Embed Size (px)

Citation preview

FINANCIAL INSTITUTIONS

CREDIT OPINION12 October 2017

Update

RATINGS

Ulster Bank Ireland DACDomicile Dublin, Ireland

Long Term Debt Withdrawn

Type Senior Unsecured -Dom Curr

Outlook Not Assigned

Long Term Deposit Baa2

Type LT Bank Deposits - FgnCurr

Outlook Positive

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Roland Auquier 33-1-5330-3341AVP-Analyst/[email protected]

Maija Sankauskaite 44-20-7772-1092Associate [email protected]

Irakli Pipia 44-20-7772-1690VP-Sr Credit [email protected]

Laurie Mayers 44-20-7772-5582Associate [email protected]

Nick Hill [email protected]

Ulster Bank Ireland DACUpdate following affirmation of Baa2 rating; outlook changedto positive

SummaryOn 2 October 2017 we affirmed Ulster Bank Ireland DAC's (UBID) long-term deposit andissuer ratings at Baa2 and Baa3, respectively. The outlook on both ratings was changed topositive from stable. We also affirmed UBID's standalone BCA at ba1 and its adjusted BCAat baa3. The bank's Counterparty Risk Assessment (CR Assessment) was affirmed at A3(cr)/Prime-2(cr).

The rating action followed the 27 September 2017 rating action on the bank's parent, TheRoyal Bank of Scotland plc (RBS, A2/A3 negative, baa3), reflecting our view on the likelydirection of the group's subsidiaries' ratings, following the implementation of forthcomingring-fencing regulations. RBS is planning to transfer most of its Personal & Business Bankingand Commercial & Private Banking operations to a ring-fenced banking sub-group (underan intermediate holding company, NatWest Holdings Ltd, expected to become a directsubsidiary of The Royal Bank of Scotland Group plc (RBSG). UBID will become a part ofthe ring-fenced bank sub-group, which will also include National Westminster Bank PLC(NatWest Bank), Ulster Bank Limited (UBL, A2/A3 positive, baa3) and Adam & Company PLCand Coutts & Company.

The change in outlook on the ratings of UBID was driven by our expectation that UBID willremain an integral part of the ring-fenced banking sub-group, which will have a strongercredit profile as it will retain mostly retail and SME activities, and have a more deposit-basedfunding profile.

The bank’s BCA at ba1 incorporates: (1) the successful deleveraging measures undertaken bythe bank in order to restore its balance sheet, leading to a reduction of 81% in impaired loansto €3.7 billion (15.9% of gross loans) at December 2016 from the peak level of €19.2 billion(44.6% of gross loans) at December 2013; (2) very high capital levels, which will remainelevated despite our expectation of a decline over the outlook period following dividendpayments to RBS; (3) weak, but improving quality of earnings and pre-provision profitability;and (4) balanced funding profile and comfortable liquidity position.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

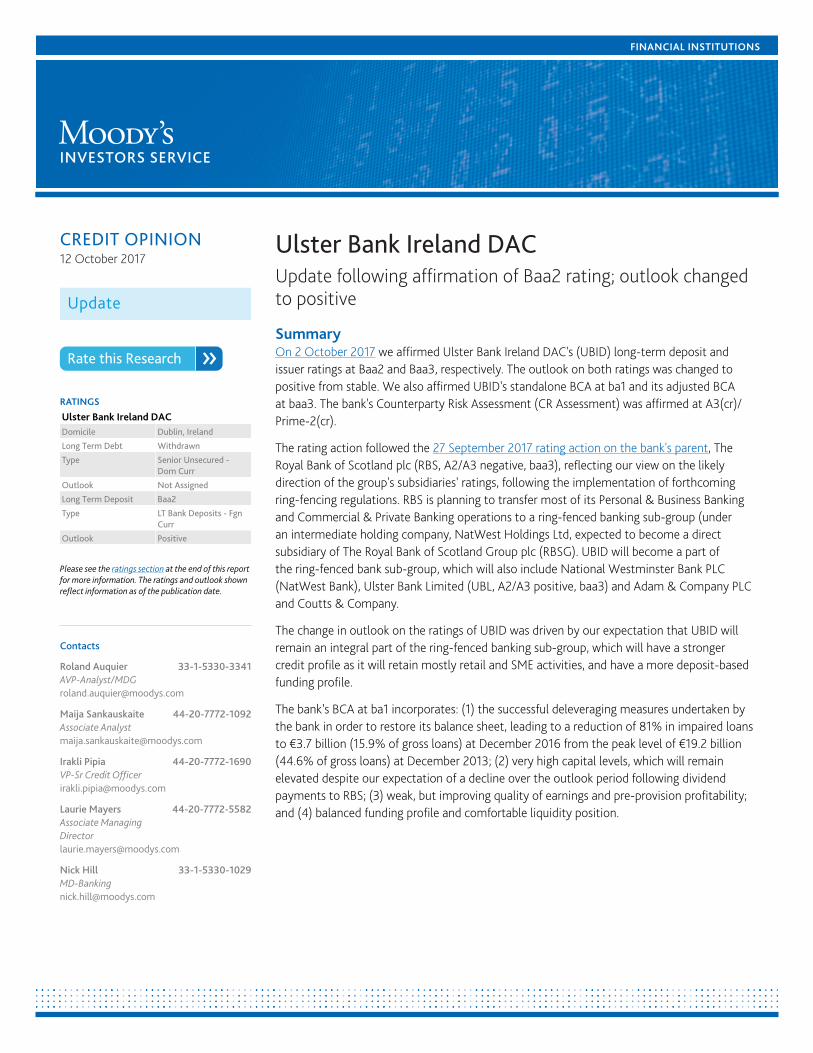

Exhibit 1

Key Financial Ratios

15.9% 30.9%

0.4%

12.8% 23.7%

0%

5%

10%

15%

20%

25%

30%

0%

5%

10%

15%

20%

25%

30%

35%

Asset Risk:Problem Loans/

Gross Loans

Capital:Tangible Common

Equity/Risk-WeightedAssets

Profitability:Net Income/

Tangible Assets

Funding Structure:Market Funds/

Tangible BankingAssets

Liquid Resources:Liquid Banking

Assets/TangibleBanking Assets

Solvency Factors (LHS) Liquidity Factors (RHS)

UBID (BCA: ba1) Median ba1-rated banks

So

lve

ncy F

acto

rsL

iqu

idity

Fa

cto

rs

December 2016 data for UBIDSource: Moody's Banking Financial Metrics

Credit Strengths

» Strong capital ratios, which we expect to decline owing to dividend payments, but to remain adequate in relation to the bank's riskprofile;

» Solid funding profile, primarily made of retail and corporate deposits; and

» Comfortable liquidity position, supported by a portfolio of high-quality liquid assets.

Credit Challenges

» Sizeable stock of problem loans, although declining and adequately provisioned, and large share of loans in forbearance andnegative equity;

» Weak pre-provision profitability, although expected to gradually improve over the outlook period.

Rating OutlookThe outlook on UBID's deposit and issuer ratings is positive. We believe UBID will remain an integral part of the ring-fenced bankingsub-group, which will have a stronger credit profile as it will retain mostly retail and SME activities, and have a more deposit-basedfunding profile. Our expectation that the creditworthiness of the ring-fenced sub-group will be higher than that of UBID's currentsupport provider creates positive pressures on UBID's adjusted BCA and drives the positive outlook.

Factors that Could Lead to an UpgradeUBID's BCA could be upgraded if the bank continues to strengthen its credit fundamentals, reduces the amount of legacy and non-performing assets on its balance sheet and improves its pre-provision profitability.

UBID's deposit and issuer ratings could be upgraded if its parent's own creditworthiness were to improve further due to improved creditfundamentals and or the implementation of ring-fencing in the UK resulting in an upgrade of its adjusted BCA.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 12 October 2017 Ulster Bank Ireland DAC: Update following affirmation of Baa2 rating; outlook changed to positive

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Factors that Could Lead to a DowngradeGiven the positive outlook, a downgrade is unlikely. However, UBID's BCA could be downgraded due to a decline in its capital levelsbeyond that already factored into our assessment; a significant increase in the use of market funding; or a deterioration in the bank'sliquidity position. A downgrade of its parent's creditworthiness could result in a reduced capacity to support UBID and thereforedowngrades to all of UBID's instrument ratings.

Key Indicators

Exhibit 2

Ulster Bank Ireland DAC (Consolidated Financials) [1]12-162 12-152 12-142 12-133 12-123 CAGR/Avg.4

Total Assets (EUR million) 30,694 31,019 33,841 35,375 40,879 -6.95

Total Assets (USD million) 32,375 33,696 40,949 48,745 53,894 -12.05

Tangible Common Equity (EUR million) 6,484 7,834 6,527 4,611 7,933 -4.95

Tangible Common Equity (USD million) 6,839 8,510 7,898 6,354 10,459 -10.15

Problem Loans / Gross Loans (%) 15.9 23.9 43.5 44.6 40.4 33.76

Tangible Common Equity / Risk Weighted Assets (%) 30.9 29.9 21.0 11.9 17.5 27.37

Problem Loans / (Tangible Common Equity + Loan Loss Reserve) (%) 47.2 53.9 89.9 100.0 99.3 78.16

Net Interest Margin (%) 1.5 1.2 1.1 1.1 1.2 1.26

PPI / Average RWA (%) -0.4 0.7 1.0 0.5 0.7 0.47

Net Income / Tangible Assets (%) 0.4 3.5 6.9 -12.8 -5.8 -1.66

Cost / Income Ratio (%) 115.2 73.4 62.1 74.2 65.1 78.06

Market Funds / Tangible Banking Assets (%) 12.8 12.3 17.9 28.1 28.2 19.86

Liquid Banking Assets / Tangible Banking Assets (%) 23.6 21.7 19.0 16.3 10.5 18.26

Gross Loans / Due to Customers (%) 123.5 149.9 193.0 224.2 230.6 184.26

[1] All figures and ratios are adjusted using Moody's standard adjustments [2] Basel III - fully-loaded or transitional phase-in; IFRS [3] Basel II; IFRS [4] May include rounding differences dueto scale of reported amounts [5] Compound Annual Growth Rate (%) based on time period presented for the latest accounting regime [6] Simple average of periods presented for the latestaccounting regime. [7] Simple average of Basel III periods presentedSource: Moody's Financial Metrics

Detailed Credit ConsiderationsThe financial data in the following sections are sourced from the UBID's consolidated financial statements unless otherwise stated.

Despite rapid deleveraging, the stock of problem loans remains high; downside risks are aggravated by a large share offorborne loans and loans in negative equityUBID was one of the most severely hit institutions by the recent financial crisis, but the bank undertook drastic efforts in loandeleveraging and the restoring of its balance sheet. In 2013 UBID’s parent company established the “RBS Capital ResolutionIreland” (RCRI) segment to manage an accelerated reduction in the Group’s non-performing capital intensive assets. A portfolio of €4.8billion of net assets was identified to be managed by RCRI, which has now been entirely run down.

The measures undertaken resulted in impaired loans reducing by 81% to €3.7 billion at December 2016 from the peak level of €19.2billion at December 2013. The reduction was primarily driven by the sale of non-performing portfolios, but the pace of migration tonewly impaired loans declined as well, as economic conditions in Ireland improved.

Nevertheless, UBID’s stock of problem loans remains high (€3.7 billion, or 15.9% of gross lending, at December 2016) and continuesto weigh down on the bank's standalone assessment. Provision coverage of problem loans at 37% is lower than the level of peers, butwhen taking into account UBID’s higher capital level, we view the overall coverage of problem loans is adequate (problem loans overtangible common equity and loan loss reserves ratio of 47% at December 2016 versus a range of 60%-115% for Irish peers).

3 12 October 2017 Ulster Bank Ireland DAC: Update following affirmation of Baa2 rating; outlook changed to positive

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

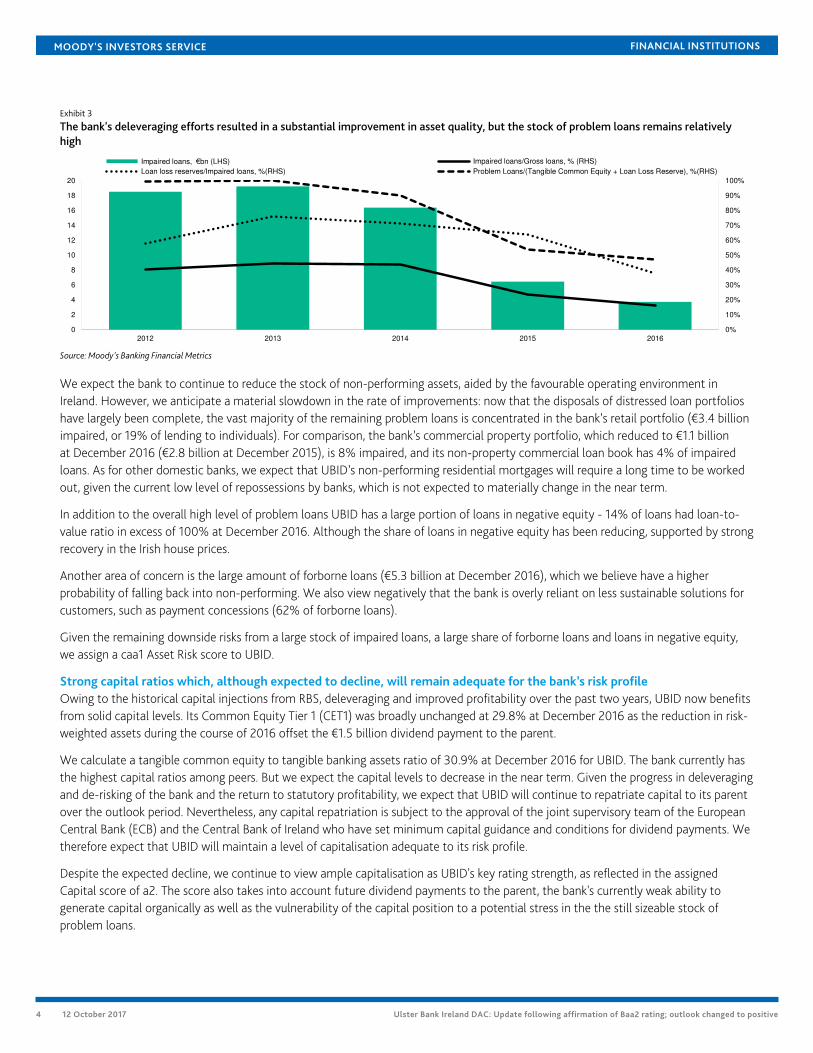

Exhibit 3

The bank's deleveraging efforts resulted in a substantial improvement in asset quality, but the stock of problem loans remains relativelyhigh

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

2

4

6

8

10

12

14

16

18

20

2012 2013 2014 2015 2016

Impaired loans, €bn (LHS) Impaired loans/Gross loans, % (RHS)

Loan loss reserves/Impaired loans, %(RHS) Problem Loans/(Tangible Common Equity + Loan Loss Reserve), %(RHS)

Source: Moody's Banking Financial Metrics

We expect the bank to continue to reduce the stock of non-performing assets, aided by the favourable operating environment inIreland. However, we anticipate a material slowdown in the rate of improvements: now that the disposals of distressed loan portfolioshave largely been complete, the vast majority of the remaining problem loans is concentrated in the bank’s retail portfolio (€3.4 billionimpaired, or 19% of lending to individuals). For comparison, the bank’s commercial property portfolio, which reduced to €1.1 billionat December 2016 (€2.8 billion at December 2015), is 8% impaired, and its non-property commercial loan book has 4% of impairedloans. As for other domestic banks, we expect that UBID’s non-performing residential mortgages will require a long time to be workedout, given the current low level of repossessions by banks, which is not expected to materially change in the near term.

In addition to the overall high level of problem loans UBID has a large portion of loans in negative equity - 14% of loans had loan-to-value ratio in excess of 100% at December 2016. Although the share of loans in negative equity has been reducing, supported by strongrecovery in the Irish house prices.

Another area of concern is the large amount of forborne loans (€5.3 billion at December 2016), which we believe have a higherprobability of falling back into non-performing. We also view negatively that the bank is overly reliant on less sustainable solutions forcustomers, such as payment concessions (62% of forborne loans).

Given the remaining downside risks from a large stock of impaired loans, a large share of forborne loans and loans in negative equity,we assign a caa1 Asset Risk score to UBID.

Strong capital ratios which, although expected to decline, will remain adequate for the bank’s risk profileOwing to the historical capital injections from RBS, deleveraging and improved profitability over the past two years, UBID now benefitsfrom solid capital levels. Its Common Equity Tier 1 (CET1) was broadly unchanged at 29.8% at December 2016 as the reduction in risk-weighted assets during the course of 2016 offset the €1.5 billion dividend payment to the parent.

We calculate a tangible common equity to tangible banking assets ratio of 30.9% at December 2016 for UBID. The bank currently hasthe highest capital ratios among peers. But we expect the capital levels to decrease in the near term. Given the progress in deleveragingand de-risking of the bank and the return to statutory profitability, we expect that UBID will continue to repatriate capital to its parentover the outlook period. Nevertheless, any capital repatriation is subject to the approval of the joint supervisory team of the EuropeanCentral Bank (ECB) and the Central Bank of Ireland who have set minimum capital guidance and conditions for dividend payments. Wetherefore expect that UBID will maintain a level of capitalisation adequate to its risk profile.

Despite the expected decline, we continue to view ample capitalisation as UBID's key rating strength, as reflected in the assignedCapital score of a2. The score also takes into account future dividend payments to the parent, the bank's currently weak ability togenerate capital organically as well as the vulnerability of the capital position to a potential stress in the the still sizeable stock ofproblem loans.

4 12 October 2017 Ulster Bank Ireland DAC: Update following affirmation of Baa2 rating; outlook changed to positive

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Pre-provision profitability is weak, but we expect it to improve over the outlook periodSimilar to the previous two years, UBID’s profitability in 2016 was supported by write-backs of loan loss provisions (€138 million, downfrom €929 million in 2015). We do not consider the release of loan impairment charges a sustainable profitability driver and anticipatethe bank's bottom-line profitability will decrease to a more modest level over the outlook period, as the bank's cost of risk (measuredas impairment charges over gross loans) starts to normalise. On the positive side, we expect gradual improvements in pre-provisionprofitability, as the bank replaces legacy low-yielding tracker mortgages (€10.8 billion, or 49% of the loan book) with new lending andimplements its costs saving programme.

Exhibit 4

Substantial write-backs of loan loss provisions contributed to profitability in 2014-2016

-15%

-10%

-5%

0%

5%

10%

-3

-2

-1

0

1

2

3

4

5

6

2012 2013 2014 2015 2016

Loan loss provisions, €bn (LHS) Net income/Tangible assets, % (RHS)

Source: Moody's Banking Financial Metrics

UBID’s net interest income increased by 3% to €489 million in 2016, as improved lending margins and re-pricing actions taken ondeposits outweighed the lower income on free funds and the negative impact of loan book reduction. The bank’s net interest marginimproved to 1.47% in 2016 from 1.19% in 2015, according to our calculations, but remains low compared to higher rated peers, due toa larger proportion of tracker loans. Reported non-interest income decreased from to €177 million from €242 million in 2015, driven byreduced income on interest rate swaps, lower fees receivable as a result of reduced loan volumes and lower gains on asset disposals.

The bank's cost base remains elevated ( we calculate 115% cost-to-income ratio in 2016, or 85% if adjusted for conduct charges whichthe bank reports in operating costs) and is a drag on profitability. In 2016 UBID commenced a bank-wide transformation programme,and realigning operating expenses to the resized balance sheet is one of its central areas of focus. We expect investments in the bank'sdigitalisation and simplification to start materialising into cost savings towards the end of the outlook period.

Following the launch of the Tracker Mortgage Examination by the Central Bank of Ireland (CBI), UBID recorded a €198 million provisioncharge in 2016 in respect of potential non-compliance. In addition, UBID provisioned for customer redress related to the FinancialConduct Authority’s review of complex fees charged to SME customers during the period 2008-2013. UBID recognised a €39 millionconduct and litigation provision in the first half of 2017. CBI required that banks complete the identification of impacted trackermortgage customers by the end of September. We therefore believe some further conduct provisions are likely in 2017, but do notexpect them to be at the level recorded in 2016.

We assign a Profitability score of b1 to the bank, which reflects our anticipation of a gradual improvement in UBID's core profitability,but also takes into account the volatility of earnings and a possibility of unexpected further conduct charges or credit losses.

Stabilised funding profile and sufficient liquidityWe consider UBID’s funding structure a relative strength. The ongoing loan deleveraging, combined with an increased focus on longterm funding, has materially reduced UBID’s funding gap and its reliance on parent funding, bringing its funding profile more in linewith its Irish peers. The intra-group funding was fully repaid in 2015. The bank's gross loan-to-deposit ratio is still high at 123% atDecember 2016, but we expect it to decline further: the bank has demonstrated strong growth in deposit balances in 2016 (up 5% to€19 billion), while the loan book has continued to shrink. We calculate market funds over tangible banking assets ratio of 12.8% at

5 12 October 2017 Ulster Bank Ireland DAC: Update following affirmation of Baa2 rating; outlook changed to positive

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

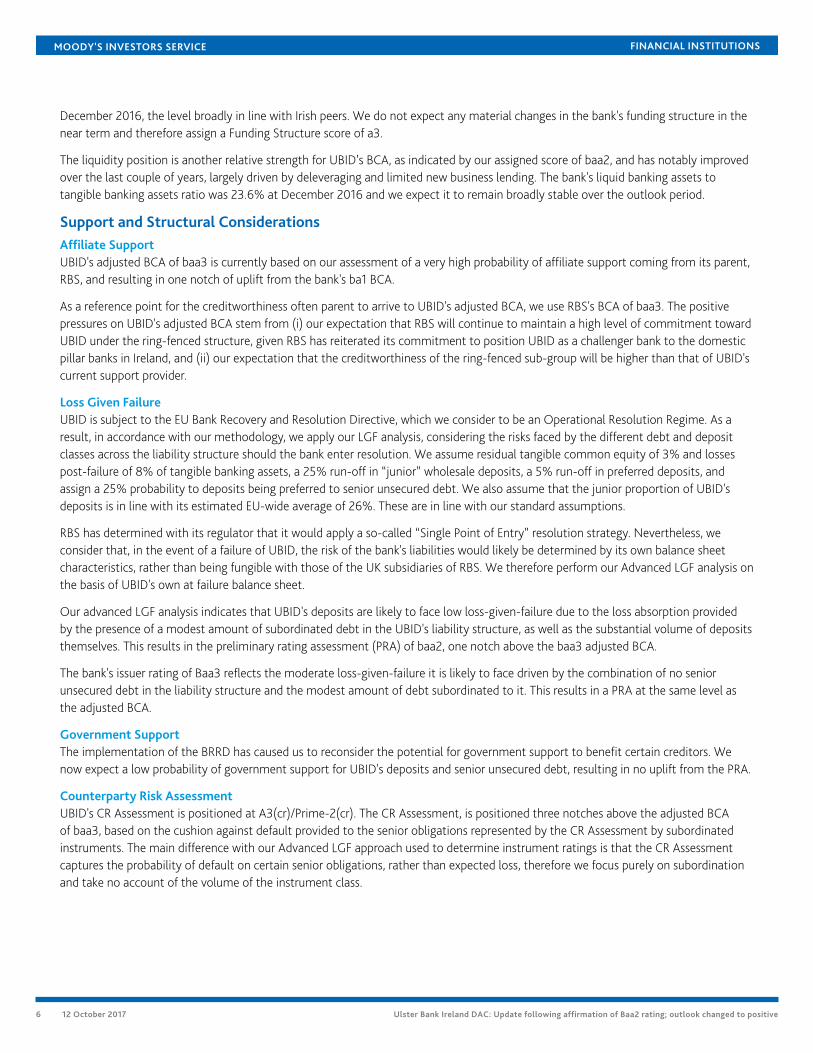

December 2016, the level broadly in line with Irish peers. We do not expect any material changes in the bank's funding structure in thenear term and therefore assign a Funding Structure score of a3.

The liquidity position is another relative strength for UBID’s BCA, as indicated by our assigned score of baa2, and has notably improvedover the last couple of years, largely driven by deleveraging and limited new business lending. The bank's liquid banking assets totangible banking assets ratio was 23.6% at December 2016 and we expect it to remain broadly stable over the outlook period.

Support and Structural ConsiderationsAffiliate SupportUBID's adjusted BCA of baa3 is currently based on our assessment of a very high probability of affiliate support coming from its parent,RBS, and resulting in one notch of uplift from the bank's ba1 BCA.

As a reference point for the creditworthiness often parent to arrive to UBID's adjusted BCA, we use RBS's BCA of baa3. The positivepressures on UBID's adjusted BCA stem from (i) our expectation that RBS will continue to maintain a high level of commitment towardUBID under the ring-fenced structure, given RBS has reiterated its commitment to position UBID as a challenger bank to the domesticpillar banks in Ireland, and (ii) our expectation that the creditworthiness of the ring-fenced sub-group will be higher than that of UBID'scurrent support provider.

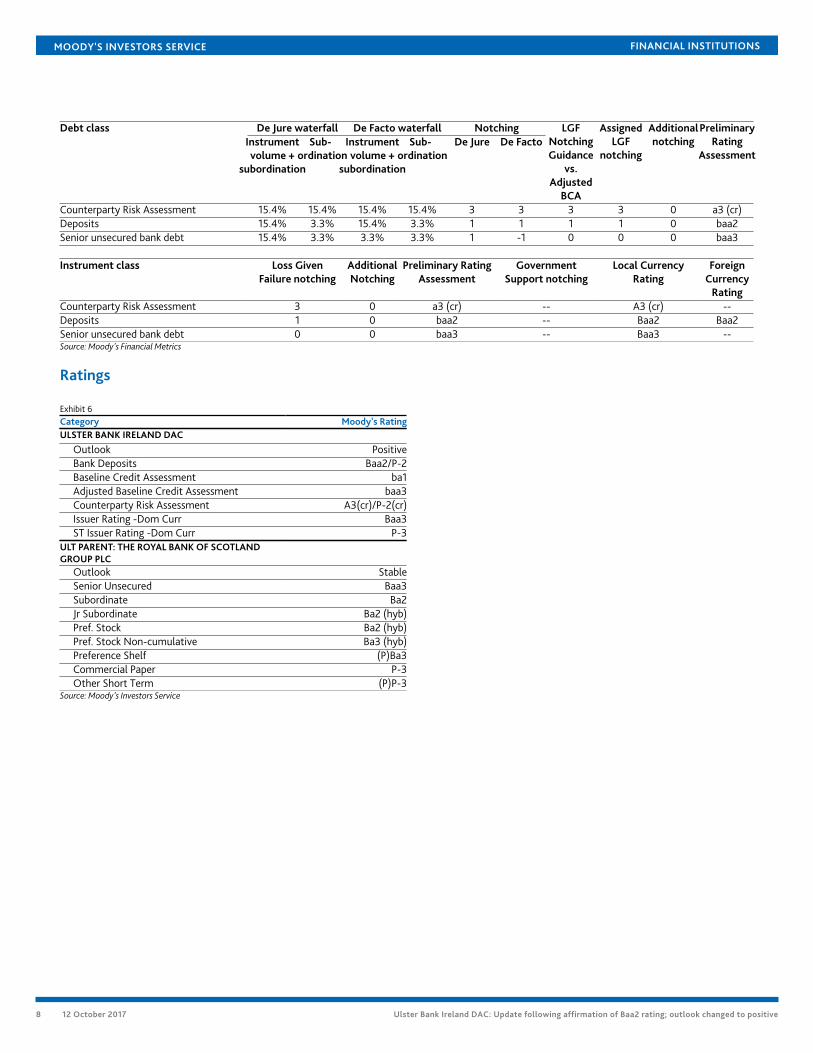

Loss Given FailureUBID is subject to the EU Bank Recovery and Resolution Directive, which we consider to be an Operational Resolution Regime. As aresult, in accordance with our methodology, we apply our LGF analysis, considering the risks faced by the different debt and depositclasses across the liability structure should the bank enter resolution. We assume residual tangible common equity of 3% and lossespost-failure of 8% of tangible banking assets, a 25% run-off in “junior” wholesale deposits, a 5% run-off in preferred deposits, andassign a 25% probability to deposits being preferred to senior unsecured debt. We also assume that the junior proportion of UBID'sdeposits is in line with its estimated EU-wide average of 26%. These are in line with our standard assumptions.

RBS has determined with its regulator that it would apply a so-called “Single Point of Entry” resolution strategy. Nevertheless, weconsider that, in the event of a failure of UBID, the risk of the bank's liabilities would likely be determined by its own balance sheetcharacteristics, rather than being fungible with those of the UK subsidiaries of RBS. We therefore perform our Advanced LGF analysis onthe basis of UBID's own at failure balance sheet.

Our advanced LGF analysis indicates that UBID's deposits are likely to face low loss-given-failure due to the loss absorption providedby the presence of a modest amount of subordinated debt in the UBID's liability structure, as well as the substantial volume of depositsthemselves. This results in the preliminary rating assessment (PRA) of baa2, one notch above the baa3 adjusted BCA.

The bank's issuer rating of Baa3 reflects the moderate loss-given-failure it is likely to face driven by the combination of no seniorunsecured debt in the liability structure and the modest amount of debt subordinated to it. This results in a PRA at the same level asthe adjusted BCA.

Government SupportThe implementation of the BRRD has caused us to reconsider the potential for government support to benefit certain creditors. Wenow expect a low probability of government support for UBID's deposits and senior unsecured debt, resulting in no uplift from the PRA.

Counterparty Risk AssessmentUBID's CR Assessment is positioned at A3(cr)/Prime-2(cr). The CR Assessment, is positioned three notches above the adjusted BCAof baa3, based on the cushion against default provided to the senior obligations represented by the CR Assessment by subordinatedinstruments. The main difference with our Advanced LGF approach used to determine instrument ratings is that the CR Assessmentcaptures the probability of default on certain senior obligations, rather than expected loss, therefore we focus purely on subordinationand take no account of the volume of the instrument class.

6 12 October 2017 Ulster Bank Ireland DAC: Update following affirmation of Baa2 rating; outlook changed to positive

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

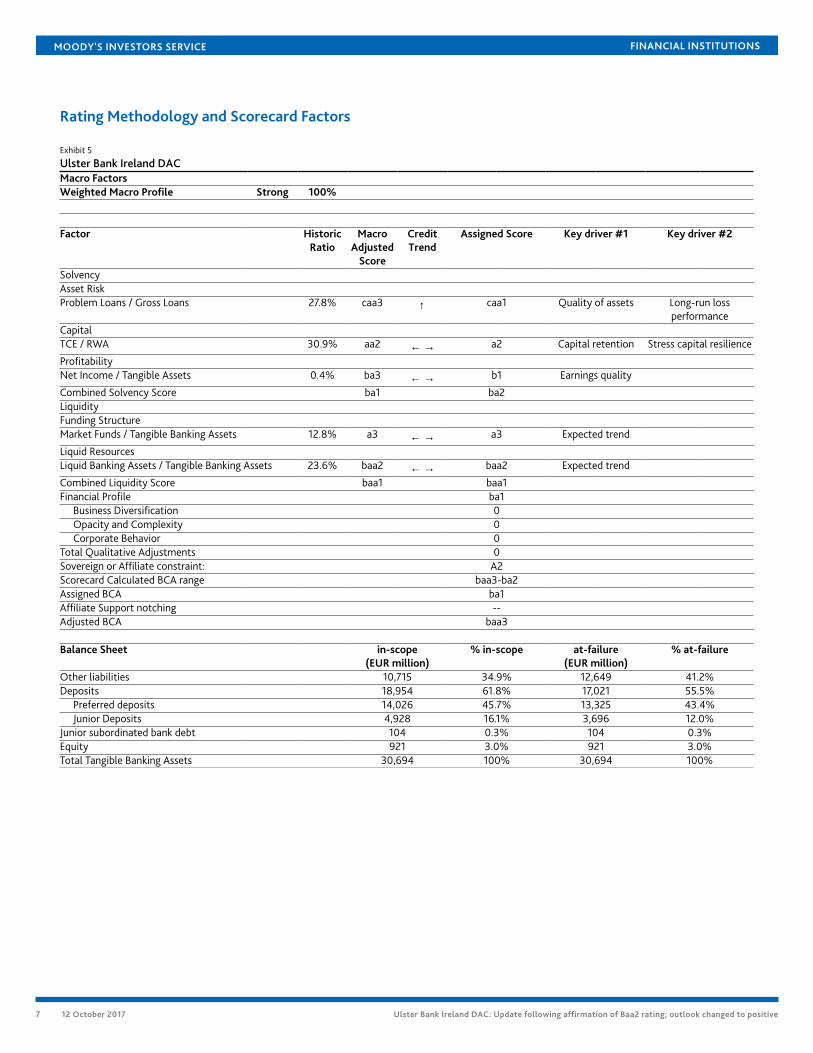

Rating Methodology and Scorecard Factors

Exhibit 5

Ulster Bank Ireland DACMacro FactorsWeighted Macro Profile Strong 100%

Factor HistoricRatio

MacroAdjusted

Score

CreditTrend

Assigned Score Key driver #1 Key driver #2

SolvencyAsset RiskProblem Loans / Gross Loans 27.8% caa3 ↑ caa1 Quality of assets Long-run loss

performanceCapitalTCE / RWA 30.9% aa2 ← → a2 Capital retention Stress capital resilience

ProfitabilityNet Income / Tangible Assets 0.4% ba3 ← → b1 Earnings quality

Combined Solvency Score ba1 ba2LiquidityFunding StructureMarket Funds / Tangible Banking Assets 12.8% a3 ← → a3 Expected trend

Liquid ResourcesLiquid Banking Assets / Tangible Banking Assets 23.6% baa2 ← → baa2 Expected trend

Combined Liquidity Score baa1 baa1Financial Profile ba1

Business Diversification 0Opacity and Complexity 0Corporate Behavior 0

Total Qualitative Adjustments 0Sovereign or Affiliate constraint: A2Scorecard Calculated BCA range baa3-ba2Assigned BCA ba1Affiliate Support notching --Adjusted BCA baa3

Balance Sheet in-scope(EUR million)

% in-scope at-failure(EUR million)

% at-failure

Other liabilities 10,715 34.9% 12,649 41.2%Deposits 18,954 61.8% 17,021 55.5%

Preferred deposits 14,026 45.7% 13,325 43.4%Junior Deposits 4,928 16.1% 3,696 12.0%

Junior subordinated bank debt 104 0.3% 104 0.3%Equity 921 3.0% 921 3.0%Total Tangible Banking Assets 30,694 100% 30,694 100%

7 12 October 2017 Ulster Bank Ireland DAC: Update following affirmation of Baa2 rating; outlook changed to positive

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

De Jure waterfall De Facto waterfall NotchingDebt classInstrumentvolume +

subordination

Sub-ordination

Instrumentvolume +

subordination

Sub-ordination

De Jure De FactoLGF

NotchingGuidance

vs.Adjusted

BCA

AssignedLGF

notching

Additionalnotching

PreliminaryRating

Assessment

Counterparty Risk Assessment 15.4% 15.4% 15.4% 15.4% 3 3 3 3 0 a3 (cr)Deposits 15.4% 3.3% 15.4% 3.3% 1 1 1 1 0 baa2Senior unsecured bank debt 15.4% 3.3% 3.3% 3.3% 1 -1 0 0 0 baa3

Instrument class Loss GivenFailure notching

AdditionalNotching

Preliminary RatingAssessment

GovernmentSupport notching

Local CurrencyRating

ForeignCurrency

RatingCounterparty Risk Assessment 3 0 a3 (cr) -- A3 (cr) --Deposits 1 0 baa2 -- Baa2 Baa2Senior unsecured bank debt 0 0 baa3 -- Baa3 --Source: Moody's Financial Metrics

Ratings

Exhibit 6Category Moody's RatingULSTER BANK IRELAND DAC

Outlook PositiveBank Deposits Baa2/P-2Baseline Credit Assessment ba1Adjusted Baseline Credit Assessment baa3Counterparty Risk Assessment A3(cr)/P-2(cr)Issuer Rating -Dom Curr Baa3ST Issuer Rating -Dom Curr P-3

ULT PARENT: THE ROYAL BANK OF SCOTLANDGROUP PLC

Outlook StableSenior Unsecured Baa3Subordinate Ba2Jr Subordinate Ba2 (hyb)Pref. Stock Ba2 (hyb)Pref. Stock Non-cumulative Ba3 (hyb)Preference Shelf (P)Ba3Commercial Paper P-3Other Short Term (P)P-3

Source: Moody's Investors Service

8 12 October 2017 Ulster Bank Ireland DAC: Update following affirmation of Baa2 rating; outlook changed to positive

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1094009

9 12 October 2017 Ulster Bank Ireland DAC: Update following affirmation of Baa2 rating; outlook changed to positive