1st Annual DMMA Publisher Conference

Increasing ICT competitiveness and usage in

South Africa: the Challenge and

Opportunity

Loren Braithwaite-Kabosha SA Communications Forum

09 October 2013

Agenda

• Introduction of SACF

• Current Challenges

• Digital Media Opportunity

• Issues requiring urgent attention

2

Background of SACF

- Members of SACF also include numerous small and medium enterprises in the ICT and broadcasting industries, including electronic manufacturers ( this is only a partial list for the sake of brevity)

- The SACF is an organisation which pools together high level technical skills and business expertise in the ICT sector.

- Among South African ICT industry associations, SACF is the association which includes members from across the entire spectrum of the industry, rather than specific silos.

4

SACF Mission

To be the credible, nationally supported umbrella industry

platform:

• that serves, promotes and protects the interests of SACF members and other ICT associations,

• to enable the achievement of Vision 2020 and other initiatives,

• to create an innovative and globally competitive ICT industry,

• to accelerate national development,

• by proactively engaging the government and all other stakeholders.

5

SACF Vision

Unleashing the power of the SA ICT industry to create the

most enabling ecosystem for a universally connected and

prosperous South Africa

SACF Strategic Objectives:• To become the unifying platform of the ICT sector• To be instrumental in developing the appropriate policy and

regulatory ecosystem• To provide thought leadership through research and development• To coordinate the development of ICT human capital• To promote ICT as a means for socio-economic development• To further transformation in the ICT sector

6

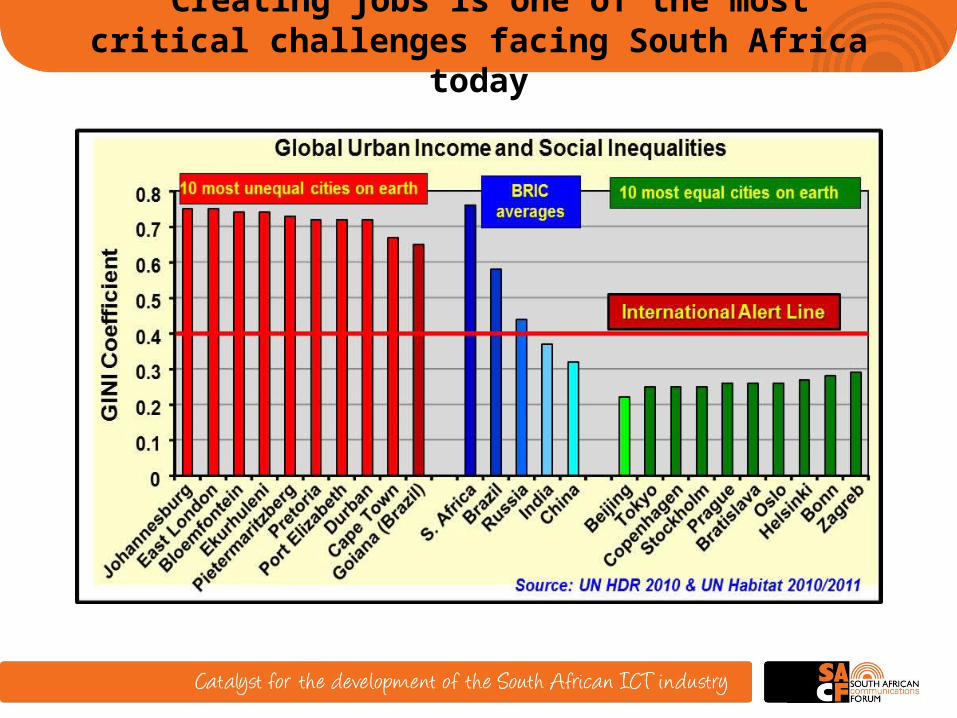

Creating jobs is one of the most critical challenges facing South Africa today

Recommendation

This UN recommendation, specific to the Southern African region, suggests how to help reduce the sub-region’s alarming and dangerously provocative income inequalities: SACF recommends consideration of its adoption

Recommended Intervention Areas in Southern Africa• As part of development policies, public authorities must mobilise urban young

peoples’ potentials and energies with proper training in entrepreneur skills and information/ communication technologies, in order to enable them to set up and run their own businesses. Some urban authorities have tried to foster inclusive cities, but none have fully considered children and youth in their service provision and governance strategies. Cities should make more efforts to deliver broadband Internet to all urban neighbourhoods, rather than reinforcing existing inequalities in services delivery.

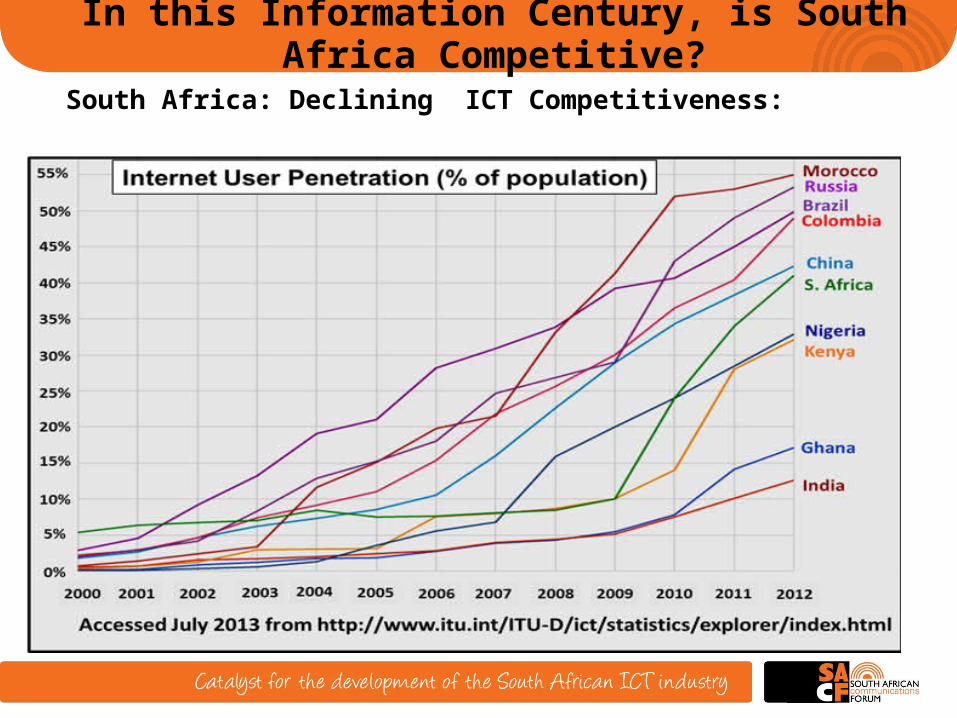

In this Information Century, is South Africa Competitive?

South Africa: Declining ICT Competitiveness:

Minister Carrim’s Priorities:

1. Set a firm foundation for a further reduction in the costs of communication. Carrim says the “digital revolution” is “changing very fabric of our society” but that it’s important the poor are not left behind.

2. See realistic progress in broadband becoming more extensive, affordable and speedier. "We intend to finalise the government's National Broadband Policy and Implementation Programme by end of November”, and says his department wants to have an “effective spectrum policy related to broadband” before March next year.

3. Reduce the digital divide between the haves and have-nots. "We are going to place much greater stress on delivering in rural and underserviced areas.The Internet presents a great opportunity for government to provide services to citizens,” Carrim says. “We must reduce, not increase, divides. We have made some progress, but not enough. We are lagging behind our peers.”

10

Minister Carrim’s Priorities, cont.

4. Stabilise the department of communications; state-owned companies and public entities in the ICT sector and make them more effective.

5. Begin with the roll-out of digital migration before the end of this year.

5. “Locating ICT in the national development plan and broader policies of the majority party”;

6. Finalising government’s ICT policy review.

11

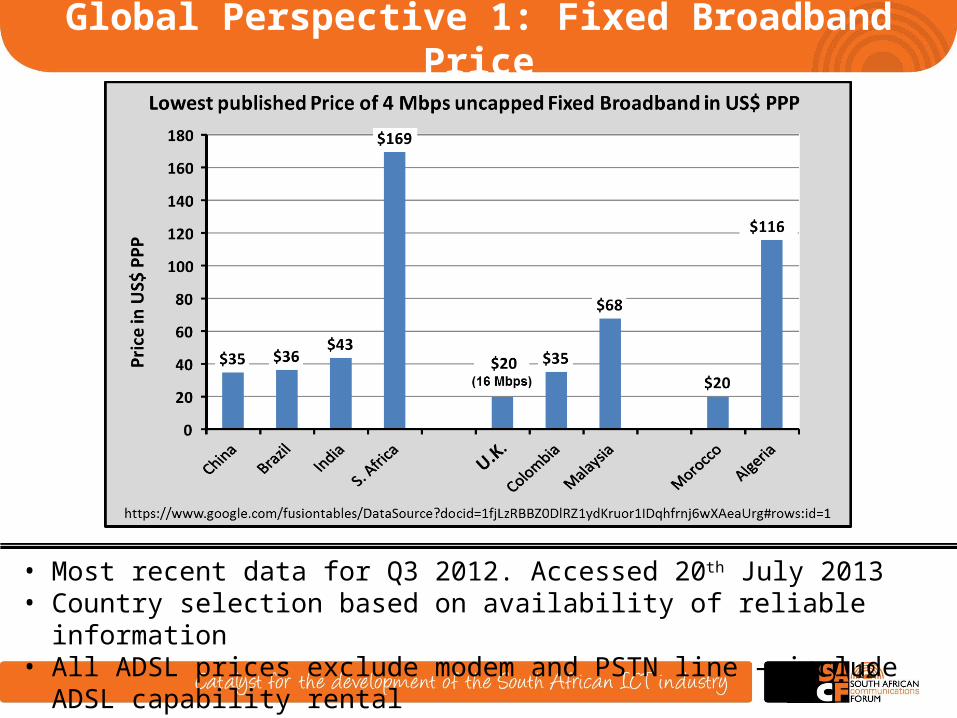

Global Perspective 1: Fixed Broadband Price

• Most recent data for Q3 2012. Accessed 20th July 2013• Country selection based on availability of reliable information• All ADSL prices exclude modem and PSTN line – include ADSL capability rental

12

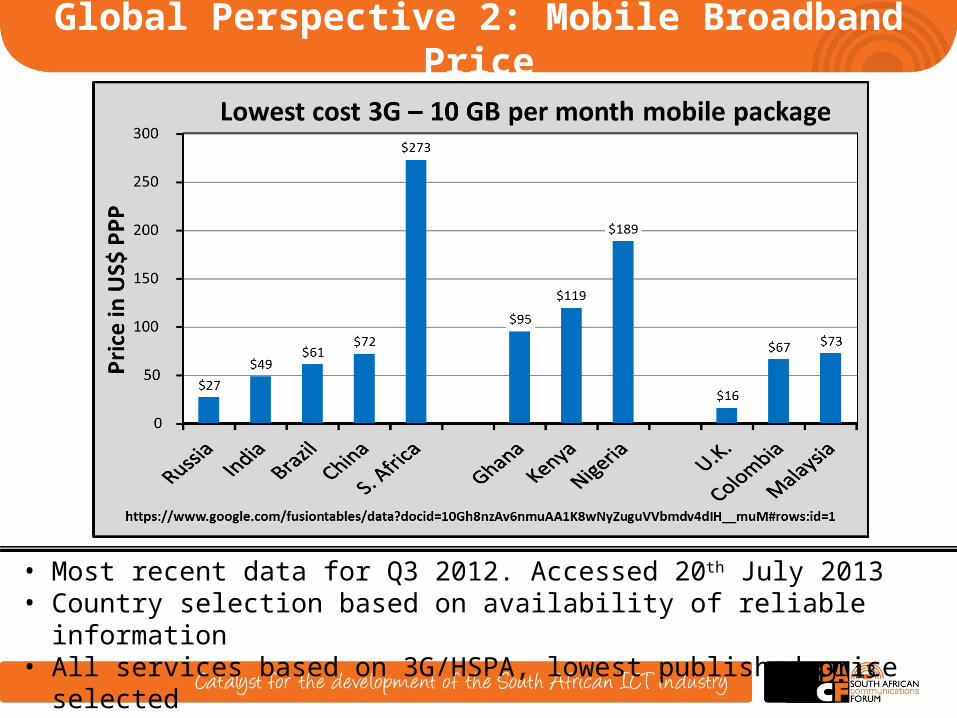

Global Perspective 2: Mobile Broadband Price

• Most recent data for Q3 2012. Accessed 20th July 2013• Country selection based on availability of reliable information• All services based on 3G/HSPA, lowest published price selected

13

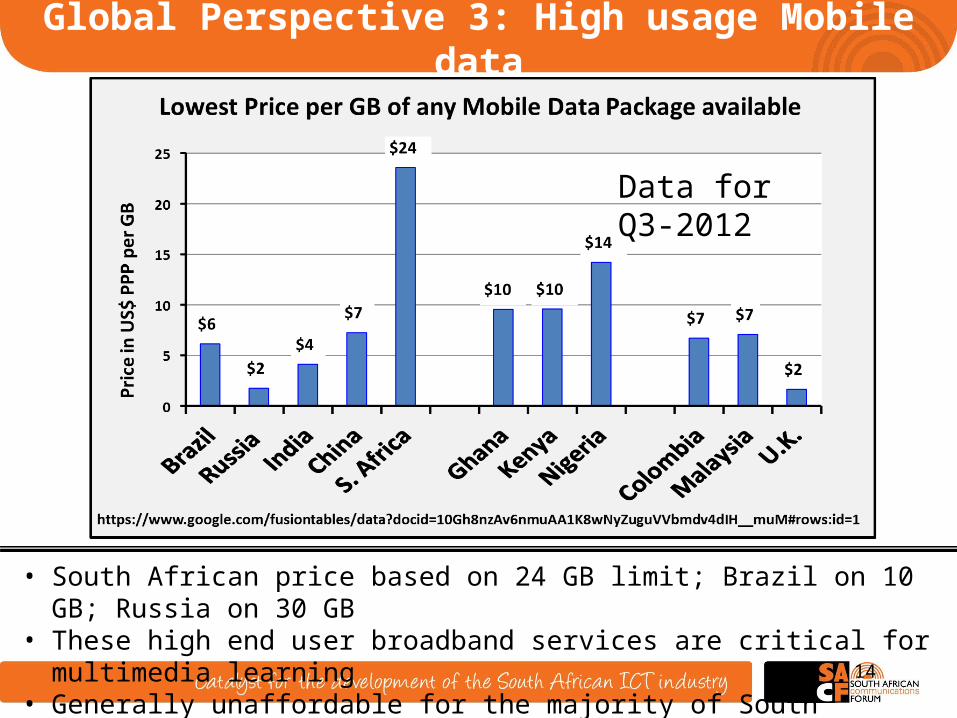

Global Perspective 3: High usage Mobile data

• South African price based on 24 GB limit; Brazil on 10 GB; Russia on 30 GB• These high end user broadband services are critical for multimedia learning• Generally unaffordable for the majority of South Africans

Data for Q3-2012

14

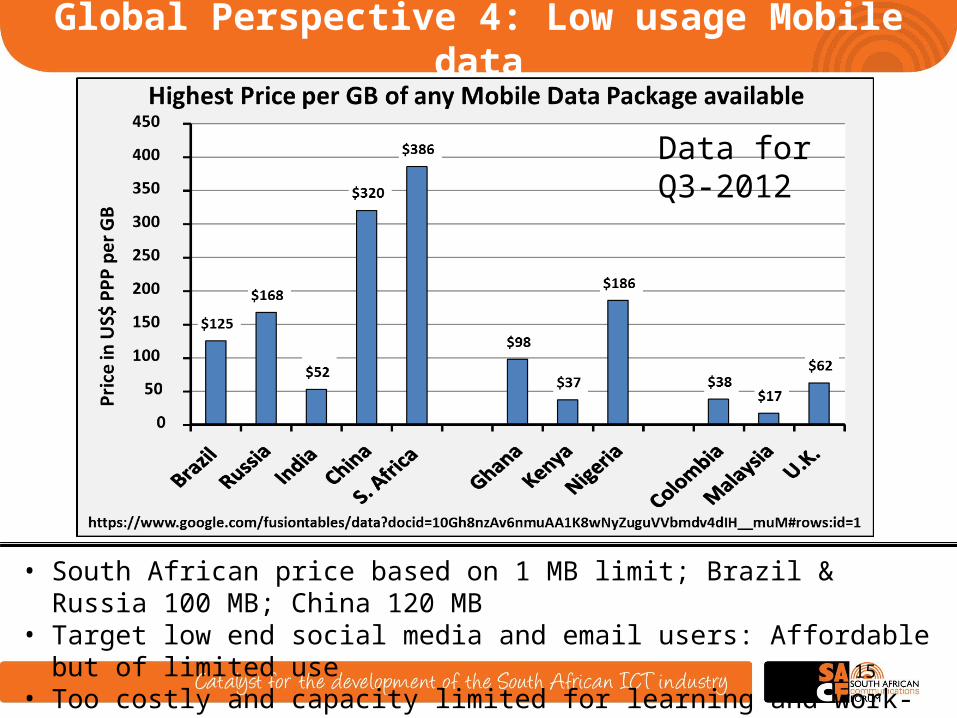

Global Perspective 4: Low usage Mobile data

• South African price based on 1 MB limit; Brazil & Russia 100 MB; China 120 MB• Target low end social media and email users: Affordable but of limited use• Too costly and capacity limited for learning and work-related usage

Data for Q3-2012

15

Economic ImplicationsInternational Implications of high Communication Costs

•Global investment decisions target countries with lower communication costs;

•South Africa losing more than competitive advantage – also losing position as favoured investment destination and ICT gateway for the continent;

•Example: Numerous global ICT companies including IBM, Google and Intel companies locating their African headquarters in Kenya – higher ICT growth, Lower ICT prices

National Implications of high Communication Costs

•High costs restrict and limit significant engagement with the tools and resources available through the internet for a majority of South Africans. Even those who have limited access (Facebook and Twitter) do not become fully fledged Digital Citizens able to utilise the maximum benefits of ICT for human development

•South Africa is among the nations with the highest income inequality in the world. High costs means large percentage of population shut out of Knowledge Economy; stuck in quagmire of poverty; and utilise a larger percentage of income for communications costs of basic needs.

•Overall drag on economic growth as access and implementation of ICT is an enabler across all industries.

16

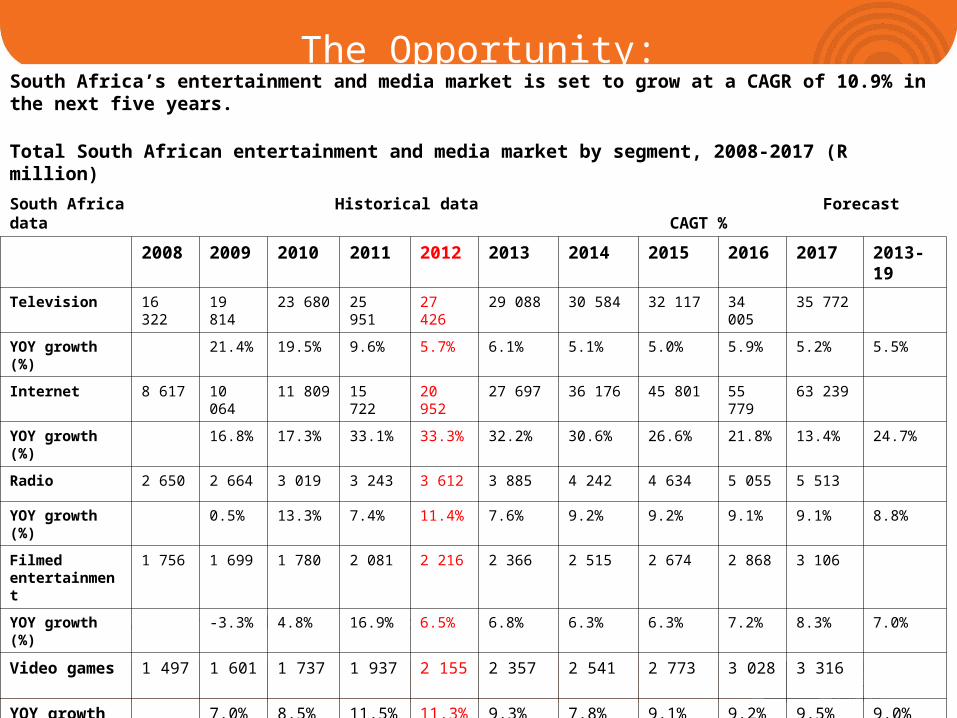

The Opportunity:

Source: PWC, Informa Telecoms & Media

South Africa’s entertainment and media market is set to grow at a CAGR of 10.9% in the next five years.

Total South African entertainment and media market by segment, 2008-2017 (R million)

South Africa Historical data Forecast data CAGT %

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2013-19

Television 16 322 19 814 23 680 25 951 27 426 29 088 30 584 32 117 34 005 35 772

YOY growth (%) 21.4% 19.5% 9.6% 5.7% 6.1% 5.1% 5.0% 5.9% 5.2% 5.5%

Internet 8 617 10 064 11 809 15 722 20 952 27 697 36 176 45 801 55 779 63 239

YOY growth (%) 16.8% 17.3% 33.1% 33.3% 32.2% 30.6% 26.6% 21.8% 13.4% 24.7%

Radio 2 650 2 664 3 019 3 243 3 612 3 885 4 242 4 634 5 055 5 513

YOY growth (%) 0.5% 13.3% 7.4% 11.4% 7.6% 9.2% 9.2% 9.1% 9.1% 8.8%

Filmed entertainment

1 756 1 699 1 780 2 081 2 216 2 366 2 515 2 674 2 868 3 106

YOY growth (%) -3.3% 4.8% 16.9% 6.5% 6.8% 6.3% 6.3% 7.2% 8.3% 7.0%

Video games 1 497 1 601 1 737 1 937 2 155 2 357 2 541 2 773 3 028 3 316

YOY growth (%)

7.0% 8.5% 11.5% 11.3% 9.3% 7.8% 9.1% 9.2% 9.5% 9.0%

The Opportunity:

Source: PWC, Informa Telecoms & Media

South African entertainment and media consumer spend 2008-2017 (R millions)

South Africa Historical data Forecast data CAGT %

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2013-19

Television 10 040

11 905 13 556 15 017 16 055 17 091 17 867 18 700 19 715 20 695

YOY growth (%)

18.6% 13.9% 10.8% 6.9% 6.5% 4.5% 4.7% 5.4% 5.0% 5.2%

Internet access

8 110 9 515 11 197 14 857 19 769 26 147 34 150 43 232 52 647 59 570

YOY growth (%)

17.3% 17.7% 32.7% 33.1% 32.3% 30.6% 26.6% 21.8% 13.2% 24.7%

Filmed entertainment

1 389 1 397 1 425 1 570 1 664 1 772 1 876 1 990 2 136 2 325

YOY growth (%)

0.6% 2.0% 10.2% 6.0% 6.5% 5.9% 6.1% 7.3% 8.9% 6.9%

Music 2 557 2 360 2 314 2 212 2 154 2 146 2 147 2 160 2 181 2 200

YOY growth (%)

-7.7% -2.0% -4.4% -2.6% -0.4% 0.1% 0.6% 1.0% 0.9% 0.4%

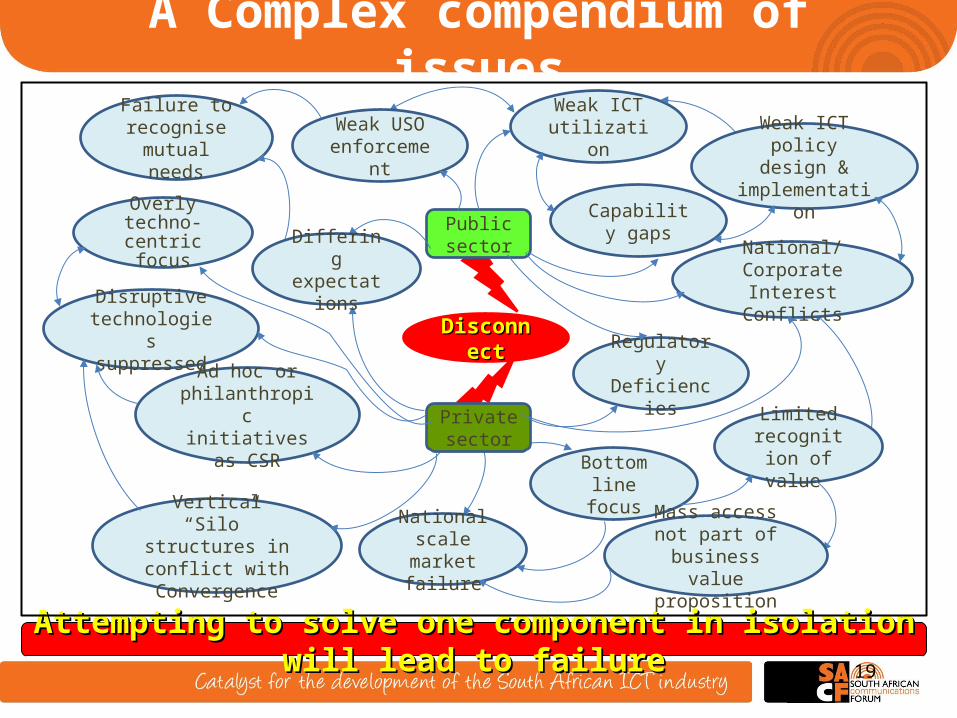

A Complex compendium of issues

Attempting to solve one component in isolation will lead to failureAttempting to solve one component in isolation will lead to failure

Public sector

DisconnectDisconnect

Bottom line focus

Limited recognition

of value

Mass access not part of business

value proposition

National scale market

failure

Ad hoc or philanthropic

initiatives as CSR

Disruptive technologies suppressed

Weak ICT utilization

Capability gaps

Overly techno-

centric focus

Failure to recognise

mutual needs

Private sector

National/Corporate Interest Conflicts

Regulatory Deficiencies

Vertical “Silo” structures in conflict

with Convergence

Weak ICT policy design &

implementation

Differing expectations

Weak USO enforcement

19

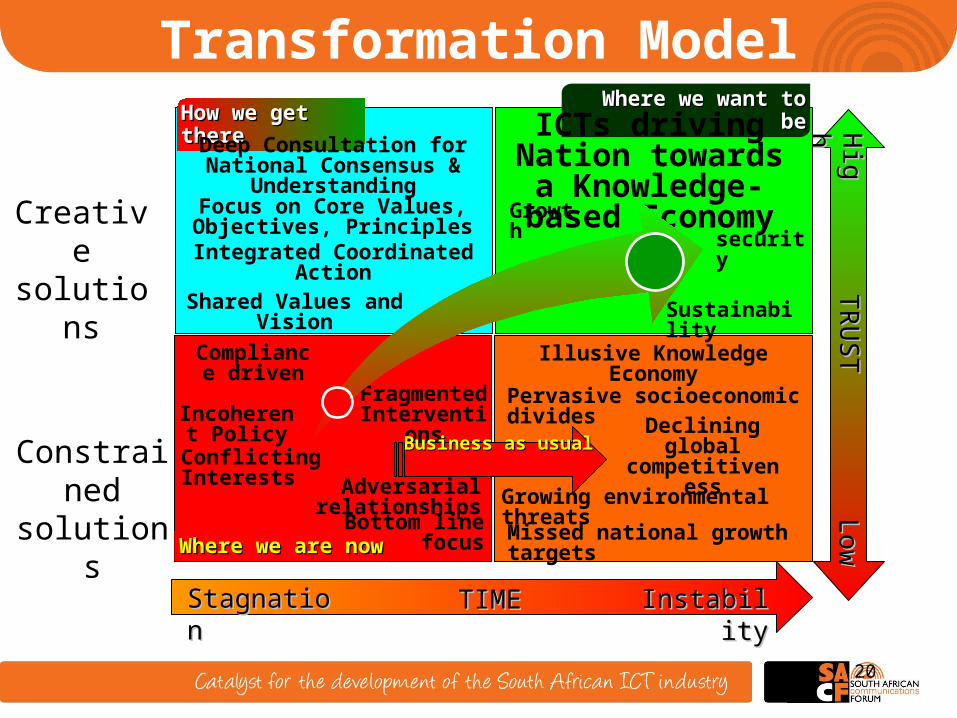

Constrained solutions

Low

Low

Hig

hH

igh

TR

US

TT

RU

ST

Where we are nowWhere we are nowBottom line

focus

Adversarial relationships

Compliance driven

Conflicting Interests

Fragmented InterventionsIncoherent

Policy Declining global competitiveness

Missed national growth targets

Illusive Knowledge Economy

Pervasive socioeconomic divides

Growing environmental threats

Where we want to beWhere we want to beICTs driving Nation towards a

Knowledge-based EconomyGrowth

Sustainability

security

Creative solutions

How we get thereHow we get thereDeep Consultation for National

Consensus & UnderstandingFocus on Core Values, Objectives,

Principles

Integrated Coordinated Action

Shared Values and Vision

Transformation Model

InstabilityInstabilityStagnationStagnation TIMETIME

Business as usualBusiness as usual

20

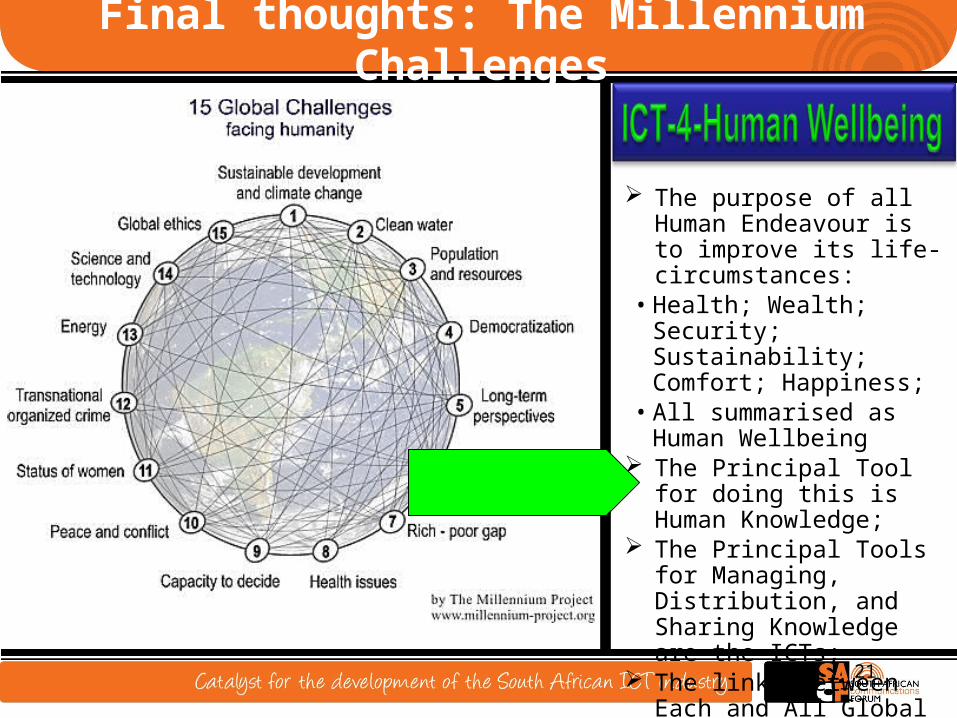

The purpose of all Human Endeavour is to improve its life-circumstances:

• Health; Wealth; Security; Sustainability; Comfort; Happiness;

• All summarised as Human Wellbeing

The Principal Tool for doing this is Human Knowledge;

The Principal Tools for Managing, Distribution, and Sharing Knowledge are the ICTs;

The links between Each and All Global Challenges

Final thoughts: The Millennium Challenges

21

ConclusionConcluding recommendations:

1. The high cost to communicate; infrastructure deficit in rural and underserviced areas; lack of capacity of important stakeholders in bridging the digital divide and other factors damages economic development generally and negatively influences inward investment decisions;

2. The PCC, Department of Communications, ICASA and the national ICT industry, including the DMMA, should collaborate to agree on the flaws in South Africa’s ICT ecosystem and solutions going forward

3. It is vital that every actual, perceived or nuanced impediment to reducing the national cost to communicate be analysed meticulously and integrated into corrective processes acceptable to, and implemented by all stakeholders, in a time-bound process;

4. These impediments examined must include policy, regulatory and industry-specific issues.

22

Ke a leboga Dankie Ngiyathokoza

Ke a leboha Thank you

Siyabonga Ngiyabonga

Inkomu Ndo livhuwa Enkosi

Loren Braithwaite Kabosha

011 315 0590

083 267 2768

Recommended