Embed Size (px)

Citation preview

VISION —Monthly Economic and Financial Monitor

April 2015

Research Analysts—

Ihor Danyliuk 416-869-7522Head of Research

Greg Colman 416-869-6775Deputy Head of Research

Caroline Jukes 416-869-8039Administrative Manager

Tanya Bouchard 416-869-7934Supervisory Analyst

Research PublicationsVanda Bright 416-869-7141Manager, Publishing Services

Wayne Chau 416-869-7140Publishing Associate

Information and Distribution Institutional Clients

Giuseppe Saltarelli [email protected]

Retail Branches

Anoochka Gokhool [email protected]

Economics and Strategy Stéfane Marion 514-879-3781Chief Economist and Strategist Paul-André Pinsonnault 514-879-3795Senior Fixed Income EconomistKrishen Rangasamy 514-879-3140Senior EconomistMarc Pinsonneault 514-879-2589Senior EconomistMatthieu Arseneau 514-879-2252Senior Economist

Communications, Media and TelecomAdam Shine 514-879-2302Associate: Peter Stusio 514-879-2564Associate: Kevin Krishnaratne 416-869-6585

Energy Agriculture and Energy Services

Greg Colman 416-869-6775Associate: Andrew Jacklin 416-869-7571Associate: Sean Wetmore 416-869-6763Associate: Michael Storry-Robertson 416-507-8007

Junior and Intermediate Oil and Gas

Dan Payne 403-290-5441Brian Milne 403-290-5625Associate: Tim Sargeant 403-441-0952Associate: Mark Hirsch 403-441-0928

Senior and Intermediate Yield Oil and Gas

Kyle Preston 403-290-5102Associate: Jason Wai 403-355-6643

Pipelines, Utilities and Energy Infrastructure

Patrick Kenny 403-290-5451Associate: Michael Nguyen 403-290-5447

Financial Services Banking and Insurance

Peter Routledge 416-869-7442Associate: Parham Fini 416-869-6515Associate: Paul Poon 416-507-8006

Diversified Financials

Shubha Khan 416-869-6425Associate: Jaeme Gloyn 416-869-8042

Merchandising and Consumer ProductsVishal Shreedhar 416-869-7930Associate: Ryan Li 416-869-6767

Metals and MiningShane Nagle 416-869-7936Associate: Raj Udayan Ray 416-507-8105Associate: Gregory Doyle 416-869-6538

Steve Parsons 416-869-6766Associate: Don DeMarco 416-869-7572

Adam Melnyk 604-643-2864Associate: David Lee 416-869-8045

Real EstateMatt Kornack 416-507-8104Associate: Dawoon Chung 416-507-8102

Trevor Johnson 416-869-8511Associate: Endri Leno 416-869-8047Associate: Kyle Stanley 416-507-8108

Special SituationsLeon Aghazarian 514-879-2574Associate: Frédéric Tremblay 514-412-0021Associate: Jean-François Bourdon 514-390-7825

Trevor Johnson 416-869-8511Associate: Endri Leno 416-869-8047Associate: Kyle Stanley 416-507-8108

Chris Bowes 416-869-7375Associate: John Xu 416-507-9115

Sustainability and Clean Tech Rupert Merer 416-869-8008Associate: Jeremy Mersereau 416-869-6768Associate: Mark Vernest 416-869-7476

Technology Kris Thompson 416-869-8049Associate: Auritro Kundu 416-869-7495Associate: Steven Walt 416-869-7938

Transportation and Industrials Cameron Doerksen 514-879-2579Associate: Umayr Allem 416-869-8577

Technical AnalysisDennis Mark 416-869-7427

ETF Research and Strategy Associate: Daniel Straus 416-869-8020Associate: Ling Zhang 416-869-7942

Geopolitical AnalysisPierre Fournier 514-879-2423Associate: Angelo Katsoras 514-879-6458

Table of Contents—Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 02

The Economy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 05

Interest Rates and Bond Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Stock Market and Portfolio Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Technical Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

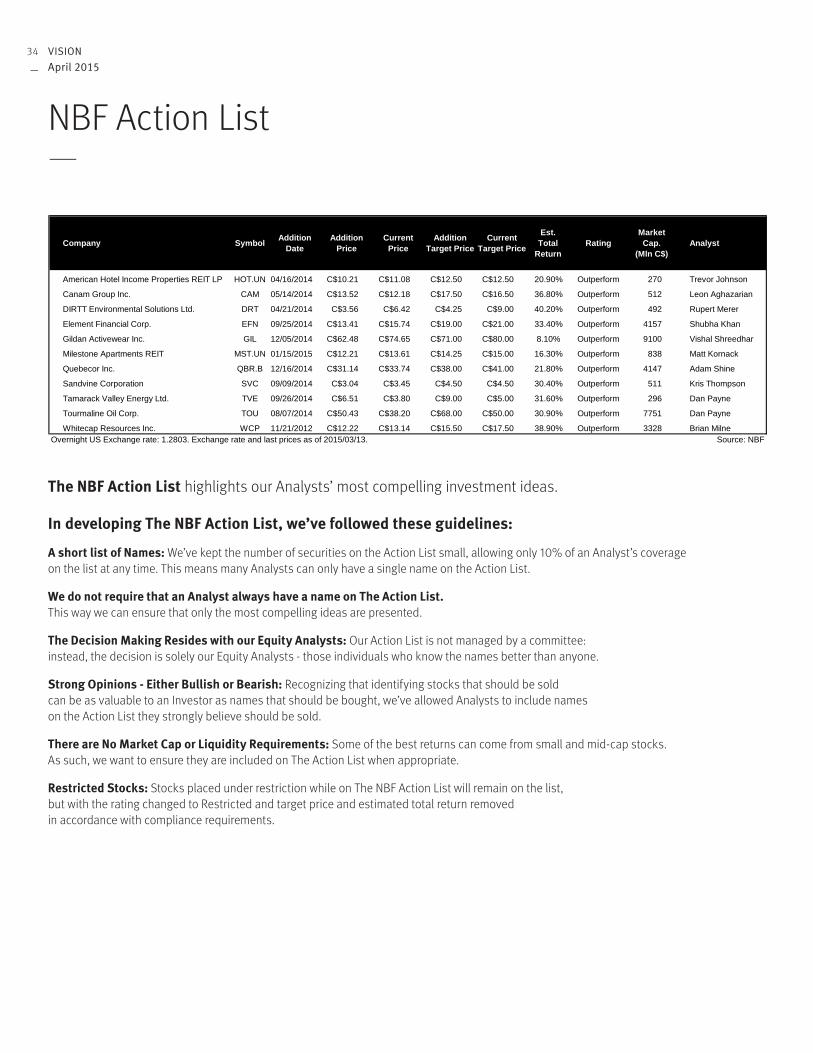

NBF Action List . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Sector Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Analyst Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Alphabetical Listing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

NBF Disclosures, please visit URL: http://www.nbcn.ca/contactus/disclosures.html

For a paper copy of the disclosures, please send a written request (indicating the name and date of the product) to:National Bank Financialc/o Giuseppe Saltarelli1155, Metcalfe Street 5th Floor Montreal (Quebec), CanadaH3B 4S9

VISIONApril 2015

02

—

Economy

Thanks in part to a weakening euro, the eurozone economy is finally showing some promising signs . We have, accordingly, raised our growth forecasts for the common currency area . Newly announced stimulus by Beijing also gives a boost to China’s prospects . However, those are more than offset by a downgrade to our U .S . outlook, which prompts us to trim by two ticks our 2015 global growth forecast to 3 .3% .

It’s déjà vu in the U .S ., as a harsh winter again wrecked Q1 economic activity . The poor start of the year forces us to cut our 2015 forecast for GDP growth to 2 .9% . That said, fundamentals for domestic demand remain strong, including a consumer that’s being lifted by the best labour market in years . The Fed remains on track to hike interest rates later this year, but don’t expect it to get aggressive when it starts tightening . The strong U .S . dollar is not only hindering exports, but is also making it more difficult for inflation to reach the Fed’s 2% target .

Like the U .S ., Canada struggled in the first quarter of the year in part due to weather-related disruptions to economic activity . GDP growth in Q1 is pacing below 1% annualized, the worst performance in years . Growth should pick up from here, but we’re not expecting stellar results considering the full impact of the oil price collapse has yet to be felt, e .g . anticipated decline in investment and employment particularly in the oil patch . We continue to forecast 2% growth this year, expecting Central provinces to make the most of a cheap currency and offset weakness in Western Canada .

Interest Rates and Currency

With the Fed no longer committed to patience, but clearly stating that its policy stance will be data-dependent, the sensitivity of the yield curve to economic indicators is likely to step up a notch . We accordingly expect greater market volatility in the months ahead . That said, since the FOMC participants’ view of the appropriate path of the target fed funds rate in 2015 is closely aligned with our own, we are leaving our year-end forecast for 10-year Treasuries unchanged at 2 .34% .

Although uncertainty about the price of oil and the path of Canadian monetary policy is relatively high, we are inclined to think the overnight rate will end the year unchanged at 0 .75% . However, our conviction that the Bank of Canada will lag the Fed in rate hikes is much stronger . We continue to see the BoC target rate at 1% in Q4 2016 .

The Canadian dollar, like several other major currencies, went on a roller coaster ride in March, courtesy of USD-related gyrations . The USD’s initial ascent was fueled by expectations the Fed would remove the word “patient” from its forward guidance and hence open the door to rate hikes . The Fed did just that, but it also downgraded its forecasts for GDP growth, inflation, and even the fed funds rate, which prompted a subsequent USD selloff . So, while the greenback should continue to benefit from diverging monetary policy in the U .S . and the rest of the world, there could be some short-term volatility if there are any hints the Fed may delay rate hikes to later, or if improving eurozone data prompts markets to question the necessity of the ECB’s QE program . We remain comfortable with our view that USDCAD will trade in the 1 .20-1 .30 range over the near to medium term .

Recommended Asset Mix and Stock Market

After a very good performance in February, global equities hit new records in March . The MSCI AC index remains on track for a record 11th consecutive quarterly increase . Although the forward P/E of the MSCI AC is close to its historical average, equities remain an attractive asset class .

Equity markets should be supported by the fall of oil and food prices in many parts of the world which allows central banks to inject more liquidity and/or to delay the process of normalization toward higher interest rates . Moreover, we see earnings still rising as the expansion phase of the U .S . economic cycle is still young and the euro zone seems to be recovering, to judge by upticks not just in industrial output but in domestic demand, as labour markets show signs of improving .

Our asset mix is unchanged this month . We remain comfortable with our current recommendation to overweight equities relative to our benchmark, with a slight preference for non-U .S . assets to reflect our view that the U .S . dollar is likely to stabilize somewhat . Our year-end targets are 16,200 for the S&P/TSX and 2,220 for the S&P 500 .

Our sector rotation is also unchanged this month with its slight preference for non-interest-sensitive sectors . We are staying with our overweight recommendation for the Canadian Energy sector . A rise in energy prices due to the combined effect of U .S . production cutbacks and a tamer greenback could reignite interest in this sector .

Highlights—

Stéfane Marion Chief Economist and Strategist 514-879-3781

03

—

Highlights—

Benchmark (%)

NBF Recommendation (%)

Change (pp)

EquitiesCanadian Equities 30 33U.S. Equities 10 12Foreign Equities (EAFE) 10 9Emerging markets 5 8

Fixed IncomeCanadian Bonds 30 28Foreign Pay Bonds 0 0Real Return Bonds 10 5

Cash 5 5Total 100 100NBF Economics and Strategy

NBF Asset AllocationActual ForecastLevel Q4 2015 (Est.)

INTEREST RATES

3-month US 0.04 0.69 CA 0.53 0.63

10 yrs US 1.92 2.34 CA 1.34 1.89

STOCK MARKET Q4 2015 (Est.)Target

S&P 500 2,061 2,220S&P/TSX 14,929 16,200

S&P/TSX Sectors Weight* Recommendation Change

Energy 21.4 Overweight

Materials 11.0 Market Weight

Industrials 8.4 Market Weight

Consumer Discretionary 6.5 Underweight

Consumer Staples 3.8 Underweight

Healthcare 4.9 Market Weight

Financials 34.6 Market Weight

Information Technology 2.4 Overweight

Telecommunication Services 4.7 Underweight

Utilities 2.2 Underweight

Total 100.0* As of March 25, 2015

NBF Sector Rotation

This page intentionally left blank .

The Economy—

VISIONApril 2015

06

—

World: Hope in Europe

Thanks in part to a weakening euro, the eurozone economy is finally showing some promising signs. We have, accordingly, raised our growth forecasts for the common currency area. Newly announced stimulus by Beijing also gives a boost to China’s prospects. However, those are more than offset by a downgrade to our U.S. outlook, which prompts us to trim by two ticks our 2015 global growth forecast to 3.3%.

The global economy ended 2014 like a lion according to latest data from the CPB . In the final quarter last year, industrial production grew at the fastest pace since 2013 as advanced economies bounced back with solid contributions from the U .S ., Japan and even the euro area . The healthy state of the world economy was further reflected by solid trade data — the value of trade fell with plunging oil prices, but more importantly volumes continued to rise, reaching a new record in December .

Unlike the prior quarter when growth was broad-based, the economic picture for Q1 is mixed . Advanced economies as a group are slowing down, but that’s largely due to disappointing data in the U .S . The prior quarter’s inventory build as well as bad weather, like last year, promise to significantly weigh on Q1 growth in the world’s largest economy (see U .S . section) . Japanese data hasn’t been great either . Besides continuing softness in housing investment, tepid demand together with lower energy prices have caused inflation to fall towards zero, moving further away from the Bank of Japan’s 2% target . The central bank, however, took no further action at its March meeting, saying it felt confident that longer term inflation expectations were rising . The economy should improve later this year considering the diminished fiscal drag (i .e . no sales tax slated for 2015), and as the trade sector continues to recover, helped by a competitive yen .

But weakness wasn’t widespread in advanced economies in Q1 . The Eurozone provided some upside surprises, helped perhaps by low expectations brought by serial disappointments earlier . The common currency area seems to be recovering based on the uptick not just for industrial output but also for domestic demand . Construction is slowly coming back, as is consumption spending as evidenced by rising new car registrations and higher retail volumes . The latter is being helped by an improvement in the labour market . The job vacancy rate in Q4 last year

climbed to 1 .8%, the highest since 2011, and the jobless rate fell to 11 .2% in January this year, the lowest since 2012 . Better credit may also be helping . Note that loans to households, while still down on a year-on-year basis, have now risen in the last two months .

-4-3-2-10123456789

1011

2011 2012 2013 2014

World: A good handoff to 2015 Global industrial production

NBF Economics and Strategy (data via CPB)

Q4

Emerging

Advanced

WORLD

q/q % chg. saar

96

100

104

108

112

116

120

124

128

132

136

140

144

2009 2010 2011 2012 2013 2014

World: Trade volumes at record high Global trade value and volumes

NBF Economics and Strategy (source CPB)

index

Volumes

Value

Dec.

-100

-80

-60

-40

-20

0

20

40

60

80

14Q1 14Q2 14Q3 14Q4 15Q1-30-25-20-15-10-505

10152025303540

14Q1 14Q2 14Q3 14Q4 15Q1

World: Mixed picture for Q1

NBF Economics and Strategy (data via Datastream)

Economic surprise index

Eurozone

U.S.

Recent drop in index for G10 … … largely due to the U.S.

G10

Emerging

Japan

Economic surprise index

The Economy—

Krishen Rangasamy Senior Economist 514-879-3140

07

—

-8

-6

-4

-2

0

2

4

6

8

10

12

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 201596

97

98

99

100

101

102

103

104

105

106

107

108

109

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Eurozone: Consumption starting to come back

NBF Economics and Strategy (data via Datastream)

Retail volumes Retail volumes and Loans to households

Retail volumes

Loans

index y/y % chg.

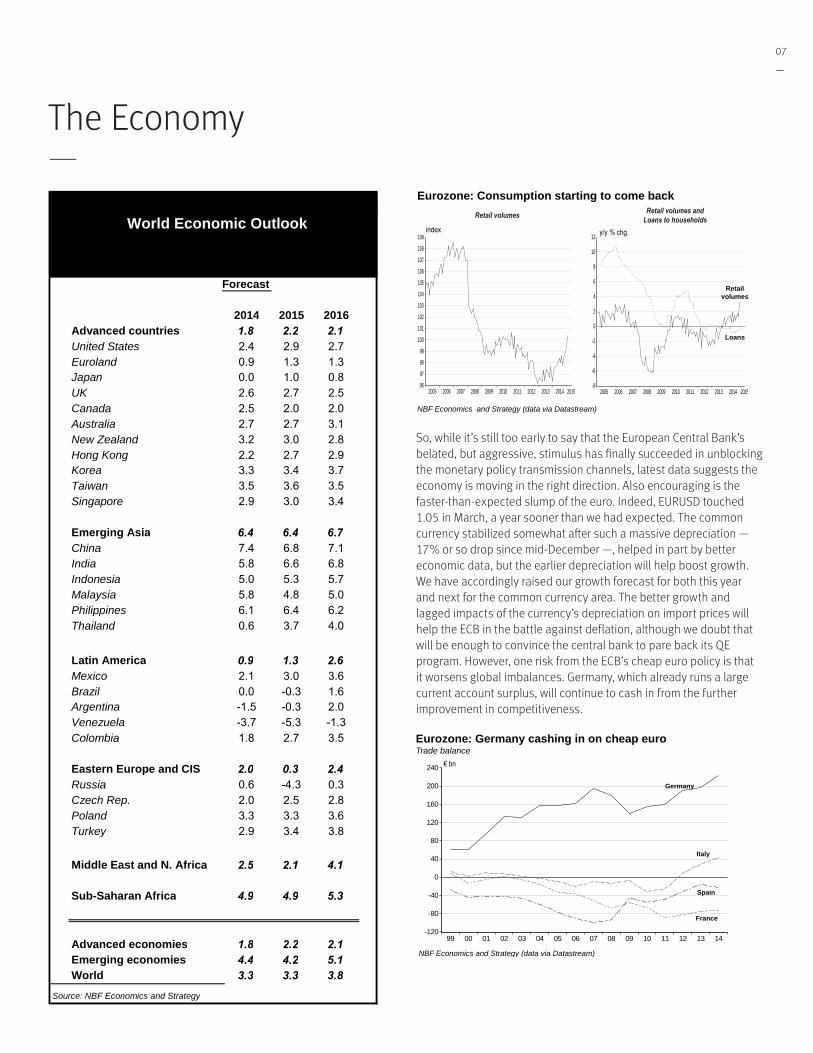

So, while it’s still too early to say that the European Central Bank’s belated, but aggressive, stimulus has finally succeeded in unblocking the monetary policy transmission channels, latest data suggests the economy is moving in the right direction . Also encouraging is the faster-than-expected slump of the euro . Indeed, EURUSD touched 1 .05 in March, a year sooner than we had expected . The common currency stabilized somewhat after such a massive depreciation — 17% or so drop since mid-December —, helped in part by better economic data, but the earlier depreciation will help boost growth . We have accordingly raised our growth forecast for both this year and next for the common currency area . The better growth and lagged impacts of the currency’s depreciation on import prices will help the ECB in the battle against deflation, although we doubt that will be enough to convince the central bank to pare back its QE program . However, one risk from the ECB’s cheap euro policy is that it worsens global imbalances . Germany, which already runs a large current account surplus, will continue to cash in from the further improvement in competitiveness .

-120

-80

-40

0

40

80

120

160

200

240

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Eurozone: Germany cashing in on cheap euro Trade balance

NBF Economics and Strategy (data via Datastream)

€ bn

Germany

France

Spain

Italy

The Economy—

World Economic Outlook

Forecast

2014 2015 2016 Advanced countries 1.8 2.2 2.1 United States 2.4 2.9 2.7 Euroland 0.9 1.3 1.3 Japan 0.0 1.0 0.8 UK 2.6 2.7 2.5 Canada 2.5 2.0 2.0 Australia 2.7 2.7 3.1 New Zealand 3.2 3.0 2.8 Hong Kong 2.2 2.7 2.9 Korea 3.3 3.4 3.7 Taiwan 3.5 3.6 3.5 Singapore 2.9 3.0 3.4

Emerging Asia 6.4 6.4 6.7 China 7.4 6.8 7.1 India 5.8 6.6 6.8 Indonesia 5.0 5.3 5.7 Malaysia 5.8 4.8 5.0 Philippines 6.1 6.4 6.2 Thailand 0.6 3.7 4.0

Latin America 0.9 1.3 2.6 Mexico 2.1 3.0 3.6 Brazil 0.0 -0.3 1.6 Argentina -1.5 -0.3 2.0 Venezuela -3.7 -5.3 -1.3 Colombia 1.8 2.7 3.5

Eastern Europe and CIS 2.0 0.3 2.4 Russia 0.6 -4.3 0.3 Czech Rep. 2.0 2.5 2.8 Poland 3.3 3.3 3.6 Turkey 2.9 3.4 3.8

Middle East and N. Africa 2.5 2.1 4.1

Sub-Saharan Africa 4.9 4.9 5.3

Advanced economies 1.8 2.2 2.1 Emerging economies 4.4 4.2 5.1 World 3.3 3.3 3.8

Source: NBF Economics and Strategy

VISIONApril 2015

08

—

Unfortunately, that erases part of the work done by the oil collapse in reducing savings imbalances across the globe — cheaper oil helps in rebalancing global savings by improving the current account balance of oil importing countries, which are often in deficit territory, at the expense of big oil exporters which usually enjoy large surpluses . As we’ve mentioned before, the global economy would be in better shape if Germany does its part by bringing down its excess savings via some fiscal stimulus which would not only help raise its own growth and inflation outlook, but also allow other eurozone members to improve relative competitiveness without having to put themselves through deflation .

Another risk brought by the ECB’s QE program, or equivalently the USD’s surge, is the impact on global financial stability . The trade-weighted USD has gained 16% since June, the fastest nine-month appreciation ever outside of the global financial crisis . That cannot be good for USD borrowers outside America . According to the Bank for International Settlements, the stock of dollar-denominated debt held by non-financial entities outside the U .S . has grown from around $6 trillion in 2008 to roughly $9 trillion . Emerging markets have seen their share of USD-denominated debt outside America rise to 40% . There is evidence that some over-extended borrowers are already under pressure, particularly in China which accounts for over $1 trillion of USD-denominated debt .

In addition to unfavourable currency movements, some debt issuers in China are also having to deal with a cash crunch as their investments sour, e .g . in the real estate sector . Sinking property prices are indeed hurting developers and their lenders, many of whom operate in the unregulated shadow banking sector . But not all is bleak . Beijing has taken action to reduce the economy’s overall exposure to the shadow sector by cracking down on that type of credit . That has led to a decline in social financing, the aggregate measure of credit, allowing conventional bank loans to increase their share of overall credit to the highest in almost three years . That’s good for sustainability of growth in China . Another positive for growth is the recent round of fiscal stimulus . In addition to increasing its budget deficit to roughly 1 .6 trillion yuan this year, or 2 .3% of GDP, Beijing has also decided to relax borrowing rules for local governments by increasing the quota for bond sales, which should help boost infrastructure spending . Low inflation has also allowed the People’s Bank of China to again cut its benchmark interest rate in March . Altogether, the new stimulus allows us to raise our growth forecast for China to 6 .8% this year and 7 .1% in 2016, both not far from Beijing’s newly-stated 7% target .

The upgrades to the Eurozone and China are, however, more than offset by a downgrade to our U .S . outlook, which prompts us to trim by two ticks our 2015 global growth forecast to 3 .3% .

-16

-12

-8

-4

0

4

8

12

16

20

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Fastest appreciation of USD since the global financial crisis … Trade-weighted U.S. dollar

NBF Economics and Strategy (data via Datastream)

9-month % chg.

Mar. 2015

0

1

2

3

4

5

6

7

8

9

10

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

… will hurt those who borrowed in USD Credit denominated in USD to non-banks outside the U.S.

NBF Economics and Strategy (data via Bank of International Settlements)

US$ trillion

TOTAL

Emerging

Euro area

Other advanced UK

40

45

50

55

60

65

70

75

80

85

90

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

China: Share of bank loans back to 2012 levels Share of bank loans in aggregate social financing, 12-month cumulative

NBF Economics and Strategy (data via Datastream)

%

Shadow loans take off

Crackdown on shadow banking starts

The Economy—

09

—

U.S.: Winter blues

It’s déjà vu in the U.S., as a harsh winter again wrecked Q1 economic activity. The poor start of the year forces us to cut our 2015 forecast for GDP growth to 2.9%. That said, fundamentals for domestic demand remain strong, including a consumer that’s being lifted by the best labour market in years. The Fed remains on track to hike interest rates later this year, but don’t expect it to get aggressive when it starts tightening. The strong U.S. dollar is not only hindering exports, but is also making it more difficult for inflation to reach the Fed’s 2% target.

Americans are getting a feeling of déjà vu . Like last year, the world’s largest economy is off to a difficult start, restrained again by awful weather . It was indeed the coldest February in over 80 years, and the deep freeze had a clear negative impact on consumer spending which accounts for nearly 70% of the U .S . economy . Retail weakness was widespread with declining sales in most of the broad categories . Discretionary spending, usually a good gauge of consumer sentiment, saw its worst performance in thirteen months in February . In addition to the frigid temperatures, snowstorms were also a nuisance, as is usually the case at this time of the year in the Northeastern U .S ., except that this time, they even battered the southern parts of the country . Residential construction took a beating as a result, with housing starts plunging in February to the lowest in over a year .

But the moderation in economic activity wasn’t all about Mother Nature . As we had pointed out last month, there was some inventory accumulation in Q4 last year, and that may have reduced the need to produce more, particularly with demand temporarily curtailed by weather . Indeed, growth in industrial production in Q1 is on track to be the worst since the 2009 recession, after February’s below-consensus increase and sharp downward revisions to January output . All in all, the poor start of the year forces us to cut our 2015 forecast for U .S . GDP growth to 2 .9%, from our initial forecast of 3 .3% .

The tepid production in Q1 may also have been a function of diminished trade volumes . On a three-month annualized basis, export volumes are contracting at the fastest pace since the recession . While bad weather may have played a role in disrupting shipments, strikes on West Coast ports were probably the major contributors to those weak trade results . With the strike and bad weather extending for yet another month, February trade volumes could be soft as well . A rebound in exports is likely in March, thanks to a tentative deal in place between management and port labour unions . But considering the U .S . dollar’s surge, we expect a return to tepid export growth, particularly in the second half of the year .

230,000

240,000

250,000

260,000

270,000

280,000

290,000

300,000

310,000

320,000

330,000

340,000

128,000

130,000

132,000

134,000

136,000

138,000

140,000

142,000

2008 2009 2010 2011 2012 2013 2014 201510

12

14

16

18

20

22

24

26

28

30

32

1900 1925 1950 1975 2000

U.S.: February shopping dented by cold snap

*Retail sales excluding excluding gasoline, groceries and health care products

NBF Economics and Strategy (data via NCDC and Datastream)

Non-farm payroll and discretionary spending* Northeast average temperature in February (1895 to 2015)

Jobs (R)

°F

Discretionary spending (L)

Coldest February since 1934…

…may have kept consumers at home

thousands thousands

-25.0-22.5-20.0-17.5-15.0-12.5-10.0-7.5-5.0-2.50.02.55.07.5

10.012.515.0

2009 2010 2011 2012 2013 2014 2015

U.S.: Rough start to 2015 Industrial production

* Assuming no change in March

NBF Economics and Strategy (data via Datastream)

Q1 est.*

q/q % chg. saar

Manufacturing

TOTAL

Worst since the 2009 recession

U.S.: Exporters have struggled lately Real exports of non-petroleum goods

NBF Economics and Strategy (data via Datastream)

-60

-50

-40

-30

-20

-10

0

10

20

30

40

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

3-month annualized change (%)

Jan. 2015

The Economy—

VISIONApril 2015

10

—

In contrast, the expected rebound in domestic demand will be more sustainable . Investment spending should improve as corporations make better use of their record profits to boost productivity which has been declining in recent quarters . That is crucial in some industries like manufacturing, which compete globally and which have been under pressure to adapt to the U .S . dollar’s surge . The investment boost should offset the expected decline in outlays in the energy sector . Consumption spending should also bounce back as warmer temperatures allow Americans to leave the comfort of their homes to go shopping again . Consumer fundamentals are indeed the best they’ve been in years . The labour market is on fire as evidenced by non farm payrolls which have risen nearly 300K/month on average in the last six months, and that is boosting household incomes and confidence . Cheap gasoline should also help . While pump prices rose in February and March, they are still down roughly 30% on a year-on-year basis courtesy of the oil price collapse . Moreover, the personal savings rate, at 5 .5% in January, was the highest since 2013, something that will further help support spending if needed .

The good economic fundamentals do not mean the Fed will aggressively hike interest rates this year . At its March meeting, while it opened the door to rate hikes by removing the word “patient” from its forward guidance, the Fed made clear that it was in no rush to hike . The FOMC said that it will be appropriate to raise rates when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2% objective . In other words, the decision to hike rates is now entirely data dependent . There’s arguably still a lot of room for improvement for both employment and inflation . Note that despite solid job creation in the last few years, wage inflation (which feeds into broader consumer inflation) remains very tame . That may be due to persistent slack in the labour market as evidenced by the wide measure of the unemployment rate — includes marginally attached, and those employed part time for economic reasons — which remains roughly three percentage points above what it was before the recession .

So, while the Fed will likely hike interest rates this year for the first time since 2006, that’s not to say it will do so imminently — an April hike has already been ruled out by the Fed itself . There’s an outside chance of a June hike, but a September move is more likely in our view . Even then, we don’t expect the Fed to get aggressive on rates . While the USD surge wasn’t explicitly mentioned, its impact is apparent in the Fed’s downgrades to both its GDP growth and inflation forecasts . The latter explains perhaps why there are now just four FOMC participants, compared to last December’s nine, expecting rates to be above 1% at the end of the year . Also, there are now as many as eleven participants who see rates remaining below 2% by the end of 2016, versus four last December .

-200-150-100-50

050

100150200250300350400450500550

Jan 10 Jan 11 Jan 12 Jan 13 Jan 14 Jan 15

U.S.: Labour market best in years … Non farm payrolls

NBF Economics and Strategy (data via Datastream)

m/m chg. thousands

6-month average

0.81.01.21.41.61.82.02.22.42.62.83.03.23.43.63.84.0

2007 2008 2009 2010 2011 2012 2013 2014 2015456789

101112131415161718

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

… but Fed will be very cautious when hiking rates

NBF Economics and Strategy (data via Datastream)

NFP hourly earnings and Core PCE deflator Unemployment rate %

U-6 (includes marginally attached, employed part time for economic reasons)

U-3 (conventional measure)

y/y % chg.

Core PCE deflator

Hourly earnings

Labour market slack is larger than what is suggested by conventional

measure of jobless rate …

… and that partly explains the disappointment on

wage growth and inflation

15500

16000

16500

17000

17500

18000

2014Q4 2015Q4 2016Q4 2017Q4 0

1

2

3

4

5

6

7

8

9

10

U.S.: Fed downgrades growth outlook

NBF Economics and Strategy (data via Federal Reserve)

Upper and lower bound projections in December 2014

Central tendency forecasts by the Fed for U.S. real GDP

Number of FOMC participants expecting the fed funds rate to be 1.00% or more at the end of 2015

December 2014 March 2015

Billions of chained (2009) dollars

Upper and lower bound projections in March 2015

The Economy—

11

—

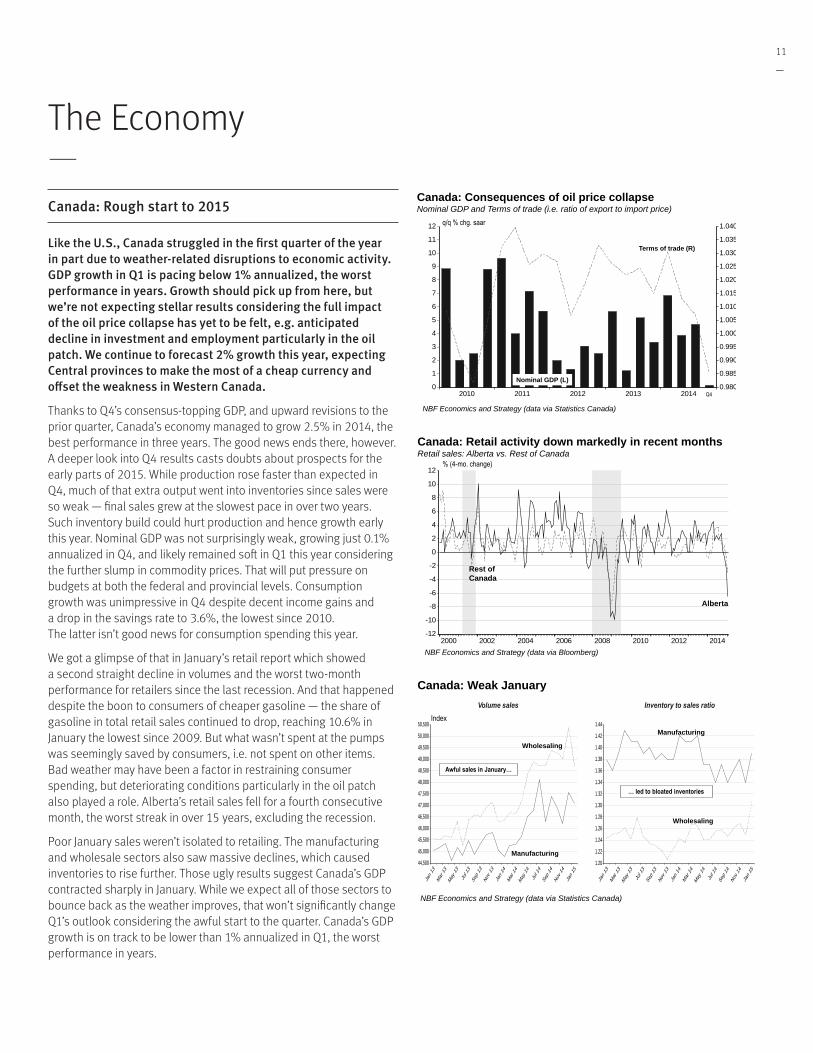

Canada: Rough start to 2015

Like the U.S., Canada struggled in the first quarter of the year in part due to weather-related disruptions to economic activity. GDP growth in Q1 is pacing below 1% annualized, the worst performance in years. Growth should pick up from here, but we’re not expecting stellar results considering the full impact of the oil price collapse has yet to be felt, e.g. anticipated decline in investment and employment particularly in the oil patch. We continue to forecast 2% growth this year, expecting Central provinces to make the most of a cheap currency and offset the weakness in Western Canada.

Thanks to Q4’s consensus-topping GDP, and upward revisions to the prior quarter, Canada’s economy managed to grow 2 .5% in 2014, the best performance in three years . The good news ends there, however . A deeper look into Q4 results casts doubts about prospects for the early parts of 2015 . While production rose faster than expected in Q4, much of that extra output went into inventories since sales were so weak — final sales grew at the slowest pace in over two years . Such inventory build could hurt production and hence growth early this year . Nominal GDP was not surprisingly weak, growing just 0 .1% annualized in Q4, and likely remained soft in Q1 this year considering the further slump in commodity prices . That will put pressure on budgets at both the federal and provincial levels . Consumption growth was unimpressive in Q4 despite decent income gains and a drop in the savings rate to 3 .6%, the lowest since 2010 . The latter isn’t good news for consumption spending this year .

We got a glimpse of that in January’s retail report which showed a second straight decline in volumes and the worst two-month performance for retailers since the last recession . And that happened despite the boon to consumers of cheaper gasoline — the share of gasoline in total retail sales continued to drop, reaching 10 .6% in January the lowest since 2009 . But what wasn’t spent at the pumps was seemingly saved by consumers, i .e . not spent on other items . Bad weather may have been a factor in restraining consumer spending, but deteriorating conditions particularly in the oil patch also played a role . Alberta’s retail sales fell for a fourth consecutive month, the worst streak in over 15 years, excluding the recession .

Poor January sales weren’t isolated to retailing . The manufacturing and wholesale sectors also saw massive declines, which caused inventories to rise further . Those ugly results suggest Canada’s GDP contracted sharply in January . While we expect all of those sectors to bounce back as the weather improves, that won’t significantly change Q1’s outlook considering the awful start to the quarter . Canada’s GDP growth is on track to be lower than 1% annualized in Q1, the worst performance in years .

0

1

2

3

4

5

6

7

8

9

10

11

12

0.980

0.985

0.990

0.995

1.000

1.005

1.010

1.015

1.020

1.025

1.030

1.035

1.040

2010 2011 2012 2013 2014

Canada: Consequences of oil price collapse Nominal GDP and Terms of trade (i.e. ratio of export to import price)

Nominal GDP (L)

Terms of trade (R)

q/q % chg. saar

Q4

NBF Economics and Strategy (data via Statistics Canada)

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

2000 2002 2004 2006 2008 2010 2012 2014

Canada: Retail activity down markedly in recent months Retail sales: Alberta vs. Rest of Canada

NBF Economics and Strategy (data via Bloomberg)

Alberta

% (4-mo. change)

Rest of Canada

44,500

45,000

45,500

46,000

46,500

47,000

47,500

48,000

48,500

49,000

49,500

50,000

50,500

Jan 13

Mar 13

May 13

Jul 13

Sep 13

Nov 13

Jan 14

Mar 14

May 14

Jul 14

Sep 14

Nov 14

Jan 15

1.20

1.22

1.24

1.26

1.28

1.30

1.32

1.34

1.36

1.38

1.40

1.42

1.44

Jan 13

Mar 13

May

13

Jul 1

3

Sep 13

Nov 1

3

Jan 14

Mar 14

May

14

Jul 1

4

Sep 14

Nov 1

4

Jan 15

Canada: Weak January

NBF Economics and Strategy (data via Statistics Canada)

Index Volume sales Inventory to sales ratio

Manufacturing

Wholesaling

Manufacturing

Wholesaling

Awful sales in January…

… led to bloated inventories

The Economy—

VISIONApril 2015

12

—

Softer growth usually translates into a weaker labour market, and this time is no different . The last three months have averaged less than 8K jobs/month, with gains in the public sector and self-employment offsetting sharp declines in the private sector . Alberta and Saskatchewan are starting to feel the pinch of the oil price collapse, with both provinces seeing job losses since the start of the year . Shrinking job opportunities on the oil patch are, not surprisingly, having repercussion on the housing market, particularly in Alberta’s two largest cities . Over the December-February period, Edmonton has seen a 17% drop in sales compared to a similar three-month period a year earlier, while Calgary sales were down a stunning 29% . In sharp contrast, new listings have surged more than 25% in both cities over that period, causing a sudden shift from sellers’ market to buyers’ market in Alberta . Five of the ten provinces are now in buyers’ market territory, while the other five, including Ontario and BC, are still balanced . Can there be contagion from the weak housing markets to the stronger ones? After all, a portion of mortgages in Alberta are non-recourse, i .e . some lenders would bear the brunt of related losses . And if those lenders also service other provinces, they could restrict credit to the latter as they attempt to repair their balance sheets .

But, in our view, odds of such an outcome are quite low . For one, home prices would have to fall more than 20% before households start to think of strategic defaults — only uninsured mortgage loans are non-recourse in Alberta, and such loans usually required a down payment of at least 20%, which borrowers would have to forfeit if they opt to default . And even if they eventually choose to default, the overall impact is likely to be muted considering that only about 5% of the aggregate portfolio of residential mortgage loans of the six largest Canadian chartered banks are non-recourse (for more information, see our special report: “The oil price shock and the Canadian housing market”) . We continue to expect housing strength in Central Canada, buoyed by employment prospects, to offset weakness in the West, leaving home prices roughly flat at the national level .

That, of course, depends on the ability, in Central Canada, of the private sector to offset the expected fiscal drag from provincial governments . We’re reasonably optimistic on that front considering that the much-depreciated Canadian dollar and a strengthening U .S . economy should both help manufacturers boost sales stateside . There’s certainly room for improvement given that non-energy exports are still around 10% below peak levels reached eight years ago . All told, we continue to expect GDP growth of 2% this year, with exports offsetting anticipated weakness in domestic demand, particularly investment spending . Under such a scenario, expect the Bank of Canada to keep monetary policy highly stimulative, more so considering that inflation remains soft .

-10

-8

-6

-4

-2

0

2

4

6

8

10

TOTAL Privatesector

QC AB ON MB NB PE BC NS NL SK

Canada: Private sector employment has been weak Average net employment creation in last three months (i.e. Dec-Feb)

NBF Economics and Strategy (data via Statistics Canada)

Thousands/month

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

CA NL PE NS NB QC ON MB SK AB BC

NBF Economics and Strategy (data from CREA)

Alberta housing now in buyer’s market territory, and

deteriorating fast …

Canada: Housing market still balanced at national level

ratio

Rest of Canada

84.7

Alberta uninsured/non recourse 5.3

Alberta insured 10.0

New-listings-to-sales ratio in February 2015, seasonally adjusted

Residential mortgage loans originated by big 6 banks (%)

… but odds of contagion to the rest of the country are capped somewhat by low share of non-recourse mortgages

Buyers’ market Balanced

Sellers

65

70

75

80

85

90

95

100

105

110

115

120

125

130

2007 2008 2009 2010 2011 2012 2013 2014

Canada: Non-energy export volumes still below 2007 peak Real exports

NBF Economics and Strategy (data via Statistics Canada)

Index=100 in April 2007

Jan. 2015

Energy

Non-energy

TOTAL

The Economy—

13

—

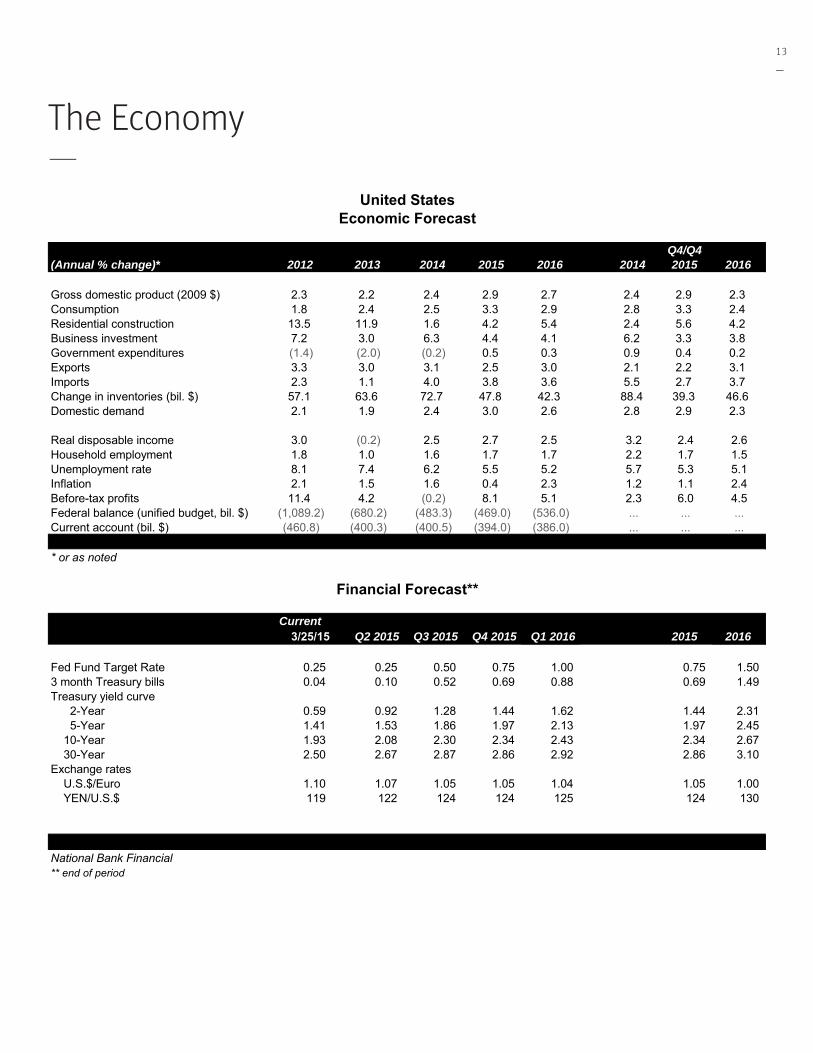

Q4/Q4(Annual % change)* 2012 2013 2014 2015 2016 ### 2014 2015 2016

Gross domestic product (2009 $) 2.3 2.2 2.4 2.9 2.7 2.4 2.9 2.3Consumption 1.8 2.4 2.5 3.3 2.9 2.8 3.3 2.4Residential construction 13.5 11.9 1.6 4.2 5.4 2.4 5.6 4.2Business investment 7.2 3.0 6.3 4.4 4.1 6.2 3.3 3.8Government expenditures (1.4) (2.0) (0.2) 0.5 0.3 0.9 0.4 0.2Exports 3.3 3.0 3.1 2.5 3.0 2.1 2.2 3.1Imports 2.3 1.1 4.0 3.8 3.6 5.5 2.7 3.7Change in inventories (bil. $) 57.1 63.6 72.7 47.8 42.3 88.4 39.3 46.6Domestic demand 2.1 1.9 2.4 3.0 2.6 2.8 2.9 2.3

Real disposable income 3.0 (0.2) 2.5 2.7 2.5 3.2 2.4 2.6Household employment 1.8 1.0 1.6 1.7 1.7 2.2 1.7 1.5Unemployment rate 8.1 7.4 6.2 5.5 5.2 5.7 5.3 5.1Inflation 2.1 1.5 1.6 0.4 2.3 1.2 1.1 2.4Before-tax profits 11.4 4.2 (0.2) 8.1 5.1 2.3 6.0 4.5Federal balance (unified budget, bil. $) (1,089.2) (680.2) (483.3) (469.0) (536.0) ... ... ...Current account (bil. $) (460.8) (400.3) (400.5) (394.0) (386.0) ... ... ...

-304* or as noted

Current Q4 Q4 2015 Q4 20163/25/15 Q2 2015 Q3 2015 Q4 2015 Q1 2016 2015 2016

Fed Fund Target Rate 0.25 0.25 0.50 0.75 1.00 0.75 1.50 3 month Treasury bills 0.04 0.10 0.52 0.69 0.88 0.69 1.49 Treasury yield curve 2-Year 0.59 0.92 1.28 1.44 1.62 1.44 2.31 5-Year 1.41 1.53 1.86 1.97 2.13 1.97 2.45 10-Year 1.93 2.08 2.30 2.34 2.43 2.34 2.67 30-Year 2.50 2.67 2.87 2.86 2.92 2.86 3.10 Exchange rates U.S.$/Euro 1.10 1.07 1.05 1.05 1.04 1.05 1.00 YEN/U.S.$ 119 122 124 124 125 124 130

National Bank Financial** end of period

United StatesEconomic Forecast

Financial Forecast**

The Economy—

VISIONApril 2015

14

—

Q4/Q4(Annual % change)* 2012 2013 2014 2015 2016 2014 2015 2016

Gross domestic product (2007 $) 1.9 2.0 2.5 2.0 2.0 2.6 1.6 1.9Consumption 1.9 2.5 2.8 2.2 2.1 2.6 2.0 1.9Residential construction 5.7 (0.4) 2.8 1.3 (0.1) 5.2 (1.3) 0.0Business investment 9.0 2.6 0.1 (1.7) (0.3) 0.5 (2.2) 0.5Government expenditures 0.2 0.1 (0.1) 0.3 (0.0) 0.6 (0.3) 0.2Exports 2.6 2.0 5.4 5.1 7.0 6.5 6.2 5.7Imports 3.7 1.3 1.7 2.9 3.2 2.6 2.5 3.0Change in inventories (millions $) 7,437 12,368 7,433 6,968 4,094 8,017 4,445 3,226Domestic demand 2.5 1.5 1.6 1.4 1.1 2.0 0.9 1.2

Real disposable income 2.8 2.5 1.5 1.7 1.9 1.2 1.9 1.9Employment 1.3 1.4 0.6 0.8 1.0 0.7 0.7 1.0Unemployment rate 7.3 7.1 6.9 6.8 6.7 6.7 6.8 6.6Inflation 1.5 0.9 1.9 0.7 2.2 1.9 1.3 2.3Before-tax profits (4.2) (0.6) 9.0 (2.0) 4.2 6.7 (0.7) 5.0Current account (bil. $) (59.9) (56.3) (43.5) (52.6) (44.5) .... .... ....

* or as noted

Current Q4 Q4 2015 Q4 20163/25/15 Q2 2015 Q3 2015 Q4 2015 Q1 2016 2015 2016

Overnight rate 0.75 0.75 0.75 0.75 0.75 0.75 1.00 3 month T-Bills 0.54 0.63 0.63 0.63 0.68 0.63 1.02 Treasury yield curve 2-Year 0.51 0.83 0.88 1.00 1.06 1.00 1.80 5-Year 0.77 1.17 1.39 1.54 1.59 1.54 2.02 10-Year 1.34 1.67 1.81 1.89 1.94 1.89 2.20 30-Year 1.98 2.30 2.41 2.47 2.50 2.47 2.67

CAD per USD 1.25 1.25 1.27 1.28 1.28 1.28 1.23 Oil price (WTI), U.S.$ 49 53 55 60 62 60 70

National Bank Financial** end of period

CanadaEconomic Forecast

Financial Forecast**

The Economy—

Interest Rates and Bond Markets—

VISIONApril 2015

16

—

Last call? Not yet!

The FOMC surprised markets with a stance more dovish than expected at its March rate-setting meeting .

Going into the meeting, the market expected the FOMC to drop the word “patient,” and it did . But Fed chair Janet Yellen was quick to calm any fear that rate hikes were coming soon . Early in her press conference – in her sixth sentence – she said: “just because we removed the word ‘patient’ from the statement doesn’t mean we are going to be impatient” (our emphasis) . And she noted more than once that “the modification in the forward guidance should not be read as indicating that the committee has decided on the timing of the initial increase in the target range for the federal funds rate … the decision to raise the target range will depend on our assessment of realized and expected progress toward our objectives of maximum employment and 2 percent inflation .”

Those words turned all eyes to the updated Summary of Economic Projections released by the FOMC . It shows participants’ projections of 2015 economic growth (Q4/Q4) revised down 0 .3 percentage points to a range of 2 .3%-2 .7% . Ms . Yellen said many participants cited a weaker outlook for exports . Participants also saw inflation remaining quite low in 2015 – 0 .6% to 0 .8% .

Having lowered their economic projections, most of the 17 FOMC participants also revised down their path for the fed funds rate, as can be seen in the dot plot of their projections of the midpoint of the appropriate target range for the policy rate at each of the next three year ends:

FOMC participants’ views of appropriate year-end rates

NBF Economics and Strategy (data from Federal Reserve Board)

Many participants now share our January 28 forecast that the appropriate target range for the fed funds rate at year end 2015 would be 0 .50% to 0 .75%, up 50 basis points from the current zero-to-0 .25% target range .

Although the pace of monetary policy normalization looks smoother than was suggested by the previous FOMC dot plot, it is also clear from the Fed’s communications that the U .S . central bank plans to take away the proverbial punch bowl in 2015 . But it has not yet said when it will announce “Last call!” With job creation consistently solid and the unemployment rate low, the decision clearly depends on the inflation clock .

Retail prices

Inflation expectations

Labour costs

Producer prices

Materials and commodities

Money and credit

The Atlanta Fed’s “Inflation Dashboard” Current inflation picture reflecting 30 series grouped in 6 categories

NBF Economics and Strategy (data via Federal Reserve Bank of Atlanta)

Typical

Typical

Typical

Typical

Typical

Typical

For a snapshot of the inflation picture, the Atlanta Fed groups 30 data series into six broad categories . From its resulting Inflation Dashboard, it is clear that the current picture does not call the Fed to action this spring . Of the readings for the six categories, four are rather weak, one is moderately hot and one may be flashing caution .

In the case of labour costs, what is driving the arrow toward the upper end of its typical range is an NFIB Survey that reports a percentage of small businesses raising wages over the past three months that exceeds the 12-month trend . Falling unemployment and low jobless claims are also pushing up the labour cost inflation indicator, while average hourly earnings in private industry are moderating it . If hourly earnings were to accelerate, the FOMC would obviously gain confidence that inflation was heading in the right direction . The high reading of the Money and Credit category is probably more a comfort to the FOMC than a cause for concern . It reflects strength in bank credit and growth in the money supply . These are indications that monetary policy has had traction .

In our outlook, it will be late this summer before the Inflation Dashboard shows enough momentum for the FOMC to feel confident enough about inflation to begin normalizing its policy rate . In the meantime the bond market will remain quite sensitive to the price of crude . A dovish Fed and a new fall of WTI oil below US$50 were enough to push the 10-year Treasury yield from a year-to-date high of 2 .26% on March 6 to 1 .93% at the March 20 close . Moreover, with export growth softening

Interest Rates and Bond Markets—

Paul-André Pinsonnault Senior Fixed Income Economist 514-879-3795

17

—

in response to the strength of the U .S . dollar, the FOMC and market participants will keep an eye on the greenback and its dampening effect on the economy and the inflation outlook .

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

NBF Economics and Strategy (data via Bloomberg) 2015-03-20

U.S. interest rates Weekly observations and quarter-end forecasts

%

U.S. 2-year

U.S. 10-year

Target fed funds – upper bound

Interest rate forecast03/20/15 Q2 Q3 Q4 Q1/16 Q2 Q3 Q4 Q1/17

F.F. - upper bound 0.25 0.25 0.50 0.75 1.00 1.25 1.50 1.50 1.75 2-YR 0.58 0.92 1.28 1.44 1.62 1.76 1.89 2.31 2.46 10-YR 1.93 2.08 2.30 2.34 2.43 2.47 2.57 2.67 2.72Forward 10-yr rate 2.00 2.06 2.11 2.16 2.21 2.25 2.28 2.31

With the Fed no longer committed to patience, but clearly stating that its policy stance will be data-dependent, the sensitivity of the yield curve to economic indicators is likely to step up a notch . We accordingly expect greater market volatility in the months ahead . That said, since the FOMC participants’ view of the appropriate path of the target fed funds rate in 2015 is closely aligned with our own, we are leaving our year-end forecast for 10-year Treasuries unchanged at 2 .34% .

100150200250300350400450500550600

2345678910

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

U.S.: Spread of corporate bonds to Treasuries Yield of Moody’s BAA corporate bond index minus yield of 30-year Treasuries

NBF Economics and Strategy (data via Bloomberg) 2015-03-20

U.S. 30-year

Moody’s BAA

Spread (Left)

Basis points

%

We expect the FOMC to take a gradual approach in normalizing its policy stance, an approach that would over time support economic growth while avoiding a disorderly acceleration of inflation . In this scenario the economic expansion will have legs, favouring a further narrowing of corporate spreads .

... and in Canada

In early March the Bank of Canada kept its target overnight rate unchanged at 0 .75% . To justify this decision the Bank noted that crude prices were close to its assumptions and financial conditions had eased materially . The Canadian dollar had weakened and the yield curve had

shifted down over the year to date . In light of these developments the Bank seemed confident that no further action was justified .

NBF Economics and Strategy (data via Bloomberg) 2015-03-20

Price of crude somewhat lower than projected Bank of Canada MPR assumption was US$60 for Brent

45

50

55

60

65

70

75

80

85

90

95

100

Sep 14 Oct 14 Nov 14 Dec 14 Jan 15 Feb 15 Mar 15

USD/bbl.

Since then the price of oil has moved down somewhat from the Bank’s assumption . At this writing it is trading close to US$55, versus the $60 projected by the Bank . In our view this variance is not large enough to justify another central bank rate cut .

On the currency front, the picture is mixed . Among the currencies of our competitors for market share of U .S . imports, the euro has weakened much more than the Canadian dollar . Against the Mexican peso, however, the loonie now plays on a field that is more level than it was four months ago .

As for interest rates, the Canadian yield curve has shifted down since March 4 .

If the Bank had had to make its rate announcement on March 20, we think it would have left its overnight rate unchanged . But if the next rate announcement were to be preceded by an Ontario budget more austere than expected, the scales could tip in the other direction .

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 321-Year 5 10 20 30 95.097.5100.0102.5105.0107.5110.0112.5115.0117.5120.0122.5125.0127.5130.0

14Q1 14Q2 14Q3 14Q4 15Q1

The USD is up: 23% against the euro 17% against the yen 12% against the CAD 12% against the peso

Jan 2014 = 100

The Canadian yield curve has moved down since March 4

Canadian financial conditions: No grounds for panic

EUR

JPY

CAD

MXN

NBF Economics and Strategy (data via Bloomberg) 2015-03-20

March 20, 2015

March 4, 2015

%

While we recognize that uncertainty about the Canadian monetary policy path is relatively high, we are inclined to think the overnight rate

Interest Rates and Bond Markets—

VISIONApril 2015

18

—

will end the year at 0 .75% . However, our conviction that the Bank of Canada will lag the Fed in rate hikes is much stronger . We continue to see the BoC target rate at 1% in Q4 2016 .

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

NBF Economics and Strategy (data via Bloomberg)

Canadian interest rates Weekly observations and quarter-end forecasts

Canada 10-year

Canada 2-year

BoC overnight target

%

Interest rate forecast03/20/15 Q2 Q3 Q4 Q1/16 Q2 Q3 Q4 Q1/17

Overnight 0.75 0.75 0.75 0.75 0.75 0.75 0.75 1.00 1.25 2-YR 0.45 0.83 0.88 1.00 1.06 1.40 1.59 1.80 1.95 10-YR 1.30 1.67 1.81 1.89 1.94 2.07 2.12 2.20 2.26Forward 10-yr rate 1.35 1.39 1.43 1.47 1.51 1.56 1.61 1.66

Given our expectation of a less-aggressive Bank of Canada, we have revised up our projection for the front end of the yield curve . We expect bonds maturing in 2 years to trade at about 1 .00% at year end, up from 0 .78% in our previous projection . We now see Canada 10-years at 1 .89% in December 2015 and at about 2 .20% a year later . Given our forecast for higher rates along the yield curve, we are reducing the portfolio duration below benchmark .

As we noted last month, the Bank of Canada’s January rate cut gave the domestic search for yield a shot in the arm, supporting narrower provincial spreads . International demand for provincials was also pretty strong, with net purchases of $9 .2 billion in January . Although much of the foreign investment in Canadian bonds was in new instru-ments denominated in foreign currencies, these issues supported domestic spreads by reducing the required volume of domestic issuance .

8486889092949698100102104106108110112

13Q1 13Q2 13Q3 13Q4 14Q1 14Q2 14Q3 14Q4 15Q1

Weighted average spread of long provincials Maturing 2040 to 2042

Basis points

NBF Economics and Strategy (data via Bloomberg) 2015-03-20

-4-3-2-1012345678910

2006 2007 2008 2009 2010 2011 2012 2013 2014

NBF Economics and Strategy (data via Statistics Canada)

Net foreign purchases of provincial bonds C$ billion

–

As a result of lower yields for Canadas, narrower provincial spreads and the relatively long duration of the provincial sub-index, provincial bonds have generated a year-to-date total return of 5 .99%, compared to 3 .65% for Canadas and 2 .26% for Canadian equities .

Interest Rates and Bond Markets—

19

—

Interest Rates and Bond Markets—

Recommended bond allocation Recommended duration 7.27 vs.7.57 for the benchmark Reduce duration below benchmark

Long 31.8%

Short 42.0%

Mid 24.7%

Federal 33.0%

Corporate 32.0%

Provinces 35.0%

Benchmark Allocation

Short 42.0%, Mid 24.7%, Long 33.3% Federal 36.9%, Provinces 34.5%

Corporations 28.6%

Cash 1.5%

0

1

2

3

4

5

6

7

8

9

10

03 04 05 06 07 08 09 10 11 12 13 14 15

U.S. interest rates Last observation March 20, 2015

%

NBF Economics and Strategy (data via Bloomberg)

Long corporate

U.S. 10-year

U.S. 2-year

Target fed funds

30-year mortgage

Canadian Bond Market – Total Returns

NBF Economics and Strategy (data via Datastream)

Total Returns 3/20/2015Since Since Since Since

2/20/2015 12/19/2014 9/19/2014 3/21/2014Cash 0.03 0.27 0.49 0.94

CanadaShort 0.07 1.93 2.92 3.67Mid 0.66 4.79 7.96 10.36Long 2.02 7.45 14.75 19.96Universe 0.65 3.80 6.56 8.57

Provincial 1.20 6.44 11.01 15.16Municipal 0.91 5.39 9.42 13.57

CorporateAA 0.27 2.69 3.81 5.23A 1.31 4.94 7.70 10.71BBB 1.08 4.33 6.66 9.66Universe 0.93 4.09 6.23 8.76

Total 0.91 4.75 7.91 10.76

S&P/TSX -1.24 4.03 -0.67 7.26

0

1

2

3

4

5

6

7

8

03 04 05 06 07 08 09 10 11 12 13 14 15

Canadian interest rates Weekly, last observation March 20, 2015

% Long corporate A

Long provincial

Canada 10-year Canada 2-year

BoC overnight target

NBF Economics and Strategy (data via Bloomberg)

Bond Market - Canada

Close-on 3/20/2015 2/20/2015 12/19/2014 9/19/2014 3/21/2014

Interest Rates 90-day (B/A's) 0.99 0.92 1.29 1.27 1.26 2 years 0.46 0.40 1.01 1.17 1.07 5 years 0.72 0.79 1.37 1.71 1.73 10 years 1.31 1.42 1.81 2.25 2.49 30 years 1.94 2.06 2.34 2.76 2.96 Spreads 90 d - 2 years -54 -52 -28 -10 -19 2 - 5 years 27 39 36 54 66 2 - 10 years 85 102 80 108 141 10 - 30 years 63 64 53 51 47 Currencies CAD / USD 1.2552 1.2531 1.1604 1.0964 1.1221 EUR / CAD 0.7362 0.7010 0.7048 0.7112 0.6458

Source: NBF Economics and Strategy (data via Bloomberg)

This page intentionally left blank .

Stock Market and Portfolio Strategy—

VISIONApril 2015

22

—

Central banks still pro-growth

After a very good performance in February, global equities hit new records in March . The MSCI AC index remains on track for a record 11th consecutive quarterly increase . Although the forward P/E of the MSCI AC is close to its historical average, equities remain an attractive asset class .

80

120

160

200

240

280

320

360

400

440

480

520

1990 1995 2000 2005 2010 2015

World equities: A new record MSCI AC index

NBF Economics and Strategy (data via Bloomberg)

Importantly, the gains remain broad-based across regions and industry groups .

MSCI indexes: Price performance

NBF Economics and Strategy (data via Datastream)

Month to date Quarter to

date Year to date MSCI AC World -0.4 4.6 4.6 MSCI World -0.4 4.7 4.7 MSCI USA -2.0 0.5 0.5 MSCI Canada -2.0 2.3 2.3 MSCI Europe 1.7 11.9 11.9 MSCI Pacific ex Jp 0.3 7.5 7.5 MSCI Japan 4.6 13.2 13.2 MSCI EM -0.5 4.1 4.1 MSCI EM EMEA -2.7 4.3 4.3 MSCI EM Latin America -1.0 0.9 0.9 MSCI EM Asia 0.2 4.8 4.8 3/25/2015

Although the forward P/E of the MSCI AC is close to its historical average, equities remain an attractive asset class .

For one thing, the expansion phase of the U .S . economic cycle is still young (17 months – chart), which helps explain why wage inflation is low .

3.5

3.6

3.7

3.8

3.9

4.0

4.1

4.2

4.3

4.4

4.5

4.6

4.7

4.8

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

U.S.: The expansion phase is still young Contractions, recoveries and expansions based on the coincident economic indicator

19

log. scale

32

25

23

33 68 Shaded area: Contraction and recovery (months) Between the arrows: Expansion (months)

30 61 82 104 50 17

NBF Economics and Strategy (data via Datastream)

For another, the fall of oil and food prices in many parts of the world allows central banks to inject more liquidity and/or to delay the process of normalization toward higher interest rates . As this juncture, we note that the dividend yield of the MSCI AC index is still higher than the yield of global corporate bonds .

1.01.52.02.53.03.54.04.55.05.56.06.57.07.58.08.5

1998 2000 2002 2004 2006 2008 2010 2012 2014

World: Dividend yield remains attractive MSCI AC index dividend yield and global corporate bond yield*

* Effective yield of BofA ML Global Large Cap Corporate Index NBF Economics and Strategy (data via Bloomberg)

index

MSCI AC dividend yield

Global corporate bond yield

Stock Market and Portfolio Strategy—

Matthieu Arseneau Senior Economist 514-879-2252

Stéfane Marion Chief Economist and Strategist 514-879-3781

23

—

We argued last month that future equity gains would depend increasingly on earnings . The developments of recent weeks have not changed our outlook of better days ahead on that front .

The euro zone seems to be recovering, to judge by upticks not just in industrial output but in domestic demand, as labour markets show signs of improving . This is crucial for the transmission of monetary policy: loans to households, while still down from a year earlier, have been rising for two months running . With the European Central Bank still in the early stages of its quantitative easing program, the euro economy (and earnings) could surprise on the upside .

In China, meanwhile, the authorities have announced some growth stimulus . In addition to increasing its budget deficit this year to roughly 1 .6 trillion yuan, or 2 .3% of GDP, Beijing has relaxed borrowing rules for local governments by increasing their quota for bond issues, a move likely to boost infrastructure spending . In addition, low inflation allowed the People’s Bank of China to cut its benchmark interest rate again in March . Altogether, the new stimulus prompts us to raise our growth forecast for China to 6 .8% this year and 7 .1% in 2016 . Both rates are close to Beijing’s newly stated target of 7% .

-100

-80

-60

-40

-20

0

20

40

60

80

14Q1 14Q2 14Q3 14Q4 15Q1-30-25-20-15-10-505

10152025303540

14Q1 14Q2 14Q3 14Q4 15Q1

World: Positive for Eurozone and emerging countries

NBF Economics and Strategy (data via Datastream)

Economic surprise index

Eurozone

U.S.

Recent drop in index for G10 … … largely due to the U.S.

G10

Emerging

Japan

Economic surprise index

A Fed to be feared?

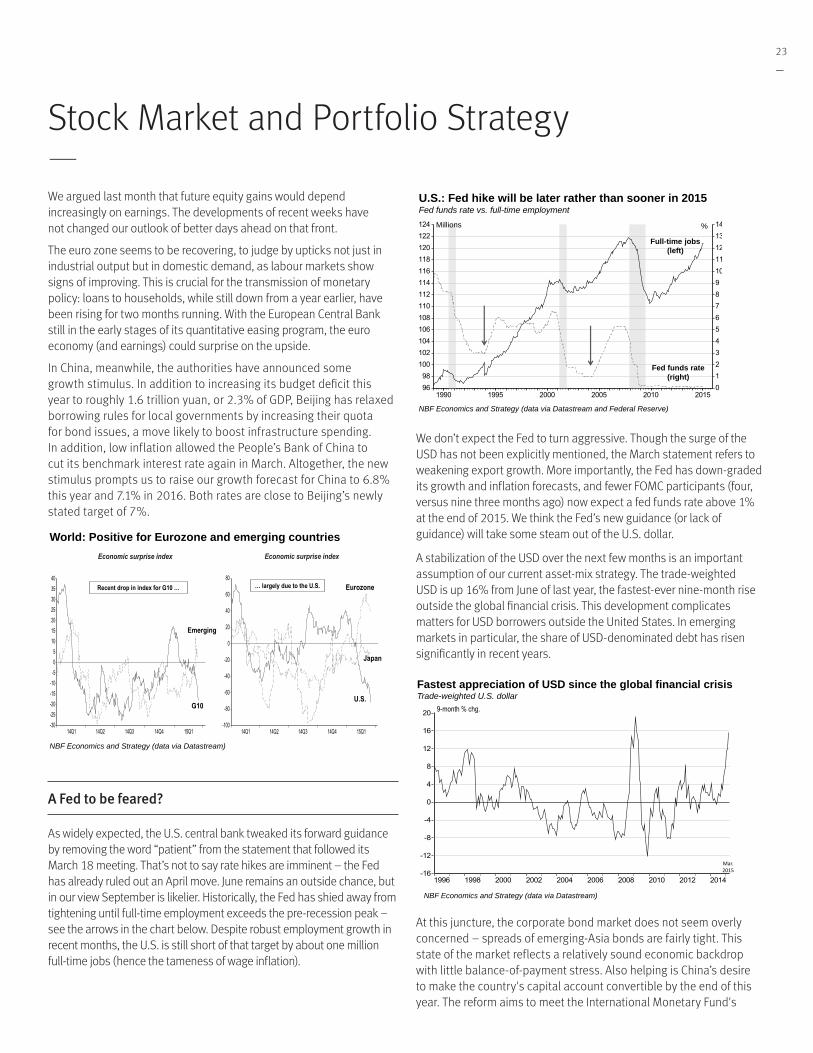

As widely expected, the U .S . central bank tweaked its forward guidance by removing the word “patient” from the statement that followed its March 18 meeting . That’s not to say rate hikes are imminent – the Fed has already ruled out an April move . June remains an outside chance, but in our view September is likelier . Historically, the Fed has shied away from tightening until full-time employment exceeds the pre-recession peak – see the arrows in the chart below . Despite robust employment growth in recent months, the U .S . is still short of that target by about one million full-time jobs (hence the tameness of wage inflation) .

9698

100102104106108110112114116118120122124

01234567891011121314

1990 1995 2000 2005 2010 2015

U.S.: Fed hike will be later rather than sooner in 2015 Fed funds rate vs. full-time employment

NBF Economics and Strategy (data via Datastream and Federal Reserve)

Millions %

Fed funds rate (right)

Full-time jobs (left)

We don’t expect the Fed to turn aggressive . Though the surge of the USD has not been explicitly mentioned, the March statement refers to weakening export growth . More importantly, the Fed has down-graded its growth and inflation forecasts, and fewer FOMC participants (four, versus nine three months ago) now expect a fed funds rate above 1% at the end of 2015 . We think the Fed’s new guidance (or lack of guidance) will take some steam out of the U .S . dollar .

A stabilization of the USD over the next few months is an important assumption of our current asset-mix strategy . The trade-weighted USD is up 16% from June of last year, the fastest-ever nine-month rise outside the global financial crisis . This development complicates matters for USD borrowers outside the United States . In emerging markets in particular, the share of USD-denominated debt has risen significantly in recent years .

-16

-12

-8

-4

0

4

8

12

16

20

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Fastest appreciation of USD since the global financial crisis Trade-weighted U.S. dollar

NBF Economics and Strategy (data via Datastream)

9-month % chg.

Mar. 2015

At this juncture, the corporate bond market does not seem overly concerned – spreads of emerging-Asia bonds are fairly tight . This state of the market reflects a relatively sound economic backdrop with little balance-of-payment stress . Also helping is China’s desire to make the country's capital account convertible by the end of this year . The reform aims to meet the International Monetary Fund's

Stock Market and Portfolio Strategy—

VISIONApril 2015

24

—

(IMF’s) requirements before its evaluation on whether the yuan could be a part of Special Drawing Rights . This means the yuan would join the US dollar, euro, British pound and Japanese yen as part of the supplementary foreign exchange reserve maintained by the IMF .

0

100

200

300

400

500

600

700

800

900

1,000

2000 2002 2004 2006 2008 2010 2012 2014

World: So far so good, but keep an eye on this one Yield spread of emerging-Asia bonds to U.S. Treasuries

NBF Economics and Strategy (data via Federal Reserve)

Basis points

Energy volatility

We argued last month that a tamer USD would tend to put a floor under commodity prices, as the negative correlation between the two asset classes is currently extreme (chart) . Our view has not changed .

-1.0-0.9-0.8-0.7-0.6-0.5-0.4-0.3-0.2-0.10.00.10.20.30.40.5

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

150

1301201101009080

70

60

50

40

30

116

114

112

110

108

106

104

102

100

98

96

94

922006 2007 2008 2009 2010 2011 2012 2013 2014 2015

World: Greenback appreciation has precipitated WTI drop

* Broad dollar index (26 currencies) NBF Economics and Strategy (data via Datastream)

Correlation between monthly changes in the USD* and WTI

USD and the price of oil (WTI)

$/barrel (log scale) 12-month moving correlation

Current

Period average

WTI (left)

USD (right)

Index (log scale)

That said, supply-demand dynamics remain the most important influence on the oil price outlook .

On the demand side, global industrial production is currently on track to expand 4% this year . In the past, that pace of growth has been accompanied by an annual rise in oil demand of at least 1% (chart) .

-10

-8

-6

-4

-2

0

2

4

6

8

10

2002 2004 2006 2008 2010 2012 201428

30

32

34

36

38

40

42

44

46

48

50

52

2002 2004 2006 2008 2010 2012 2014

23% of non-OECD

is China

World: Industrial production and demand for oil Shares of OECD and non-OECD economies

in global oil demand Change in global IP and change in global oil demand

% y/y Milions of BPD Non-

OECD

OECD

Oil demand

IP

NBF Economics and Strategy (data via Eikon)

With the bulk of the increase in oil consumption coming from emerging economies, it is little wonder that the cooling of the Chinese economy has been blamed for the recent fall of oil prices . Yet despite a slowing of industrial production growth, China’s volume imports of crude oil are still expanding at a relatively robust rate of 8% (chart) .

-30

-20

-10

0

10

20

30

40

50

2002 2004 2006 2008 2010 2012 2014

0

5

10

15

20

25

2/1/2006

9/1/2006

4/1/2007

11/1/2007

6/1/2008

1/1/2009

8/1/2009

3/1/2010

10/1/2010

5/1/2011

12/1/2011

7/1/2012

2/1/2013

9/1/2013

4/1/2014

11/1/2014

% y/y %(y/y)

NBF Economics and Strategy (data via Datastream)

China: Slowing yes, but still growing Chinese volume oil imports China industrial output

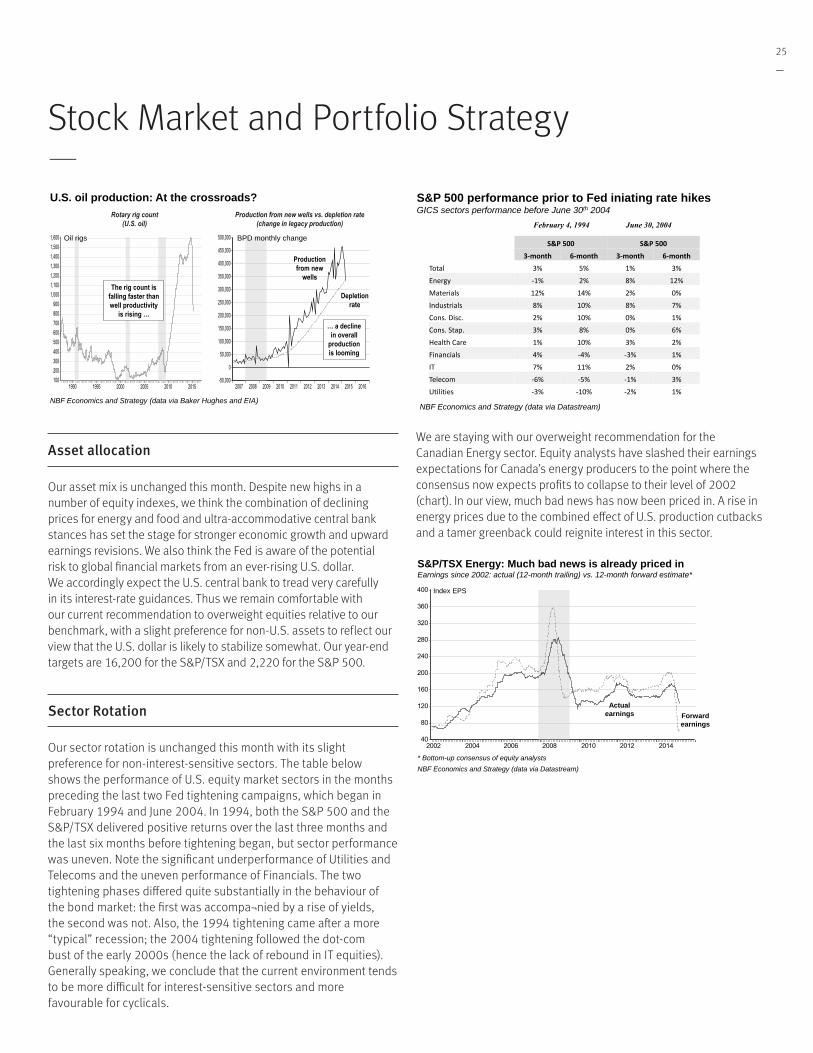

If demand is holding up, then it is supply forces that are more likely to dictate the future direction of prices . Recent data show the number of U .S . oil rigs falling to a new multi-year low of 825 in March . So far, the lower rig count has been more than offset by higher productivity at existing wells, lifting U .S . crude oil production to new highs . A change may be just around the corner . The U .S . department of energy reports that the drop in rig counts is such that production from new wells in April is likely to be, at best, hardly more than the ever-rising depletion rate of existing wells (about 325,000 barrels a day) .

If the energy department is right, it will be the first time in more than four years that U .S . crude production has failed to increase .

Stock Market and Portfolio Strategy—

25

—

100200300400500600700800900

1,0001,1001,2001,3001,4001,5001,600

1990 1995 2000 2005 2010 2015

U.S. oil production: At the crossroads?

NBF Economics and Strategy (data via Baker Hughes and EIA)

Production from new wells vs. depletion rate (change in legacy production)

Oil rigs

-50,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

BPD monthly change

Rotary rig count (U.S. oil)

The rig count is falling faster than well productivity

is rising … … a decline

in overall production is looming

Production from new

wells

Depletion rate

Asset allocation

Our asset mix is unchanged this month . Despite new highs in a number of equity indexes, we think the combination of declining prices for energy and food and ultra-accommodative central bank stances has set the stage for stronger economic growth and upward earnings revisions . We also think the Fed is aware of the potential risk to global financial markets from an ever-rising U .S . dollar . We accordingly expect the U .S . central bank to tread very carefully in its interest-rate guidances . Thus we remain comfortable with our current recommendation to overweight equities relative to our benchmark, with a slight preference for non-U .S . assets to reflect our view that the U .S . dollar is likely to stabilize somewhat . Our year-end targets are 16,200 for the S&P/TSX and 2,220 for the S&P 500 .

Sector Rotation

Our sector rotation is unchanged this month with its slight preference for non-interest-sensitive sectors . The table below shows the performance of U .S . equity market sectors in the months preceding the last two Fed tightening campaigns, which began in February 1994 and June 2004 . In 1994, both the S&P 500 and the S&P/TSX delivered positive returns over the last three months and the last six months before tightening began, but sector performance was uneven . Note the significant underperformance of Utilities and Telecoms and the uneven performance of Financials . The two tightening phases differed quite substantially in the behaviour of the bond market: the first was accompa¬nied by a rise of yields, the second was not . Also, the 1994 tightening came after a more “typical” recession; the 2004 tightening followed the dot-com bust of the early 2000s (hence the lack of rebound in IT equities) . Generally speaking, we conclude that the current environment tends to be more difficult for interest-sensitive sectors and more favourable for cyclicals .

S&P 500 performance prior to Fed iniating rate hikes GICS sectors performance before June 30th 2004

NBF Economics and Strategy (data via Datastream)

S&P 500 S&P 500 3-month 6-month 3-month 6-month Total 3% 5% 1% 3% Energy -1% 2% 8% 12% Materials 12% 14% 2% 0% Industrials 8% 10% 8% 7% Cons. Disc. 2% 10% 0% 1% Cons. Stap. 3% 8% 0% 6% Health Care 1% 10% 3% 2% Financials 4% -4% -3% 1% IT 7% 11% 2% 0% Telecom -6% -5% -1% 3% Utilities -3% -10% -2% 1%

February 4, 1994 June 30, 2004

We are staying with our overweight recommendation for the Canadian Energy sector . Equity analysts have slashed their earnings expectations for Canada’s energy producers to the point where the consensus now expects profits to collapse to their level of 2002 (chart) . In our view, much bad news has now been priced in . A rise in energy prices due to the combined effect of U .S . production cutbacks and a tamer greenback could reignite interest in this sector .

40

80

120

160

200

240

280

320

360

400

2002 2004 2006 2008 2010 2012 2014

S&P/TSX Energy: Much bad news is already priced in Earnings since 2002: actual (12-month trailing) vs. 12-month forward estimate*

Index EPS

Forward earnings

Actual earnings

* Bottom-up consensus of equity analysts NBF Economics and Strategy (data via Datastream)

Stock Market and Portfolio Strategy—

VISIONApril 2015

26

—

Stock Market and Portfolio Strategy—

NBF Fundamental Sector Rotation - April 2015

Name (Sector/Industry) Recommendation S&P/TSX weight

Energy Overweight 21.4%Energy Equipment & Services Overweight 0.8%Oil, Gas & Consumable Fuels Overweight 20.6%

Materials Market Weight 11.0%Chemicals Underweight 3.3%Containers & Packaging Market Weight 0.3%Metals & Mining * Market Weight 2.6%Gold Market Weight 4.5%Paper & Forest Products Overweight 0.5%

Industrials Market Weight 8.4%Capital Goods Overweight 1.6%Commercial & Professional Services Underweight 0.7%Transportation Market Weight 6.1%

Consumer Discretionary Underweight 6.5%Automobiles & Components Underweight 1.7%Consumer Durables & Apparel Overweight 0.6%Consumer Services Underweight 0.8%Media Market Weight 2.2%Retailing Underweight 1.2%

Consumer Staples Underweight 3.8%Food & Staples Retailing Underweight 3.1%Food, Beverage & Tobacco Underweight 0.7%

Health Care Market Weight 4.9%Health Care Equipment & Services Market Weight 0.7%Pharmaceuticals, Biotechnology & Life Sciences Market Weight 4.2%

Financials Market Weight 34.6%Banks Market Weight 21.0%Diversified Financials Market Weight 1.4%Insurance Overweight 7.0%Real Estate Market Weight 5.1%

Information Technology Overweight 2.4%Software & Services Overweight 1.9%Technology Hardware & Equipment Market Weight 0.5%

Telecommunication Services Underweight 4.7%Utilities Underweight 2.2%

* Metals & Mining excluding the Gold Sub-Industry.

27

—

Stock Market and Portfolio Strategy—

-5.

2%

-2.

1%

-0.

9%

2.8%

19

.6%

-150%

-100%

-50%

0%

50%

100%

150%

Q1-99 Q1-00 Q1-01 Q1-02 Q1-03 Q1-04 Q1-05 Q1-06 Q1-07 Q1-08 Q1-09 Q1-10 Q1-11 Q1-12 Q1-13 Q1-14 Q1-15

S&P 500 Quarterly Operating Earnings Growth (YoY)

Realized

n.a.

Actual Q4 2015 (Est.) Actual Q4 2015 (Est.)Index Level Mar-25-15 Target Index Level Mar-25-15 Target S&P/TSX 14,929 16,200 S&P 500 2,061 2,220

Assumptions Q4 2015 (Est.) Assumptions Q4 2015 (Est.) Level: Earnings * 883 900 Level: Earnings * 118 126

Dividend 433 441 Dividend 41 44PE Trailing (implied) 16.9 18.0 PE Trailing (implied) 17.5 17.6

Q4 2015 (Est.) Q4 2015 (Est.) Treasury Bills (91 days) 0.53 0.63 Treasury Bills (91 days) 0.04 0.69 10-year Bond Yield 1.34 1.89 10-year Bond Yield 1.92 2.34* Before extraordinary items, source Thomson * S&P operating earnings, bottom up.NBF Economics and Strategy

NBF Market Forecast NBF Market ForecastCanada United States

VISIONApril 2015

28

—

Stock Market and Portfolio Strategy—

Local Currency (MSCI Indices are in US$) Canadian Dollar Correlation *

Close on with S&P 50003/25/2015 M-T-D Y-T-D 1-Yr 3-Yr Y-T-D 1-Yr 3-Yr

North America - MSCI Index 2118 -2.0% 0.1% 9.5% 43.4% 8.2% 22.6% 79.7% 1.00 United States - S&P 500 2061 -2.1% 0.1% 10.5% 47.5% 8.1% 23.7% 84.9% 1.00 Canada - TSE 300 14929 -2.0% 2.0% 4.4% 19.8% 2.0% 4.4% 19.8% 0.95Europe - MSCI Index 1695 -0.6% 5.4% -3.4% 22.2% 13.9% 8.1% 53.2% 0.86 United Kingdom - FTSE 100 6991 0.6% 6.5% 5.9% 19.4% 10.0% 7.1% 40.7% 0.89 Germany - DAX 30 11865 4.1% 21.0% 27.1% 69.6% 18.7% 13.5% 76.1% 0.95 France - CAC 40 5021 1.4% 17.5% 15.6% 44.4% 15.3% 3.2% 50.0% 0.94 Switzerland - SMI 9188 1.9% 2.3% 10.7% 47.2% 14.6% 14.7% 75.1% 0.94 Italy - Milan Comit 30 246 3.3% 20.3% 12.5% 36.5% 18.0% 0.5% 41.7% 0.93 Netherlands - Amsterdam Exchanges 492 1.6% 15.8% 25.1% 50.7% 13.6% 11.7% 56.5% 0.95Pacific - MSCI Index 2542 3.2% 10.3% 10.9% 21.8% 19.2% 24.2% 52.7% 0.84 Japan - Nikkei 225 19746 5.0% 13.2% 36.9% 97.2% 22.8% 31.4% 70.6% 0.95 Australia - All ordinaries 5937 0.7% 10.2% 11.0% 36.1% 14.3% 6.7% 28.2% 0.92 Hong Kong - Hang Seng 24528 -1.2% 3.9% 12.9% 18.7% 12.3% 26.4% 49.0% 0.79World - MSCI Index 1756 -0.9% 2.7% 6.1% 34.3% 11.0% 18.8% 68.3% 0.98World Ex. U.S.A. - MSCI Index 1896 0.5% 5.9% 0.6% 19.5% 14.4% 12.6% 49.7% 0.87EAFE - MSCI Index 1900 0.7% 7.1% 1.2% 22.1% 15.7% 13.3% 53.0% 0.87Emerging markets (free) - MSCI Index 976 -1.4% 2.1% 1.8% -6.3% 10.3% 14.0% 17.4% 0.25

* Correlation of monthly returns (3 years).

Global Stock Market Performance Summary

Returns Returns

S&P 500 Sectoral Earnings- Consensus*3/25/2015

Weight Index 5 year PEG RevisionS&P 500 Level 3-m D 12-m D 2015 2016 12-m 2015 2016 12-m Growth Ratio Index**

% forward forward Forecast

S&P 500 100 2061 -1.00 10.48 1.29 13.12 4.62 17.69 15.64 17.04 10.41 3.69 -5.72

Energy 8.05 565 -4.89 -12.00 -55.67 45.54 -42.63 29.21 20.07 26.24 0.65 neg. -41.71

Materials 3.15 305 -1.18 2.16 2.64 20.11 7.25 18.09 15.06 17.14 11.14 2.36 -8.78

Industrials 10.35 477 -3.35 6.60 6.26 9.80 7.38 16.81 15.31 16.42 10.51 2.22 -2.76

Consumer Discretionary 12.59 595 4.47 16.18 11.85 14.90 12.98 19.90 17.32 19.11 14.89 1.47 -2.13

Consumer Staples 9.70 500 -1.68 13.97 1.08 9.20 4.12 20.10 18.41 19.49 7.73 4.74 -4.40