Embed Size (px)

Citation preview

www.antonydavies.org

There are two types of seat in the room:

35 Consumers14 Insurers

Sit one person to each seat.If you are comfortable doing a lot of rudimentary

math, sit at an Insurer seat.

After all the seats are filled, extra bodies should team up with insurers.

Do not team up with consumers.

www.antonydavies.org

Health Insurance

www.antonydavies.org

The Players and the Goals

In this experiment, there are CONSUMERS and INSURERS.

INSURERS sell INSURANCE.

CONSUMERS buy FOOD and INSURANCE.

3

www.antonydavies.org

Consumers

Each consumer gets $25 per day.

A unit of food costs $1.

4

$25

The more food the consumer eats, the happier the consumer becomes.

www.antonydavies.org

Consumers: The Catch

Each day, consumers face some risk of badness.

5

vs.

If badness befalls the consumer, the consumer loses all of the purchased food for that day.

www.antonydavies.org

Consumers: The Insurance

But, consumers can purchase insurance contracts from the insurance companies.

6

Each contract pays the consumer $1 worth of food if badness befalls the consumer that day.

www.antonydavies.org

Consumers: Example

Suppose you can purchase insurance contracts at a price of $0.50 each (the price of food is always $1 each).

7

$20

You spend $5 on insurance contracts. The remaining $20 is automatically spent on food.

10 insurance contracts

20 food

(Consumers may buy fractions of a unit of food.)

$20$5

www.antonydavies.org

Consumers: Example

If badness does not befall you, then you eat 20 units of food and are very happy.

8

Very Happy !

!

www.antonydavies.org

Consumers: Example

If badness does befall you, the 20 units of food disappear, and each insurance contract pays $1. You automatically buy food, eat it, and are somewhat happy.

9

Somewhat Happy

www.antonydavies.org

Decision

Consumers: Example

The consumer makes one set of decisions that are repeated for each of the three days. Daily outcomes may change due to randomness.

Day 1

10 insurance contracts 15 food

Day 2

10 insurance contracts 15 food

Day 3

10 insurance contracts 15 food

10

www.antonydavies.org

Consumers

Each consumer’s goal: Maximize happiness

More insurance means

More food when badness befalls.

Less food when badness does not befall.

Too little insurance is bad. Too much insurance is also bad.

11

www.antonydavies.org

Insurers

Each insurer can write as many insurance contracts as liked and charge any price.

12

www.antonydavies.org

Insurers

If badness does not befall the consumer, the insurer walks away with the money the consumer paid for the contracts.

13

$ $ $

$ $ $

www.antonydavies.org

Insurers

If badness does befall the consumer, the insurer pays the consumer $1 for each contract the insurer sold the consumer.

14

www.antonydavies.org

Insurers: Example

You sell Consumer A six contracts for $0.60 each, and sell Consumer B five contracts for $0.30 each.

15

For each of the three days, you collect $3.60 from Consumer A and $1.50 from Consumer B.

$15.30

Revenue =

$3.60 $3.60$3.60

$1.50 $1.50$1.50

$3.60

$1.50

www.antonydavies.org

Insurers: Example

Suppose that badness then befalls Consumer B on two of the days, but Consumer A on none of the days.

16

You owe Consumer B $1 for each contract for the two days.

$15.30

Revenue =

$10.00

Cost =

$5.30Profit =

$5.00 $5.00

www.antonydavies.org

Insurers: Example

Alternatively, suppose that badness befalls Consumer A on all three days, but Consumer B on none of the days.

17

You owe Consumer A $1 for each contract for the three days.

$15.30

Revenue =

$18.00

Cost =

$2.70Loss =

(Insurers do not need cash reserves to cover policies.)

$6.00 $6.00$6.00

www.antonydavies.org

Insurers

Each insurer’s goal: Maximize expected profit

Insurers can ask whatever prices they like for contracts

Too low a price is bad. Too high a price is also bad.

18

www.antonydavies.org 19

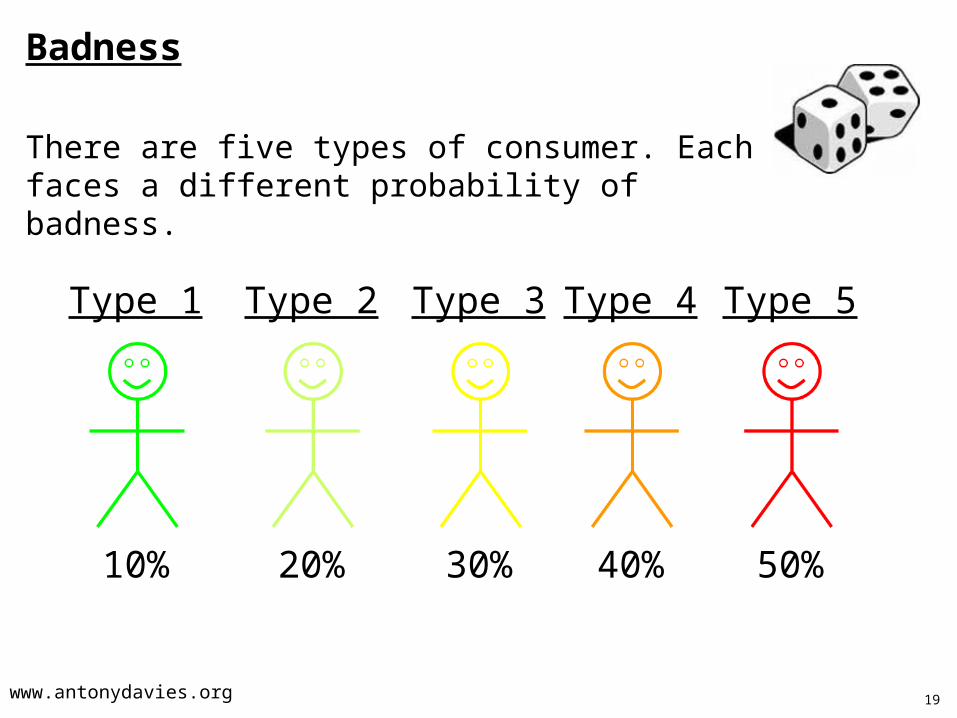

Type 1

10%

Badness

There are five types of consumer. Each faces a different probability of badness.

Type 2

20%

Type 3

30%

Type 4

40%

Type 5

50%

www.antonydavies.org

The Objects

20

= insurance contract(s)

Contracts Sold BuyerSuspected Risk

(0.1 to 0.5 )Total Revenue

Expected Cost (contracts x risk )

Expected Profit (revenue - cost )

= sales register

www.antonydavies.org

Contracts

21

12 6

$4.80

Customer 6 purchases 12 contracts from insurer 4 for $0.40 each.

This contract generates $4.80 daily income for three days for the insurer.

www.antonydavies.org

Contracts Sold Buyer Risk (0.1 to 0.5 )Total Revenue

per DayCost per Day

(contracts x risk )Expected Profit

per Day

Register

22

12

6 0.3

The register is for your own use in tracking your customers.• Be aware of customers who buy a lot of insurance.

• At the end of the round, watch to see which of your customers has badness befall them.

These are possible signs that the customer is high risk.

You will need to estimate consumers’ risks.

www.antonydavies.org

The Mechanics

23

Agent

Insurers Consumers

Head Office $0.50

Prices are per contract.You may buy multiple contracts.

www.antonydavies.org

The Mechanics

24

Agent

Insurers Consumers

Head Office

www.antonydavies.org

The Mechanics

25

Agent

Insurers Consumers

Head Office

Consumers:Keep track of how much you have spent. You need to save cash to buy food and you only have $20.

Head Office:Keep track of risk estimates and expected profits. Advise the agent on setting prices.

Agent:Try to estimate consumers’ risks based on how many contracts they want and the prices they are willing to pay.

www.antonydavies.org

Risk Types

26

www.antonydavies.org 27

Risk Type Prob. Of Badness Risk Type Prob. Of BadnessConsumer #1 5 50% Consumer #18 3 30%Consumer #2 1 10% Consumer #19 2 20%Consumer #3 3 30% Consumer #20 4 40%Consumer #4 2 20% Consumer #21 5 50%Consumer #5 4 40% Consumer #22 1 10%Consumer #6 5 50% Consumer #23 3 30%Consumer #7 1 10% Consumer #24 2 20%Consumer #8 3 30% Consumer #25 4 40%Consumer #9 2 20% Consumer #26 5 50%Consumer #10 4 40% Consumer #27 1 10%Consumer #11 5 50% Consumer #28 3 30%Consumer #12 1 10% Consumer #29 2 20%Consumer #13 3 30% Consumer #30 4 40%Consumer #14 2 20% Consumer #31 5 50%Consumer #15 4 40% Consumer #32 1 10%Consumer #16 5 50% Consumer #33 3 30%Consumer #17 1 10% Consumer #34 2 20%

Consumer #35 4 40%

www.antonydavies.org 28

Risk Type Prob. Of BadnessConsumer #1 5 50%Consumer #2 1 10%Consumer #3 3 30%Consumer #4 2 20%Consumer #5 4 40%Consumer #6 5 50%Consumer #7 1 10%Consumer #8 3 30%Consumer #9 2 20%Consumer #10 4 40%Consumer #11 5 50%Consumer #12 1 10%Consumer #13 3 30%Consumer #14 2 20%Consumer #15 4 40%Consumer #16 5 50%Consumer #17 1 10%

www.antonydavies.org 29

Risk Type Prob. Of BadnessConsumer #18 3 30%Consumer #19 2 20%Consumer #20 4 40%Consumer #21 5 50%Consumer #22 1 10%Consumer #23 3 30%Consumer #24 2 20%Consumer #25 4 40%Consumer #26 5 50%Consumer #27 1 10%Consumer #28 3 30%Consumer #29 2 20%Consumer #30 4 40%Consumer #31 5 50%Consumer #32 1 10%Consumer #33 3 30%Consumer #34 2 20%Consumer #35 4 40%

www.antonydavies.org

Ready to begin…

30

www.antonydavies.org 31

Consumers: You have $25.

Buy some insurance (if you want).

All remaining money goes to food.

Insurers: Sell insurance to maximize expected profit.

www.antonydavies.org

Accounting Phase

Consumers report:

• Contracts purchased, cost, and from which insurer(s)

32

www.antonydavies.org 33

Food Contracts1 18.6 19 YES YES YES 57.02 22.5 10 no no no 67.53 22.8 10 no YES no 55.64 24.5 5 no no no 73.55 22.5 10 no no no 67.56 20.8 15 no YES no 56.57 25.0 0 no no no 75.08 22.8 10 no YES YES 42.89 22.0 10 no no no 66.010 21.0 20 no no YES 62.011 18.0 20 YES YES no 58.012 24.4 3 no no no 73.213 18.7 18 no no no 56.114 20.5 15 no no YES 56.015 16.5 20 YES YES YES 60.016 22.9 10 YES YES YES 30.017 20.7 18 no YES no 59.418 22.6 8 YES YES no 38.619 21.9 13 no no YES 56.8

ConsumerDaily Purchases Badness

Day 1Badness

Day 2Badness

Day 3Total

Consumption

www.antonydavies.org

Food Contracts20 23.4 4 no no YES 50.821 22.5 10 YES no YES 42.522 22.8 20 no no no 68.423 21.7 12 YES no no 55.424 22.4 13 no no no 67.225 23.0 8 YES YES YES 24.026 23.1 9 no no no 69.227 24.0 10 no no no 72.028 24.4 5 no no YES 53.729 24.5 5 no no no 73.530 11.0 16 YES YES YES 48.031 19.4 22 YES YES no 63.432 23.7 7 no no no 71.133 21.7 10 no no no 65.134 23.8 2 no no no 71.435 23.4 7 no YES no 53.8

Maximum 75.0Median 58.0Minimum 30.0

ConsumerDaily Purchases Badness

Day 1Badness

Day 2Badness

Day 3Total

Consumption

34

www.antonydavies.org 35

TotalCosts

1 $21.45 $51.00 ($29.55)2 $13.80 $36.00 ($22.20)3 $8.10 $5.00 $3.104 $32.55 $35.00 ($2.45)5 $27.90 $10.00 $17.906 $28.50 $59.00 ($30.50)7 $27.75 $42.00 ($14.25)8 $28.50 $40.00 ($11.50)9 $16.50 $14.00 $2.5010 $58.35 $46.00 $12.3511 $23.40 $61.00 ($37.60)12 $12.00 $9.00 $3.0013 $20.10 $36.00 ($15.90)14 $16.05 $34.00 ($17.95)

InsurerTotal

PremiaTotal Profit

www.antonydavies.org

Mandated Insurance

People have lobbied the government to require insurance companies to provide at least 50 contracts’ worth of coverage.

Insurers now may not sell fewer than 50 contracts to a consumer.*

*(unless the consumer already owns at least 50 contracts)

36

www.antonydavies.org

Ready to begin…

37

www.antonydavies.org 38

Consumers: You have $25.

Buy some insurance (if you want).

All remaining money goes to food.

Insurers: Sell insurance to maximize expected profit.

You may not sell fewer than 50 contracts to a consumer unless that consumer already owns at least 50 contracts.

www.antonydavies.org 39

Accounting Phase

Consumers report:

• Contracts purchased, cost, and from which insurer(s)

www.antonydavies.org 40

Food Contracts1 9.5 50 YES no YES 109.52 25.0 0 no no no 75.03 12.5 50 no YES no 75.04 25.0 0 no no no 75.05 12.3 85 no YES no 109.56 6.8 70 no YES no 83.57 22.5 50 no no no 67.58 25.0 0 YES YES YES 0.09 8.0 60 no no no 24.010 11.5 50 no no no 34.511 12.0 50 YES YES YES 150.012 17.5 50 no no no 52.513 14.0 50 no no no 42.014 18.0 50 no no YES 86.015 12.5 50 YES no YES 112.516 11.0 55 YES YES YES 165.017 25.0 0 no no no 75.018 8.3 50 no no YES 66.719 10.5 54 no no no 31.5

Total Consumption

ConsumerDaily Purchases Badness

Day 1Badness

Day 2Badness

Day 3

www.antonydavies.org 41

Food Contracts20 25.0 0 no no YES 50.021 15.0 50 no YES no 80.022 20.0 50 no no no 60.023 9.3 50 no no no 27.824 17.5 50 no YES no 85.025 13.5 50 YES no no 77.026 11.5 50 no YES no 73.027 25.0 0 no no no 75.028 17.0 50 no no YES 84.029 17.5 50 no no no 52.530 10.0 50 no no no 30.031 15.0 50 no YES no 80.032 17.5 50 no no YES 85.033 15.0 50 YES no YES 115.034 20.0 50 YES no no 90.035 25.0 0 no no YES 50.0

Maximum 165.0Median 75.0Minimum 0.0

Badness Day 3

Total Consumption

ConsumerDaily Purchases Badness

Day 1Badness

Day 2

www.antonydavies.org 42

TotalCosts

1 $43.50 $100.00 ($56.50)2 $81.51 $120.00 ($38.49)3 $27.00 $85.00 ($58.00)4 $58.50 $130.00 ($71.50)5 $57.75 $60.00 ($2.25)6 $94.50 $120.00 ($25.50)7 $76.50 $170.00 ($93.50)8 $82.50 $100.00 ($17.50)9 $33.00 $60.00 ($27.00)10 $89.25 $110.00 ($20.75)11 $18.00 $20.00 ($2.00)12 $114.00 $140.00 ($26.00)13 $71.25 $80.00 ($8.75)14 $96.00 $25.00 $71.00

InsurerTotal

PremiaTotal Profit

www.antonydavies.org

Mandatory Insurance

Concerned that some consumers are uninsured, the government requires that all consumers buy at least 50 contracts.

43

www.antonydavies.org

Ready to begin…

44

www.antonydavies.org 45

Consumers: You have $25.

You must buy at least 50 contracts.

All remaining money goes to food.

Insurers: Sell insurance to maximize expected profit.

www.antonydavies.org 46

Accounting Phase

Consumers report:

• Contracts purchased, cost, and from which insurer(s)

www.antonydavies.org 47

Food Contracts1 7.3 55 YES no YES 117.32 22.5 50 no no no 67.53 13.8 50 no YES no 77.54 22.5 50 no no YES 95.05 9.5 80 YES YES no 169.56 3.0 95 no no YES 101.07 17.0 200 no no no 51.08 1.0 80 YES no no 82.09 19.5 50 no no YES 89.010 15.0 50 no no no 45.011 11.0 50 YES no no 72.012 15.0 50 no no no 45.013 15.4 50 no no YES 80.814 16.5 50 YES no no 83.015 11.3 50 no no YES 72.516 16.3 55 no no YES 87.517 15.0 50 no no no 45.018 7.0 50 no no YES 64.019 13.3 50 no no no 39.8

Total Consumption

ConsumerDaily Purchases Badness

Day 1Badness

Day 2Badness

Day 3

www.antonydavies.org 48

Food Contracts20 14.0 50 no no no 42.021 12.5 55 no YES no 80.022 19.0 50 YES YES no 119.023 12.5 50 no YES YES 112.524 16.0 65 no no no 48.025 12.5 50 YES YES YES 150.026 10.0 50 no YES no 70.027 14.5 50 no no no 43.528 15.0 50 YES no no 80.029 17.5 50 no no no 52.530 -1.5 100 YES YES YES 300.031 16.3 50 no YES YES 116.332 17.5 50 no no no 52.533 22.4 60 YES no YES 142.434 17.0 50 no no YES 84.035 15.0 50 no no YES 80.0

Maximum 169.5Median 77.5Minimum 39.8

Badness Day 3

Total Consumption

ConsumerDaily Purchases Badness

Day 1Badness

Day 2

www.antonydavies.org 49

TotalCosts

1 $36.00 $110.00 ($74.00)2 $97.50 $105.00 ($7.50)3 $27.45 $62.00 ($34.55)4 $99.00 $250.00 ($151.00)5 $66.75 $125.00 ($58.25)6 $64.50 $105.00 ($40.50)7 $138.00 $210.00 ($72.00)8 $112.50 $100.00 $12.509 $42.00 $115.00 ($73.00)10 $135.00 $95.00 $40.0011 $46.35 $78.00 ($31.65)12 $135.00 $195.00 ($60.00)13 $62.55 $250.00 ($187.45)14 $117.00 $225.00 ($108.00)

InsurerTotal

PremiaTotal Profit

www.antonydavies.org

Results…

50

www.antonydavies.org

Compared to the free market, what do you believe happens to the price of insurance under…

1.Mandated insurance

2.Mandatory insurance

51

www.antonydavies.org

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

Free Market Mandated Mandatory

Insurance Price per Contract

52

www.antonydavies.org 53

Compared to the free market, what do you believe happens to the number of uninsured people under…

1.Mandated insurance

2.Mandatory insurance

www.antonydavies.org 54

0%

5%

10%

15%

20%

25%

Free Market Mandated Mandatory

Uninsured

www.antonydavies.org

Consider

The price per contract isn’t the consumer’s health care cost.

The consumer’s health care cost is the total amount of money the consumer pays for insurance.

55

www.antonydavies.org

Compared to the free market, what do you believe happens to the total cost of insurance per insured person under…

1.Mandated insurance

2.Mandatory insurance

56

www.antonydavies.org 57

$0

$2

$4

$6

$8

$10

$12

Free Market Mandated Mandatory

Insurance Cost per Insured Person

www.antonydavies.org

$0

$5

$10

$15

$20

$25

Free Market Mandated Mandatory

Insurance Cost per Insured Person

58

www.antonydavies.org 59

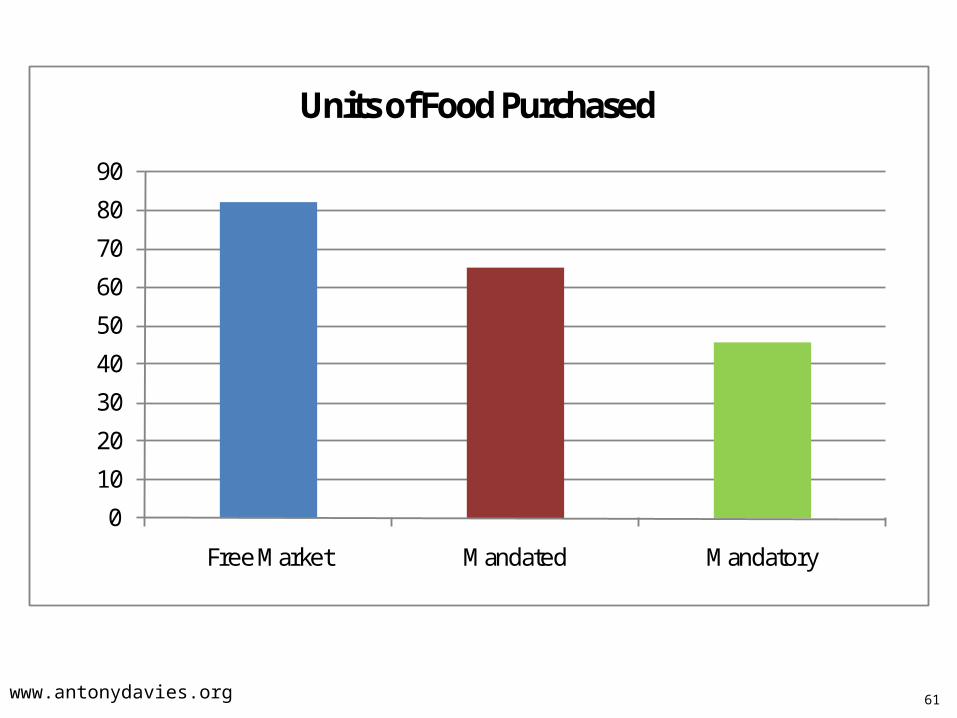

Compared to the free market, what do you believe happens to food purchases under…

1.Mandated insurance

2.Mandatory insurance

www.antonydavies.org 60

0

100

200

300

400

500

600

700

800

900

Free Market Mandated Mandatory

Units of Food Purchased

www.antonydavies.org 61

0

10

20

30

40

50

60

70

80

90

Free Market Mandated Mandatory

Units of Food Purchased

www.antonydavies.org 62

On whom do you believe the insurance companies make or lose money in each scenario?

www.antonydavies.org 63

-$350

-$300

-$250

-$200

-$150

-$100

-$50

$0

$50

$100

Type 1 Type 2 Type 3 Type 4 Type 5

Source of Insurance Profits

Free Market Mandated Mandatory

www.antonydavies.org 64

($800)

($600)

($400)

($200)

$0

$200

$400

$600

Type 1 Type 2 Type 3 Type 4 Type 5

Source of Insurance Profits (all firms per 3 days)

Free Market Mandated Mandatory

www.antonydavies.org

• Forces people to consume quantities of goods and insurance that they may not want to consume.

• Transfers wealth from low risk to high risk people.

A better solution is simply to tax the low risk people, give the money to the high risk people and let them buy what they want.

65

What is the effect of insurance mandates?

(but what if they don’t buy insurance?)

www.antonydavies.org

But, we have to do something!

Look at what has been happening to the cost of health care over time!

66

www.antonydavies.org

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

1980

1981

1982

1983

1984

1985

1986

1987

1988

19

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

06

Price of Medical Care Consumer Prices Excluding Medical Care

67

Source: Bureau of Labor Statistics (www.economy.com)

Price of medical care has increased 350% since 1980 versus 135% for other consumer prices.

www.antonydavies.org

But, the cost of health care is only half of the picture.

What has been happening to the quality of health care?

68

www.antonydavies.org

How do we measure the quality of health care?

1. What is “quality?”

69

2. How do we account for care didn’t exist in the past?

3. How do we weigh qualities across different types of care?

www.antonydavies.org

How does one measure the quality of health care?

An easy and only-somewhat-sucky measure of the effectiveness of health care is the mortality rate.

70

www.antonydavies.org

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1960

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Infant Mortality per 1,000 Live Births

71

Source: Statistical Abstract of the United States, 2008, Table 77.

From 1960 to 2006, infant mortality fell 70%.

www.antonydavies.org 72

Source: Statistical Abstract of the United States, 2008, Table 110.

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Deaths by Influence and Pneumonia (per 100,000 population)Deaths by Influenza and Pneumonia (per 100,000 population)

From 1960 to 2004, deaths due to influenza and pneumonia fell 60%.

www.antonydavies.org 73

7.5

8.0

8.5

9.0

9.5

10.0

1960

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Deaths per 1,000 People

Source: Statistical Abstract of the United States, 2008, Table 77.

From 1960 to 2006, the mortality rate fell by 15%.

www.antonydavies.org 74

What does the increased cost of health care buy us?

www.antonydavies.org

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Mill

ions

Actual Deaths

75

Source: Derived from Statistical Abstract of the United States, and the Bureau of Economic Analysis.

If the quality of our health care had remained at the level it was in 1967, how many people would have died each year since 1967?

www.antonydavies.org

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Mill

ions

Actual Deaths Deaths at 1967 Mortality Rate

76

Source: Derived from Statistical Abstract of the United States, and the Bureau of Economic Analysis.

600,000 lives saved just in 2010

www.antonydavies.org

What are the claimed problems?

77

• Many people are uninsured.

• Many people cannot afford insurance.

• Lack of competition makes insurance too expensive.

www.antonydavies.org 78

Many people are uninsured

www.antonydavies.org

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

79

Source: Income, Poverty, and Health Insurance Coverage in the U.S.: 2006, US Census Bureau.

The percentage of the population that is uninsured has remained rather stable over time.

www.antonydavies.org 80

Source: Bureau of Labor Statistics, Census Bureau

Insured

Uninsured (15% of the population)

How many Americans are uninsured?

www.antonydavies.org

Insured

Claim to be Uninsured but

Aren't

Medicaid or SCHIP Eligible

Uninsured

81

Source: Bureau of Labor Statistics, Census Bureau

(12% of the population)

How many Americans are uninsured?

www.antonydavies.org

Insured

Claim to be Uninsured but

Aren't

Medicaid or SCHIP Eligible

Uninsured Less Than 4 Months

18 to 34 and Childless

Uninsured

82

Source: Bureau of Labor Statistics, Census Bureau

(4% of the population)

How many Americans are uninsured?

If we count one-third of this group, the uninsured are between 6% and 8% of the population depending on whether or not we count this group.

www.antonydavies.org 83

Many people cannot afford insurance

www.antonydavies.org

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

New

Yor

kM

assa

chus

etts

Rhod

e Is

land

Mai

neCo

nnec

ticut

New

Ham

pshi

reM

onta

naN

evad

aVi

rgin

iaG

eorg

iaO

klah

oma

Texa

sSo

uth

Caro

lina

Flor

ida

Tenn

esse

eM

inne

sota

Ari

zona

Neb

rask

aCa

lifor

nia

Indi

ana

Penn

sylv

ania

Illin

ois

Colo

rado

Kent

ucky

Mis

sour

iO

hio

Kans

asN

orth

Car

olin

aIo

wa

Ann

ual P

rem

ium

Single Family (adjusted for differing family sizes)

84

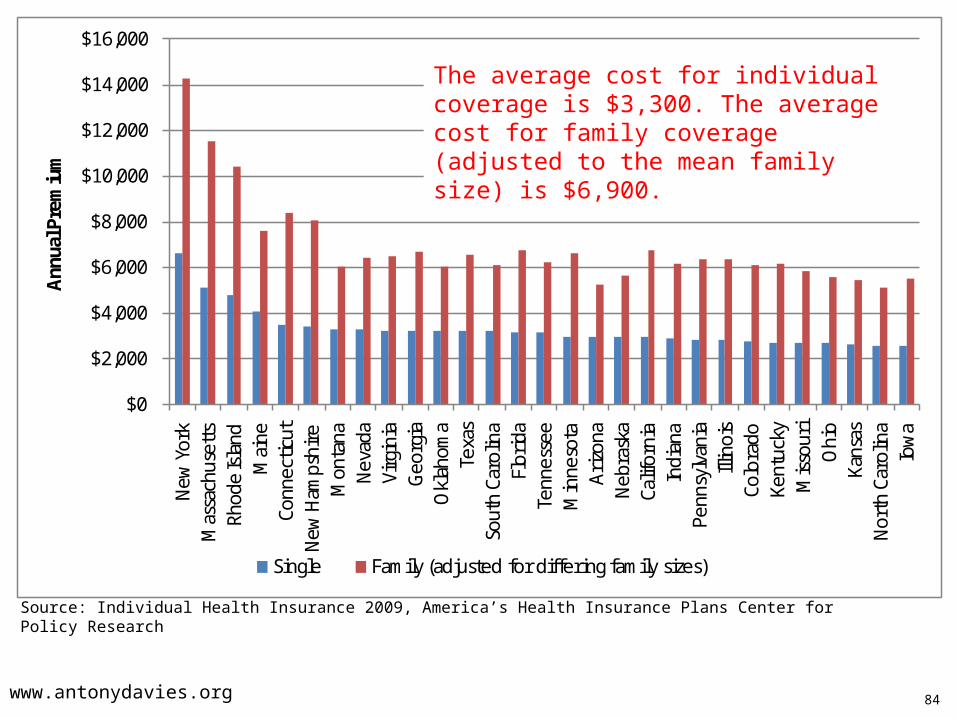

Source: Individual Health Insurance 2009, America’s Health Insurance Plans Center for Policy Research

The average cost for individual coverage is $3,300. The average cost for family coverage (adjusted to the mean family size) is $6,900.

www.antonydavies.org

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

New

Yor

kM

assa

chus

etts

Rhod

e Is

land

Mai

neCo

nnec

ticut

New

Ham

pshi

reM

onta

naN

evad

aVi

rgin

iaG

eorg

iaO

klah

oma

Texa

sSo

uth

Caro

lina

Flor

ida

Tenn

esse

eM

inne

sota

Ari

zona

Neb

rask

aCa

lifor

nia

Indi

ana

Penn

sylv

ania

Illin

ois

Colo

rado

Kent

ucky

Mis

sour

iO

hio

Kans

asN

orth

Car

olin

aIo

wa

Ann

ual P

rem

ium

Single Family (adjusted for differing family sizes)

85

Source: Individual Health Insurance 2009, America’s Health Insurance Plans Center for Policy Research

Community Rating Cannot charge based on

health history

Guaranteed Issue May not deny coverage

www.antonydavies.org

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$0 $1,000 $2,000 $3,000 $5,000 $10,000

Ann

ual P

rem

ium

(fam

ily p

olic

ies)

Deductible

86

Source: Individual Health Insurance 2009, America’s Health Insurance Plans Center for Policy Research

Annual premia are significantly higher for low deductible policies.

www.antonydavies.org

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000 A

nnua

l Cos

ts f

or A

vera

ge A

mer

ican

Fam

ily

87

Source: Consumer Expenditures, US Bureau of Labor Statistics, 2009.

Average annual expenditures (per household) compared to the cost of family health insurance.

www.antonydavies.org 88

Lack of competition makes insurance expensive.

www.antonydavies.org 89

The law makes it difficult for insurance companies to operate across state lines.

Individual insurance is subject to mandates that employer-provided insurance is not.

Employer-provided insurance benefits are tax-free, which causes an increase in demand for insurance and health services.

www.antonydavies.org 90

Can one place a value on a human life?(and, if yes, is it wrong to do so?)

Yes, it is possible.No, it is not wrong to do so.

Almost everyone does it almost every day.

www.antonydavies.org

Seat Belts on School Buses

It costs (on average) $2.5 million for every child’s life saved.

Should we install seatbelts on school buses?

www.antonydavies.org

Spend $2.5 million on: # Lives Saved Annually

Seatbelts on school buses 1

Airbags in cars 3

Heart transplants 13

Malaria prevention 975

If our concern is saving lives, then we should not spend money for seatbelts on school buses because every 1 life saved will be offset by 975 lives we might otherwise have saved.