Embed Size (px)

Citation preview

Wealth and Investment Management

Volume 2

White Paper

Entrepreneurs IndexMapping business activity and wealth creation across the UK & Ireland

1

About BarclaysBarclays is a major global financial services provider engaged in personal banking, credit cards, corporate and investment banking, and wealth and investment management. With over 300 years of history and expertise in banking, Barclays moves, lends, invests and manages money for customers and clients worldwide.

As a leading global wealth and investment manager, Barclays provides international and private banking, wealth planning, trust and fiduciary services, investment management, brokerage services and research to private and intermediary clients across the world. Additionally our clients may benefit from access to the breadth of personal, corporate and investment banking expertise across Barclays, one of the largest financial services groups in the world.

For further information about Barclays, please visit our website barclays.com/wealth

Follow us on twitter.com/barclayswealth

ForewordSince the publication of the inaugural Barclays Entrepreneurs Index report we have been watching the indicators for business activity in the UK and Ireland with interest.

While it has undoubtedly continued to be a tumultuous time for enterprise, with a backdrop of uneven economic growth, on-going Eurozone troubles and fears of a triple-dip recession, it is encouraging to see that private and active companies in the UK and Ireland have shown not only remarkable resilience, but even growth in certain sectors. Through this Index, we aim to track the growth of enterprise and wealth creation, using a pioneering methodology to scrutinise the entrepreneurial landscape by exploring the levels of shareholder activity occurring across the UK and Ireland.

This second report from our Barclays Entrepreneurs Index series, produced in co-operation with Ledbury Research, reveals a rise in the profitability of these growing companies and the resurgence of traditional industries, such as manufacturing. We are hopeful that this uptick in entrepreneurial activity may signal an important turning point for the wider economy and business confidence in general.

We must also remember that behind these figures for entrepreneurial activity are the entrepreneurs themselves. Our past insights, and our focus on studying the personalities and behaviour traits of our clients – whether they have created their wealth through the sale of a business, inheritance or their investments – has enabled us to form an understanding of the “financial personalities” of the people building these businesses. As such, we know that the psychological make-up of a business owner plays a crucial role in their success. Even in a thriving economy, the tenacity to drive a fledgling operation from start up to success is no mean feat, but in a more uncertain climate, fostering a growing and profitable business is not for the faint-hearted. At Barclays, we are committed to understanding and helping with the challenges and opportunities faced by this generation of entrepreneurs, through all phases of the business cycle.

I hope you find the second Entrepreneurs Index report as interesting and insightful as we do.

Thomas L. Kalaris Chief Executive Barclays Wealth and Investment Management Executive Chairman of Barclays in the Americas

321 Source: Department for Business, Innovation & Skills

Our Expert PanelWe are extremely grateful for the time and help from the experts on our panel

Oli Barrett is a co-founder of Start-up Britain and has been described by Wired magazine as “the most connected man in Britain”. He brought Speednetworking to the UK and has fronted and co-organised six trade missions for 112 British Companies to San Francisco, helping them to pitch for funding and explore business opportunities.

Professor Jonathan Levie is Director of Knowledge Exchange at the Hunter Centre for Entrepreneurship at the University of Strathclyde. He co-directs the UK Research team of Global Entrepreneurship Monitor, a major international research project on entrepreneurial activity.

Karl von Bezing is a Senior Consultant in Banking & Wealth Management at Ernst & Young. He has worked extensively with private banks, asset managers, IFAs, family offices, UHNW clients and retail financial service providers on many projects across EMEA and Asia Pacific. Prior to joining Ernst & Young in 2011, he worked for Scorpio Partnership.

Richard Phelps is Managing Director, Corporate & Employer Solutions at Barclays. This business advises SMEs and entrepreneurs on risks relating to human capital, as well as delivering protection solutions.

Andrew Carter, Director of Policy & Research, Centre for Cities, has 15 years of experience working with business, community and public sector leaders to address issues including urban competitiveness, economic development and finance and inner city entrepreneurship. He has also worked for Rocket Science, an economic development consultancy, and for the London Development Agency.

Carl Pihl founded cloud-based ticketing platform TicketingHub in 2012 and has set up or co-founded a variety of start-ups including StudentBox and Drinkyz. He participated in the BBC show ‘The Last Millionaire’ and in 2006 created the Entrepreneurial Society at King’s College in London.

Imran Hakim, CEO at Hakim Group, is an optometrist by profession and secured investment on BBC2’s Dragons’ Den from entrepreneurs Peter Jones and Theo Paphitis for his innovative iTeddy product which now retails in more than 45 countries worldwide. He has since invested in early stage businesses across a variety of sectors. He is a director for entrepreneurship at the University of Manchester Innovation Centre and an ambassador for the UK India Business Council in the North West, where he is based.

Guy Rigby is a chartered accountant and leads the entrepreneurial services group at Smith & Williamson. He sold his own accountancy firm and has been a director and part-owner of a number of different ventures. He also wrote the book From Vision to Exit: The Entrepreneur’s Guide to Building and Selling A Business.

Phil Jones is a consultant and mentor to a number of creative, digital and sports agencies. Described as the “Godfather of Digital”, his specialities are connecting people, particularly in the creative, digital and sports industries and helping entrepreneurs grow their businesses.

Will Stirling is Editorial Director of the influential trade magazine The Manufacturer. He is an authority on matters relating to the UK manufacturing sector, including industry skills development and enterprise. He has also worked for Euromoney and IPC Media.

54

BackgroundMore than 40% of people in the UK with wealth of over £5m have derived it from the sale of a business1. This makes the wealth realised by entrepreneurs through the sale of all or part of their businesses one of the keys to the nation’s economic progress; success at this stage of the entrepreneurial cycle unlocks funds for future reinvestment and creates the potential to inject wealth into new ventures, thus helping to grow the future economy. It also provides inspiration for other people to found and invest in entrepreneurial ventures.

While there is established and well-respected data on the earlier stages of entrepreneurial activity, what has been missing to date is research tracking share transactions by successful entrepreneurs – individuals with stakes in privately owned, active and growing businesses – and how this is changing over time. It is this chapter of entrepreneurial activity in the UK and Republic of Ireland (ROI) that the Entrepreneurs Index focuses on.

This is the second report in an on-going series which uses an innovative methodology to analyse this stage of an entrepreneurial journey. The results of this analysis for H2 2012 are presented here, compared against those from H2 2011, with breakdowns by sector and across the UK and ROI followed by a detailed analysis region by region.

Our research findings are supported by commentary from experts in relevant fields of research, industry and trade bodies, as well as entrepreneurs themselves and those that work with them, to support and provide background to the data findings.

Executive Summary• A resurgence in the number of growing

companies with shares changing hands. 24,000 of these companies had shares changing hands in H2 2012, compared to 13,000 in H1 2012 and 21,000 in H2 2011.

• Substantial increase in financial health of growing companies with shares changing hands. There has been an increase in profitability in each wave of our research, from £1.3m in H2 2011, to £1.7m in H1 2012 to £2m in H2 2012.

• Green shoots of a recovery. Entrepreneurs are by nature optimists and risk takers and seek out opportunities to buy quality assets more cheaply ahead of an upturn. Therefore, entrepreneurial activity is increasingly being seen as a leading indicator of economic activity.

• Yorkshire, Wales and the North West see a marked revival in manufacturing. In the North West, the number of companies with shares changing hands in the industrial sector increased from 411 to 595 year on year (up 45%). In Yorkshire, this figure rose from 399 to 587 (up 47%) and in Wales 127 to 185 (up 46%).

• Signs of health in both the ‘old’ economies and ‘new’ economies. The industrial sector, 70% of which is made up of manufacturing companies, saw the largest number of companies with shares changing hands of any sector – up 30%. The technology sector saw a 40% increase in the number of companies with shares changing hands from 1,313 in H2 2011 to 1,838 in H2 2012. The finance sector also saw a marked increase, up by 58% from 1,165 to 1,838.

• London and the North West set the pace for others nationally. London has the highest increase in numbers of companies with shares changing hands at 36%; the North West saw an impressive rise of 23%. The number of companies with shares changing hands is highest in London (3,792), followed by the South East (3,510) and the Midlands (2,070).

• Many successful entrepreneurs stay involved after exiting. Insight from our expert panel reveals that successful entrepreneurs are making investments in up and coming entrepreneurs. They also take a more structured approach to mentoring them in order to give “something back and pass something on.”

• A significant increase in employment by these companies led by a rise in the entrepreneurial activity. These companies now employ some 4.5m people – providing around 14% of total employment in the UK and Ireland. This means that an additional half a million people are employed in growing businesses with shares changing hands than a year ago.

1 Ledbury Research, 2010.

Definitions of terms used in this report

• Growing companies with shares changing hands: private and active companies with growing revenues between £5m and £200m, which have had a complete or partial change in shareholding during a six month period.

• Entrepreneurial activity: change in the number of growing companies with shares changing hands (as above).

• Wealth creation: the wealth realised for individuals as a result of selling or transferring their shareholdings in these companies.

• Profitability: based on the latest available annual profit/loss before tax of growing companies with shares changing hands.

• Jobs per hundred people: number of people employed by these companies per 100 people in the region (looking at regional population figures).

• Knowledge sector: consists of a number of professional service sub-sectors with management consultancy representing the largest proportion (44%).

76

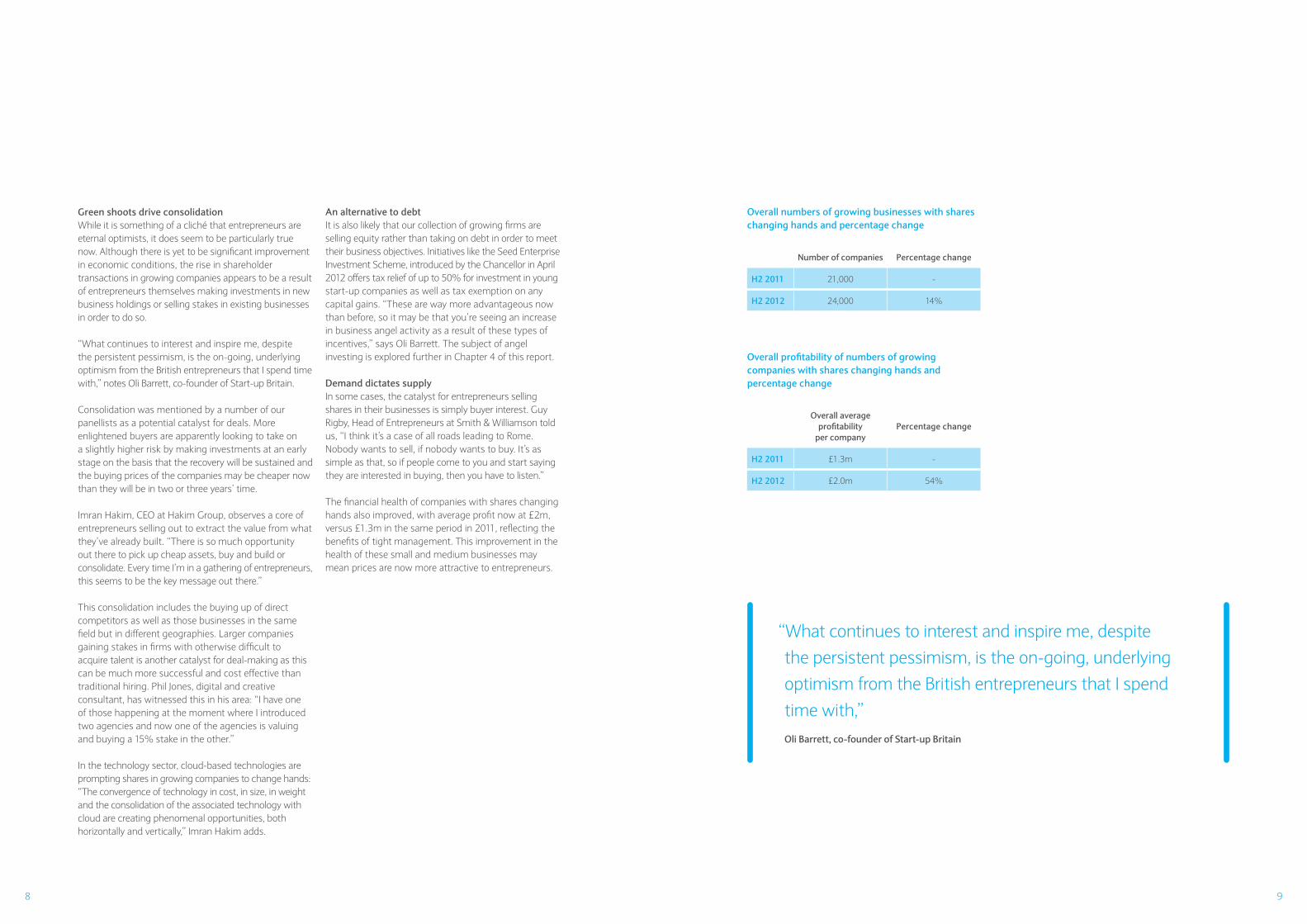

The number of growing companies with shares changing hands rose by 14% between H2 2011 and H2 2012. At the same time, the average profitability of these companies increased by 54%. This section explores the likely reasons for this resurgence, including the improving economic backdrop, key government initiatives and the financial health of companies.

Overall trends – positive news for the economy

A leading indicator24,000 growing companies had a change in shareholding in the second half of 2012, a 14% rise compared to the same period in 2011. This bounce back in the number of growing companies with shares changing hands is possibly an early sign of improvement in business and economic health. As in our previous report, these transactions were not “quick flips”. The average age of the businesses in which shares were changing hands was more than 20 years.

The findings, which focus on final stage entrepreneurial activity, are in line with those recently published by Global Entrepreneurship Monitor (GEM)2. GEM noted a potential “break out” in early-stage entrepreneurial activity which moved above its stable long-term rate of around 6% to 7.5% in 2011, jumping again in 2012 to 9%.

“You could almost argue that early stage entrepreneurial activity is a leading indicator of economic activity generally, so it seems to be at least trying to lead the economy out of recession, and along with that would go investment, certainly in growing businesses,” explains Jonathan Levie, Co-Director of GEM UK.

Chapter 1

2 An annual assessment of the entrepreneurial activity, aspirations and attitudes of individuals across a wide range of countries, conducted by a consortium of universities and academic institutions.

98

Green shoots drive consolidation While it is something of a cliché that entrepreneurs are eternal optimists, it does seem to be particularly true now. Although there is yet to be significant improvement in economic conditions, the rise in shareholder transactions in growing companies appears to be a result of entrepreneurs themselves making investments in new business holdings or selling stakes in existing businesses in order to do so.

“What continues to interest and inspire me, despite the persistent pessimism, is the on-going, underlying optimism from the British entrepreneurs that I spend time with,” notes Oli Barrett, co-founder of Start-up Britain.

Consolidation was mentioned by a number of our panellists as a potential catalyst for deals. More enlightened buyers are apparently looking to take on a slightly higher risk by making investments at an early stage on the basis that the recovery will be sustained and the buying prices of the companies may be cheaper now than they will be in two or three years’ time.

Imran Hakim, CEO at Hakim Group, observes a core of entrepreneurs selling out to extract the value from what they’ve already built. “There is so much opportunity out there to pick up cheap assets, buy and build or consolidate. Every time I’m in a gathering of entrepreneurs, this seems to be the key message out there.”

This consolidation includes the buying up of direct competitors as well as those businesses in the same field but in different geographies. Larger companies gaining stakes in firms with otherwise difficult to acquire talent is another catalyst for deal-making as this can be much more successful and cost effective than traditional hiring. Phil Jones, digital and creative consultant, has witnessed this in his area: “I have one of those happening at the moment where I introduced two agencies and now one of the agencies is valuing and buying a 15% stake in the other.”

In the technology sector, cloud-based technologies are prompting shares in growing companies to change hands: “The convergence of technology in cost, in size, in weight and the consolidation of the associated technology with cloud are creating phenomenal opportunities, both horizontally and vertically,” Imran Hakim adds.

An alternative to debt It is also likely that our collection of growing firms are selling equity rather than taking on debt in order to meet their business objectives. Initiatives like the Seed Enterprise Investment Scheme, introduced by the Chancellor in April 2012 offers tax relief of up to 50% for investment in young start-up companies as well as tax exemption on any capital gains. “These are way more advantageous now than before, so it may be that you’re seeing an increase in business angel activity as a result of these types of incentives,” says Oli Barrett. The subject of angel investing is explored further in Chapter 4 of this report.

Demand dictates supply In some cases, the catalyst for entrepreneurs selling shares in their businesses is simply buyer interest. Guy Rigby, Head of Entrepreneurs at Smith & Williamson told us, “I think it’s a case of all roads leading to Rome. Nobody wants to sell, if nobody wants to buy. It’s as simple as that, so if people come to you and start saying they are interested in buying, then you have to listen.”

The financial health of companies with shares changing hands also improved, with average profit now at £2m, versus £1.3m in the same period in 2011, reflecting the benefits of tight management. This improvement in the health of these small and medium businesses may mean prices are now more attractive to entrepreneurs.

Overall numbers of growing businesses with shares changing hands and percentage change

Number of companies Percentage change

H2 2011 21,000 -

H2 2012 24,000 14%

Overall profitability of numbers of growing companies with shares changing hands and percentage change

Overall average profitability

per companyPercentage change

H2 2011 £1.3m -

H2 2012 £2.0m 54%

“What continues to interest and inspire me, despite the persistent pessimism, is the on-going, underlying optimism from the British entrepreneurs that I spend time with,”Oli Barrett, co-founder of Start-up Britain

1110

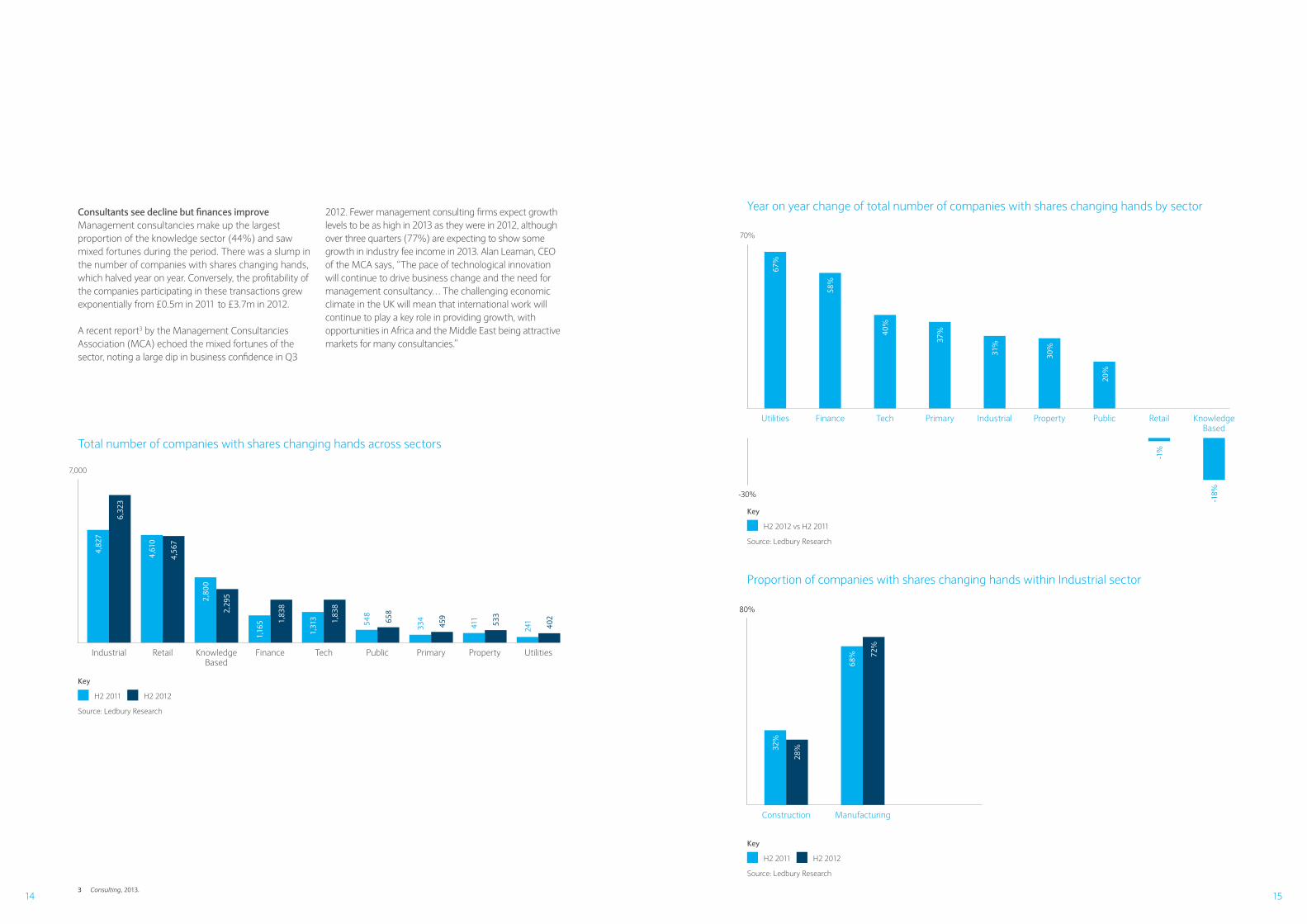

Among the nine sectors monitored in our index, the three with the largest numbers of companies with shares changing hands were again found in the industrial, retail and knowledge sectors. These sectors accounted for more than half of all entrepreneurial activity. The sectors of scale that saw the most notable increases in entrepreneurial activity were finance, technology and industrial. The knowledge sector, dominated by management consultancies, was the only sector which saw a fall in the number of companies with shares changing hands.

Growth in both the new economy and old economy

Chapter 2

1312

Infrastructure, skills acquisition and IP drive technology deals There was a significant rise in the number of growing technology companies with shares changing hands, up 40% compared to the same period a year ago.

A number of our panellists attributed this to a recent focus on online infrastructure opportunities which enable internet-based trading to take place. Successful start-ups in this area have the potential to be very attractive to larger players and rather than be afraid that technology giants are going to copy their ideas, entrepreneurs are advised to view any interest as a potential opportunity. “Big companies don’t want to copy ideas from start-ups. They much prefer to buy out a start-up once the project is developed, the concept is proven, the customer base is defined and the team is in place. It is less risky than starting with a concept,” observes Carl Pihl, founder of cloud-based ticketing platform TicketingHub.

Among technology companies, Carl Pihl also observes more of an emphasis on creating products instead of services, because they are harder to copy and enjoy more intellectual property protection. Taking a product to market can be an onerous process, and requires development, prototyping, manufacturing, storage and even European Union certification.

As the technology sector matures, lateral acquisitions are also key. Phil Jones has personal experience in developing lists of prospects in the digital and technology space for potential buyers. “There is definitely a lot of activity among the larger agencies and groups within this sector wanting to buy agencies with skills and clients that add value,” he explains.

One key change brought about by the recession and noted by a number of our panellists is the shift to internet-based buying and the reluctance of many big businesses with a vested interest in bricks and mortar to migrate to an online business model. “This opens up opportunities for those who don’t have that kind of residual resource base to move in and steal market share from them,” according to Jonathan Levie.

Government initiatives to support the sector are also playing their part. Tech City, an area in East London around Shoreditch’s Silicon Roundabout, was designated ‘a world-leading technology city to rival Silicon Valley’ in the US by the Government in 2010 and seen a five-fold increase in resident technology companies. Established technology firms like Google, Amazon and Facebook have invested in the long-term future of the area and work alongside smaller start-up firms.

“It may come in for criticism, but I know, first hand, that it has forged some very useful introductions and international connections between universities, investment groups, civil servants and entrepreneur groups that want to bring their companies or conferences to London, and that’s important,” explains Oli Barrett.

An industrial renaissance The industrial sector, which consists mainly of manufacturing companies, saw a 31% increase in the number of growing companies with shares changing hands.

Although this diverse sector is traditionally associated with the ‘old economy’ and heavy industry, advanced manufacturing is often extremely sophisticated, encompassing such areas as aerospace and life sciences. With manufacturing’s share of the overall economy having shrunk from 23% in 1980 to 10% in 2012, a number of Government initiatives to boost the sector are significant in explaining the increase in entrepreneurial activity found in this report.

Attention is currently focused on more technical and skilled areas of manufacturing where it is perceived that the UK has a potential competitive advantage. The ‘industrial strategy’ announced by Secretary of State for Business, Innovation and Skills, Vince Cable in September 2012 aims to identify sectors to boost with access to funding, better skills and Government contracts. The first of the Technology Strategy Board’s Catapult centres (opened October 2011) is also centred on high value manufacturing and involves a consortium of seven manufacturing technology centres across the UK.

For the manufacturing sector more generally, the Chancellor’s 2012 Autumn statement increased the annual investment allowance for plant and machinery tenfold from £25,000 to £250,000 for two years. Will Stirling, Editorial Director of The Manufacturer, explains that when investing in plant and equipment, tax relief is crucial right at the beginning of the investment cycle as opposed to lower corporation tax on profits. “If you buy new kit, your productivity is more efficient, so the higher capital allowance is a good step forward.”

Guy Rigby describes a “mini resurgence in manufacturing” particularly outside London which he attributes to the reduced differentials between manufacturing in the UK and abroad, helped by a weak pound, increased fuel costs and high Chinese wage inflation. “It is easier to manage logistics moving products from Leeds to London than it is from Shanghai to London.”

Jonathan Levie agrees that a desire for ‘Just In Time’ delivery may be boosting UK manufacturing. “People want very short supply times, and that’s difficult to do if your suppliers are in China. There’s also new technology which enables rapid manufacturing, and I think that’s helping to rebalance the profitability of manufacturing around the world, so it doesn’t surprise me that there are new style manufacturing businesses growing in the UK again.”

At the same time as wage inflation in the Far East is making manufacturing in the UK cheaper in relative terms, fast growing wealth in Asia is providing the UK automotive industry with a boost. Rolls Royce is experiencing a second record year, driven by growing demand from Asian clients who now account for 40% of its sales.

Perhaps more fundamentally, and identified by Richard Phelps, Managing Director, Corporate & Employer Solutions at Barclays, are innovation and technical design as enduring competencies of Britain. “We shouldn’t be surprised by the resurgence of the manufacturing sector. Since Stephenson’s Rocket, Britain has led the world in design and innovation. With a move to a new style of production our manufacturing sector is, once again, at the forefront.”

Finance sector consolidates, driven by regulation The finance sector saw a 58% increase in companies with shares changing hands compared to a year ago. This widespread consolidation could be attributed to the Retail Distribution Review (RDR), which came into force on 1 January 2013. It was widely anticipated that RDR would prompt a huge number of advisers to retire and sell their businesses or pool resources, and this seems to be borne out by the data. Finance was the only sector to have seen a rise in entrepreneurial activity in all regions – the only exception being the Republic of Ireland where the RDR does not apply.

Monitoring of merger and acquisition activity in the personal financial advice space by Ernst & Young certainly shows accelerating numbers of deals in this sub-sector in 2012. It attributes this increase primarily to the RDR and the perceived challenges of adjusting to the regulatory environment for smaller intermediaries coupled with the presence of a few large consolidators.

Angelina Kouznetsova, Senior Manager, European Financial Services at Ernst & Young, thinks that the current pace of consolidation is likely to be maintained in 2013. “Consolidation among industry players will continue to be the primary form of transaction activity, with a few main consolidators who have access to funding benefiting from advisers who no longer want to be a part of the industry and are looking to realise some value from their existing client relationships.”

Brian Spence, Founder of Harrison Spence Partnership, an independent consultancy in retail financial services that has advised on many sales and purchases of financial advice firms, provides insight into what the owners of these smaller intermediaries do after the sale: “Some of the shareholder changes in the finance sector will reflect owners selling up and leaving the industry. However, many continue to work under the umbrella of the larger firm to which they have sold their business, and they often have a stake in the larger entity.”

1514

Consultants see decline but finances improveManagement consultancies make up the largest proportion of the knowledge sector (44%) and saw mixed fortunes during the period. There was a slump in the number of companies with shares changing hands, which halved year on year. Conversely, the profitability of the companies participating in these transactions grew exponentially from £0.5m in 2011 to £3.7m in 2012.

A recent report3 by the Management Consultancies Association (MCA) echoed the mixed fortunes of the sector, noting a large dip in business confidence in Q3

2012. Fewer management consulting firms expect growth levels to be as high in 2013 as they were in 2012, although over three quarters (77%) are expecting to show some growth in industry fee income in 2013. Alan Leaman, CEO of the MCA says, “The pace of technological innovation will continue to drive business change and the need for management consultancy… The challenging economic climate in the UK will mean that international work will continue to play a key role in providing growth, with opportunities in Africa and the Middle East being attractive markets for many consultancies.”

3 Consulting, 2013.

Key

H2 2011 H2 2012

Source: Ledbury Research

80%

Construction

32%

28%

Manufacturing

68% 72

%

Year on year change of total number of companies with shares changing hands by sector

Total number of companies with shares changing hands across sectors

Proportion of companies with shares changing hands within Industrial sector

Industrial Retail Knowledge Based

Finance Property UtilitiesPrimaryPublicTech

7,000

Key

H2 2011 H2 2012

Source: Ledbury Research

4,82

7

6,32

3

4,61

0

4,56

7

2,80

0

2,29

5

1,16

5 1,83

8

1,31

3 1,83

8

658

334

459

411

533

241 40

2

548

70%

-30%

Utilities TechFinance IndustrialPrimary Property Public Retail Knowledge Based

67%

58%

40%

37%

31%

20%

-1%

-18%

30%

Key

H2 2012 vs H2 2011

Source: Ledbury Research

1716

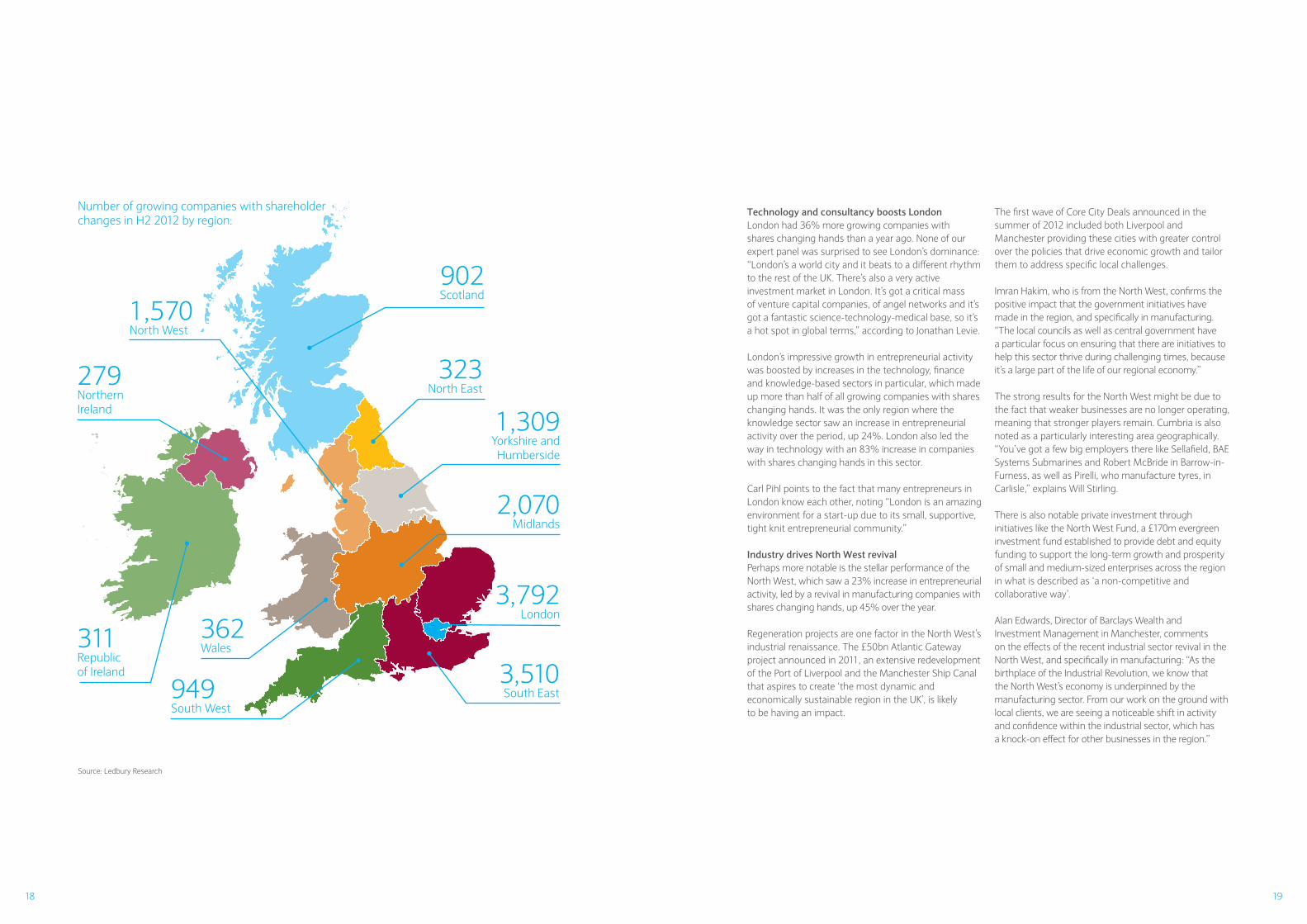

London, the South East and the Midlands remain the regions with the largest number of companies with shares changing hands year on year. Comparing wealth creation nationally, nearly all regions saw an increase in the number of companies with shares changing hands. London saw 36% more growing companies with shares changing hands, particularly impressive off such a high base. London and the North West saw the most pronounced overall growth across all sectors, with the growth in technology companies most striking in London and companies in the industrial sector most noteworthy in the North West. Scotland, the Republic of Ireland and Northern Ireland registered falls in companies with shares changing hands.

Putting entrepreneurial activity on the map – the North West and London set the pace for regions nationally

Chapter 3

1918

Number of growing companies with shareholder changes in H2 2012 by region:

Technology and consultancy boosts London London had 36% more growing companies with shares changing hands than a year ago. None of our expert panel was surprised to see London’s dominance: “London’s a world city and it beats to a different rhythm to the rest of the UK. There’s also a very active investment market in London. It’s got a critical mass of venture capital companies, of angel networks and it’s got a fantastic science-technology-medical base, so it’s a hot spot in global terms,” according to Jonathan Levie.

London’s impressive growth in entrepreneurial activity was boosted by increases in the technology, finance and knowledge-based sectors in particular, which made up more than half of all growing companies with shares changing hands. It was the only region where the knowledge sector saw an increase in entrepreneurial activity over the period, up 24%. London also led the way in technology with an 83% increase in companies with shares changing hands in this sector.

Carl Pihl points to the fact that many entrepreneurs in London know each other, noting “London is an amazing environment for a start-up due to its small, supportive, tight knit entrepreneurial community.”

Industry drives North West revival Perhaps more notable is the stellar performance of the North West, which saw a 23% increase in entrepreneurial activity, led by a revival in manufacturing companies with shares changing hands, up 45% over the year.

Regeneration projects are one factor in the North West’s industrial renaissance. The £50bn Atlantic Gateway project announced in 2011, an extensive redevelopment of the Port of Liverpool and the Manchester Ship Canal that aspires to create ‘the most dynamic and economically sustainable region in the UK’, is likely to be having an impact.

The first wave of Core City Deals announced in the summer of 2012 included both Liverpool and Manchester providing these cities with greater control over the policies that drive economic growth and tailor them to address specific local challenges.

Imran Hakim, who is from the North West, confirms the positive impact that the government initiatives have made in the region, and specifically in manufacturing. “The local councils as well as central government have a particular focus on ensuring that there are initiatives to help this sector thrive during challenging times, because it’s a large part of the life of our regional economy.”

The strong results for the North West might be due to the fact that weaker businesses are no longer operating, meaning that stronger players remain. Cumbria is also noted as a particularly interesting area geographically. “You’ve got a few big employers there like Sellafield, BAE Systems Submarines and Robert McBride in Barrow-in-Furness, as well as Pirelli, who manufacture tyres, in Carlisle,” explains Will Stirling.

There is also notable private investment through initiatives like the North West Fund, a £170m evergreen investment fund established to provide debt and equity funding to support the long-term growth and prosperity of small and medium-sized enterprises across the region in what is described as ‘a non-competitive and collaborative way’.

Alan Edwards, Director of Barclays Wealth and Investment Management in Manchester, comments on the effects of the recent industrial sector revival in the North West, and specifically in manufacturing: “As the birthplace of the Industrial Revolution, we know that the North West’s economy is underpinned by the manufacturing sector. From our work on the ground with local clients, we are seeing a noticeable shift in activity and confidence within the industrial sector, which has a knock-on effect for other businesses in the region.”

323 North East

1,309 Yorkshire and Humberside

2,070 Midlands

3,792 London

1,570 North West

902 Scotland

311 Republic of Ireland

279 Northern Ireland

3,510 South East949

South West

362 Wales

Source: Ledbury Research

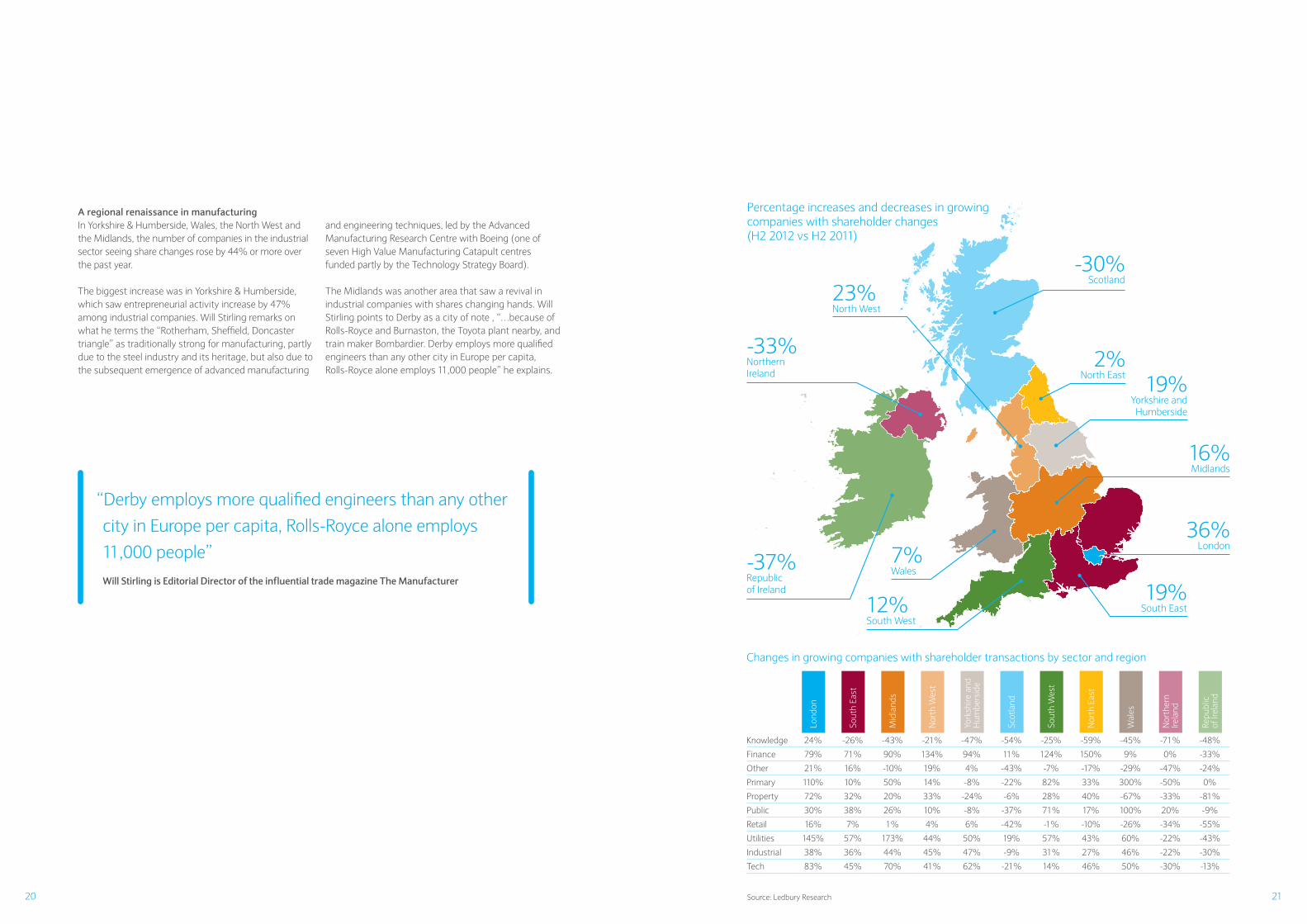

2120

2% North East

19% Yorkshire and Humberside

16% Midlands

36% London

23% North West

-30% Scotland

-37% Republic of Ireland

-33% Northern Ireland

19% South East12%

South West

7% Wales

A regional renaissance in manufacturingIn Yorkshire & Humberside, Wales, the North West and the Midlands, the number of companies in the industrial sector seeing share changes rose by 44% or more over the past year.

The biggest increase was in Yorkshire & Humberside, which saw entrepreneurial activity increase by 47% among industrial companies. Will Stirling remarks on what he terms the “Rotherham, Sheffield, Doncaster triangle” as traditionally strong for manufacturing, partly due to the steel industry and its heritage, but also due to the subsequent emergence of advanced manufacturing

and engineering techniques, led by the Advanced Manufacturing Research Centre with Boeing (one of seven High Value Manufacturing Catapult centres funded partly by the Technology Strategy Board).

The Midlands was another area that saw a revival in industrial companies with shares changing hands. Will Stirling points to Derby as a city of note , “…because of Rolls-Royce and Burnaston, the Toyota plant nearby, and train maker Bombardier. Derby employs more qualified engineers than any other city in Europe per capita, Rolls-Royce alone employs 11,000 people” he explains.

Percentage increases and decreases in growing companies with shareholder changes (H2 2012 vs H2 2011)

Lond

on

Sout

h Ea

st

Mid

land

s

Nor

th W

est

York

shire

and

H

umbe

rsid

e

Scot

land

Sout

h W

est

Nor

th E

ast

Wal

es

Nor

ther

n Ire

land

Repu

blic

of

Irel

and

Knowledge 24% -26% -43% -21% -47% -54% -25% -59% -45% -71% -48%

Finance 79% 71% 90% 134% 94% 11% 124% 150% 9% 0% -33%

Other 21% 16% -10% 19% 4% -43% -7% -17% -29% -47% -24%

Primary 110% 10% 50% 14% -8% -22% 82% 33% 300% -50% 0%

Property 72% 32% 20% 33% -24% -6% 28% 40% -67% -33% -81%

Public 30% 38% 26% 10% -8% -37% 71% 17% 100% 20% -9%

Retail 16% 7% 1% 4% 6% -42% -1% -10% -26% -34% -55%

Utilities 145% 57% 173% 44% 50% 19% 57% 43% 60% -22% -43%

Industrial 38% 36% 44% 45% 47% -9% 31% 27% 46% -22% -30%

Tech 83% 45% 70% 41% 62% -21% 14% 46% 50% -30% -13%

Changes in growing companies with shareholder transactions by sector and region

“Derby employs more qualified engineers than any other city in Europe per capita, Rolls-Royce alone employs 11,000 people”Will Stirling is Editorial Director of the influential trade magazine The Manufacturer

Source: Ledbury Research

2322

Looking to the future

Chapter 4

There will always be sharply different responses to the ‘what next?’ question that entrepreneurs who have successfully exited their businesses face. There will be those who happily retire to the proverbial desert island - never to be seen again in the business world. Many others will look to return to the entrepreneurial space sooner or later. The earlier they are in their wealth journey the more likely they may want to return but that isn’t a hard and fast rule. Greater levels of optimism and an inherent love of business also serve to entice individuals back.

This report has identified the fact that many successful entrepreneurs are currently staying involved after exiting,

believing that it is an ideal time in which to pick up cheap assets, buy and build or consolidate. Richard Phelps confirms that returning entrepreneurs are taking stakes of various sizes in ventures, seeing the upside from today’s valuations and an expectation of further growth.

For these successful entrepreneurs who wish to return to the entrepreneurial space, there are three key routes, which place different demands on their time and money. These routes cater for most individuals, from those who want the full start-up experience to those who just want to pass on some of the wisdom gleaned from their entrepreneurial experience.

These three routes are:

Routes for getting involved post-exit

1. Complete ownership and control

2. Active holding and influence

3. Passive investment

Tim

e, m

oney

and

risk

app

etite

2524

1. Complete ownership and control A successful entrepreneur who takes a complete or controlling stake in a new business venture, and also assumes executive charge of the company.

This is the classic build-it-again-from-scratch option and is probably the most demanding in terms of time, money and risk. Although having a successful track-record allows these entrepreneurs to access other forms of funding and manage risk to some degree, “typically, those entrepreneurs who have exited successfully are the ones who are most able to find the backing of others. They are generally not doing it with all their own money,” observes Guy Rigby.

Individuals choosing this option tend to have a greater tendency to go back into the same or a similar industry where they can apply their existing skill-sets, or something one or two steps removed in the value chain: “If they successfully launched a start-up, they are more willing to do so again or invest in operating companies where they are able to turn around and sell on the business,” explains Karl von Bezing, Senior Consultant in Banking & Wealth Management at Ernst & Young.

2. Active holding and influence A successful entrepreneur who takes a significant, but not controlling stake in one or more start-ups, and has some level of influence.

In this instance, returning entrepreneurs will take meaningful, albeit minority, stakes in a variety of start-ups and early stage businesses, possibly where they have existing relationships. If they find something they are passionate about, they may become engaged in a management role, but they will certainly have an influence in the business. Individuals pursuing this route may also act as mentors to the management, sharing their knowledge, skills and perspectives with them (see accompanying box out).

Richard Phelps comments; “The key thing for individuals wanting to pursue this route is connecting with new opportunities – to meet the next generation with exciting ideas. There are many ways of achieving this: through regional or industry networks, local Chambers of Commerce or wealth managers who increasingly see their role as creating a market place for those with funds and experience to meet those with ideas.”

3. Passive investment (angel investor) A successful entrepreneur who provides capital to start-ups but has fairly limited influence over these businesses.

Where enough money has been made and there is on-going interest, entrepreneurs often come back into the market as angel investors, making a number of smaller speculative investments, in the hope that some of them will pay off handsomely. They will have fairly limited influence over the business, but may provide advice or act as mentors for the management.

Carl Pihl’s experience is that entrepreneurs in the technology space will often support and finance smaller companies: “A lot of successful entrepreneurs go back into the start-up ecosystem as investors, venture capitalists, angels, or through other means of participation. They may start their own venture capital firm with some friends,” he observes. Phil Jones confirms that a variety of people who sold businesses in the digital sector are now taking stakes in a range of companies they believe have growth potential.

Mentoring in the Technology Sector Mentoring of up-and-coming talent is common among successful entrepreneurs who make either active investments (route 2) or passive investments (route 3) in businesses (see accompanying chapter). But successful entrepreneurs don’t have to be investors in order to be mentors. A couple of our panellists identify a recent move among successful entrepreneurs within the technology sector to mentor individuals without there being a direct financial incentive. Their motivation is to give something back or pass something on.

One panellist observes that individuals in the UK are emulating their US counterparts when it comes to mentoring. Oli Barrett first went to Silicon Valley in San Francisco in 2008 and has since been back six times. He describes being struck by the level of mixing between people who had exited and the next generation of entrepreneurs, leading to informal and formal mentoring and relatively small scale investment. Whereas in the past, relationships between UK entrepreneurs and investors tended to be transactional, British entrepreneurs are being inspired by their counterparts in San Francisco to attend networking events and mixers and investing in their peers on a small scale. Oli attributes this to the relatively young age at which entrepreneurs are selling out and the fact they are often investing in friends of friends.

A new Barclays-sponsored partnership with a company called ‘Central Working’ in the heart of Tech City specifically seeks to foster this collaboration and peer development among digital businesses through ‘clubs’ which are springing up across London. ”The sharing of experience and passing-on of advice between new start-ups and post-exit individuals that we see at Central Working is inspirational, and something that every industry would benefit from,” says Richard Phelps.

2726

One Entrepreneur’s Attitude To Selling A BusinessCarl Pihl, founder of cloud-based ticketing platform, TicketingHub, is a serial entrepreneur who, at the age of 29, has a rich history of founding and selling various start-ups. Carl’s

previous ventures include StudentBox and Drinkyz, both of which he co-founded, as well as custom-made luxury belt company, Monte Napoleone.

Here, he provides his insights into successfully selling your business:

Timing is critical When selling your company, one day more or one day less can make or break things and the bubble can burst as the market changes.

… but it has to be right for you Your decision to exit will depend on a combination of personal, business and external market factors.

As an entrepreneur, you just build your company and when you have an offer you decide whether that’s enough or not. Factors such as hitting another plateau where you start to compete with other, bigger firms, might be the catalyst.

It could be that it’s what you wrote in your business plan, that you have investors looking for an exit, whether you think that you can still grow within the market you’re in and if you can actually sell that potential growth to your investor, or not.

Ensure you value your company using the right measures A foothold in a new market can increase the value of your business exponentially as valuing a company is all about potential. If someone approaches you as an event promoter and you have a big database, you don’t value it by ten years revenue, but rather by your database of contacts, which is likely to be much more valuable.

…but don’t be too greedy I think one of the biggest errors from people is expecting too much. You just have to be reasonable, particularly if you have a good offer and you don’t see potential growth. A lot of people hold on, hold on, hold on, and then it’s too late and they go bust, although occasionally they hold on and are very successful.

Always have one eye on the next opportunity I don’t like management. I just love creating. What I do in most of my companies is create a cashless situation, and from the moment I have cash flow I try to create other products or other avenues to develop. You just put a budget to that and try to see if it works or it doesn’t.

Don’t be afraid to pivot … The whole idea of a start-up is you come up with an idea, work a direction, and then you can always pivot your business. By pivoting I mean understanding that there’s a bigger opportunity by going left than going right. It doesn’t mean changing your business model, it could mean just concentrating on a more narrow market or it could be just changing the way you pitch to someone.

Always have one eye on the next opportunity … I love the whole idea of serial entrepreneurs. I haven’t done an exit as beautiful as some other people, but I’ve done some and, for me, it is always a question of exiting because I have another opportunity or because I’ve found something else and I want to develop that.

It’s all about life stage My ambition is to become an angel investor at some point because I want to have the time in the future to be with my family. When I have children I want to be able to be present for them and not living the life that I live now.

Think laterally … I have worked in lots of different sectors. I think it’s good to specialise, but I specialise in branding … I create a brand and create a story around that brand.

Always keep a small share in the business initially. It’s good to have a small stake in its future success. And the investors might want to buy you out at a premium in the future!

2928

This section looks at the growing companies that have changed hands across the major regions in the UK and in Ireland in the second half of 2012 compared to the second half of 2011.

Spotlight on regions

Chapter 5

• London

• South East

• Midlands

• North West

• Yorkshire & Humberside

• Scotland

• South West

• North East

• Wales

• Northern Ireland

• Republic of Ireland

3130

Chapter 5

Industrial

15% 14%

Retail

25%

21%

Tech

8%10%

Knowledge Based

26%

17%

23%21%

Utilities

1% 2%

Property

4% 5%

Primary

2%1%

Public

3%3%

Finance

60%

0%

Companies with shares changing hands

2,790 3,7922011 2012

Average profit

£2.5m £3.2m2011 2012

Average age of company

17 192011 2012

Jobs per hundred people in region

7.1 8.72011 2012

% increase from H2 2011

36%2012

Of all the regions across the UK and ROI, London was the region with both the highest number of companies changing hands and the highest year on year increase in entrepreneurial activity, up 36%. This was particularly impressive off such a high base.

“On all the business indicators London continues to do well. It’s got the highest rate of start-ups, it’s got the biggest overall stock, its levels of businesses per 10,000 population are high,” Andrew Carter, Director of Policy & Research, Centre for Cities, explains. He adds that the more recent expansion has been fuelled by technology and media sectors more than by classic finance sectors in which employment has remained pretty static.

Colin Stanbridge, Chief Executive at the London Chamber of Commerce, is also unsurprised to see entrepreneurial activity so high in London: “Seeing such high levels of entrepreneurial activity chimes with the fact that we saw business confidence increase by 10 points in the fourth

quarter of 2012 – approaching pre-recession levels. Anecdotally, we also typically see people turn to entrepreneurial endeavours in tough times for business – so it may be that recent harsh economic conditions have actually helped boost entrepreneurial activity.”

The average profit of companies with shares changing hands in London was £3.2m, up on the previous year, and well ahead of the national average of £2m. Colin Stanbridge says that this is always likely to be the case, pointing out that productivity has always been higher in the capital.

While the knowledge sector, 44% of which are management consultancies, had the highest proportion of entrepreneurial activity, closely followed by finance and retail, it was the technology sector that saw the most notable increase in entrepreneurial activity compared to other regions. The 83% increase was the highest across the UK and ROI and might explain why the average age

of companies with shares changing hands was amongst the youngest across the UK and ROI, at 19 years.

Colin Stanbridge makes the point that high levels of activity in both knowledge-based and technology sectors may not be unrelated: “Growth in entrepreneurial activity in the technology sector can boost business in the knowledge sector, because consultancy-based work such as marketing and management consultancy lends itself well to supporting start-ups in the technology sector.”

The number of people employed by those companies that had share changes in London was much higher than in any other region, at nearly 9 people for every 100 in the nation’s capital.

London

“On all the business indicators London continues to do well. It’s got the highest rate of start-ups, it’s got the biggest overall stock, its levels of businesses per 10,000 population are high...” Andrew Carter, Director of Policy & Research, Centre for Cities

Key

H2 2011 H2 2012

Source: Ledbury Research

3332

MidlandsSouth East

The number of companies with shares changing hands in the South East remained second highest after London at 3,510, up 19% year on year. The profitability of these companies also rose by an impressive 50% year on year to £1.8m, just under the national average.

Those growing companies that had share changes in the South East employed almost 5 people out of every 100 in the region, above the national average.

The largest number of companies with shares that changed hands in the South East was in the industrial sector, up 36% to 977. However, finance companies saw the largest increase in share transactions, up 71% to 186. Whilst technology transactions also increased from 269 to 391, a rise of 45%, this was below the national average for the sector.

The 2012 Centre for Cities Outlook 2013, which ranks the performance of 64 UK cities and towns across a range of economic indicators including claimant counts, wages, size of the business base and house prices notes that cites in the traditionally prosperous South East, along with London, tend to be strongest on a number of measures. The study also found that the best recovering areas are those with strong private sectors, such as Brighton and Cambridge.

Companies with shares changing hands

2,943 3,5102011 2012

Average profit

£1.2m £1.8m2011 2012

Average age of company

21 232011 2012

Jobs per hundred people in region

3.8 4.62011 2012

% increase from H2 2011

19%2012

Companies with shares changing hands

1,790 2,0702011 2012

Average profit

£1.0m £1.7m2011 2012

Average age of company

23 252011 2012

Jobs per hundred people in region

3.4 4.22011 2012

% increase from H2 2011

16%2012

The Midlands saw the third-highest activity in companies with shares changing hands at 2,070. This 16% year on year rise ranked the region fifth in terms of increase in entrepreneurial activity.

The average profit of companies with shares changing hands in the period was £1.7m, up by an impressive 70% year on year from £1m. These companies employed around 4 people for every 100 in the Midlands.

Growth in deals in the technology sector rose by 70%, second only to London. However, this represented just 6% of all companies with shares changing hands. Best known for its focus on aerospace and automotive industries, growth in share transactions in the industrial sector were far greater, affecting 875 companies, an increase of 44% compared to the previous year.

Derby is home to Rolls Royce, the biggest private sector employer in the city which, despite tough economic conditions, had its best year in 2012 since being founded 100 years ago. Train manufacturer Bombardier also announced it would remain in the city.

According to Centre for Cities’ Cities Outlook 2013, Milton Keynes and Northampton are noted as cities that have recovered well from the recession due to their strong private sectors. The Midlands’ cities of Birmingham and Nottingham are amongst the first wave of Core City Deals, which provide cities with greater control over the policies that drive economic growth and tailor them to address specific local challenges. In Birmingham, this includes the creation of a £1.5bn investment fund and in Nottingham providing support to enterprise through access to finance schemes.

IndustrialIndustrial

41%

31%

48%

35%

RetailRetail

30%28%

25%25%

TechTech

11%14%

7%

14%

Knowledge Based

Knowledge Based

16%

5%6%

10%7%

UtilitiesUtilities

1%1% 2%2%

PropertyProperty

2%1% 2%2%

PrimaryPrimary

2%2% 2%3%

PublicPublic

3%4%4% 3%3%3%5%

FinanceFinance

60%60%

0%0%

Key

H2 2011 H2 2012

Source: Ledbury Research

3534

12%

Yorkshire & HumbersideNorth West

The North West was second place only to London in terms of the year on year increase in companies with shares changing hands, which stood at 23%. However, the average profit of these companies had fallen marginally to £1.2m. They employed just over 4 people out of every 100 in the North West.

As the birthplace of the Industrial Revolution, perhaps unsurprisingly, this stellar performance was led by the region’s industrial sector. 595 growing industrial companies in the region had shares changing hands, a rise of 45%, the third highest increase nationally.

Initiatives such as the Atlantic Gateway redevelopment project focused on the corridor between Greater Manchester and Merseyside and the BBC’s move to Media City are notable.

The creation of a £75m mayoral investment fund to support economic development in Liverpool and a £1.2bn revolving infrastructure fund in Manchester as key elements of their Core City Deals, combined with private investment by initiatives such as the £155m North West Fund, appear to have boosted entrepreneurial activity in the region.

Clive Memmot, Chief Executive of the Greater Manchester Chamber of Commerce, agrees that these schemes are invaluable for the development of the region. “Investment in urban areas is crucial, which is why we are really pleased to see centralised initiatives such as City Deals. The region has a strong culture of co-operation between the private and public sectors. This unity helps to ensure that business is still being done even in typically more austere times.”

Companies with shares changing hands

1,281 1,5702011 2012

Average profit

£1.3m £1.2m2011 2012

Average age of company

23 242011 2012

Jobs per hundred people in region

3.4 4.32011 2012

% increase from H2 2011

23%2012

Companies with shares changing hands

1,098 1,3092011 2012

Average profit

£0.8m £0.7m2011 2012

Average age of company

25 262011 2012

Jobs per hundred people in region

4.0 5.12011 2012

% increase from H2 2011

19%2012

Yorkshire & Humberside saw a 19% increase in companies with shares changing hands over the period, to 1,309, the fourth largest increase nationally and the fifth highest number in total. These companies employed 5 people out of every 100 in the Yorkshire & Humberside region, above the average for the UK and ROI. The average profit of these companies was the lowest nationally at £0.7m, down from £0.8m in the previous year.

The sector with the largest number of companies with shares changing hands in the region was the industrial sector (587).

Sheffield’s steel industry heritage and a focus on advanced manufacturing research have stood the region in good stead. “There are lots of things going on in the Sheffield City Region. The common denominator is materials and metals, and aerospace engineering, nuclear and oil & gas engineering,” according to Will Stirling. Sheffield is also one of the cities that hosts one of the Technology Strategy Board’s principle Catapult centres focused on High Value Manufacturing, the AMRC with Boeing.

IndustrialIndustrial

43%

39%

52%

45%

RetailRetail

28%31%

25%26%

TechTech

6%6% 6%

Knowledge Based

Knowledge Based

14%

9%

UtilitiesUtilities

1%2% 1%2%

PropertyProperty

3%2% 2%2%

PrimaryPrimary

2%1%3%

1%

PublicPublic

2%5% 5%

3% 3%4%4%3%3%5%

FinanceFinance

60%60%

0%0%

Key

H2 2011 H2 2012

Source: Ledbury Research

3736

South WestScotland

Scotland had the seventh highest number of companies with shares changing hands across the UK and ROI, although the number had fallen 30% compared to 2011. The average age of these companies was 25 years, up from 21 a year ago and they employed almost 4 people for every 100 in Scotland, decrease in line with the number of companies changing hands.

It was one of only three regions to see a fall in entrepreneurial activity, but the financial health of those companies with shares changing hands was the highest across the UK and ROI, at £5.9m – almost three times the national average and a huge increase from £1.8m a year ago, up more than 200%.

Almost all sectors in Scotland saw a fall in the number of companies with shares changing hands. However, the largest proportion of companies changing hands were in the industrial sector (44%) and retail (21%). The only sectors seeing increases were utilities and finance companies, but these represented only 4% and 5% of all companies in Scotland.

Companies with shares changing hands

1,288 9022011 2012

Average profit

£1.8m £5.9m2011 2012

Average age of company

21 252011 2012

Jobs per hundred people in region

5.0 3.82011 2012

% increase from H2 2011

-30%2012

Companies with shares changing hands

850 9492011 2012

Average profit

£1.5m £1.7m2011 2012

Average age of company

23 232011 2012

Jobs per hundred people in region

2.9 3.92011 2012

% increase from H2 2011

12%2012

The South West had a 12% rise in companies with shares changing hands, ranked midway among other regions nationally. The average profit made by these companies was £1.7m, up from a year ago, but just under the average for the UK and ROI. These companies also employed slightly fewer than 4 people in every 100 in the region.

The largest number of companies with shares changing hands in the South West was in the industrial sector, with a rise of 31% compared to the previous year.

Will Stirling believes that entrepreneurial activity in the region will have been driven partly by the strength of the South West’s aerospace industry which dates back to WWII when many of the factories that made aircraft and parts in London were established beyond the range of the Luftwaffe: “The South West is very strong for aerospace, because you’ve got Airbus down in Filton, GKN have a couple of plants there and Messier-Bugatti-Dowty make landing gear near Gloucester. GE Aviation also in south east Wales. If you looked at the numbers, there are probably more qualified engineering and science-based employees based in the Bristol region in that sector than elsewhere in the UK.”

Bristol has also recently been awarded a £1bn economic development fund as part of the first wave of Core City Deals, which is likely to have supported entrepreneurial activity in the region.

North & North East Somerset & Gloucestershire’s strength in aerospace is pinpointed by the Department for Business Innovation and Skills Industrial strategy: UK Sector Analysis report.

IndustrialIndustrial

34%36%

39%

44%

RetailRetail

31%28%

26%

21%

TechTech

8%

15%

8%

Knowledge Based

Knowledge Based

14%

10%

6%9%

UtilitiesUtilities

2%2% 3%4%

PropertyProperty

2% 2%

PrimaryPrimary

6%6%

PublicPublic

4%2% 2%3%3%

5% 4%5% 5%

FinanceFinance

60%60%

0%0%

3%3%2% 2%

Key

H2 2011 H2 2012

Source: Ledbury Research

3938

WalesNorth East

The North East was the region with the lowest rise in entrepreneurial activity at 2% (although three other regions saw a fall). 323 companies had shares that changed hands, marginally up from 318 a year earlier. The average financial health of these companies was £1.4m, below the national average and down on a year ago. These companies also employed 2.4 people out of every 100 in the region, which was among the lowest across the UK and ROI.

Ross Smith, Director of Policy at the North East Chamber of Commerce attributes this low-level activity to the shape of the business economy in the region. “Historically, the North East has been home to a lower number of local businesses than other UK regions, as our private sector is smaller than perhaps it should be for a region this size.” He is, however, beginning to see growth in new ventures and employment.

The industrial sector led the way with more than half of all entrepreneurial activity taking place in this sector. 141 companies had shares changing hands in this sector, up 27% compared to a year ago. The greatest rise in companies with shares changing hands was in the finance and technology sectors, but these were only a small proportion of overall activity (2% and 7% respectively).

“We are currently seeing a very successful programme of start-up activity in the technology sector,” Ross Smith remarks, with a recent business exit resulting in “Teesside’s first technology multi-millionaire” being created.

Cities Outlook 2013 found that those areas more dominated by the public sector or displaying a heavier dependence on manufacturing have shown weaker recoveries noting Middlesbrough in particular. Middlesbrough’s Corus steel plant closed in 2010, negatively affecting all businesses in the area as it spent approximately £58m per annum with other businesses in the North East. However, the plant has now been reopened by SSI, which might boost entrepreneurial activity in the region.

Companies with shares changing hands

318 3232011 2012

Average profit

£1.9m £1.4m2011 2012

Average age of company

22 242011 2012

Jobs per hundred people in region

2.6 2.42011 2012

% increase from H2 2011

2%2012

Companies with shares changing hands

338 3622011 2012

Average profit

£0.9m £2.1m2011 2012

Average age of company

23 252011 2012

Jobs per hundred people in region

1.7 2.02011 2012

% increase from H2 2011

7%2012

Wales saw a 7% rise in entrepreneurial activity, up to 362 from 338 a year ago. Although this was at the lower end of the spectrum, the financial health of companies in Wales with shares changing hands was above average across the UK and ROI at £2.1m, up a remarkable 133% compared to a year ago. At the same time, the average age of these companies had also increased to 24.6 years.

These companies also employed just fewer than 2 people out of every 100 in the region, one of the lowest across the UK and ROI. Graham Morgan, Chief Executive at the Wales Chamber of Commerce believes that high employment levels in the area in the public sector may be the indirect cause of low levels of entrepreneurial activity: “Wales has been slightly insulated from public sector job losses, which have impacted other areas of the UK. With low levels of unemployment, the incentive to start your own business is perhaps less here than elsewhere.”

Wales was one of a handful of regions, including the North West, Midlands and Yorkshire & Humberside, where industry led the way with shareholder transactions in growing companies in this sector up 46%. More than half of companies (185) with shares changing hands were in the industrial sector. Retail and technology had the next largest proportions of shareholder transactions but paled into insignificance by comparison.

Graham Morgan sees the logic in the industrial sector’s dominance of entrepreneurial activity: “Our regional economy is steeped in traditions of industry. Folks with experience in the coal and steel sectors have developed tangible skills which they are able to bring to entrepreneurial endeavours.”

IndustrialIndustrial

45%48%

57%

52%

RetailRetail

28%28%

18%

23%

TechTech

6%

12%

8%7%

Knowledge Based

Knowledge Based

16%

6%

UtilitiesUtilities

2%3% 2%4%

PropertyProperty

1%2%0%

3%

PrimaryPrimary

1%1%2%0%0% 1%

PublicPublic

3%4%3%5%

2%4%

2%1%

FinanceFinance

60%60%

0%0%

Key

H2 2011 H2 2012

Source: Ledbury Research

4140

Republic of IrelandNorthern Ireland

Northern Ireland saw a 33% fall in companies with shares changing hands from 418 down to 279, the second lowest result nationally.

More than half of the businesses with shares changing hands in Northern Ireland were in the industrial sector and a further third in the retail sector. The sectors with the greatest fall in shareholder transactions amongst growing companies were in the knowledge sector, made up largely of management consultancies.

This contrasted strongly with profitability, which increased by 160%, but was still below the average across the UK & ROI at £1.3m. Northern Ireland also had the most mature businesses changing hands, with an average age of 27, an increase of 5 years compared to the average age a year ago.

In line with the fall in number of companies changing hands, the number of people employed by these companies also fell to 3.2 out of every 100 in the region, from 4.1 a year ago.

Companies with shares changing hands

418 2792011 2012

Average profit

£0.5m £1.3m2011 2012

Average age of company

22 272011 2012

Jobs per hundred people in region

4.1 3.22011 2012

% increase from H2 2011

-33%2012

Companies with shares changing hands

495 3112011 2012

Average profit

-£1.1m £3.8m2011 2012

Average age of company

15 182011 2012

Jobs per hundred people in region

1.7 0.82011 2012

% increase from H2 2011

-37%2012

The Republic of Ireland had the biggest fall in numbers of companies with shares changing hands, down from 495 to 311. These companies were the youngest across the UK and ROI (18 years on average). However, it was second only to Scotland in the profitability of businesses with shares changing hands at £3.8m, quite remarkable as these businesses were making an average loss of £1.1m a year ago.

Ian Talbot, Chief Executive, Chambers Ireland, is not surprised by this jump in profitability. “Irish companies have been forced to become more competitive over the last four years. This surge in profits is down to businesses adapting to drive down costs and survive in a very different marketplace.”

When it comes to falls in the number of companies reporting shareholder transactions, Ian Talbot suspects this is down to less opportunistic transactions taking place. “There are less distressed sales now,” he remarks. “Companies are no longer buying at the bottom of the market.

The greatest fall in shareholder transactions in growing companies was in property companies, followed by retail. Notably, the Republic of Ireland was the only region to see a decrease in the number of companies with shares changing hands in the finance sector. This is likely to be because it was not affected by the increasing regulation brought in by the Retail Distribution Review on 1 January 2013, which caused consolidation in every other region.

In line with the fall in number of companies changing hands, the number of people employed by these companies also fell to 0.8 out of every 100 in the region, from 1.7 a year ago. As the amount of start-up activity increases in new sectors, such as technology, and falls in more traditional industries, there are now worries there could be a skills shortage amongst employees.

IndustrialIndustrial

22%

46%

25%

51%

RetailRetail

28%25%

33%

21%

27%

31%

TechTech

9%6%

13%

Knowledge Based

Knowledge Based

9%

UtilitiesUtilities

2%3% 2%3%

PropertyProperty

4%1% 1%1%

PrimaryPrimary

2%2% 1%2%

PublicPublic

4%5%3%3% 3%4% 3%

1%3% 2%

FinanceFinance

60%60%

0%0%

Key

H2 2011 H2 2012

Source: Ledbury Research

42

Legal note

Whilst every effort has been taken to verify the accuracy of this information, neither Ledbury Research nor Barclays can accept any responsibility or liability for reliance by any person on this report or any of the information, opinions or conclusions set out in the report. This document is intended solely for informational purposes, and is not intended to be a solicitation or offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or to provide any investment advice or service.

This item can be provided in Braille, large print or audio by calling 0800 400 100* (via TextDirect if appropriate). If outside the U.K. call +44 (0)1624 684 444* or order online via our website barclays.com/wealth. *Calls may be recorded so that we can monitor the quality of our service and for security purposes. Calls made to 0800 numbers are free if made from a U.K. landline. Other call costs may vary, please check with your telecoms provider. Lines are open from 8 a.m. to 6 p.m. U.K. time Monday to Friday.

“Barclays” refers to any company in the Barclays PLC group of companies.

Barclays offers wealth management products and services to its clients through Barclays Bank PLC (“BBPLC”) that functions in the United States

through Barclays Capital Inc. (“BCI”), an affiliate of BBPLC. BCI is a registered broker dealer and investment adviser, regulated by the U.S. Securities

and Exchange Commission, with offices at 200 Park Avenue, New York, New York 10166. Member FINRA and SIPC.

Barclays Bank PLC, registered in England and Wales (no. 1026167), has a registered office at 1 Churchill Place, London, E14 5HP, United Kingdom,

and is regulated by the Financial Services Authority.

Mortgage products and services in the U.S are offered by Barclays Bank Delaware (“BBD”), member FDIC. Custom lending is offered via BBPLC, New

York Branch. Securities investing and brokerage products and services are offered exclusively through BCI. A relationship with the Barclays Wealth and

Investment Management unit need not be established or maintained to obtain BBD or BBPLC, New York Branch products or pricing. Bank regulations

require that the loan review and approval proves to be independent of, and cannot be impacted by, brokerage/investment-related matters or other

business dealings.

Trust and fiduciary services are offered through Barclays Wealth Trustees (U.S.), N.A. (“BWT”) a limited purpose national bank. BWT is subject to

regulation and examination by the Office of the Comptroller of the Currency. BWT is an indirect, wholly-owned subsidiary of BBPLC and an affiliate

of BCI and various other subsidiaries of, and entities affiliated with, BBPLC.

This is not a solicitation of any products or services.

IRS Circular 230 Disclosure: BCI and its affiliates do not provide tax advice. Please note that (i) any discussion of U.S. tax matters contained in this

communication (including any attachments) cannot be used by you for the purpose of avoiding tax penalties; (ii) this communication was written

to support the promotion or marketing of the matters addressed herein; and (iii) you should seek advice based on your particular circumstances

from an independent tax advisor.

© Barclays 2013. All rights reserved.

Contact us

Tel. 0800 851 851 or dial internationally +44 (0)141 352 3952

For further information about Barclays, please visit our website barclays.com/wealth

MethodologyLedbury Research looked at the Annual Returns of all companies in the UK and Ireland and analysed the demographics of private companies that had changed the details of their shareholders over three reporting periods: H2 2011, H1 2012 and H2 2012. The reasons for these shareholder transactions can be summarised as follows: • To realise wealth through the sale of shares;• For personal tax reasons;• To effect corporate restructuring;• Life event related.

A core reason for a shareholder change is a liquidity event triggered by individuals selling their stakes in businesses, making it a suitable proxy for tracking entrepreneurial activity. The focus of the research was on active companies with growing revenues, to sift out distressed sales which would not be representative of entrepreneurial activity. This was further narrowed down to include only those companies with revenues between £5m and £200m. This was to position our dataset to be independent of FTSE 250 companies and also recognising the complications of the use of the limited company structure to help tax planning for contractors and other professionals, and that some registered companies are shell companies.

We analysed primary trading addresses of these companies, as opposed to their primary registered addresses.

In H2 2012, the vast majority (87%) of the shareholders making share transactions sold all of their holdings. The average change in total shareholding in these companies during the period was relatively small, at 14%.

The research also looked at the gender split of the shareholders who had made changes to their shareholding, although the interpretation of this

data is complicated by the fact that there may be tax reasons for holding company shares in a spouse’s name. By keeping the methodology consistent in each wave, we can track changes in the make-up of these entrepreneurial transactions over time.

Graphic 1: H2 2012 Numbers

Graphic 2: H2 2011 Numbers

There were 7.7m active companies in the period …

… of which 1.7m registered a change in shareholding …

.. and 35,000 of these had annual revenues of £5-£200m …

… and 24,000 of these had growing sales

There were 7.3m active companies in the period …

… of which 2.2m registered a change in shareholding …

.. and 33,000 of these had annual revenues of £5-£200m …

… and 21,000 of these had growing sales

![Fixed Income Index Guide - BlackRock · [10] FIXED INCOME INDEX GUIDE Bloomberg Barclays index family ... Broad family of fixed income indices, including: aggregate, government, corporate,](https://img.dokumen.tips/doc/110x75/5b0274907f8b9af1148fb575/fixed-income-index-guide-blackrock-10-fixed-income-index-guide-bloomberg-barclays.jpg)