Embed Size (px)

Citation preview

1

Unravelling BEPS

Background:

Developments brought about by globalization and digitalization of the economy have led to

growing perceptions and concerns of the tax authorities that there is substantial loss of

corporate tax revenues to the government due to the planning adopted by corporates which

aim at eroding the tax base and/or shifting of profits to locations where they are subject to a

more favorable tax treatment. While there are certain companies that do not pay the taxes

they legally owe, there is a more fundamental concern that the international tax rules by

which taxing rights are shared between states have not kept pace with the changing business

environment.

The BEPS project is driven by these perceptions and concerns of the tax authorities.

Base erosion and profit shifting (BEPS) refers to tax planning strategies that exploit gaps

and mismatches in tax rules to make profits „disappear‟ for tax purposes or to shift profits to

locations where there is little or no real activity but the taxes are low resulting in little or no

overall corporate tax being paid.1

BEPS strategies take advantage of a combination of features of home and host countries‟ tax

systems. It is the interaction of domestic and international tax systems which at times leave

gaps, resulting in income not being taxed anywhere. Hence, it leads to corporations urging

for bilateral and multilateral co-operation among countries to address these differences in

tax rules which result in double taxation.

The most astonishing fact is that these strategies are not illegal.

Base erosion constitutes a serious risk to tax revenues, tax sovereignty and tax fairness for

OECD member countries and non-member countries alike. The debate over BEPS has

reached the highest political level across the world.

This article aims at giving the reader an insight into the concept of BEPS, its evolution over a

span of time and the impact of the recent developments in the Indian tax scenario.

Before looking at the detailed provisions recommended by the OECD, it would be interesting

to understand the evolution and growth of this project.

1 Base Erosion and Profit Shifting : Frequently asked Questions, http://www.oecd.org/ctp/beps-frquentlyaskedquestions.htm

2

Evolution of BEPS Project:

The BEPS project was coined at the G20 Leaders meet in Mexico in June 2012 where they

explicitly referred to „the need to prevent base erosion and profit shifting' in its final

declaration.2 This message was reiterated at the G20 finance ministers' meeting held on 5-6

November 2012, the final communiqué of which stated: “We welcome the work that the

OECD is undertaking into the problem of base erosion and profit shifting and look forward

to a report about progress of the work at our next meeting.”3

In the same month, the UK's Chancellor of the Exchequer George Osborne and Germany's

Minister of Finance Wolfgang Schäuble issued a joint statement, 4 which backed by France's

Economy and Finance Minister Pierre Moscovici, called for coordinated action to back the

OECD work on identifying possible gaps in the standards as a first step in promoting a better

way of dealing with profit shifting and the erosion of the corporate tax base at the global

level.

Following this call, the OECD at the behest of the G-20 finance ministers published a report

titled “Addressing Base Erosion and Profit Shifting” in February 2013.This report assessed

the current position, issues related to BEPS and how BEPS could be addressed using a

collaborative approach.

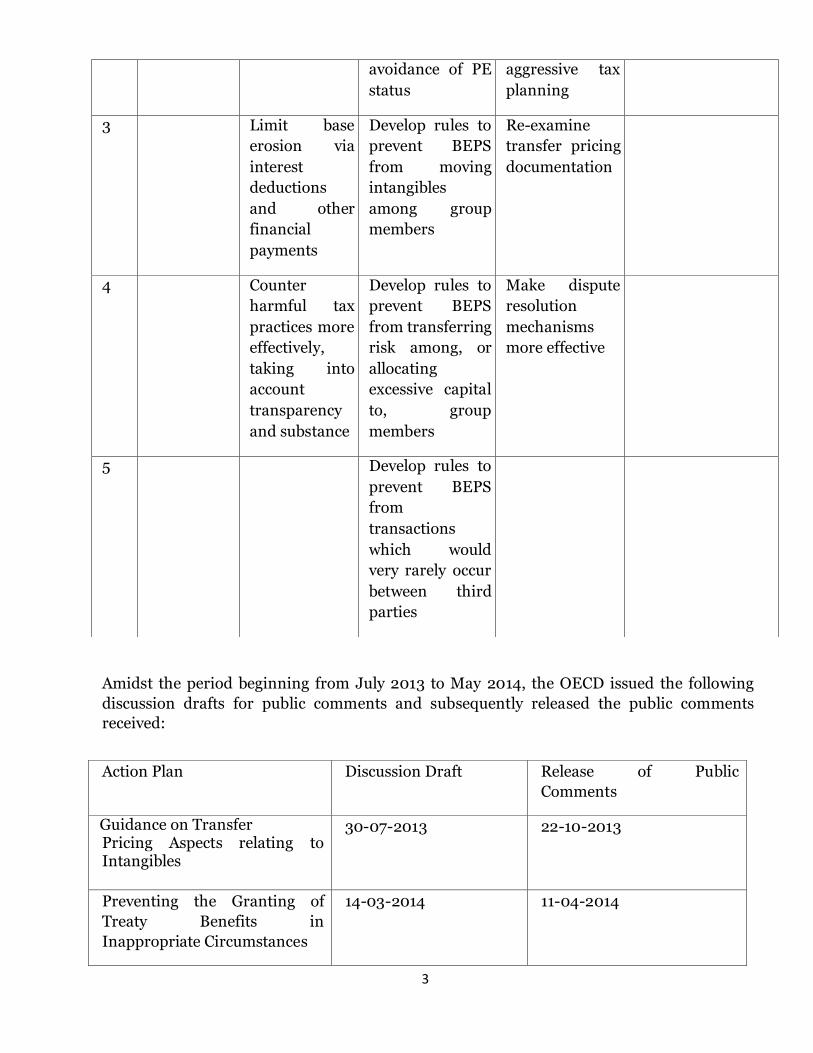

Subsequently the OECD released an action plan on July 19, 2013 which identified 15 action

points to tackle BEPS and set a time line of two years to achieve those plans. The OECD

document details its 15 point action plan under 5 key areas. The following table details a

summary of these action points that are prescribed under the above mentioned document:

3 www.taxjustice.net/cms/upload/pdf/OECD_Beps_130327_No_more_shifty_business.pdf 4 www.hm_treasury.gov.uk/chx_statement

Sr.

No.

The

Digital

Economy

Establishing

Coherence

of Corporate

Income

Taxation

International

Standards

Transparency Implementation

1 Address the

tax

challenges

of the

digital

economy

Neutralize the

effects of

hybrid

mismatch

arrangements

Prevent treaty

abuse

Establish

methodologies

to collect and

analyse data on

BEPS

Develop a

multilateral

instrument

2 Strengthen

CFC rules

Develop changes

to PE definition

to avoid artificial

Require

taxpayers to

disclose

3

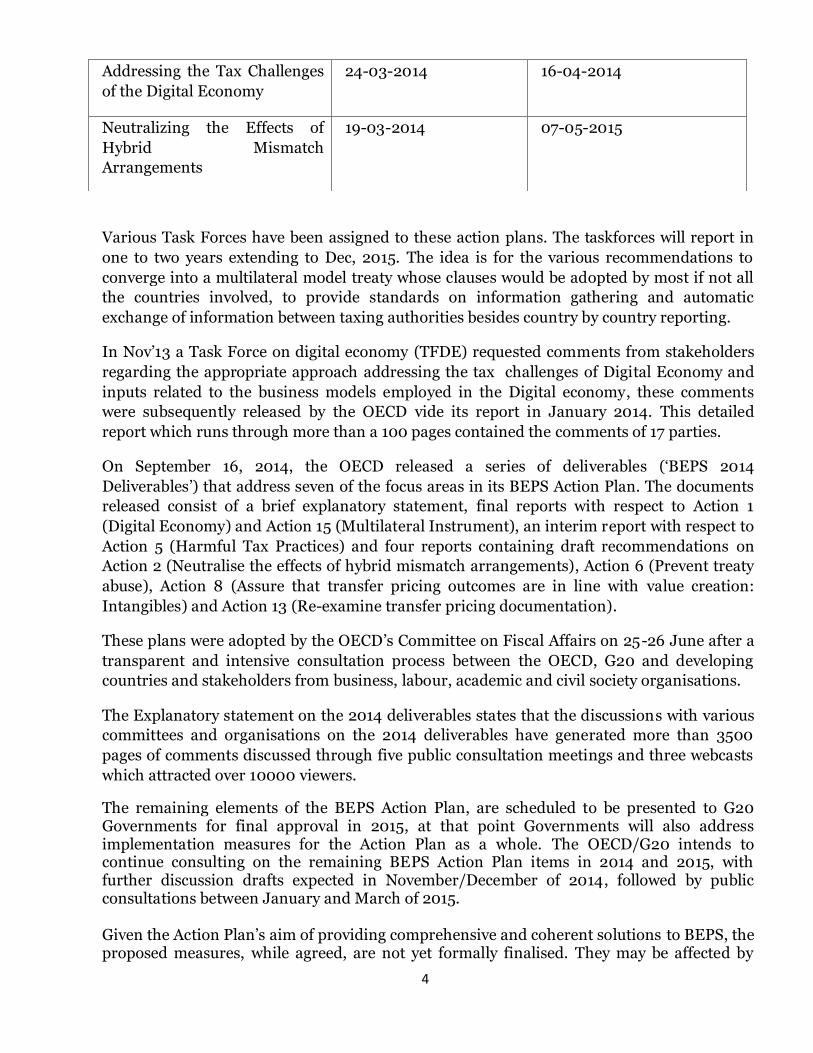

Amidst the period beginning from July 2013 to May 2014, the OECD issued the following

discussion drafts for public comments and subsequently released the public comments

received:

avoidance of PE

status

aggressive tax

planning

3 Limit base

erosion via

interest

deductions

and other

financial

payments

Develop rules to

prevent BEPS

from moving

intangibles

among group

members

Re-examine

transfer pricing

documentation

4 Counter

harmful tax

practices more

effectively,

taking into

account

transparency

and substance

Develop rules to

prevent BEPS

from transferring

risk among, or

allocating

excessive capital

to, group

members

Make dispute

resolution

mechanisms

more effective

5 Develop rules to

prevent BEPS

from

transactions

which would

very rarely occur

between third

parties

Action Plan Discussion Draft Release of Public

Comments

Guidance on Transfer Pricing Aspects relating to Intangibles

30-07-2013 22-10-2013

Preventing the Granting of

Treaty Benefits in

Inappropriate Circumstances

14-03-2014 11-04-2014

4

Various Task Forces have been assigned to these action plans. The taskforces will report in

one to two years extending to Dec, 2015. The idea is for the various recommendations to

converge into a multilateral model treaty whose clauses would be adopted by most if not all

the countries involved, to provide standards on information gathering and automatic

exchange of information between taxing authorities besides country by country reporting.

In Nov‟13 a Task Force on digital economy (TFDE) requested comments from stakeholders

regarding the appropriate approach addressing the tax challenges of Digital Economy and

inputs related to the business models employed in the Digital economy, these comments

were subsequently released by the OECD vide its report in January 2014. This detailed

report which runs through more than a 100 pages contained the comments of 17 parties.

On September 16, 2014, the OECD released a series of deliverables („BEPS 2014

Deliverables‟) that address seven of the focus areas in its BEPS Action Plan. The documents

released consist of a brief explanatory statement, final reports with respect to Action 1

(Digital Economy) and Action 15 (Multilateral Instrument), an interim report with respect to

Action 5 (Harmful Tax Practices) and four reports containing draft recommendations on

Action 2 (Neutralise the effects of hybrid mismatch arrangements), Action 6 (Prevent treaty

abuse), Action 8 (Assure that transfer pricing outcomes are in line with value creation:

Intangibles) and Action 13 (Re-examine transfer pricing documentation).

These plans were adopted by the OECD‟s Committee on Fiscal Affairs on 25-26 June after a

transparent and intensive consultation process between the OECD, G20 and developing

countries and stakeholders from business, labour, academic and civil society organisations.

The Explanatory statement on the 2014 deliverables states that the discussions with various

committees and organisations on the 2014 deliverables have generated more than 3500

pages of comments discussed through five public consultation meetings and three webcasts

which attracted over 10000 viewers.

The remaining elements of the BEPS Action Plan, are scheduled to be presented to G20 Governments for final approval in 2015, at that point Governments will also address implementation measures for the Action Plan as a whole. The OECD/G20 intends to continue consulting on the remaining BEPS Action Plan items in 2014 and 2015, with further discussion drafts expected in November/December of 2014, followed by public consultations between January and March of 2015. Given the Action Plan‟s aim of providing comprehensive and coherent solutions to BEPS, the proposed measures, while agreed, are not yet formally finalised. They may be affected by

Addressing the Tax Challenges

of the Digital Economy

24-03-2014 16-04-2014

Neutralizing the Effects of

Hybrid Mismatch

Arrangements

19-03-2014 07-05-2015

5

some of the decisions to be taken with respect to the 2015 deliverables with which the 2014 deliverable will interact. In the recently concluded Meeting of G20 Finance Ministers and Central Bank Governors in Cairns, Australia on the 20-21 September 2014, the members welcomed the significant progress achieved by the OECD and committed to finalise all action plans by 2015. Further a resolution mandating the OECD and its Global Forum on Transparency and Exchange of Information was also passed so as to support developing countries addressing BEPS and to launch pilot projects to assist them to move towards automatic exchange of information.

Next, the deliverables will be presented to the G20 leaders in November 2014 so as to

deepen the involvement of developing countries in the OECD/G20 BEPS project and ensure

that their concerns are addressed.

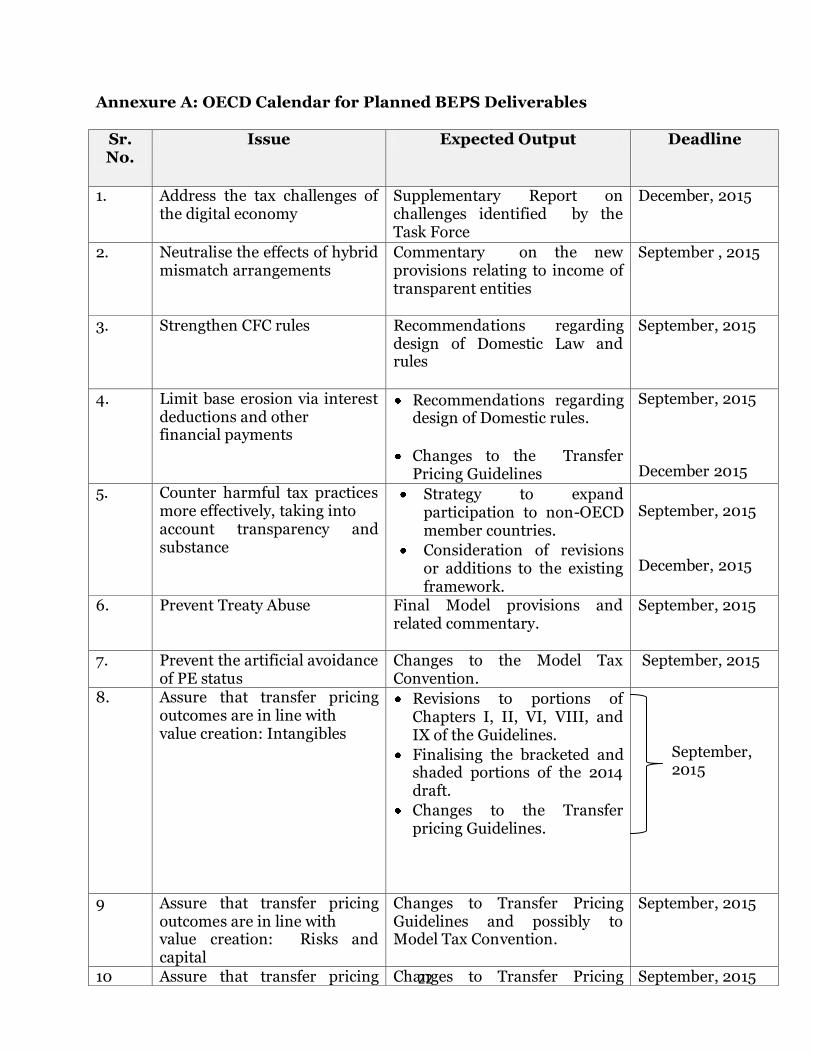

A tabular statement providing a bird eye view of the planned deliverables by the OECD in

regard to the 15 action plans along with the set deadlines is annexed in Annexure A.

Core Issues relating to BEPS

The OECD report on “Addressing Base Erosion and Profit Shifting” as released in February

2013, identified the following areas to be the key pressure areas for combatting BEPS:

1. International mismatches in entity and instrument characterization including, hybrid

mismatch arrangements and arbitration :

Hybrid mismatch arrangements can be described as practices where differences in the

countries legislations are exploited and the same expense is deducted in multiple countries

or multiple tax deductions are applied for a single tax paid.

2. Application of Treaty Concepts to Profits derived from the delivery of digital goods and

services:

Development of digital economy raises the questions as to how enterprises in the digital

economy add value and make their profits and how the digital economy relates to the

concepts of source and residence or the characterization of income for tax purposes. Thus it

becomes important to analyse the manner in which these enterprises add value and make

profits.

3. The tax treatment of related Party debt financing, captive insurance and other intra group

financial transactions:

Captive Insurance: A captive insurance company is generally a wholly owned insurance

subsidiary with its main object being insuring the risks of the parent and affiliated

companies. A captive is mainly established by the parent company for reducing its insurance

premiums or for retaining the profits made on insuring or to funnel income to a country

with no or lower income tax rate. These transactions are framed mainly at tax avoidance and

to prevent countries losing their revenue base.

6

Related Party debt : Under international taxation regime, profits could be shifted through

the transaction of borrowing and lending in the form of charging no interest or at a lower

rate than the market rate on loan and advances made to its associated enterprise or,

otherwise becoming a creditor of an associated enterprise either being parent company or

subsidiary company. Multi National Enterprises (“MNE‟s”) enter into these kinds of

transactions in order to avoid their tax liability by taking loan from their parent or

subsidiary company situated in low tax jurisdiction or through the establishment of

controlled foreign companies (CFC) in low tax jurisdiction.

4. Transfer pricing, particularly in relation to the shifting of risks and intangibles, the artificial

splitting of ownership of assets between legal entities within a group of transactions between

such entities that would rarely take place between independents:

Many corporate tax structures focus on allocating significant risks and hard to value

intangibles to low tax jurisdictions where their returns may benefit from favorable tax

regimes. Such arrangements may lead to BEPS. Shifting income through transfer pricing

arrangements raise questions as to how risk is actually distributed among the members of a

MNE group and whether transfer pricing rules should easily accept contractual allocations

of risk.

5. The effectiveness of anti-avoidance measures, in particular GAARs, CFC regimes, thin

capitalization rules and rules to prevent tax treaty abuse :

Countries around the world have failed to implement properly the anti-avoidance measures

which are aimed at addressing tax avoidance by MNE‟s. Further the rules relating to CFC

regimes and thin capitalization are not very effective and need further modifications to curb

the problem of BEPS.

6. The availability of harmful preferential regimes:

Governments have long accepted that there are limits and they should not be engaged in

harmful tax practices. When a regime has been found harmful, the relevant country will be

given the opportunity to abolish the regime or remove the features that create the harmful

effect. However, when a country does not do this, it creates BEPS.

The role of the OECD Committee on Fiscal Affairs5 The technical work on BEPS is being undertaken by the OECD Committee on Fiscal Affairs (CFA) through its subsidiary bodies, namely:

1. Working Party 1 (Tax Conventions and Related Questions), in relation to part of action 2 (Neutralise the Effects of Hybrid Mismatch Arrangements), action 6 (Prevent Treaty Abuse),

5 https://www.gov.uk/government/speeches/statement-by-the-chancellor-of-the-exchequer-rt-hon-george-osborne-mp-britain-germany-call-for-international-action-to-strengthen-tax-standards

7

action 7 (Prevent the Artificial Avoidance of PE Status), and action 14 (Make Dispute Resolution Mechanisms More Effective);

2. Working Party 2 (Tax Policy Analysis and Tax Statistics), in relation to action 11 (Establish Methodologies to Collect and Analyse Data on BEPS);

3. Working Party 6 (Taxation of Multinational Enterprises), in relation to part of action 4 (Limit Base Erosion via Interest Deductions and Other Financial Payments), actions 8 (Assure that Transfer Pricing Outcomes are in Line With Value Creation / Intangibles), 9 (Assure that Transfer Pricing Outcomes are in Line With Value Creation / Risks and Capital), 10 (Assure that Transfer Pricing Outcomes are in Line With Value Creation / Other High-Risk Transactions), and 13 (Re-examine Transfer Pricing Documentation);

4. Working Party 11 (Aggressive Tax Planning), established by the CFA to carry out the work in relation to part of action 2 (Neutralise the Effects of Hybrid Mismatch Arrangements), action 3 (Strengthen CFC rules), part of action 4 (Limit Base Erosion via Interest Deductions and Other Financial Payments), and action 12 (Require Taxpayers to Disclose their Aggressive Tax Planning Arrangements).

5. Forum on Harmful Tax Practices (FHTP), in relation to action 5 (Counter Harmful Tax Practices More Effectively, Taking into Account Transparency and Substance); and

6. Task Force on Digital Economy (TFDE), established by the CFA to carry out the work in relation action 1 (Address the Tax Challenges of the Digital Economy).

BEPS 2014 deliverables: OECD‟s agreed recommendations for changing the international tax rules are wide-ranging under its first stage of work in connection with base erosion and profit shifting (BEPS). As stated above, seven of the fifteen areas of the BEPS Action Plan are covered under this first stage. The following paragraphs provide a brief analysis of these seven action plans and their impact on the Indian tax regime:

1. Action 1: Addressing the Tax Challenges of the Digital Economy: The Digital Economy Report builds upon the March 2014 discussion draft which identified the major tax challenges raised by the rapidly developing digital economy and which summarized several possible options to address these challenges. Some of the key features of the digital economy identified in the Digital Economy Report include mobility, volatility, data reliance and multi-sided business models (e.g., a payment system acting as a third participant in an e-commerce sales transaction). The report clarified that because the digital economy is increasingly becoming the economy itself, it would be difficult, if not impossible, to ring-fence the digital economy from the rest of the economy for tax purposes. Further an attempt to isolate the digital economy as a separate sector would inevitably require arbitrary lines to be drawn between what is digital and what is not.

8

As a result, it was concluded that the tax challenges and BEPS concerns raised by the digital economy are better identified and addressed by analysing existing structures adopted by multinational enterprises (MNEs) together with new business models. The key tax areas which are needed to be addressed are identifying the specific remedies to be considered by the other BEPS workstreams – specifically, CFC rules; artificial avoidance of permanent establishment (PE); and transfer pricing measures. The Digital Economy Report also includes a new chapter that discusses the fundamental principles of taxation and, in the process of doing so; it also reconsiders some of proposed approaches for addressing the tax challenges of the digital economy. The report also explains the role of the Task Force of Digital Economy (TFDE) for the remainder of the BEPS project. The Task Force, based on its discussion of the tax challenges and potential options to address them, concluded as follows:

1. The work in the consumption tax questions in the draft report area should focus upon administrative procedures to collect B2C VAT type taxes rather than suggest changes to VAT regimes.

2. The general operation of the preparatory or auxiliary exemption in the PE article needs to be reviewed along with the specific warehouse exception. In addition, there is the suggestion that the reliance on concluding a contract in one territory to avoid taxation in another should be reviewed.

3. The role of intangibles in fragmented business models and the increasing importance of data needs to be highlighted. Transfer pricing allocation methodologies need to be reviewed. Further there is the suggestion that relying upon a model which allocates a routine return to a low risk subsidiary and the balance to a low tax entrepreneur company may not be wholly appropriate.

4. The possibility of changing CFC rules to target the types of income that may typically feature in a digital economy business needs to be examined.

5. Working party No. 1 of the CFA should consider the characterisation of various payments

arising in the new information and communication technology enabled world. Further, the OECD also indicated that as the recommendations on the other Actions Items are finalized, will evaluate how the outcomes of the recommendations affect the broader tax challenges raised by the digital economy and will complete an evaluation of the options to address them. This work will be concluded by December 2015 and a supplementary report reflecting the outcomes of the work will be finalized at that time.

Current Indian Scenario and Way forward:

In the current global tax scenario assessees doing their business through E-Commerce can

avoid almost total tax. Firstly, they can shift their operations to a tax haven and avoid

domestic tax in their state of residence. Further based on the double tax convention there is

a high probability that their incomes may be categorised as "Business Profits". Hence as they

9

have no PE in most of the countries from which they earn their revenues, they escape tax in

the source countries also.

The domestic law in India does not have any specific provisions dealing with the issues

arising out of the digital economy. The Finance Act 2012, made an effort in this direction by

amending the definition of the term „royalty‟ retrospectively to include within its definition

most of the digital economy and technology transactions.

It is important to note that as per BEPS report India‟s export of ICT services is around 13.5

billion US$ and ranks number 1.6 These statistics highlights the importance of the need to

address the concerns arising from the digital economy in India.

The concept of digital economy was introduced way back in 2003, by the OECD in its Model

Commentary which stated that entry into an economy wholly through a digital economy

would not create a PE. At the time when the PE concept was created, the emerging countries

including India were not on the table of the OECD. However, as seen from the above

statistics, India having a higher stake in the controversy involving digital economy, it has

been highly involved in the OECD discussions about reviewing the PE definition in its

capacity as an observer.

India has expressed reservations and taken a position that websites and acquisition of a

place of business by hosting a website on a particular server at a particular location may

constitute a PE, however this position has not been given much weightage by the Indian

Courts while dealing with such issues. In recent times, the Courts have been considering the

impact of the digital economy and its activities while pronouncing its rulings. Further,

information provided through the various sources of ICT are also being considered to be of

persuasive value by the Courts in course of judicial proceedings. Recently the Delhi Tribunal

in the case of GE Energy Parts Inc. v. Addl. Director of Income-tax (ITA No.

671/Del/2011 dated 04.07.2014) held that information available on social networking site -

LinkedIn, is admissible as additional evidence for determination of permanent

establishment. Though, the Delhi High Court has vide its order dated July 4, 2014 stayed the

above order of the Delhi Tribunal, it cannot be ignored that the Courts are definitely

considering the information available through Digital Platforms to be of considerable

relevance while determining the fate of a case.

Amongst all the recommendations of the TFDE, the recommendation in regard to the

amendment of the preparatory and auxiliary exemption of the PE definition if implemented

would have far reaching effect in the Indian tax regime wherein a huge number of MNE‟s

have been taking shield behind this exemption so as to avoid the clutches of the Indian

taxman.

6 Digital Economy Report Page. 88

10

2. Action 2: Neutralizing the Effects of Hybrid Mismatch Arrangements: Action 2 of the BEPS Action Plan calls for the development of model treaty provisions and recommendations regarding the design of domestic rules to neutralise the effect of hybrid instruments and entities. This Report sets out these recommendations in two parts. Part I contains recommendations on domestic law rules to address arrangements that result in double non-taxation or long-term tax deferral. Part II contains recommended changes to the OECD Model Tax Convention to deal with transparent entities including hybrid entities and addresses the interaction between the recommendations included in Part I and the provisions of the OECD Model Tax Convention. The Hybrid Report recommends linked domestic rules. The linking element arises because the treatment of an amount in one jurisdiction would be linked to its treatment in the other jurisdiction. The linking approach is not intended to harmonize tax systems in different countries. Rather, the intent is for one country to link the tax results of certain hybrid arrangements to the tax treatment of such arrangements in another country. Action 2 also calls for hybrid mismatch rules that adjust the tax outcomes in one jurisdiction to align them with the tax consequences in another. These actions call for domestic rules targeting two types of payments being:

payments under a hybrid mismatch arrangement that are deductible under the rules of the payer jurisdiction and not included in the ordinary income of the payee or a related investor (deduction / no inclusion or D/NI outcomes); and

payments under a hybrid mismatch arrangements that give rise to duplicate deductions for the same payment (double deduction or DD outcomes). The report recommends a “rule order” under which primary and defensive rules would operate to address double non-taxation outcomes and avoid double taxation. Thirdly, reflecting extensive comments received from stakeholders, the report limits the scope of the recommended rules by using the “bottom up approach”. The recommended rules would apply to hybrid arrangements involving related parties and members of the same controlled group and to certain “structured” arrangements. For this purpose, the related party threshold to be used has been raised to 25% from 10% as proposed in the Hybrid Mismatch Discussion Draft. The recommendations with respect to the OECD Model Tax Convention include: (i) a change to Article 4 of the Model Tax Convention to deal with dual resident entities; (ii) a new provision in Article 1 and changes to the Commentary to address fiscally transparent entities; and (iii) various proposed changes to address treaty issues that may arise from the recommended domestic law changes. The OECD and G20 will consider the coordination of the timing of the implementation of these rules. It is possible that this may not be until after a commentary and guidance has been produced, which will be by September 2015.

11

Current Indian Scenario and Way forward:

India does not recognize differential tax treatments for hybrid financial instruments or the

concept of tax transparent entities.

The recommendations in the Hybrid Report represent sweeping measures that, if enacted

into Indian domestic law and tax treaties, could have a significant impact on various entities

and transactions. Currently, India already has foreign tax credit generator rules in place.

However the adoption of the linking rules recommended in the report would not be an easy

task as the changes to the domestic laws would be an exorbitant issue. Similarly, crafting

rules that are also linked to the tax treatment which is accorded to a particular payment in

another country also appears to be a magnificent task.

Further, post incorporations of these recommendations in the domestic laws, co-ordination

amongst the countries involved in such hybrid arrangements would be required to avoid

double taxation by the way of both countries applying the recommended rule. On the perusal

of the action plan it appears that many of the complex tax policy and technical issues which

are associated with the proposals remain unresolved, and will presumably be addressed in

the second phase of the work relating to implementation. For example, significant

transitional issues may arise where a delay in implementation in one country leaves other

countries uncertain about whether to apply a primary or defensive measure. Nevertheless,

the Hybrid Report represents the consensus view of the OECD and G20 countries that

hybrid mismatches should be neutralized although it is unclear what measures will be taken

to reflect this consensus.

3. Action 5 :Countering Harmful Tax Practices More Effectively, taking into Account Transparency and Substance Under Action Item 5, the FHTP is to deliver three outputs: first, finalisation of the review of member country preferential regimes; second, a strategy to expand participation to non-OECD member countries; and, third, consideration of revisions or additions to the existing framework. The interim report on Action 5 (the Harmful Tax Practices Report) discusses the progress on the first output. The second and third outputs are expected by September and December 2015, respectively. In the review of preferential regimes, the FHTP concentrated first on intellectual property (IP) regimes. It suggested that a “nexus approach” would be most appropriate when determining whether the substantial activity test is met. Under this approach the application of an IP regime would be dependent on the level of R&D activities carried out by the taxpayer. The FHTP will focus primarily on a “nexus” approach, which requires a direct nexus between the income receiving benefits under a preferential regime and the expenditures contributing to that income. Under this approach, the proportionate amount of expenditures is used as a proxy for substantial activity. Initial guidance is provided on how proportionate expenditures will be determined (such as outsourced R&D only being an eligible expenditure if outsourced to a third party, or expenditures on acquired IP only being eligible if incurred for post-acquisition improvements). Further intangible regimes in member countries are also being reviewed at

12

the same time (none of which were previously reviewed). The FHTP will also consider how to apply an elaborated substantial activity test to non IP regimes. With respect to the goal of improving transparency, the FHTP developed a framework for compulsory spontaneous exchange of information by tax administrations on taxpayer-specific tax rulings and Advance Pricing Agreements (APAs). The framework would require rulings (or summaries of such rulings) on preferential regimes that meet certain criteria to be exchanged spontaneously with the competent authorities of the tax jurisdictions involved. Finally, it provides a progress report on the ongoing review of the regimes of OECD member and associate countries in the OECD/G20 Project on BEPS. Current Indian Scenario and Way forward:

For a country like India, tax havens pose a real danger to its economy. They play an active

role by letting criminals, black marketers and tax evaders park their funds in tax havens. Tax

havens also enable them to bring back such funds through official channels and make

investments in the country. From an Indian perspective, this would mean an increased focus

on the India-Mauritius route used for bringing FDI into the country. BEPS may accelerate

the process of treaty re-negotiation based on the suggested measures, which has been a long

overdue agenda for India.

The report provides for a requirement of substantial activity test in the context of intangible regimes inorder to be eligible to claim tax benefits in a jurisdiction. The compliance of this test is determined on the basis of the expenditure incurred by the assessee. However in the absence information from the taxpayer a jurisdiction would determine the income receiving tax benefits on the basis of a calculation where a percentage of the qualifying expenditure to the overall expenditure incurred by the taxpayer to develop IP asset is applied to the overall income from the IP asset. Presently, this substantial activity test requirement is missing in India. If implemented, this version of the nexus approach may require greater record-keeping on the part of taxpayers, and jurisdictions may need to establish notification and monitoring procedures. Difficulties may also arise around how to establish the direct linkage between expenditures and income, but it could ensure that taxpayers that engaged in greater value creating activity than is reflected in the calculation above would be permitted to have more income benefit from the IP regime. Jurisdictions that did decide to adopt this version would still use the calculation above to establish the presumed amount of income that could qualify for tax benefits.

Further, the framework, as currently contemplated, only requires spontaneous information exchange on taxpayer-specific rulings related to preferential regimes, i.e. rulings that are specific to an individual taxpayer and on which that taxpayer is entitled to rely. There is at present no such requirement for general rulings, i.e. rulings that apply to groups or types of taxpayers or maybe given in relation to a defined set of circumstances or activities. One reason for not currently requiring spontaneous information exchange of general rulings is that in the absence of a link between the ruling and a specific taxpayer, to which the ruling applies, it would be very difficult to determine with which country or countries information should be exchanged. Spontaneous information exchange of general rulings with each country with whom a relevant tax administration has an information exchange relationship would impose a disproportionate administrative burden and is unlikely to be very effective.

13

In addition, general rulings appear to pose less of a risk since they are often published and their conditions of applicability will therefore be available. As general rulings are not suitable for spontaneous exchange of information, the FHTP will consider them separately under the second step of the work on transparency which will consider the actual ruling regimes of member countries and associate countries against the factors in the 1998 Report. This work will also consider whether countries‟ general ruling regimes are transparent and will seek to establish best practices to ensure they are indeed available to other countries. Since work on the major portion of the report is still pending, the impact of the outcomes of the report on the Indian Economy can be determined only in 2015 when the final report is made available.

4. Action 6: Preventing the Granting of Treaty Benefits in Inappropriate Circumstances Action 6 in the BEPS Action Plan had identified treaty abuse, and in particular treaty shopping, as an important source of BEPS concern. The Treaty Report makes recommendations in three distinct areas for preventing the facilitation of BEPS through the use of tax treaties:

1. Develop model treaty provisions and recommendations regarding the design of domestic rules to prevent the granting of treaty benefits in inappropriate circumstances.

2. Clarify that tax treaties are not intended to be used to generate double non-taxation. 3. Identify the tax policy considerations that, in general countries should consider before

deciding to enter into a tax treaty with another country The report suggests that at a minimum, countries should: (i) affirm through an express statement in their tax treaties that they intend to eliminate double taxation without creating opportunities for non-taxation or reduced taxation through tax evasion or avoidance; and (ii) adopt either (A) the Limitation of Benefit (LOB) and the Principal Purpose Test (PPT) rules, (B) the PPT rule, or (C) the LOB rule supplemented by a mechanism (such as a restricted PPT rule applicable to conduit financing arrangements or domestic anti-abuse rules or judicial doctrines that would achieve a similar result) that would address conduit financing arrangements not already addressed in tax treaties. The LOB provision in the Treaty Abuse Report includes a derivative benefits test. The "derivative benefits" provision allowing certain entities owned by residents of other States to obtain treaty benefits that these residents would have obtained if they had invested directly. The Treaty Abuse Discussion Draft had discussed derivative benefits tests but had raised concerns about the implications of such a test. Further, the PPT rule included in the report incorporates principles already recognised in the Commentary on Article 1 of the Model Tax Convention. It provides a more general way to address treaty abuse cases, including treaty shopping situations that would not be covered by the LOB rule (such as certain conduit financing arrangements). In addition, The Treaty Abuse Report also adds a proposed change to the OECD Model Tax Convention addressing the availability of treaty benefits to collective investment vehicles (CIVs) and other funds. It further indicates that further work will be needed with respect to the precise contents of the anti-abuse rules, in particular the LOB rule.

14

The report also addresses two specific issues related to the interaction between treaties and specific domestic anti-abuse rules. The first issue relates to the application of tax treaties to restrict a Contracting State‟s right to tax its own residents. The report recommends that the principle that treaties do not restrict a State‟s right to tax its own residents (subject to certain exceptions) should be expressly recognized through the addition of a new treaty provision based on the so-called “saving clause” already found in United States tax treaties. The second issue deals with so-called “departure” or “exit” taxes, under which liability to tax on some types of income that has accrued for the benefit of a resident (whether an individual or a legal person) is triggered in the event that the resident ceases to be a resident of that State. The report recommends changes to the Commentary included in the Model Tax Convention in order to clarify that treaties do not prevent the application of these taxes. Finally, the report indicates that the proposed OECD Model Tax Convention provisions and related Commentary should be considered as drafts that are subject to improvement prior to the release of the final version in September 2015.

Current Indian Scenario and Way forward:

Treaty abuse is the most often used tactic to evade taxes and shifting of profits from one

country to another. This aspect has been the subject matter of serious debate in India.

In India, the Revenue Authorities have been constantly striving to prevent treaty abuse. The

requirement of a Tax Residency Certificate introduced by the Finance Bill 2012 and the

other self-declarations in Form No 10F by Finance Bill 2013 are steps taken towards this

initiative. The GAAR provisions in line with the OECD, which is proposed to be effective

from F.Y 2015-16 are also found in the Indian tax laws. At present, CFC rules and thin

capitalization rules are missing in India.

The first part of the action plan aims at developing model treaty provisions. However, the

adoptions of these provisions are purely based on the negotiations between the bilateral

states. The same has also been recognized by the Supreme Court in the case of Union of

Inia v. Azadi Bachao Andolan [2003] 263 ITR 706 wherein it was noted that treaties

are negotiated and entered into at a political level and have several considerations at their

bases. Thus, the effectiveness of this action plan in all countries including India would

depend upon the level of willingness for negotiations between the contracting states. In

regard to the introduction of the LOB clause, it should be noted that India has a LOB article

and PPI clause in place with approx. 33 countries. Thus, in regards to that part of the action

plan which deals with designing of domestic rules to deny treaty benefit it may be pointed

out that India already has the relevant rules in the domestic law. Hence, in this regard, the

BEPS project may not have a perceptible impact on India‟s domestic law. However, in terms

of certain treaties signed by India which support double non-taxation for e.g. The India-

Mauritius treaty on capital gains, the BEPS project may pressurize the countries to adopt a

suitable LOB clause in their treaties.

The exact impact of the Report is difficult to assess. The Report is an interim report which is

subject to further improvement before the final version is scheduled to be released in

15

September 2015 and considering that even the Report recognizes that the draft model tax

treaty provisions will need to be adapted to the specific needs of the countries.

5. Action 8: Guidance on Transfer Pricing Aspects of Intangibles

The draft recommendations under Action 8 (The Transfer Pricing Aspects of Intangibles Report) contained revised standards for transfer pricing of intangibles and additional standards with respect to comparability and transfer pricing methods. The first part of the Report contains amendments to Chapter I (The Arm‟s Length Principle) of the OECD Transfer Pricing Guidelines which related to the transfer pricing treatment of location savings and other local market features, assembled workforce, and the existence of MNEs group synergies. The second part of the report contains an entirely revised Chapter VI (Special considerations for intangibles) of the OECD Transfer Pricing Guidelines. Given that a portion of the content of the intangibles report will clearly be influenced by the

work the OECD is doing over the course of the next year on risk, recharacterisation, hard to

value intangibles, and special measures, parts of the intangibles document will not be

finalised now but will represent only interim guidance.

The Transfer Pricing Aspects of Intangibles Report contains interim guidance on:

ownership of intangibles Intangibles whose valuation is uncertain at the time of the transaction.

use of unspecified methods, and

using profit split methods.

The Interim guidance also includes several examples relating to:

The allocation of returns between the legal owners of intangibles and those who control or perform functions relating to the development, enhancement, maintenance, protection and exploitation of intangibles;

Arm‟s length pricing relating to intangibles whose valuation is uncertain at the time of the transaction;

The use of “other methods” to determine arm‟s length pricing; and

The application of the profit split method. In completing the transfer pricing work required by the BEPS Action Plan, the OECD will, as directed by the Action Plan, consider both the application of the arm‟s length principle and special measures in order to identify effective responses to the concerns raised in the BEPS Action Plan. Discussions on the special measures required to address the concerns identified in the Action Plan are ongoing. Among the special measures that will be considered during the course of the 2015 work are the following:

Permitting tax authorities in appropriate instances to apply rules based on “actual results” to price transfers of hard to value intangibles and, potentially, other assets, suggesting a

16

retrospective approach to the valuation of some transfers of property within multinational groups;

Treating entities whose activities are limited to providing funding for the development of intangibles (i.e., rather than performing “people functions”) as lenders under some circumstances, or otherwise limiting the return to such entities;

Requiring contingent payment terms and/or the application of profit split methods to certain transfers of hard to value intangibles;

Applying analogous rules to the Authorised OECD Approach to certain situations involving excessive capitalisation of low function entities. In the next several months, additional work will be undertaken in connection with risk, recharacterization, and hard to value intangibles, which will lead to partial revisions of Chapters I, II, VI, VIII and IX of the OECD Transfer Pricing Guidelines. In this process, so-called “special measures” which deviate from the arm‟s length principle may be considered. Current Indian Scenario and Way forward:

Globalisation and tax benefits have led to the establishment of many R&D centers in India.

However, there has been quite a bit of controversy on the transfer pricing issues related to

R&D centers. Amidst this controversy, the Indian Govt issued circular no 6/2013, addressing

the transfer pricing aspects related to development centres. The Circular laid down

guidelines for identifying contract with R&D service providers with insignificant risk. The

tax authorities recognized that economically significant functions to be performed by foreign

principal could be performed either through own employees or through its associated

enterprises in India. Thus, the associated enterprises in India can also exercise control over

the operational and other risks, hence the allocation of routine cost plus return will not

reflect the arms length price for the services rendered and the AO should choose the most

appropriate method after considering all the possible factors.

For India, the precedence of economic ownership over legal ownership, as asserted by the

Guidelines, is significant in order to protect its tax base since it is home to companies which

may perform functions and assume risks related to the intangible without legally owning the

intangibles. Also, the report identifies key functions, assets and risks which would entitle an

entity to the intangible related return.

Further, the observations regarding distinction between funding related return and

intangible related return are critical since almost all contract R&D activities undertaken in

India (by captives) are funded by the foreign principal. OECD‟s observation in the report

that funding alone should not entitle a taxpayer to an intangible related return assumes

significance in assisting the Indian Revenue Authorities to lay a legitimate claim on the

intangible related return accruing from Indian operations, provided the Indian entity

performs the key functions, owns the key assets and assumes key risks related to the

development, enhancement, maintenance and protection of intangibles. In such a scenario,

the report provides that the compensation to the entity performing the key R&D functions

may comprise a share in the total anticipated return from the intangible which would mean

17

that something similar to a profit split method, and not a comparable based margin method,

may have to be considered for computation of the arm‟s length margin.

In most of the TP Documentation in India, local comparables are selected to determine the

arm‟s length return. Hence, in these cases, the question of further attribution on account of

location savings does not arise. In recent audits the tax authorities have proposed high cost

plus mark up for captive R&D/ITES centres on account of location savings. Though it has

been argued by the authorities that economic benefit arising from the shifting of operations

to a low cost jurisdiction like India should accrue to the country where such operations are

carried out, the impact of these savings while computing the arms-length price is not

explicitly factored in the TP orders.

The Indian Authorities have advocated that benchmarking against local comparables does

not take into account the benefit of local savings and the use of Profit Split Method should be

encouraged wherein the functional analysis and bargaining power of the parties to the

transaction are relevant. They acknowledge that an arm‟s length compensation should

reflect an appropriate split of cost savings between the parties otherwise there would be no

incentive for an unrelated party to move to a jurisdiction with low cost operations.

Hence, the views of the Indian tax authorities contradict with the position in the OECD

guidance which stipulate that no separate compensation for location specific advantages is

required if there exists local comparable uncontrolled transaction. The Indian tax

authorities‟ view is that such an approach may not consider the benefit of location savings

and location specific advantages which can be computed by taking into account the cost

difference between costs in the low cost country and in the high cost country from where the

business activity was relocated.

In the area of marketing intangibles, it has been debated in the past rulings if it would be a

sufficient compensation if a distributor developing marketing intangibles earns higher

distribution profits or gets other concession such as royalty free license of intangibles or

should there be independent compensation towards the development of intangibles. In this

regard, the OECD suggests that independent compensation would not always be necessary

and the distributor can also be compensated by way of increased profits on distribution by

other modes such as reduction in the price of the materials purchased, reduction in royalty

payments etc. In other words, no transfer pricing adjustment would be necessary, in terms

of the report, if the distributors‟ profits are sufficiently higher to cover the expected

compensation towards the development of intangibles over and above the comparable

profits earned by normal distributors.

Further the report advocates use of guidance on location savings in all situations and not limited to those emerging from business restructuring. Hence, one may argue that relocation of functions may not be a trigger point for alleging additional returns (for Indian operations) for location savings.

18

Potentially, all MNCs operating in India have a threat of being questioned on existence of location savings because there is a high probability of a cost arbitrage by operating in India. Since India (although being non-OECD member country), as part of G 20 countries is supporting the BEPs initiative, it needs to be seen if the view of the OECD would find acceptance with the Indian tax authorities. In light of the above and given potential litigation, the taxpayers are advised to take requisite steps to defend themselves on this vexatious issue involving location savings and location saving advantages. It is prudent for the taxpayers to maintain robust TP documentation and undertake a detailed FAR (functions, assets, risks) analysis to support the commercial conduct, competitive forces, and relative bargaining power of the parties to the transaction.

6. Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting This document contains revised standards for transfer pricing documentation and a template for country-by-country reporting of income, earnings, taxes paid and certain measures of economic activity. The country-by-country report (CbCR) requires MNEs to report annually and for each tax jurisdiction in which they do business the amount of revenue, profit before income tax and income tax paid and accrued. The guidance on transfer pricing documentation requires MNEs to provide tax administrations high-level global information regarding their global business operations and transfer pricing policies in a “master file” that would be available to all relevant country tax administrations. It also requires that more transactional transfer pricing documentation be provided in a local file in each country, identifying relevant related party transactions, the amounts involved in those transactions, and the company‟s analysis of the transfer pricing determinations they have made with regard to those transactions. These three documents will require taxpayers to articulate consistent transfer pricing positions, will provide tax administrations with useful information to assess transfer pricing risks, make determinations about where audit resources can most effectively be deployed, and, in the event audits are called for, provide information to commence and target audit enquiries. Concerns regarding confidentiality of this data and the potential for adjustments by tax administrations based on a formulary apportionment approach leading to many more transfer pricing controversies, have been raised The specific content of the various documents reflects an effort to balance tax administration information needs, concerns about inappropriate use of the information, and the compliance costs and burdens imposed on business. Some countries would strike that balance in a different way by requiring reporting in the country-by-country report of additional transactional data (beyond that available in the master file and local file for transactions of entities operating in their jurisdictions) regarding related party interest payments, royalty payments and especially related party service fees. Additional work will be undertaken by the OECD over the next months with respect to implementation and filing of the master file and the CbCR. The Transfer Pricing Documentation and CbCR states that “due regard will be given to considerations related to protection of the confidentiality of the information required by the reporting standards, the need for making the information available on a timely basis to all relevant countries,

19

and other relevant factors.” Guidance in this respect is expected to be delivered in early 2015.

Current Indian Scenario and Way forward:

Transfer pricing provisions in India have evolved over the years to reach a level where

legislations like Dispute Resolution Panel (DRP) and Advanced Pricing Agreements (APA)

have been introduced.

Currently, the taxpayers in India are justifying the arms length price of their transactions

based on the TP documentation which they are required to maintain in accordance with the

provisions of rule 10D of the Act. Further during the course of assessment proceedings the

taxpayer needs to provide certain additional information other than those specified in Form

10D, as desired by the Assessing officer inorder to enable him determine the ALP for the

transaction.

Presently, the TP documentation maintained by taxpayers in India are in line with the local

file template recommended by the OECD. Thus, the adaption of the recommended

documentation as proposed by the OECD would not be very burdensome for the Indian

taxpayer. On perusal of the executive summary of the report, it can be noted that country by

country reporting for some countries like India would require reporting of additional

transactional data.

The OECD guidance may lead to the demand by the tax authorities for the master file and

the CbCR maintained by the headquarter of the MNE. Hence the tax payer would need to be

extremely cautious while preparing these documents and would also need to adopt for a co-

ordinated approach. The documentation would also be referred by the Indian tax authorities

for reviewing the global value chain of an MNE as prevalent from the master file and CbC

report so as to assess whether the transfer pricing outcome to the Indian affiliate is

consistent with value creation in India.

It is also relevant to note that the Guidance allows the taxpayer to update the comparable

companies in the local file once in three years, whereas the Indian TP Regulations require

the taxpayer to update the comparable companies in the TP documentation annually.

However, the Finance Bill 2014 provides companies with a benefit to use multi-year data,

comprising the data of comparable companies pertaining to a period not more than two

years prior to the relevant financial year.

On a positive front India is quite open to the liberal use of the exchange of information

protocol in its treaties and the formal ability to extract portions of the Master File and the

use of such information at the local level is likely to be exploited by the Indian Revenue

Authorities to keep BEPS at bay. Therefore, the documentation action is one item where

20

there would need to be more definitive rules defined in terms of the proposed multilateral

instrument that would curtail the access to the Master File or other Local File to only

relevant information, so that the confidentiality of potentially sensitive information is

maintained.

From the above recommendations, it can be inferred that the OECD guidance will enable the

tax authorities to scrutinize the business structures more closely and the onus will be wholly

on the MNEs to provide evidence of commercial substance.

7. Action 15: Developing a Multilateral Instrument to Modify Bilateral Tax Treaties

The BEPS Action Plan considered whether a multilateral instrument (i.e., a treaty or convention signed by multiple countries) could be used as an alternative to separately amending more than 3,000 bilateral tax treaties in a more timely and efficient manner. The 2014 BEPS Package includes a report on Developing a Multilateral Instrument to Modify Bilateral Tax Treaties (the Multilateral Instrument Report) in response to this action item. The Multilateral Instrument Report concludes that a multilateral instrument is (a) feasible, based on non-tax precedents; and (b) desirable, to ensure the sustainability of the consensual framework to eliminate double taxation on cross-border trade and investment. The Multilateral Instrument Report refers to the desire to use a multilateral instrument to address BEPS in a targeted and synchronized manner. While the Report focuses on implementing treaty measures, a multilateral instrument could potentially also be used to express commitments to implement certain domestic law measures. In an effort to expedite and streamline the implementation of BEPS initiatives and amending tax treaties, an international convention to begin negotiations for a multilateral instrument will be convened in 2015. The negotiating mandate is to be limited in scope (implementing the BEPS Action Plan) and in time (no more than two years). While many of the details will need to be confirmed, the multilateral instrument would likely coexist with existing bilateral treaty networks. The multilateral instrument could modify (or add) a limited number of provisions common to most existing bilateral tax treaties, including new provisions specifically designed to counter BEPS.

The CFA will consider a draft mandate for negotiation of the multilateral instrument in

January 2015.

Current Indian Scenario and Way forward:

In the current Indian scenario the concept of a multilateral instrument is not a very popular

one in the field of tax treaties though the same is prevalent in the areas of trade and

commerce.

Multilateral instrument appears to be a practical solution approach since it would be

cumbersome for the government to renegotiate all its tax treaties. The concept of

multilateral instrument would ensure consistency in the adoption of the article on exchange

of information rather than interpretational issues arising on account of various clauses in

different tax treaties.

21

Further the right of obtaining information by the introduction of the above clause puts the tax

payer under the scanner and inculcates in him a sense of caution as he would perceive a threat of

enquires being initiated in regard to his every action. However, this also puts a responsibility on

the Authorities to maintain the confidentiality of the data shared with them in course of the above

proceedings. In the Indian tax regime, maintaining confidentiality would be a difficult issue

especially in the context of the advance pricing agreement and MAP proceedings wherein the

confidentiality of information is not guaranteed.

Conclusion: The issues surrounding BEPS are universal in the generic sense as it applies to all countries around the world. Some issues, however, might be limited to regional regimes based on certain chief characteristics of transactional structuring or tax administrations. India's concerns to the issue of BEPS is primarily two fold, i.e., safeguarding its own revenue interests with respect to profit shifting by Indian multinationals and effectiveness of the tax administration to check (and recover) taxation revenues from cross-border and offshore transactions having an integral connection to India.

Developments in the next 24 months would be closely watched as many countries would be gearing up for cleaning up their domestic law to address the G2o expectations. The coming year is also going to be one where the Action Points are far more quarrelsome, and which may prove to be difficult so as to move towards a common outcome.

The implementation would require greater degree of cooperation between tax administrators and alignment of tax regulations, particularly the ones that affect cross border movement of goods and services. It is anticipated that the G20 would work closely with the tax payer community and address vexed issues such that the functioning of business is not impacted and there is free flow of trade, investment and services.

This is of particular significance for India where MNC's have been at the receiving end and are craving for certainty, transparency and timely resolution of disputes. MNC‟s are also aware that the project could produce very costly outcomes for them, and they are mobilized to lobby against some of the outcomes. This is an opportunity for BRIC's countries, particularly India to embrace a host of new principles which would entail raising the level of compliance and disputes resolution. How the different jurisdictions will collaborate to affect the action plan, will undoubtedly depend upon each government‟s political and economic compulsions and their consequent willingness to understand the other‟s laws. Needless to add, adopting countries would be required to first settle their domestic challenges before getting on to an international bandwagon to circumvent BEPS.

22

Annexure A: OECD Calendar for Planned BEPS Deliverables

Sr. No.

Issue Expected Output Deadline

1. Address the tax challenges of the digital economy

Supplementary Report on challenges identified by the Task Force

December, 2015

2. Neutralise the effects of hybrid mismatch arrangements

Commentary on the new provisions relating to income of transparent entities

September , 2015

3. Strengthen CFC rules Recommendations regarding design of Domestic Law and rules

September, 2015

4. Limit base erosion via interest deductions and other financial payments

Recommendations regarding design of Domestic rules.

Changes to the Transfer Pricing Guidelines

September, 2015 December 2015

5. Counter harmful tax practices more effectively, taking into account transparency and substance

Strategy to expand participation to non-OECD member countries.

Consideration of revisions or additions to the existing framework.

September, 2015 December, 2015

6. Prevent Treaty Abuse Final Model provisions and related commentary.

September, 2015

7. Prevent the artificial avoidance of PE status

Changes to the Model Tax Convention.

September, 2015

8. Assure that transfer pricing outcomes are in line with value creation: Intangibles

Revisions to portions of Chapters I, II, VI, VIII, and IX of the Guidelines.

Finalising the bracketed and shaded portions of the 2014 draft.

Changes to the Transfer pricing Guidelines.

September, 2015

9 Assure that transfer pricing outcomes are in line with value creation: Risks and capital

Changes to Transfer Pricing Guidelines and possibly to Model Tax Convention.

September, 2015

10 Assure that transfer pricing Changes to Transfer Pricing September, 2015

23

outcomes are in line with value creation: Other high-risk transactions

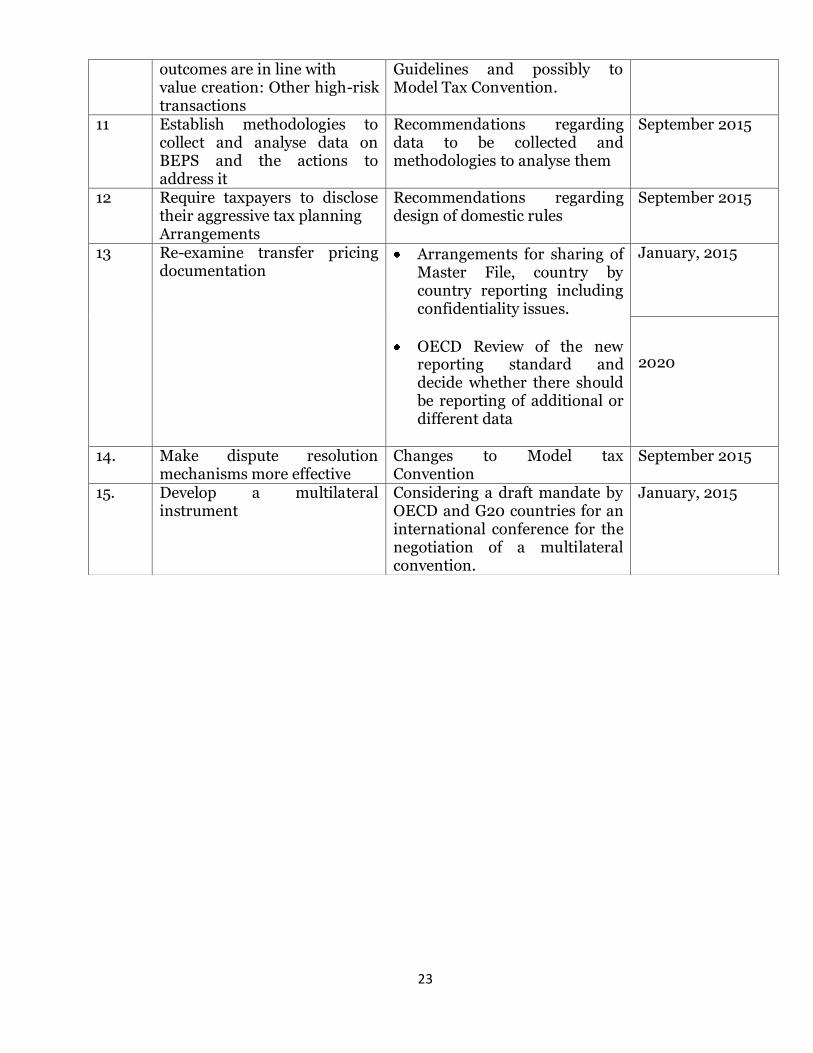

Guidelines and possibly to Model Tax Convention.

11 Establish methodologies to collect and analyse data on BEPS and the actions to address it

Recommendations regarding data to be collected and methodologies to analyse them

September 2015

12 Require taxpayers to disclose their aggressive tax planning Arrangements

Recommendations regarding design of domestic rules

September 2015

13 Re-examine transfer pricing documentation

Arrangements for sharing of Master File, country by country reporting including confidentiality issues.

OECD Review of the new reporting standard and decide whether there should be reporting of additional or different data

January, 2015 2020

14. Make dispute resolution mechanisms more effective

Changes to Model tax Convention

September 2015

15. Develop a multilateral instrument

Considering a draft mandate by OECD and G20 countries for an international conference for the negotiation of a multilateral convention.

January, 2015