Embed Size (px)

Citation preview

Document of

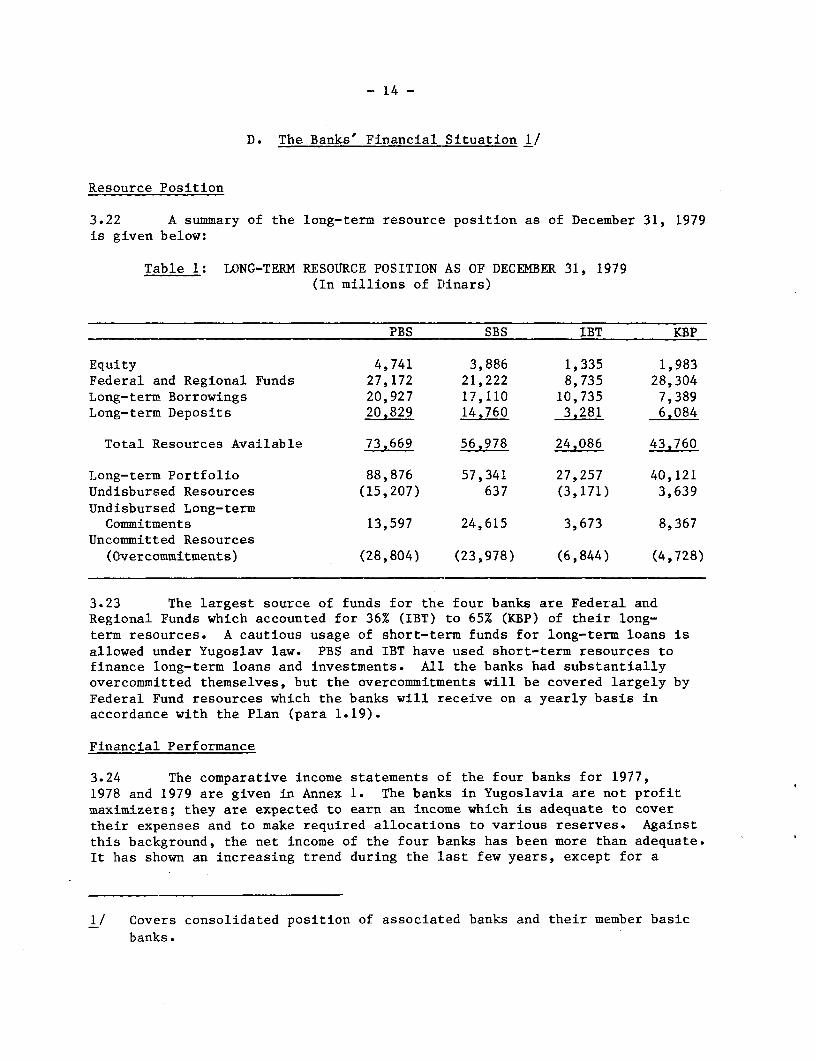

The World Bank

FOR OFFICIAL USE ONLY

Report No. 2965-YU

STAFF APPRAISAL REPORT

ON A

FIFTH INDUSTRIAL CREDIT PROJECT

YUGOSLAVIA

September 5, 1980

Industrial Development and Finance DivisionProjects DepartmentEurope, Middle East and North AfricaRegional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

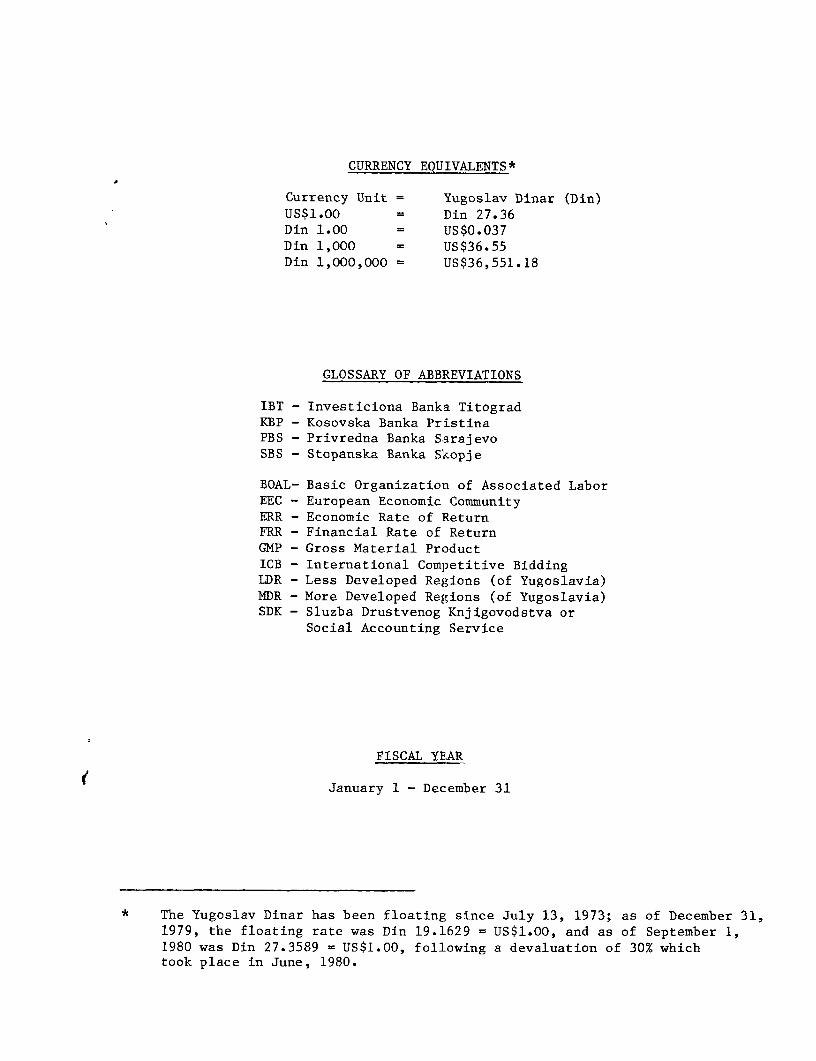

CURRENCY EQUIVALENTS*

Currency Unit = Yugoslav Dinar (Din)US$1.00 = Din 27.36Din 1.00 = US$0.037Din 1,000 = US$36.55

Din 1,000,000 = US$36,551.18

GLOSSARY OF ABBREVIATIONS

IBT - Investiciona Banka TitogradKBP - Kosovska Banka PristinaPBS - Privredna Banka SarajevoSBS - Stopanska Banka Skopje

BOAL- Basic Organization of Associated LaborEEC - European Economic CommunityERR - Economic Rate of ReturnFRR - Financial Rate of ReturnGMP - Gross Material Product

ICB - International Competitive BiddingLDR - Less Developed Regions (of Yugoslavia)MDR - More Developed Regions (of Yugoslavia)SDK - Sluzba Drustvenog Knjigovodstva or

Social Accounting Service

FISCAL YEAR

January 1 - December 31

* The Yugoslav Dinar has been floating since July 13, 1973; as of December 31,1979, the floating rate was Din 19.1629 = US$1.00, and as of September 1,1980 was Din 27.3589 = US$1.00, following a devaluation of 30% whichtook place in June, 1980.

FOR OFFICIAL USE ONLY

STAFF APPRAISAL REPORT ON

A FIFTH INDUSTRIAL CREDIT PROJECT

YUGOSLAVIA

Table of Contents

Page No.

PREFACE ................. ....................... . i

I. THE INDUSTRIAL SECTOR ....... *.....*......... 1

A. The Institutional Framework ...................... 1B. Industry - Characteristics and Performance ...... . 1

C. Industry in the LDR ....... 3D. Planning Objectives 5 ... .. 5

II. THE FINANCIAL SECTOR .... . .................. . 6

A. Financial Institutions .............. .......... 6B. The New Banking Law ........ .............. . 7C. Interest Rates . ... **...........*.... 7

D. The Role of the Borrowing Banks ..... .......... 8

III. THE BORROWING BANKS. ............ ........ ...... 9

A. The Banks' Structure ........................ ..... 9

B. Policies and Procedures ........ ......... 11

C. The Operations of the Banks . ......... 13

D. The Banks' Financial Situation ..... 14E. Performance Under the Previous Industrial Credit

Projects ...... ............................ 17

F. Forecast of the Banks' Operations and FinancialPerformance .............. ...................... . 19

IV. THE PROJECT .................. .... .......... . 20

A. Objectives ................. 0 .......... 20

B. Use of Loan Proceeds.. 22

C. Economic Justification. 23

D. Main Features of the Loan .............. .......... 23

V. AGREEMENTS AND RECOMMENDATIONS ....................... 28

rhis report is based on the findings of an appraisal mission composed of

lessrs. J. M. R. Feige, Z. S. Khan, S. F. Thomas (YP) and Ms. K. Nguyen,which visited Yugoslavia in October/November 1979.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contenst may not otherwise be disclosed without World Bank authorization.

Tabl1e of Contents (continued)

A.NNEXES

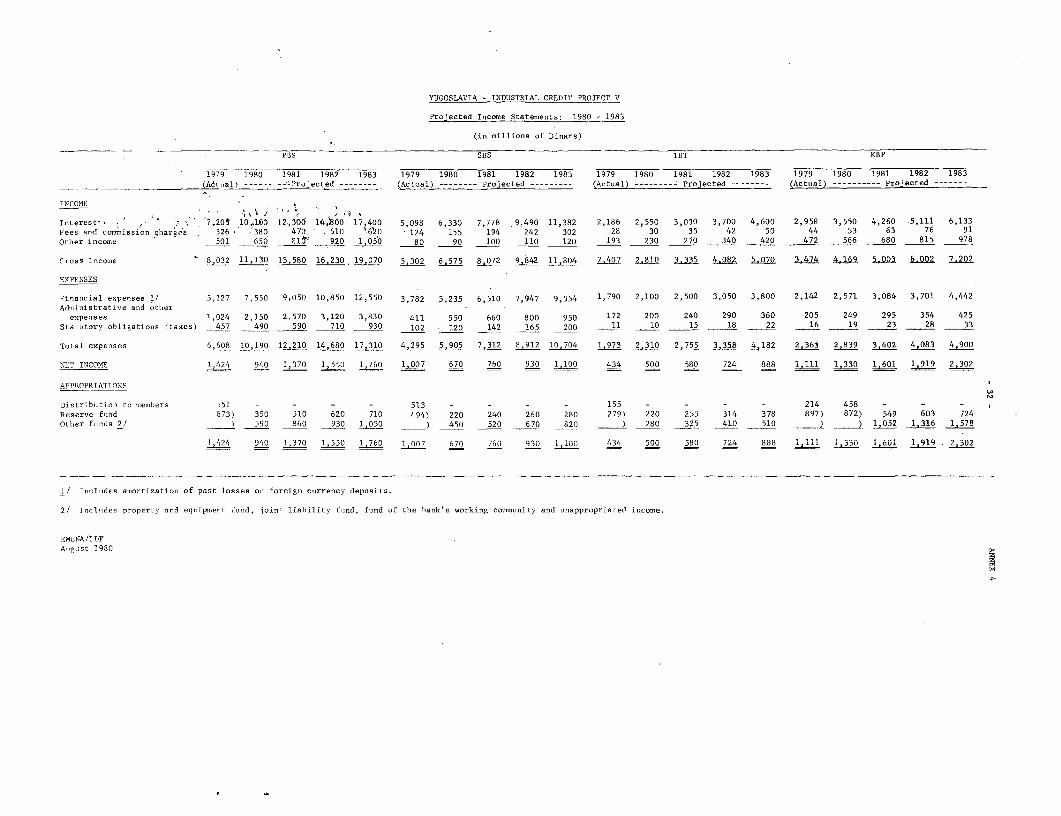

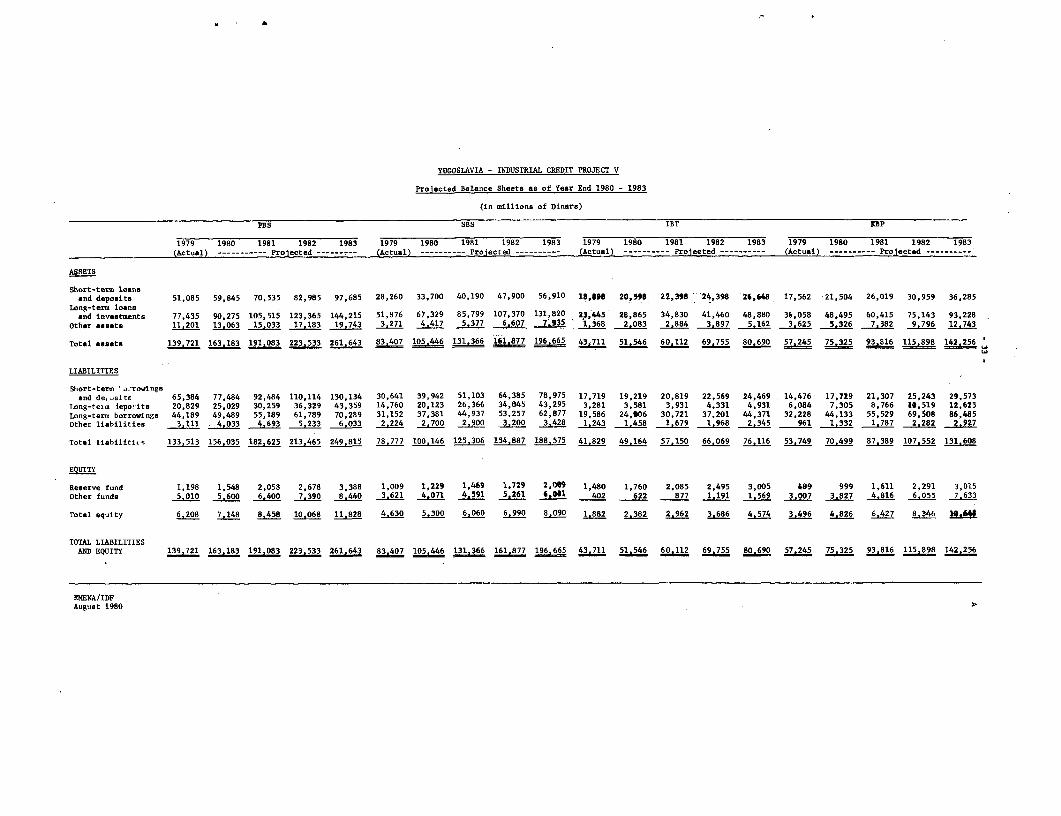

Annex 1 Statements of Income and Expenses 1977-1979Annex 2 Balance Sheets 1977-1979A-nnex 3 Statements of Sources and Applicationis of Funds 1980-1983Annex 4 Income Statements 1980-1983Annex5 Balance Sheets 1980-1983

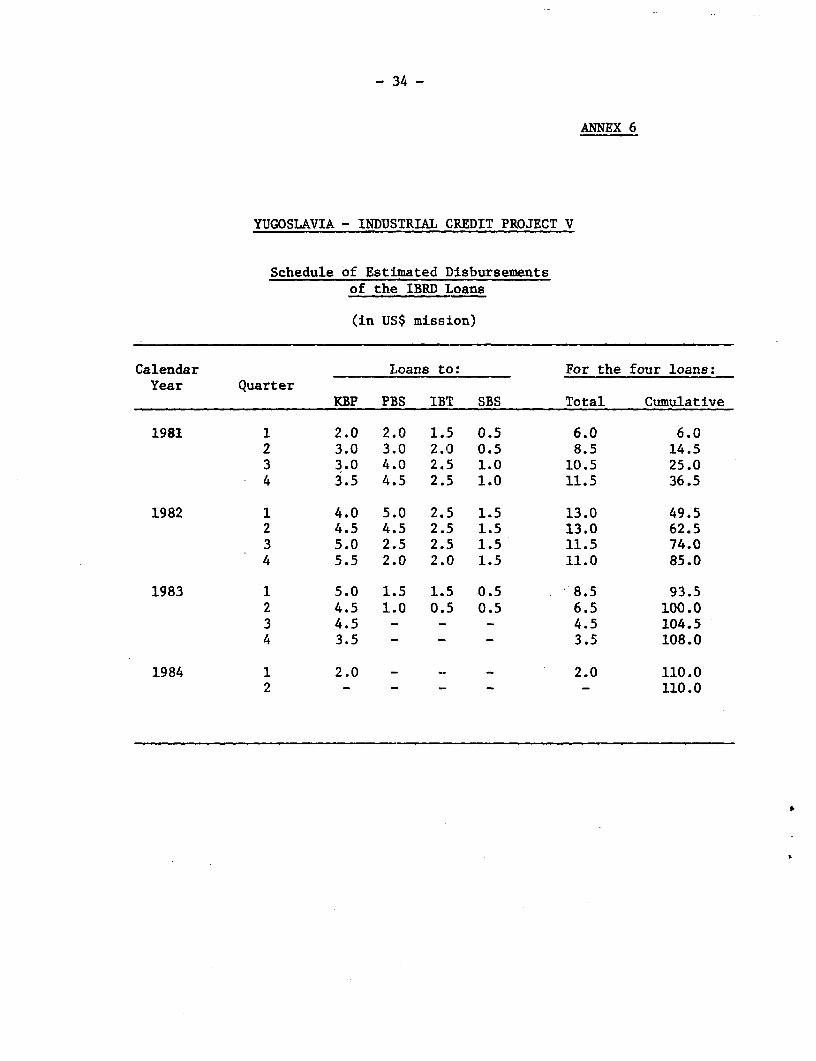

Annex 6 Projected Schedule of Disbursem.entsAnnex 7 Selected Documents and Data Available in the Project File

STAFF APPRAISAL REPORT ON

A FIFTH INDUSTRIAL CREDIT PROJECT

YUGOSLAVIA

PREFACE

This report appraises a proposed fifth industrial credit projectfor the four less developed regions (LDR) of Yugoslavia. Under the proposedloan $110 million equivalent would be lent to the four regional multipurposebanks in the LDR, which would act as intermediary lending institutions for theon-lending of the Bank funds to small- and medium-sized industrial projects 1/in the manufacturing sector, including labor intensive projects. The lendingto this sector is in line with the Bank's industrial development objectives inthe LDR. The four banks and the LDR in which they are located are the KosovskaBanka Pristina in Kosovo (KBP), Investiciona Banka Titograd in Montenegro (IBT),Privredna Banka Sarajevo in Bosnia-Herzegovina(PBS), and Stopanska Banka Skopjein Macedonia (SBS). The allocation of the loan would be $50 million for KBP,$30 million for PBS, $20 million for IBT, and $10 million for SBS.

In many respects the proposed loan is similar to the third andfourth industrial credits approved together in 1978 ($100 million total), aswell as to the second ($50 million) and first ($50 million) industrial creditsapproved in 1976 and 1974 respectively. The main differences with the previouscredits approved in 1978 are an increased emphasis on labor intensive projects(from $20 million to $27.5 million), assistance given to joint ventureprojects between enterprises in the LDR and MDR, and the elimination of a loanallocation to a special category of larger projects in the basic industriespreviously given to KBP. These larger, more capital-intensive projects wereincluded in the fourth industrial credit to assist Kosovo, the least developedLDR region, in appraising complex priority investments with Bank assistance.Since 1978 the development of new small- and medium-sized manufacturingprojects in Kosovo, and the improvement and strengthening of KBP, make itpossible to allocate the full loan component of $50 million to such projects.

The loan is directed towards manufacturing industries larger thanthose covered by the IFC investment in small scale enterprises (Reports No.IFC/P-380 and IFC/T-308 of April 23, 1980; Board approval May 6, 1980), butsmaller than those which would be considered for direct loans or investmentsby the Bank and IFC.

1/ In the Yugoslav context, to differentiate from the large enterprises inthe energy, mining, metallurgical and chemical sectors.

I. THE INDUSTRIAL SECTOR

A. The Institutional Framework

1.01 The unique institutional framework surrounding economic activitythat has evolved in Yugoslavia since the war was described in the IBRD report"Yugoslavia: Self-Management Socialism and the Challenges of Development"(No. 1615a-YU, dated March 21, 1978). The latest assessment of the Yugoslaveconomy is found in the report "Recent Economic Developments" (No. 2623-YU,dated November 1, 1979).

1.02 Yugoslavia's economic system is characterized by social ownershipand control of the means of production, decentralization of political andeconomic decision-making, and the principle of workers' self-management.The 1974 Constitution extended the principle of workers' self-management tomacro-economic decision-making. The new planning mechanism (self-managementplanning) aims essentially at giving workers more control over their workplaces and involves the harmonization of planning activities at all levels,from the smallest production units called Basic Organization of AssociatedLabor (BOAL) to socio-political entities (Communes, Autonomous Provinces,Republics, Federal Government). An important feature of the system is theparticipation of individual BOALs in various aspects of planning, includingthe source of investment funds, the ultimate disposition of retained earnings,and foreign exchange distribution. The operation of the system has been morefully described in Staff Appraisal Report No. 1865a-YU of June 23, 1978,covering the Third and Fourth Industrial Credit. A new Banking Law which hasbecome operative since 1978 is described in paras. 2.04 and 2.05 of thisreport.

B. Industry - Characteristics and Performance

1.03 Industry has been one of the principal sources of growth for theYugoslav economy since 1954. The industrial sector has continued to growvery rapidly at 7.6% p.a. during 1973-1978, as compared to the 6.2% p.a.growth registered for the economy as a whole for the same period. In 1978,industry accounted for 39% of Gross Material Product (GMP) 1/ while absorbing55% of total social sector fixed assets. Industry generated 38% of employmentand 94% of total merchandise exports. Industry is playing a particularlyimportant role in the development of the LDR (para 1.08).

1/ Gross material product or social product excludes "non-productive (inYugoslav terminology) services such as education, health, administration,defence and other public services. GDP is approximately 14% higher thanGMP.

-2-

Structure of Industry

1.04 While the industrial structure of Yugoslavia is fairly diversified,it is still characterized by the predominance of large scale basic industrieswith their pronounced capital intensive investment patterns. This is essen-tially the result of development emphasis on energy production and exploita-tion of, and processing facilities based on, the country's natural resources. a

In 1977 basic industries, namely energy, ferrous and non-ferrous metals,chemicals and pulp and paper, accounted for 56% of social sector fixed assetsbut only 32% of industrial value-added and 21% of social sector employment.

1.05 One of the notable trends in the industrial sector between 1970 and1977 is the increasing share of its annual investment in total social sectorinvestment (from 37% to 44%) leading to the rapid growth of investment infixed assets (8.4% per annum) in real terms. During the period, the energyand chemical sectors experienced sharp increases in their shares of investment,while investment shares of other sectors, notably those producing intermediatecapital goods, declined over the period. There was also a noticeable increasein value-added generated by subsectors producing final commodities, mainly atthe expense of subsectors producing intermediate capital goods. Following thepolicy of the 1976-80 (Federal) Plan of reoriienting industries towards importsubstitution of intermediate goods, during the first two years of the Plan allpriority sectors increased their shares in investment, except for the metallurgyand non-metallic mineral sectors.

1.06 The high rate of investment has enabled rapid expansion of employ-ment opportunities, particularly in the LDR where social sector employment 1/during 1975-78 grew at an annual rate of 4.5%, compared to 4.2% in Yugoslavia.Aggregate data on investment projects completed or undertaken in the indus-trial sector during 1977-78 suggest an estimated average cost per job of about$110,000, excluding working capital. Jobs created in the manufacturingindustries are the least expensive, averaging an estimated cost of $50,000 to$75,000 in the four LDR.

1.07 In 1978 industrial exports at about $5.3 billion accounted for 94%2/ of total merchandise exports. Exports are fairly diversified, with no oneindustry contributing more than 10% to total merchandise exports. Despitethe high investment growth in industry, performance of industrial exports hasbeen disappointing, with total exports increasing by only 1.4% per annum inreal terms between 1973-78, compared to a real growth of 3.1% per annum formerchandise imports. Total industrial imports in 1978 at $8.5 billion werealmost double industrial export earnings, and represented 91% of total imports.The bulk of industrial imports comprised intermediate/capital goods and rawmaterials. The large amount of industrial imports contributed to the substan-tial and worsening balance of payment deficit; the current account balance ofpayment deficit for 1979 is estimated at $3 billion (5% of GDP), up from $1billion in 1978 (2% of GDP).

1/ Most of Yugoslavia's industrial enterprises are in the social sector.

2/ Of which 17% from basic industries, and 77% from manufacturing industries.

- 3 -

C. Industry in the LDR

1.08 Over the past 30 years, the share of industry in GMP in the fourLDR grew faster than in the other regions. Though the LDR started with aconsiderably lower share of industry after the Second World War, by 1978industry's share in the GMP was 41% in the LDR compared to 38% in the moredeveloped regions (MDR). Because of the LDR's considerable wealth of naturalresources in mining and energy, basic industries have played a very importantrole in the economies of the LDR, implying a more capital intensive industrialstructure than for the MDR. Thus, for 1977 the average overall capital-outputratio for the LDR (3.6) was about 1.5 times greater than the average for theMDR (2.4), while the average value of fixed assets per worker in the LDR (Din413,000) was almost 1.2 times higher than the average in the MDR. Among theLDR, Montenegro and Kosovo continued to have the most capital-intensiveindustrial structures. In spite of their rapid development, the industries inthe LDR continue to be affected by a number of development issues which thisproject expects to tackle in part, as detailed below.

Regional Distribution of Income

1.09 Progress toward reduction of inter-regional disparities of incomehas been below expectations. The relative per capita income position of theLDR has not improved since 1970, although the earlier declining trend haslargely been stopped. The principal obstacle to bridging the gap betweenLDR and MDR has been the high population growth in the former (1.7% p.a. ascompared to 0.6% in the latter during 1971-78). Per capita GMP in 1978 forthe LDR as a group was only $1,366, compared to $2,860 for the MDR and theYugoslav average of $2,309. Kosovo, with a population increase of 3.0% perannum, remains the least developed region as its GMP per capita was 30% of theYugoslav average, and only 23% of the MDR average. The disparities are not,however, the result of stagnation in the LDR. On the contrary, the GMP growthrates enjoyed by the LDR have been generally comparable with those enjoyed bythe MDR. This growth was achieved through high rates of investment in thesocial sector (45% of GMP in the LDR, in 1977, compared to 33% in the MDR),supported by transfers of resources through the Federal Budget and the FederalFund. It is imperative that the momentum of production growth is maintained,if per capita income in the LDR is to increase. The proposed fifth industrialcredit will precisely assist in the development of manufacturing industries inthe LDR, and in Kosovo in particular.

Employment

1.10 The rate of unemployment in Yugoslavia reached 12% in 1978. Theproblem is worse in the four LDR where unemployment averaged 17%, with ahigh of 26% in Kosovo. The high rate of natural population growth, thecontinued migration from the agricultural sector, the limited inter-regionalmigration and the return of migrant workers from abroad are important causesof the LDR's employment situation. Further contributing to this problemis the high capital intensity of the LDR's investment projects. This patternresults from the continued predominance of basic industries in their economyto follow the objectives of the 1976-1980 Plan. The need to lessen and over-come the problems of unemployment and inter-regional disparities is, there-fore, seen as necessitating a policy of industrial development for the LDR

-4-

that gives a more rigorous emphasis to diversifying its industrial structureby encouraging investment in medium- and small-scale processing industries,and promoting labor intensive projects. These objectives are supported inthe proposed loan.

Exports

1.11 The weak performance of Yugoslav exports in the face of import needswill further worsen Yugoslavia's balance of payment difficulties (para 1.07).This could, in due course, constrain capacity utilization in industry.Enterprises have paid little attention to developing export strategies,preferring to sell in the easier domestic market. The steady deterioration inthe price competitiveness of Yugoslavia during the last five years is also amajor factor hindering exports; the rise in export prices of 31% for manu-factured goods between 1976 and 1978 has caused a slowdown in their exportvolume growth to only 1.5% p.a.

1.12 The deterioration in the balance of payments, accentuated by thepoor performance in 1979, raises concern. The Bank is completing a studyon balance of payment problems in Yugoslavia and on exports, and this studywill be the subject of discussions between the Bank and the Yugoslav authori-ties later this year. The Yugoslavs themselves are also undertaking a numberof studies. This project will not fully address export promotion because ofthe difficulty to propose an export strategy to the banks until the variousstudies and associated policy measures are completed and/or enacted. We haveagreed at negotiations with the borrowing banks on a work program to prepare,before future Bank industrial credit lines are considered, a study in theirregions on financing export related projects and future potential in thelight of existing policies and incentives to encourage exports. These studieswill be coordinated with the other work on developing an appropriate exportstrategy referred to above.

Other Issues

1.13 Further assistance to the LDR banks would help to strengthen theirappraisal and supervision capability further. Substantial progress has beenmade during the previous industrial credits, including adoption of Bankmethodologies for appraisals and supervision, and the start of full auditingprocedures by independent auditors. Assistancze is, however, still required,particularly in the case of the two smaller bianks, IBT and KBP.

1.14 Methods to assist joint-ventures between enterprises in the LDRand MDR, including allocation of funds, were diligently explored during theappraisal of the proposed fifth industrial cr(edit loan. By encouraging suchjoint-ventures it is hoped to speed up a transfer of technology to the LDR,increase local employment, and provide management and marketing assistanceto LDR enterprises. However, in the absence of an established system ofsuch cooperation between MDR and LDR, and taking into account the politicaldiversity between the various Republics and Provinces, it has not been possibleto agree with the Yugoslav authorities on an appropriate mechanism that wouldpermit allocating a loan component to joint-ventures under this industrialcredit loan. We will ask the Government to propose a realistic mechanism to

see whether we can make an allocation in the next loan. In the meantime,joint-ventures will be assisted by softening ;he condition for eligibility forfinancing such projects under the Bank loans.

1.15 Access by the industrial enterprises, through the banks, to inter-national sources of financing is required to supplement funding recieved fromthe Bank and other official sources. Cofinancing, which has been satisfactoryunder the previous industrial credits, should continue to be encouraged.

D. Planning Objectives

Yugoslav Plan 1981-85

1.16 The Yugoslavs are still in the process of preparing a Social Planfor 1981-85. Policy guidelines for that Plan have been published and includethe following targets: (i) continued development of socialist self-managementrelations; (ii) improved living standards and protection of the environment;(iii) strengthening of the accumulative and productive capacity of the economy;(iv) improved position in the international economic order; (v) faster rate ofdevelopment of the LDR; (vi) accelerated reduction of unemployment; and (vii)strengthening of national defense. Of particular interest for the presentproject are the objectives of reducing unemployment and regional disparitiesthrough the accelerated development of the LDR, which are in line with thoseof the Bank's previous industrial credits. (A translation of the Plan policyguidelines is in the Project File.)

1.17 A pivotal role is seen for the industrial sector in this developmenteffort. Priority sub-sectors within industry include production of basicmetals, energy based on domestic resources, basic chemicals, constructionmaterials and machinery. The rationale behind the designation of thesesub-sectors as priority areas is twofold: to have a positive effect on thebalance of payments through import substitution, and second, to eliminate somedisharmonies between primary production and processing industries. As afurther priority, the manufacture of products with a higher degree of valueadded is to be accelerated, primarily those based on domestic raw materials.

1.18 While appearing to favor import-substitution as a surer way toimproving the balance of payments situation, export promotion is also tobe encouraged. The draft Plan calls for the creation of conditions in whichexports will grow at a faster rate than the social product, noting a need fora more organized presence of the Yugoslav economy on the world market as apre-condition to ensuring a stable growth of exports.

1.19 To accelerate the development of the LDR, the transfer of resourcesfrom the developed regions to the LDR through the Federal Fund 1/ will con-tinue. A system of stimulative measures affecting the transfer of organiza-tional and technological know-how from the MDR to the LDR is also contemplated;

1/ Federal Fund for the Accelerated Development of the LDR; resources forthe Federal Fund are provided by (compulsory) loans - against a nominalinterest - given by all Yugoslav enterprises.

-6-

oint-ventures involving enterprises from the MDR and the LDR are to be encour-_ged. In addition, the development problems affecting in particular Kosovoare to be studied, with a view to determine the necessary conditions to ensurea faster growth of this Province.

Bank Objectives

1.20 The proposed Plan is therefore likely to have a number of aspectswhich would be in line with the Bank's objectives in the industrial sector,namely (i) to support the rapid development of the LDR, with special emphasison Kosovo; (ii) employment creation; (iii) to support export-oriented indus-trial projects; (iv) to further strengthen the appraisal and supervisory

capabilities of participating banks in the industrial sector; (v) to promotegreater regional cooperation through joint-ventures between enterprises inthe LDR and MDR; and (vi) to secure access to the world money markets forYugoslav industrial enterprises by encouraging co-financing.

II. THE FINANCIAL SECTOR

A. Financial Institutions

2.01 Multi-purpose banks are the dominant form of financial intermediariesin Yugoslavia, carrying out all commercial and investment banking functionsfor all sectors of the economy. Each region of Yugoslavia has such a bank,though these banks can also be active in other regions. The four proposedborrowers are in this category and, together with their member basic banks(para 2.05), handle some 80% of investment and commercial banking in theirrespective regions. In addition to these banks the financial sector includesthe National Banks, savings institutions, investment loan funds and insuranceinstitutions.

2.02 The National Banks essentially perform the role of central banksat the federal and regional levels, except that they appear to have relativelyless influence over interest rates; they do not lend directly to industrialor other enterprises, but they do provide credit to the multi-purpose banksfor financing priority activities. The main institution devoted solely toattracting savings is the Post Office Savings Bank. It accepts savingsthroughout the country, depositing the funds with the banks according toagreements reached among the Republics and Autonomous Provinces. The invest-ment loan funds consist primarily of the Federal Fund (see para 1.19) andsimilar funds within the regions. As these funds derive their resources fromobligatory loans levied on enterprise income, and transfer a substantialamount of these resources to the banks, they are mainly a media for collectingand channeling resources rather than decision-making bodies. Insuranceinstitutions have a limited role in view of the prevalence of comprehensivesocial insurance coverage. The vast majority of their resources are depositsin the banks.

- 7 -

2.03 There are few financial instruments available to potential saversother than short- and medium-term bonds issued to finance the Federal budgetdeficit and, to a lesser extent, to finance major infrastructure investments.

B. The New Banking Law

2.04 A new Federal Banking Law became effective in January 1978. Theessential change is the evolution of banks from autonomous decision-makingunits to institutions fully integrated with the organizations of associatedlabor and other organizations who are their founder-members. This change isreinforced by (a) the dual notion of joint management and profit-sharing bythe members together with unlimited liability for obligations and risk-sharing,(b) increasing independence from socio-political communities, which may not bebank members, and (c) greater linkage between sources and uses of funds.

2.05 The Law established a three-tier organizational commercial bankingstructure consisting of internal banks, basic banks, and associated banks.An internal bank is essentially a financial service organization establishedas a legal entity through a self-management agreement by two or more BOALswithin a Kombinat. A basic bank is the only banking organization which maycarry out credit and banking operations in Yugoslavia within the framework ofits own resources, and as such forms the core of the restructured bankingsystem. It can be founded by BOALs, internal banks, or other social legalentities, and in fact has tended to evolve from branches of the business bankspredating the new Law. An associated bank is established as a legal entitythrough a self-management agreement of two or more basic banks (para 3.02).Associated banks are formed mainly to concentrate resources for financingmajor investments, including IBRD projects, and to carry out foreign businesstransactions on behalf of their member basic banks. It also administers theFederal Fund allocations in its region. The associated banks of the four '-DRare the borrowers under this project. The new Banking Law has not changed afundamental principle of financial philosophy in Yugoslavia that financialresources should be controlled by the workers who use these resources in theproduction process. In fact, it has increased the scope of its application bygreater integration of the banks with the needs of their founders. It is tooearly to judge whether this reorganization will affect the decision-makingrole and autonomy of the associated banks; this is an important aspect whichwe are monitoring closely (para 4.05). The institutional aspects of the banks(legal framework, ownerships, management, policies and procedures, etc.) arediscussed in paras 3.01-3.16.

C. Interest Rates

2.06 Most of the long-term loans made from the banks' domestic sourcescarry interest rates between 3% and 10%. The annual inflation rates inYugoslavia averaged about 13% during 1977-78, and is estimated to have been22% during 1979. In real terms, therefore, the interest rates in Yugoslaviahave been traditionally negative. The projected annual rate of inflation for1980 is 30%, for 1981 is 18%, and for 1982 is 14%.

- 8 -

2.07 Interest rates in Yugoslavia are assigned a limited role in resourcemobilization and allocation. As a result, interest rates are often set at lowlevels compared to inflation rates and their structure is characterized bygeneral lack of uniformity. In order to better understand the role of interestrates in the present system of decision making in Yugoslavia, and at the Bank'sinsistence, the Government has carried out a comprehensive study which examinesin depth the effect of interest rates on resource mobilization and allocationand on capital intensity of investment. The study concludes that non-interestfactors arising out of the uniqueness of the Yugoslav system and its planningmechanism, rather than interest rate factors, predominate in setting the demandfor investment funds, allocation of resources and capital intensity of invest-ments. It finds that in the Yugoslav context, interest rates are a significantfactor only in the allocation of resources for non-priority investments whereincome maximization as opposed to social objectives is the criterion. Itconcludes that an interest rate policy should provide for higher interestrates on non-priority investments, time deposits of individuals and depositsof institutional savers. In relation to Bank loans, it argues for removal offloor rates on domestic funds to allow a lower "blended" rate to beneficiariesof Bank loans who are currently in a less favorable position than users ofdomestic and alternative foreign credits. The interest rate structure to beapplied under the proposed fifith industrial credit is given in para. 4.14.

D. The Role of the Borrowing Banks

Resource Allocation

2.08 Within the framework of the regional development plans and theirown plans, the four borrowing banks 1/ play a key role in allocating funds tosound projects. Each bank is the major lender in its region, especially forindustrial projects; at least three-quarters of institutional industrialfinancing has been channeled through these banks in recent years. This shareis expected to be maintained in the future.

2.09 The demand on the banks for financing has consistently exceededtheir resources. This has allowed the banks to be selective in choosingthe projects they will support. Under their Statutes, they have the authority,working in cooperation with the Economic Chambers, to approve, modify or rejectspecific investment proposals, whether they are included in the Plan or not.Between 10% and 30% of the projects brought to the banks either undergo majormodifications or are shelved indefinitely. The banks' impact on projectpreparation is even larger than this would suggest as many projects, especiallythe larger ones, are brought to the banks' attention at an early stage. Ifthe proposal is unattractive it is dropped at that point, or is reformulatedwith the assistance of the banks' experienced project appraisal staff into aviable project.

2.10 The banks are keenly aware of the unemployment situation and thedisparities between developed and underdeveLoped communes in their regions.

1/ Associated banks and their basic banks.

- 9 -

They therefore give priority to labor intensive projects, not only to reduceunemployment but also to provide job opportunities for emigrant workers return-ing from Western Europe. They encourage new enterprises whenever possible tolocate in the underdeveloped communes, and such communes are given advice andassistance by the banks in formulating their own investment projects.

Resource Mobilization

2.11 While the four banks compete with other banks in Yugoslavia fordomestic resources, each is dominant in its respective region. Total depositshave increased substantially in the three years up to the end of 1979, rangingfrom 96% for SBS to 253% for KBP. Most of these deposits are of a short termmaturity and, therefore, the banks have to rely substantially on the federaland regional funds to meet the medium- and long-term domestic investmentrequirements. A small portion of short-term resources have been used by PBSand IBT to meet the long-term requirements within the liquidity controlsexercised by the National Banks (para 2.02).

2.12 One of the most important activities of the banks in mobilizingforeign resources has been the issue of guarantees in favor of machinerysuppliers. At the end of 1979 outstanding guarantees in foreign currenty,including letters of credit, ranged from $405 million equivalent by IBT to$1,198 million equivalent by PBS. The banks' other efforts in mobilizingforeign resources are directed at attracting deposits of Yugoslav workersabroad and obtaining foreign loans. Foreign exchange deposits (demand as wellas savings and time) at the end of 1979 ranged from $26 million equivalentwith IBT to $562 million equivalent with PBS. Outstanding foreign loanbalances varied from $57 million equivalent at KBP to $630 million equivalentat PBS. The foreign currency loans of banks have increased several timesduring the last few years, mainly because of drawdowns under various Bankloans and borrowings from international markets to finance priority develop-ment projects. As the current account deficit is expected to continue in theforeseeable future, the banks have to continue their efforts to mobilize longterm foreign currency resources for priority development projects mainlythrough guarantees, and borrowings from international markets and the IBRD.

III. THE BORROWING BANKS 1/

A. The Banks' Structure

Legal Framework

3.01 Each bank has its own Self-Management Agreement and Statutes. Thebanks' operations are regulated by the National Bank and various Federal direc-tives, and conformity with various laws and regulations is ensured throughsupervision by the National Bank and the Social Accounting Service (SDK).

1/ In this Chapter, institutional aspects essentially relate to associatedbanks, whereas operational and financial aspects cover the combinedposition of associated banks and their member basic banks.

- 10 -

Ownership

3.02 Yugoslav enterprises in general are owned by "the society" and donot have share capital or shareholders. Banks, however, have shareholders(founders or members) and share capital (founders' fund). Members of associa-ted banks are the basic banks which, in turn, are owned by organizations ofassociated labor from most of the enterprises in the region served by indi-vidual banks. The number of member basic banks varies from 7 for KBP to 24for SBS. Each member has an unlimited liability for the obligations of itsbank (para 3.30).

Assembly and Committees

3.03 The Assembly of a bank is its highest governing body and is made upof delegates elected by its members. The Assembly approves the bank's FiveYear Plan, Annual Plan and Business Policy, including interest rates, andelects from among its delegates the Executive ard Credit Committees. It alsodecides on the distribution in aggregate of the bank's income to employees andmembers.

3.04 The Executive Committee is responsible for executing the plans andpolicies approved by the Assembly and for approving lending and borrowingoperations. In each bank, the Executive Committee has delegated authorityto the Credit Committee to approve smaller loans.

Management and Staff

3.05 The chief executive of each bank is the President of the ManagingBoard, who is appointed for a four-year term by the bank's Assembly. VicePresidents supervise two or more department Directors. Senior managementof each bank is competent. Managers are typically university graduates withmany years experience, often in both banking and industry. Changes of topmanagers are infrequent, and professional competence is the main criterionfor selection and appointment at all levels.

3.06 In mid-1979 the number of employees ranged from 173 in IBT to 448in SBS. The average rate of growth over the previous two years was 10.8%p.a. for KBP and 4.2% p.a. for SBS; the number of staff at IBT has remainedunchanged whereas PBS's staff decreased by 2%. About 40% of the staff areprofessionals, defined as those with a minimum of two years' college education.

Organization

3.07 All four banks have a similar organization. They are functionallyorganized with departments for such activities as resource planning, investmentand administration. The investment activity is subdivided into groups forindustry, agriculture, etc., with a common en;gineering department. The formerbranch offices of these banks have been given the status of basic banks underthe new Federal Banking Law. The member basic banks together with theiroffices in different towns carry out main banking functions with considerableautonomy.

- 11 -

B. Policies and Procedures

Policies

3.08 The annual business policy of each bank, approved by the Assemblyas an integral part of the bank's plan, is prepared against the backgroundof the regional development plan, the bank's own medium range plan and theplans of the basic banks and their members who are also their borrowers.The business policy covers the mobilization and allocation of resources, andthe budget for the forthcoming year.

3.09 The banks do not have formal financial policies concerning theiroperations such as exposure limits and maximum debt to equity ratio. Never-theless, the banks generally follow prudent practices. Any substantialallocation of funds, to a particular project or enterprise, has to be inaccordance with the regional plan. Debt to equity ratios are not verymeaningful in the Yugoslav context, as large amounts of Federal and Republic/Provincial Funds are available to the banks which, while treated as debt, havemore the character of managed funds.

Appraisal Procedures

3.10 The four banks use similar procedures for project appraisal. Allprojects are first examined and approved by member basic banks and those whichexceed their resources, and/or those involving federal or republic/provincialfunds, or foreign exchange, are forwarded to the associated bank for furtherdetailed appraisal and approval; these include all projects or lines ofcredit financed by IBRD funds.

3.11 All banks have qualified project appraisal and supervision staff.However, staff shortages sometimes occur because highly qualified staff tendto leave the banks to accept senior posts with enterprises. In the past, thisproblem was particularly acute at KBP, but it has taken measures to alleviatethis situation. KBP established, in 1979, an Engineering Department with fiveengineers, and created ten additional positions of economists and financialanalysts. In addition, it has appointed more translators, and this is expectedto improve the presentation in appraisal reports and thus facilitate communica-tion between KBP and the Bank. Turnover of staff at KBP has dropped sharplyas a result of new management policies. IBT is experiencing staff shortagesmore acutely, and necessary action is envisaged in this respect as discussedin paras 3.12 and 3.13 respectively. In-house and outside training programsare arranged for the staff to enhance their professional capability at all thebanks.

3.12 The quality of appraisal reports received from the banks is generallyacceptable and has shown an overall improvement, with occasional relapses.However, a further raising of standards is aimed at, particularly in economicand marketing aspects, in translation, and in technical information provided.There has been a marked improvement in the appraisals submitted by KBP. Thequality of appraisal work of IBT had shown some inconsistencies in the recent

- 12 -

past, and a few reports were far below the standard. A supervision missionvisited IBT in March 1980 and found that staff shortages, coupled with theextraordinary situation arising from the financing of a large number ofearthquake related projects on an emergency basis, was mainly responsible forthe deterioration in the appraisal work. The IBT management is consideringincreasing the number of staff, and to introduce certain procedural changeswhich will improve the quality of supervision and appraisal work. The imple-mentation of these measures will be a condition of effectiveness of the IBTcomponent of the proposed loan (para 4.25). The financial rate of return(FRR) and the economic rate of return (ERR) is calculated by the banks for allsub-projects above the free limit as well as for some of the smaller projects.

Supervision, Procurement and Disbursement

3.13 Supervision work in general is satisfactory, with the sites ofmajor projects being visited by technical and financial staff at leastevery three months, and by some banks more frequently, during construction.Financial supervision relies on monthly reports and quarterly financialstatements. However, staff shortages often Lnterfere with regular supervisionschedules. IBT in particular needs to further intensify its project super-vision work, and the Bank's last supervision mission was assured of necessaryaction, including more frequent visits to projects and a regular reportingby borrowers on the status of implementation or operations of their projects.

3.14 Procurement procedures followed by the banks are uniform andgenerally acceptable. Under Yugoslav laws, the borrower must obtain at leastthree bids for all equipment and services. Exceptions to this requirement areallowed in special circumstances, for example for Yugoslav contractors forspecialized installation work when there are less than three firms capable ofdoing the work. Large projects require international tendering. In determin-ing the most appropriate procurement procedure for any sub-project the borrow-ing banks should consider international competitive bidding (ICB), and suchICB requirements were for the first time included in Industrial Credits IIIand IV. Similar ICB requirements will have to be met under Industrial CreditV (para 4.27).

3.15 Disbursements are made on the basis of invoices from suppliers andcontractors or similar evidence of deliveries, or on the execution of con-tracts. The disbursement procedures are satisfactory.

Promotion and Project Pipelines

3.16 The banks are usually involved in the earlier, promotional aspectsof project development, both directly and through basic banks. This mayinclude technical assistance, syndication of loans, as well as assistingindustrial enterprises in financial negotiations with potential equipmentsuppliers or engineering contractors. The tentative project pipelines for allfour banks are substantial.

- 13 -

C. The Operations of the Banks 1/

3.17 The main areas of operations of the banks continue to be loans andguarantees, equity investments being negligible. Each bank also manages largeamounts of funds on behalf of the local government and other socio-politicalorganizations without bearing any risk. The overall loan and guaranteeoperations have shown a growing trend, both individually and collectively.

3.18 Short-Term Loans: The majority of short-term loans are three-monthrevolving crdits to provide working capital to enterprises and are generallymade by the basic banks from their own resources. The total short-term loancommitments of the four banks have increased from Din 81.8 billion ($4,305million equivalent) in 1977 to Din 141.5 billion ($7,448 million equivalent)in 1979. The short-term loans were 70% of the total loan commitments duringthe 1977-1979 period. During 1979, short-term commitments ranged from Din 4.5billion ($237 million equivalent) at IBT to Din 87.9 billion ($4,626 millionequivalent) at PBS, which was broadly consistent with the past trend.

3.19 Long-Term Loans: Commitments for long-term loans (above one year'smaturity) of the four banks decreased from Din 48.5 billion ($2,552 millionequivalent) in 1977 to Din 36 billion ($1,893 million equivalent) in 1978, butincreased to Din 54.1 billion ($2,846 million) in 1979. Long-term loancommitments were exceptionally high in 1977, mainly due to investments byPBS and IBT in a few very large projects. During 1979, the long-term loancommitments ranged from Din 8.6 billion ($424 million equivalent) for IBT toDin 18.5 billion ($974 million equivalent) for KBP. Industrial loans accountedfor 68% (59% for SBS to 83% for KBP) of the total long-term loan commitmentsmade in 1979 but the average foreign exchange portion of these loans was smallat 16% of the total loan amount. The enterprises met the remaining foreignexchange requirements through suppliers' credits and/or their own foreignresources.

3.20 Guarantees: The total amount of guarantees provided by the fourbanks in favor of enterprises in 1979 amounted to Din 58 billion ($3,051million equivalent) which was 57% more than in 1978. The guarantees hadincreased by 22% in 1978. PBS contributed to 61% of all guarantees issued bythe four banks during the 1977-1979 period, but its foreign currency share isestimated at about 20%. The other three banks had issued, on an aggregate,more than half of their guarantees in foreign currency. The industrial sectorreceived 69% of the total guarantees during the 1977-1979 period.

3.21 The total financial assistance extended by the four banks has notincreased significantly in real terms considering the inflation rate inYugoslavia.

1/ Covers the combined position of associated banks and their memberbasic banks. Exchange rate used is Din 19.00=US$1.00.

- 14 -

D. The Banks' Financial Situation 1/

Resource Position

3.22 A summary of the long-term resource position as of December 31, 1979is given below:

Table 1: LONG-TERM RESOURCE POSITION AS OF DECEMBER 31, 1979(In millions of Dinars)

PBS SBS IBT KBP

Equity 4,741 3,886 1,335 1,983Federal and Regional Funds 27,172 21,222 8,735 28,304Long-term Borrowings 20,927 17,110 10,735 7,389Long-term Deposits 20,829 14,760 3,281 6,084

Total Resources Available 73,669 56,978 24,086 43,760

Long-term Portfolio 88,876 57,341 27,257 40,121Undisbursed Resources (15,207) 637 (3,171) 3,639Undisbursed Long-term

Commitments 13,597 24,615 3,673 8,367Uncommitted Resources

(Overcommitments) (28,804) (23,978) (6,844) (4,728)

3.23 The largest source of funds for the four banks are Federal andRegional Funds which accounted for 36% (IBT) to 65% (KBP) of their long-term resources. A cautious usage of short-term funds for long-term loans isallowed under Yugoslav law. PBS and IBT have used short-term resources tofinance long-term loans and investments. All the banks had substantiallyovercommitted themselves, but the overcommitments will be covered largely byFederal Fund resources which the banks will receive on a yearly basis inaccordance with the Plan (para 1.19).

Financial Performance

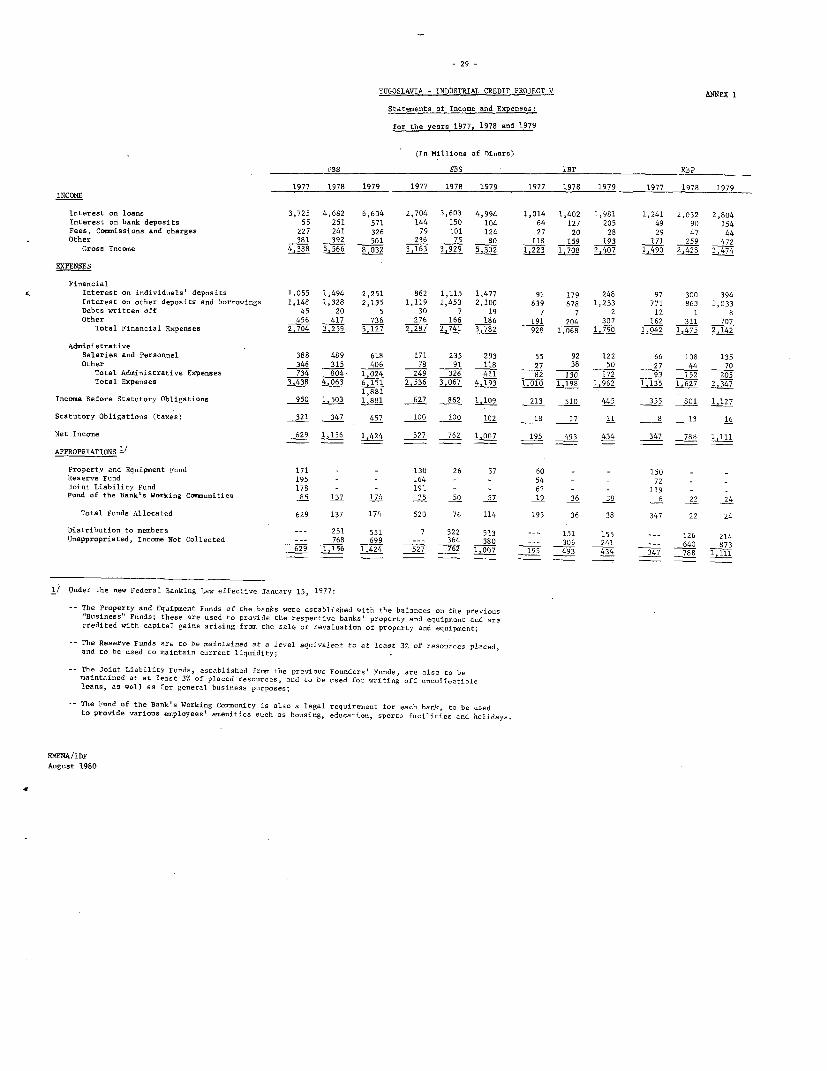

3.24 The comparative income statements of the four banks for 1977,1978 and 1979 are given in Annex 1. The banks in Yugoslavia are not profitmaximizers; they are expected to earn an income which is adequate to covertheir expenses and to make required allocations to various reserves. Againstthis background, the net income of the four banks has been more than adequate.It has shown an increasing trend during the last few years, except for a

1/ Covers consolidated position of associated banks and their member basic

banks.

- 15 -

slight decline for IBT in 1979. During 1975-September 1978, the four bankssuffered foreign exchange losses ranging from Din 100 million ($5.3 million)for IBT to Din 1,623 million ($85.4 million) for PBS on foreign currencysavings accounts due to currency revaluation. These losses were originallyexpected to be reimbursed by Federal sources and were, therefore, treated asan accrued income. However, a law effective June 16, 1979, stipulates thatthe bulk of these losses will be borne by the banks and amortized over aperiod of up to 40 years. Although the above procedure is not consistent withthe generally accepted accounting principles, the banks are saved from asudden decrease in their current income and equity. Besides, the aforemen-tioned law provides for the protection of banks from such losses in future.

3.25 During 1977-1979, the average interest spread was between 2.0%(SBS) to 3.5% (KBP) whereas administrative expenses when related to totalaverage assets were between 0.4% (KBP) to 1.0% (PBS). The banks have maderequired allocation to various reserves out of net income. The banks startedin 1978 the distribution of a significant portion of their net income tomembers to comply with the new Federal Banking Law. The payout ratio (pay-ments to members as percentage of net income) ranged from 19% (KBP) to 51%(SBS) in 1979.

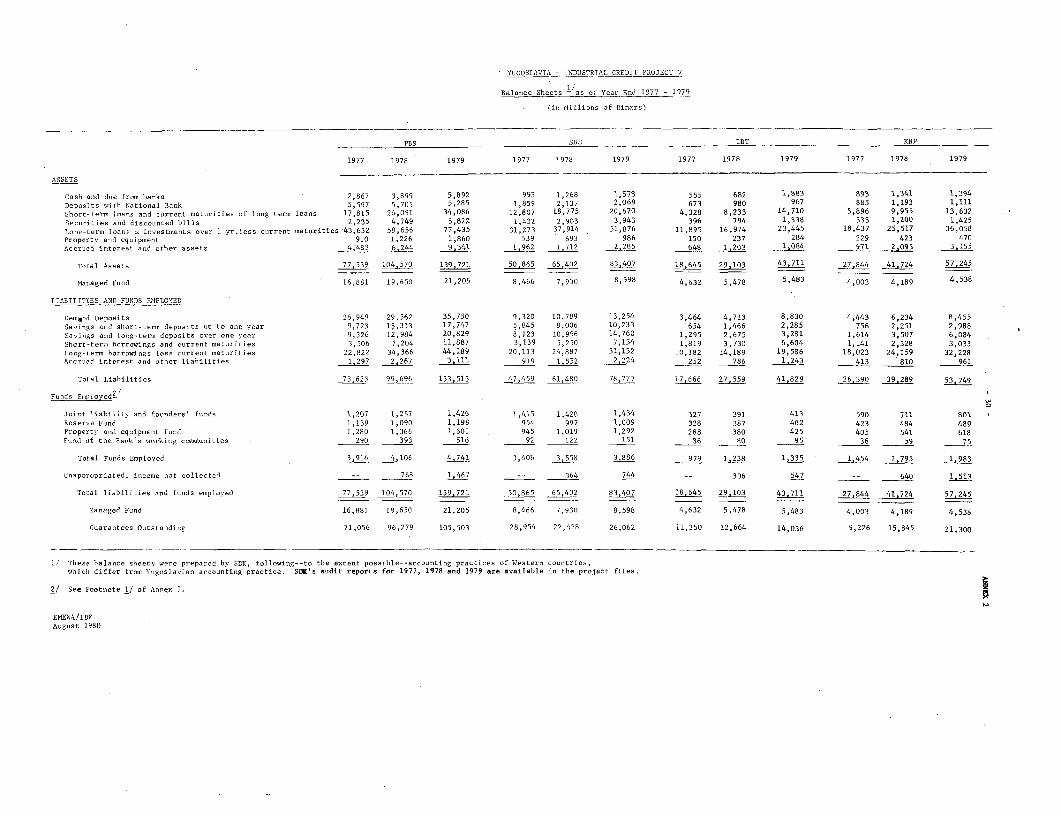

Financial Position

3.26 The comparative balance sheets of the four banks for December 31,1977-1979 period are given in Annex 2. As of December 31, 1979, the totalassets ranged from Din 43.7 billion ($2,301 million equivalent) (IBT) to Din139.7 billion ($7,354 million equivalent) (PBS) of which the long-termloan portfolio ranged from 56% at PBS to 63% at KBP. As a result of rapidlygrowing operations, total assets increased by 64% (PBS) to 134% (IBT) duringthe 3-year period ended December 31, 1979. The liquidity positon of the banksis regulated by the National Bank of Yugoslavia together with the regionalnational banks and this is supervised by SDK. Long term debt/equity ratiosas of December 31, 1979 were high for all banks, ranging from 12.6:1 for SBSto 19.4:1 for KBP. However, if the Federal and Republic/Provincial Funds areexcluded from the debt/equity calculations in view of their special nature(see para 3.09), the maximum and minimum ratios would reduce to 11.2:1 (IBT)and 5.2:1 (KBP) respectively.

Arrears

3.27 The arrears on long-term loans of the four banks are presented in thefollowing table:

- 16 -

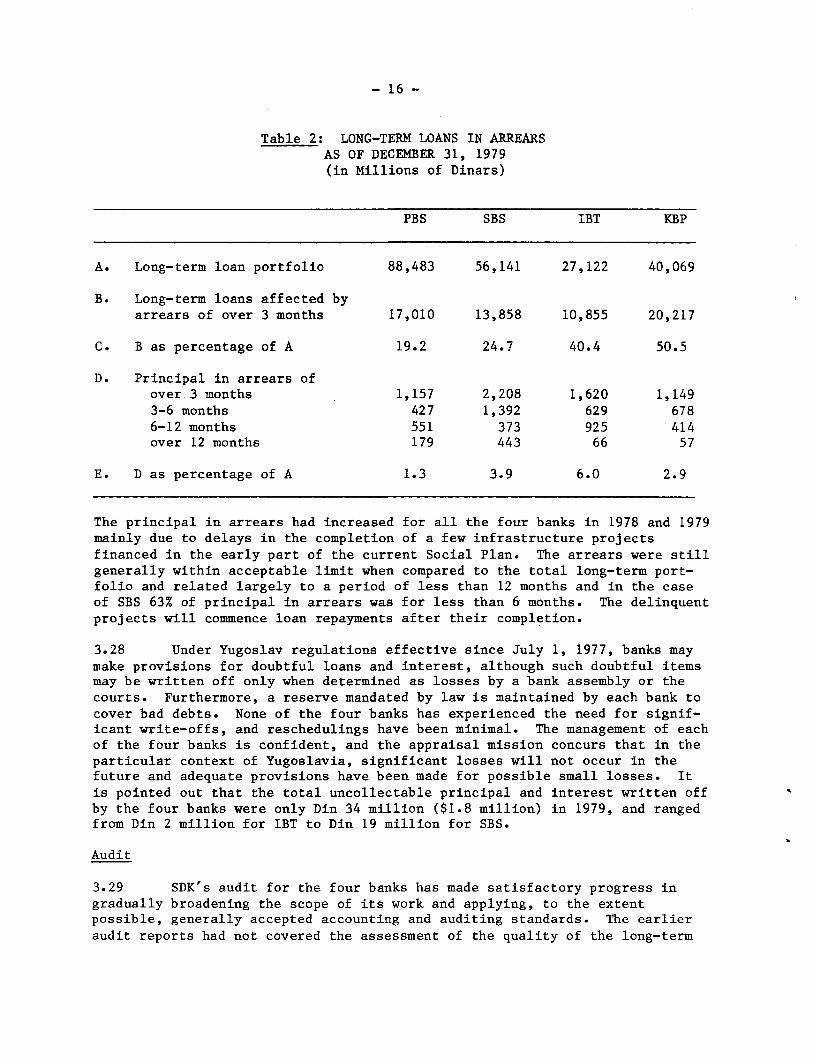

Table 2: LONG-TERM LOANS IN ARREARSAS OF DECEMBER 31, 1979(in Millions of Dinars)

PBS SBS IBT KBP

A. Long-term loan portfolio 88,483 56,141 27,122 40,069

B. Long-term loans affected byarrears of over 3 months 17,010 13,858 10,855 20,217

C. B as percentage of A 19.2 24.7 40.4 50.5

D. Principal in arrears ofover 3 months 1,157 2,208 1,620 1,1493-6 months 427 1,392 629 6786-12 months 551 373 925 414over 12 months 179 443 66 57

E. D as percentage of A 1.3 3.9 6.0 2.9

The principal in arrears had increased for aLl the four banks in 1978 and 1979mainly due to delays in the completion of a few infrastructure projectsfinanced in the early part of the current Social Plan. The arrears were stillgenerally within acceptable limit when compared to the total long-term port-folio and related largely to a period of less than 12 months and in the caseof SBS 63% of principal in arrears was for less than 6 months. The delinquentprojects will commence loan repayments after their completion.

3.28 Under Yugoslav regulations effective since July 1, 1977, banks maymake provisions for doubtful loans and interest, although such doubtful itemsmay be written off only when determined as losses by a bank assembly or thecourts. Furthermore, a reserve mandated by :Law is maintained by each bank tocover bad debts. None of the four banks has experienced the need for signif-icant write-offs, and reschedulings have been minimal. The management of eachof the four banks is confident, and the appraisal mission concurs that in theparticular context of Yugoslavia, significant: losses will not occur in thefuture and adequate provisions have been made for possible small losses. Itis pointed out that the total uncollectable principal and interest written offby the four banks were only Din 34 million ($1.8 million) in 1979, and rangedfrom Din 2 million for IBT to Din 19 million for SBS.

Audit

3.29 SDK's audit for the four banks has made satisfactory progress ingradually broadening the scope of its work and applying, to the extentpossible, generally accepted accounting and auditing standards. The earlieraudit reports had not covered the assessment of the quality of the long-term

- 17 -

loan portfolio. For the first time, in 1978, SDK performed a detailed port-folio analysis covering loan arrears and rescheduling of PBS and SBS. Arelatively brief reviev of the portfolio was done for IBT and KBP because oflack of adequate data. SDK performed the detailed portfolio analysis of allthe four banks in 1979 as a part of their annual audit. The audit arrange-ments are considered satisfactory, particularly as SDK has expanded itsin-depth coverage of the banks' operations.

Creditworthiness

3.30 Conventional assessments of creditworthiness are not appropriatein the Yugoslav banking system. The assessment of creditworthiness is basedon the same arguments that were advanced for the previous Industrial Creditswhich are the following:

(a) Loan losses in the past have been insignificant and the arrearsposition is manageable;

(b) The management of each bank observes sound banking principlesin respect of resource management and project selection;

(c) The continued solvency of each bank is assured for the followingreasons:

(i) The basic member banks and, in turn, their founder membershave unlimited liability for the associated banks' obliga-tions;

(ii) Under the existing Yugoslav economic system each bank'screditworthiness is closely related to that of the Yugoslaveconomy itself. The possibility of a bank failure isconceivable only with the concurrent failure of the entireeconomic system.

E. Performance Under the Previous Industrial Credit Projects

3.31 The Bank has so far provided four industrial credit lines toYugoslavia and their utilization has been generally satisfactory. The firstcredit line ($50 million) has been fully committed and disbursed, althoughbehind the originally anticipated schedule. The commitments under the secondcredit line have been completed, but the last date for disbursements has beenextended by one year to cover final payments to be made upon satisfactorycompletion of initial operations of certain subprojects.

3.32 The second industrial credit project resulted in a total investmentof $230.7 million in 65 subprojects covering a wide variety of manufacturingindustries. Fifteen Bank-financed subprojects above the free limit and elevensubprojects below the free limit received foreign currency cofinancingtotalling $29.1 million equivalent (58% of the total Bank loan amount of

- 18 -

$50 million). The estimated average total cost per job created by thesesabprojects was $39,804 in 1979 prices, which is a satisfactory figure in viewof the advanced stage of economic development of Yugoslavia. For comparison,the average fixed investment cost per job created in the industrial sectorexcluding the capital intensive, basic industry (sub-sectors of electricity,coal and petroleum) in the LDR during 1974 and 1975 was $52,100 equivalent in1977 prices. Total employment created in projects partly financed under theSecond Industrial Credit is estimated at 7,400 jobs. The financial rate ofreturn (FRR) estimated by the banks for subprojects financed under the SecondIndustrial Credit project ranged from 14% to 50%, with 75% of the subprojectshaving FRR of 18% or above. The estimated economic rate of return (ERR) forsubprojects above the free limit ranged from 15% to 41%, with 75% of thesesubprojects having an ERR of 20% or above. The above FRR and ERR comparefavorably with the agreed minimum of 11%.

3.33 As of December 31, 1979, $67 million were committed for 40 sub-projects under the $100 million Third and Fourth Industrial Credit projects.These sub-projects will result in a total long-term investment of $256 millionequivalent. Of the 40 subprojects, eleven subprojects above the free limitand ten subprojects below the free limit received total foreign currencycofinancing of $24.7 million equivalent (41% of Bank loan commitment as ofDecember 31, 1979). The cost per job created ranged between $5,400 and$172,000, with the-average cost per job creatied by subprojects calculated as$31,297 in 1979 prices, which is considered satisfactory. Total employ-ment created by projects financed under the Third and Fourth IndustrialCredit is estimated at 12,200 jobs. The FRR and ERR of these subprojectsranged from 12% to 41%, and 12% to 47%, respectively, with 75% of sub-projects having a FRR of 16% or above, and an FRR of 20% or above. Thesesubprojects are thus both financially and economicallay viable, and theirFRR and ERR were well above the minimum agreed limit of 11%. Commitments hadincreased to $86.5 million as of September 1, 1980.

3.34 Out of the third and fourth industrLal credit, $20 million ($5million by each bank) were to be used for labor-intensive subprojects, i.e.those creating jobs at a cost of less than $23,000 equivalent each. As ofSeptember 1, 1980, the four banks had committed $19.0 million for suchprojects and the average cost per job therein was about $18,300.

3.35 Disbursements under Industrial Credits III and IV (Loans 1611-YUthrough 1614-YU) have been very satisfactory. As of September 1, 1980, dis-bursements were about 25% higher than those expected at the time of appraisal,indicating the absorptive capacity in the LDR for the Bank financing provided.Of the technical assistance component of $0.3 million provided to KBP under thethird industrial credit, about one-half has already been used to pay forshort-term consultancy assignments for (i) an evaluation of the lead metallurgyspecial projects financed under this credit (consultants fees @ $8,000 perman-month approximately), and (ii) for a consultant's study in connection withthe preparation of a new agro-industry project (consultants fees @ $11,000 perman-month).

- 19 -

3.36 In addition to partly filling the foreign currency resource gap ofthe recipient banks, the Bank's industrial credit projects have also beeninstrumental in the institution-building of these banks. The quality of theirproject appraisal has shown an overall improvement (para 3.12). Besides,steps are being taken to further improve the economic and market appraisal ofsubprojects. As agreed with the Bank during negotiations for the third andfourth industrial credit projects, the four banks have also initiated anannual portfolio analysis and this is being covered by SDK in its auditreports (para 3.29).

F. Forecast of the Banks' Operations and Financial Performance 1/

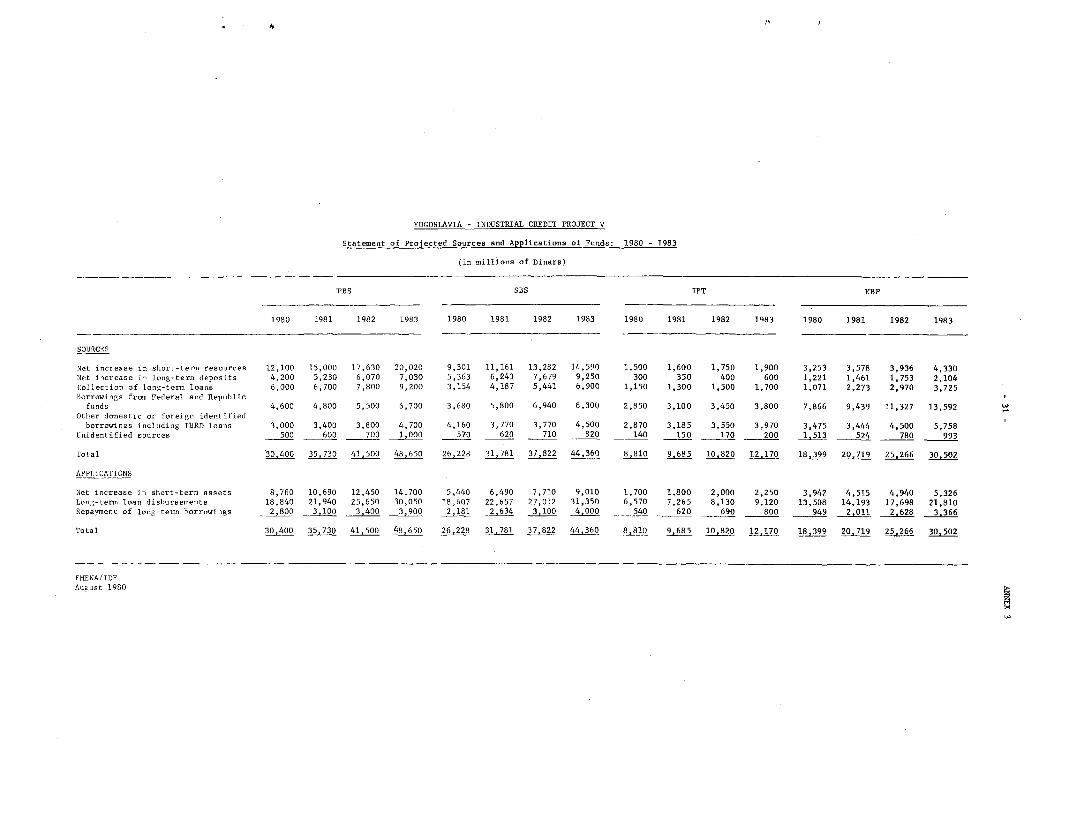

3.37 At present, all the four banks are preparing separate medium-termplans for the 1981-1985 period. Each plan, which is also linked to theregion's plan, will form the basis for the preparation of financial projectionsupon its finalization. Pending completion of this planning exercise, onlytentative financial projections for 1980-1983 could be used to support thepresent appraisal. These projections are based on projects in the pipeline,past performance of individual banks as well as regional economic trends, andtake into account the devaluation of Dinar in June 1980. These projections asgiven below will be modified upon the finalization of the mid-term plans, butare considered acceptable in the meantime. Projected cash flows, incomestatements, and balance sheets are given in Annexes 3, 4 and 5.

3.38 Short-term Lending Operations. PBS and IBT project average growthof short-term loans at about 11% p.a., whereas SBS and KBP project averagegrowth of about 18% p.a. The projected growth rates are almost consistentwith past performance during 1974-1979 except for PBS which had achievedan average annual growth rate of 29% during the said period.

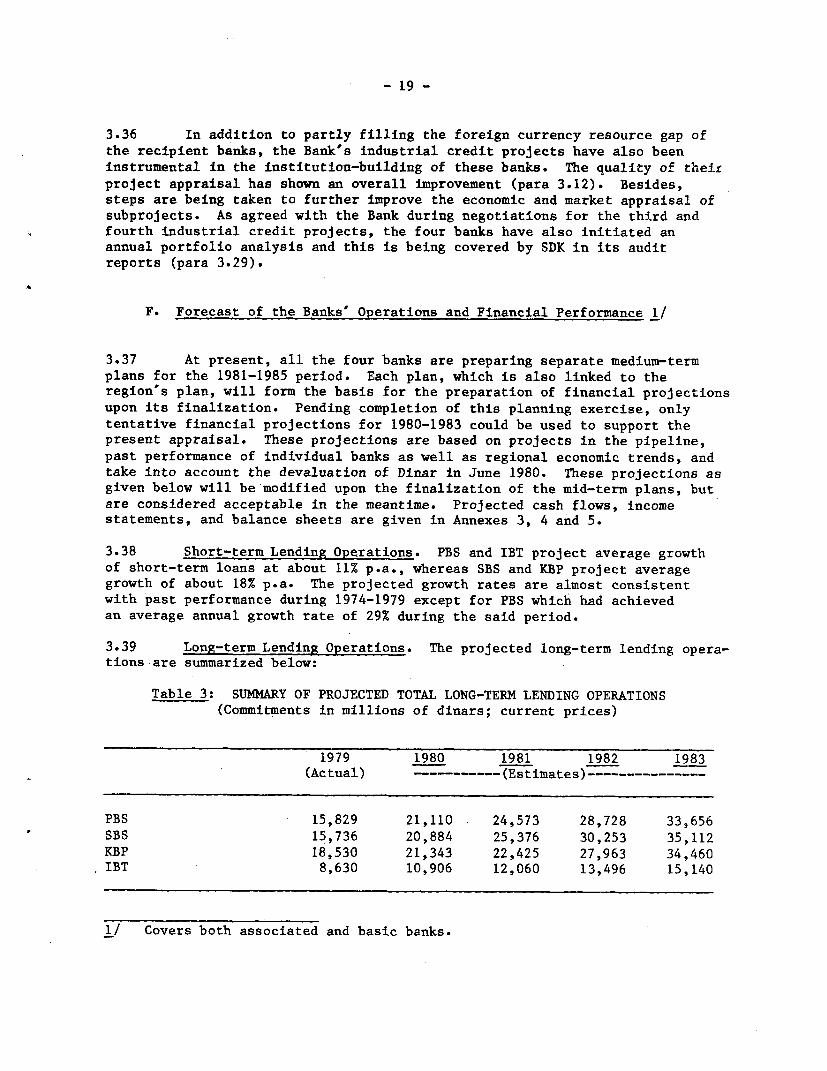

3.39 Long-term Lending Operations. The projected long-term lending opera-tions are summarized below:

Table 3: SUMMARY OF PROJECTED TOTAL LONG-TERM LENDING OPERATIONS(Commitments in millions of dinars; current prices)

1979 1980 1981 1982 1983(Actual) ------- -- (Estimates)---------------

PBS 15,829 21,110 24,573 28,728 33,656SBS 15,736 20,884 25,376 30,253 35,112KBP 18,530 21,343 22,425 27,963 34,460IBT 8,630 10,906 12,060 13,496 15,140

1/ Covers both associated and basic banks.

- 20 -

The long-term loan commitments are expected to increase between 12% (IBT) and19% (SBS) per annum. The industrial sector is expected to receive 61% oftotal commitments during the 1980-1983 period.

3.40 Resource Requirements. The resource mobilization plans of the fourbanks are considered acceptable. The banks will continue to rely signif-icantly on Federal and Republic Funds to meet their fund requirements. During1980-1983, KBP and IBT expect to meet respectively 45% and 32% of theirrequirements from the said Funds.

3.41 PBS and SBS will meet 14% and 18% of their requirements from thesefunds. They will continue to use a part of their short-term resources forfinancing long-term loans. In view of the growth trend of short-term depositsand the adherence to the liquidity requirements of the National Bank, theusage of short-term funds as projected would not pose a problem for the twobanks.

3.42 Financial Projections. Each bank intends to continue the main-tenance of a spread just sufficient to cover administrative expenses andmandatory provisions. The projected liquidity position of IBT and KBP isconsidered satisfactory with the current ratio ranging between 1.1 to 1.2.Due to the use of some short-term funds to finance long-term loans, thecurrent ratio of PBS and SBS would be between 0.7 and 0.8, which is stillacceptable as mentioned in para 3.41, although this matter and underlyingtrends will be more closely scrutinized as part of the overall assessment ofthe bank's creditworthiness and performance (para 4.05). The long-termdebt/equity will continue to rise since the banks will be building up theirequity only to the extent required by law. IHowever, in the context of theYugoslav economic system, the crucial question is not the size of the banks'own funds (equity) but the financial strength of the borrowing banks in awider sense, as discussed in para 3.30. Under these premises, the four banksare expected to remain creditworthy in th foreseeable future.

IV. THE PROJECT

A. Objectives

4.01 The proposed project will: (i) prcvide foreign exchange resourcesto the LDR of Yugoslavia to finance industrial enterprises, in order to accel-erate the LDR economic development; (ii) provide additional job opportunitiesto reduce unemployment; (iii) assist the four banks, and in particular IBT andKBP, to continue to strengthen their institutional capabilities. In addition,the project provides for an in-depth analysis of the achievements of the indus-trial credit loans, extended since 1974 to the same four banks, as part of thepreparation of the first completion report on these loans. Such an in-depthanalysis will become feasible and meaningful on the basis of the first full

- 21 -

audit report on the four banks received in August 1980. Finally, an agree-ment has been reached on a work program to prepare for further industrial

credit lending.

4.02 The $110 million loan proposed under the project will materiallyassist the LDR, and Kosovo in particular, to continue their industrial devel-opment program. In line with the previous industrial credits, cofinancingwill be encouraged by allowing longer grace periods on the sub-loans and,

based on past performance, it is estimated that a further $45 million in

foreign exchange cofinancing will be attracted in conjunction with Bank

financed projects. Joint-ventures will be encouraged by allowing longer grace

periods and higher total projects costs.

4.03 On the basis of past experience, but taking into account the pro-

jected dollar inflation rate 1/ for equipment to be financed under this project,it is estimated that the $110 million loan will assist in the creation of

projects with a total employment of about 11,000, at an average cost of

$38,000 equivalent (see also para 4.10). By way of comparison, the historical

cost per job created in the industrial sector in Yugoslavia in 1977 was

$110,000 overall (para 1.06).

4.04 With reference to paras 3.32 and 3.33, it should be noted thatin spite of the increasing technological sophistication of the Yugoslav

manufacturing industry, the Bank's industrial credit loans have succeeded inthe objective of increasing employment. The cost per job created underIndustrial Credit II ($31,175 at 1977 prices) would be $39,804 at 1979 prices,

while the cost per job created under Industrial Credit III and IV at 1979prices was only $31,297. Based on the tentative projections for IndustrialCredit V a similar cost per job (at 1979 prices) will be achieved under theproposed loan.

4.05 The four banks have shown increasing maturity in their projectappraisal and supervision work, except for occasional relapses due to staffconstraints, particularly at IBT and KBP. Further association with the Bankwill be beneficial in increasing the critical appraisal capabilities of the

banks, particularly concerning the economic and technical aspects of projectspresented to them. Since the first industrial credit was approved in 1974,

the four banks have shown, in general, a commendable progress in their opera-tions as intermediary lending institutions. Audits were gradually introduced,and in August 1980 we received the first full audit on all four banks by SDK.

A study on the role of interest rates in Yugoslavia, instigated at the requestof the Bank, was completed by the Yugoslavs earlier this year and is nowunder joint discussion. The new Banking Law (para 2.04 and 2.05) has resultedin internal reorganizations of the four banks, of which the effects areslowly being felt. Finally, an economic mission has visited Yugoslavia

I/ 14.0% (1978); 12.0% (1979); 10.5% (1980); 9.0% (1981); 8.0% (1982); 7.0%(1983).

- 22 -

this summer to review the prospects for small scale and labor intensiveindustries. The information resulting from the above will enable us toconduct an in-depth analysis of the banks in conjunction with the prepara-tion of the first Project Completion Report on the industrial credits.

B. Use of Loan Proceeds

4.06 It is proposed to allocate $50 milLion to KBP, $30 million to PBS,$20 million to IBT and $10 million to SBS, of which 25% will be for laborintensive projects, as follows:

Loan Allocation(Millions US$) KBP PBS IBT SBS Total

Labor intensive projects 12.5 7.5 5.0 2.5 27.5Normal projects 37.5 22.5 15.0 7.5 82.5

50.0 30.0 20.0 10.0 110.0

4.07 This distribution, reached in consultation with the Yugoslavauthorities, stresses the continued importance given to the development ofKosovo, which is in line with the Bank's objectives. The smaller amountfor SBS reflects the high allocation of overall Yugoslav foreign exchangeresources already made by the Federal Government to Macedonia. There islittle doubt that the proceeds of the Bank's loan will be utilized quickly.

4.08 It is gratifying to note that KBP, which in the past has haddifficulty in committing and disbursing its Bank loan share, has shown amarked improvement under Industrial Credit IV, following a strengthening ofits staff. Not only are disbursements well ahead of appraisal estimates(para 3.25), but its pipeline of medium sizedL industrial projects is nowsubstantial. As a consequence, no provisions have to be made to allow KBPto finance large "special", capital intensive projects in basic industries,as was the case under the previous industrial credit, to enable it to usethe full proceeds of the proposed Bank loan. The improvements in KBP werein part the results of exceptionally close monitoring and supervision by theBank in 1979, after KBP's performance had seriously deteriorated. We arecurrently turning our attention to IBT, where a somewhat similar effort isneeded (para 3.12).

4.09 A minimum of 25% of the funds loaned to each bank would be allocatedfor exclusive use in financing labor-intensive projects. As the purpose ofthese projects is to provide employment at low cost, there would be no limita-tions on the size of the subprojects, or the sub-loan size; besides the usualtechnical, financial and economic criteria applicable to all sub-loans, theonly condition would be that the projects provide jobs at a cost of no morethan $31,000 equivalent. This figure was arrived at by updating for infla-tion the labor-intensive criteria used under the previous industrial credit.It is expected, based on the experience under the previous industrial credits,

- 23 -

that the average actual cost per job for such labor-intensive projects financedby the Bank will be $24,500. The remainder of the loan would be used forother small and medium size industrial projects. There would be limits onthe size of the project and of the sub-loan (para 4.19) for other than labor-intensive projects.

C. Economic Justification

4.10 The main justification at the macroeconomic level for the proposedloan is the creation of additional employment, a priority need in all theLDR, and to correct regional disparities in development and standards ofliving. The emphasis on maximizing the number of jobs will result in approxi-mately 3,800 of the total number of 11,000 jobs being created at a cost of about$24,500 each (para 4.09). The proceeds of the loan will not be used tofinance projects in basic industry, which are relatively capital intensive,but instead will be used to diversify the industrial structures of the LDRwhich are skewed toward basic industries.

4.11 At the project level, the ERR of subprojects to be financed isexpected to be between 12% and 40%, based on the experience gained underthe past industrial credits. About half of the projects are expected toattract foreign exchange cofinancing equivalent to about 40% of the Bank'stotal commitments; some projects might also involve foreign cofinancing forlocal cost, a form of financing permitted under Yugoslav regulations.

D. Main Features of the Loan

Loan Amount and Period of Commitment

4.12 The amount of the proposed loan, $110 million, has been establishedwithin the framework of the total Bank lending program to Yugoslavia. Itwill only provide about 3.5% of the four development banks' total industriallending program. In industrial development banking lending, projects are onlytentatively identified at the time of appraisal and negotiations, but on thebasis of project data submitted by the four banks it would appear thatmost of the total Bank loan amount will be utilized well within the usual2-1/2 year commitment period for such loans. To allow for some small paymentsdue only on completion or after start-up of certain projects, a three-yearcommitment period from the date of the signing of the Loan Agreement isrecommended.

Use of Proceeds

4.13 The loan proceeds will be used, together with other sources, tofinance the foreign exchange cost of fixed assets and permanent working capital

- 24 -

(and in rare instances the local cost--see para 4.27). As with the recentlyapproved Third Agricultural Credit project, subprojects must meet a minimumFRR and ERR of 12%.

Interest Rates

4.14 The interest rates for onlending in the project will be as follows:

(a) For Bank funds, the onlending rate will be set to reflectthe cost of alternative foreign exchange loans, which approxi-mates 11% with the subborrower bearing the foreign exchangerisk;

(b) For the portion of domestic funds which are provided fromthe banks' own resources (the mobi]Lization and allocation ofwhich are interest elastic) floor rates will continue to bespecified as they have been in recent agricultural andindustrial credit projects. For the present project the floorrate would be increased to 10 percent, or about 3 percentmore than the current minimum level of 7 percent charged bythe banks, with provision for an annual review during thecommitment period of the loan;

(c) For the portion of domestic funds provided from speciallyearmarked funds (the mobilization and allocation of which areinterest inelastic) no floor rates would apply and the ratescurrently applicable to such funds (3-7 percent) would continue.Most of these funds are mobilized on the basis of obligatory contri-butions in the form of long-term loans, imposed on enterprises inYugoslavia to meet specific social objectives.

4.15 The above represents no change in the Bank's position with respectto the on-lending rate for Bank funds in recent industrial and agriculturalcredit projects, but it represents a modification with respect to the lendingrate for domestic funds. Under previous Bank loans, a floor rate of 6 percentwas set on domestic funds, i.e., the weighted average of rates on the banks'own funds and spcial funds for each subloan had to be at least 6 percent. Thecurrent proposal was arrived at after giving due consideration to the recentlycompleted study on the role of interest rates in the Yugoslav economy (para.2.07), the Bank's policy in relation to real interest rates, and specificcountry considerations.

4.16 The recommended lending rates embody both the principles of movingtowards positive real rates on the banks' own resources, while acknowledgingthe Yugoslav principle of directing specially earmarked, low-cost funds topriority projects. Our proposals may lead to blended domestic lending ratesthat could be marginally lower than under previous Bank loans if the Yugoslavbanks drastically increase the proportion of specially earmarked funds tofinance subprojects under this project. In oiur view, however, while this ispossible, any such increase is restricted by ithe limited availability of suchfunds, and by the intensely competing claims by subborrowers for them.

- 25 -

Administrative Arrangements

4.17 Similar to previous arrangements, administrative functions willbe handled by a joint Unit consisting of four Sub-Units, one from each bank.Each Sub-Unit will consist of a suitable number of appropriate staff membersfrom its bank. The Unit will coordinate those activities under the proposedprojects and the previous industrial credit projects which involve all fourbanks. These include ensuring systematic and consistent preparation ofprogress reports and the promotion within the banks of improved appraisaland supervision methodology, including the organization of periodic seminars.The individual Sub-Units will handle those matters which affect only onebank.

4.18 Sub-loan applications to IBRD for sub-projects under the proposedloans will be submitted directly by each bank. The Sub-Unit of the banksubmitting a sub-loan application will ensure that the sub-loan requestand the sub-project satisfy the criteria established under the proposedloans; a statement to this effect by the Sub-Unit will accompany each appli-cation. These arrangements are the same as for the previous industrialcredit projects.

Sub-Loan and Sub-Project Size LImitations

4.19 The maximum sub-project loan to be financed by the Bank must normallynot exceed $4 million equivalent, except for labor intensive projects; thiscompares with a limit of $3 million under the previous two industrial credits,and takes into account the equipment cost inflation in dollar terms. At thesame time, the total sub-project cost is raised to $15 million maximum (from$10 million). To assist joint-ventures between industries in the differentRepublics and autonomous Provinces in Yugoslavia, joint venture projects--involving transfer of know-how and capital--will be allowed a maximum sub-project cost of $20 million. These new limits consider the increasing sizeof Yugoslav industries, as well as the dollar equipment cost inflation, andalso takes into account that a minimum of 25% of the loan will be used forlabor-intensive industries, which are often small-sized. The higher sub-project total cost limits are strongly advocated by the Yugoslavs in orderthat Bank funds can be used, in part, for the modern industrial sector.

Free Limit and Aggregate Free Limit

4.20 In view of the bank's greater familiarity with, and greater pro-ficiencies in appraisal work, and taking into account the inflation in dollarterms of the cost of equipment and services, the free limit for individualsub-loans will be ra±sed from $1.0 million under the third and fourth indus-trial credit projects to $2.0 million in the fifth project. The aggregatefree limit will be 60% of the total loan amount allocated to each bank,identical to the limit set under the previous two industrial credits.

4.21 It is expected that this will result in the Bank reviewing in detailbetween 12 and 15 sub-projects, while it will check in a more cursory way afurther 25 to 30 sub-projects below the free limit.

- 26 -

Labor Intensive Sub-Projects

4.22 In line with the objectives to provide additional employment, 25%of the tota' loan ($27.5 million) can only be used for the financing ofprojects in labor-intensive industries where the cost per job will be lessthan $31,000, with an estimated average of $24,500 per job, as detailed inpara 4.09. This compares with an allocation of 20% ($20 million) to labor-intensive industries under the two previous industrial credits. There will beno limit on project size or sub-loan amount for labor-intensive industries.

Loan and Sub-Loan Terms

4.23 The proposed loan will be made on the Bank's normal terms and con-ditions as applicable to DFC loans, including the standard commitment charge,with repayment schedules reflecting the composite repayments of sub-loans.The repayment period of individual sub-loans will not exceed 15 years fromthe date of signing of the proposed loan. Grace period will be up to threeyears; to encourage blending of Bank funds with other foreign exchange re-sources, which are expected to be mainly medium-term credits, grace periodsof up to five years will be allowed when there is co-financing and the needfor such a longer grace period can be demonstrated.

4.24 The on-lending rate to be charged 'by the banks on IBRD funds willbe at least 11%, with the sub-borrowers assuming the foreign exchange risk.This rate will result in a positive interest rate for the ultimate borrowers,and will provide the banks an adequate spread. In addition, domestic resourceslent to social sector sub-projects receiving IBRD funds will carry an interestrate of at least 10%, unless these funds are especially earmarked allocations(see para 4.14).

Special Condition for IBT

4.25 In view of the recent poor performance of IBT, assurances will besought from IBT that remedial steps have been taken before the IBT part of theloan is declared effective. These steps, which have been communicated to IBT,consist of strengthening their staff, including training of new staff, achange in project approval procedures, and an increase in project supervision(para. 3.12). If, as anticipated, IBT will have taken steps to resolve thisproblem at the time of Board presentation, t'his special condition for IBT willbe waived.

Procurement