BUSINESS BOOKKEEPING & ACCOUNTSModule One

CONTENTSThe Ledger - the Main Book of Accountpage 7Transactions; what is involvedThe functions of accounting:recording, analysing, presentingBookkeeping: the recording functionManual bookkeeping and computerised accountingMeanings of the terms:assets and liabilitiesdebtors and creditorsincome and expenditurecapitalprofit and lossInformation recorded in/provided by the ledgerLedger accounts described:what their debit and credit sides recordrules concerning ledger accountsThe need for double-entry bookkeeping:the receiving and giving aspects of every transactionThe basic rule of double-entry bookkeepingAbbreviations used in ledger accountsEntries in a ledger account examined and explainedBalancing ledger accounts:debit and credit balancesFoliosClasses of ledger accounts:real, personal and nominal:what they recordrules for posting to themspecimens of each examinedSpecial notes on ledger accountsSpecial notes on balancing ledger accounts

THE LEDGER -THE MAIN ‘BOOK OF ACCOUNT’

IntroductionIn business, “guesswork” is simply not good enough! The owners or managements of everybusiness needs accurate and up to date informationabout the activities of their business. Thatinformation can come only from records kept abouteach and every‘transaction’which occurs.In the context of accounting, a‘transaction’is any activity which involves the exchangeof moneyor money’s worth between a business and others, be they people or organizations. A transactionmight involve a purchase or a sale, the receipt or the payment of money, the circulation of assets(possessions), the settlement of a debt, or anything else which has a‘monetary value’.The main functions of the process called accountingare:)Recordingthe financial transactions which affect an ‘enterprise’(which might range from a smallone-man business to a huge public company).)Analysingthe transactions recorded.)Presentingthe records of the transactions - usually in a “summarised” format - in variousstatements which should show clearly the effectsof those transactions on the performance andfinancial position of the enterprise.

The recording function of accounting is calledbookkeeping.The purpose of bookkeeping is toprovide an accurate and detailed record of each andeverytransaction involving the exchange ofmoney or money’s worth between a business and other parties, whether those are individuals ororganizations.Those records might be made “manually” (by hand) in actual books or - in large organizations -in numerous cards or sheets, which collectively can still be thought of as comprising very large books.Some enterprises make use of mechanised accounting machines to make‘entries’in their records,whilst the modern method is increasingly towards the use of computers to maintain bookkeepingrecords.Howsoever bookkeeping records are maintained, it is essential that they are always accurate, thatthey can be crosschecked when necessary, and that they are readily available when needed.Although computers might have many advantages over traditional manual bookkeeping - which isstill very widely practised - they still perform ‘bookkeeping’according to the same basic rules. Inthis Program we shall therefore first study the principles of manual bookkeeping, and relate them laterto computerised systems.Terms Used in Bookkeeping and Accounts

Before you start studying bookkeeping, it is important that you clearly understand the specialisedmeanings of certain words and terms commonly used in bookkeeping and accounting. At this stage,you should learn thoroughly the following explanations to ensure that your progress in further stagesof the Program will be rapid and easy. Any “skipping” through the explanations or an “I know it already”8BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukattitude at this stage, can lead to misunderstanding or difficulty in your learning other topics whichwill be taught as you progress through this Program.EAssetsThese are the possessionsof an enterprise, that is, what it owns. Assets include actual cash(currency notes and coins) and money in bank accounts; investments and, depending on the type

and size of an enterprise, land and buildings; plant, equipment and machinery; furniture; stocks ofgoods for sale and/or stocks of materials to be utilised in manufacturing goods; and anything elseowned by the enterprise which has monetary value, including moneyowed to itby individuals andother enterprises, and often called‘book debts’.What are called ‘fixed assets’are items which an enterprise “acquires” (by renting, leasing orpurchasing) in order to be able to carry out its activities. They are usually acquired with the intentionof their being retained for some time, perhaps many years. The variety of such items is great and,depending on the type and size of a particular enterprise, might range from desks and chairs,computers and other office equipment, to factory buildings, machinery and plant, motor vehicles, etc;in fact, any material item large or small in size or value which assiststhe enterprise to run efficientlyand profitably. In some countries fixed assets are called ‘working assets’ because they enable theenterprise to perform its “work”.All other assets of an enterprise are called‘current assets’, and their total value is constantlychanging or fluctuating with the day to day operations of the enterprise. Current assets include stocksof goods and/or raw materials, cash and bank balances, debts owing to the enterprise, etc, whosetotal values change daily as purchases and sales are made, as bills are paid and as customers paytheir debts.ELiabilities

These are any sums, measured in monetary value, which an enterprise owes to others, that is,they are the debtsof the enterprise. Liabilities might include the values of goods, materials or servicesprovided by suppliers but not yet paid for; or goods, materials or services paid for by customers butnot yet provided to them; as well as bank overdrafts, and loans made to the enterprise by banks andother financial institutions, etc.EDebtorsThese are people and organizations whoowe money or money’s worth tothe enterprise.Debtors are mainly customers who have been supplied with goods or services ‘on credit’, that is,without having had to pay for them at the time of sale. But they can also be those to whom theenterprise has loaned money and those who have been “paid in advance” for goods or services notyet provided (e.g. insurance cover is usually paid in advance for a whole year).Those who incur debts to a business as the result of its normal business activities are commonlycalled its ‘trade debtors’. As mentioned earlier, debts owing toan enterprise are assets; and sumsowed by trade debtors (book debts) are therefore classed as current assets.

ECreditorsThese are people and organizations to whom an enterprise owes money or money’s worth.Creditors might be suppliers who have supplied goods, materials or services on credit, that is, withoutdemanding payment at the time of supply, or might be people or organizations who have “paid in9BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukadvance” (e.g. rent paid in advance to a landlord); both groups of whom are commonly referred toas ‘trade creditors’.Other creditors might be banks or other financial institutions which have loaned money to theenterprise, or banks which have permitted the enterprise to‘overdraw’its current account (a matterwhich is dealt with fully in Module 10). As we have already stated, all sums owed to creditors areliabilities

of an enterprise.ECapitalThis is an essential prerequisite of any business enterprise; whatever its intended or eventual sizeit will requireinitial capitalto enable it to commence its operations. Initial capital requirements will,of course, vary considerably, but moneywill be needed to acquire the necessary fixed assets as wellas the relevant current assets - stocks of raw materials and/or goods for sale.Sufficient capital - called ‘working capital’- will also be required to ‘finance’the enterprise, thatis, to meet all the expenses which will be incurred (e.g. rent, salaries, electricity, advertising, and manyothers) until sufficient income from initial production and/or sales is generated.The amount of an enterprise’s working capital at any point in time is the total value of its currentassets less the total value of its current liabilities.EEEEEIncome and ExpenditureThe term ‘income’refers to all the money, in whatever form, receivedby an enterprise; whilst‘expenditure’ is all the money, in whatever form, paid out

by the enterprise to enable it to keeprunning - itsexpenses.ProfitEnterprises - which in the private sector are often called‘businesses’- are started and run to makeprofits or gains for their owners. Any person involved with bookkeeping and accounting needs toknow what profit is and how it arises. A simple example will help to make the concept clear:A shoemaker sells a pair of shoes he has made, and with the money he receives for it hebuys food or clothing or buys materials or pays the rent of his workshop. What he has doneis to exchangehis materials and labour for the materials and labour of other people; what wecall ‘money’is only the mediumwhich makes the exchange easier. In order to produce hisshoes, the shoemaker has to make use of three items: land, labour, and capital, which are calledthe ‘factors of production’.Withoutland there would be no place or workshop for the shoemaker to work.Without hislabourno shoes would be made.Withoutcapitalthere would not be the money which he needs to pay the rent of his workshop,

to buy leather, tools, nails, etc, from which to produce more shoes, and to feed and clothehimself until the next shoes are made and sold.The shoemaker must be sure in advance that his production will bring back the money he spenton materials, on labour, and on rent and bring a ‘return’on the capital employed; and it is thatreturnorgainwhich is called profit.10BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukPut simply, we can see that capital is really the result of previous production; if the shoemakerworks so well that he sells his products for more money than his immediate needs, he can use thatextra money as capital to finance more production. We return to the consideration of profit in Module8, but at this stage it should be noted that the opposite of making a profit is incurring a

loss.The LedgerThe books which are the subject of bookkeeping are referred to as the ‘books of account’.Themain book of account is theledger. In a summarised form the ledger records - and can provide -all the following information:-*The total income of the business, and in general the different sources from which it is derived.*The amounts involved in meeting each type of expense, and the total expenditure incurred by thebusiness.*What assets are owned by the business, the values of each general type and the total value ofall its assets.*The values of the different liabilities of the business, and the total value of all its liabilities.*Who its debtors are, how much they owe to the business, and the total amount owed to thebusiness.*Who the creditors of the business are, how much is owed to each by the business, and the totalamount owed by the business.*Whether the business has made a profit or a loss during a given period of time, and the amountof that profit or loss.*The amount of working capital available to the business at any point in time.Ledger Accounts

A ledger comprises many different sections, each of which is called an ‘account’.In a ledger“book”, there will usually be one account on each page of it; in a large business each account mighthave its own card or sheet - all the account-cards or account-sheets together jointly make up thebusiness’ ledger. The following important points must be noted about ledger accounts:-+Eachindividual account is headed by anameor by atitle. That name or title may be the nameof a person or an organization or a type of asset, a type of liability, a type of expense or a sourceof income.+Onlyinformation about transactions concerning the person, organization or item named at its headmay be recorded in that account.+Each account must be keptseparate, or treated separately, from all the other accounts in theledger, and there must be only oneaccount in the ledger for any one particular person,organisation or item.+In addition to a name or title, each account also has a number allocated to it; that number is calledafolioor an account number

. (The uses and values of folios or account numbers will bedescribed shortly).11BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.uk+Each ledger account is divided into two parts, often called ‘sides’, by a line - or by two closeparallel lines - drawn down the middle of it, from top to bottom.+The left-hand side of an account is called its ‘debit’side, and it records all values receivedby theperson, organization or item named at the top, or “head”, of it.+The right-hand side of an account is called its ‘credit’ side, and it records all values given(or paid)

out by the person, organization or item named at its head.Note:Accounts are also used in computerised boookkeeping or accounting systems, and they alsorecord the “giving” and “receiving” aspects. However, the two parts of each account might not beso obvious in a computerised system as in manual systems, and might not be “side by side” as theyare likely to be in a ledger kept manually. For convenience we shall use the description “sides”.Practical ExampleAs we stated earlier, bookkeeping and ledgers (in one form or another) are used by businessesof all types and sizes. However, for the purpose of learning, it is easier to examine a small businesswhich has relatively few transactions - and which therefore needs to make relatively few‘entries’in its books of account - than it is to examine a very large business; although, of course, the principlesapplied will be the same in both cases, and it is only the “scale” which differs.For the purpose of this Program we first consider the bookkeeping required by a business called“Market Grocers”, which is owned and run by Mr A Trader.Mr Trader’s business deals in groceries; some it sells on ‘wholesale’terms, that is, in bulk or infairly large quantities, to other organizations, such as restaurants, hotels, and small kiosks. Othergoods are sold ‘retail’or “across the counter” to people who come into the shop/store from whichthe business operates.The business rents its shop/store, and the storehouse it needs to hold stocks of goods (groceriesin this case) which it hopes to sell. Mr Trader has a storeman/delivery-man, two shop assistants anda clerk to assist him in running the business.The business buys the goods which it intends to sell from the manufacturers and producers of them.

The business owns various assets, such as shop furniture and equipment: counters, cash registers,shelving, etc, storage equipment: racks, shelving, etc, office furniture and equipment: desks, chairs,an adding machine, filing cabinet, etc, and a delivery van.An accurate record of each and every transaction which involves the exchange of money oranything worth money between the business and any other person or organization mustbe recorded- in a summarised format at least - in its ledger.Depending in particular on the number of customers to whom Mr Trader sells goods ‘on credit’,that is, without requiring them to pay for those goods at once, and on the numbers of suppliers whoallow him to purchase goods from them‘on credit’,that is, without requiring him to pay for thosegoods at once (sales and purchases on credit are dealt with in Module 3), there will have to be anumber of different accounts in the ledger of the business. For example, there will be an accountheaded “sales”,which will record the values of all sales made to customers, so that Mr Trader willalways be able to find out the total value of sales made. There will also be an account headed“purchases”, in which will be recorded the values of all goods purchased (bought) by the business,and which will be able to show the total value of all purchases made.12BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:

International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukThere will also be an account headed by the name of each general type of asset owned, forexample, “shop furniture & equipment”, “office furniture & equipment”, “delivery van”, “stocks of goods”,and so on. Similarly there will be an account for each type of expense incurred by the business, whichmight include: “rent”, “salaries”, “advertising”, “stationery”, “postage”, “telephone”, “electricity”, “vanrunning expenses”, and so on.Finally, there will need to be an account for each debtor who owes money to the business, for goodssold to them on credit and not yet paid for. And also an account for each creditor to whom the businessowes money. Mainly creditors will be suppliers from whom the business has purchased goods oncredit and who have not yet been paid for those goods, but if, for example, the business has beenmade a loan by a bank or by some other organization or person, an account for each such debt orliability will also be required in the ledger. One such account will be headed“A Trader capital”,andwill record the amount of money which Mr Trader has “invested” in the business and which, in effect,

it owes to him (this concept is dealt with in detail in Module 4).Now study Fig.1/1 carefully and note in particular its layout. The reason why each entry has beenmade in the account, that is, the “interpretation” of the information it contains, will be explained shortly.Note: These Manuals are studied in some 200 countries around the world. Therefore, we do notuse the “name” of the currency or money of a particular country against the amount or values oftransactions. We call them simply “units” (of money). You may read the word “units” as being thename of the currency in use in your own country, e.g. pounds or dollars or francs or naira or kwachaor ryal or shillings or dinar or rupee, or any other, or as being the name of a currency with which youare familiar. Similarly, although we may use the symbol £against some amounts of money, you shouldregard the symbol£as referring to the currency with which you are familiar.Fig.1/1. a specimen ledger account13BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email:

[email protected] Website: www.cambridgecollege.co.uk

Double-Entry BookkeepingEach ledger account needs two “sides” or parts because in everybusiness transaction whichoccurs - no matter how large or small in value it may be - twothings happen at the same time:-One party receives value, whilst at the very same timeanother party gives out that very same value.For example, when a business sells goods and receives the payment for them at once - called a‘cash sale’- it has given out goods but at the same time it has received moneyin exchange for them.Likewise, the customer has given out money, but at the same time he or she has received goods inexchangefor that money.The same happens in everybusiness transaction, and therefore in order to record the “dual” or“double” aspect, TWO entriesare required somewhere in the ledger for each and every transactionthat occurs. The two entries must be:-)One on the creditside of an account - to record the ‘giving’aspect;

and)One on thedebitside of an account to record the ‘receiving’aspect.The method used to record the double aspect of each transaction is, logically, called ‘double-entrybookkeeping’. It is vital to remember always the basicrule of double-entry bookkeeping, which is:-“There must be a debit entry and a corresponding credit entry ofthe same value (and vice versa) for every transaction that occurs.”It is worth your noting at this stage that if there is both a debit and an equal (corresponding) creditentrysomewhere in the ledger for each and every transaction that takes place, the total of all thedebit entries in the ledger should agreeexactly with the total of all the credit entries.Information - or entries - is rarely recorded direct into the ledger accounts. Generally informationis first recorded in one of the ‘subsidiarybooks’ or ‘day books’- which are collectively often called‘the books of

original entry’.The information is then transferred - or ‘posted’, as the process iscalled in bookkeeping - to the appropriate ledger accounts in a summarised form.The most commonly used subsidiary books are the cash book, the sales book, the purchases bookand the returns inwards and outwards books, which we describe in detail in Module 2 and 3.Before we turn to an examination of the specimen ledger account illustrated in Fig.1/1. First notethe meanings of the following ‘abbreviations’(shortened words or terms) used in the specimenaccount, and which will frequently be met with in bookkeeping and accounting:-c/f is the abbreviation for‘carried forward’ and means that the figure, total or balance against whichit appears has been transferred to another place, for example from the bottom of one page to thetop of another, or from one book or account to another.b/fis the abbreviation which stands for ‘brought forward’and means that the figure, total or balancealongside which it appears was transferred from another place, e.g. to the top of one page fromthe bottom of another, or to one book or account from another.14BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain

International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukc/dis the abbreviation for ‘carried down’ and indicates that the balance alongside which it is writtenhas been transferred to a lower position on the same page.b/d is the abbreviation which stands for‘brought down’and means that the balance against whichit is written has been transferred from a higher position on the same page.bal is the common abbreviation for the word‘balance’,which is the difference between the total valueof the debit entries in an account and the total value of the credit entries in it.Interpreting the EntriesNow look again carefully at the ledger account shown in Fig.1/1. The account appears on page93 of Market Grocers’ ledger, and is headed “Clarendon Hotel Ltd”.It is, in fact, the account for oneof Mr Trader’s customers who buys goods from him fairly frequently on credit.As the account is in the name of “Clarendon”,it shows the position of transactions from the viewof that customer, and not

from the view of the seller or vendor, in this case, Market Grocers. Withthat in mind, we can “read” the account as giving, in date order, the following information:-May 2 The entry is on the debit side of the account which means that Clarendonreceivedvalue;in fact the customer purchased goods on credit (without paying for them at once,remember) worth 474.60 units. From Market’s point of view the goods were given out, andthat aspect of the transaction will be recorded in a different account, as you will see whenwe study Module 3.May 4 The entry is on the credit side, so therefore Clarendongave outvalue; the word “returns”included in the entry tells us that Clarendonreturned toMarket Grocers goods worth 14 units- perhaps they were the wrong type or size or brand, or were damaged or substandard -whatever the reason, they were not wanted and so were returned. The effect of the return,and the recorded entry of it in the account, is to reduceClarendon’sdebt to Market Grocersfrom 474.60 units to 460.60 units.May 8 A debit entry recording a credit purchase of goods byClarendon - whom, you will appreciateby now, receivedthe goods.May 12

Another debit entry, which records a further credit purchase by Clarendon, this time of goodsworth 162.50 units.May 14 A debit entry for a fourth credit purchase, and receipt, of goods by Clarendon,valued at296.20 units.May 15 A credit entry showing at once that Clarendongave outvalue; the description “payment”tells us that Clarendonpaid the sum of 800 units to Market.A quick calculation tells us,further, that the payment covered the values of the credit purchases of May 2 and May 8less the value of the returns made on May 4. The payment can be said to have been made‘on account’ because it did not settle the total amount owing byClarendon at the date itwas made (or at least on the date on which it was received byMarket).15BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.

Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukBalancing a Ledger AccountAfter making the entry for the payment received from Clarendonon May 15, Mr Trader neededto know how much was still owed to his business by Clarendon.To obtain that information, he carriedout a process called ‘balancing’. This is what he did, step by step:-Step 1He added up the values of the entries on the debit side of Clarendon’saccount in the ledger;their total amounted to 1,272.70 units, and he wrote that total below the fourth entry -remember that Fig.1/1 shows an “historical” record, and that on May 15 the other entriesshown in the account had not yetbeen made.Step 2He added up the values of the entries on the credit side of the account - their total, whichwas 814 units, was deductedor subtractedfrom 1,272.70 units to give the balance- theamount still owing by Clarendon- of 458.70 units.Step 3That amount was entered on the credit side, making the totals of the entries on both sides

equal. The total was entered on the credit side, on the sameline as the total of the debitentries; and both - equal - totals were neatly underlined, or ‘ruled off’as the process is called.Step 4The balance was carried down from the credit side to the debit side, showing that Clarendonhad received an excess value of 458.70 units over what it had given out.Balancing is an easy process and can be carried out on any account at any time that it is considerednecessary to do so. It is generally carried out on the accounts of all debtors and creditors at the endof each month. It is also done for allaccounts at the end of a “financial year” or “trading year” or otheraccounting period, and you will learn in Module 4 the reasons why that is done.Let us now return to an examination of the other entries in the ledger account:-May 25 A debit entry recording a credit purchase by Clarendon of goods worth 113.40 units.May 27 A credit entry recording the return of goods worth 21 units from Clarendonto Market-remember, the account is credited with the value of the return because it was given out byClarendon.May 31 It is customary for a business to send each credit customer a statement - called a ‘statementof account’- at the end of each month, stating the values of the goods purchased by the

customer during the month, the values of any payments received from the customer duringthe month, and the values of any returns of goods made by the customer during the monthand - most importantly - the balance still owing by the customer on the last day of the month.Mr. Trader therefore balanced Clarendon’s account again on May 31 and the balancecalculated (458.70 plus 113.40 less 21 = 551.10 units) was brought down to the start of thenext month.Note that the entries above the last “ruling off” are ignored when balancing the next timebecause, of course, the balance between their totals (if there is one, as was the case withClarendon) has already been carried down and is included in the next totalling.You can therefore see that a ledger account, even one like that illustrated in Fig.1/1 which containsonly a few entries, can give a great deal of information. In this and succeeding Modules you will beshown many other ledger accounts, and will be given information about them and the ways in whichthey differ from the one we have so far illustrated; balancing will also be considered further.16BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain

International Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukThe Folio ColumnThe narrow column to the left of the value column on each side of the account is called the‘foliocolumn’, and it contains a reference which tells us from where the entry was posted, i.e. its source,or where the corresponding entry - to complete the double-entry for the transaction - will be found.We explain fully the importance of folios and their value in Module 2.Classes of Ledger AccountsAll the many accounts which jointly make up the ledger of a business can be divided into threeclasses, which are as follows:-)Real AccountsThese contain the records of all the “physical” or “tangible” assets of the business, for example, shopfurniture, stocks of goods, delivery van, etc.)Personal AccountsThese are usually in the names of people or organizations, and they maintain records of (a) thetransactions which a business has with its credit customers, showing the amounts still owed to thebusiness by any of them; whilst (b) other personal accounts record the transactions which the businesshas with suppliers from whom it purchases goods on credit, and they will show to which creditors thebusiness still owes money, and how much is owed to each.)Nominal AccountsThese keep the records of all the different types of income (sometimes called‘revenue’) of the

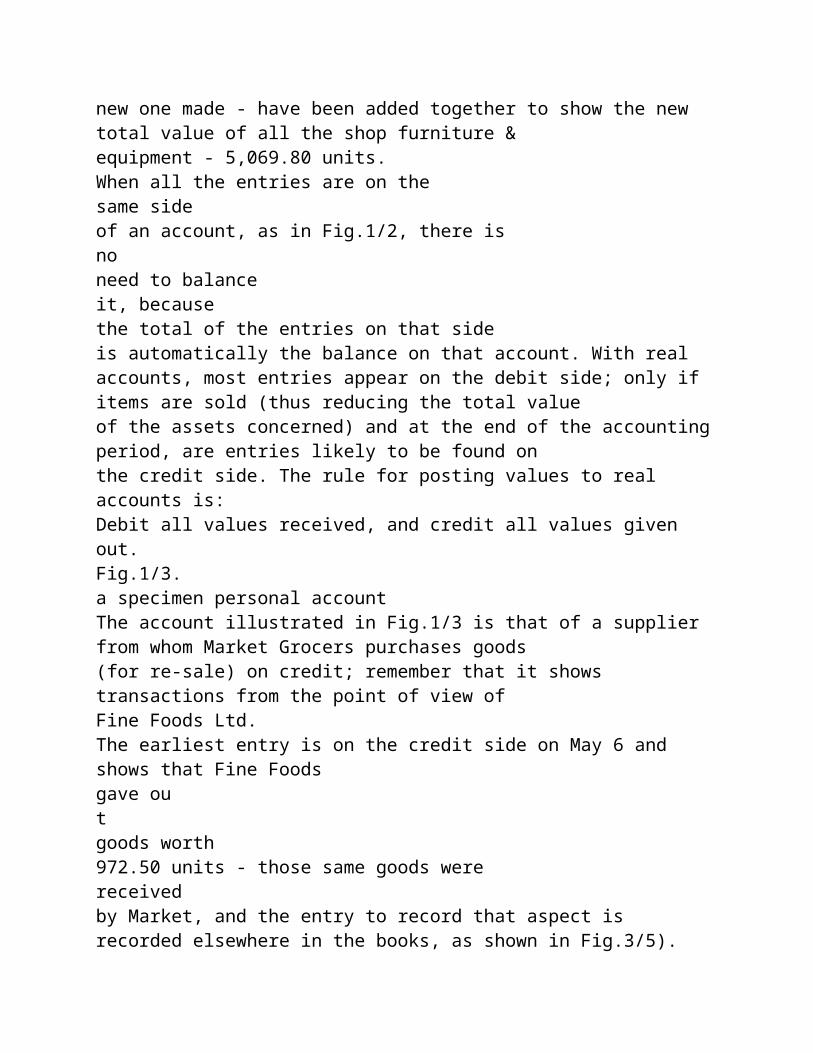

business, and also the records of the different types of expenditure incurred by the business in carryingout its activities.Now let us look at a specimen of each class of account: -Fig.1/2. a specimen real accountThe account shown in Fig.1/2 records the values of the different items owned by Market Grocerswhich together are classified as “shop furniture & equipment”;there might be many different items,but as they are all used in helping the shop to run efficiently, the records of them are kept togetherin one account instead of having a separate account for each type of item. You will appreciate thatthey are all fixed or working assets.17BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukThe first entry in the account is the balance, or total value, of shop furniture and equipment “broughtforward”, from an earlier page, perhaps page 11 in the ledger. The second entry, being on the debit

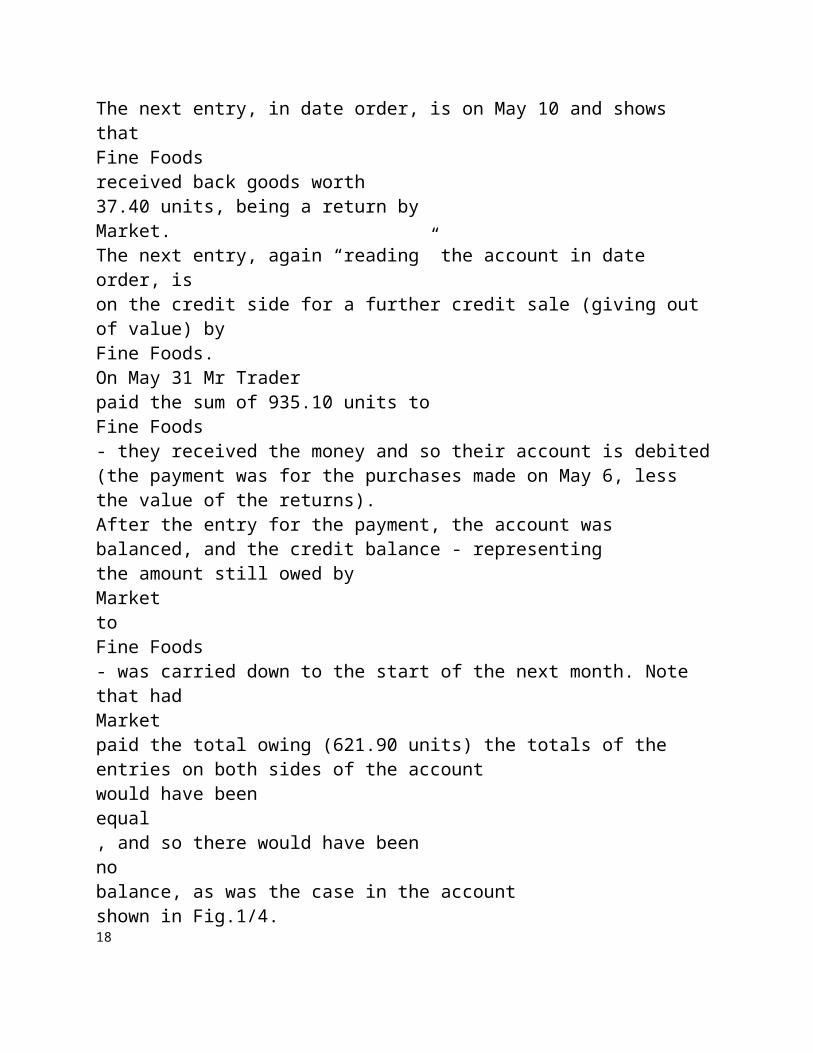

side, shows a receipt of value by the account; that is, a new set of scales was purchased for use inthe shop, and so the total value of shop furniture & equipment is increased. (At the same time, moneywas given out to pay for the scales, and the credit entry to record that giving aspect is recordedelsewhere in the books - see Fig.2/1). The two values - that of the “opening” entry and that of thenew one made - have been added together to show the new total value of all the shop furniture &equipment - 5,069.80 units.When all the entries are on the same sideof an account, as in Fig.1/2, there is no need to balanceit, becausethe total of the entries on that sideis automatically the balance on that account. With realaccounts, most entries appear on the debit side; only if items are sold (thus reducing the total valueof the assets concerned) and at the end of the accounting period, are entries likely to be found onthe credit side. The rule for posting values to real accounts is:Debit all values received, and credit all values given out.Fig.1/3. a specimen personal accountThe account illustrated in Fig.1/3 is that of a supplier from whom Market Grocers purchases goods(for re-sale) on credit; remember that it shows transactions from the point of view of Fine Foods Ltd.The earliest entry is on the credit side on May 6 and shows that Fine Foods gave out goods worth972.50 units - those same goods werereceived by Market, and the entry to record that aspect isrecorded elsewhere in the books, as shown in Fig.3/5).The next entry, in date order, is on May 10 and shows that

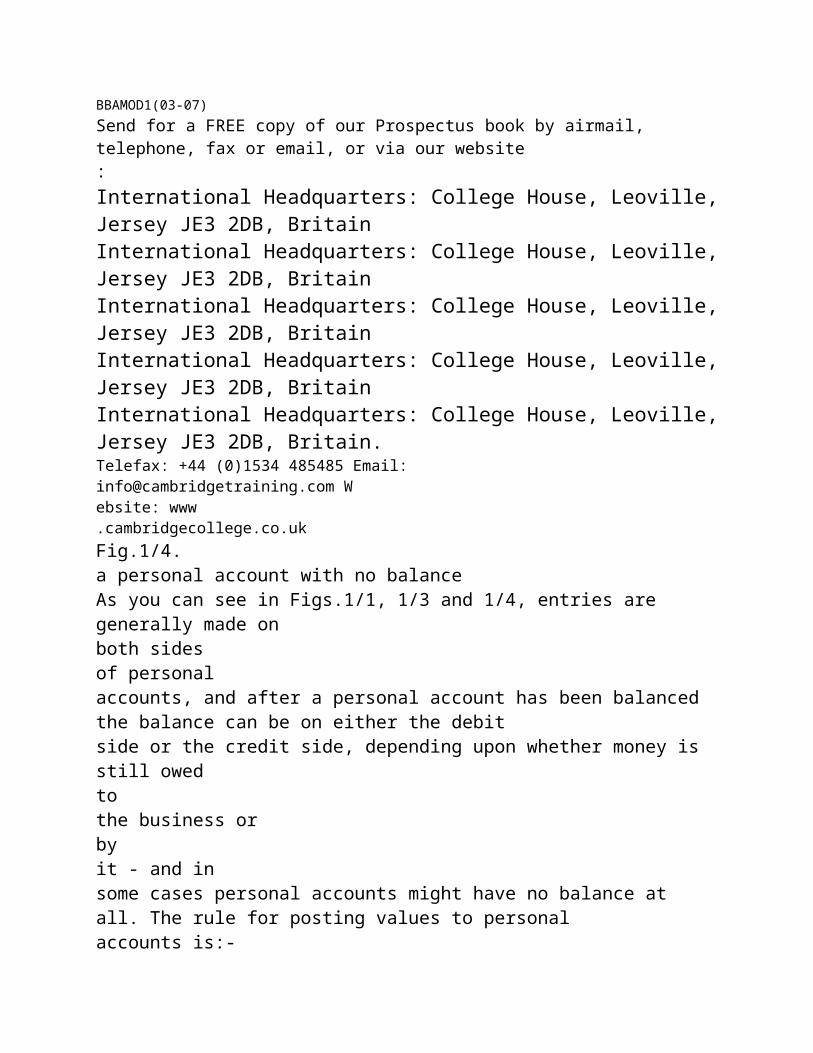

Fine Foods received back goods worth37.40 units, being a return byMarket.The next entry, again “reading” the account in date order, ison the credit side for a further credit sale (giving out of value) by Fine Foods.On May 31 Mr Traderpaid the sum of 935.10 units to Fine Foods- they received the money and so their account is debited(the payment was for the purchases made on May 6, less the value of the returns).After the entry for the payment, the account was balanced, and the credit balance - representingthe amount still owed byMarketto Fine Foods- was carried down to the start of the next month. Notethat had Marketpaid the total owing (621.90 units) the totals of the entries on both sides of the accountwould have been equal, and so there would have beennobalance, as was the case in the accountshown in Fig.1/4.18BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain

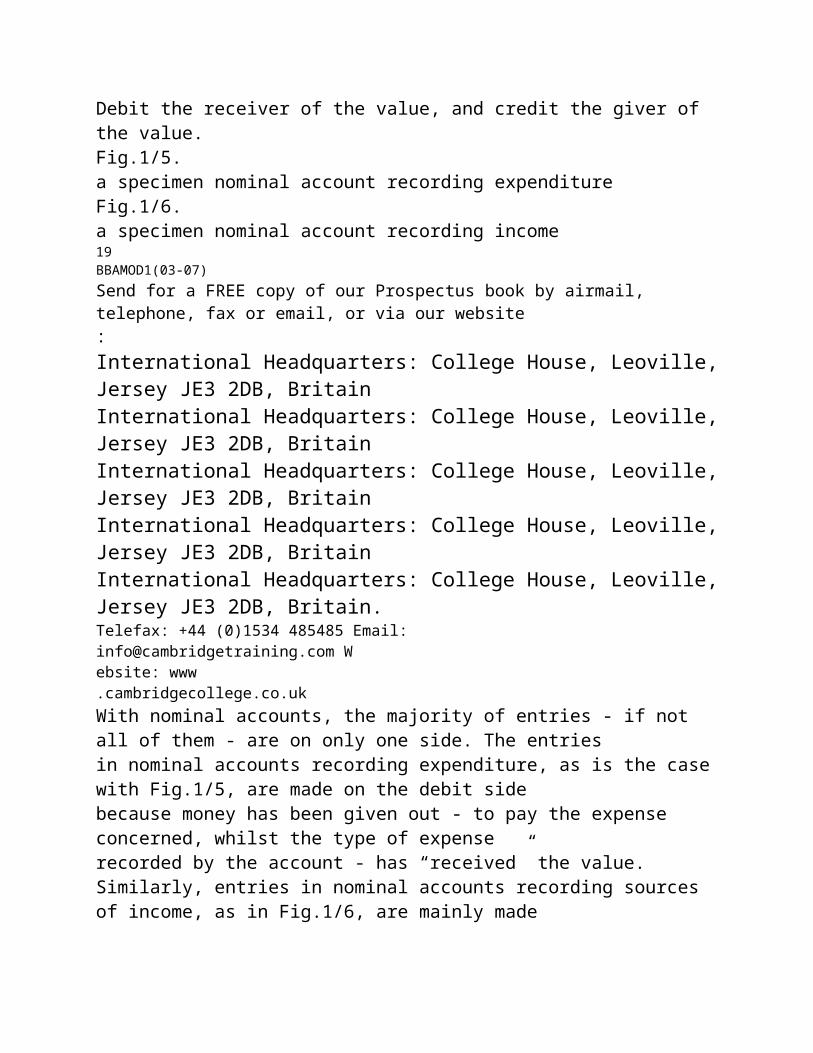

International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukFig.1/4. a personal account with no balanceAs you can see in Figs.1/1, 1/3 and 1/4, entries are generally made on both sidesof personalaccounts, and after a personal account has been balanced the balance can be on either the debitside or the credit side, depending upon whether money is still owed tothe business orbyit - and insome cases personal accounts might have no balance at all. The rule for posting values to personalaccounts is:-Debit the receiver of the value, and credit the giver of the value.Fig.1/5. a specimen nominal account recording expenditureFig.1/6. a specimen nominal account recording income19BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain

International Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukWith nominal accounts, the majority of entries - if not all of them - are on only one side. The entriesin nominal accounts recording expenditure, as is the case with Fig.1/5, are made on the debit sidebecause money has been given out - to pay the expense concerned, whilst the type of expenserecorded by the account - has “received” the value.Similarly, entries in nominal accounts recording sources of income, as in Fig.1/6, are mainly madeon their credit side, because although money has, or will, be received in exchange for the items sold,the accounts record the “giving” aspect of the transactions concerned. This matter will become quiteclear when we consider the cash book and other books of original entry in Modules 2 and 3.The rule for posting to nominal accounts is:-Debit the values of all expenses and losses,and credit the values of all gains.The “balance” on an account is the differencebetween the total value of the entries on its debitside, and the total value of the entries on its credit side. If the total of the debit entries is the larger- as is the case with the accounts shown in Figs.1/1, 1/2 and 1/5 - the account concerned is said tohave a ‘debitbalance’. If, on the other hand, the total value of the credit entries is the larger - asis the case with the accounts in Figs.1/3 and 1/6 - the account concerned is said to have a ‘creditbalance’. It is most important to bear those facts firmly in mind.

Special Notes:EIn some cases the word “debit” might be abbreviated to “DR”, and the word “credit” might beabbreviated to “CR”. These abbreviations should not be used in “written” or “worked” answersto Test or Examination Questions.EThe word “credit” as used in bookkeeping and accounts has two different meanings:1. It is the name of the right-hand side/receiving part of a ledger account.2. It means that goods or services have been sold or purchased without payment having beenmade at the time of the sale/purchase.It is most important that you do notconfuse two different meanings of the same word. Always readthe word carefully in the ‘context’ (its relationship with other words in the sentence) in which it isused.ETraditionally the description of each entry on the debit side of a ledger account had to be startedwith the word “to”, and the description of each transaction on the credit side of a ledger accounthad to be started with the word “by”. Some examining bodies might still require that that is done,but the busy bookkeeper rarely has the time in practice for such “niceties” which, in any case,contribute nothing to the accuracy or meanings of entries.EIn practice, some accounts might contain very many more entries than we have shown in ourexamples. Nevertheless, whether an account contains one entry or hundreds, it mustconformto the rules of double-entry bookkeeping we have so far taught you, and which will be taught in

subsequent Modules of this Manual. And the same applies whether bookkeeping is carried outmanually or by computer.20BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.ukEALL entries in ledger accounts - and indeed in all books of account - must always be madeneatly and accurately. Any untidy, unclear, careless or inaccurate entries will lead to errors, andit can be very time-wasting to trace, and correct, errors. Carelessness and inaccuracy can, further,lead to losses for a business and even - in extreme cases - to the loss of the job of the personresponsible. Accuracy is just as important when making entries in - or ‘inputting’to - acomputerised accounting system. So ALWAYS be accurate in your bookkeeping work, be neat- and take

pride in your work and your profession.Additional Notes on Balancing Ledger AccountsCommit the following points to memory, as they will help you avoid making errors in balancingaccounts manually.As soon as both sides of an account are equal in total value it should be neatly ‘ruled off’. If thereis only one entryon each side of the account (equal in value) then theruling off lines shouldbe drawn below the entry on each side of the account; there is no need to write the total again (seeFig.1/4). However, if there is more than one entryon either side of the account, the values of those entriesshould be totalled, the same total should be written on each side of the account, and ruling offlines should be ruled below those equal totals (see Fig.1/7).If there is only one entry in an account, there is no need to balance that account, because thevalue of that one entry is the balance;do not rule off the account.If

all entriesin an account are on the same sideof it, the total valueof those entries is thebalanceon that account,and so there is no need to balance it; the total value of the entries maybe written in, but the account should not be ruled off (see Figs.1/5 and 1/6).Fig.1/7.a personal account with no balance21BBAMOD1(03-07)Send for a FREE copy of our Prospectus book by airmail, telephone, fax or email, or via our website:International Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, BritainInternational Headquarters: College House, Leoville, Jersey JE3 2DB, Britain.Telefax: +44 (0)1534 485485 Email: [email protected] Website: www.cambridgecollege.co.uk

SELF-ASSESSMENT TEST ONERecommended Answers to these Questions - against which you may compare your answers - willbe found on page 23. The maximum mark which may be awarded for each Question appears in

brackets at the end of the Question. Do NOT send your answers to these Questions to the Collegefor examination.No.1.What is the meaning of the term “assets”? In what ways do the “fixed assets” of a businessdiffer from its “current” assets? (maximum 20 marks)No.2.What are the differences between the “debtors” and the “creditors” of a business? Who arethe debtors and creditors of a small trading business likely to be in general?(maximum 20 marks)No.3.State exactly the wording of the basic rule of double-entry bookkeeping. Explain why that ruleis necessary, and why it must be strictly complied with in recording every transaction which occursin business. (maximum 20 marks)No.4. A business called Carib Catering Supplieshas a number of “credit customers”. Below areits transactions with one of them during the month of June. Rule up a ledger account, and recordeach transaction - in date order - into the account for Beachview Hotel in the ledger ofCarib CateringSupplies, and balance the account at the end of the month.(maximum 20 marks)June 6 Sold goods on credit to Beachview Hotel worth 277 units.June 8 Sold goods on credit to Beachview Hotel worth 199 units.June 10 Received back from Beachview Hotel goods worth 22 units.

June 15 Received a payment of 454 units from Beachview Hotel.June 16 Sold goods on credit to Beachview Hotel worth 210 units.June 22 Sold goods on credit to Beachview Hotel worth 306 units.June 25 Received back from Beachview Hotel goods worth 26 units.No.5. Place a tick in the box against theone correct statement in each set.(a)A transaction takes place when:1an entry is made in a ledger account.2a debit entry and a corresponding debit entry have been made.3one party gives out value and another party receives the same value.4all the entries are on the same side of a ledger account.(b)“Real accounts”:1actually exist in the ledger of a business.2record the values of the tangible assets of a business.3record the different types of revenue earned by a business, and the types of expenditureit incurs.4record transactions with people and organizations.(c)In bookkeeping a “balance” means:1

the difference between the total value of the debit and the total value of the credit entriesin a ledger account.2a scale used for weighing goods sold to customers.3there are the same numbers of entries on the debit and credit sides.4that a debit entry and a corresponding credit entry have been made.

RECOMMENDED ANSWERS TOSELF-ASSESSMENT TEST ONENo.1. The term “assets” refers to anything which a business owns; its possessions, in whatever formthose possessions might be. Some assets might be “tangible” items, such as buildings, machineryand cash, whilst other assets might be “intangible”, such as book debts and investments.Fixed assets are items which a business acquires in order to be able to run smoothly and efficientlyand to carry out its intended activities, whether they involve the manufacture of products, the saleof products or the provision of services. Generally, fixed assets are acquired with the intention oftheir being retained for some considerable time, and they are not bought and sold in the course ofnormal business activities.Current assets, on the other hand, are constantly changing in value in the normal course of abusiness’ activities; they include such possessions as cash, stocks of goods, and debts owed to thebusiness by trade debtors.No.2. Debtors are the people and/or organizations which owe money to a business, whilst creditorsare the people and/or organizations to whom a business owes money. In general, the debtors of a small business are likely to be mainly customers to whom it has sold

goods or services on credit, and who have not yet paid for those goods or services. In a smallernumber of cases debtors might also include people or organizations to whom the business has paidin advance of receiving the goods or services paid for; for example, there are times when a businesshas to pay a “deposit” before it is supplied with its requirements, whilst sometimes certain expenses,such as rent and insurance premiums, have to be paid a month or longer in advance - the recipientsof such payments are debtors of the business for the values of any goods or services not yet provided.The creditors of a small business are likely to be people or organizations who have supplied it withgoods or services for which it has not yet made payment. Others might be those who paid in advancefor goods or services not yet provided, or who have loaned money to the business, e.g. a bank.No.3. The wording of the basic rule of double-entry bookkeeping is:-There must be a debit and a corresponding credit entry (and vice versa)of the same value for every transaction that occurs.The rule is necessary, and must always be strictly complied with, because in every businesstransaction that occurs, no matter how large or small it might be, two things always happen at oneand the same time: one party to the transaction receives value, whilst the other party gives out thatvalue. To record that dual aspect of every transaction, two entries are required in the ledger; oneof those entries must be a debit entry, whilst the other - of an identical value - must be a credit entry.The debit entry records the “receiving” aspect, whilst the credit entry records the “giving” aspect.

Recommended