Embed Size (px)

Citation preview

Why India Now?

December 2016!

For Professional and Accredited Investors only not for redistribution!

Spike Hughes, Founder & CEO (T): +44 20 7399 6718 (M): +44 7920 888200 (E): [email protected] (W): www.cohesioninvestments.com

Why$India$Now?$One of the most exciting things in India’s recent history is the very positive and unprecedented steps that the Indian Prime Minister, Mr Modi, has just taken on demonetisation in India and the reissue of existing Rupee notes. We believe this is an absolute ‘game changer’ for the Indian economy. Historically, two of the key things that have held India back have been corruption and the cash-driven black economy. Mr Modi masterfully addressed both of these overnight in a way we cannot recall ever seeing from any world leader on this scale before. PM Modi announced in November that INR 500 and 1000 denomination notes will cease to be legal tender with immediate effect, barring a few emergency transactions. This measure is aimed at reducing the stock of black money. From an economic perspective, 86.4% of the notes in circulation (amounting to USD 220bn - as of March 2016) ceased to be legal tender. Demonetisation has led to disruption in the short-term in an economy where 80% of transactions were in cash. The most impacted sectors in the short-term are Autos, Cement, Consumer Discretionary, Real Estate, NBFCs and Banks. Whilst this might impact the short-term growth negatively, inflation is expected to come down and the fiscal situation should improve with better tax collections. The Reserve Bank of India (RBI) has forecast that the negative impact of demonetisation on the GDP will be -15bps for FY17 in its monetary policy, which is not a material impact and India’s GDP growth is still the highest amongst all the major emerging and developed economies of the world. However, looking forward, this huge event will potentially transform the Indian economy and enable it to grow to a much bigger size, similar to China. Imagine India's potential with a much cleaner economy. As expected, the FOMC raised the Fed funds rate by 25 bps and now sees three hikes in 2017 on account of a strengthening labour market and inflation gradually approaching the policy target. Since the beginning of November, the 10-year US treasury yields were up 60bps in anticipation of a Fed rate hike in December, which led to a strengthening in the Dollar Index by 3.3% and outflows from emerging markets. Even the Indian market saw FPI outflows in both equities (-US$2.6bn) and debt (-US$2.9bn) in the month of November. However, the Indian Rupee has been one of the best-performing currencies amongst all emerging market currencies as can be seen in the chart below and this again illustrates the financial health of India and the structural strength of the Rupee currency as the rest of this paper will demonstrate.

Source:(Bloomberg,(December(2016(

12(Month(Forward(Sensex(P/E( India’s(market(cap/GDP((%)(

Long0Term$Story$Remains$Intact(

A;rac<ve$Valua<ons(

16.46(

9(

13(

17(

21(

25(

DecP06

(

DecP07

(

DecP08

(

DecP09

(

DecP10

(

DecP11

(

DecP12

(

DecP13

(

DecP14

(

DecP15

(

DecP16

(

10(Year(Avg:(17.1x(

82$ 83$

103$

55$

95$88$

71$64$ 66$

81$70$ 71$

FY06(

FY07(

FY08(

FY09(

FY10(

FY11(

FY12(

FY13(

FY14(

FY15(

FY16(

FY17E(

Average of 78% for the

period

As we can see from the above figures following the recent correction in the market, the valuations are below the long-term average. Demonetisation is forecast to have an impact of 2% on FY17e and FY18e earnings. BSE Sensex is trading at 16.46x one-year forward earnings, at a discount to its long-term average of 17.1x. Sensex P/B is trading at 2.45x, close to its 10-year average of 2.7x. On FY18e earnings, Sensex is trading at 15.7x PE. The market cap-to-GDP ratio of 71% (FY17E GDP) is below the long-term average of 78%. If the global liquidity environment remains “risk on” then there won’t be much choice in emerging markets and India will be a standout beneficiary. Monsoon, rate cuts, economic acceleration mean that earnings could be positive. Considering this scenario, FIIs have already invested US$4.2bn in the first 11 months of CY16, compared to US$3.3bn in full CY15. From the below figure, we can see that earnings are expected to follow a much stronger trajectory for next few years vs. the last 8 years, leading to valuation strengthening.

81( 129( 181( 250( 266( 291( 278( 280( 216( 236( 272( 361( 446(540(

720( 833( 820( 834(1,024(

1,120( 1,181(1,337( 1,356(1,324$

1,379$

1,703$

FY93(

FY94(

FY95(

FY96(

FY97(

FY98(

FY99(

FY00(

FY01(

FY02(

FY03(

FY04(

FY05(

FY06(

FY07(

FY08(

FY09(

FY10(

FY11(

FY12(

FY13(

FY14(

FY15(

FY16(

FY17E(

FY18E(

FY93096:$$45%$CAGR$

FY96003:$$1%$CAGR$

FY03008:$$25%$CAGR$

FY08016:$$6%$CAGR$

FY930FY16:$13%$CAGR(

FY18:$!23%$CAGR!

Source:(MoUlal(Oswal(SecuriUes,(December(2016(

Source:(MoUlal(Oswal(SecuriUes,(December(2016(

Rural$Growth$Prospects$Remain$Strong$–$Good$Monsoons(

The monsoon has been good this year and we should see strong growth from rural India once the sales from Kharif crop start flowing back to the farmers. Also, the government has announced a double-digit rise in the minimum support price (MSP) for various crops last month after very little change in the past two years. This will benefit income within the farming industry and increase the rural consumption.

Interest$Rate$SoVening$Con<nues(

Since the beginning of November, the 10-year US treasury yields are up 60bps in anticipation of Fed Rate hike in December, while the Indian 10-year Gsec yields are down 40bps – the lowest in 6 years. So the cost of funding in India is constantly getting cheaper, whilst it is becoming more expensive globally. There is expectation of another 50-75bps fall in rates within the next year. This will help in the pickup of the private capex cycle in India, although levels will only rise following utilisation.

Fiscal$Deficit$in$Control(

With the rising tax collections of the government through GST and the demonetisation impact, the government should be able to control the fiscal deficit well in the longer term.

India$is$Very$A;rac<ve$vs.$Other$Countries(

Short term Factors Global India

Interest rates Look set to rise Falling

Growth Subdued Rising

Reform momentum Muted Improving

Corporate Prospects Weak Improving

Long term Factors Global India

Demographics Unfavourable Favourable

Debt Levels High Moderate

Growth Subdued Strong

Productivity Falling Rising

Indian$Rupee$is$a$Stable$Currency(

From India’s perspective, there was a time when the currency was very volatile (2010-2013), however, more recently, the Indian Rupee has been amongst the best performing EM currencies.

From both a medium-term and long-term perspective, India is in a rare sweet spot. In the history of the financial markets, there have been very few markets which have had these edges over the rest of the world.

Reasons for the above are: 1. Improvement in Current Accout Deficit (CAD): India’s CAD has come down from over 5% of GDP in

FY14 to 0.1% of GDP in Q1FY17.

Capital Account balance nearly doubled to US$90bn in FY15, which resulted in a Balance of Payment (BoP) surplus of US$61bn, as shown in the table. For FY16, the BoP was US$17.8bn.

Source:(Bloomberg,(December(2016(

Source:(Morgan(Stanley,(June(2016(

2. Owing to the sharp improvement in India's balance of payment situation, India's foreign exchange reserve increased by US$116bn from the lows in Sep 2013 to US$364bn in Nov 2016. In fact, this has been the largest percentage rise in FX reserves amongst most of the emerging markets.

3. Corporate earnings growth looks strong: Indian currency, historically, has been weak when corporate

earnings are weak. However, it has been stable and strong when corporate earnings are improving. For the reasons already outlined above, a corporate earnings pick up should drive the currency forward.

4. Inflation moderation resulting in rate cuts: After remaining in double digits for previous 4 years,

inflation in India has declined since Q4FY14 and is currently in the RBI comfort zone of 4-5%. This has resulted in easing of RBI policy rates by 175bps in the last 18 months. In an environment where globally rates are expected to rise, India is the only country where rates have fallen. Going by the interest rate parity theory, this provides more stability to the currency.

(

Foreign Reserve(

Nov 16 (US$Bn)( Sep 13 (US$Bn)( % Change(

China( 3051.6( 3644.0( -16%(

Brazil( 358.9( 376.0( -5%(

India( 363.9( 247.9( 47%(

Indonesia( 109.2( 89.4( 22%(

Russia( 385.3( 472.0( -18%(

Thailand( 171.9( 163.0( 5%(

Turkey( 99.6( 110.0( -9%(

Malaysia( 94.3( 132.0( -29%(

South Africa( 39.1( 41.5( -6%(

Source:(Bloomberg,(December(2016(

Source:(Morgan(Stanley,(October(2016(

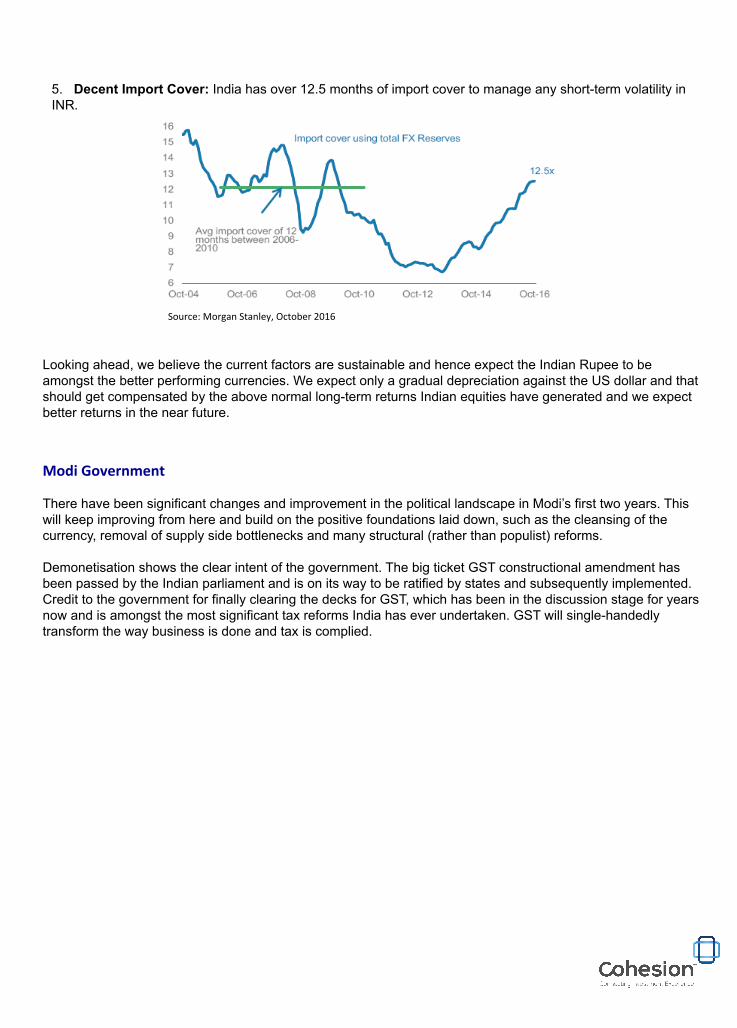

5. Decent Import Cover: India has over 12.5 months of import cover to manage any short-term volatility in INR.((

(

Source:(Morgan(Stanley,(October(2016(

Looking ahead, we believe the current factors are sustainable and hence expect the Indian Rupee to be amongst the better performing currencies. We expect only a gradual depreciation against the US dollar and that should get compensated by the above normal long-term returns Indian equities have generated and we expect better returns in the near future.

There have been significant changes and improvement in the political landscape in Modi’s first two years. This will keep improving from here and build on the positive foundations laid down, such as the cleansing of the currency, removal of supply side bottlenecks and many structural (rather than populist) reforms. Demonetisation shows the clear intent of the government. The big ticket GST constructional amendment has been passed by the Indian parliament and is on its way to be ratified by states and subsequently implemented. Credit to the government for finally clearing the decks for GST, which has been in the discussion stage for years now and is amongst the most significant tax reforms India has ever undertaken. GST will single-handedly transform the way business is done and tax is complied.

Modi$Government(

For$Professional$and$Accredited$Investors$only$and$should$not$be$relied$upon$by$retail$clients.$$!This!document!may!not!be!disseminated,!distributed!or!used!without!the!prior!wri5en!consent!of!Cohesion!Investments!Limited!and!Sapia!Partners!LLP!(the!“Companies”).!This!document!is!sourced!from!Reliance!Asset!Management!(Singapore)!Pte!Ltd!and!is!not!a!financial!promoHon!but!only!markeHng!material!for!educaHonal!and!informaHonal!purposes.!PotenHal!investors!should!refer!to!fund!documentaHon!before!considering!any!investment!and!read!the!relevant!risk!secHons!within!such!documentaHon.!The!informaHon!contained!in!this!document!is!based!on!material!that!Companies!believe!to!be!reliable.!AssumpHons,!esHmates!and!opinions!contained!in!this!document!consHtute!informaHon!we!received!from!reliable!sources!as!of!the!date!of!the!document!and!are!subject!to!change!without!noHce.!Neither!the!Companies!or!any!of!their!respecHve!officers,!directors,!employees,!agents,!controlling!persons!or!affiliates!makes!any!representaHon!or!warranty,!expressed!or!implied,!as!to!the!accuracy!or!completeness!of!the!informaHon!contained!in!this!document,!and!nothing!contained!herein!is,!or!shall!be!relied!upon!as,!a!promise!or!representaHon,!whether!as!to!past!or!future!facts!or!results.!!!Cohesion!Investments!Limited!is!an!Appointed!RepresentaHve!of!Sapia!Partners!LLP,!an!enHty!which!is!authorised!and!regulated!by!the!Financial!Conduct!Authority!(FCA).!