Embed Size (px)

Citation preview

Water: Back to GrowthThomas Kunz

Summary

Significant topline growth is back

Our crisis strategy clearly worked and has helped to give

the category new relevance and meaning

Input costs are a challenge. Our productivity mindset goes

a long way to compensate, but pricing action has been

inevitable

Aquadrinks become an increasingly important growth driver

– 2 –

Reminder 2009: Our objectives

– 3 –

Accelerate

in Developing Countries

Return Mature Countries to growth

Reminder 2009:Three priorities across all geographies

– 4 –

1 2 3

Per Capita Consumption

CATEGORY GROWTH BRAND PRESENCE COST BASE

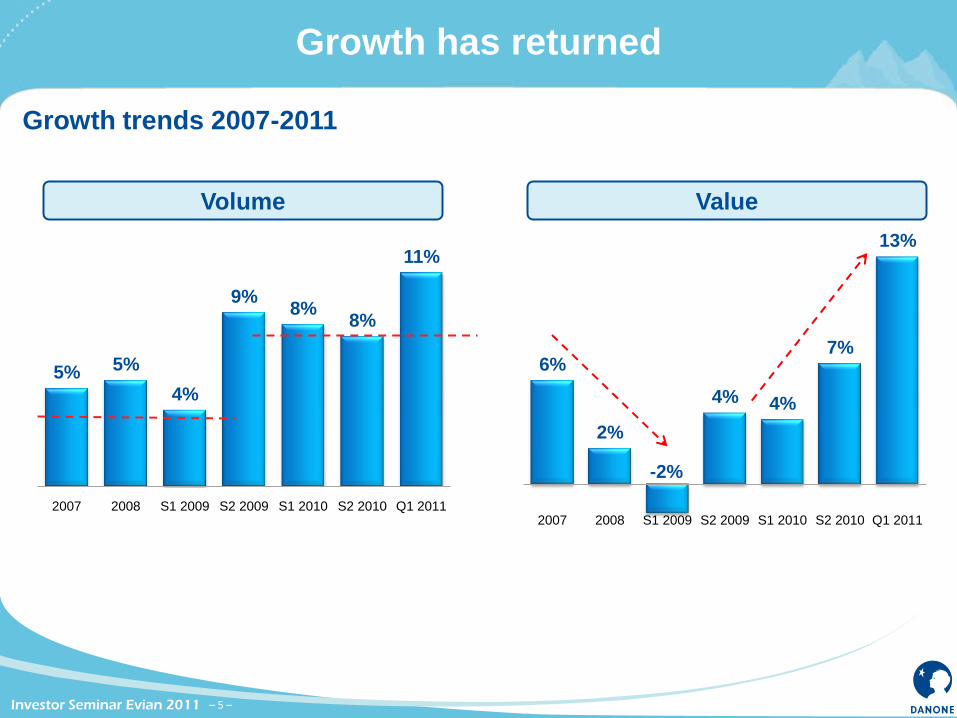

Growth has returned

– 5 –

5% 5%

4%

9%8%

8%

11%

2007 2008 S1 2009 S2 2009 S1 2010 S2 2010 Q1 2011

6%

2%

-2%

4% 4%

7%

13%

2007 2008 S1 2009 S2 2009 S1 2010 S2 2010 Q1 2011

Volume Value

Growth trends 2007-2011

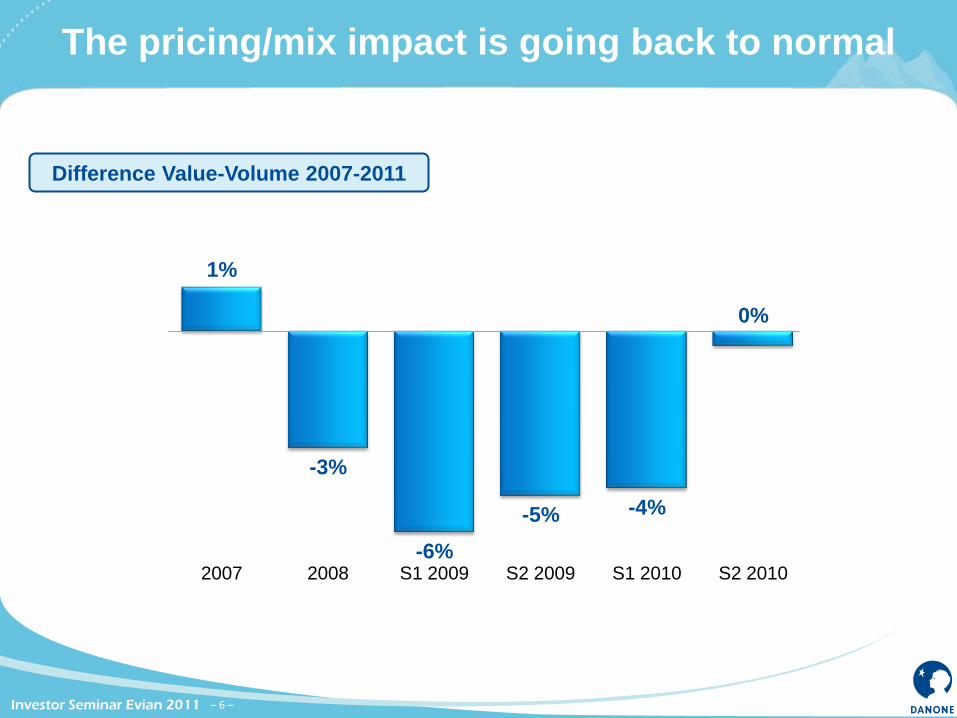

The pricing/mix impact is going back to normal

– 6 –

1%

-3%

-6%

-5% -4%

0%

3%

2007 2008 S1 2009 S2 2009 S1 2010 S2 2010 Q1 2011

Difference Value-Volume 2007-2011

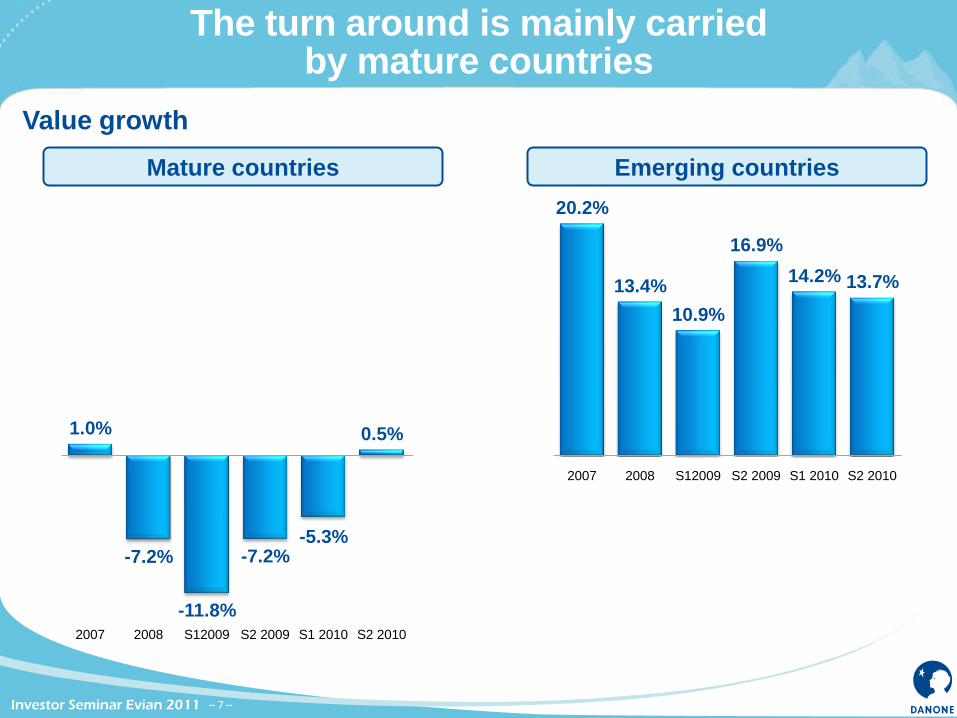

The turn around is mainly carried by mature countries

– 7 –

20.2%

13.4%

10.9%

16.9%

14.2% 13.7%

19.2%

2007 2008 S12009 S2 2009 S1 2010 S2 2010 Q1 2011

Mature countries Emerging countries

Value growth

1.0%

-7.2%

-11.8%

-7.2%-5.3%

0.5%

5.7%

2007 2008 S12009 S2 2009 S1 2010 S2 2010 Q1 2011

Sorecard: Our objectives

– 8 –

Accelerate

in Developing Countries

Return Mature Countries to growth

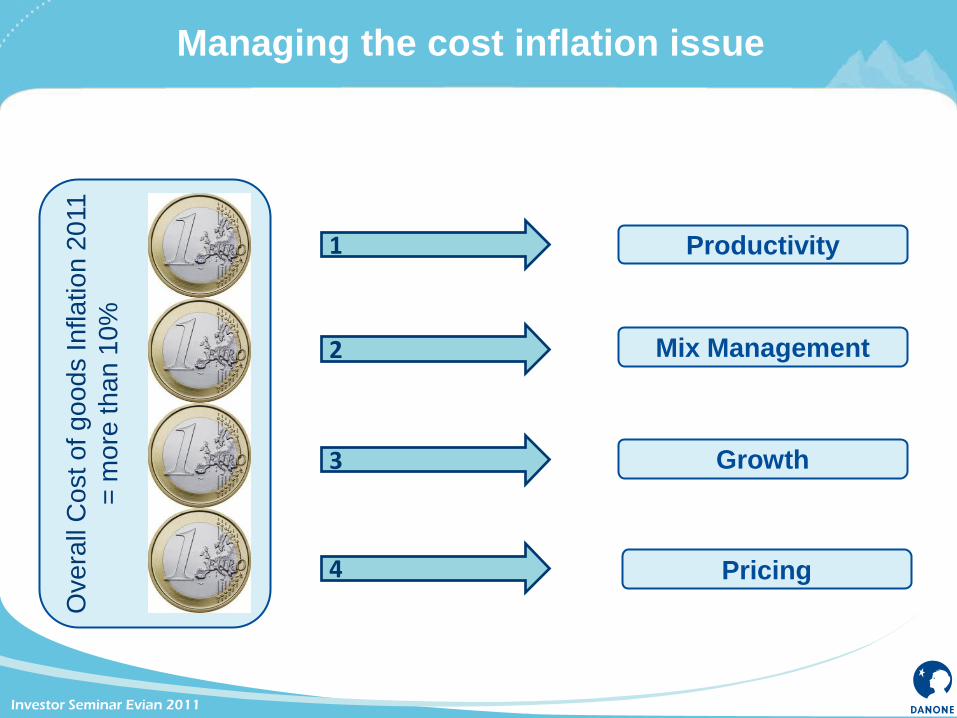

Managing the cost inflation issue O

vera

ll C

ost of goods Inflation 2

011

= m

ore

th

an

10

%

1

2

3

4

Productivity

Growth

Mix Management

Pricing

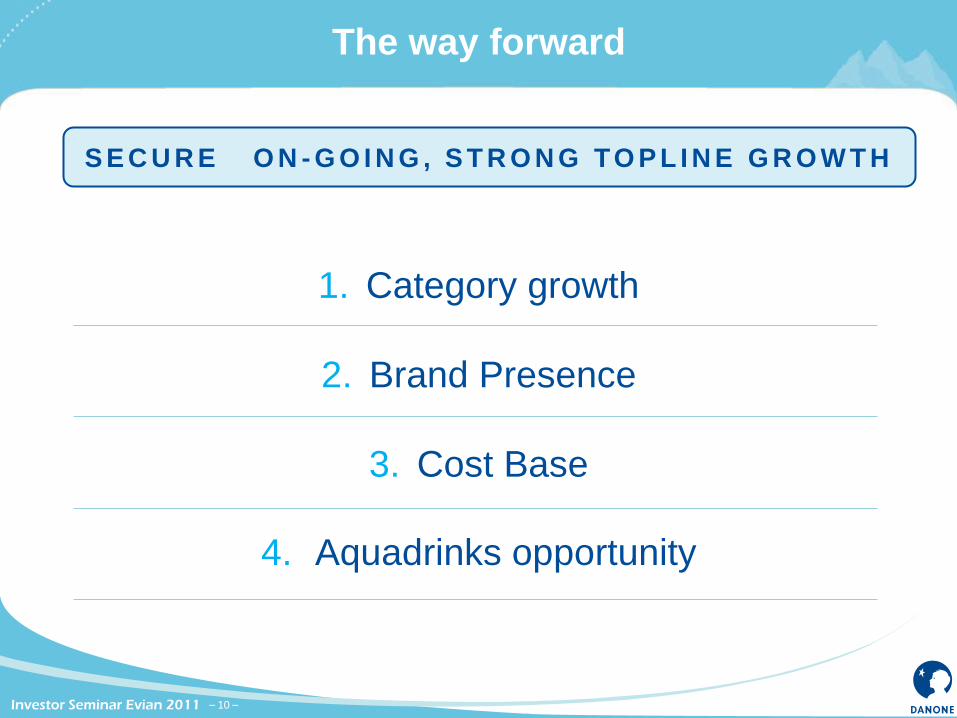

The way forward

– 10 –

1. Category growth

2. Brand Presence

3. Cost Base

4. Aquadrinks opportunity

S E C U R E O N - G O I N G , S T R O N G TO P L I N E G R O W T H

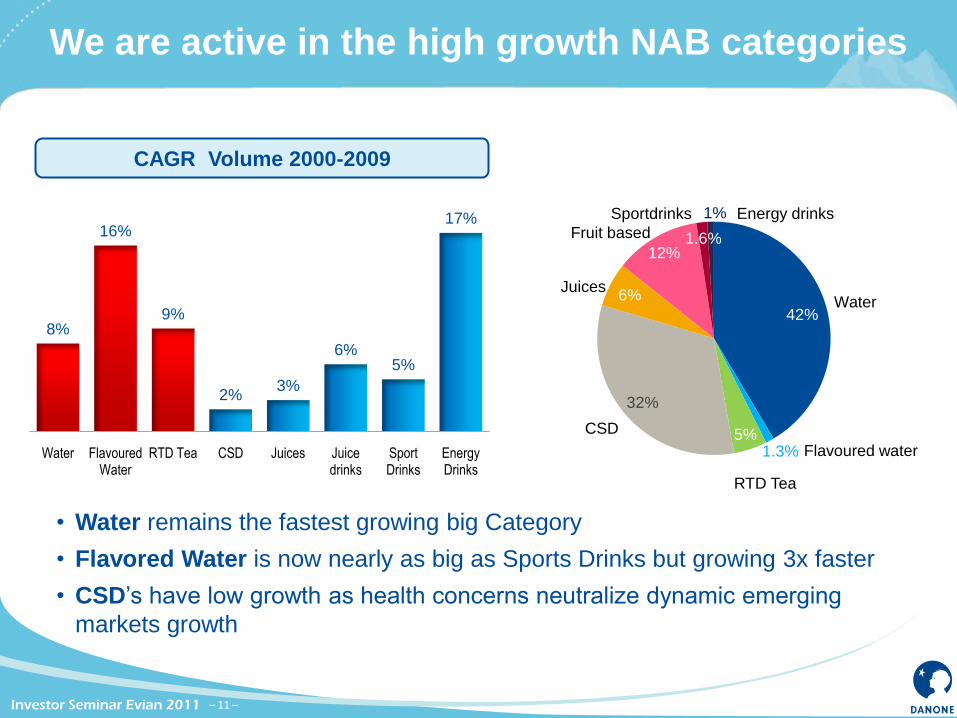

We are active in the high growth NAB categories

– 11 –

• Water remains the fastest growing big Category

• Flavored Water is now nearly as big as Sports Drinks but growing 3x faster

• CSD’s have low growth as health concerns neutralize dynamic emerging

markets growth

8%

16%

9%

2%3%

6%5%

17%

Water Flavoured Water

RTD Tea CSD Juices Juice drinks

Sport Drinks

Energy Drinks

42%

1.3%5%

32%

6%

12%1.6%

1% Energy drinksSportdrinks

Juices

CSD

RTD Tea

Flavoured water

Water

Fruit based

CAGR Volume 2000-2009

– 12 –

Growing the Water Category

96 mln mangroves planted since 2009

(Danone Ramsar wetlands protection initiative)

22% CO2 reduction achieved since 2008

The first bottle 100% from R-Pet

21% water usage reduction in 2009-2010

Sustainable development remains at the heart of our model

The first (partial) Bio bottle for water

Key achievements

Our Marketing battles for category and Brand growth

The battle for WATER

The battle for

NATURAL WATER

The battle for

our BRANDS

The battle for

WATER

Grow Water share of throat

Grow our brands

Promote NW superiority

1. Water is the healthiest

beverage2. We don’t drink enough

Water

The battle for WATERThe battle for

WATER

The Way Forward – Category Growth remainskey focus

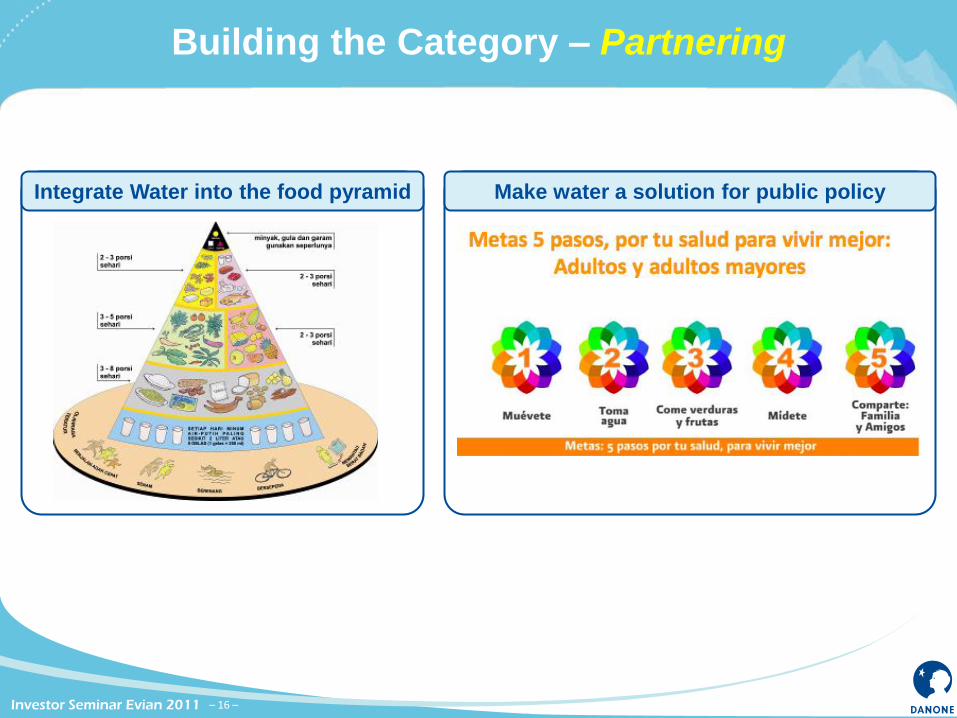

Building the Category – Partnering

– 16 –

Make water a solution for public policy Integrate Water into the food pyramid

Targeted Activities

Building the Category – Consumer Action

– 17 –

EducationCommunication

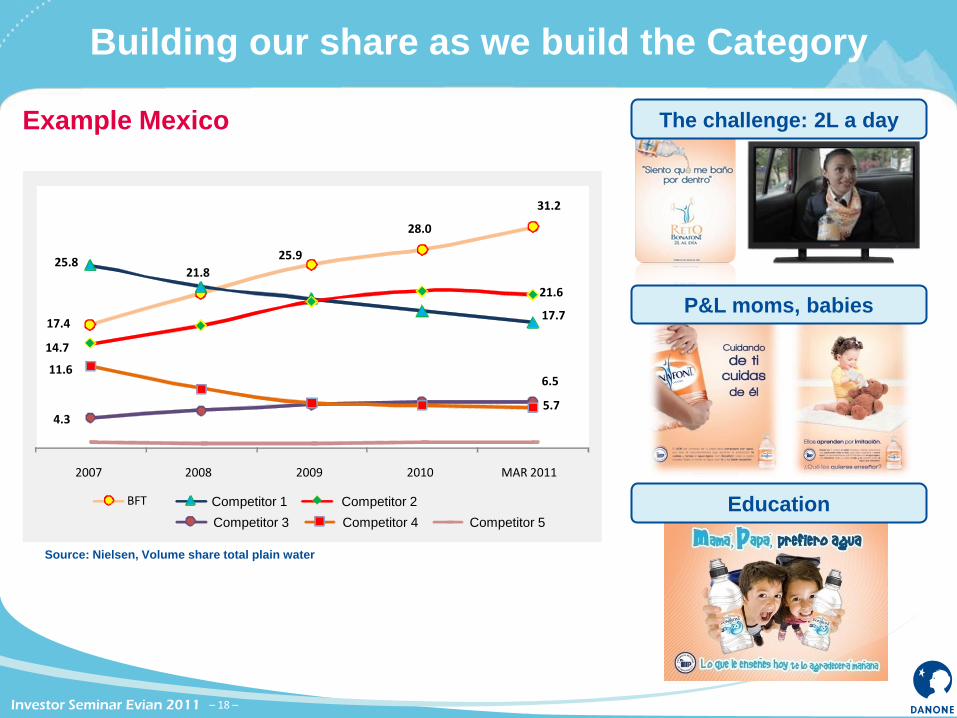

Building our share as we build the Category

– 18 –

Example Mexico The challenge: 2L a day

P&L moms, babies

Education

17.4

21.8

25.9

28.0

31.2

25.8

17.7

14.7

21.6

4.3

6.511.6

5.7

2007 2008 2009 2010 MAR 2011

BFT Competitor 1

Source: Nielsen, Volume share total plain water

Competitor 5Competitor 4Competitor 3

Competitor 2

BRw/o SP

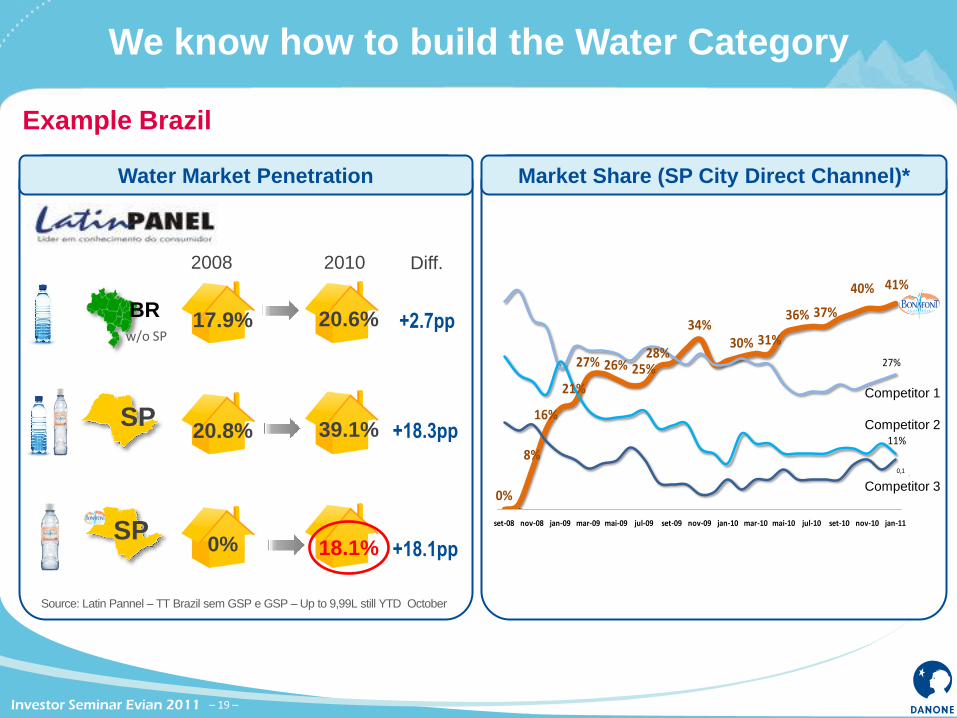

17.9%

2008 2010 Diff.

Source: Latin Pannel – TT Brazil sem GSP e GSP – Up to 9,99L still YTD October

SP20.8%

Water Market Penetration

We know how to build the Water Category

– 19 –

Example Brazil

20.6% +2.7pp

SP18.1% +18.1pp0%

39.1% +18.3pp

0%

8%

16%

21%

27% 26% 25%28%

34%30% 31%

36% 37%

40% 41%

27%

11%

0,1

set-08 nov-08 jan-09 mar-09 mai-09 jul-09 set-09 nov-09 jan-10 mar-10 mai-10 jul-10 set-10 nov-10 jan-11

Market Share (SP City Direct Channel)*

Competitor 1

Competitor 2

Competitor 3

Aqua Indonesia grows and grows and…

– 20 –

2007 2008 2009 2010

Every year,

we add the

VOLUME of:x0.6

Indonesia Volume growth

+ 753 ML

+ 780 ML

+ 842 ML

– 21 –

Exploiting the Aquadrinks Opportunity

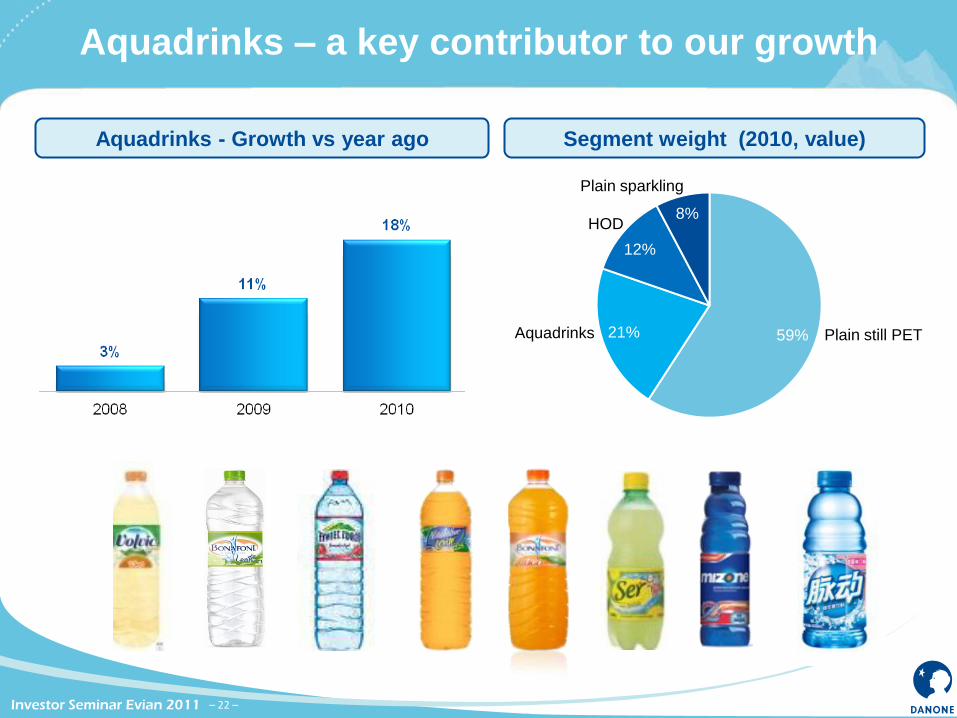

Aquadrinks – a key contributor to our growth

– 22 –

Aquadrinks - Growth vs year ago

59%21%

12%

8%

Segment weight (2010, value)

Plain still PET

Plain sparkling

HOD

Aquadrinks

Aquadrinks – two main development categories

– 23 –

Enhanced Water

• Water based Drink with flavor

and other ingredients (Vitamins,

Minerals…)

• Specific Brand

• Hydration plus additional (soft)

functionality

• Mostly positioned in-between

Flavoured Water

• Water with flavoring ingredients

(flavors, juice, tea extracts..)

• Based on Water Brand

• No additional functionality

on top of hydration

• Mostly positioned for meal usage

Drinkable

NaturalHydrating

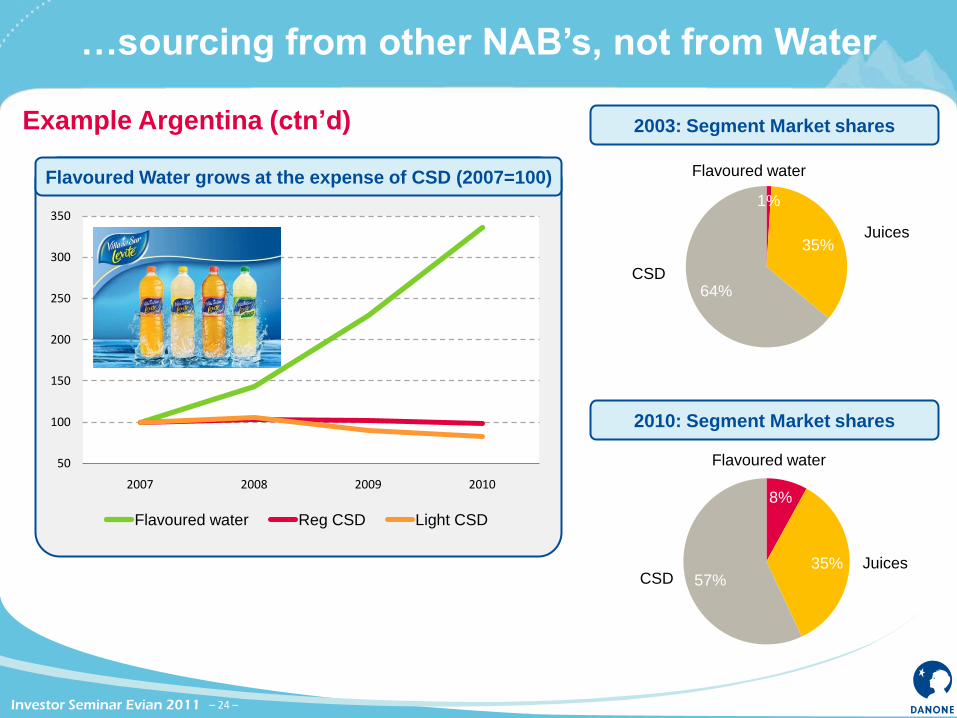

…sourcing from other NAB’s, not from Water

– 24 –

Example Argentina (ctn’d)

Flavoured Water grows at the expense of CSD (2007=100)

50

100

150

200

250

300

350

2007 2008 2009 2010

Flavoured water Reg CSD Light CSD

1%

35%

64%

2003: Segment Market shares

Juices

Flavoured water

CSD

2010: Segment Market shares

Juices

Flavoured water

CSD

8%

35%57%

An success story in more and more countries

– 25 –

Aquadrinks growth (indexed, 2007=100))

Mexico Germany

Poland UK

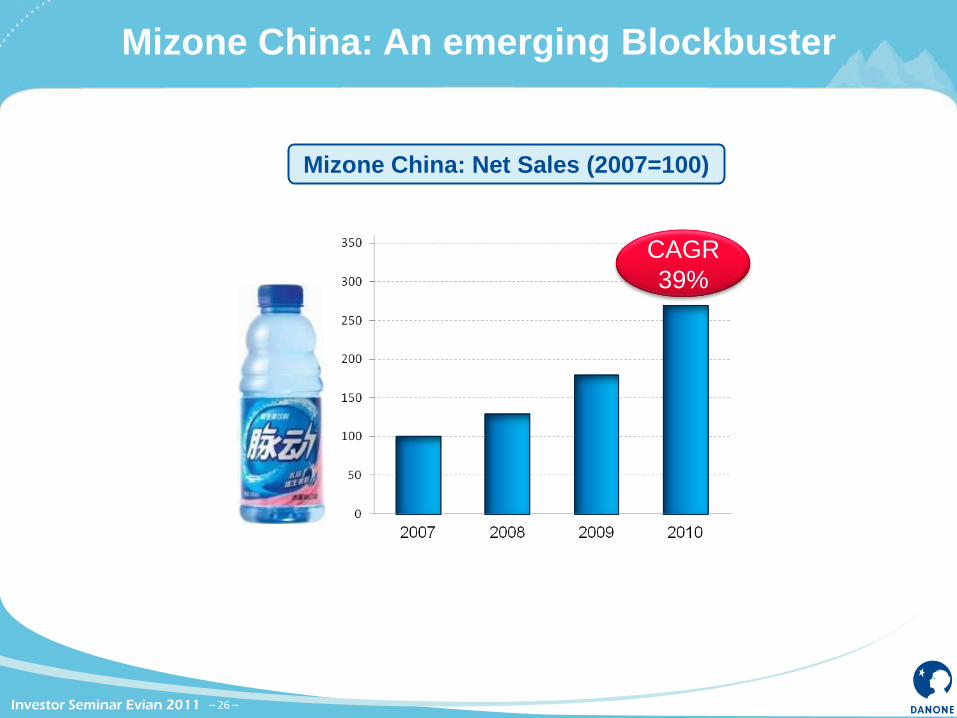

Mizone China: An emerging Blockbuster

– 26 –

Mizone China: Net Sales (2007=100)

CAGR

39%

– 27 –

Healthy Brandsfor

Healthy Growth