Embed Size (px)

DESCRIPTION

Insurance

Citation preview

1. Introduction

1.1 Insurance Industry Insurance is one of the oldest and most wide spread financial services across the globe. In 200, global

insurance premiums exceeded $4 trillion. With the advent of information technology and high speed

communication, the insurance products are being sold almost everywhere in the world. Increasing

affluence, especially in developing countries, and a rising understanding of the need to protect wealth

and human capital has led to significant growth in the insurance industry.

Given the evolving and growing socio-economic conditions worldwide, insurance companies are

increasingly reaching out across borders and are offering more competitive and customized products

than ever before. Over the past ten years, global insurance premiums have risen by more than 50%,

with annual growth rates ranging between 2 and 10%. The majority of insurance comes from developed

nations such as most of Europe, the US, and Japan. In 2007, premiums in North American amounted to

$1,330 billion, while the European Union generated $1,681 billion, and Asia produced $814 billion.

Emerging markets accounted for over 85% of the world’s population but generated only around 10% of

premiums.

1.2 Claims Processing Management Claims and loss handling is the materialized utility of insurance; it is the actual "product" paid for,

though one hopes it will never need to be used. Claims management is the most important client

interaction and business process for the insurance industry. It has huge impact on profitability and

financial health of the organization. Claims expenditure is the biggest cost head for any insurance

provider and is used in most of the business health indicators. With nearly 80 percent of premium

income spent on claims and claims related processing costs, insurers seek ways to streamline processes

while improving customer service. Speedy and hassle free claims settlement is not only desired but is

essential for survival in today’s highly competitive business environment. But, this is restricted by the

requirement of fraud detection to keep premiums competitive. Thus, in managing the claims handling

function, insurers seek to balance the elements of customer satisfaction, administrative handling

expenses, and claims overpayment leakages. As part of this balancing act, fraudulent insurance practices

are a major business risk that must be managed and overcome. Disputes between insurers and insureds

over the validity of claims or claims handling practices occasionally escalate into litigation; see insurance

bad faith.

2. Claims Processes Claims may be filed by insureds directly with the insurer or through brokers or agents. The insurer may

require that the claim be filed on its own proprietary forms, or may accept claims on a standard industry

form such as those produced by ACORD. Insurance company claim departments employ a large number

of claims adjusters supported by a staff of records management and data entry clerks. Incoming claims

are classified based on severity and are assigned to adjusters whose settlement authority varies with

their knowledge and experience. The adjuster undertakes a thorough investigation of each claim, usually

in close cooperation with the insured, determines its reasonable monetary value, and authorizes

payment. Adjusting liability insurance claims is particularly difficult because there is a third party

involved (the plaintiff who is suing the insured) who is under no contractual obligation to cooperate with

the insurer and in fact may regard the insurer as a deep pocket. The adjuster must obtain legal counsel

for the insured (either inside "house" counsel or outside "panel" counsel), monitor litigation that may

take years to complete, and appear in person or over the telephone with settlement authority at a

mandatory settlement conference when requested by the judge.

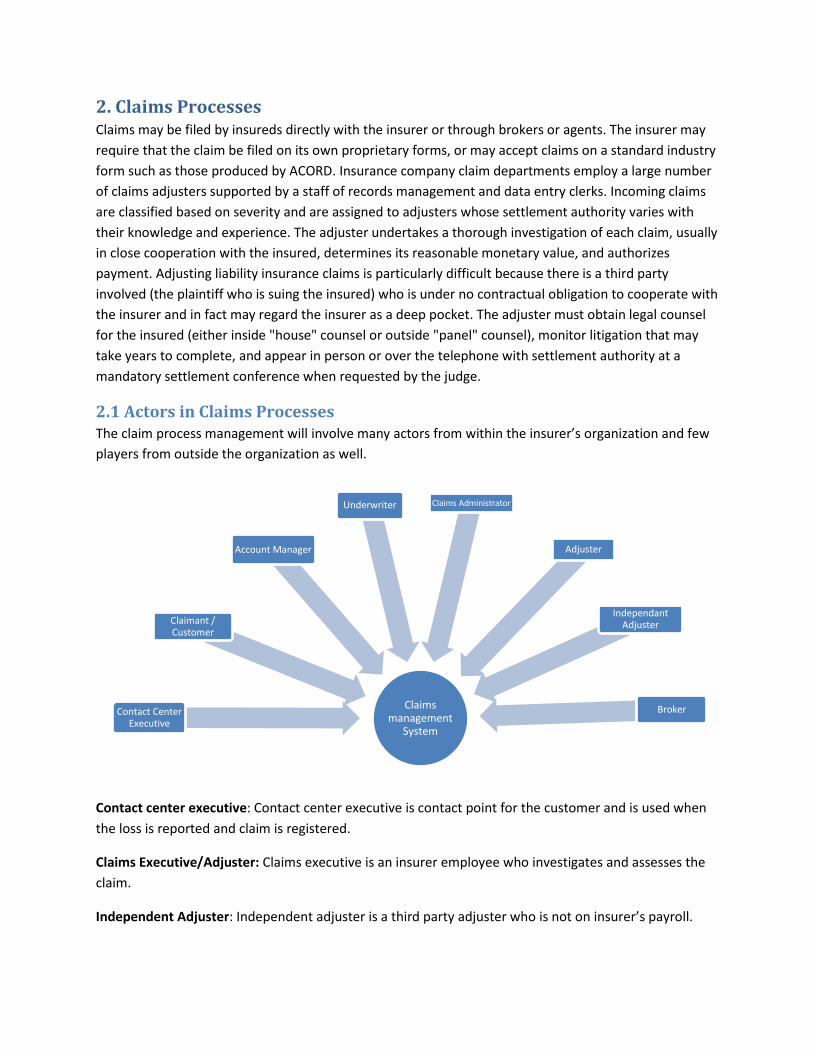

2.1 Actors in Claims Processes The claim process management will involve many actors from within the insurer’s organization and few

players from outside the organization as well.

Contact center executive: Contact center executive is contact point for the customer and is used when

the loss is reported and claim is registered.

Claims Executive/Adjuster: Claims executive is an insurer employee who investigates and assesses the

claim.

Independent Adjuster: Independent adjuster is a third party adjuster who is not on insurer’s payroll.

Claims management

System

Contact Center Executive

Claimant / Customer

Account Manager

Underwriter Claims Administrator

Adjuster

Independant Adjuster

Broker

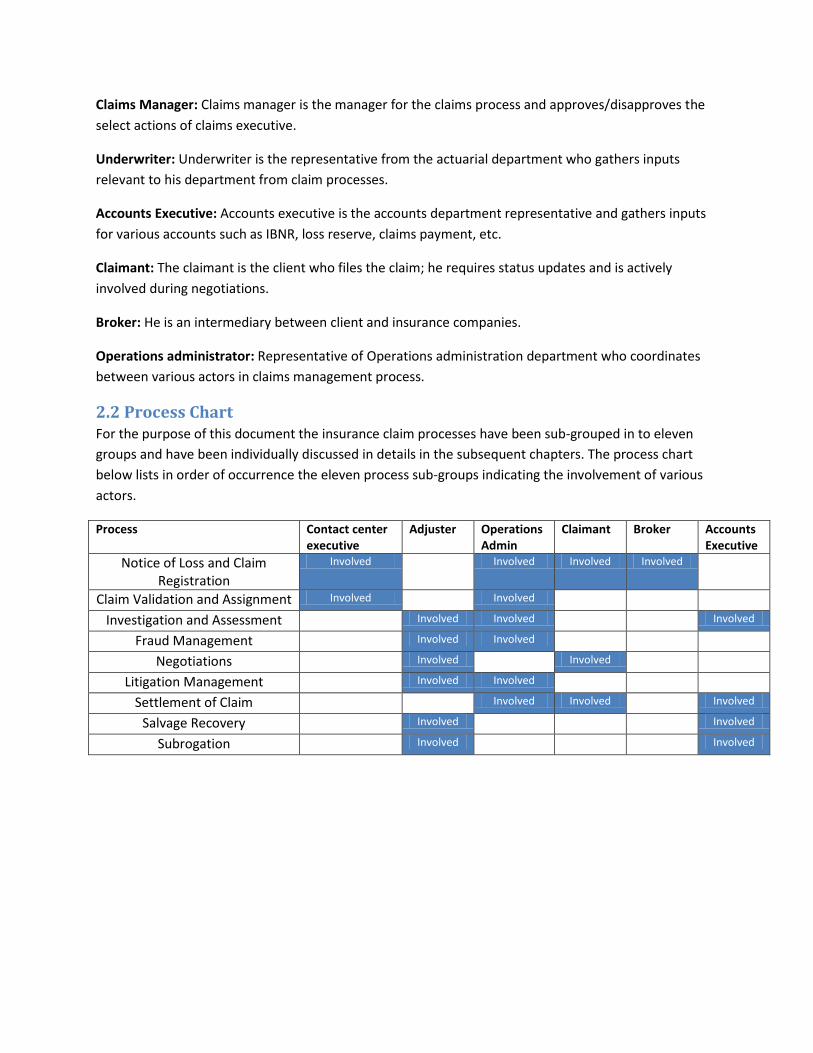

Claims Manager: Claims manager is the manager for the claims process and approves/disapproves the

select actions of claims executive.

Underwriter: Underwriter is the representative from the actuarial department who gathers inputs

relevant to his department from claim processes.

Accounts Executive: Accounts executive is the accounts department representative and gathers inputs

for various accounts such as IBNR, loss reserve, claims payment, etc.

Claimant: The claimant is the client who files the claim; he requires status updates and is actively

involved during negotiations.

Broker: He is an intermediary between client and insurance companies.

Operations administrator: Representative of Operations administration department who coordinates

between various actors in claims management process.

2.2 Process Chart For the purpose of this document the insurance claim processes have been sub-grouped in to eleven

groups and have been individually discussed in details in the subsequent chapters. The process chart

below lists in order of occurrence the eleven process sub-groups indicating the involvement of various

actors.

Process Contact center executive

Adjuster Operations Admin

Claimant Broker Accounts Executive

Notice of Loss and Claim Registration

Involved Involved Involved Involved

Claim Validation and Assignment Involved Involved

Investigation and Assessment Involved Involved Involved

Fraud Management Involved Involved

Negotiations Involved Involved

Litigation Management Involved Involved

Settlement of Claim Involved Involved Involved

Salvage Recovery Involved Involved

Subrogation Involved Involved

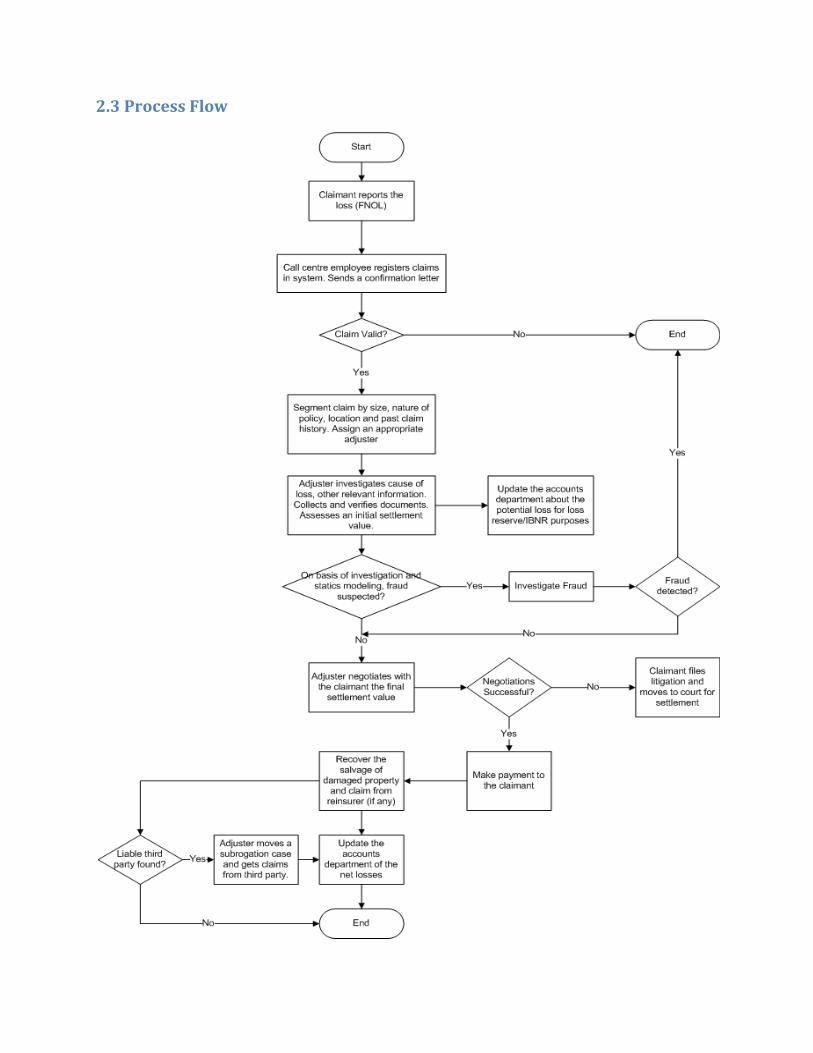

2.3 Process Flow

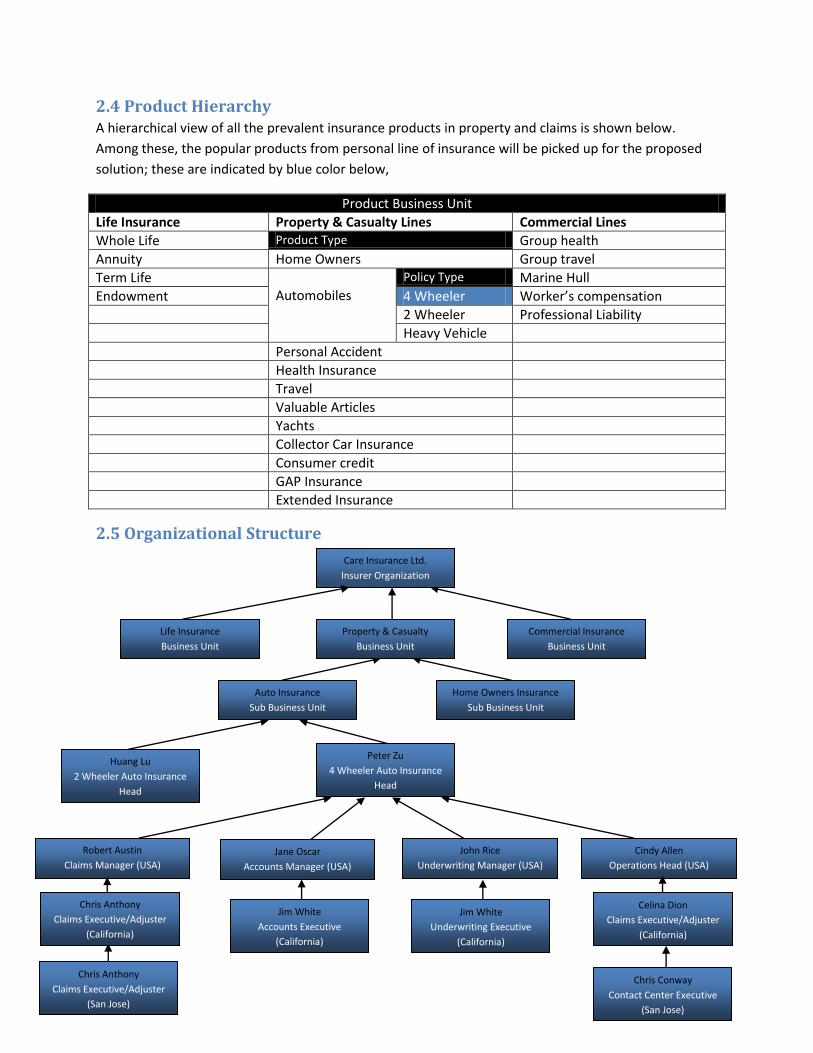

2.4 Product Hierarchy A hierarchical view of all the prevalent insurance products in property and claims is shown below.

Among these, the popular products from personal line of insurance will be picked up for the proposed

solution; these are indicated by blue color below,

Product Business Unit Life Insurance Property & Casualty Lines Commercial Lines

Whole Life Product Type Group health

Annuity Home Owners Group travel

Term Life Automobiles

Policy Type Marine Hull

Endowment 4 Wheeler Worker’s compensation

2 Wheeler Professional Liability

Heavy Vehicle

Personal Accident

Health Insurance

Travel

Valuable Articles

Yachts

Collector Car Insurance

Consumer credit

GAP Insurance

Extended Insurance

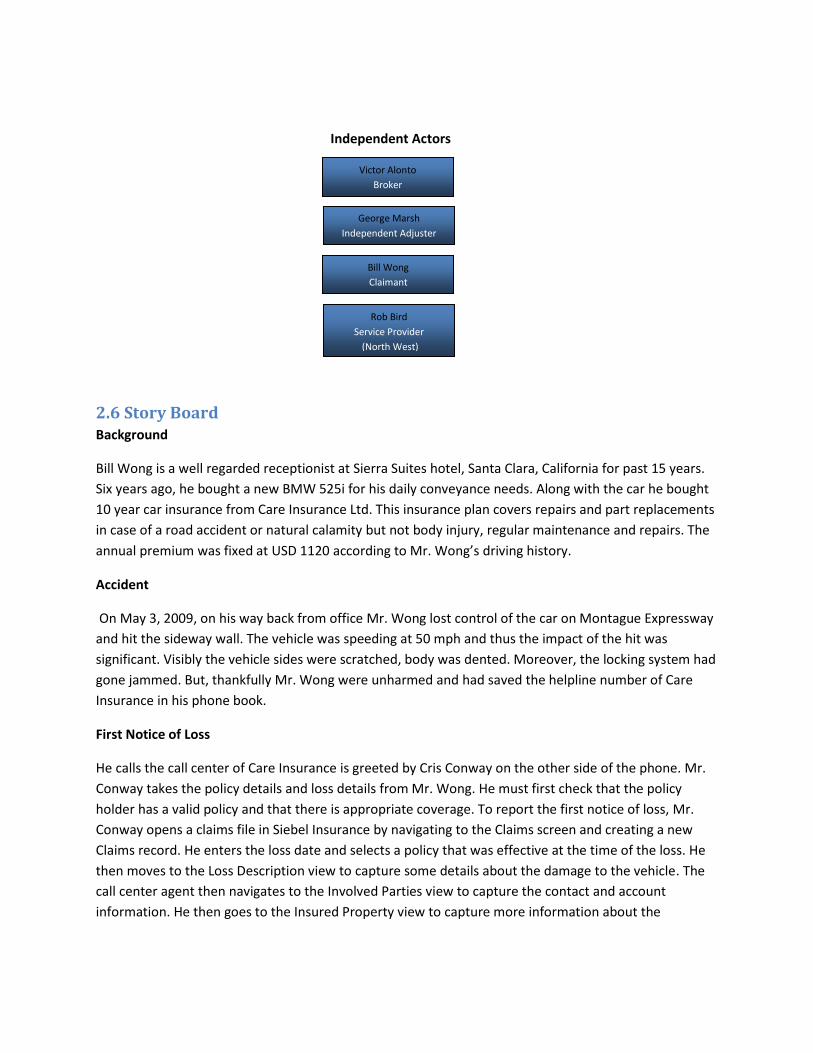

2.5 Organizational Structure

Robert Austin

Claims Manager (USA)

John Rice

Underwriting Manager (USA)

Jane Oscar

Accounts Manager (USA) Cindy Allen

Operations Head (USA)

Chris Conway

Contact Center Executive

(San Jose)

Jim White

Accounts Executive

(California)

Chris Anthony

Claims Executive/Adjuster

(San Jose)

Chris Anthony

Claims Executive/Adjuster

(California)

Celina Dion

Claims Executive/Adjuster

(California)

Jim White

Underwriting Executive

(California)

Auto Insurance

Sub Business Unit

Home Owners Insurance

Sub Business Unit

Peter Zu

4 Wheeler Auto Insurance

Head

Care Insurance Ltd.

Insurer Organization

Property & Casualty

Business Unit

Commercial Insurance

Business Unit

Huang Lu

2 Wheeler Auto Insurance

Head

Life Insurance

Business Unit

Organization

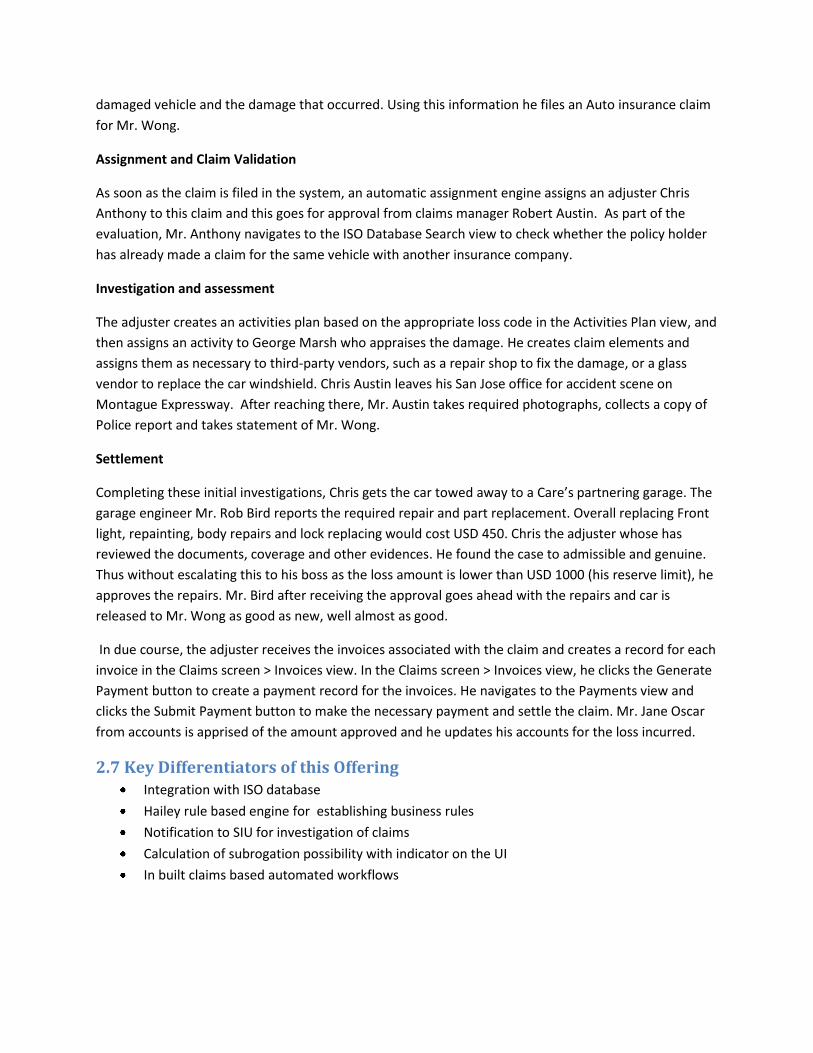

Independent Actors

2.6 Story Board Background

Bill Wong is a well regarded receptionist at Sierra Suites hotel, Santa Clara, California for past 15 years.

Six years ago, he bought a new BMW 525i for his daily conveyance needs. Along with the car he bought

10 year car insurance from Care Insurance Ltd. This insurance plan covers repairs and part replacements

in case of a road accident or natural calamity but not body injury, regular maintenance and repairs. The

annual premium was fixed at USD 1120 according to Mr. Wong’s driving history.

Accident

On May 3, 2009, on his way back from office Mr. Wong lost control of the car on Montague Expressway

and hit the sideway wall. The vehicle was speeding at 50 mph and thus the impact of the hit was

significant. Visibly the vehicle sides were scratched, body was dented. Moreover, the locking system had

gone jammed. But, thankfully Mr. Wong were unharmed and had saved the helpline number of Care

Insurance in his phone book.

First Notice of Loss

He calls the call center of Care Insurance is greeted by Cris Conway on the other side of the phone. Mr.

Conway takes the policy details and loss details from Mr. Wong. He must first check that the policy

holder has a valid policy and that there is appropriate coverage. To report the first notice of loss, Mr.

Conway opens a claims file in Siebel Insurance by navigating to the Claims screen and creating a new

Claims record. He enters the loss date and selects a policy that was effective at the time of the loss. He

then moves to the Loss Description view to capture some details about the damage to the vehicle. The

call center agent then navigates to the Involved Parties view to capture the contact and account

information. He then goes to the Insured Property view to capture more information about the

George Marsh

Independent Adjuster

Victor Alonto

Broker

Bill Wong

Claimant

Rob Bird

Service Provider

(North West)

damaged vehicle and the damage that occurred. Using this information he files an Auto insurance claim

for Mr. Wong.

Assignment and Claim Validation

As soon as the claim is filed in the system, an automatic assignment engine assigns an adjuster Chris

Anthony to this claim and this goes for approval from claims manager Robert Austin. As part of the

evaluation, Mr. Anthony navigates to the ISO Database Search view to check whether the policy holder

has already made a claim for the same vehicle with another insurance company.

Investigation and assessment

The adjuster creates an activities plan based on the appropriate loss code in the Activities Plan view, and

then assigns an activity to George Marsh who appraises the damage. He creates claim elements and

assigns them as necessary to third-party vendors, such as a repair shop to fix the damage, or a glass

vendor to replace the car windshield. Chris Austin leaves his San Jose office for accident scene on

Montague Expressway. After reaching there, Mr. Austin takes required photographs, collects a copy of

Police report and takes statement of Mr. Wong.

Settlement

Completing these initial investigations, Chris gets the car towed away to a Care’s partnering garage. The

garage engineer Mr. Rob Bird reports the required repair and part replacement. Overall replacing Front

light, repainting, body repairs and lock replacing would cost USD 450. Chris the adjuster whose has

reviewed the documents, coverage and other evidences. He found the case to admissible and genuine.

Thus without escalating this to his boss as the loss amount is lower than USD 1000 (his reserve limit), he

approves the repairs. Mr. Bird after receiving the approval goes ahead with the repairs and car is

released to Mr. Wong as good as new, well almost as good.

In due course, the adjuster receives the invoices associated with the claim and creates a record for each

invoice in the Claims screen > Invoices view. In the Claims screen > Invoices view, he clicks the Generate

Payment button to create a payment record for the invoices. He navigates to the Payments view and

clicks the Submit Payment button to make the necessary payment and settle the claim. Mr. Jane Oscar

from accounts is apprised of the amount approved and he updates his accounts for the loss incurred.

2.7 Key Differentiators of this Offering Integration with ISO database

Hailey rule based engine for establishing business rules

Notification to SIU for investigation of claims

Calculation of subrogation possibility with indicator on the UI

In built claims based automated workflows

3. Claims Processing management – Sub Processes

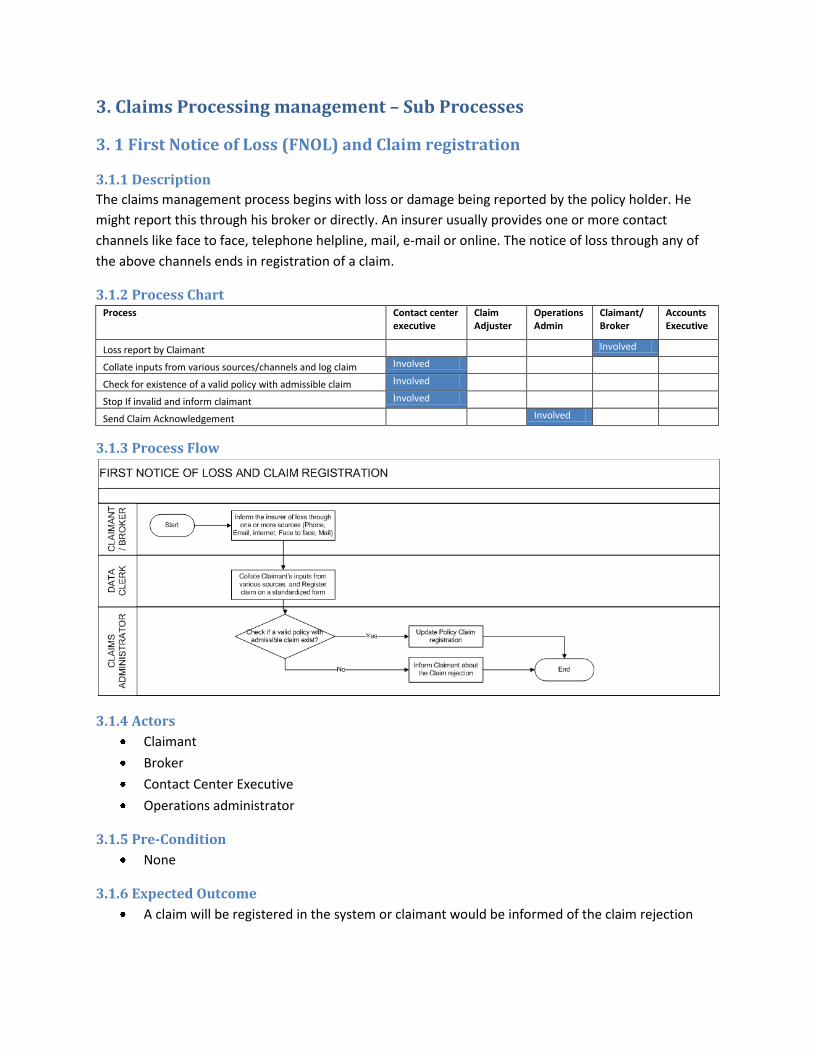

3. 1 First Notice of Loss (FNOL) and Claim registration

3.1.1 Description

The claims management process begins with loss or damage being reported by the policy holder. He

might report this through his broker or directly. An insurer usually provides one or more contact

channels like face to face, telephone helpline, mail, e-mail or online. The notice of loss through any of

the above channels ends in registration of a claim.

3.1.2 Process Chart Process Contact center

executive Claim Adjuster

Operations Admin

Claimant/ Broker

Accounts Executive

Loss report by Claimant Involved

Collate inputs from various sources/channels and log claim Involved

Check for existence of a valid policy with admissible claim Involved

Stop If invalid and inform claimant Involved

Send Claim Acknowledgement Involved

3.1.3 Process Flow

3.1.4 Actors

Claimant

Broker

Contact Center Executive

Operations administrator

3.1.5 Pre-Condition

None

3.1.6 Expected Outcome

A claim will be registered in the system or claimant would be informed of the claim rejection

3.1.7 Business Rules

Check for existence of a valid policy with admissible claim before filing a claim

3.1.8 Requirements covered:

Ability to capture details of the loss incident

Ability to validate the claim against a policy

Ability to generate a unique identifier for every claim

Ability to report claim through different mediums like call centre, email, fax

3.1.9 Important Fields

Field Group Individual Fields

Claim Identification Claim Number

Policy Details Policy Number

Loss Description

Loss Date

Reported By

Location

Involved Parties

Insured Property License Number

Vehicle Identification

Claimant Details Name

Address

Phone No.

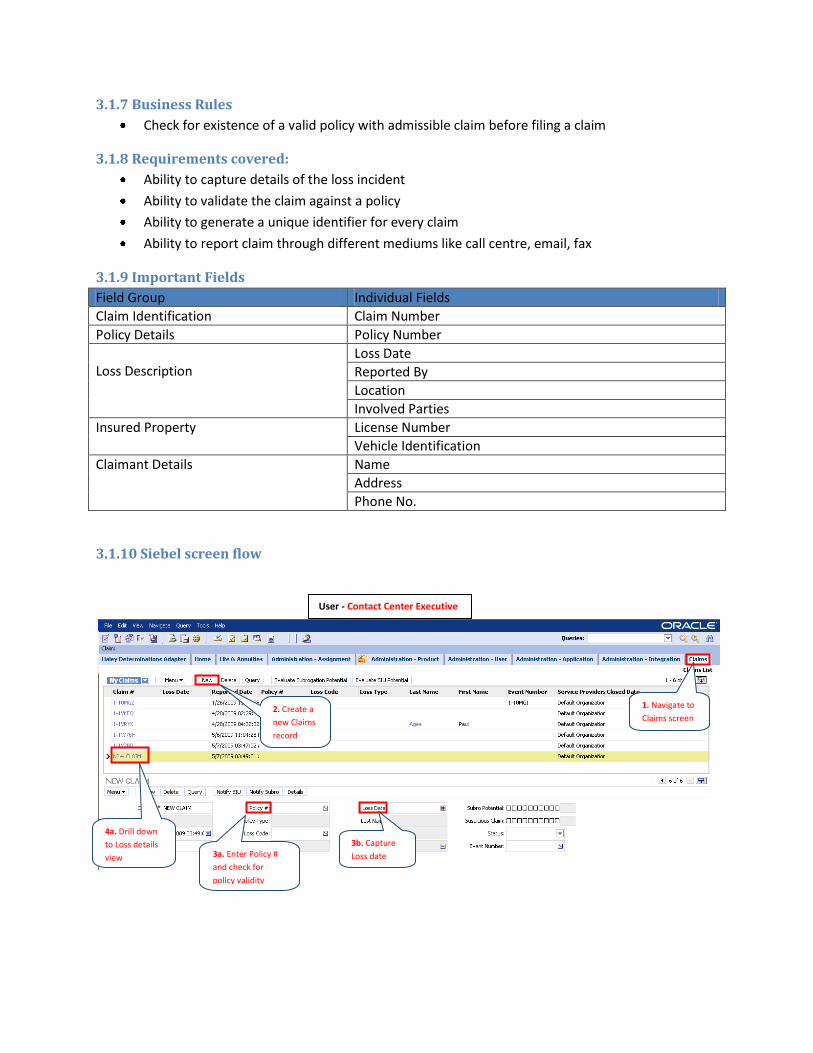

3.1.10 Siebel screen flow

1. Navigate to

Claims screen 2. Create a

new Claims

record

3a. Enter Policy #

and check for

policy validity

4a. Drill down

to Loss details

view

3b. Capture

Loss date

User - Contact Center Executive

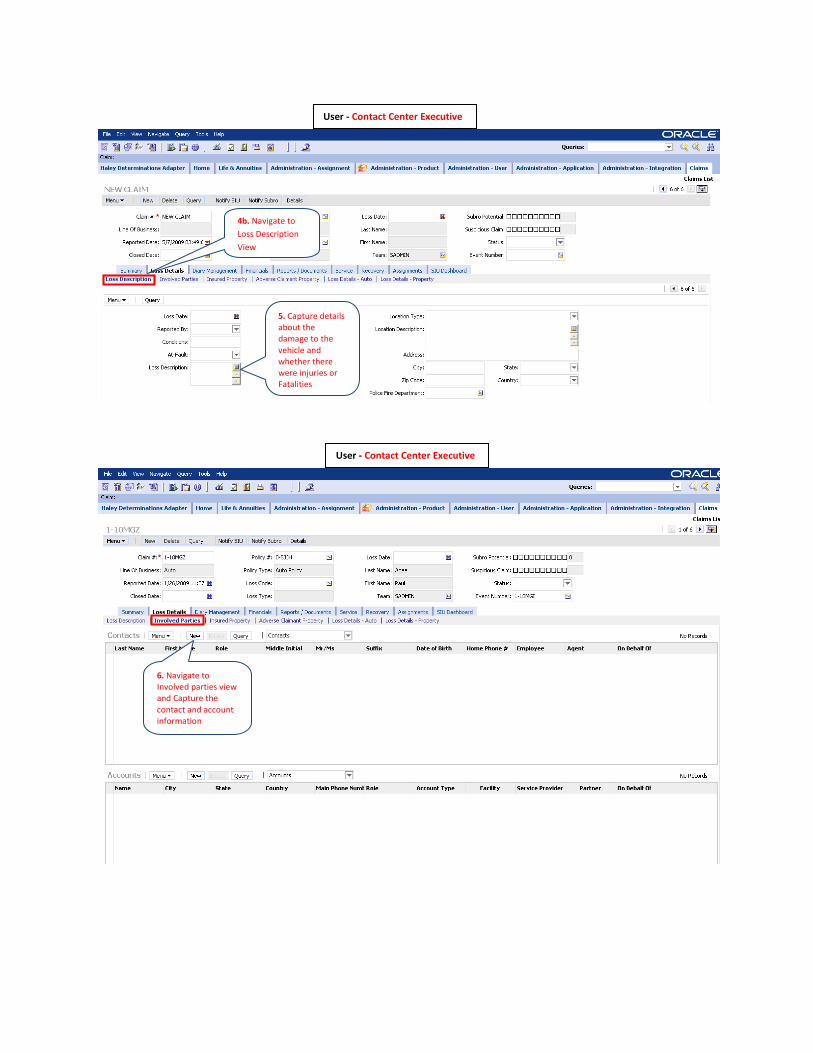

4b. Navigate to

Loss Description

View

5. Capture details about the

damage to the vehicle and whether there were injuries or Fatalities

6. Navigate to Involved parties view and Capture the contact and account information

User - Contact Center Executive

User - Contact Center Executive

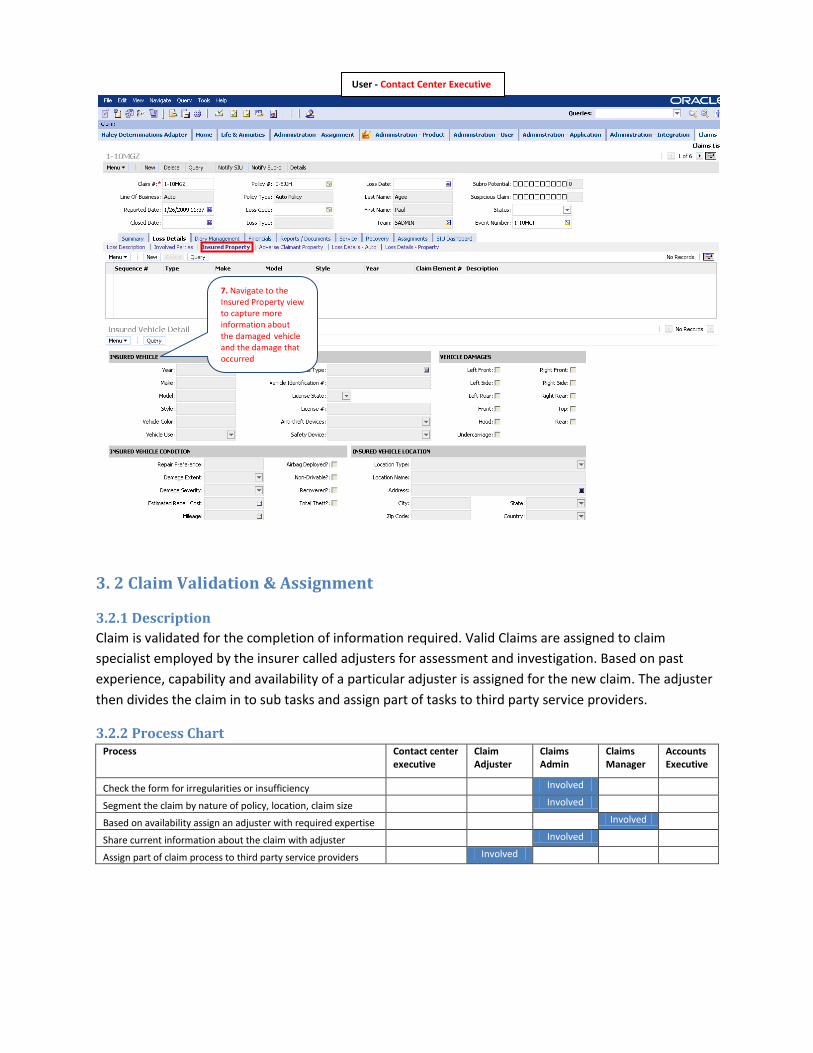

3. 2 Claim Validation & Assignment

3.2.1 Description

Claim is validated for the completion of information required. Valid Claims are assigned to claim

specialist employed by the insurer called adjusters for assessment and investigation. Based on past

experience, capability and availability of a particular adjuster is assigned for the new claim. The adjuster

then divides the claim in to sub tasks and assign part of tasks to third party service providers.

3.2.2 Process Chart Process Contact center

executive Claim Adjuster

Claims Admin

Claims Manager

Accounts Executive

Check the form for irregularities or insufficiency Involved

Segment the claim by nature of policy, location, claim size Involved

Based on availability assign an adjuster with required expertise Involved

Share current information about the claim with adjuster Involved

Assign part of claim process to third party service providers Involved

7. Navigate to the Insured Property view to capture more information about the damaged vehicle and the damage that occurred

User - Contact Center Executive

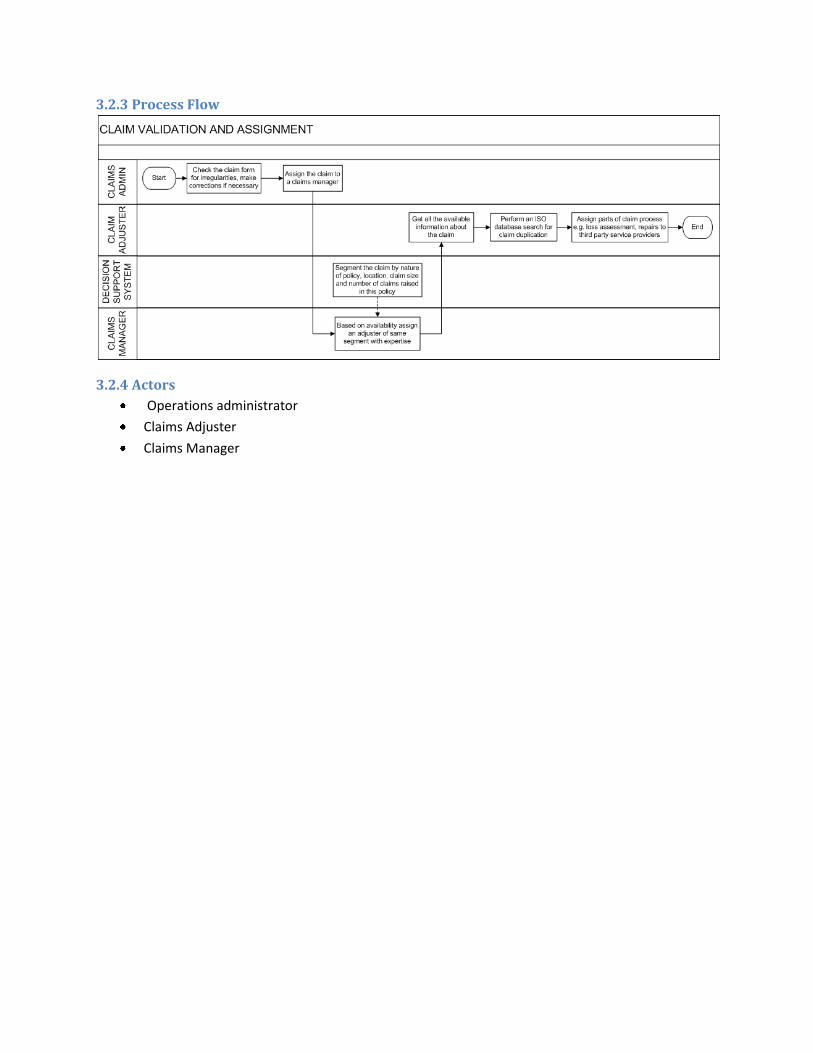

3.2.3 Process Flow

3.2.4 Actors

Operations administrator

Claims Adjuster

Claims Manager