Embed Size (px)

Citation preview

Using Data StandardseXtensible Business Reporting

Language - XBRL Overview Grant Boyd, CA - Associate – Booz Allen Hamilton

2

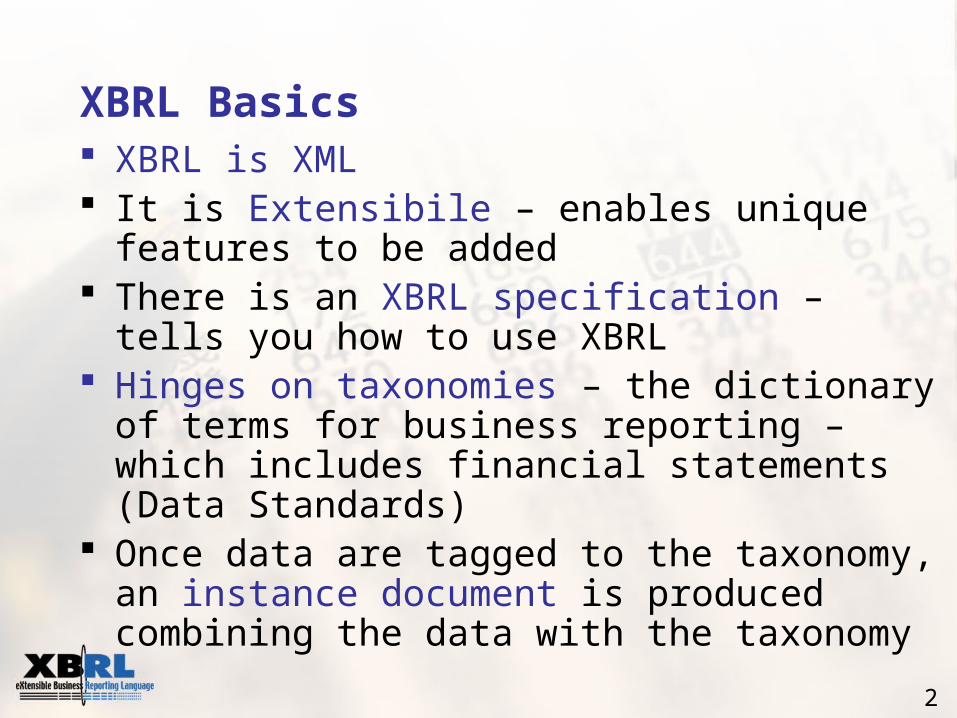

XBRL Basics XBRL is XML It is Extensibile – enables unique features to be

added There is an XBRL specification – tells you how to

use XBRL Hinges on taxonomies – the dictionary of terms

for business reporting – which includes financial statements (Data Standards)

Once data are tagged to the taxonomy, an instance document is produced combining the data with the taxonomy

3

Validation

Standardization

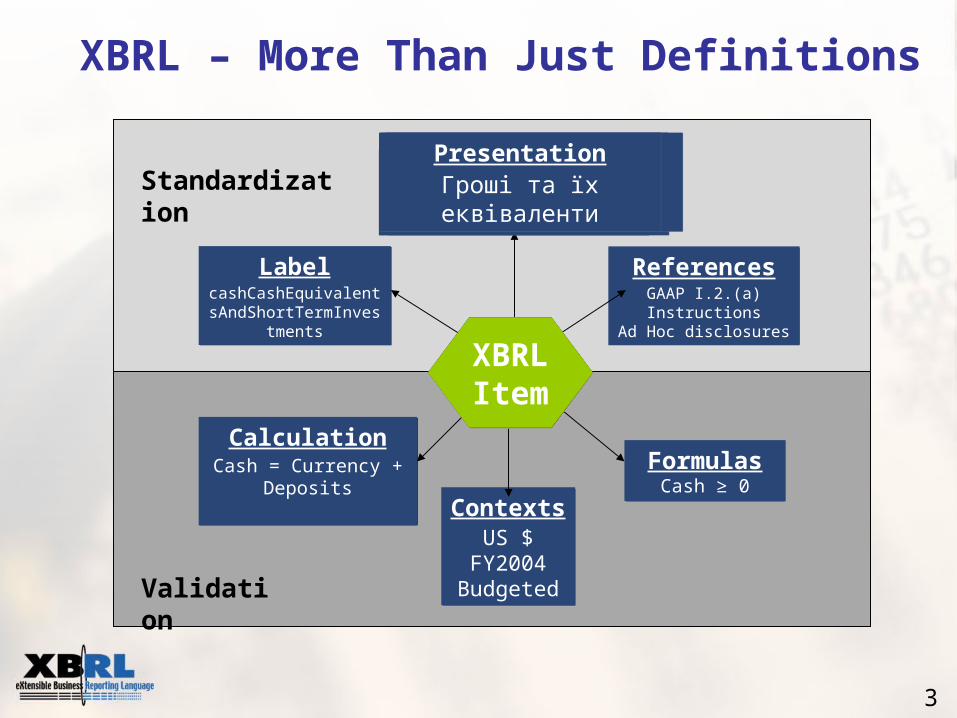

XBRL – More Than Just Definitions

CalculationCash = Currency +

Deposits

CalculationCash = Currency +

DepositsFormulas

Cash ≥ 0Formulas

Cash ≥ 0Contexts

US $FY2004

Budgeted

ContextsUS $

FY2004Budgeted

LabelcashCashEquivalentsAndShortTermInvestment

s

LabelcashCashEquivalentsAndShortTermInvestment

s

ReferencesGAAP I.2.(a)Instructions

Ad Hoc disclosures

ReferencesGAAP I.2.(a)Instructions

Ad Hoc disclosures

PresentationCash & Cash Equivalents

PresentationCash & Cash Equivalents

XBRLItem

XBRLItemXMLItemXMLItem

XBRLItem

XBRLItem

PresentationComptant et Comptant

Equivalents

PresentationComptant et Comptant

Equivalents

PresentationGeld & Geld nahe Mittel

PresentationGeld & Geld nahe Mittel

PresentationKas en Geldmiddelen

PresentationKas en Geldmiddelen

Presentation现金与现金等价物

Presentation现金与现金等价物

Presentation現金及び現金等価物

Presentation現金及び現金等価物

PresentationДеньги и их эквиваленты

PresentationДеньги и их эквиваленты

PresentationГроші та їх еквіваленти

PresentationГроші та їх еквіваленти

4

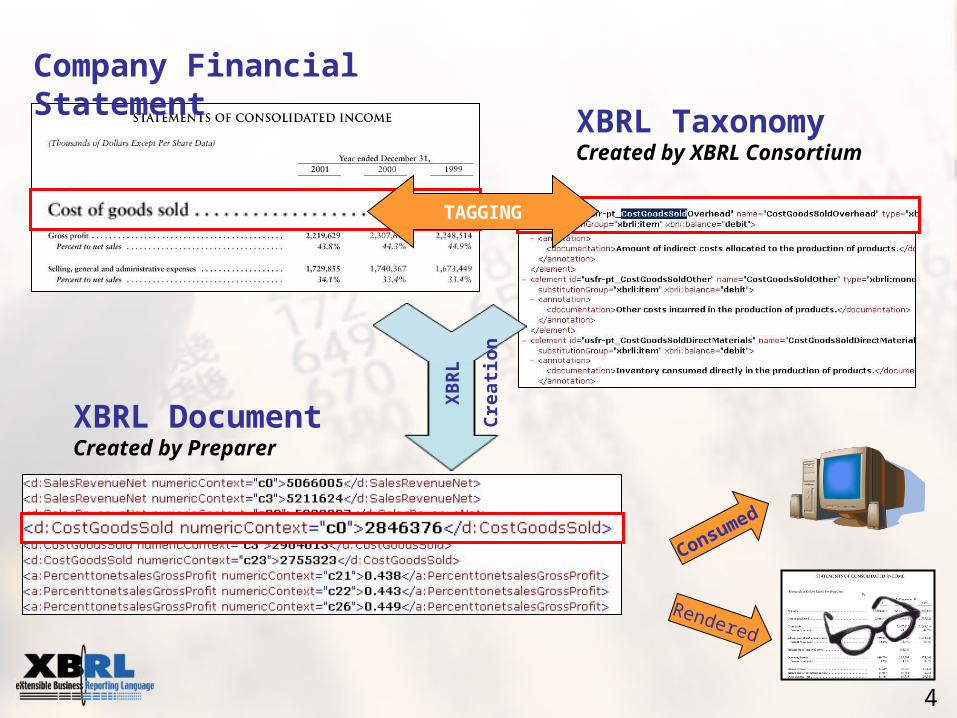

XBRL TaxonomyCreated by XBRL Consortium

Consumed

Rendered

XB

RL

Cre

ati

on

XBRL DocumentCreated by Preparer

Company Financial Statement

TAGGING

5

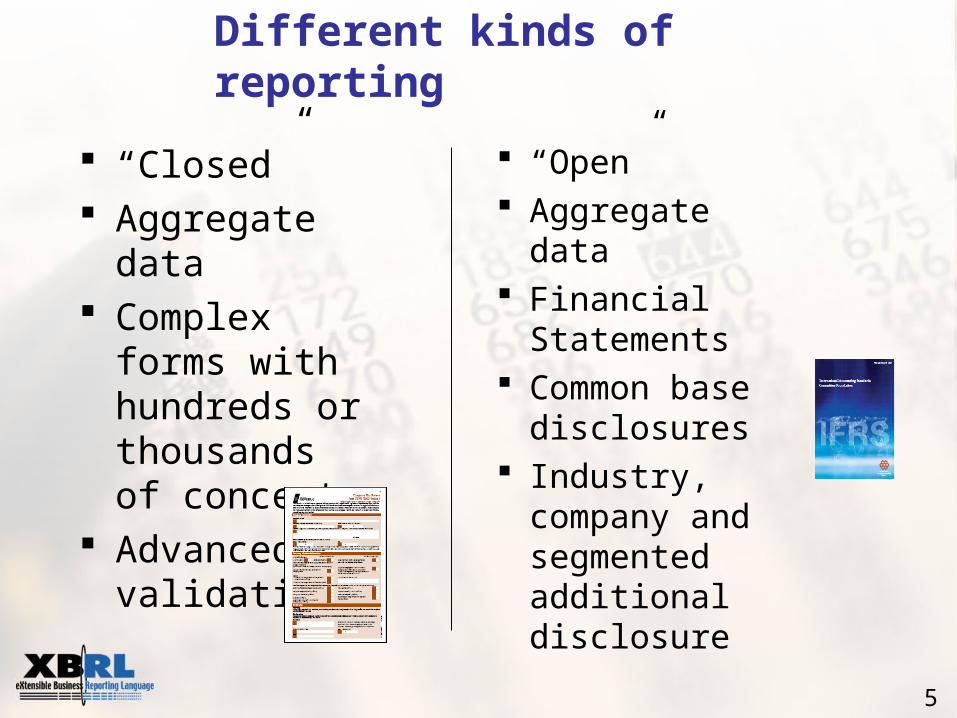

Different kinds of reporting

“Closed” Aggregate data Complex forms

with hundreds or thousands of concepts

Advanced validation

“Open” Aggregate data Financial

Statements Common base

disclosures Industry,

company and segmented additional disclosure

6

XBRL GL and FR

7

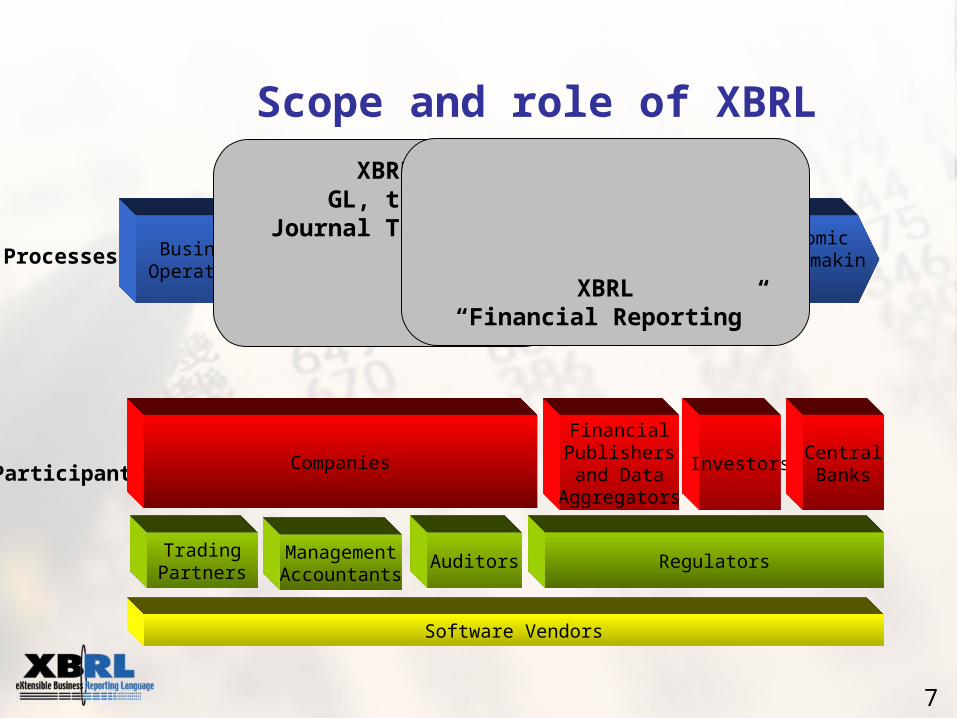

Scope and role of XBRL

ExternalBusinessReporting

BusinessOperations

InternalBusinessReporting

Investment,Lending,

RegulationProcesses

Participants

AuditorsTradingPartners

Investors

FinancialPublishersand Data

Aggregators

Regulators

Software Vendors

ManagementAccountants

Companies

Economic Policymaking

CentralBanks

XBRLGL, the

Journal Taxonomy

XBRL“Financial Reporting”

8

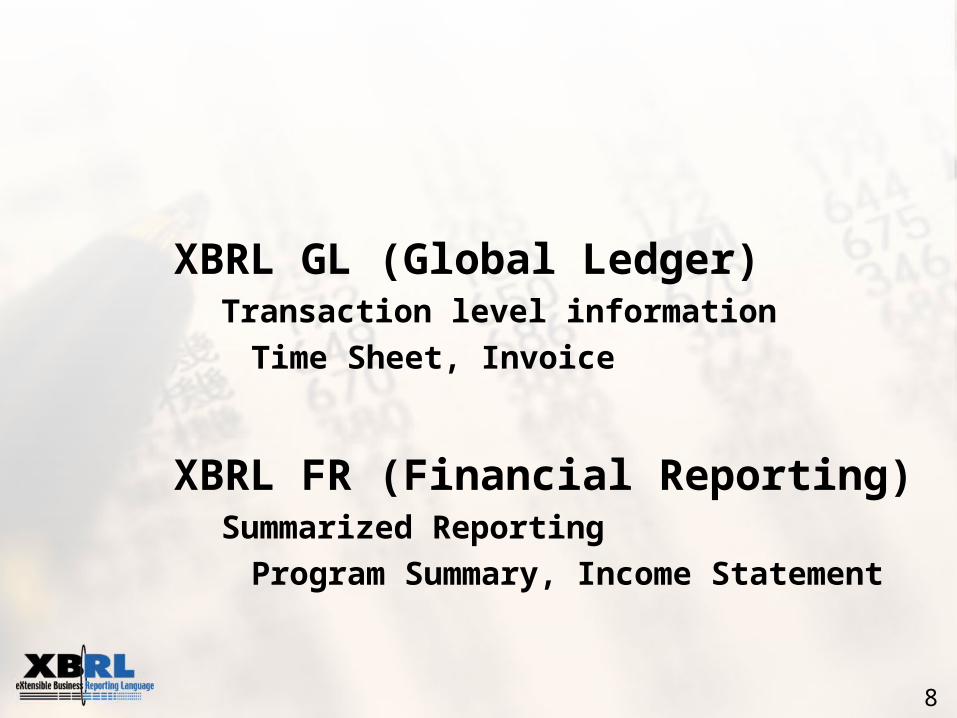

XBRL GL (Global Ledger)Transaction level information

Time Sheet, Invoice

XBRL FR (Financial Reporting)Summarized Reporting

Program Summary, Income Statement

9

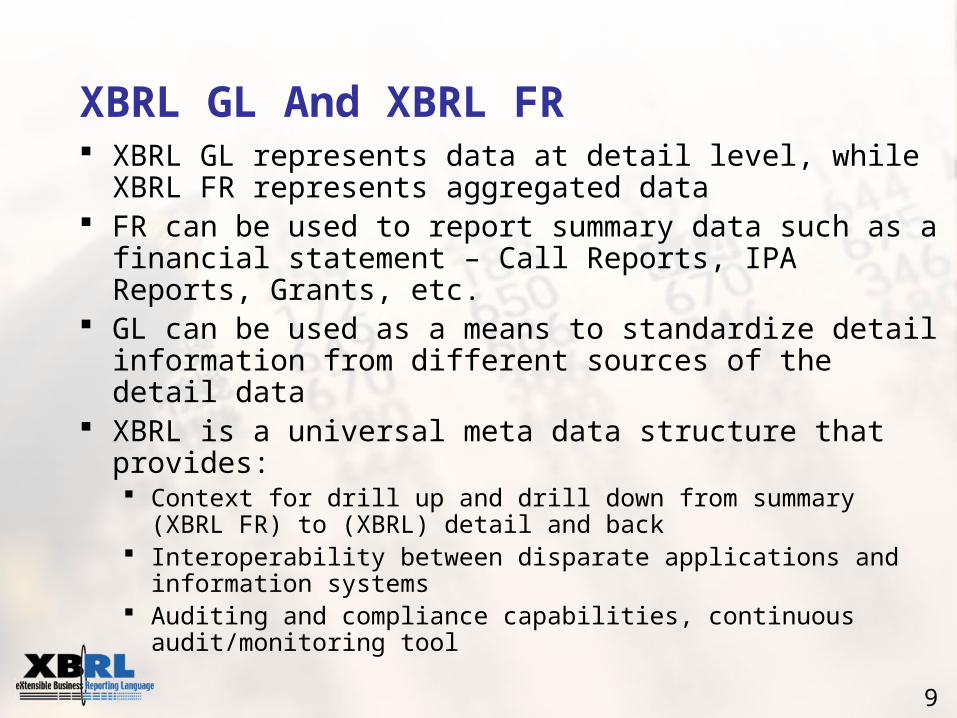

XBRL GL And XBRL FR XBRL GL represents data at detail level, while XBRL FR

represents aggregated data FR can be used to report summary data such as a

financial statement – Call Reports, IPA Reports, Grants, etc.

GL can be used as a means to standardize detail information from different sources of the detail data

XBRL is a universal meta data structure that provides: Context for drill up and drill down from summary (XBRL FR) to

(XBRL) detail and back Interoperability between disparate applications and information

systems Auditing and compliance capabilities, continuous audit/monitoring

tool

10

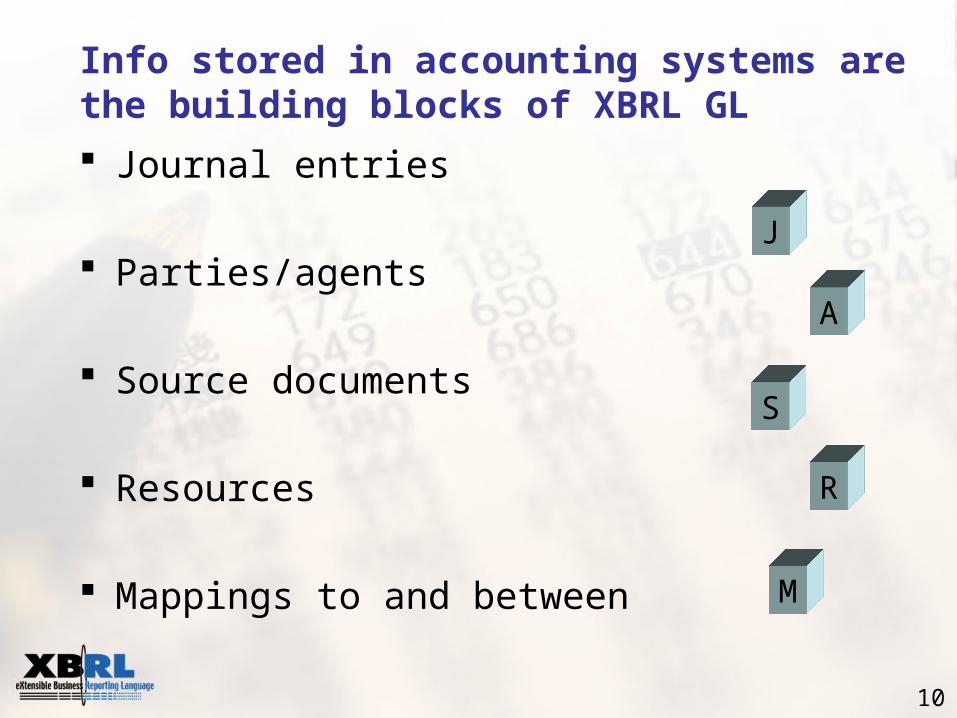

Info stored in accounting systems are the building blocks of XBRL GL

Journal entries

Parties/agents

Source documents

Resources

Mappings to and between

J

A

S

R

M

11

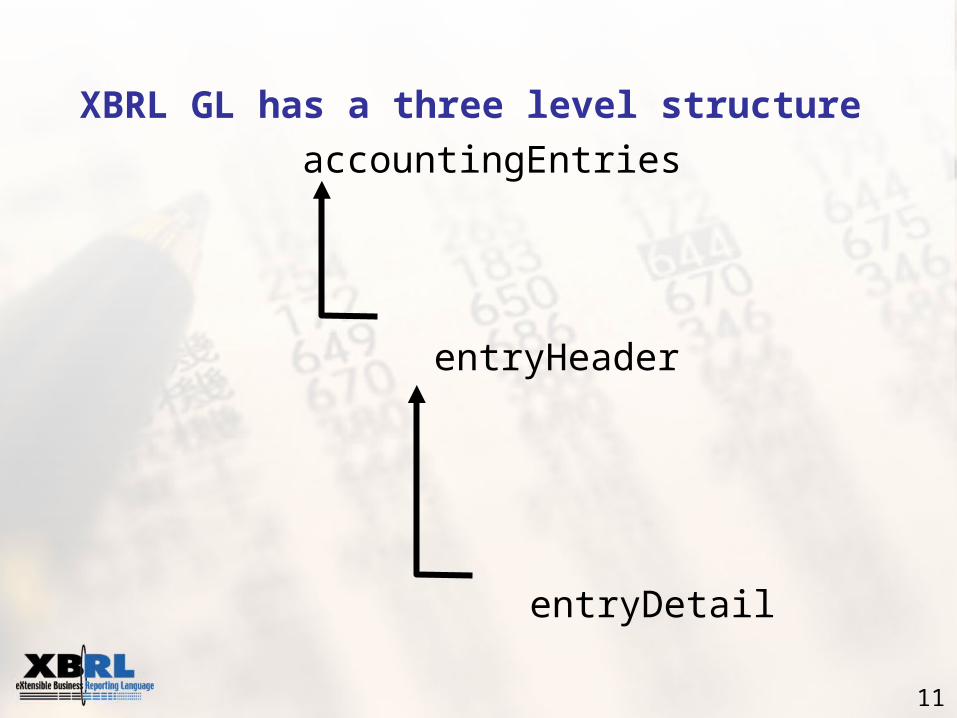

XBRL GL has a three level structure

accountingEntries

entryHeader

entryDetail

12

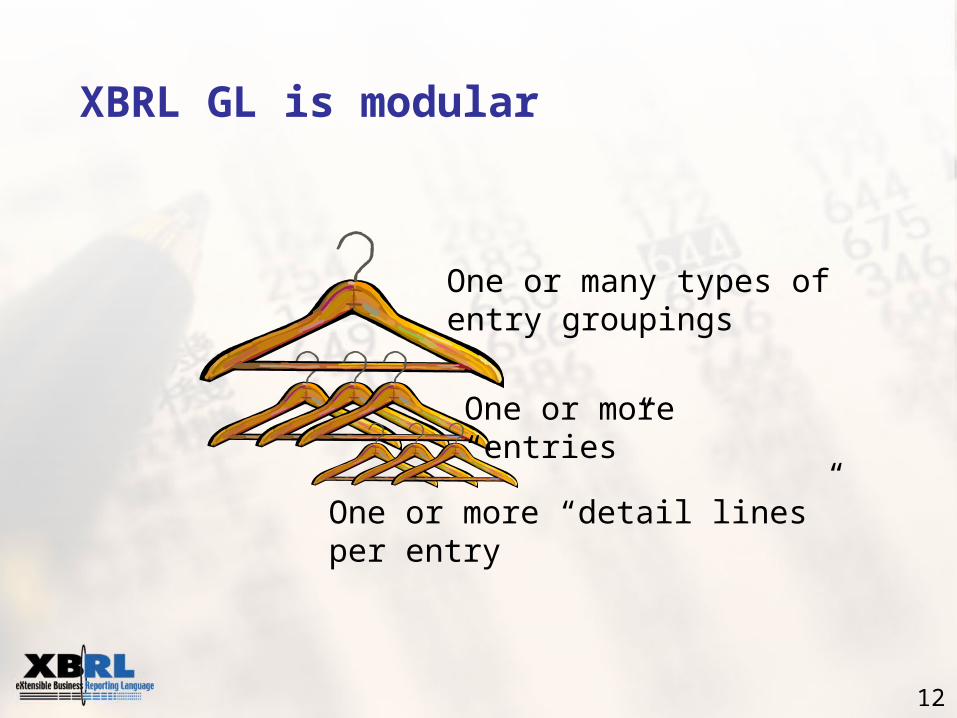

XBRL GL is modular

One or many types of entry groupings

One or more “entries”

One or more “detail lines” per entry

13

Summary Value Propositions By using a common standard, agencies gain

More productive data collection and reporting System interoperability and data reusability Data provided from source systems directly into

financial, analytic, planning and reporting systems and tools

Improved data quality, accuracy, and timeliness

Regulators can make constituent reporting a simpler process

Financial Managers can speed reporting