Embed Size (px)

Citation preview

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-1

Using Lead and LagMeasures to Communicate,

Motivate, and Evaluate

Student Tutorial

2

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-2

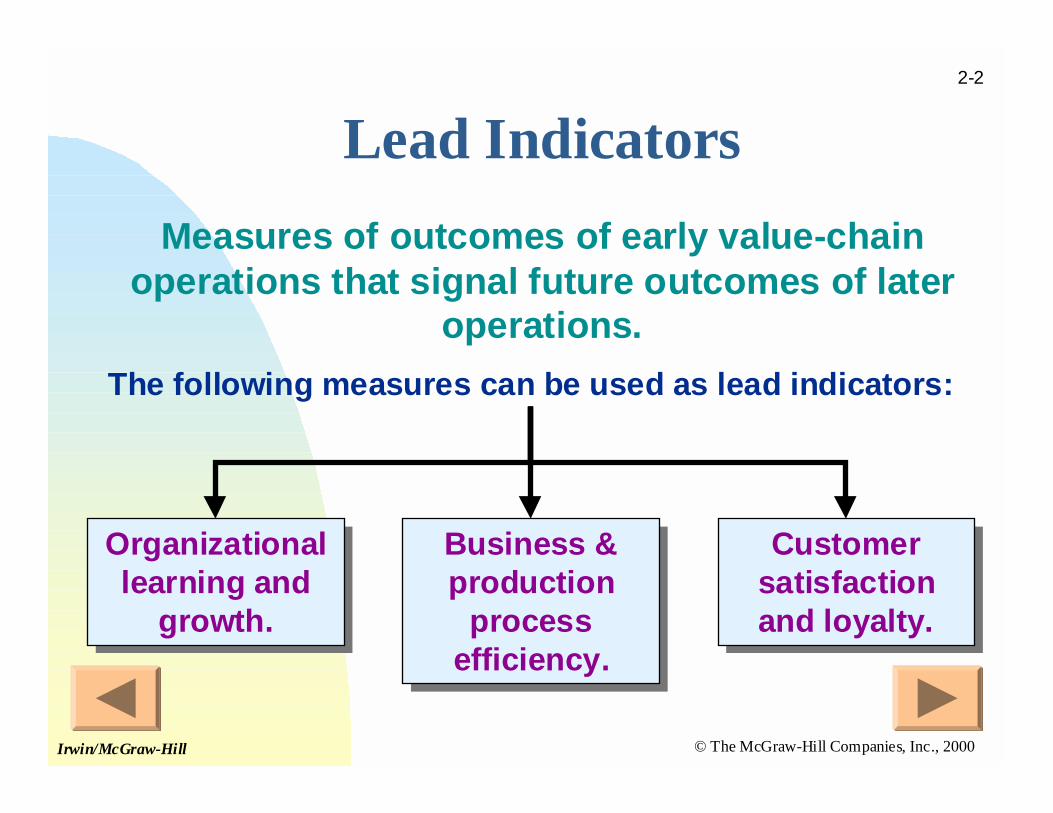

Lead Indicators

Measures of outcomes of early value-chainoperations that signal future outcomes of later

operations.

The following measures can be used as lead indicators:

Business &production

processefficiency.

Business &production

processefficiency.

Organizationallearning and

growth.

Organizationallearning and

growth.

Customersatisfactionand loyalty.

Customersatisfactionand loyalty.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-3

Lead Indicators

Can you think of some examples of leadindicators that you might use in business?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-4

Lead Indicators

Can you think of some examples of leadindicators that you might use in business?

! A decrease in new home starts may indicate afuture decrease in demand for appliances such asrefrigerators or ovens.

! An increase in quality measures, may indicate afuture increase in customer satisfaction.

! News of unrest in the Middle East may foretell anincrease in the price of fuel and petroleum-basedproducts.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-5

Lag Indicators

Measures of final outcomes of managementplans and their execution.

Measures of final outcomes of managementplans and their execution.

Lead and Lag relations among Indicators ofPerformance:

Business &productionprocesses

Business &productionprocesses

Customervalue

Customervalue

Organizationallearning and

growth

Organizationallearning and

growth

Financialperformance

Financialperformance

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-6

Lag Indicators

Can you think of some examples of lagindicators that you might use in business?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-7

Lag Indicators

Can you think of some examples of lagindicators that you might use in business?

! Improved employee morale might indicate that arecent employee seminar was successful.

! Increased productivity might be a signal that arecent training course was successful.

! Improved quality can be a sign that using a highergrade material reduces defects.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-8

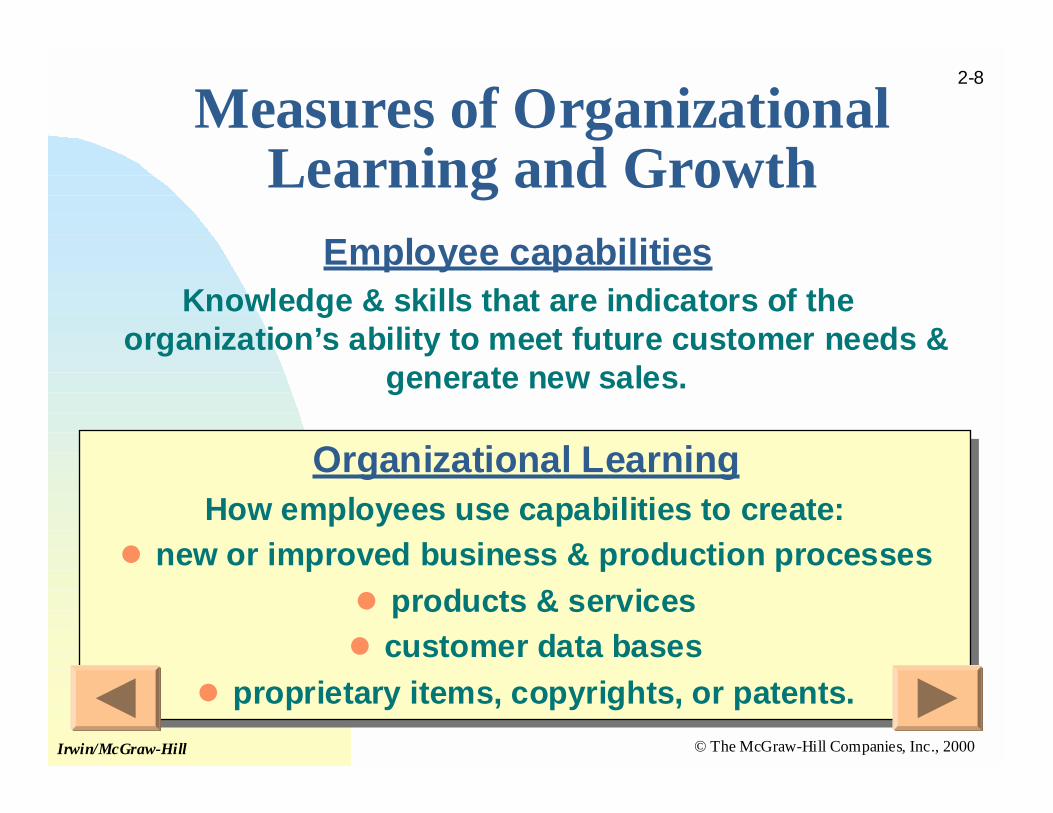

Measures of OrganizationalLearning and Growth

Employee capabilitiesKnowledge & skills that are indicators of the

organization’s ability to meet future customer needs &generate new sales.

Organizational LearningHow employees use capabilities to create:

! new or improved business & production processes

! products & services

! customer data bases

! proprietary items, copyrights, or patents.

Organizational LearningHow employees use capabilities to create:

! new or improved business & production processes

! products & services

! customer data bases

! proprietary items, copyrights, or patents.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-9

Opportunitiesfor

improvement

Opportunitiesfor

improvement

Productdevelopment

time.

Productdevelopment

time.

Employee training& education

Employee training& education

InnovativenessInnovativeness

Measures of OrganizationalLearning and Growth

Measuresinclude:

Measuresinclude:

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-10

Measuring Results: ProcessEfficiency

Process efficiency! The ability to transform inputs into

outputs at lowest cost.

Process efficiency! The ability to transform inputs into

outputs at lowest cost.

Production processes! Result directly in the production of

products or services provided to externalcustomers.

Production processes! Result directly in the production of

products or services provided to externalcustomers.

Business process! Support or enable production processes.

Business process! Support or enable production processes.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-11

Measuring Results: ProcessEfficiency

Highproductivity

Highproductivity

HighqualityHigh

quality

Low cycletime

Low cycletime

Highthroughput

Highthroughput

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-12

Measuring Quality

Internal Customers

(Click for definition)

Internal Customers

(Click for definition)

External Customers

(Click for definition)

External Customers

(Click for definition)

If internal customersare satisfied,

profitability of theproduction process is

maximized.

If internal customersare satisfied,

profitability of theproduction process is

maximized.

If internal customersare NOT satisfied,

external customerscannot be profitably

satisfied.

If internal customersare NOT satisfied,

external customerscannot be profitably

satisfied.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-13

Measuring Quality

External Customers

(Click for definition)organization.

External Customers

(Click for definition)organization.

If internal customersare satisfied,

profitability of theproduction process is

maximized.

If internal customersare satisfied,

profitability of theproduction process is

maximized.

If internal customersare NOT satisfied,

external customerscannot be profitably

satisfied.

If internal customersare NOT satisfied,

external customerscannot be profitably

satisfied.

Internal CustomersEmployees involved inthe next “downstream”process.

Internal CustomersEmployees involved inthe next “downstream”process.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-14

Measuring Quality

Internal Customers

(Click for definition)

Internal Customers

(Click for definition)

External CustomersUltimate users ofproducts and servicesthat generate profits forthe organization.

External CustomersUltimate users ofproducts and servicesthat generate profits forthe organization.

If internal customersare satisfied,

profitability of theproduction process is

maximized.

If internal customersare satisfied,

profitability of theproduction process is

maximized.

If internal customersare NOT satisfied,

external customerscannot be profitably

satisfied.

If internal customersare NOT satisfied,

external customerscannot be profitably

satisfied.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-15

Measuring Quality

Internal CustomersEmployees involved inthe next “downstream”process.

Internal CustomersEmployees involved inthe next “downstream”process.

External CustomersUltimate users ofproducts and servicesthat generate profits forthe organization.

External CustomersUltimate users ofproducts and servicesthat generate profits forthe organization.

If internal customersare satisfied,

profitability of theproduction process is

maximized.

If internal customersare satisfied,

profitability of theproduction process is

maximized.

If internal customersare NOT satisfied,

external customerscannot be profitably

satisfied.

If internal customersare NOT satisfied,

external customerscannot be profitably

satisfied.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-16

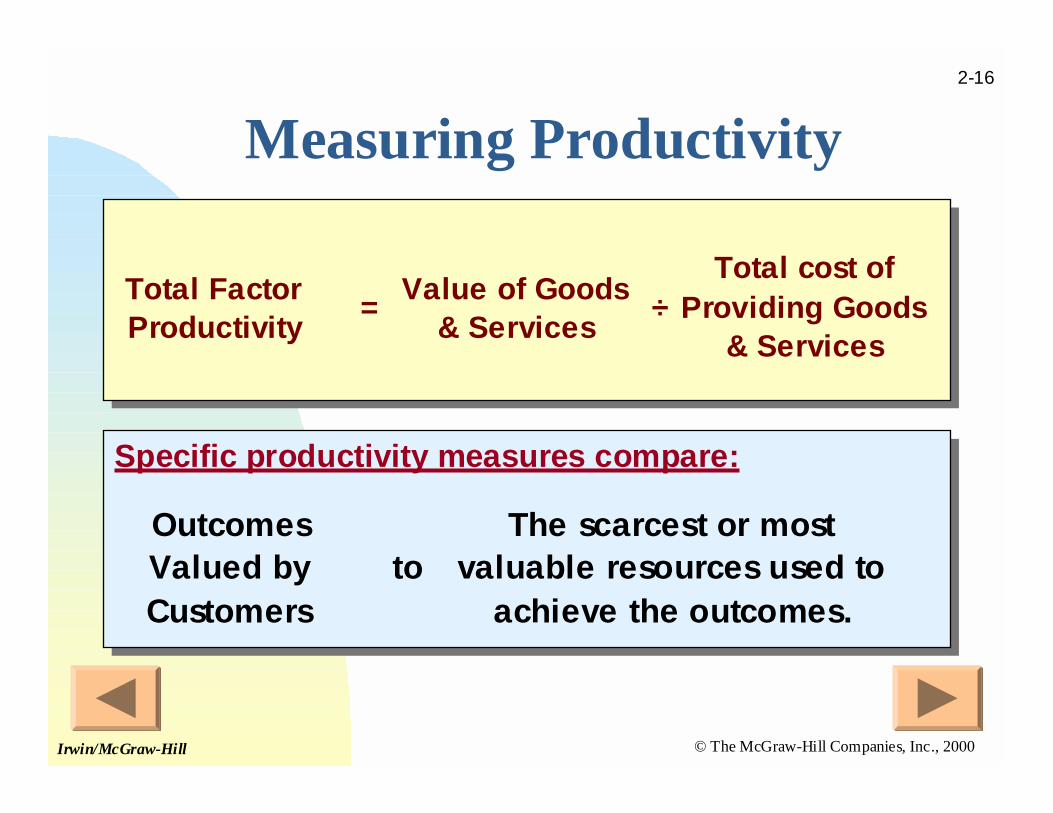

Measuring Productivity

Total Factor Productivity

=Value of Goods

& Services÷

Total cost of Providing Goods

& Services

Specific productivity measures compare:Specific productivity measures compare:

Outcomes Valued by Customers

toThe scarcest or most

valuable resources used to achieve the outcomes.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-17

Measuring Productivity

?

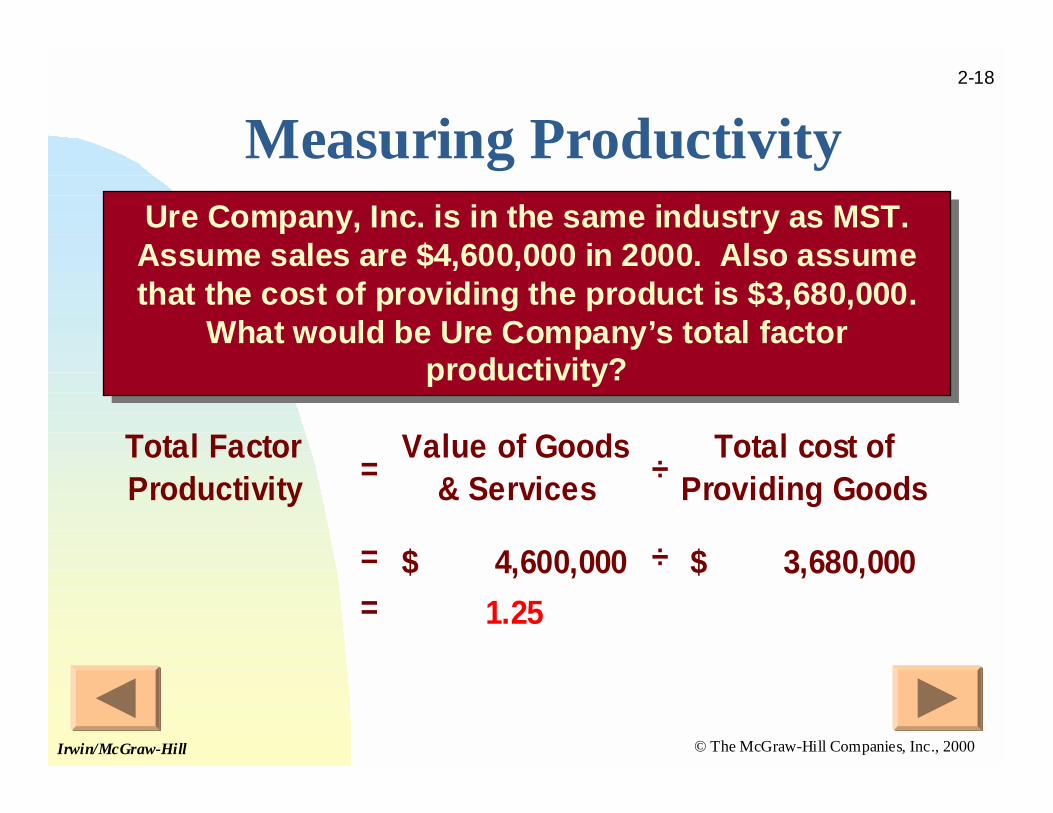

Ure Company, Inc. is in the same industry as MST.Assume sales are $4,600,000 in 2000. Also assumethat the cost of providing the product is $3,680,000.

What would be Ure Company’s total factorproductivity?

Ure Company, Inc. is in the same industry as MST.Assume sales are $4,600,000 in 2000. Also assumethat the cost of providing the product is $3,680,000.

What would be Ure Company’s total factorproductivity?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-18

Measuring ProductivityUre Company, Inc. is in the same industry as MST.Assume sales are $4,600,000 in 2000. Also assumethat the cost of providing the product is $3,680,000.

What would be Ure Company’s total factorproductivity?

Ure Company, Inc. is in the same industry as MST.Assume sales are $4,600,000 in 2000. Also assumethat the cost of providing the product is $3,680,000.

What would be Ure Company’s total factorproductivity?

Total Factor Productivity

=Value of Goods

& Services÷

Total cost of Providing Goods

= 4,600,000$ ÷ 3,680,000$ = 1.25

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-19

Measuring ThroughputEfficiency

A measure of the amount of time spent addingvalue compared to the total cycle time.

A measure of the amount of time spent addingvalue compared to the total cycle time.

Throughput Ratio

=Value-added

Time÷

Total Processing

Time

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-20

Preventing Process Mistakes

" It is easier andless costly to

prevent mistakesthan to fix them.

" It is easier andless costly to

prevent mistakesthan to fix them.

# When mistakes dooccur, lead indicatorscan identify problems

before they become tooserious.

# When mistakes dooccur, lead indicatorscan identify problems

before they become tooserious.

Six-Sigma Programs, such as atMotorola, are designed to resultin nearly error-free production

processes.

Six-Sigma Programs, such as atMotorola, are designed to resultin nearly error-free production

processes.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-21

Preventing Process Mistakes

" It is easier andless costly to

prevent mistakesthan to fix them.

" It is easier andless costly to

prevent mistakesthan to fix them.

# When mistakes dooccur, lead indicatorscan identify problems

before they become tooserious.

# When mistakes dooccur, lead indicatorscan identify problems

before they become tooserious.

Six-Sigma Programs, such as atMotorola, are designed to resultin nearly error-free production

processes.

Six-Sigma Programs, such as atMotorola, are designed to resultin nearly error-free production

processes.

Six Sigma refers to a process thathas a 99.9999998% probability of

being error free. The concept wasoriginally implemented by

Motorola. Typically, Six Sigmaprocesses result in an average of

only 3.4 production defects forevery 1,000,000 units produced.

Six Sigma refers to a process thathas a 99.9999998% probability of

being error free. The concept wasoriginally implemented by

Motorola. Typically, Six Sigmaprocesses result in an average of

only 3.4 production defects forevery 1,000,000 units produced.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-22

Measuring Customer Satisfaction

Customer Satisfaction is the degree to which productsand services meet customers’ needs.

Customer Satisfaction is the degree to which productsand services meet customers’ needs.

Attributes ofcustomer

satisfactioninclude:

•Meeting customer needs.

•Meeting technical requirements.

•Delivering superior service before and afterthe sale.

•A commitment to work with the customer.

•Flexible, competent, and helpful employees.

•Company’s reliability and ability to meetcommitments.

•Meeting customer needs.

•Meeting technical requirements.

•Delivering superior service before and afterthe sale.

•A commitment to work with the customer.

•Flexible, competent, and helpful employees.

•Company’s reliability and ability to meetcommitments.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-23

Measuring Customer Loyalty

Customer Loyalty is the tendency for existingcustomers to continue to obtain products and

services from the same organization.

Customer Loyalty is the tendency for existingcustomers to continue to obtain products and

services from the same organization.

Customerretention rate

Customerretention rate

% of sales torepeat

customers

% of sales torepeat

customers

Measuresinclude:

Measuresinclude:

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-24

Target Costing for ProductDesign

An approach for designing products to simultaneouslymeet both customer needs and company profit targets.

An approach for designing products to simultaneouslymeet both customer needs and company profit targets.

"Computetarget price.

"Computetarget price.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-25

Target Costing for ProductDesign

An approach for designing products to simultaneouslymeet both customer needs and company profit targets.

An approach for designing products to simultaneouslymeet both customer needs and company profit targets.

"Computetarget price.

"Computetarget price.

#Computetarget costper unit.

#Computetarget costper unit.

Target Cost per Unit

=Expected market price over the life

of the product -

Required profit per unit

Target Cost per Unit

=Expected market price over the life

of the product -

Required profit per unit

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-26

Target Costing for ProductDesign

An approach for designing products to simultaneouslymeet both customer needs and company profit targets.

An approach for designing products to simultaneouslymeet both customer needs and company profit targets.

"Computetarget price.

"Computetarget price.

#Computetarget costper unit.

#Computetarget costper unit.

$Compute thecurrently feasibletotal cost.

$Compute thecurrently feasibletotal cost.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-27

Target Costing for ProductDesign

An approach for designing products to simultaneouslymeet both customer needs and company profit targets.

An approach for designing products to simultaneouslymeet both customer needs and company profit targets.

"Computetarget price.

"Computetarget price.

#Computetarget costper unit.

#Computetarget costper unit.

$Compute thecurrently feasibletotal cost.

$Compute thecurrently feasibletotal cost.

%Compare totaltarget cost tocurrently feasibletotal cost.

%Compare totaltarget cost tocurrently feasibletotal cost.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-28

Target Costing for ProductDesign - Example

Dig Corp. produces titanium shovels. These shovelsdig easier and last longer than traditional steel

shovels. Dig Corp. currently sells 75,000 shovels peryear at a sales price of $125 each. However,

competing products set to hit the market in 6 weekswill drive prices immediately to a unit sales price of

only $70 per shovel.

Dig Corp. must maintain a 30% profit margin. With thenew sales price of $70, they expect sales to increase

to 105,000 shovels per year. The current variable costis $52 per shovel. Fixed costs are $1,200,000.

What is Dig’s cost reduction target?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-29

Target Costing for ProductDesign - Example

"Computetarget price

= ?

"Computetarget price

= ?

In this problem, thisis given. Usually thetarget price must beestimated by carefulstudy of prevailing

and expectedeconomic and

market conditions.

In this problem, thisis given. Usually thetarget price must beestimated by carefulstudy of prevailing

and expectedeconomic and

market conditions.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-30

Target Costing for ProductDesign - Example

"Computetarget price

= $70

"Computetarget price

= $70

In this problem, thisis given. Usually thetarget price must beestimated by carefulstudy of prevailing

and expectedeconomic and

market conditions.

In this problem, thisis given. Usually thetarget price must beestimated by carefulstudy of prevailing

and expectedeconomic and

market conditions.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-31

Target Costing for ProductDesign - Example

#Computetarget costper unit = ?

#Computetarget costper unit = ?

"Computetarget price

= $70

"Computetarget price

= $70

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-32

Target Costing for ProductDesign - Example

Target Cost per Unit

= $70 - ( $ 70 × 30% )

= 49$

Target Cost per Unit

= $70 - ( $ 70 × 30% )

= 49$

#Computetarget cost

per unit = $49

#Computetarget cost

per unit = $49

"Computetarget price

= $70

"Computetarget price

= $70

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-33

Target Costing for ProductDesign - Example

$Compute thecurrently feasibletotal cost.

$Compute thecurrently feasibletotal cost.

"Computetarget price

= $70

"Computetarget price

= $70

#Computetarget cost

per unit = $49

#Computetarget cost

per unit = $49

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-34

Target Costing for ProductDesign - Example

$Compute thecurrently feasibletotal cost.

$Compute thecurrently feasibletotal cost.

Currently Feasible

Cost = ( VC × Est. Sales ) + FC

= ( $52 × 105,000 ) + $1,200,000 = $6,660,000

"Computetarget price

= $70

"Computetarget price

= $70

#Computetarget cost

per unit = $49

#Computetarget cost

per unit = $49

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-35

Target Costing for ProductDesign - Example

$Compute thecurrently feasibletotal cost.

$Compute thecurrently feasibletotal cost.

"Computetarget price

= $70

"Computetarget price

= $70

#Computetarget cost

per unit = $49

#Computetarget cost

per unit = $49

%Compare total target costto currently feasible totalcost = $?

%Compare total target costto currently feasible totalcost = $?

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-36

Target Costing for ProductDesign - Example

$Compute thecurrently feasibletotal cost.

$Compute thecurrently feasibletotal cost.

"Computetarget price

= $70

"Computetarget price

= $70

#Computetarget cost

per unit = $49

#Computetarget cost

per unit = $49

%Compare total target costto currently feasible totalcost = $1,515,000

%Compare total target costto currently feasible totalcost = $1,515,000

Cost Reduction

Target =

Currently Feasible

Cost - (

Target Unit Cost

× Est. Sales )

= $6,660,000 - ( $49.00 × 105,000 ) = $1,515,000

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-37

Balanced Scorecard

A cause-and-effect model of lead and lag indicators ofperformance that demonstrates how changes in one

operation cause or are balanced by changes in others.

A cause-and-effect model of lead and lag indicators ofperformance that demonstrates how changes in one

operation cause or are balanced by changes in others.

Four majorareas of

performance

"Learning and growth.

#Business and productionprocess efficiency.

$Customer value.

%Financial performance.

"Learning and growth.

#Business and productionprocess efficiency.

$Customer value.

%Financial performance.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-38

Avg. employeeeducation level

Avg. employeeeducation level

Hours of job-related training.

Hours of job-related training.

% of defectiveproducts

% of defectiveproducts

Process cycletime

Process cycletime

Retention ofexisting customers

Retention ofexisting customers

% of on-timedeliveries

% of on-timedeliveries

Return on SalesReturn on Sales

Measures of performance

Learning & growth

Business &production process

efficiency

Customer value

Final performance

Dimensions of performance

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-39

Quantifying the CausalRelationships

A mathematical model that allows managers toestimate the effects on profitability from changes in

activities.

A mathematical model that allows managers toestimate the effects on profitability from changes in

activities.

The basicrelationship model

is:

δδδδY = b(δδδδX)

The basicrelationship model

is:

δδδδY = b(δδδδX)

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-40

Quantifying the CausalRelationships

A mathematical model that allows managers toestimate the effects on profitability from changes in

activities.

A mathematical model that allows managers toestimate the effects on profitability from changes in

activities.

Weightings (b) areassigned to eachrelationship in thecausal BalancedScorecard Model.

The basicrelationship model

is:

δδδδY = b(δδδδX)

The basicrelationship model

is:

δδδδY = b(δδδδX)

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-41

Balanced Scorecard - ExampleBennett Industries realizes that

a simple 1% increase in on-time deliveries will lead to a

.8% increase in customersatisfaction. A 1% increase incustomer satisfaction will lead

to a .3% increase in sales.If on-time delivery

improves by 5%, what willbe the effect on sales?

Bennett Industries realizes thata simple 1% increase in on-time deliveries will lead to a

.8% increase in customersatisfaction. A 1% increase incustomer satisfaction will lead

to a .3% increase in sales.If on-time delivery

improves by 5%, what willbe the effect on sales?

Retention ofexisting customers

Retention ofexisting customers

% of on-timedeliveries

% of on-timedeliveries

Sales RevenuesSales Revenues

+ .8 %

+.3 %

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-42

Balanced Scorecard - ExampleIf on-time delivery

improves by 5%, what willbe the effect on sales?A 5% increase in on-timedelivery results in a 4%

increase in customer retention.This will lead, in turn, to a 1.2%

increase in sales revenues!

If on-time deliveryimproves by 5%, what will

be the effect on sales?A 5% increase in on-timedelivery results in a 4%

increase in customer retention.This will lead, in turn, to a 1.2%

increase in sales revenues!

Retention ofexisting customers

Retention ofexisting customers

% of on-timedeliveries

% of on-timedeliveries

Sales RevenuesSales Revenues

+ .8 %

+.3 %

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

2-43

End of Chapter 2

I alwaysbalance myscorecards

before anyoneelse sees them!