Embed Size (px)

Citation preview

1

THE EFFECT OF EARNINGS GROWTH ON THE MARKET

REACTION TO DIVIDEND CHANGE ANNOUNCEMENTS:

CASE FROM INDONESIAN PUBLIC FIRM IN 2009-2013

Yudha Putra Hima

Pratiwi Budiharta

International Financial Accounting Program

Faculty of Economics

University of Atma Jaya Yogyakarta

Babarsari Street No. 43 – 44 Yogyakarta

ABSTRACT

The purpose of this research is a consideration for stockholders in

economic decisions to buy, sell or hold the stock on the dividend change

which is considered to have information content. The population in this

research are all companies listed and issue shares on the Indonesia Stock

Exchange (IDX) 2009-2013. For hyphothesis testing methods of analysis

using multiple linear regression with SPSS program.

Result for the hyphothesis is earnings growth doesn’t moderate the

relationship between dividend change announcements and the market

reaction. It indicates that earnings growth is not informative enough to

affect the relationship between dividend change announcements and the

market reaction. This can be caused by operating cashflow information is

superior to earnings growth and the act of income smoothing.

Keywords: Dividend Signalling Theory, Dividend Change

Announcements, Market Reaction, Earnings Growth.

2

1. Research Background

Bhattacharya (1979), who developed the dividend signaling theory

states that the company uses a dividend announcement as a signal about

the company's prospects. In dividends, the company would require

sufficient cash that the company's liquidity is not disturbed. Markets tend

to interpret the company making the increase distribution as companies

that have good prospects and liquidity, because it is able to maintain the

amount of dividends paid even able to pay dividends higher than the last

period. Instead, the market tends to interpret the company making the

decreases distribution as the company has bad prospects and less liquidity,

and unable to retain the amount of the dividends.

Basis of the signaling theory is information asymmetry which

exists on market and represents an unequal access to information between

managers and stockholders. Signaling theory is possible solution for

hidden information problem. Hidden information problem presents the

situation in which manager is in the advantage because having hidden

information that stockholders don’t have and having the possibility to hide

information. The presumption from this theory is based on the possibility

of reducing information asymmetry by dividends which are used by

insiders when they want to signal company situation.

A vast number of empirical studies found evidence supporting the

dividend signalling hypothesis, such as Pettit (1972, 1976), Aharony and

Swary (1980), Asquith and Mullins (1983), Dhillon and Johnson (1994),

Lee and Ryan (2000, 2002), Hussin et al. (2010), Yilmaz and Selcuk

(2010) and Jiang and Stark (2011), among others. However, some authors

found no evidence of a significant market reaction to dividend change

announcements, suggesting that dividend announcements does not convey

valuable information to the market, contrary to the content information

dividend hypothesis (Lang and Litzenberger, 1989; Benartzi et al., 1997;

Conroy et al., 2000; Chen et al., 2002; Abeyratna and Power, 2002; Fu

and Morgan, 2008; Ali and Chowdhury, 2010 and Asamoah, 2010).

Several authors have documented a relationship between market

share price reaction to dividend change announcements and firm-specific

factors (Asquith and Mullins, 1983; Ghosh and Woolridge, 1988; Eddy

and Seifert, 1988; Haw and Kim, 1991; Mitra and Owers, 1995; Healy et

al., 1997 and Malkawi, 2008). Viera (2011), tries to identify firm-specific

factors include firm size, dividend changes, earnings growth, market to

book ratio, price/earnings ratio and the debt/equity ratio that contribute to

explain the market reaction to dividend change announcements, using data

from three different European countries.

Lintner (1956) and Fama and Babiak (1968) have found a

relationship between dividend and earnings consistent with the hypothesis

that companies which paid out dividend, increase the dividend only when

management is convinced that it can be sustained in the future. The

managers intentionally or unintentionally portray the message to external

investor about the pattern of firm’s future earnings and value by

announcement of cash dividends (Miller & Modigliani, 1961). In the

Conroy et al. (2000), the study pricing effects of dividend and earnings

3

announcements by taking advantage of the unique setting in Japan where

managers simultaneously announce the current year's dividends and

earnings as well as forecasts of next year's dividends and earnings.

Research on the information content of earnings has been done by

many researchers. Research that examine the market reaction to earnings

announcement proved that earnings announcement has information

content. The reaction is reflected in the rise and fall of stock prices and

trading volume around the announcement date (Ball and Brown, 1968;

Bamber and Cheon, 1995). While research in Indonesia also proved that

earnings publication contained in the financial statements response by the

market in the announcements period (Utami and Suharmadi, 1998;

Hidayat and Manao, 2000; Lako, 2003; Telaumbanua and Sumiyana,

2006).

Based on the explanation above, this research attempts to evaluate

the effect of the dividend change announcement to the market reaction

with earnings growth as moderating variabel, in the Indonesian stock

market firms.

2. Research Problem

Based on the background above, the problem to be studied is formulated

as follows: Does earnings growth moderate the relationship between dividend

change announcements with the market reaction ?

3. Previous Research and Hyphothesis Development

Results of several research on earnings growth says that earnings

increase information responded more positively than earnings decrease

information (Ball and Brown, 1968; Foster, 1977; Hayn, 1995). This

means that the higher earnings the higher response. However, the results

above contradict with other research results that says earnings decrease

information in the market reacted as good news while earnings decrease

information reacted as bad news (Lako, 2003; Telaumbanua and

Sumiyana, 2006).

In the Conroy et al. (2000) research, the study pricing effects of

dividend and earnings announcements by taking advantage of the unique

setting in Japan where managers simultaneously announce the current

year's dividends and earnings as well as forecasts of next year's dividends

and earnings.

Lintner (1956) and Fama and Babiak (1968) have found a

relationship between dividend and earnings consistent with the hypothesis

that companies which paid out dividend, increase the dividend only when

management is convinced that it can be sustained in the future. Past

earnings is a determinant of dividend policy (Lintner, 1956). Thus, from

that previous research it can be concluded that earnings growth amount is

a predictor of the market reaction to dividend change announcements.

Earnings growth is computed as the average earnings growth rate based on

the year prior to the dividend change year (Viera, 2011). Therefore, it

expected that the coefficient have a positive signal as moderating variabel:

4

Ha: Earnings growth positively moderates the effect of dividend

change towards market reaction.

4. Research Variable and Operational Definition

4.1 Research Variable

The dependent variable in this research is the market reaction of

dividend change announcements received by shareholders of companies

listed on Indonesia stock exchange in 2009 until 2013. The market

reaction is calculated with abnormal returns. The independent variable in

this research is the percentage change of dividends while the moderating

variable is earnings growth.

1. Dependent Variable

Dependent variable in this research using the market reaction.

Market reaction can be calculated by cumulative abnormal return.

Some research on the event study use the accumulated abnormal return

called cumulative abnormal return (CAR). CAR is using the sum of

previous day’s abnormal return in the event period for each of the

securities. This research using total abnormal return from t-3 » t+3 with

t0 being the event date of dividend announcement (7 days).

CAR formula is as follows, Hartono (2010):

∑

Where,

Note:

CAR = Accumulated abnormal return from t-3 to t+3

AR = Abnormal return

Rt = Realized return t period

(E)Rt = Expected return t period

Pt = Closing price t period

Pt-1 = Closing price t-1 period

JKSEt = Market index return t period

JKSEt-1 = Market index return t-1 period

2. Independent Variable

Independent variable in this research is percentage change of dividends

(PCD). PCD is defined as the change in dividends divided by dividend

in the previous year (Choi, 2011).

Note:

Dt = Dividend that announce in the current year

Dt-1 = Dividend that announce in the previous year

5

3. Moderating Variable

The last is moderating variable using earnings growth (EG). EG is

computed as the average earnings growth rate based on the year prior

to the dividend change year (Viera, 2011). This research using

earnings after tax (EAT) or in the financial statement called net income

after tax.

Note:

EATt-1 = Earning after tax previous year

EATt-2 = Earning after tax two years ago

5. Hyphothesis Testing

Methods of analysis using multiple linear regression with SPSS program.

The first and second hypothesis tested with regression equation:

Y = a + b1.X1 + b2.X2 + b3.X1.X2 + e Note:

Y = Cumulative abnormal return

a = Constanta

b1, b2, & b3 = Regression coefficient

X1 = Percentage change of dividends (PCD)

X2 = Earning growth (EG)

X1.X2 = Interaction between PCD & EG

e = Residual error

Decision making in this research based on the hypothesis is:

Ho : Earnings growth doesn’t positively moderate the effect of dividend

change toward market reaction.

Ha : Earnings growth positively moderates the effect of dividend change

toward market reaction.

Using the significant value of Ghozali (2005), for hyphothesis :

a. The significance value ≥ 5%, Ha rejected

b. The significance value < 5%, b3 positive, Ha accepted

6. Results

Hypothesis test in this research using multiple linear regression

with significance value of 0.05. Hypothesis test results contained in Table

IV.7, as well as the complete data results of hypothesis test contained in

appendix 9.

6

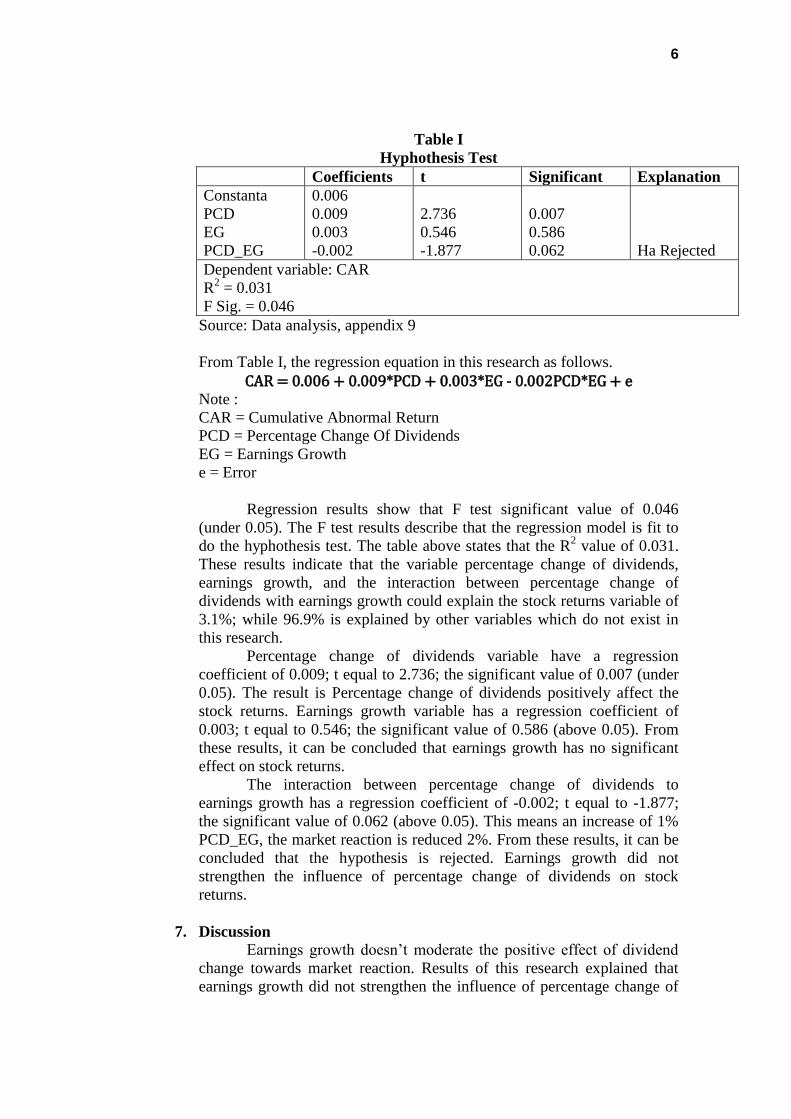

Table I

Hyphothesis Test

Coefficients t Significant Explanation

Constanta

PCD

EG

PCD_EG

0.006

0.009

0.003

-0.002

2.736

0.546

-1.877

0.007

0.586

0.062

Ha Rejected

Dependent variable: CAR

R2 = 0.031

F Sig. = 0.046

Source: Data analysis, appendix 9

From Table I, the regression equation in this research as follows.

CAR = 0.006 + 0.009*PCD + 0.003*EG - 0.002PCD*EG + e Note :

CAR = Cumulative Abnormal Return

PCD = Percentage Change Of Dividends

EG = Earnings Growth

e = Error

Regression results show that F test significant value of 0.046

(under 0.05). The F test results describe that the regression model is fit to

do the hyphothesis test. The table above states that the R2 value of 0.031.

These results indicate that the variable percentage change of dividends,

earnings growth, and the interaction between percentage change of

dividends with earnings growth could explain the stock returns variable of

3.1%; while 96.9% is explained by other variables which do not exist in

this research.

Percentage change of dividends variable have a regression

coefficient of 0.009; t equal to 2.736; the significant value of 0.007 (under

0.05). The result is Percentage change of dividends positively affect the

stock returns. Earnings growth variable has a regression coefficient of

0.003; t equal to 0.546; the significant value of 0.586 (above 0.05). From

these results, it can be concluded that earnings growth has no significant

effect on stock returns.

The interaction between percentage change of dividends to

earnings growth has a regression coefficient of -0.002; t equal to -1.877;

the significant value of 0.062 (above 0.05). This means an increase of 1%

PCD_EG, the market reaction is reduced 2%. From these results, it can be

concluded that the hypothesis is rejected. Earnings growth did not

strengthen the influence of percentage change of dividends on stock

returns.

7. Discussion

Earnings growth doesn’t moderate the positive effect of dividend

change towards market reaction. Results of this research explained that

earnings growth did not strengthen the influence of percentage change of

7

dividends on stock returns. Results of this research are not consistent with

the results of Lintner (1956) and Fama and Babiak (1968).

Explanation of earnings growth did not strengthen the influence of

percentage change of dividends on stock returns is similiar to that of

Manurung (2009), which examines whether the net income and operating

cash flows affect the dividend policy. The results obtained from this

research showed that partially net income has no effect on dividend policy.

It indicates that the net income is not the main element that need to be

considered and used as good benchmark by management in making the

decision to determine the amount of the dividend. It support that the

amount of the dividend is the excess funds from operating activities over

investment needs to generate profits in the future. So, it can be concluded

that the earnings growth is not a variable that can affect the dividend

change announcements against stock returns because to pay cash

dividends needed cash. The company's operating cash flow as an indicator

can know whether company has enough cash to pay cash dividends or not.

Another reason is the profit generated by the company is a result of

engineering by the management (income smoothing) to attract investors.

Based on calculations using Eckel index (Eckel, 1981) there are 19

companies or 33% of total sample that are indicated to income smoothing.

For example based on earnings in 2007 and 2008 ADHI company

experienced 27% decrease in earnings. Based on eckel index ADHI

company indicated doing income smoothing. This means that the earnings

have been manipulated to smooth earnings reported in 5 years, so earnings

reported is not fluctuative. Because of earnings reported have been

manipulated, earnings growth did not moderate the effect of dividend

change toward market reaction. In the result of the statistical test, earnings

growth negatively moderates the relationship between dividend change

and market reaction, if using 10% significant level. This proves that

manipulated earnings has a negative market reaction.

8. Conclusions

8.1 Conclusions

Based on the analysis perform on chapter IV, it can be concluded

that earnings growth doesn’t moderate the relationship between dividend

change announcements and the market reaction. It indicates that earnings

growth is not informative enough to affect the relationship between

dividend change announcements and the market reaction. This can be

caused by operating cashflow information is superior to earnings growth

and the act of income smoothing.

8.2 Limitations and Suggestions

This research has several limitations. Several suggestions are also

made for future research.

Limitation:

1. Limitation in this research is the researcher did not consider the

operating cash flow variable that moderating the relationship

between percentage change of dividends and the market reaction.

8

2. Researcher did not consider companies that perform income

smoothing and companies that do not perform income smoothing

in moderating the relationship between percentage change of

dividends and the market reaction.

Suggestion: 1. For other researchers who want to research the similiar topic is

strongly recommended consider operating cash flow as a variable

that may moderate the relationship between percentage change of

dividends and the market reaction.

2. For other researchers who want to research the similiar topic is

strongly recommended consider the income smoothing in the

calculation of earnings growth that moderating the relationship

between percentage change of dividends and the market reaction. It

is expected to provide better evidence in the future research.

9

REFERENCES

Abeyratna, G., & Power, D. M. 2002. The Post-announcement Performance of

Dividend-changing Companies: The Dividend-signalling Hypothesis

Revisited. Accounting and Finance 42:131-151.

Aharony, J., & Swary, I. 1980. Quarterly Dividend and Earnings Announcements

and Stockholders Returns: An Empirical Analysis. The Journal of Finance

35 (1):1-12.

Ali, M. B., & Chowdhury, T. A. 2010. Effect of Dividend on Stock Price in

Emerging Stock Market: A Study on the Listed Private Commercial Banks

in DSE. International Journal of Economics and Finance 2 (4):52-64.

Algifari. 2000. Analisis Regresi, Teori, Kasus & Solusi. BPFE UGM, Yogyakarta.

Ang, Robbert. 1997. Buku Pintar Pasar Modal Indonesia. Edisi Pertama,

Mediasoft Indonesia.

Asamoah, G. N. 2010. The Impact of Dividend Announcement on Share Price

Behaviour in Ghana. Journal of Business & Economics Research 8 (4):47-

58.

Asquith, P., & Mullins, D. W. 1983. The Impact of Initiating Dividend Payments

on Shareholder Wealth. The Journal of Business 56 (1):77-96.

Ball, R., And Brown, P. 1968. An Empirical Evaluation of Accounting Income

Numbers. Journal of Accounting Research Autumn 159-178.

Bamber, Linda, Smith and Youngsoon Susan Cheon. 1995. Differential Price and

Volume Reactions to Accounting Earnings Announcements. Accounting

Review 417-441.

Benartzi, S., Michaely, R., & Thaler, R. 1997. Do Changes in Dividends Signal

the Future or the Past?. The Journal of Finance 52 (3):1007-1034.

Bhattacharya, S. 1979. Imperfect Information, Dividend Policy, and “The Bird in

the Hand” Fallacy. The Bell Journal of Economics 10 (1):259-270.

Brigham & Weston. 1998. Dasar-dasar Manajemen Keuangan penerjemah Ali

Akbar Yulianto. Salemba Empat. Jakarta.

Briloff, A.J. 1972. Unaccountable Accounting. Harper & Row. New York.

Brown, S., and J. Warner. 1985. Using Daily Stock Returns: The Case of Event

Studies. Journal of Financial Economics 14:3-31.

Chen, G., Firth, M., & Gao, N. 2002. The Information Content of Concurrently

Announced Earnings, Cash Dividends, and Stock Dividends: An

Investigation of the Chinese Stock Market. Journal of International

Financial Management & Accounting 13 (2):101-124.

Choi, Y. M., Ju, H. K. and Park, Y. K. 2011. Do dividend changes predict the

future profitability of firms?. Accounting & Finance 51.

Conroy, R. M., Eades, K. M., & Harris, R. S. 2000. A Test of the Relative Pricing

Effects of Dividends and Earnings: Evidence from Simultaneous

Announcements in Japan. The Journal of Finance 55 (3):1199-1227.

Cooper, M., Dimitrov, O., Rau, P. 2001. A Rose.com by Any Other Name.

Journal of Finance 56.

Dhillon, U. S., & Johnson, H. 1994. The Effect of Dividend Changes on Stock

10

and Bond Prices. The Journal of Finance 49 (1):281-289.

Eckel, N. 1981. The Income Smoothing Hypothesis Revisited. Abacus 17 (1):28-

40.

Eddy, A., & Seifert, B. 1988. Firm Size and Dividend Announcements. The

Journal of Financial Research 11 (4):295-302.

Endri. 2010. Keterkaitan Pasar Saham Berkembang dan Maju:Implikasi

Diversifikasi Portofolio Internasional. Journal Elektronik Universitas

Gunadarma 15 (2).

Fama, E. F. 1970. Efficient Capital Markets: A Review of Theory and Empirical

Work. The Journal of Finance 25 (2):383-417.

Fama, Eugene F., and Harvey Babiak. 1968. Dividend policy: an empirical

analysis. Journal of the American Statistical Association 63 1132-1161.

Foster, G. 1977. Accounting Earnings and Stock Prices of Insurances Companies.

The Accounting Review October 686-698.

Fu, Y., and Morgan, H. 2008. Dividend Policy and the Signalling Hypothesis: Is

the Signalling Hypothesis Still Alive?, working paper available at

http://www.sfu.ca/~hmorgan/sigallinghypothesis-HM,Yufen-

spring2008.pdf.

Ghosh, C., & Woolridge, J. R. 1988. An Analysis of Shareholder Reaction to

Dividend Cuts and Omissions?. The Journal of Financial Research 11 (4):

281- 294.

Ghozali, Imam. 2005. Aplikasi Analisis Multivariate dengan program SPSS.

Badan Penerbit Universitas Diponegoro. Semarang.

Gordon, M. J. 1963. Optimal Investment and Financing Policy. Journal of

Finance May 264-272.

Hartono. Jogiyanto. 2010. Metodologi Penelitian Bisnis: Salah Kaprah dan

Pengalaman-Pengalaman. Edisi 6. BPFE. Yogyakarta.

Hartono. Jogiyanto. 2010. Teori Portofolio dan Analisis. Edisi Ketujuh. Cetakan

Pertama. BPFE. Yogyakarta.

Haw, I., & Kim, W. 1991. Firm Size and Dividend Announcement Effect. Journal

of Accounting, Auditing and Finance 6 (3):325-347.

Hayn, C. 1995. The Information Content of Losses. Journal of Accounting and

Economics Vol LIX October 574-603.

Healy, J., Hathorn, J., & Kirch, D. 1997. Earnings and the Differential

Information Content of Initial Dividend Announcements. Accounting

Enquiries 6 (2):187-220.

Healy, P. M., & Palepu, K. G. 1988. Earnings Information Conveyed by Dividend

Initiations and Omissions. Journal of Financial Economics 21:149-175.

Hendriksen, E. S., & Van, B. M. F. 1992. Accounting Theory. Irwin. Homewood,

IL.

Hidayat, H., and Manao, H. 2000. Asosiasi Laba Tahunan Emiten dengan Harga

Saham ditinjau dari Ukuran dan Debt-Equity Ratio Perusahaan.

Simposium Nasional Akuntansi III 522-536.

11

Hussin, B. M., Ahmed, A. D., & Ying, T. C. 2010. Semi-strong Form Efficiency:

Market Reaction to Dividend and Earnings Announcements in Malaysian

Stock Exchange. The IUP Journal of Applied Finance 16 (5):36-60.

Jiang, W. & Stark, A. 2011. Dividends, Accounting Information, and the

Valuation of Loss-Making Firms in the UK. Working Paper. Available at

SSRN: http://ssrn.com/abstract=1734287.

Jin, Z. (2000). On The Differential Market Reaction To Dividend Inititions. The

Quarterly Review of Economics and Finance 12:263-277.

Jones, Charles P,. 2010. Investments Principles and Concepts. 11th Edition. North

Carolina State University.

Kartini. 2001. Analisis Reaksi Pemegang Saham Terhadap Pengumuman

Perubahan Pembayaran Dividen di Bursa Efek Jakarta. Jurnal Siasat

Bisnis No.6 Vol.2.

Lako, A. 2003. Anomali Reaksi Investor terhadap Pengumuman Laba Good

News dan Laba Bad News Bukti Empiris dari Bursa Efek Indonesia.

Usahawan No. 02. Th. XXXII. Februari 2003 3-12.

Lang, L. H. P., & Litzenberger, R. H. 1989. Dividend Announcements: Cash Flow

Signalling Versus Free Cash Flow Hypothesis. Journal of Financial

Economics 24 (1):181-191.

Lee, H. W., & Ryan, P. A. 2002. Dividends and Earnings Revisited: Cause or

Effect?. American Business Review 20 (1):117-122.

Lee, H. W., & Ryan, P. A. 2000. The Information Content of Dividend Initiations

and Omissions: The Free Cash Flow and Dividend Signalling Hypotheses.

The Journal of Research in Finance 3 (2):196-277.

Lintner, J. 1962. Dividends, Earnings, Leverage, Stock Prices, and the Supply of

Capital to Corporations. Review of Economics and Statistics August pp.

243-269.

Lintner, J. 1956. Distribution of Incomes of Corporations among Dividends,

Retained Earnings and Taxes. The American Economic Review 46 (2):97-

113.

Litzenberger, R. H. and K, Ramaswamy. 1979. The Effects of Personal Taxes and

Dividends on Capital Asset Prices: Theory and Empirical Evidence.

Journal of Financial Economics 7:163-195.

Malkawi, H. 2008. Factors Influencing Corporate Dividend Decision: Evidence

from Jordanian Panel Data. International Journal of Business 13 (2):177-

195.

Manurung, Indah Agustina. 2009. Pengaruh Laba Bersih dan Arus Kas Operasi

terhadap Kebijakan Dividen. Jurnal Akuntansi 3. Universitas Sumatera

Utara.

Miller, M. H., & Modigliani, F. 1961. Dividend Policy, Growth, and The

Valuation of Shares. The Journal of Business 34:411-433.

Mitra, D., & Owers, J. E. 1995. Dividend initiation announcement effects and the

firm's information environment. Journal of Business Finance &

Accounting 22 (4):551-573.

Pettit, R. 1976. The Impact of Dividends and Earnings Announcements: A

Reconciliation. The Journal of Business 49 (1):86-96.

Pettit, R. 1972. Dividend Announcements, Security Performance, and Capital

Market Efficiency. The Journal of Finance 27 (5):993-1007.

12

Sekaran, Uma. 1992. Research Methods For Business: A Skill Building Approach.

Second Edition. John Willey & Sons, Inc. New York.

Sugiyono. 2004. Metode Penelitian Bisnis: Penerbit CV. Alfabeta. Bandung.

Sularso, R. A. 2003. Pengaruh Pengumuman Dividen terhadap Perubahan Harga

Saham (Return) Sebelum dan Sesudah Ex-Dividend Date di Bursa Efek

Jakarta (BEJ). Jurnal Akuntansi dan Keuangan Vol. 5 No. 1.

Suliyono, Joko. 2010. 6 Hari Jago SPSS. Yogyakarta: Cakrawala.

Telaumbanua, Binsar. I. K., and Sumiyana. 2006. Event Study: Pengumuman

Laba Terhadap Reaksi Pasar Modal. Universitas Gajah Mada.

Utami, W., and Suharmadi. 1998. Pengaruh Informasi Penghasilan terhadap

Harga Saham di Bursa Efek Indonesia. Jurnal Riset Akuntansi Indonesia

Vol. 1 No. 2 July 255-268.

Viera, Elisabete. S. 2011. Firm-Specific Factors and The Market Reaction To

Dividend Change Announcements: Evidence From Europe. Marmara

Journal of European Studies Volume 19 (1).

Widarjono. 2010. Analisis Statistika Multivariat Terapan. Penerbit UPP STIM

YPKN. Yogyakarta.

Yilmaz, A. A., & Selcuk, E. A. 2010. Information Content of Dividends:

Evidence from Istanbul Stock Exchange. International Business Research

3 (3):126-132.

Website Source

http://en.wikipedia.org/wiki/Earnings_growth

http://en.wikipedia.org/wiki/Indonesia_Stock_Exchange

http://finance.yahoo.com/q?s=^JKSE

http://id.wikipedia.org/wiki/Indeks_Harga_Saham_Gabungan

http://www.idx.co.id/index-En.html