Embed Size (px)

Citation preview

Zero-Base Budgeting Redux in Georgia:Efficiency or Ideology?

THOMAS P. LAUTH

Zero-base budgeting reentered the Georgia budgetary process in 2012 after a hiatusof approximately three decades. This article describes the events leading up to thereentry of ZBB, compares the new version of ZBB with the original versionimplemented during the administration of Governor Jimmy Carter in the 1970s, andassesses the likely impact of this latest budget reform for Georgia and other stategovernments. Even though the nomenclature, “ZBB,” used to describe the currentGeorgia budget process is the same as that used to describe the state’s budget processduring the Carter administration, operationally the Carter-era and new ZBB are notthe same. The Carter-era ZBB had a unique and clearly defined terminology and setof procedures, whereas the new ZBB relies mostly on existing performance-budgetprocedures. The Carter-era ZBB purported to build the budget up from a zero base.The new ZBB is about drilling down into the base or continuation budget. TheCarter-era ZBB was a managerial process intended to achieve efficiency andeffectiveness. The new ZBB is more ideologically conservative with the aim ofcutting the budget and shrinking state government. Claimed budget reductions maybe significant at the micro-level, but they probably are not at the macro-level.However, it may not matter what cost reductions are actually realized. The symboliceffect of the ZBB process is what is most important, confirming the fiscalconservative bona fides of state government leaders.

INTRODUCTION

Zero-base budgeting (ZBB) reentered the Georgia budgetary process in 2012 after a hiatus of

approximately three decades. It is not often that a budgetary innovation goes through a life-cycle

of advocacy, adoption, implementation, decline, and discontinuation and then returns at a later

time in the same venue for a second iteration. Such an occurrence presents an analytical

opportunity too rich to ignore. This article describes the events leading up to the reentry of ZBB,

compares the new version of ZBB with the original version implemented during the

Thomas P. Lauth is Dean Emeritus and Professor Emeritus in the School of Public and International Affairs, the

University of Georgia, 107 Baldwin Hall, Athens, GA 30602. He can be reached at [email protected].

© 2014 Public Financial Publications, Inc.

Lauth / ZBB Redux in Georgia 1

administration of Governor Jimmy Carter in the 1970s, and assesses the likely impact of this

latest budget reform for Georgia and other governments. It is based upon interviews with agency

heads, agency budget personnel, executive budget office personnel, and legislative leaders,1 as

well as a review of the legislative history, budget preparation instructions, and zero-base budget

documents.

CARTER-ERA ZERO-BASE BUDGETING

ZBB was initiated in Georgia in 1973 by Governor Jimmy Carter. It was a budgeting procedure

pioneered at Texas Instruments (Pyhrr 1970, 1973, 1977). As installed in the 1970s, ZBB was

applied to all state government agencies and each agency was expected to use it every year to

assess all of its programs and activities. It sought to focus budget deliberations on the whole

budget not just on proposed increases, and required state agencies to defend their entire budget

each year with no assurance that their prior year budget would be retained. It was potentially a

good idea for improving financial management in Georgia state government, but it generally

failed in its implementation. The architects and advocates of ZBB underestimated the volume of

information that would be generated, which turned out to defy the ability of decision makers to

digest and use that information during the annual budget cycle. The result was that state agencies

came to believe that the executive budget office was overwhelmed by the information they

produced and that the legislative budget office, as well as the legislature, disregarded the

information in making their appropriation decisions. Agencies soon began to take the process

less seriously and to fudge the analytical data they produced in subsequent years. Eventually, the

process broke down and gradually fell into disuse (Lauth 1978; Huckaby and Lauth 1998).

Governor Carter transported ZBB with him to Washington and in 1977, as President Carter,

proclaimed it as the official budgeting system for all federal government agencies. However,

ZBB never quite penetrated the federal budget system and President Ronald Reagan terminated

it in 1981 (Newland 1983).

ZERO-BASE BUDGETING AS RATIONAL-COMPREHENSIVE REFORM

Before further consideration of the new ZBB in Georgia, it will be useful to locate ZBB within

the context of budget reform initiatives. Budget reforms generally have been of two broad types,

1. This research included several elite interviews. “Elites” in this context are individuals who by virtue of their

official position, duties, and responsibilities possess information and perspectives not generally available to

nonelites. The purpose of the interviews was to obtain information about why ZBB reemerged and how it emerged as

it did. Not all interviewees were asked the same questions; questions were designed based upon the interviewee’s

position in the budget process. Agency heads and budget officers were selected based upon whether or not their

agencies were included in the first two years of ZBB review. Legislative leaders and central budget office personnel

were selected by virtue of their positions. Interviews lasted between 30 and 60minutes. Bullet-point notes were taken

during some interviews and detailed notes were written or voice recorded immediately after the interview.

2 Public Budgeting & Finance / Spring 2014

those that seek to restructure institutional relationships and rational-comprehensive reforms

(Lindblom 1959; Lindblom 1979) that seek to introduce additional information into the decision-

making process. Institutional reforms have been about strengthening the role of the chief

executive or alternatively the role of the legislature in the budget process (Budgeting and

Accounting 1921; Congressional Budgeting and Impoundment Control Act 1974).

During the second half of the twentieth century, rational-comprehensive budgeting reforms

attempted to integrate program and performance information into budget deliberations. The

reforms were rational in that they sought to consider program performance in relationship to

organizational mission and goals, alternative methods to achieve mission and goals, as well as

the costs and benefits associated with various alternatives. They were comprehensive in that they

sought to consider all organizational resource allocations, not just proposals for new or

additional spending. The most prominent reforms were the Planning Programming Budgeting

System (Schick 1966, 1971) and ZBB, as well as efforts to link various management and policy

approaches such as productivity improvement (Rabin 1987), policy analysis (Lee and

Staffeld 1977; Lee 1997), and performance assessment (Melkers and Willoughby 1998;

Willoughby and Melkers 2000; Melkers and Willoughby 2001; Kelly and Rivenbark 2003;

Mikesell 2003; Willoughby 2004) to the budget process. These rational-comprehensive

budgeting approaches required the consideration of program and performance information, in

quantitative form where feasible, along with conventional financial information. The objective

of the budget reforms was to focus greater attention on planning, policy analysis, and program/

performance evaluation, without diminishing the importance of financial control.

In its ideal form, ZBB is rational in that agencies develop budget requests at different funding

and service levels for each activity or program. Agencies begin the zero-base process by

identifying cost centers (agency subunits or programs) for which it is feasible and appropriate to

assign costs for activities or services. Decision packages are prepared for each cost center which

include: a statement of goals, a description of the work program by which goals are to be

achieved, a statement of benefits expected from activities or services in relationship to costs, an

assessment of alternative methods of achieving goals, alternative levels of funding for the

decision packages, and a statement of the consequences of not funding a decision package.

In ideal form, ZBB is comprehensive in that each program is required to justify its existence

during each budget cycle, and every item included in a proposed budget needs to be justified. The

core elements of ZBB are decision packages and a ranking process. Funding for each decision

package usually is expressed as a percentage of the previous year’s budget, packages are ranked

in order of decreasing benefit to the agency and a cumulative percentage is calculated as each

package is entered into the ranking. Before the first (highest priority or most essential) decision

package is entered into the ranking, the cumulative ranking total stands at zero, hence the

designation ZBB. ZBB was proposed as an alternative to incrementalism, an approach to

budgeting that tends to assume that funding for existing programs will be continued and focuses

budget preparation and review activity mostly on proposals for new or additional funding. In

ZBB, agencies may not assume continued funding for programs.

In the years between the Carter-era ZBB and the new ZBB, the Georgia budget process passed

through several other rational-comprehensive budget reforms.

Lauth / ZBB Redux in Georgia 3

Budget Redirection

Budget Redirection emerged in Georgia in the mid-1990s as an innovation designed to achieve

both managerial and policy objectives within a constricted fiscal environment (Huckaby and

Lauth 1998). Redirection was an approach to budgeting that sought to: (1) fund ongoing agency

services and enhancements using the current level of resources, (2) fund formula and

entitlement-related services in a way that minimized the need for additional resources, and

(3) increase fund availability for priority areas within state government as a whole. Agencies

were encouraged to identify activities or programs that no longer were necessary, or of high

priority, and eliminate or downsize them. Specifically, agencies were required to so identify a

minimum of 5 percent of their current year’s budget. Funds realized through this process became

available for redirection to activities or programs that had a higher priority for the agency, or to

other sectors of state government that had a high priority for the governor.

Results-Based Budgeting

Results-based budgeting (RBB), implemented in Georgia in 1997 for the 1998 fiscal year,

required that for each program a purpose, goal, and desired result be developed that could be

accomplished during the coming fiscal year. The objective of RBB was to change budget

conversations by shifting the focus from inputs to outcomes. However, the state General

Assembly resisted, still preferring to focus on inputs and line items to control the budget. Initially

RBB and Budget Redirection co-existed, but because the governor becamemore interested in the

ability of Redirection to generate funds for his program priorities (e.g., removing the sales tax on

food and increasing teacher salaries), RBB as amanagement approach was of less interest to him.

In the absence of either legislative support or strong gubernatorial support, RBB rapidly

diminished in importance as either a management or budget tool in Georgia.

Prioritized Program Budgeting

Following the election of Georgia’s first Republican governor in more than 130 years, prioritized

program budgeting (PPB) was introduced in 2004 for the 2005 fiscal year as the state’s new

budgeting system. PPB is predicated on each agency having developed a strategic business plan.

It emphasizes programs, rather than agencies, as the primary budgetary units (Bourdeaux 2008),

and requires that measures of demand for the program, program efficiency, program output, and

program results be delineated and utilized. Agencies were required to propose program budgets

at three levels: a 5 percent reduction of the base budget; redistribution of an amount equal to 3

percent of the base budget; and enhancement limited to 2 percent of the base budget.

Redistribution is a way to shift existing funds from low priority programs or sub-programs to

higher priority programs or sub-programs. Redistribution seems conceptually indistinguishable

from Budget Redirection used in the mid-1990s, and the requirement that program results be

measured is very similar to RBB of the late 1990s. Nevertheless, a new governor and new

administration were seeking to promote their own brand of program budgeting. As will be shown

below, PPB came to be an important part in the new ZBB in Georgia.

4 Public Budgeting & Finance / Spring 2014

LEGISLATIVE HISTORY OF THE NEW ZERO-BASE BUDGETING

In the 1970s, Governor Jimmy Carter was the principal advocate of ZBB in Georgia. It was an

executive branch initiative intended to improve managerial efficiency and effectiveness in the

operations of the executive branch of state government.2 The legislative branch rejected ZBB,

preferring instead continuation or incremental budgeting with its presumption that resource

allocation commitments of previous years would, for the most part, be continued and that the

current year budget process would focus mostly on reviewing proposals for new resource

commitments (Lauth 1978).

In contrast, in the 2000smembers of theGeorgiaGeneral Assemblywere the principal advocates

of ZBB with the governor initially rejecting it. In 2009, the Georgia Senate passed a ZBB bill, but

the House of Representatives did not. In 2010, both chambers passed a ZBB bill, but Governor

Sonny Perdue vetoed it saying that it was unnecessary because his staff already examined all facets

of each agency’s budget each year.3 The Senate voted to over-ride the governor’s veto, but the

House did not. In 2011, the House of Representatives passed a ZBB bill, but the Senate did not. In

those years, the House and Senate versions differed on such matters as (1) how frequently agencies

would be subject to ZBB review (every five, eight or 10 years), and (2) who would select the

agencies or programs for annual review (the executive branchOffice of Planning andBudget (OPB)

or the legislative branch Fiscal Affairs Committees). In 2012, the Georgia General Assembly

enacted and Governor Nathan Deal signed a bill requiring ZBB for selected state agencies to begin

with the FY 2014 budget.4 Governor Deal had voluntarily implemented ZBB for selected state

agencies beginning with the FY 2013 budget. The ZBB act passed in 2012 requires that agencies

and programs are subject to ZBB review at least once every 10 years but not more often than once

every eight years, and that agencies and programs are selected for ZBB review by theHouse Budget

Office and Senate Budget and Evaluation Office in consultation with the Governor’s OPB.

There are generally two explanations for whyGovernor Sonny Perdue vetoed ZBB legislation

in 2010 and Governor Nathan Deal signed such legislation in 2012. The political explanation is

that Governor Perdue’s relationship with the General Assembly was more contentious and

Governor Deal’s relationship was more cooperative.5 The policy explanation, while not

discounting the political explanation, is that the bill presented to Governor Perdue applied ZBB

to every agency every four years, but the bill that was presented to Governor Deal was for a

selected number of agencies not more than every eight years.6

2. Governor Carter’s 1972 reorganization initiative generally streamlined the executive branch of state

government, eliminated or consolidated agencies, and reconstituted the Bureau of the Budget as the OPB.

3. Governor’s Veto Message, SB 1, June 8, 2010. He also stated that other states that have used ZBB have

abandoned it because of the additional bureaucratic process and overhead while producing few identifiable results.

4. Senate Bill 33, 2012 Session of the Georgia General Assembly, signed by Governor Nathan Deal May 2, 2012.

5. Interview with Senator Jack Hill, Chair, Senate Appropriations Committee, March 8, 2013. Also see Lauth

(2010).

6. Interview with John E. Brown, Vice Chancellor for Fiscal Affairs, University System of Georgia, August 10,

2012.

Lauth / ZBB Redux in Georgia 5

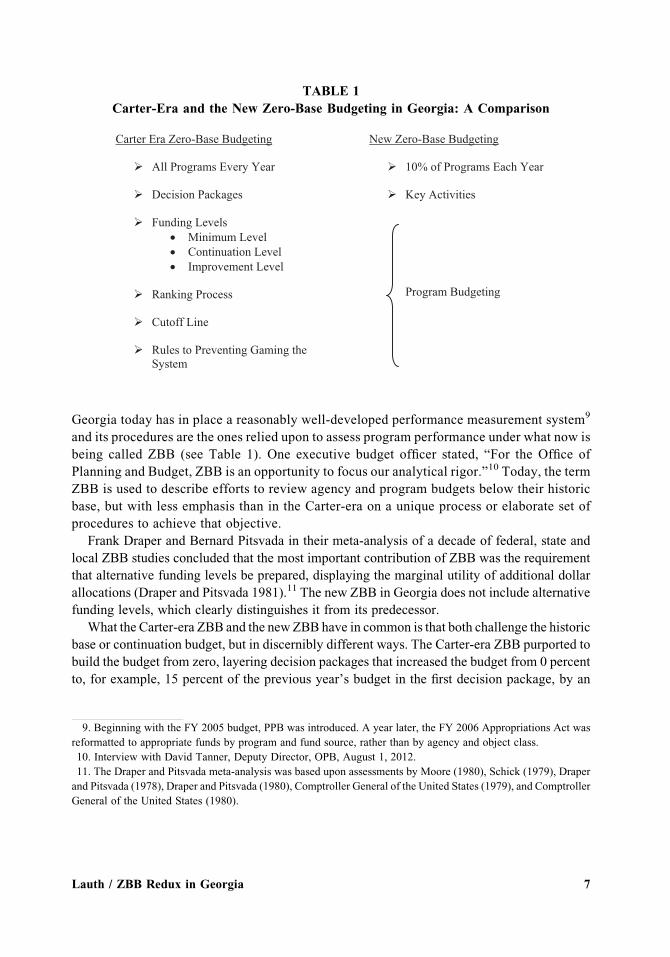

COMPARISON OF THE CARTER-ERA ZBB WITH THE NEW ZBB

The procedures that are associated with the new version of ZBB in Georgia are quite different

from the procedures that defined ZBB in the 1970s in Georgia, and elsewhere across the country.

There is no mention in the current zero-base instructions (OPB 2011) of decision packages, a

ranking process, minimum funding level, continuation funding level, improvement funding

levels, or a cut-off line, all staples of the original ZBB process in Georgia.7 The Carter-era ZBB

utilized a well-defined set of procedures such as (a) decision packages, which defined subunits or

activities to which costs could be assigned, delineated benefits expected from activities or

services in relationship to costs and assessed the consequences of not funding the decision

package, (b) three funding levels—minimum, the level below which it would no longer be

feasible to perform an activity, continuation, the cost of providing the same level of activity and

service as in the previous year, with salary and price increases reflected in the calculation and

nonrecurring costs eliminated, and improvements, higher levels of spending for ongoing

programs and funding for new activities and programs (more than one improvement level of

funding could be prepared in a decision package), (c) a process of ranking decision packages at

each of the three funding levels in order of decreasing benefit to the agencywith managers giving

higher priority to the packages that satisfy essential operating requirements and lower rankings

to more discretionary packages, (d) a cut-off line drawn where available revenue supported

funding decision packages above the line but not funding packages below the line, and (e) rules

that prevented agencies from gaming the system by ranking improvement packages ahead of

minimum or continuation packages in the hope that they wouldmore easily be funded (Lauth and

Reick 1979).

The new ZBB undertakes detailed evaluations of selected agencies and programs each year,

“assessing a particular program’s activities against its statutory responsibilities, purpose, cost to

provide services and desired performance outcomes” (OPB 2012). Agencies are asked to

identify their program’s “key activities” and explain why the program and its activities are

critical and necessary and if there are alternative ways of delivering the services of the program

(Official Code of Georgia Annotated). “Key activities” are seen by some observers as the new

ZBB counterpart to the Carter-era decision packages.8 Performance measures for programs and

their activities evaluate, for example, the workload, efficiency, and effectiveness of the activity

or program. Performancemetrics are vetted by the OPB, theHouse Budget Office, and the Senate

Budget and Evaluation Office. Finally, financial analysis of a program examines historical

expenditures by object class, with the goal of assessing cost effectiveness and return on

investment. Although these procedures are identified as zero-base budget analysis, in reality they

are fairly standard performance-budgeting reviews.

The initial version of ZBB installed during the Carter administration consisted of an

elaborate and unique set of budget preparation procedures. However, unlike the 1970s,

7. For a full description of the original ZBB process in Georgia, see Lauth (1997).

8. Interview with David Tanner, Deputy Director, OPB, August 1, 2012.

6 Public Budgeting & Finance / Spring 2014

Georgia today has in place a reasonably well-developed performance measurement system9

and its procedures are the ones relied upon to assess program performance under what now is

being called ZBB (see Table 1). One executive budget officer stated, “For the Office of

Planning and Budget, ZBB is an opportunity to focus our analytical rigor.”10 Today, the term

ZBB is used to describe efforts to review agency and program budgets below their historic

base, but with less emphasis than in the Carter-era on a unique process or elaborate set of

procedures to achieve that objective.

Frank Draper and Bernard Pitsvada in their meta-analysis of a decade of federal, state and

local ZBB studies concluded that the most important contribution of ZBB was the requirement

that alternative funding levels be prepared, displaying the marginal utility of additional dollar

allocations (Draper and Pitsvada 1981).11 The new ZBB in Georgia does not include alternative

funding levels, which clearly distinguishes it from its predecessor.

What the Carter-era ZBB and the new ZBB have in common is that both challenge the historic

base or continuation budget, but in discernibly different ways. The Carter-era ZBB purported to

build the budget from zero, layering decision packages that increased the budget from 0 percent

to, for example, 15 percent of the previous year’s budget in the first decision package, by an

TABLE 1

Carter-Era and the New Zero-Base Budgeting in Georgia: A Comparison

Carter Era Zero-Base Budgeting

All Programs Every Year

Decision Packages

Funding Levels • Minimum Level • Continuation Level • Improvement Level

Ranking Process

Cutoff Line

Rules to Preventing Gaming the

System

New Zero-Base Budgeting

10% of Programs Each Year

Key Activities

Program Budgeting

9. Beginning with the FY 2005 budget, PPB was introduced. A year later, the FY 2006 Appropriations Act was

reformatted to appropriate funds by program and fund source, rather than by agency and object class.

10. Interview with David Tanner, Deputy Director, OPB, August 1, 2012.

11. The Draper and Pitsvada meta-analysis was based upon assessments by Moore (1980), Schick (1979), Draper

and Pitsvada (1978), Draper and Pitsvada (1980), Comptroller General of the United States (1979), and Comptroller

General of the United States (1980).

Lauth / ZBB Redux in Georgia 7

additional 10 percent in the next ranked package (for a total of 25 percent of the previous year)

and so on until the layered packages reached approximately 85 percent at the minimum funding

level and perhaps 105 percent at the continuation level and 115 percent at the improvement level.

The new ZBB in Georgia is not about building the budget from zero or the bottom up. It is about

reviewing the base or continuation budget, using the performance review techniques described

above, with the expectation of finding duplication, waste and obsolescence and thereby reducing

the size of government.12 The new ZBB essentially expresses a Republican-conservative13

philosophy in fiscal matters (Lauth 2006) and is a “rallying cry” for fiscal conservative state

legislators.14

EXECUTIVE BRANCH ZERO-BASE PRACTICES AND PROCEDURES

The locus of the new ZBB in Georgia is in the OPB, a unit in the executive office of the governor.

The new ZBB applies to programs, not agencies, and has been melded with the program

budgeting system. The new concept for Georgia budgeting is “key activities.” The purpose is to

look at what programs are being delivered andwhat activities are being performed in conjunction

with those programs, that is, what programs do. What programs do is a combination of federal

mandates, state law, and annual budget actions or appropriation decisions. OPB has seen ZBB as

an opportunity to identify programs and activities that have become part of the historic budget by

way of annual budget actions or appropriation decisions, and require that their continuance be

justified. Of course, this could have been done through program budget review but ZBB has

given such reviews greater impetus and legitimacy. Legislative advocates of ZBB wanted

something that drilled into the base or continuation budget. However, the design and

implementation of the new ZBB was left up to OPB.15

The way in which the OPB drills into the base or continuation budget is through a series of

steps, including (1) identification and evaluation of agency “key activities,” (2) development and

evaluation of performance measures, (3) financial analysis of a program including its historical

expenditures by object class, (4) summarizing the results of analysis, and (5) identification of

alternative approaches to deliver services. With regard to key activities, agencies are required to

identify the policy objective of the activity, the primary constituency for the activity, statutory

authority requiring the activity, the cost to carry out the activity and to explain why a program

and its activities are critical and necessary. With regard to performance measures, OPB and

the House and Senate budget offices are expected to reach an agreement on the appropriate

performance measures an agency should use and report for each key activity. Performance

12. Interview with Senator David Shafer, September 6, 2012.

13. In the 1970s, Democrats controlled the governor’s office and both houses of the General Assembly. Since 2004,

Republicans have controlled the governor’s office and both houses of the General Assembly. Georgia Democrats and

Republicans are both fiscally conservative, but in the twenty-first century Republicans are discernibly more

conservative than Democrats.

14. Interview with Senator David Shafer, September 6, 2012.

15. Interviews with David Tanner, August 1, 2012 and November 28, 2012.

8 Public Budgeting & Finance / Spring 2014

measures are expected to describe the workload, efficiency and effectiveness of an activity or

program. OPB analysts are tasked with working with agencies to define and refine performance

measures. Measures are expected to be clear, valid, reliable and relevant to the purpose of

the activity, program or agency. With regard to financial analysis, agencies are expected to

provide expenditure analysis for personnel services, operating expenses for approximately 10

standard object classifications and any unique object classes. With regard to results of analysis,

OPB analysts and agencies are expected to identify positive results as well as areas that need

improvement. With regard to alternative approaches, OPB analysts and agencies are expected to

identify alternative ways of achieving the objective of an activity or program.

In FY 2013, the first year of the new ZBB, 35 programs across 25 state agencies

(approximately 10 percent of the state’s approximately 370 programs) were subject to ZBB

review. The number was based mostly on a reasonable workload for OPB staff. The programs

chosen for review were a combination of what programs OPB already had targeted for closer

review, a few volunteers, for example, the Department of Agriculture,16 and a reasonable

workload based upon size and scope of programs. Recalling that one of the reasons for the failure

of the Carter-era ZBB was that the process became over-burdened by the requirement that all

programs of all agencies were reviewed every year, applying ZBB to only a segment of state

agencies and programs each year was thought to be a sensible approach. The Chair of the House

Appropriations Committee reported that he had received advice from a veteran budget staff

member to avoid the Carter-era ZBB model because it would “load us down with mounds of

paper.”17

In FY 2014, the second year of the new ZBB, 56 programs across 24 agencies, including most

of the programs from the Department of Education,18 were subject to ZBB review. The ZBB

legislation passed by the General Assembly in its 2012 session and signed by Governor Nathan

Deal on May 2, 2012 contains the following language, “Without in any way limiting the other

provisions of the Code section, it is specifically provided that in the budget report presented to the

General Assembly in January of 2013 the Department of Education’s budget shall be submitted

as a zero-base budget according to the guidelines contained in this Code section.”19Whywas the

Department of Education specifically identified in the legislation? TheAssistant Budget Director

of that department offered that it was because of the size and importance of the agency.20 The

more likely reason is because appropriators in the General Assembly perceived the Department

16. The newly elected Commissioner of the Department of Agriculture requested a thorough review of his agency,

which under the previous administration had for decades resisted any use of program or performance budgeting.

Interview with Gary Black, Commissioner of Agriculture, January 3, 2013.

17. Interview with Terry England, Chair, House Appropriations Committee, April 22, 2013.

18. Twenty-three in FY 2014; two had been included in FY 2013.

19. The other state agency identified by name in the legislation was the Board of Regents of the University System

of Georgia. However, because the state appropriation to the Board of Regents is a lump-sum based largely upon

student credit hour production by the System’s several institutions, ZBB does not have much impact on the Board of

Regents. In FY 2013, only the Regents Central Office and two administratively attached programs were part of the

ZBB process.

20. Interview with Denise Peterson, Assistant Budget Director, Department of Education, April 30, 2013.

Lauth / ZBB Redux in Georgia 9

of Education leadership as very uncooperative and resistant to the General Assembly’s oversight

requests for information, with agency budget staff viewed as frightened to share information.

Calling out the department by name was intended to get its attention and assert the will of the

General Assembly.21

The core activity of the new ZBB is the interaction between OPB analysts and agency budget

officers. The Zero Base Budgeting Report is produced by the OPB.22 Agencies define their “key

activities” but their definitions are reviewed by OPB analysts as well as House and Senate budget

analysts who look at the agency’s authorizing legislation, the agency mission, and past

expenditure line items (the history of which is available in electronic storage). ZBB is perceived

by agency personnel as being much more focused on developing performance measures and

linking performance measures to agency funding. During the ZBB review process some new

performance indicators have been developed through negotiation among the agency, OPB

analysts and legislative budget analysts. In short, there has been a heightened level of interaction

between agency budgeters andOPB and legislative budget analysts withmore questions posed to

agencies and a greater level of effort required responding to them.

However, within this general pattern, interactions vary somewhat across agencies. Five

examples serve to illustrate. TheDepartment of Agriculture sought basic help in defining its “key

activities” and developing performance measures because under prior leadership the agency had

long resisted any movement in the direction of program or performance budgeting. For the new

Department of Agriculture leadership, ZBB was fortuitous.23 The Department of Education

perceived ZBB review as requiring considerable effort and resulting in some loss of operational

autonomy.24 Given that General Assembly appropriators perceived the Department of Education

leadership as uncooperative and resistant to their oversight requests,25 it is not surprising that the

department felt somewhat pressed during ZBB review. The Board of Regents of the University

System of Georgia receives an annual lump-sum appropriation based largely upon student credit

production by the System’s several institutions and for that reason ZBB has less significance for

this agency than it does for other state agencies.26 The Department of Human Services has

several established performance measures that are required by federal program compliance.

Usually, such measures are adaptable to state requirements, but when they are not, agency

program personnel and OPB and legislative budget analysts negotiate the additional

performance measures that will be used. Representatives of that agency observed that for

programs under regular budget review, they start from the base budget and do not have to answer

21. Interview with Terry England, Chair, House Appropriations Committee, April 22, 2013.

22. The Zero-Base Budgeting Report is not integrated into the Governor’s Budget Report, but is included as an

appendix to the main document.

23. Interview with Gary Black, Commissioner, Department of Agriculture; Sydney Moody, Director of Public

Policy, Department of Agriculture; and James Sutton, Chief Administrative Officer, Department of Agriculture,

January 3, 2013.

24. Interview with Denise Peterson, Assistant Budget Director, Department of Education, April 30, 2013.

25. Interview with Terry England, Chair, House Appropriations Committee, April 22, 2013.

26. Interview with Henry M. Huckaby, Chancellor and John Brown, Vice Chancellor for Fiscal Affairs, University

System of Georgia, August 10, 2012.

10 Public Budgeting & Finance / Spring 2014

many OPB or legislative budget analyst questions. However, for programs under ZBB review,

they have to respond to all the questions; the review is more holistic.27 The Department of

Economic Development is a high priority program for Governor Nathan Deal. For that reason,

the agency has had a positive experience with ZBB. The agency identifies its key activities and,

for the most part, defines its performance measures. According to the Chief Financial Officer,

ZBB is not much different from the ordinary budget process, except for a need for somewhat

greater justification of the programs undergoing ZBB review.28 The ZBB process applies

program budgeting to all state agencies selected for review in a given year, but as can be seen

from these examples agencies are impacted in different ways depending upon their unique

situations.

LEGISLATIVE BRANCH USE OF ZERO-BASE BUDGETING

Budget reform in the states usually has been initiated by the executive branch and the success of

the reform has been affected by the extent to which the state legislature has embraced it. Indeed,

Carolyn Bourdeaux found that legislative involvement is critical in promoting use of

performance information throughout the budgetary process (Bourdeaux 2006). Because the new

ZBB in Georgia was a legislative initiative, there is reason to expect that the legislature would

embrace it and integrate it into the budgetary process across the branches. Did it? Yes, it

embraced it philosophically, but it has not fully integrated it into the legislative budget process.

Senator David Shafer was the principal advocate of ZBB since he arrived in the Senate in 2003.

He began to advocate ZBB during his first term in the General Assembly because he thought he

might be called upon to support a tax increase proposed by fellow Republican Governor Sonny

Perdue,29 and wanted to be able to demonstrate to his constituents that he was a fiscal conservative.

Senator Shafer does not know exactly where he got the idea of ZBB, but believed it expressed his

Republican-conservative philosophy in fiscal matters.30 After he continued to use the idea, other

members of theGeneral Assembly seemed to have adopted it as well. Senator Shafer expressed how

surprised he was to find upon his arrival in the General Assembly that the state budget was not

considered as a whole each year but that the focus of reviewwas only on new spending proposals. It

probably is not entirely accurate to say that the base or continuation budget is never considered,31

but that was Senator Shafer’s perception of how things worked. Shafer cites as an example of waste

and abuse in the budget process that vacant positions are routinely funded and agency heads move

27. Interview with Lynn Vellinga, Chief Financial Officer, Department of Human Services and Demetrius Taylor,

Director of Budget Administration, Department of Human Services, July 2, 2013.

28. Interview with John Moffatt, Chief Financial Officer, Department of Economic Development, July 12, 2013.

29. In 2003, Governor Sonny Perdue recommended and the General Assembly enacted a tax increase on cigarettes

from 12 cents to 37 cents per pack.

30. Interviews with David Shafer, September 6, 2012 and April 17, 2013.

31. Alan Essig, Director of the Georgia Budget and Policy Institute and former state budget analyst said, “The idea

that they never look at existing programs is an old wives’ tale. I never believed that.” “1st Year of Zero-Based

Budgeting Impresses Some,” Available from: www.times-herald.com, Newnan, Georgia, March 21, 2012.

Lauth / ZBB Redux in Georgia 11

personnel funds to other purposes. He concedes that these other purposes may be worthy, but

believes they should not be funded in this hidden manner. State Representative Earl Ehrhart

characterized the new ZBB as primarily about drilling into the continuation budget, not about

building a budget from zero base. He said, ZBB asks “How do prior year priorities stand up with

today’s priorities? If they do, they may be continued, if they do not, they should be reduced or

eliminated and replaced with funding for new priorities.”32

Along with the Budget Report for the next fiscal year, the Governor and the OPB now present

to the General Assembly the Zero-Base Budget Report. To what extent is this appendix document

in play in the General Assembly appropriations process? The Georgia General Assembly meets

for only 40 legislative days.33 It has never adequately funded itself. Consequently, committees are

understaffed, theHouse and Senate Budget Offices are understaffed and individual members have

no staff. This staffing deficit is an impediment when it comes to incorporating ZBB into the

appropriations process.34 Representative Terry England, Chair of the House Appropriations

Committee, acknowledges that during the annual session of the General Assembly it is difficult

for the Appropriations Committee to focus on the Zero-Base Budgeting Report. Senator Jack Hill,

Chair of the Senate Appropriations Committee, noted that for his committee ZBB activity is

mostly in the off-season when sub-committees drill into agencies at the activity level, asking

questions about program activities or expenditure amounts, not during the session.

In summary, selected individuals in the Georgia General Assembly today are much more

enthusiastic about ZBB thanwere their counterparts in the 1970s (Lauth 1978). However, even today

ZBB remains primarily an executive branch budget activitywith the legislative branch cheering it on

but leaving most of the heavy lifting to the executive agencies and the Governor’s OPB.

ZERO-BASE BUDGETING OUTCOMES IN FY 2013 AND FY 2014

In FY 2013, 35 programs across 25 state agencies were subject to ZBB assessment. The

Governor’s OPB reported a total reduction of $8,890,376 for programs undergoing ZBB

assessment in FY 2013.35 An $8.9million reduction on a state budget of $19,244,924,133 is 0.046

percent; on a total budget of $38,716,320,572 it is 0.023 percent.36 Are these large reductions?

Probably not based upon the total or state budget, but based upon 10 percent of state programs

undergoingZBBassessment in that year, the reductions are not insignificant—1.49 percent for the

state budget ($595,713,989) and 0.868 percent for the total budget ($1,024,373,246).

32. Interview with Earl Ehrhart, Chair, Higher Education Sub-Committee, House Appropriations Committee,

April 29, 2013.

33. During the months of January–April.

34. Interview with Earl Ehrhart, Chair, Higher Education Sub-Committee, House Appropriations Committee,

April 29, 2013.

35. State of Georgia, Budget Report, FY 2013. p 44. This is a total of all reductions among programs designated for

ZBB review in that year, not a net reduction. Interview, David Tanner, Deputy Director, OPB, November 28, 2012.

36. It is common practice to reference the size of the Georgia budget as consisting of only state revenue and

appropriations, $19.2 billion in FY 2013. However, the total Georgia budget consisting also of federal and other

funds is approximately double in size, $38.7 billion in FY 2013.

12 Public Budgeting & Finance / Spring 2014

Of the 35 programs across 25 agencies undergoing ZBB assessment, 18 were increased in FY

2013 over FY 2012, nine had reductions in state funds, seven had reductions in federal37 and

other funds, and one remained the same.

In FY 2014, the Governor’s OPB did not report a total reduction for programs undergoing

ZBB assessment. In that year, 56 programs across 24 agencies were subject to ZBB assessment,

more than 40 percent of which (23) were programs within the Department of Education. In the

Department of Education, 11 of 23 programs were reduced in FY 2014 over FY 2013. Nine of

11 were reductions in state funds, one was a reduction from both state and total funds, and one

was a reduction from state funds but an increase in total funds. Ten of 23 programs were

increased in FY 2014 over 2013. Two of 23 programs had no change.

One might assume or expect that most programs undergoing ZBB assessment would be

reduced year over year. However, during Georgia’s first two years with the new ZBB the record

of reductions and increases is much more mixed. The OPB reported that some “key activity”

analysis may lead to funding increases.38 The Chair of the House Appropriations Committee

noted that some program increases resulted from the fact that programs were under-performing

because they were under-funded. Increased funding was intended to improve their performance.

He also noted that ZBB is not just about saving more money, but it also is about identifying

places to improve even if that means funding increases.39

It is difficult, if not impossible, to know for certain if the program reduction results reported

by the Governor’s OPB were directly attributable to ZBB review or if the program budget

analysis used in previous years would not have produced the same results. It is very likely that

some of the program reductions would have happened without ZBB. However, OPB believed it

was fair to claim any reductions that occurred in programs designated for zero-base

assessment.40

It is also possible that ZBB might have been able to claim even greater budget reductions had

it been in place in different economic times. The following observation was echoed by several

individuals close to the process.41 If ZBB had been introduced in good economic times such as

FY 2005 and FY 2006, greater budget reductions might have been realized. However, because

ZBBwas introduced shortly after the Great Recession, recession-driven budget cuts in FY 2008,

FY 2009, and FY 2010 had eliminated most of the slack in agency budgets. The low-hanging

fruit of suspected duplication or obsolescence was largely gone.

On the one hand, it is difficult to know precisely what budget reductions can be attributable to

ZBB, while on the other hand it is likely that in different economic circumstances claimed budget

reductions might have been somewhat greater.

37. Often, the termination of federal stimulus funding.

38. Interview with David Tanner, Deputy Director, OPB, August 1, 2012.

39. Interview with Terry England, Chair, House Appropriations Committee, April 22, 2013.

40. Interview with David Tanner, Deputy Director, OPB, November 28, 2012.

41. Interviewswith HenryM.Huckaby, Chancellor, University System of Georgia, August 10, 2012; David Tanner,

Deputy Director, OPB, November 28, 2012; Jack Hill, Chair, Senate Appropriations Committee, March 8, 2013;

Terry England, Chair, House Appropriations Committee, April 22, 2013; and John Moffatt, Chief Financial Officer,

Department of Economic Development, July 12, 2013.

Lauth / ZBB Redux in Georgia 13

MACRO- AND MICRO-LEVEL VIEWS OF COST SAVINGS

Draper and Pitsvada conclude in their 10-year study that zero-based budgeting is not successful

in dealingwith “uncontrollable” spending at the federal level or “mandated” spending at the state

level; it operates best where programs are discretionary (Draper and Pitsvada 1981).

Cost savings are likely to always be relatively small as long as ZBB activity focuses only on

programs and program activities that are easily changed in the annual budget cycle.42 However, the

big money in the state’s budget is found in the Department of Community Health (14 percent of the

total budget in FY 2013), Department of Corrections (6 percent in FY 2013), Department of

Education (37 percent in FY 2013), Board of Regents of the University System of Georgia (9

percent in FY 2013), and General Obligation Debt Service (6 percent in FY 2013).43 The core

programs of these agencies are largely off the table in the annual budget cycle except for their

administrative and ancillary activities. The Department of Community Health administers the

federal/state Medicaid program, including payments to Care Management Organizations for

services provided to the Medicaid population, and reimbursements to providers of hospital and

nursing home services. The Department of Corrections’ costs are driven largely by the size and

composition of the prison population, which is mostly a function of judicial sentencing policies and

practices. The Department of Education allocates the state’s Quality Basic Education (QBE) funds

to 180 local school districts and 17 charter schools. Only a one-time reduction or a permanent

change in the QBE funding formula would produce significant cost savings in this department. For

FY 2014, the Department of Education central office sustained the largest reduction while the QBE

formulawas increased. The Board of Regents of the University System funds the state’s 31 colleges

and universities through a lump-sum allocation (92 percent of its total budget in FY 2013) based

upon the state’s higher education funding formula. Similar to the Department of Education, only a

one-time reduction or a permanent change in the funding formula would produce significant cost

savings in this agency. General Obligation Debt Service is a legal obligation, totally insulated from

zero-based budgeting. In order to achieve significant cost savings from these big money agencies,

public policies as imbedded in statutory authority would have to be changed. ZBB focuses on

marginal “efficiencies,” and is highly unlikely to achieve major cost savings.

THE BOTTOM LINE

The principal impact of the newZBB has been a heightened analytical focus on programs that are

identified for zero-base review in a particular year. As seen in FY 2013, the first year of the new

ZBB, total cost reductions may be small but they have become symbolically important.

42. Thanks to Alan Essig, Executive Director, Georgia Budget and Policy Institute for bringing the following

discussion to my attention.

43. Totaling $14 billion in the FY 2013 budget of $19.3 billion, these agencies comprise 72 percent of the state’s

budget.

14 Public Budgeting & Finance / Spring 2014

Even though the nomenclature, “ZBB,” used to describe the current Georgia budget process is

the same as that used to describe the state’s budget process during the administration of Governor

Jimmy Carter in the 1970s, operationally the Carter-era and new ZBB are not the same. The

Carter-era ZBB had a unique and clearly defined terminology and set of procedures, whereas the

new ZBB relies mostly on existing performance-budget procedures. The Carter-era ZBB

purported to build the budget up from a zero base.44 The new ZBB is about drilling down into the

base or continuation budget. The Carter-era ZBB was a managerial process intended to achieve

efficiency and effectiveness. The new ZBB is more ideologically conservative with the aim of

cutting the budget and shrinking state government.45 Perhaps what the Carter-era and the new

ZBB have most in common is the symbol of “zero” in ZBB, signaling a budget cutting exercise

whether that exercise is in the service of management efficiency or fiscal conservatism.

ZBB is likely to continue in the Georgia budget process until all agencies are reviewed at least

once, before advocates lose interest or a new reform comes along. It is difficult to know whether

the claimed budget reductions are significant or not.46 They may be at the micro level, but they

probably are not at the macro level. However, it may not matter what cost reductions are actually

realized. The symbolic effect of the ZBB process is what is most important, confirming the fiscal

conservative bona fides of state government leaders.

IMPLICATIONS FOR OTHER GOVERNMENTS

A recent study by the National Conference of State Legislatures reported, “By the early 1980s,

use of the original form of ZBB had all but disappeared. States had developed a simplified form

of it to address the fiscal difficulties of the time, which omitted decision units, decision packages

and the numerous rankings required as the process moved through agencies,”(Snell 2012).

Another recent report by the Government Finance Officers Association concluded that “ZBB

systems that conform to the theoretical ideal are almost unheard of in present day financial

management,”(Government Finance Officers Association 2011). However, elements of ZBB are

incorporated into some local government budget systems. Further, the GFOA reported that

although interest in ZBB declined in the 1970s and 1980s there has been a resurgence of interest

in it since the Great Recession (2008–2009) as governments look for budget reducing techniques

that also signal that taxes and spending are being constrained.

In states or local governments where fiscal conservatives gain control of the levers of

government and seek ways to reduce taxes and spending they may look to ZBB as a device to

44. Even though, for the most part, it did not (see Lauth 1978).

45. When Governor Nathan Deal signed ZBB into law, Senator David Shafer thanked the following groups for

supporting the bill, Americans for Prosperity, Republican Liberty Caucus of Georgia, Libertarian Party of Georgia

andAtlanta Tea Party. “Shafer’s Zero-based Budgeting Bill Signed byGovernor,” camie.young@gwinnettdailypost.

com, May 9, 2012.

46. In a 1981 review of ZBB, Draper and Pitsvada based upon their review of federal, state and local government

experiences concluded, “… to the disappointment of its many advocates, ZBB, as a process, has not had a major

impact on reducing spending …” (Draper and Pitsvada 1981).

Lauth / ZBB Redux in Georgia 15

achieve those objectives. Their success will likely depend upon which elements of ZBB they

adopt and how they merge those elements with the existing budget system. Some financial

reductions may be realized, but as in Georgia, the symbolic benefit of “zero”may be as important

for fiscal conservatives as any actual budget reductions.

ACKNOWLEDGMENTS

Thanks to David Tanner, Associate Director of the Carl Vinson Institute of Government at the

University of Georgia and former Deputy Director of the Georgia OPB, Alan Essig, Executive

Director of the Georgia Budget and Policy Institute, and three anonymous reviewers for reading

an earlier version of this manuscript and making suggestions for its improvement. Of course,

they are not responsible for remaining imperfections.

REFERENCES

Bourdeaux, Carolyn. 2006. “Do Legislatures Matter in Budgetary Reform?” Public Budgeting & Finance. 26

(Spring): 120–142.

———. 2008. “The Problems with Programs:Multiple Perspectives on Program Structures in Program-Based

Performance-Oriented Budgets.” Public Budgeting & Finance. 28 (Summer): 20–47.

Budgeting and Accounting Act of 1921, PL 67-13.

Comptroller General of the United States. 1979. “Streamlining Zero-Base Budgeting Will Benefit Decision

Making.” PAD-79-45.

———. 1980. “Budget Formulation: Many Approaches Work But Some Improvements Are Needed.” PAD-

80-31.

Congressional Budget and Impoundment Control Act of 1974, PL 104-4.

Draper, Frank D. and Bernard T. Pitsvada. 1978.A First Year’s Assessment of ZBB in the Federal Government

—Another View. Arlington, VA: Association of Government Accountants.

———. 1980. “Congress and Executive Branch Budget Reform: The House Appropriations Committee and

Zero-Base Budgeting.” International Journal of Public Administration. 2 (3): 331–374.

———. 1981. “ZBB—Looking Back After Ten Years.” Public Administration Review. 41 (January/

February): 76–83.

Government Finance Officers Association. 2011. Zero-Base Budgeting: Modern Experiences and Current

Perspectives. Chicago, IL: Government Finance Officers Association.

Huckaby, Henry M. and Thomas P. Lauth. 1998. “Budget Redirection in Georgia State Government.” Public

Budgeting &Finance. 18 (Winter): 36–44.

Kelly, Janet M. and William C. Rivenbark. 2003. Performance Budgeting for State and Local Government.

Armonk, NY: M.E. Sharpe.

Lauth, Thomas P. 1978. “Zero-Base Budgeting in Georgia State Government: Myth and Reality.” Public

Administration Review. 38 (September/October): 420–430.

———. 1997. “Zero-Base Budgeting.” In The International Encyclopedia of Public Policy and

Administration. edited by Jay Shafritz, 2429–2431. Boulder, CO: Westview Press.

———. 2006. “Georgia: Shared Power and Fiscal Conservatism.” In Budgeting in the States: Institutions,

Processes and Politics. edited by Edward J. Clynch and Thomas P. Lauth, 33–53 at 33–35.Westport, CT:

Praeger Publishers.

———. 2010. “Budget Deficits in the States: Georgia.” Public Budgeting & Finance. 30 (Spring): 15–32 at

25–29.

16 Public Budgeting & Finance / Spring 2014

Lauth, Thomas P. and Steven C. Reick. 1979. “Modifications in Georgia Zero-Base Budgeting Procedures:

1973–1980.” Midwest Review of Public Administration. 13 (December): 225–258.

Lee, Robert D. 1997. “A Quarter Century of State Budgeting Practices.” Public Administration Review. 57

(March/April): 133–140.

Lee, Robert D. and Raymond J. Staffeld. 1977. “Executive and Legislative Use of Policy Analysis in the State

Budgeting Process: Survey Results.” Policy Analysis. 3 (Summer): 395–405.

Lindblom, Charles E. 1959. “The Science of ‘Muddling Through’.” Public Administration Review. 19

(Spring): 79–88.

———. 1979. “Still Muddling, Not Yet Through.”Public Administration Review. 39 (November/December):

517–526.

Melkers, Julia E. and Katherine G.Willoughby. 1998. “The State of the States: Performance-Based Budgeting

Requirements in 47 Out of 50.” Public Administration Review. 58 (January/February): 66–75.

———. 2001. “Budgeters’ Views of State Performance-Budgeting Systems: Distinctions Across Branches.”

Public Administration Review. 61 (January/February): 54–64.

Mikesell, John L. 2003. Fiscal Administration: Analysis and Applications for the Public Sector, 206–217.

Belmont, CA: Wadsworth Publications.

Moore, Perry. 1980. “Zero-Base Budgeting in American Cities.” Public Administration Review. 40 (May/

June): 253–258.

Newland, Chester A. 1983. “A Mid-Term Appraisal—The Reagan Presidency: Limited Government and

Political Administration.” Public Administration Review. 43 (January/February): 1–21 at 13.

Office of Planning and Budget. 2011. General Budget Preparation Procedures for Prioritized Program

Budgets, Amended Fiscal Year 2012 and Fiscal Year 2013. July 25, 2011.

———. 2012. Procedures for Zero Based Budget Analysis, Fiscal Year 2014. May 4, 2012.

Official Code of Georgia Annotated. O.C.G.A. 45-12-75. 1.

Pyhrr, Peter A. 1970. “Zero-Base Budgeting.” Harvard Business Review. 49 (November/December): 111–

121.

———. 1973. Zero-Base Budgeting: A Practical Management Tool for Evaluating Expenses. NewYork, NY:

John Wiley and Sons, Inc.

———. 1977. “The Zero-Base Approach to Government Budgeting.” Public Administration Review, 37

(January/February): 1–8.

Rabin, Jack, editor. 1987. “Budgeting for Improved Productivity.” Public Productivity Review. 41 (Spring):

1–71.

Schick, Allen. 1966. “The Road to PPB: The Status of Budget Reform.” Public Administration Review. 26

(December): 243–258.

———. 1971. Budget Innovations in the States. Washington, DC: The Brookings Institution.

———. 1979. Zero-Base 80: The Status of Zero-Base Budgeting in the States. Washington, DC: National

Association of State Budget Officers and the Urban Institute.

Snell, Ronald. 2012. “NCSL Brief: Zero-Base Budgeting in the States.” National Conference of State

Legislatures. (January): 3.

Willoughby, Katherine G. 2004. “Performance Measurement and Budget Balancing: State Government

Perspective.” Public Budgeting & Finance. 24 (Summer): 21–39.

Willoughby, Katherine G. and Julia E. Melkers. 2000. “Implementing PBB: Conflicting Views of Success.”

Public Budgeting & Finance. 20 (Spring): 105–120.

Lauth / ZBB Redux in Georgia 17