preassessment, (3) assess-ment, (4) option generation and screening, (5) feasibility analysis, (6) optionimplementation, and (7) continuing cleaner production (CNCPC 1995).Although there are other ways to implement cleaner production, this seven-step methodology is promoted by the CNCPC as the recommended wayto perform an audit.

In the first two steps of the audit process, top factory management shouldassemble a multi-disciplinary audit team, and that team should conduct abasic survey of the plant site’s operations to identify one particular manufac-turing area, or workshop,2 as the focus of the audit. The team shouldestablish pollution prevention goals and begin implementing low- and no-cost options as they are identified. During the third step of the audit process(assessment), the audit team is supposed to conduct an in-depth analysisof each manufacturing operation carried out in the selected workshop and,from this analysis, identify further cleaner production options that the teamshould consider implementing. In the fourth step (option generation andscreening), the audit team should implement low- and no-cost optionsidentified during the previous step as well as conduct a general analysisof medium- and high-cost cleaner production options. The CNCPC alsorecommends writing a mid-term audit report during step 4.

In step 5, feasibility analysis, the audit team should further analyze me-dium- and high-cost options using criteria related to technical and financialfeasibility, as well as environmental benefits. Based on this analysis, theteam members determine which, if any, of the medium- or high-cost options

2 In China, manufacturing facilities are organized into units called chejian workshops, which are product-or process-specific.

572 KATHERINE KAO CUSHING ET AL.

they want to implement. In step 6, option implementation, the audit teamcarries out the medium- and high-cost options that appear feasible basedon the analysis performed in the previous step. The seventh and final stepin the process is continuing cleaner production. Here, the audit team shouldanalyze what it learned from the initial audit and develop ways to continueimplementing cleaner production throughout the factory.

Project Background

Market opportunities motivated a US state environmental protectionagency, the IL EPA, to become involved in an international cleaner produc-tion project. Although the US currently holds a large share of the totalworld market for environmental technology, the sales of most US companiesare domestic (IL EPA 1997). Moreover, the world market for environmen-tal technologies is expected to grow from $300 billion in 1994 to $600 billionby 2000 (US EPA 1994). The US portion of the IL EPA-NEPA projectwas funded by the US EPA Environmental Technology Initiative (ETI),a program established in 1994 to maximize US opportunities for enteringthe world market for environmental technology through a strategic use ofUS government funds and collaboration between government agenciesand private stakeholders. To implement the ETI program, the US EPAannounced a grant competition in which federal, state, and tribal entities, inpartnership with other government agencies or private industries, proposedprojects that would serve the program’s purpose. The IL EPA-NEPA proj-ect—led by the IL EPA in cooperation with NEPA, the World Bank, theUNEP, and the Chemical Industry Council of Illinois—was one of the USEPA’s grant competition winners.

The IL EPA selected China as the project location for several reasons.First, China is faced with significant sustainable development issues. Thecountry’s rapid industrialization, combined with and problematic enforce-ment of its environmental laws (Cushing 1998; Ma 1997; Sinkule 1993) hasled to severe environmental degradation (Edmonds 1994; He 1991; Smil1993). Thus, the perceived need for a cleaner production demonstrationproject in China was high. Second, Chinese government institutions andthe general public have become increasingly aware of and interested inenvironmental protection issues, including cleaner production. And third,the US government views China as an important potential market forAmerican environmental products and services. By conducting the projectin China, the IL EPA would be able to obtain information on the currentand future environmental technology needs of several Chinese industries.

The pharmaceutical industry was selected as one of the IL EPA-NEPAproject’s target sectors for three reasons: (1) previous initiatives by theWorld Bank and UNEP identified this sector as a major source of pollutionin China; (2) the pharmaceutical industry was the focus of previous US EPA

CP AUDIT DEMONSTRATION PROJECTS 573

pollution prevention outreach efforts, thus a substantial body of cleanerproduction research materials existed for this industry; and (3) pharmaceuti-cal companies and environmental technology vendors that support themwere prevalent in Illinois and throughout the US. The IL EPA consideredthe Chinese pharmaceutical sector in China to be expanding rapidly, withneeds for environmental technologies similar to those being utilized in the US.

Audit Implementation Results

The two case pharmaceutical factories that participated in the IL EPA-NEPA project, Huabei and Xinhua, are representative of the 50 very largestate-owned enterprises that form the backbone of the Chinese pharmaceu-tical industry. In total, these large firms accounted for approximately 40%of the industry’s total output in 1995 (Shen 1996). Nationwide, there areabout 1,500 firms in China that produce Western pharmaceuticals (e.g.,antibiotics, cardiovascular drugs) (SPAC 1995).

The Huabei and Xinhua audit teams conducted the majority of theiraudit work between January and October 1996. During this period, auditteam members received training and assistance from IL EPA staff, USpharmaceutical industry experts, UNEP cleaner production specialists, andCNCPC staff. On the Chinese side, two national-level Chinese organiza-tions, NEPA and the State Pharmaceutical Administration of China(SPAC), oversaw the audits’ implementation (e.g., by attending workshopsand visiting factories).

Each of the case factories had several on-site manufacturing areas, orworkshops, where different types of production operations were carriedout. For example, Huabei had 10 workshops and a branch factory locatedin another area of town. Xinhua had 16 workshops under its direct supervi-sion. At both factories, cleaner production projects were conducted in asingle workshop at the main factory site—a solvent workshop at Huabeiand a caffeine workshop at Xinhua. Each of these workshops was the mainsource of organic pollution at its factory, accounting for 25% and 30% ofthe total chemical oxygen demand (COD)3 in wastewater discharges atHuabei and Xinhua, respectively.

Both factories implemented about half of the options identified by theiraudit teams. Huabei followed through with 5 of 10 options, and they aredescribed in Table 1. All of the implemented options were categorized bythe audit team as low or no cost.4 Two of the options the team imple-mented—recycling equipment washwater and hot wastewater, and increas-ing the quantity of distiller material recirculated—fall into the cleaner

3 COD is a widely used indicator of the amount of organic material in wastewater.4 Typically, there are three cost categories for analyzing cleaner production options: (1) low and no cost;

medium cost; and high cost. The ranges for each of these categories are typically determined by eachindividual audit team and often depend on the factory’s size, with larger factories having larger ranges forthe cost categories.

574 KATHERINE KAO CUSHING ET AL.

TABLE 1. Cleaner Production Options Implemented by Huabei

Option No. Description

1 Recycling equipment cleaning water and hot wastewater2 Increasing the quantity of distiller material recirculated3 Recovering butanol from wastestream4 Increasing the concentration of base added to the distillation tower5 Adding measuring equipment to economize on water consumption

Source: Huabei Pharmaceutical Factory (1996).

production category of recycling and reuse. The other three implementedoptions—recovering butanol from wastestream, increasing the concentra-tion of base added to the distillation tower, and adding measuring equip-ment to economize on water consumption—involved efforts to optimizeoperating conditions.

The Huabei team chose not to implement five other options identifiedthrough the audit process, and these included measures such as improvingthe waste distiller unit treatment process, recycling solid carbon dioxidefrom fermentation exhaust gas, culturing higher quality bacteria for thefermentation process, and redesigning the distillation process. In the processof screening options, these projects were eliminated for implementationbased on reasons such as the high degree of new technology required, highcost, and the length of time required to implement the project (HuabeiPharmaceutical Factory, 1996). The following excerpt from the audit team’sfinal report explains, for example, why two of the these options weren’t se-lected:

Options F5 [redesigning distillation tower] and F9 [culturing high qualitybacteria] are high cost and high tech options. No mature technologyexists [in China] to implement these options at the present time, so wecan’t implement them immediately (Huabei Pharmaceutical Factory,1996, p. 37).

The Xinhua factory team implemented 11 of 21 cleaner production op-tions. Table 2 presents descriptions of these projects. The audit team catego-rized the first four options as enhancing internal management (i.e., viatraining, monitoring, and maintenance) and the remaining seven optionsas optimizing process conditions (e.g., decreasing active carbon usage).Eight of the 21 options identified by the audit team were related to technol-ogy and equipment renovation, but none of these options was carried outas part of this project. The vast majority of the options implemented bythe project team, 10 of 11, were low or no cost (options 1 through 10 inTable 2), whereas one of the implemented options (option 11) was mediumcost. The audit team estimated the cost of option 11 to be approximately$30,000 US. Of the 10 options identified by the audit team that were not

CP AUDIT DEMONSTRATION PROJECTS 575

TABLE 2. Cleaner Production Options Implemented by Xinhua

Option No. Description

1 Providing cleaner production training to operatorsImproving operating procedures by including cleaner production-

2 related components3 Periodically maintaining and repairing equipment4 Periodically monitoring and analyzing wastestream

Controlling raw material quality, improving yield rate of5 dimethyl FAU

Increasing amount of vacuum in chamber, decreasing amount of6 acetic andryhide7 Decreasing formic acid usage8 Decreasing active carbon usage9 Decreasing consumption of dimethyl urea

Recycling distilled water from mother liquor concentration into10 primary refining11 Treat water containing cyanide, recover NaCN, recycle water

Source: Xinhua Pharmaceutical Factory (1996).

carried out, two were low cost ($1,800 to $4,000), three were medium cost($6,000 to $30,000), and five were high cost ($144,000 to $360,000) (XinhuaPharmaceutical Factory 1996). Reasons cited for not implementing certaincleaner production options included additional equipment requirements,technical complexity, and high cost (Xinhua Pharmaceutical Factory 1996).

Environmental Significance

To analyze the environmental benefits of the projects, we examined twovariables: reduction in COD generated, and reduction in wastewater gener-ated.5 We selected these variables because, in the Chinese pharmaceuticalindustry, wastewater is the most significant type of pollution and COD isthe wastewater pollutant indicator of greatest concern (Cushing 1998).We compared the amounts of COD and wastewater generated before theimplementation of the cleaner production project to the amount of CODand wastewater generated after project implementation. We defined theenvironmental effects of project implementation to be significant if they

5 The issue of regulatory compliance was not a major part of the factories’ cleaner production auditsand, as such, was not emphasized in our analysis. Originally, we had planned to interpret the effects ofimplementing cleaner production as significant from a regulatory perspective if a factory went from ex-ceeding local discharge standards to being in compliance with local discharge standards as a result offollowing through on options identified through the audit. However, in the course of collecting data onthe factories’ regulatory status before and after the project, we found that the factories themselves paidlittle attention to the state of their environmental compliance, both during their participation in projectconferences and in their final audit reports. Furthermore, interviews with IL EPA officials and US consul-tants working on the project confirmed that regulatory compliance was not a major priority of the auditteams.

576 KATHERINE KAO CUSHING ET AL.

approximated the reduction goals set by the factory in the preassessmentstage of the audit process.

Tables 3 and 4 present estimated reductions in COD and wastewater gener-ation that resulted from executing options identified through the cleanerproduction audits. Differences between the targeted and actual reductionvalues are in the far right columns of the tables. Because the two factoriesused different units for setting their reduction targets, their results are notcomparable. In each case, however, the tables indicate whether the factorymet its own reduction goals.

Table 3 lists COD reduction. Huabei’s main reduction objective in thisregard was to reduce the COD concentration in its wastestream. In Huabei’scleaner production audit plans, the target was to reduce COD concentrationby 2%. As shown in Table 3, Huabei exceeded its COD reduction goalby 32%. Xinhua’s COD reduction goals had different units—tons CODgenerated per year. In Xinhua’s cleaner production audit plans, the goalwas to reduce tons of COD generated per year by 29%. Table 3 showsthat Xinhua came close to meeting its COD reduction goal. The factory’sactual reduction was 25%, which was 4% less than the target.

Table 4 lists reduction data for wastewater generation in units of tonswastewater per year. For this variable, Huabei analyzed two different waste-water streams within the workshop. One wastewater stream came from adistillation unit and had a high concentration of COD; the other streamcame from cooling water and washwater and had a low concentration ofCOD. Table 4 shows that Huabei exceeded its goal for wastewater reductionin its low COD concentration wastestream by 18% and came close tomeeting its goal for wastewater reduction in its high COD concentrationwastestream. The Xinhua factory was concerned only with wastewaterreduction in its high concentration COD wastestream, and Table 4 showsthat Huabei exceeded its goal for wastewater reduction by 1%. Becauseboth Huabei and Xinhua either exceeded or came close to meeting theirCOD and wastewater reduction goals, we characterized the environmentalbenefits of audit implementation as “significant.”

Financial Significance

To evaluate the financial impact of the projects, we examined the factoryaudit teams’ analyses of estimated financial benefits for the cleaner produc-tion options they implemented. According to factory audit teams reports,Huabei and Xinhua estimated that the annual monetary benefits of imple-menting cleaner production in the targeted workshops were ¥228,000($27,500 US)6 and ¥1.6 million ($193,000 US), respectively. However, afterexamining the methods used to derive these amounts, we had doubts aboutthe credibility of those figures.

6 In 1997, 1 US dollar 5 approximately 8.3 yuan (¥).

CP AUDIT DEMONSTRATION PROJECTS 577

TA

BL

E3.

Est

imat

edR

educ

tion

inC

hem

ical

Oxy

gen

Dem

and

(CO

D)

for

Hua

bei

and

Xin

hua

Dif

fere

nce

Act

ual

Tar

get

Bet

wee

nA

ctua

lW

aste

stre

amV

alue

Val

ueR

educ

tion

Red

ucti

onR

educ

tion

and

Fac

tory

Des

crip

tion

Var

iabl

eB

efor

eC

PA

fter

CP

(%)

(%)

Tar

get

(%)

Hua

bei

Hig

hco

ncen

trat

ion

CO

DC

OD

conc

entr

atio

n(m

g/L

)24

,800

16,3

0034

21

32

Xin

hua

Hig

hco

ncen

trat

ion

CO

DT

ons

CO

D/y

ear

1,20

090

025

292

4

Sour

ces:

Hua

bei

Pha

rmac

euti

cal

Fac

tory

(199

6)an

dX

inhu

aP

harm

aceu

tica

lF

acto

ry(1

996)

.C

P5

clea

ner

prod

ucti

on.5

55

No

targ

etse

tfo

rth

isva

riab

le.

TA

BL

E4.

Est

imat

edR

educ

tion

inW

aste

wat

erG

ener

atio

nfo

rH

uabe

ian

dX

inhu

a

Was

tew

ater

Was

tew

ater

Dif

fere

nce

Gen

erat

edpe

rG

ener

ated

per

Act

ual

Tar

get

Bet

wee

nA

ctua

lW

aste

stre

amY

ear

Bef

ore

CP

Yea

rA

fter

CP

Red

ucti

onR

educ

tion

Red

ucti

onan

dF

acto

ryD

escr

ipti

on(t

ons/

year

)(t

ons/

year

)(%

)(%

)T

arge

t(%

)

Hua

bei

Hig

hco

ncen

tati

onC

OD

475

310

344

33

103

79

22

Low

conc

entr

atio

nC

OD

285

310

320

43

103

2810

118

Xin

hua

Hig

hco

ncen

trat

ion

CO

D13

63

103

110

310

319

181

1

Sour

ces:

Hua

bei

Pha

rmac

euti

cal

Fac

tory

(199

6)an

dX

inhu

aP

harm

aceu

tica

lF

acto

ry(1

996)

.C

P5

clea

ner

prod

ucti

on.

578 KATHERINE KAO CUSHING ET AL.

TABLE 5. Variables Used to Estimate Financial Benefits of CleanerProduction Options

Factory Variables Included in Estimates Calculation Data

Huabei 1. Decreased water consumption Cost of water 5 ¥1/ton2. Increased solvent production Solvent 5 ¥10,000/ton

Xinhua 1. Decreased consumption of raw material No details on calculation2. Decreased wastewater drainage expenses No details on calculation

Sources: Huabei Pharmaceutical Factory (1996) and Xinhua Pharmaceutical Factory (1996).

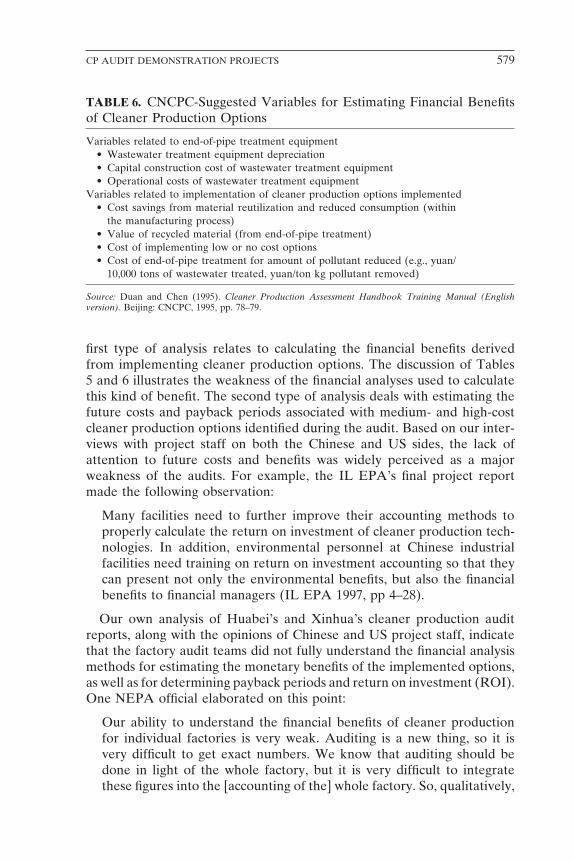

For example, the variables used by both Huabei and Xinhua to calculatefinancial benefits are clearly not as comprehensive as the variables that theCNCPC recommends using for evaluating the financial benefits of cleanerproduction. Table 5 shows that the Xinhua and Huabei used only twovariables (decreased water consumption and increased solvent productionfor Huabei) for estimating the monetary benefits of carrying out cleanerproduction options. This contrasts markedly with the more complete setof variables the CNCPC recommends using. As shown in Table 6, theCNCPC recommendations include a much more comprehensive set of vari-ables for estimating both savings related to reduced end-of-pipe treatmentcosts and savings resulting from reduced raw material consumption.

Interviews we conducted with US and Chinese project personnel revealedthat they were skeptical of the accuracy and reliability of financial benefitscalculated by the project staff at Xinhua and Huabei.7–11 At best, the financialbenefit analyses represent only a very general approximation of the projects’financial benefits. In the end, we concluded that although the cleaner pro-duction options implemented generated some financial gains to the factor-ies, the calculations of those benefits were not detailed enough to provideinsights into the significance of those gains.

Explaining Financial Analysis Results

Two reasons explain the apparent weakness in the case factories’ financialbenefit analyses. The first reason is that factory audit teams were inexperi-enced in the techniques and procedures used to determine monetary bene-fits. Implementing a cleaner production audit involves two types of financialanalysis, and both were completely new to the participating factories. The

7 Du, B. Illinois Environmental Protection Agency, Engineer. 1997. Interview by author, 8 September.Springfield, IL.

8 Mathur, B. Illinois Environmental Protection Agency, Air Bureau Chief. 1997. Interview by author, 9September. Springfield, IL.

9 Miner, B. Tetratech, EMI consultant. 1997. Interview by author, 5 September. Rolling Meadows, IL.10 Durley, S. Tetratech, EMI Consultant. 1997. Interview by author, 5 September. Rolling Meadows, IL.11 Zhou, Z. China National Cleaner Production Center, Senior Engineer. 1997. Interview by author, 9

June, Beijing.

CP AUDIT DEMONSTRATION PROJECTS 579

TABLE 6. CNCPC-Suggested Variables for Estimating Financial Benefitsof Cleaner Production Options

Variables related to end-of-pipe treatment equipment• Wastewater treatment equipment depreciation• Capital construction cost of wastewater treatment equipment• Operational costs of wastewater treatment equipment

Variables related to implementation of cleaner production options implemented• Cost savings from material reutilization and reduced consumption (within

the manufacturing process)• Value of recycled material (from end-of-pipe treatment)• Cost of implementing low or no cost options• Cost of end-of-pipe treatment for amount of pollutant reduced (e.g., yuan/

10,000 tons of wastewater treated, yuan/ton kg pollutant removed)

Source: Duan and Chen (1995). Cleaner Production Assessment Handbook Training Manual (Englishversion). Beijing: CNCPC, 1995, pp. 78–79.

first type of analysis relates to calculating the financial benefits derivedfrom implementing cleaner production options. The discussion of Tables5 and 6 illustrates the weakness of the financial analyses used to calculatethis kind of benefit. The second type of analysis deals with estimating thefuture costs and payback periods associated with medium- and high-costcleaner production options identified during the audit. Based on our inter-views with project staff on both the Chinese and US sides, the lack ofattention to future costs and benefits was widely perceived as a majorweakness of the audits. For example, the IL EPA’s final project reportmade the following observation:

Many facilities need to further improve their accounting methods toproperly calculate the return on investment of cleaner production tech-nologies. In addition, environmental personnel at Chinese industrialfacilities need training on return on investment accounting so that theycan present not only the environmental benefits, but also the financialbenefits to financial managers (IL EPA 1997, pp 4–28).

Our own analysis of Huabei’s and Xinhua’s cleaner production auditreports, along with the opinions of Chinese and US project staff, indicatethat the factory audit teams did not fully understand the financial analysismethods for estimating the monetary benefits of the implemented options,as well as for determining payback periods and return on investment (ROI).One NEPA official elaborated on this point:

Our ability to understand the financial benefits of cleaner productionfor individual factories is very weak. Auditing is a new thing, so it isvery difficult to get exact numbers. We know that auditing should bedone in light of the whole factory, but it is very difficult to integratethese figures into the [accounting of the] whole factory. So, qualitatively,

580 KATHERINE KAO CUSHING ET AL.

you can say the financial benefits are good, but quantitatively, you can’tsay anything very specific.12

Although the factory audit team members received some training onestimating financial benefits, payback periods, and ROI, it was only a smallpart of the overall project training. Because of their high level of technicalskills, the factory teams were able to do a good job carrying out aspectsof the audit related to manufacturing. However, because they were not asknowledgeable of the financial dimensions of cleaner production, they werenot able to conduct as thorough an analysis of the financial benefits of theimplemented options. Nor were the audit teams able to fully understandthe potential financial benefits of implementing higher cost options andeffectively “sell” them to upper factory management. This partially explainswhy neither of the case factories chose to implement any high-cost optionsand why Xinhua implemented only one medium-cost option.

The second reason why the audit teams’ financial benefit analyses wereincomplete is because project personnel were motivated to participate inthe demonstration project for reasons that were not centered on attainingthe monetary benefits of cleaner production. Although the idea of savingmoney for the factory played some role in motivating staff at the two casefactories to participate, other factors related to the international natureof the demonstration project were more crucial. Based on interviews weconducted with six key US and Chinese officials involved in the case factorydemonstration projects,7,9,10,12–14 the most important factors motivating casefactory personnel participation in the project were the high degree of statelevel oversight and involvement, the opportunity to learn about cleanerproduction and US technologies, the prestige associated with working onan international project, and the opportunity for factory staff to travel tothe US on a study tour.

State-Level Oversight

In China, attention from higher-level government organizations commandsrespect. National agencies such as NEPA (now SEPA) and SPAC aregovernment organizations at the highest level. The case factories involvedin the IL EPA-NEPA project were hand picked by NEPA and SPAC toparticipate in the project, and NEPA and SPAC representatives continuedtheir involvement throughout the duration of the projects. In addition,representatives from NEPA and SPAC attended all the IL EPA-NEPAproject’s workshops and seminars and kept abreast of the cleaner produc-tion projects’ progress.

12 Wang, J. National Environmental Protection Agency, Industrial Pollution Control Division, DeputyDivision Chief. 1997. Personal communication, 15 November.

13 Duan, N. China National Cleaner Production Center, Director. 1997. Personal communication, 16 No-vember.

14 Wise, P. Illinois Environmental Protection Agency, Associate Director. 1997. Personal communication,8 September.

CP AUDIT DEMONSTRATION PROJECTS 581

The influence of state-level oversight and involvement was cited by allsix interviewees as a primary motivating factor. One NEPA official ex-plained the importance of state-level participation in the following way.

This is a demonstration project, so the administration from NEPA,SPAC, and so on, is very strong. You know, SPAC’s Zhang Mingqi[the environmental protection manager for SPAC], personally called thefactory directors to tell them to participate. So they [the factory directors]think this is an issue of national significance, a national demonstrationproject, and that they were selected by the national government. . . .Also, the project was overseen by these agencies from the beginning ofthe project to its end. In China, leadership is very important (lingdaozhongshi). If it’s coming from the top, it’s important.12

One of the key IL EPA staff participating in the IL EPA-NEPA projectwas a Chinese-born engineer who was working for IL EPA during theproject. He often served as a translator and liaison between the US andChinese sides of the project. His comments also emphasize the importanceof high-level oversight.

For our project we involved national-level industry organizations. Thepolitical impact is so big, no one dare drop out. In China, everythingfrom the top is important. If they are doing something with NEPA orany national state-level organization, the factory directors like that.7

Learning Opportunities

Another important factor motivating case factory participation in the ILEPA-NEPA project was the opportunity to learn. Five of the six peopleinvolved in the IL EPA-NEPA project who we interviewed cited learningopportunities as an important motivating factor. The different types oflearning mentioned included learning about US cleaner production technol-ogy and implementation, learning how to reduce pollution, and learningabout ways to cut costs. The Chinese-born IL EPA staff person provideda perspective on this point:

The project gave them [the project participants] a lot. They got a lot oftechnical information for free. They also got to see and confirm if theirfactory was “on the same page” technologically, as the US.7

Two interviewees who worked on the Chinese side of the project specifi-cally mentioned learning about ways to cut costs as an important motivationfor factory participation. In fact, they cited this incentive as a very important,if not the most important, factor influencing participation.12,13

Prestige

The prestige associated with working on an international project was athird factor that motivated factory participation. Four of the six interviewees

582 KATHERINE KAO CUSHING ET AL.

posited that prestige was a strong incentive. The fact that the US, considereda technology leader, was sponsoring this cleaner production project piquedfactory management’s interest in participating. Being involved in an interna-tional project bestowed prestige on the participants, especially at loweradministrative levels in the factories, where interaction with foreigners canbe rare. The following comments from an IL EPA project participantillustrates this point.

IL EPA’s role is that of “boosting the atmosphere” of doing cleanerproduction in China. Having an international project helped market theproject, and gave it a good image to the participating industries. Bypartnering with the US government, NEPA was able to get the factoriesinterested in participating in cleaner production. . . . The US is consideredthe top level internationally, like a brand name. It represents the stateof the art. So even though all the training material was developed byNEPA, it means more to the participants if they think it comes fromthe US EPA or the World Bank.7

A high-level CNCPC official also had an opinion about how the interna-tional nature of the project affected the demonstration factories’ participation.

If we inform them that this is an international project, they pay moreattention to the project. In some provinces, some factories will pay muchattention to this. For example, if you are in a place where they don’tget a lot of foreigners, then, it makes a difference . . . in Shijiazhuang[where Huabei is located] they receive little exposure to foreigners.Where Xinhua is, Shandong, they get more than Shijiazhuang. I thinkbeing international played a big role in this project.13

The CNCPC official’s statement reiterates the importance of a high-profile international project in getting factories to pay more attention tocleaner production.

Travel

The final motivating factor cited by the majority of our interviewees was theopportunity to travel to the US on a study tour. Four of the six intervieweesconsidered this an important incentive. In July 1996, some factory personnelparticipating in the audit got the opportunity to go to the US. This travelopportunity was a major windfall for project participants. Due to the diffi-culty of obtaining a US visa and the substantial costs associated with airfare,food, and lodging in the US, it is often difficult for Chinese people to visitthe US on their own. Frequently, work provides their only chance. The ILEPA-NEPA project afforded personnel in the factories a rare internationaltravel opportunity. The following comments made by a CNCPC officialexplain the challenges Chinese nationals often face in traveling to the US.

CP AUDIT DEMONSTRATION PROJECTS 583

Two reasons prevent travel to the US. First, it requires a lot of money.This way [through the project], they can use project money, or theircompany’s money to pay for the trip. Second, the practice in China isthat it is easier to get a US visa for work purposes than for leisure. Itis possible to get a visa for leisure, but there are a lot of restrictions onthe US side. . . .

Going abroad for study tour was a very strong factor to get them [thefactory staff] to join [in the project]. Going to the US is a big deal. Someof the managers want to try new things, they are willing to see thingsfrom a new side, and they think this [study tour] is a good way to learn.Sometimes, for some of the projects, this gives them an opportunity tolearn about what is going on in the US. The better factory managerswant to do this. For Xinhua, especially I think this was the case.13

By participating in the IL EPA-NEPA project, case factory personnelwere able to overcome the financial and procedural obstacles that typicallymake travel to the US infeasible.

Discussion

An important implication of this research relates to the utility of usinghigh-profile demonstration projects as a means to promote the practiceof cleaner production. Of seven major multilateral and bilateral cleanerproduction projects conducted in China from 1994 to 1997, six have involveddemonstration projects. All together, these projects have funded at least59 cleaner production audit demonstration projects (NEPA and CNCPC1996). According to a NEPA official, the demonstration project hasemerged as the primary mechanism for promoting cleaner production auditsin China.12

Our research shows that although demonstration projects at the casefactories generated substantial environmental benefits, the financial benefitswere unclear, and the audit teams’ motivations to participate in the projectstemmed largely from the project’s international nature. That financial incen-tives at the factory level were not major motives driving participation in thecase factories suggests that the diffusion of cleaner production practices viademonstration projects on a larger scale may face significant challenges.

For cleaner production to spread effectively, sound financial analysesare needed to provide convincing evidence to the factories participating inthe demonstration project, as well as other factories in the same industry,that clear financial gains can be realized by adopting cleaner productionpractices. The monetary benefits of audit implementation in the case factor-ies’ analyses were unclear. This represents a crucial deficiency in the imple-mentation of the audits because it fails to demonstrate to the case factorypersonnel and staff at other factories in the industry that adopting cleanerproduction practices pays off. Without such proof, other factories will not

584 KATHERINE KAO CUSHING ET AL.

have incentives to adopt cleaner production independently, and staff at thedemonstration factories themselves will lack motivation to continue withtheir own cleaner production activities.

Lack of financial incentives for participating in cleaner production-relatedactivities is not universal in China. Some Chinese enterprises are quiteserious about reaping the monetary benefits of implementing cleaner pro-duction. For example, in the study by Warren (1996) of pollution preventionin Chinese electroplating factories, “lowering costs or improving benefits”was cited by all of her nine case factory managers as a criterion thatvery strongly influenced pollution prevention decisions.15 In Warren’s cases,cleaner production was implemented by the factories predominantly ontheir own initiative and often in a piecemeal fashion, as opposed to theformalized, top-down audit process used with our case factories. The differ-ence between our findings and Warren’s suggests that there are connectionsbetween the way in which a cleaner production project is initiated andimplemented (i.e., bottom-up and piecemail versus top-down using a formalaudit process) and the incentives of factory personnel to engage in cleanerproduction-related activities.

When cleaner production is promoted in China on a nationwide basis,most projects will not be funded by international or multilateral sources,and they will not have the same political, financial, technical, and humanresources associated with them as the demonstration projects at Huabeiand Xinhua. Unless there are clear incentives (financial or otherwise)16 andadequate financial analysis training for cleaner production, the Chinesegovernment’s efforts to diffuse the practice of cleaner production usingdemonstration projects will have limited results. Without incentives, factorymanagement will be unwilling to participate in cleaner production pro-grams. Without proper financial training, factory staff will be unable torecognize and act on the financial benefits of higher cost cleaner produc-tion options.

Demonstration projects can be a useful tool for transferring importantknowledge about cleaner production practices from developed countriesto China and other developing nations. The formalized audit process pro-vides a way to systematically and comprehensively identify a host of cleanerproduction options that benefit both the factory and the environment. Thecase studies analyzed here show how implementing demonstration projectsresulted in significant reductions in water pollution. However, these re-search findings also suggest that a wider consideration of the factors thatinfluence project personnel behavior—factors that go beyond the traditional

15 See Warren et al. (1999) for more details on these Chinese factories and see Higgins (1995), Sarokinet al. (1985), Clark (1995), and Welch (1997) for discussions of the financial incentives for implementingcleaner production in Western firms.

16 Warren (1996) shows that other incentives, such as winning environmental management competitions,also can be effective motivating factors that encourage factories to adopt cleaner production practices.

CP AUDIT DEMONSTRATION PROJECTS 585

direct benefits of cleaner production (e.g., saving money and improvingproduct quality)—is necessary to better understand why and how factoriesadopt cleaner production practices.

References

CNCPC (China National Cleaner Production Center). 1995. Cleaner ProductionAssessment Handbook: Training Manual (English version). N. Duan and W. Chen(eds). Beijing: CNCPC, July 1995.

Clark, J.H. (ed). 1995. Chemistry of Waste Minimization. New York: Blackie Aca-demic and Professional.

Cushing, K.K. 1998. Wastewater Treatment and Cleaner Production in the ChinesePharmaceutical Industry: How Institutions, Incentives, and Capabilities InfluenceOrganizational Behavior, PhD dissertation, Department of Civil and Environ-mental Engineering, Stanford University.

Duan, N. 1996. Presentation Given at the Cleaner Production China Project FinalWorkshop, 15 October 1996, Beijing.

Edmonds, R.L. 1994. Patterns of China’s Lost Harmony: A Survey of the Country’sEnvironmental Degradation and Protection. London: Routledge.

He, B. 1991. China on the Edge: The Crisis of Ecology and Development. SanFrancisco: China Books and Periodicals.

Higgins, T.E. 1995. Pollution Prevention Handbook. Boca Raton: Lewis Publishers.

Huabei Pharmaceutical Factory. 1996. Clean Production Audit Report. August1996, Shijiazhuang, PRC.

IL EPA (Illinois Environmental Protection Agency). 1997. International Diffusionof Pollution Prevention Technologies through Technical Outreach, Assessments,Demonstrations, and Evaluations of the Metal Finishing, Petrochemical, andPharmaceutical Industries in China. Prepared by Tetratech, EMI.

Ma, X. 1997. Controlling Industrial Water Pollution in China: Compliance in theContext of Economic Transition. PhD dissertation, Department of Civil andEnvironmental Engineering, Stanford University.

NEPA (National Environmental Protection Agency) and CNCPC. 1996. CleanerProduction in China: Challenge, Opportunity, Cooperation. Beijing: NEPA.

Sarokin, D.J., Muir, W.R., Miller, C.G., and Sperber, S.R. 1985. Cutting ChemicalWaste: What 29 Organic Chemical Plants are Doing to Reduce Hazardous Waste.New York: INFORM.

Shen, J. 1996. Rx for China’s Pharmaceutical Sector. China Business Review23(4):16–23.

Sinkule, B. 1993. Implementation of Industrial Water Pollution Control Policies inthe Pearl River Delta Region of China. Ph.D. dissertation, Stanford University.

Smil, V. 1993. China’s Environmental Crisis: An Inquiry into the Limits of NationalDevelopment. New York: ME Sharpe.

586 KATHERINE KAO CUSHING ET AL.

Song, J. 1993. Building a New Modern Industrial Civilization. A speech at theSecond Annual Working Conference on Industrial Pollution Prevention andControl (Beijing, October 1993) Zhongguo Huanjing Bao [China EnvironmentNews] November 2, 1993.

SSBC (State Statistical Bureau of the People’s Republic of China). 1996. ChinaStatistical Yearbook. Beijing: China Statistical Publishing House.

US EPA (United States Environmental Protection Agency). 1991. Risk ReductionEngineering Laboratory and Center for Environmental Research InformationOffice of Research and Development. 1991. Guides to Pollution Prevention: ThePharmaceutical Industry. Washington DC: US EPA, October 1991 (EPA/625/7-91/017).

US EPA. 1994. Environmental News. “EPA Administrator Announces Environ-mental Technology Initiative.” Department of Communications, Education, andPublic Affairs. January 27.

Warren, K. 1996. Going Green in China: Pollution Prevention Practices in ChineseElectroplating Factories. Ph.D. Dissertation, Department of Civil and Environ-mental Engineering, Stanford University.

Warren, K.A., Ortolano, L., and Rozelle, S. 1999. Pollution Prevention Incentivesand Responses in Chinese Firms. Environmental Impact Assessment Review19(5/6):521–540.

Welch, T. 1997. Moving Beyond Environmental Compliance: A Handbook for Inte-grating Pollution Prevention with ISO 14000. Boca Raton: CRC Press.

Wise, P. 1997. Associate Director, Illinois Environmental Protection Agency. Pre-sentation made at Doing Business in China Workshop. November 19, McDonald’sHamburger University, Oak Brook, IL.

World Bank. 1997. China 2020 China’s Environment in the New Century: ClearWater, Blue Skies. Washington DC: World Bank.

Xinhua Pharmaceutical Factory. 1996. Cleaner Production Audit Report. March1996, Zibo, PRC.

Recommended