Embed Size (px)

Citation preview

UNDERSTANDING INDEX OPTIONS

The Options Industry Council(OIC) is an industry cooperativecreated to educate the investing

public and brokers about the benefits and risks of exchange-tradedoptions. Options are a versatile but complex product and that is whyOIC conducts seminars, distributes educational software andbrochures, and maintains a web site focused on options education.

All seminars are taught by experienced options instructors who provide valuable insight on the challenges and successes that indi-vidual investors encounter when trading options. In addition, thecontent in our software, brochures and web site has been created by options industry experts. All OIC-produced information hasbeen reviewed by appropriate compliance and legal staff to ensurethat both the benefits and risks of options are covered.

OIC was formed in 1992. Today, its sponsors include BATSOptions Exchange, BOX Options Exchange, Chicago BoardOptions Exchange, C2 Options Exchange, International SecuritiesExchange, Miami International Securities Exchange, LLC, NASDAQ OMX PHLX , NASDAQ Options Market, NYSEAmex Options, NYSE Arca Options and OCC. These organiza-tions have one goal in mind for the options investing public: to pro-vide a financially sound and efficient marketplace where investorscan hedge investment risk and find new opportunities for profitingfrom market participation. Education is one of many areas thatassist in accomplishing that goal. More and more individuals areunderstanding the versatility that options offer their investmentportfolio, due in large part to the industry’s ongoing educational efforts.

Table of Contents

Introduction 3

Benefits of Listed Index Options 5

What Is an Index? 7

Equity vs. Index Options 9n Pricing Factorsn Underlying Instrumentn Volatilityn Riskn Cash Settlementn Purchasing Rightsn Option Classesn Strike Pricen In-the-money, At-the-money,

Out-of-the-moneyn Premiumn American vs. European Exercisen AM and PM Settlementn Exercise and Assignmentn Exercise Settlementn Closing Transactions

Basic Strategies 15n Buying Index Callsn Buying Index Puts

Index Options Glossary 21

For More Information 26

1

This publication discusses exchange-traded optionsissued by The Options Clearing Corporation. Nostatement in this publication is to be construed as arecommendation to purchase or sell a security, or toprovide investment advice. Options involve risk andare not suitable for all investors. Prior to buying orselling an option, a person must receive a copy ofCharacteristics and Risks of Standardized Options.Copies of this document may be obtained from yourbroker, by calling 1-888-OPTIONS, or by visitingwww.OptionsEducation.org.

2013

2

Introduction

The purpose of this booklet is to provide an intro-ductory understanding of index options and howthey can be used. Index options may be listed on allU.S. option exchanges. Like trading in stocks,options trading is regulated by the Securities andExchange Commission (SEC).

Options exchanges seek to provide competi-tive, liquid and orderly markets for the purchase andsale of standardized options. All option contractstraded on U.S. securities exchanges are issued, guar-anteed and cleared by OCC. OCC is a registeredclearing corporation with the SEC and plays a criti-cal role in the U.S. capital markets as the exclusiveclearinghouse for exchange-traded options. OCC’sconservative financial and procedural safeguards,substantial and readily available financial resources,and its members’ mutual incentives protect theorganization from settlement losses.

As referred to in this booklet, an index is ameasure of the prices of a group of securities orother interests. Although indexes have been devel-oped to cover a variety of interests such as stocksand other equity securities, debt securities and for-eign currencies, and even to measure the cost of liv-ing, indexes on equity securities (which are calledstock indexes) are among the most familiar. The fol-lowing discussion refers only to stock indexes andstock index options.

Stock indexes are compiled and published byvarious sources, including securities markets. Anindex may be designed to be representative of thestock market of a particular nation as a whole, secu-rities traded in a particular market, a broad marketsector (e.g., industrials) or a particular industry (e.g.,electronics). An index may be based on the prices ofall or only a sample of the securities whose prices itis intended to represent. Indexes may be based onsecurities traded primarily in U.S. markets, securi-

3

ties traded primarily in a foreign market or a combi-nation of securities whose primary markets are invarious countries.

Readers who intend to trade index optionsshould familiarize themselves with the features ofthe underlying indexes*, including the general meth-ods of calculation. Readers who are attempting tofollow a precise and sophisticated strategy involvingindex options may wish to inform themselves aboutthe exact method for calculating each indexinvolved. Information regarding the method of cal-culation of any index on which options are traded,including information concerning the standardsused in adjusting the index, adding or deleting secu-rities and making similar changes is generally avail-able from the options market where the options are traded.

While this discussion will focus on generalcharacteristics of index options, specific classes ofindex options can have slightly different productspecifications. Before investing, you should deter-mine the specific terms of each product class. Thisand other information on index options or optionproducts not included in this booklet can beobtained by contacting the appropriate exchange orThe Options Industry Council (OIC). In addition,OCC publishes a booklet, Understanding EquityOptions, which covers the basics of exchange-listedequity options and is recommended to investorscontemplating the use of index options. This book-let can also be obtained either by callingI-888-OPTIONS or by visiting OIC’s web site,www.OptionsEducation.org.

This introductory booklet should be read inconjunction with the basic options disclosure docu-ment, Characteristics and Risks of StandardizedOptions, which outlines the purposes and risks oflisted options transactions. Despite their many ben-efits, options are not suitable for all investors.

Individuals should not enter into optiontransactions until they have read and understood the

4

*Definitions for italicized words in bold can be found in theglossary section of this booklet.

risk disclosure document which can be obtainedfrom their broker, by calling 1-888-OPTIONS, orby visiting www.OptionsEducation.org. It must benoted that despite the efforts of each exchange toprovide liquid markets, under certain conditions itmay be difficult or impossible to liquidate an optionposition. Please refer to the disclosure document forfurther discussion on this risk and other risks oftrading index options. In addition, margin require-ments, transaction and commission costs and taxramifications of buying or selling options should bediscussed thoroughly with a broker and/or tax advi-sor before engaging in option transactions.Note: For the sake of simplicity, the calculations of profitand loss amounts in this booklet do not account for theimpact of commissions, transaction costs and taxes.

Benefits of Listed Index Options

Like equity options, index options offer the investor anopportunity either to capitalize on an expected marketmove or to protect holdings in the underlying instru-ments. The difference is that the underlying instru-ments are indexes. These indexes can reflect the char-acteristics of either the broad equity market as a wholeor specific industry sectors within the marketplace.

Diversification

Index options enable investors to gain exposure to themarket as a whole or to specific segments of the mar-ket with one trading decision and frequently with onetransaction. To obtain the same level of diversifica-tion using individual stock issues or individual equityoption classes, numerous decisions and transactionswould be required. Employing index options candefray both the costs and complexities of doing so.

Predetermined Risk for Buyer

Unlike other investments where the risks may have

5

no limit, index options offer a known risk to buyers.An index option buyer absolutely cannot lose morethan the price of the option, the premium.

Leverage

Index options can provide leverage. This means anindex option buyer can pay a relatively small premi-um for market exposure in relation to the contractvalue. An investor can see large percentage gainsfrom relatively small, favorable percentage moves inthe underlying index. If the index does not move asanticipated, the buyer's risk is limited to the premi-um paid. However, because of this leverage a smalladverse move in the market can result in a substan-tial or complete loss of the buyer's premium.Writers of index options can bear substantiallygreater, if not unlimited, risk.

Guaranteed Contract Performance

An option holder is able to look to the system creat-ed by OCC's By-Laws and Rules rather than to anyparticular option writer for performance. Throughthat system, OCC guarantees performance to sell-ing and purchasing clearing members, eliminatingcounterparty credit risk. Prior to the existence ofoption exchanges and OCC, an option holder whowanted to exercise an option depended on the ethi-cal and financial integrity of the writer or his bro-kerage firm for performance. Furthermore, therewas no convenient means of closing out one's posi-tion prior to the expiration of the contract.

OCC, as the common clearing entity for allexchange-traded option transactions, resolves thesedifficulties. Once OCC is satisfied that there arematching trades from a buyer and a seller, it seversthe link between the parties. In effect, OCC becomesthe buyer to the seller and the seller to the buyer. Asa result, the seller can buy back the same option hehas written, closing out the initial transaction andterminating his obligation to deliver the cash equal tothe exercise value of the option to OCC, and this willin no way affect the right of the original buyer to sell,

6

hold or exercise his option. All premium and settle-ment payments are made between OCC and itsclearing members. In turn, OCC clearing memberssettle independently with their customers (or brokersrepresenting customers).

What Is an Index?

A stock index is a compilation of several stock pricesinto a single number. Indexes come in various shapesand sizes. Some are broad-based and measure movesin broad, diverse markets. Others are narrow-basedand measure more specific industry sectors of themarketplace. Different stock indexes can be calculat-ed in different ways. Accordingly, even where index-es are based on identical securities, they may measurethe relevant market differently because of differencesin methods of calculation.

Capitalization-Weighted

An index can be constructed so that weightings arebiased toward the securities of larger companies, amethod of calculation known as capitalization-weighted. In calculating the index value, the marketprice of each component security is multiplied by thenumber of shares outstanding. This will allow asecurity's size and capitalization to have a greaterimpact on the value of the index.

Equal Dollar-Weighted

Another type of index is known as equal dollar-weighted and assumes an equal number of shares ofeach component stock. This index is calculated byestablishing an aggregate market value for everycomponent security of the index and then deter-mining the number of shares of each security bydividing this aggregate market value by the currentmarket price of the security. This method of calcula-

7

tion does not give more weight to price changes ofthe more highly capitalized component securities.

Other Types

An index can also be a simple average: calculated bysimply adding up the prices of the securities in theindex and dividing by the number of securities, dis-regarding numbers of shares outstanding. Anothertype measures daily percentage movements of pricesby averaging the percentage price changes of allsecurities included in the index.

Adjustments & Accuracy

Securities may be dropped from an index because ofevents such as mergers and liquidations or because aparticular security is no longer thought to be repre-sentative of the types of stocks constituting theindex. Securities may also be added to an index from time to time. Adjustments to indexes might bemade because of such substitutions or due to theissuance of new stock by a component security.Such adjustments and other similar changes arewithin the discretion of the publisher of the indexand will not ordinarily cause any adjustment in theterms of outstanding index options. However, anadjustment panel has authority to make adjustmentsif the publisher of the underlying index makes achange in the index's composition or method of cal-culation that, in the panel's determination, maycause significant discontinuity in the index level.

Finally, the reported level of a stock index willbe accurate only to the extent that:n the component securities in the index are being

tradedn the prices of these securities are being promptly

reportedn the market prices of these securities, as measured

by the index, reflect price movements in the relevant markets

8

Equity vs. Index Options

An equity index option is an option whose underly-ing instrument is intangible - a stock index. Themarket value of an index put and call tends to riseand fall in relation to the underlying index. Theprice of an index call will generally increase as thelevel of its underlying index increases, and its pur-chaser has unlimited profit potential tied to thestrength of these increases. The price of an indexput will generally increase as the level of its underly-ing index decreases, and its purchaser has substan-tial profit potential tied to the strength of thesedecreases.

Pricing Factors

Generally, the factors that affect the price of anindex option are the same as those affecting theprice of an equity option: value of the underlyinginstrument (an index in this case), strike price,volatility, time until expiration, interest rates anddividends paid by the component securities.

Underlying Instrument

The underlying instrument of an equity option is anumber of shares of a specific stock, usually 100shares. Cash-settled index options do not relate to aparticular number of shares. Rather, the underlyinginstrument of an index option is usually the value ofthe underlying index of stocks times a multiplier,which is generally $100. (All references to dollarsin this booklet refer to U.S. dollars.)

Volatility

Indexes, by their nature, are less volatile than theirindividual component stocks. The up and downmovements of component stock prices tend to can-cel one another out, lessening the volatility of theindex as a whole. However, the volatility of an indexcan be influenced by factors more general than can

9

affect individual equities. These can range frominvestors' expectations of changes in inflation,unemployment, interest rates or other economicindicators issued by the government and political ormilitary situations.

Risk

As with an equity option, an index option buyer'srisk is limited to the amount of the premium paidfor the option. The premium received and kept bythe index option writer is the maximum profit awriter can realize from the sale of the option.However, the loss potential from writing an uncov-ered index option is generally unlimited. Anyinvestor considering writing index options shouldrecognize that there are significant risks involved.

Cash Settlement

The differences between equity and index optionsoccur primarily in the underlying instrument andthe method of settlement. Generally, when an indexoption is exercised by its holder, and when an indexoption writer is assigned, the exercise settlementamount (of cash) will change hands. This is knownas cash settlement.

Purchasing Rights

Purchasing an index option does not give theinvestor the right to purchase or sell all of the stocksthat are contained in the underlying index. Becausean index is simply an intangible, representativenumber, you might view the purchase of an indexoption as buying a value that changes over time asmarket sentiment and prices fluctuate.

An investor purchasing an index optionobtains certain rights per the terms of the contract.In general, this includes the right to exercise andreceive a specified amount of cash from the writerof a contract with the same terms (if the contract isin-the-money).

10

Option Classes

Available strike prices, expiration months and thelast trading day can vary with each index optionclass, a term for all option contracts of the same type (call or put) and style (American or European)that cover the same underlying index. To determinethe contract terms for the option class(es) you wishto employ, please contact your brokerage firm.

Strike Price

The strike price, or exercise price, of a cash-settledoption is the basis for determining the amount ofcash, if any, that the option holder is entitled toreceive upon exercise.

In-the-money, At-the-money,

Out-of-the-money

An index call option is in-the-money when its strikeprice is less than the reported level of the underly-ing index. It is at-the-money when its strike price isthe same as the level of that index and out-of-the-money when its strike price is greater than that level.

An index put option is in-the-money when itsstrike price is greater than the reported level of theunderlying index. It is at-the-money when its strikeprice is the same as the level of that index and out-of-the-money when its strike price is less than that level.

Premium

Premiums for index options are quoted like thosefor equity options, in points and decimal amounts,with one point ordinarily equaling $100. For exam-ple, a quoted premium of $1.00 equals $100, $1.25equals $125, $1.50 equals $150, $2.00 equals $200,etc. An index option buyer will generally pay a totalof the quoted premium amount times a multiplier of$100 for the contract. The writer, on the otherhand, will receive and keep this amount.

The amount by which an index option is in-the-money is called its intrinsic value. Any amountof premium in excess of intrinsic value is called an

11

option's time value. As with equity options, timevalue is affected by changes in volatility, time untilexpiration, interest rates and dividend amounts paidby the component securities of the underlying index.

American vs. European Exercise

Although equity option contracts generally haveonly American-style expirations, index options canhave either American- or European-style.

In the case of an American-style option, theholder of the option has the right to exercise it on orat any time before its expiration date. Otherwise, the option will expire worthless and cease to exist asa financial instrument. It follows that the writer ofan American-style option can be assigned at anytime, either at or before the option’s expiration,although early assignment is not always predictable.

A European-style option is one that can onlybe exercised by its holder during a specified periodof time prior to its expiration, and this period mayvary with different classes of index options. Thewriter of a European-style option can be assignedonly during this same period. (As of the date of thisbooklet, every European-style index option tradedon options exchanges in the US can be exercised,and assignment made, only on its expiration date.)

AM & PM Settlement

The exercise settlement values of equity indexoptions are determined by their reporting authoritiesin a variety of ways. The two most common are: n PM settlement - Exercise settlement values are

based on the reported level of the index calculatedwith the last reported prices of the index's compo-nent stocks at the close of market hours on theday of exercise.

n AM settlement - Exercise settlement values arebased on the reported level of the index calculatedwith the opening prices of the index's componentstocks on the day of exercise.

If a particular component security does not open fortrading on the day the exercise settlement value is

12

determined, the last reported price of that security isused.

Investors should be aware that the exercise set-tlement value of an index option that is derivedfrom the opening prices of the component securitiesmay not be reported for several hours following theopening of trading in those securities. A number ofupdated index levels may be reported at and afterthe opening before the exercise settlement value isreported. There could be a substantial divergencebetween those reported index levels and the report-ed exercise settlement value.

Exercise & Assignment

The exercise settlement value is an index value usedto calculate how much money will change hands, theexercise settlement amount, when a given indexoption is exercised, either before or at expiration.The value of every index underlying an option,including the exercise settlement value, is the valueof the index as determined by the reporting authori-ty designated by the market where the option istraded. Unless OCC directs otherwise, the valuedetermined by the reporting authority is conclusivelypresumed to be accurate and deemed to be final forthe purpose of calculating the exercise settlementamount.

If the holder of an index option decides toexercise his right to be paid the exercise settlementamount, he must direct his broker (if an OCC clear-ing member) to submit an exercise notice to OCC. Inorder to ensure that an index option is exercised on aparticular day before expiration, the holder mustnotify his broker before the broker’s cut-off time foraccepting exercise instructions on that day. On thelast trading day for the option, the cut-off time forexercise may be different from that for an early exer-cise (before expiration).Note: Different firms may have different cut-off times foraccepting exercise instructions from customers, and thosecut-off times may be different for different classes ofoptions. In addition, the cut-off times for index optionsmay be different from those for equity options.

13

OCC will then assign this exercise notice to one ormore clearing members with short positions in thesame series in accordance with its established proce-dures. If the exercise is assigned to a clearing mem-ber’s customers’ account, the clearing member will,in turn, allocate the exercise to one or more of itscustomers (either randomly or on a first in first outbasis) who hold short positions in that series. Uponassignment of the exercise notice, the writer of theindex option has the obligation to pay the exercisesettlement amount. Settlement and the resultingtransfer of cash generally occur on the next businessday after exercise. Note: Firms may require their customers to notify thefirm of the customer's intention to exercise, even if anoption is in-the-money. You should ask your firm tothoroughly explain its exercise procedures, including anydeadline your firm may have for exercise instructions onthe last trading day before expiration.

Exercise Settlement

The amount of cash received upon exercise of anindex option or when it expires depends on theexercise settlement value of the underlying index incomparison to the strike price of the index option.The amount of cash changing hands is called theexercise settlement amount. This amount is calcu-lated as the difference between the strike price ofthe option and the level of the underlying indexreported as its exercise settlement value, in otherwords, the option's intrinsic value, and is generallymultiplied by $100. This calculation applies whetherthe option is exercised before or at its expiration.

In the case of a call, if the underlying indexvalue is above the strike price, the holder may exercisethe option and receive the exercise settlement amount.For example, with the settlement value of the indexreported as 79.55, the holder of a long call contractwith a 78 strike price would exercise and receive $155[(79.55 − 78) x $100 multiplier = $155]. The writer ofthe option would pay the holder this cash amount.

In the case of a put, if the underlying index

14

value is below the strike price, the holder may exer-cise the option and receive the exercise settlementamount. For example, with the settlement value ofthe index reported as 74.88, the holder of a long putcontract with a 78 strike price would exercise andreceive $312 [(78 − 74.88) x $100 multiplier =$312]. The writer of the option would pay the hold-er this cash amount.

Closing Transactions

As with equity options, an index option writerwishing to close out his position buys a contractwith the same terms in the marketplace. Providedthat an exercise notice has not been assigned, anindex option writer may effect a closing transactionin order to terminate his obligations. To close out along position, the purchaser of an index option mayeither sell the contract in the marketplace or exer-cise it if profitable to do so.

Basic Strategies

The versatility of index options stems from the vari-ety of strategies available to the investor. The mostbasic uses of index options are explained in the fol-lowing examples. These examples are based onhypothetical situations and should only be consid-ered as examples of potential trading approaches.Other strategies that might be used with equityoptions, such as spreads and straddles, can beemployed with index options. For more detailedexplanations, contact your brokerage firm or theexchanges where index options are traded. Note: For purposes of illustration, commission and trans-action costs, tax considerations and the costs involved inmargin accounts have been omitted from the examples inthis booklet. These factors will affect a strategy's potentialoutcome, so always check with your brokerage firm

15

and tax advisor before entering into any of these strate-gies. The index option positions in all of the followingexamples are shown to be held until expiration. The pre-miums are intended to be reasonable, but in reality willnot necessarily exist at or prior to expiration for a simi-lar option.

Buying Index CallsLong Index Call

Market outlook: Bullish over the short termGoal: Positioning to profit from an increase in the

level of the underlying indexYou are anticipating an advance in the broad marketor market sector measured by the underlying indexin the near future. You want to take an aggressiveposition that can provide a great deal of leverage.This decision is made with the understanding thatthere is a possibility you may lose the entire premi-um you pay for the option.

An index call option gives the purchaser theright to participate in underlying index gains abovea predetermined strike price until the optionexpires. The purchaser of an index call option hasunlimited profit potential tied to the strength ofadvances in the underlying index.

ScenarioAssume the underlying index that interests you issymbolized as XYZ and is currently at a level of200. You decide to purchase a 6-month XYZ 205call for a quoted price of $4.75 per contract. Your

16

Profit

0

BEP209.75

205

Max Loss

–$475

Index LevelLower Higher

net cost for this call is $475 ($4.75 x $100 multipli-er). You are risking $475 if the underlying indexlevel is not above the strike price of 205 when theXYZ call expires. The break-even point (BEP) atexpiration is an XYZ index level of 209.75 (strikeprice 205 + premium paid $4.75) because the callwill be worth its intrinsic value of $4.75, which iswhat you originally paid for it. The higher the XYZindex settlement value is above the break-even pointat expiration, the greater your profit.

Possible Outcomes at Expiration1. XYZ index level above the break-even

point (209.75):If at expiration XYZ index has advanced to 215, theXYZ 205 call will be worth its intrinsic value of $10(settlement value 215 − strike price 205). Your netprofit in this case would be $525 (settlementamount $1000 received from exercise − net cost ofcall $475).

Buy XYZ Index 205 Call at $4.75

with Index at 200

Net Cost for Call = $475

*Exclusive of commissions, transaction costs and taxes.

2. XYZ index level between strike price (205) andbreak-even point (209.75):

If at expiration XYZ index has advanced to 207,

17

Level of XYZ index at expiration

XYZ indexdeclines

to 198(below strike)

XYZ indexadvances

to 207(betweenstrike and

BEP)

XYZ indexadvances

to 215(above BEP)

Move in level of index

-2 pts. +7 pts. +15 pts.

Value of call at expiration(per contract)

0(out-of-the

money)

$2 $10

Less premium paidfor call(per contract)

$4.75 $4.75 $4.75

Net profit/loss*(per contract x $100)

-$475 -$275 +$525

the XYZ 205 call will be worth its intrinsic valueof $2 (settlement value 207 − strike price 205). You could exercise the option and receive the set-tlement amount of $200 ($2 intrinsic value x $100multiplier). This amount would be less than thenet amount paid for the call ($475), but it wouldoffset some of that cost. The net loss in this casewould be $275 (net cost of call $475 − settlementamount $200 received from exercise). This lossrepresents a little more than half of your initialinvestment.

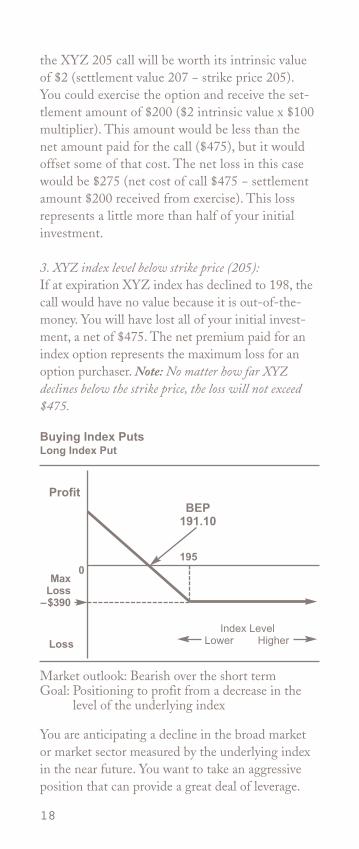

3. XYZ index level below strike price (205):If at expiration XYZ index has declined to 198, thecall would have no value because it is out-of-the-money. You will have lost all of your initial invest-ment, a net of $475. The net premium paid for anindex option represents the maximum loss for anoption purchaser. Note: No matter how far XYZdeclines below the strike price, the loss will not exceed$475.

Buying Index PutsLong Index Put

Market outlook: Bearish over the short termGoal: Positioning to profit from a decrease in the

level of the underlying index

You are anticipating a decline in the broad marketor market sector measured by the underlying indexin the near future. You want to take an aggressiveposition that can provide a great deal of leverage.

18

Profit

0

Loss

Max Loss

–$390

BEP191.10

195

Index LevelLower Higher

This decision is made with the understanding thatthere is a possibility you may lose the entire premi-um you pay for the option.

An index put option gives the purchaser theright to participate in underlying index declinesbelow a predetermined strike price until the optionexpires. The purchaser of an index put option hassubstantial profit potential tied to the degree ofdeclines in the underlying index.

ScenarioAssume the underlying index that interests you issymbolized as XYZ and is currently at a level of200. You decide to purchase a 6-month XYZ 195put for a quoted price of $3.90 per contract. Yournet cost for this call is $390 ($3.90 x $100 multipli-er). You are risking $390 if the underlying indexlevel is not below the strike price of 195 when theXYZ put expires. The break-even point (BEP) atexpiration is an XYZ index level of 191.10 (strikeprice 195 − premium paid $3.90) because the putwill be worth its intrinsic value of $3.90, which iswhat you originally paid for it. The lower the XYZindex settlement value is below the break-evenpoint at expiration, the greater your profit.

Possible Outcomes at Expiration1. XYZ index level below the break-even point

(191.10):If at expiration XYZ index has declined to 185, theXYZ 195 put will be worth its intrinsic value of $10(strike price 195 − settlement value 185). Your netprofit in this case would be $610 (settlementamount $1000 received from exercise − net cost ofput $390).

2. XYZ index level between strike price (195) andbreak-even point (191.10):

If at expiration XYZ index has declined to 193,the XYZ 195 put will be worth its intrinsic valueof $2 (strike price 195 − settlement value 193).You could exercise the option and receive the

19

settlement amount of $200 ($2 intrinsic value x$100 multiplier). This amount would be less thanthe net amount paid for the put ($390), but it wouldoffset some of that cost. The net loss in this casewould be $190 (net cost of put $390 − settlementamount $200 received from exercise). This loss repre-sents a little less than half of your initial investment.

3. XYZ index level above strike price (195):If at expiration XYZ index has advanced to 202, theput would have no value because it is out-of-the-money. You will have lost all of your initial invest-ment, a net of $390. The net premium paid for anindex option represents the maximum loss for anoption purchaser.Note: No matter how far XYZ advances above thestrike price, the loss will not exceed $390.

Buy XYZ Index 195 Put at $3.90 with Index at 200Net Cost for Put = $390

*Exclusive of commissions, transaction costs and taxes.

20

Level of XYZ index at expiration

XYZ indexadvances

to 202(above strike)

XYZ indexdeclines

to 193(betweenstrike and

BEP)

XYZ indexdeclines

to 185(below BEP)

Move in level of index

+2 pts. -7 pts. -15 pts.

Value of put at expiration(per contract)

0(out-of-the

money)

$2 $10

Less premium paidfor put(per contract)

$3.90 $3.90 $3.90

Net profit/loss*(per contract x $100)

-$390 -$190 +$610

Index Options Glossary

American-style option: An option contract thatmay be exercised at any time between the date ofpurchase and the expiration date.

AM settlement: A settlement style in which theexercise settlement values of options are based onthe reported level of the index derived from theopening prices of the component securities on theday of exercise.

Assignment (Assigned): The allocation of anexercise notice to an index option writer (seller) thatobligates him to pay (in the case of a call or put) thecash settlement amount for a particular index optionif it is exercised by its holder.

At-the-money: An index option is at-the-moneyif the strike price of the option is equal to the cur-rent level of the underlying index.

Broad-based index: An index that measuresmoves in broad, diverse markets. See Index.

Call: An index option contract that gives the holderthe right to receive, upon exercise of the option, thecash settlement amount for a fixed period of time.

Capitalization-weighted index: An equityindex constructed so that more highly capitalizedissues are weighted more heavily than the lesser-capitalized components. Changes in the stock priceof highly capitalized issues have a greater impact onthe index's value.

Cash settlement: The process by which theterms of an index option contract are fulfilledthrough the payment or receipt in dollars of theamount by which the option is in-the-money, asopposed to delivering or receiving the underlyinginstrument.

21

Class of options: Option contracts of the sametype (call or put) and style that cover the sameunderlying index.

Closing purchase: A transaction in which thepurchaser's intention is to reduce or eliminate ashort position in a given series of options.

Closing sale: A transaction in which the seller'sintention is to reduce or eliminate a long position ina given series of options.

Component securities: Securities whose pricesare used to calculate a given index.

Early exercise (or assignment): Exercise of anoption by its holder, or an assignment of an exercisenotice to an option writer, on a day before theoption expires.

Equal dollar-weighted index: An equity indexwhich assigns equivalent influence to each compo-nent stock by representing them in approximateequal-dollar amounts. These indexes are typicallyre-balanced to ensure that the components continueto have equal influence.

Equity index option: An option whose underly-ing instrument is an index. Generally, index optionsare cash-settled.

Equity options: Options on shares of an individ-ual common stock or exchange traded fund.

European-style option: An option contract thatmay be exercised only during a specified period oftime just prior to its expiration.

Exercise: To implement the right under which theholder of an option is entitled to receive (in the caseof a call or a put) the contract’s exercise settlementamount for a particular index option.

22

Exercise cut-off time: A deadline by which aninvestor must notify his brokerage firm, or a clear-ing member to notify OCC of intention to exercisea long option contract. An individual investor mustadhere to his brokerage firm's predetermined cut-off time.

Exercise notice: A notice submitted to OCC byclearing members to reflect their desire to exercisean option contract.

Exercise price: See Strike price.

Exercise settlement amount: The differencebetween the exercise price of the option and theexercise settlement value of the index on the day an exercise notice is tendered, multiplied by theindex multiplier.

Exercise settlement value: The price level of anunderlying equity index used to calculate the cashsettlement amount.

Expiration date: The day on which an option contract becomes void. All holders of options mustindicate their desire to exercise, if they wish to doso, by this date.

Expiration cut-off time: The time of day bywhich all exercise notices must be received on thelast trading day. An individual investor must adhereto his brokerage firm's predetermined cut-off time.

Holder: The purchaser of an option.

Index: A compilation of several stock prices into asingle number used as a benchmark against whichfinancial or economic performance is measured.

Index option: An option contract that has an equity index as its underlying instrument.

In-the-money: An index call option is in-the-money if the strike price is less than the currentlevel of the underlying index. An index put option is in-the-money if the strike price is greater thanthe current level of the underlying index.

23

Intrinsic value: The amount by which an option is in-the-money.

Long position: A position wherein an investor’sinterest in a particular series of options is as a netholder (i.e., the number of contracts bought exceedsthe number of contracts sold).

Margin requirement (for options): For cus-tomer level margin, the amount an option writer isrequired to deposit and maintain with his broker tocover a position. The margin requirement is calcu-lated daily.

Narrow-based index: An index that measuresspecific industry sectors of the marketplace. SeeIndex.

Opening purchase: A transaction in which thepurchaser’s intention is to create or increase a longposition in a given series of options.

Opening sale: A transaction in which the seller’sintention is to create or increase a short position in a given series of options.

Out-of-the-money: An index call option is out-of-the-money if the strike price is greater than thelevel of the underlying index. A put option is out-of-the-money if the strike price is less than the levelof the underlying index.

PM settlement: A settlement style in which the exercise settlement values of options are basedon the reported level of the index derived from the last reported prices of the component securitiesof the index at the close of market hours on the day of exercise.

Premium: The price of an option contract, asdetermined in the competitive marketplace, whichthe buyer of the option pays to the option writer for the rights conveyed by the option contract.

Put: An index option contract that gives the holderthe right to receive, upon exercise of the option, thecash settlement amount for a fixed period of time.

24

Sector: A distinct subset of a market, industry,or economy, whose components share similar characteristics.

Series: All options of the same class that have thesame strike price and expiration date.

Short position: A position wherein an investor’sinterest in a particular series of options is as a netwriter (i.e., the number of contracts sold exceeds thenumber of contracts bought).

Stock index option: See Equity index option

Strike price: The strike price (or exercise price) ofa cash-settled option is the base for the determina-tion of the amount of cash (exercise settlementamount), if any, that the option holder is entitled toreceive upon exercise.

Time value: The portion of the option premiumthat is attributable to the amount of time remaininguntil the expiration of the option contract. Timevalue is the amount of premium in excess of in -trinsic value.

Type: The classification of an option contract aseither a put or a call.

Underlying index: The equity index on which aclass of index options is based.

Volatility: A measure of the fluctuation in the pricelevel of the underlying index. Mathematically, volatil-ity is the annualized standard deviation of returns.

25

For More InformationBATS Options Exchange

www.batsoptions.com

BOX Options Exchange

www.bostonoptions.com

Chicago Board Options Exchange

www.cboe.com

C2 Options Exchange

www.c2exchange.com

International Securities Exchange

www.ise.com

Miami International Securities

Exchange, LLC

www.miaxoptions.com

NASDAQ OMX PHLX

www.nasdaqtrader.com

NASDAQ Options Market

www.nasdaqtrader.com

NYSE Amex Options

www.nyse.com

NYSE Arca Options

www.nyse.com

OCC

www.optionsclearing.com

The Options Industry Council

www.OptionsEducation.org

26

Notes

27

Notes

28