Embed Size (px)

Citation preview

Slide1LabyrinthConsultingServices,Inc. artberman.com

Tight Oil Money Return on Investment Eagle Ford Shale Case History

Art Berman Labyrinth Consulting Services, Inc.

American Chemical Society New Orleans, LA March 21, 2018

Slide2LabyrinthConsultingServices,Inc. artberman.com

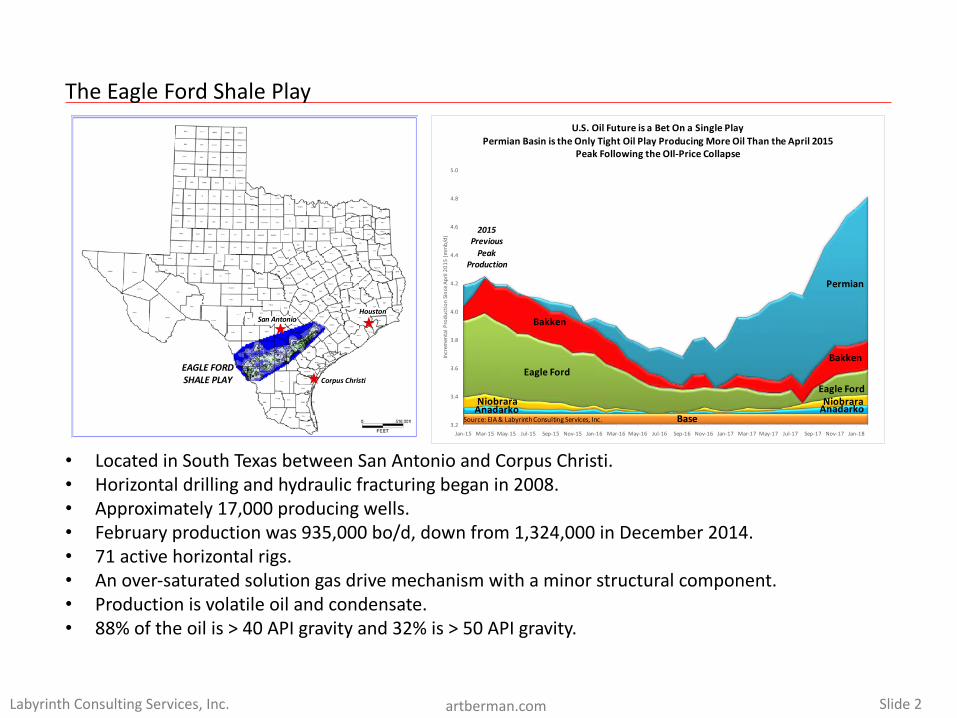

TheEagleFordShalePlay

• LocatedinSouthTexasbetweenSanAntonioandCorpusChristi.• Horizontaldrillingandhydraulicfracturingbeganin2008.• Approximately17,000producingwells.• Februaryproductionwas935,000bo/d,downfrom1,324,000inDecember2014.• 71activehorizontalrigs.• Anover-saturatedsolutiongasdrivemechanismwithaminorstructuralcomponent.• Productionisvolatileoilandcondensate.• 88%oftheoilis>40APIgravityand32%is>50APIgravity.

Corpus Christi

HoustonSan Antonio

EAGLE FORDSHALE PLAY

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

4.8

5.0

Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17 Jan-18 IncrementalProductionSinceApril2015(mmb/d)

U.S.OilFutureisaBetOnaSinglePlayPermianBasinistheOnlyTightOilPlayProducingMoreOilThantheApril2015

PeakFollowingtheOIl-PriceCollapse

Source:EIA&LabyrinthConsultingServices,Inc.

EagleFord

Bakken

AnadarkoNiobrara

Permian

EagleFord

Bakken

Base

2015PreviousPeak

Production

AnadarkoNiobrara

Slide3LabyrinthConsultingServices,Inc. artberman.com

EagleFordWellPerformanceEvaluationbyDecline-CurveAnalysis

100

1,000

10,000

100,000

1 10 100

Rate,bblsorM

scf/mon

thTimemonths

LogLogPlotRatevsTime

Points=ActualDataLine=ForecastOil=Green,Gas=Red

100

1,000

10,000

100,000

0 5 10 15 20 25 30 35 40 45 50 55 60

Mon

thlyRate,bblso

rMscf

MonthsfromFirstProduction

Semi-LogPlotofRatevs.Time

Points=ActualDataLine=Forecast

Oil=Green,Gas=Red

EOG 2013OIL GAS

Max 57,000 53,000b 1.25 1.30

Di 20.00 12.00EUR 401,691 295,699

100

1,000

10,000

100,000

1 10 100

Rate,bblsorM

scf/mon

th

Timemonths

LogLogPlotRatevsTime

Points=ActualDataLine=ForecastOil=Green,Gas=Red

100

1,000

10,000

100,000

0 5 10 15 20 25 30 35 40 45 50 55 60

Mon

thlyRate,bblso

rMscf

MonthsfromFirstProduction

Semi-LogPlotofRatevs.Time

Points=ActualDataLine=Forecast

Oil=Green,Gas=Red

DVN 2014OIL GAS

Max 30,000 70,000b 0.475 0.45

Di 1.80 1.20EUR 370,863 1,100,892

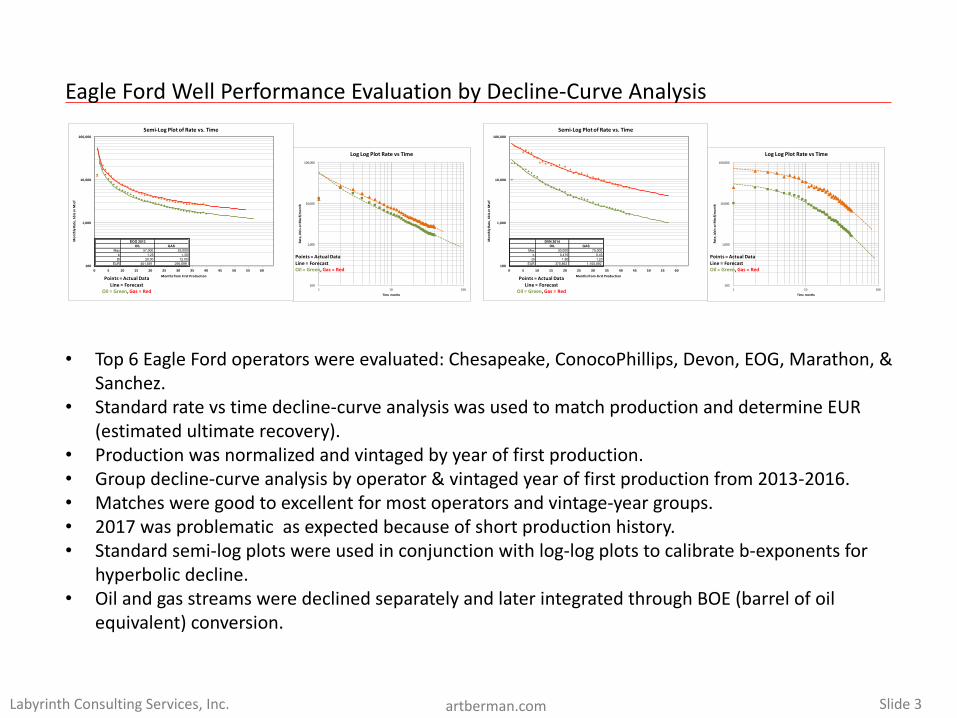

• Top6EagleFordoperatorswereevaluated:Chesapeake,ConocoPhillips,Devon,EOG,Marathon,&Sanchez.

• Standardratevstimedecline-curveanalysiswasusedtomatchproductionanddetermineEUR(estimatedultimaterecovery).

• Productionwasnormalizedandvintaged byyearoffirstproduction.• Groupdecline-curveanalysisbyoperator&vintaged yearoffirstproductionfrom2013-2016.• Matchesweregoodtoexcellentformostoperatorsandvintage-yeargroups.• 2017wasproblematicasexpectedbecauseofshortproductionhistory.• Standardsemi-logplotswereusedinconjunctionwithlog-logplotstocalibrateb-exponentsfor

hyperbolicdecline.• OilandgasstreamsweredeclinedseparatelyandlaterintegratedthroughBOE(barrelofoil

equivalent)conversion.

Slide4LabyrinthConsultingServices,Inc. artberman.com

IntegratingOil,NaturalGas&NaturalGasLiquids(NGL)Production

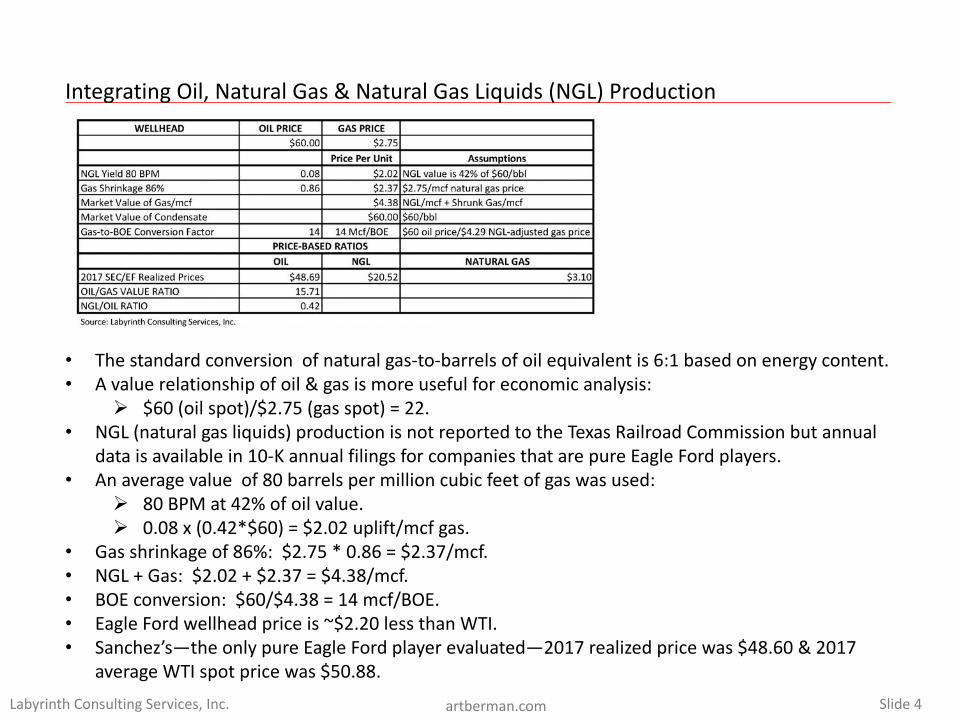

• Thestandardconversionofnaturalgas-to-barrelsofoilequivalentis6:1basedonenergycontent.• Avaluerelationshipofoil&gasismoreusefulforeconomicanalysis:

Ø $60(oilspot)/$2.75(gasspot)=22.• NGL(naturalgasliquids)productionisnotreportedtotheTexasRailroadCommissionbutannual

dataisavailablein10-KannualfilingsforcompaniesthatarepureEagleFordplayers.• Anaveragevalueof80barrelspermillioncubicfeetofgaswasused:

Ø 80BPMat42%ofoilvalue.Ø 0.08x(0.42*$60)=$2.02uplift/mcf gas.

• Gasshrinkageof86%:$2.75*0.86=$2.37/mcf.• NGL+Gas:$2.02+$2.37=$4.38/mcf.• BOEconversion:$60/$4.38=14mcf/BOE.• EagleFordwellheadpriceis~$2.20lessthanWTI.• Sanchez’s—theonlypureEagleFordplayerevaluated—2017realizedpricewas$48.60&2017

averageWTIspotpricewas$50.88.

Slide5LabyrinthConsultingServices,Inc. artberman.com

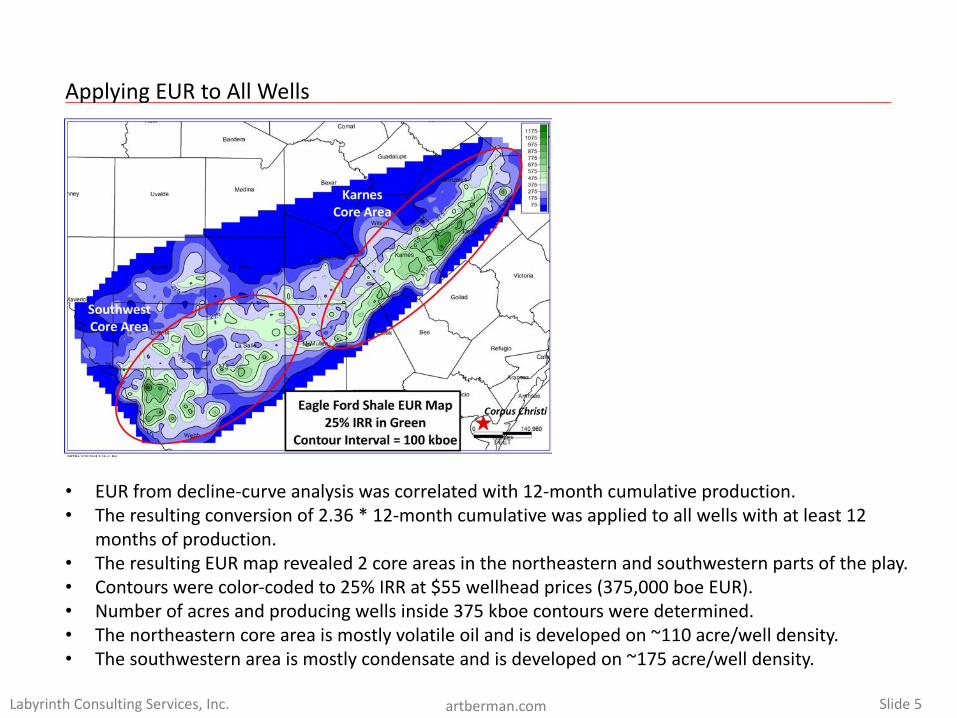

ApplyingEURtoAllWells

• EURfromdecline-curveanalysiswascorrelatedwith12-monthcumulativeproduction.• Theresultingconversionof2.36*12-monthcumulativewasappliedtoallwellswithatleast12

monthsofproduction.• TheresultingEURmaprevealed2coreareasinthenortheasternandsouthwesternpartsoftheplay.• Contourswerecolor-codedto25%IRRat$55wellheadprices(375,000boe EUR).• Numberofacresandproducingwellsinside375kboe contoursweredetermined.• Thenortheasterncoreareaismostlyvolatileoilandisdevelopedon~110acre/welldensity.• Thesouthwesternareaismostlycondensateandisdevelopedon~175acre/welldensity.

Slide6LabyrinthConsultingServices,Inc. artberman.com

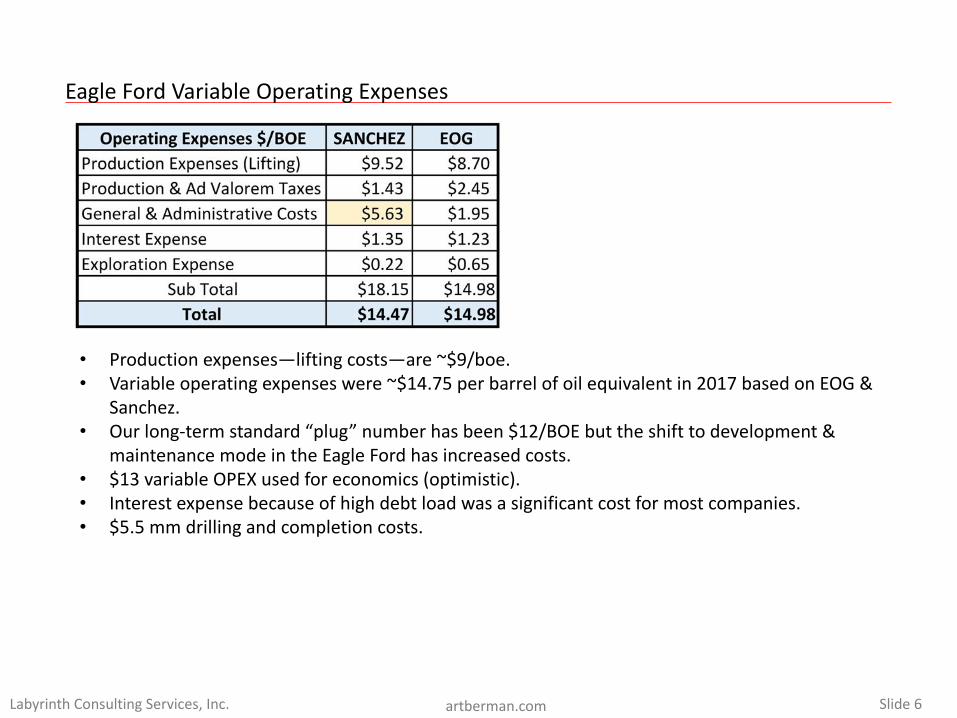

EagleFordVariableOperatingExpenses

• Productionexpenses—liftingcosts—are~$9/boe.• Variableoperatingexpenseswere~$14.75perbarrelofoilequivalentin2017basedonEOG&

Sanchez.• Ourlong-termstandard“plug”numberhasbeen$12/BOEbuttheshifttodevelopment&

maintenancemodeintheEagleFordhasincreasedcosts.• $13variableOPEXusedforeconomics(optimistic).• Interestexpensebecauseofhighdebtloadwasasignificantcostformostcompanies.• $5.5mmdrillingandcompletioncosts.

Slide7LabyrinthConsultingServices,Inc. artberman.com

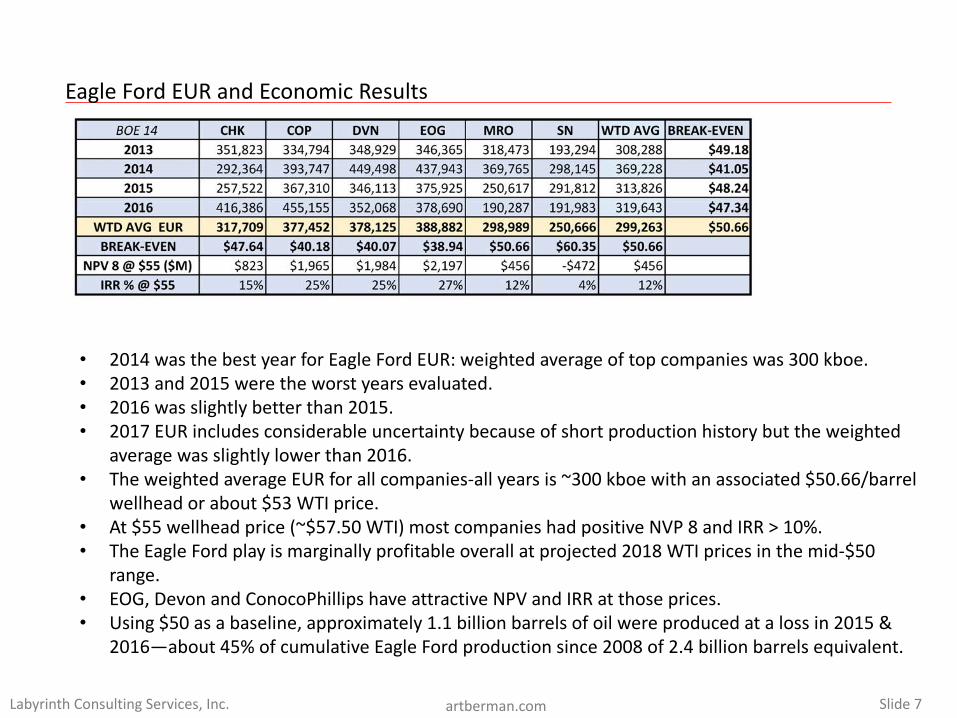

EagleFordEURandEconomicResults

• 2014wasthebestyearforEagleFordEUR:weightedaverageoftopcompanieswas300kboe.• 2013and2015weretheworstyearsevaluated.• 2016wasslightlybetterthan2015.• 2017EURincludesconsiderableuncertaintybecauseofshortproductionhistorybuttheweighted

averagewasslightlylowerthan2016.• TheweightedaverageEURforallcompanies-allyearsis~300kboe withanassociated$50.66/barrel

wellheadorabout$53WTIprice.• At$55wellheadprice(~$57.50WTI)mostcompanieshadpositiveNVP8andIRR>10%.• TheEagleFordplayismarginallyprofitableoverallatprojected2018WTIpricesinthemid-$50

range.• EOG,DevonandConocoPhillipshaveattractiveNPVandIRRatthoseprices.• Using$50asabaseline,approximately1.1billionbarrelsofoilwereproducedatalossin2015&

2016—about45%ofcumulativeEagleFordproductionsince2008of2.4billionbarrelsequivalent.

Slide8LabyrinthConsultingServices,Inc. artberman.com

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

Dec-85

Oct-86

Aug-87

Jun-88

Apr-89

Feb-90

Dec-90

Oct-91

Aug-92

Jun-93

Apr-94

Feb-95

Dec-95

Oct-96

Aug-97

Jun-98

Apr-99

Feb-00

Dec-00

Oct-01

Aug-02

Jun-03

Apr-04

Feb-05

Dec-05

Oct-06

Aug-07

Jun-08

Apr-09

Feb-10

Dec-10

Oct-11

Aug-12

Jun-13

Apr-14

Feb-15

Dec-15

Oct-16

Aug-17

WTIPrice($/barrel)

Oil&GasW

ellD

rillingProducerPriceIndex(1985=100)

4-FoldIncreaseInO&GWellDrillingProducerPriceIndexFrom2004-2014

WTIOilPrice(RHS)

Oil&GasWell DrillingCostIndex(LHS)

Source:U.S.Federal ReserveBank,EIA&LabyrinthConsulting Services,Inc.

4-FoldIncreaseinO&GPPIBecauseof

UnconventionalOil&Gas2004-2014

BecauseofHigherCostofUnconventionalTechnology40%DecreaseAfterOil PriceCollapsebut7% Increasein2017

+7%

~40%DecreaseFrom

Deflation

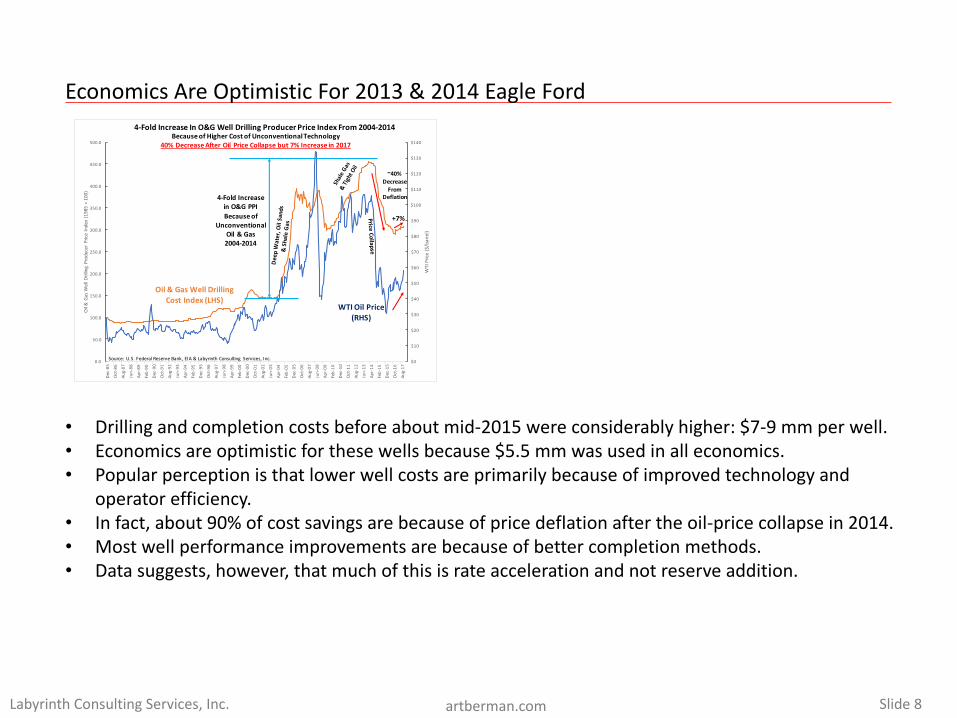

EconomicsAreOptimisticFor2013&2014EagleFord

• Drillingandcompletioncostsbeforeaboutmid-2015wereconsiderablyhigher:$7-9mmperwell.• Economicsareoptimisticforthesewellsbecause$5.5mmwasusedinalleconomics.• Popularperceptionisthatlowerwellcostsareprimarilybecauseofimprovedtechnologyand

operatorefficiency.• Infact,about90%ofcostsavingsarebecauseofpricedeflationaftertheoil-pricecollapsein2014.• Mostwellperformanceimprovementsarebecauseofbettercompletionmethods.• Datasuggests,however,thatmuchofthisisrateaccelerationandnotreserveaddition.

Slide9LabyrinthConsultingServices,Inc. artberman.com

8.3

5.3

2.01.8

1.6 1.5 1.5 1.5 1.4 1.4 1.31.2 1.1 1.1 1.1 1.1 1.0 0.9 0.9

0.7 0.7 0.6

0

1

2

3

4

5

6

7

8

9

Parsley

Oasis

Hess

Sanchez

Callon

Energen

Concho

Whitin

g

Laredo

New

field

Statoil

Maratho

n

Apache

Pion

eer

EOG

Diamon

dback

Devon

Continental

Murph

y

OXY EPE

Cono

coPh

illips

RatioofC

apitalExpenditurestoCashFrom

Operations

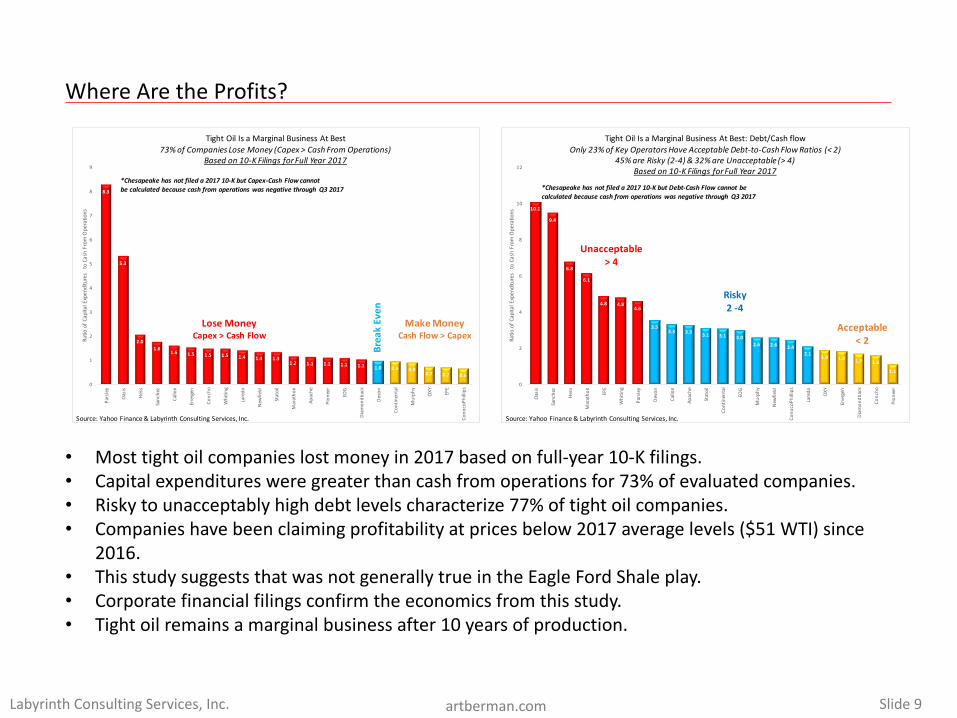

TightOilIsaMarginalBusinessAtBest73%ofCompaniesLoseMoney(Capex>CashFromOperations)

Basedon10-KFilingsforFullYear2017

MakeMoneyCashFlow>Capex

Lose MoneyCapex>CashFlow

Source:YahooFinance&LabyrinthConsultingServices,Inc.

BreakEven

*Chesapeake hasnotfileda201710-KbutCapex-CashFlowcannotbecalculatedbecausecashfromoperationswasnegativethrough Q32017

10.1

9.4

6.8

6.1

4.8 4.84.6

3.53.3 3.3 3.1 3.1 3.0

2.6 2.6 2.42.1 1.9 1.8 1.7 1.6

1.1

0

2

4

6

8

10

12

Oasis

Sanchez

Hess

Marathon

EPE

Whiting

Parsley

Devon

Callon

Apache

Statoil

Continental

EOG

Murphy

New

field

ConocoPhillips

Laredo

OXY

Energen

Diamondback

Concho

Pioneer

RatioofCapitalExpenditurestoCashFrom

Operations

TightOilIsaMarginalBusinessAtBest:Debt/CashflowOnly23%ofKeyOperatorsHaveAcceptableDebt-to-CashFlowRatios(<2)

45%areRisky(2-4)&32%areUnacceptable(>4)Basedon10-KFilingsforFullYear2017

Source:YahooFinance&LabyrinthConsultingServices,Inc.

Acceptable<2

Risky2-4

Unacceptable>4

*Chesapeake hasnotfileda201710-KbutDebt-CashFlowcannotbecalculatedbecausecashfromoperationswasnegativethrough Q32017

WhereAretheProfits?

• Mosttightoilcompanieslostmoneyin2017basedonfull-year10-Kfilings.• Capitalexpendituresweregreaterthancashfromoperationsfor73%ofevaluatedcompanies.• Riskytounacceptablyhighdebtlevelscharacterize77%oftightoilcompanies.• Companieshavebeenclaimingprofitabilityatpricesbelow2017averagelevels($51WTI)since

2016.• ThisstudysuggeststhatwasnotgenerallytrueintheEagleFordShaleplay.• Corporatefinancialfilingsconfirmtheeconomicsfromthisstudy.• Tightoilremainsamarginalbusinessafter10yearsofproduction.

Slide10LabyrinthConsultingServices,Inc. artberman.com

0

5,000

10,000

15,000

20,000

25,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50

MonthlyOilP

roduction(barrels)

MonthsofProduction

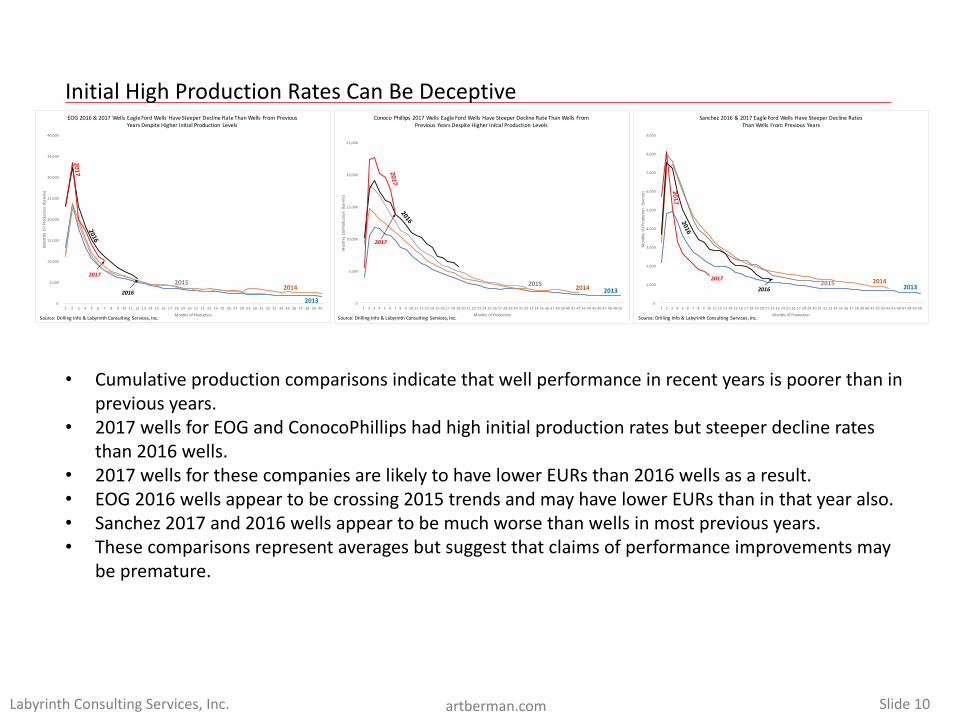

ConocoPhillips 2017Wells EagleFordWellsHaveSteeperDeclineRateThanWells FromPrevious YearsDespiteHigherInitialProduction Levels

20132015 2014

2017

Source:Drilling Info&LabyrinthConsultingServices,Inc.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50

MonthlyOilProduction(barrels)

MonthsofProduction

Sanchez2016&2017EagleFordWellsHaveSteeperDeclineRatesThanWells FromPrevious Years

2016 20132015 20142017

Source:Drilling Info&LabyrinthConsultingServices,Inc.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

MonthllyOilProduction(barrels)

MonthsofProduction

EOG2016&2017Wells EagleFordWellsHaveSteeperDeclineRateThanWells FromPreviousYearsDespiteHigherInitialProduction Levels

2013

20152014

2017

Source:Drilling Info&LabyrinthConsultingServices,Inc.

2016

InitialHighProductionRatesCanBeDeceptive

• Cumulativeproductioncomparisonsindicatethatwellperformanceinrecentyearsispoorerthaninpreviousyears.

• 2017wellsforEOGandConocoPhillipshadhighinitialproductionratesbutsteeperdeclineratesthan2016wells.

• 2017wellsforthesecompaniesarelikelytohavelowerEURsthan2016wellsasaresult.• EOG2016wellsappeartobecrossing2015trendsandmayhavelowerEURsthaninthatyearalso.• Sanchez2017and2016wellsappeartobemuchworsethanwellsinmostpreviousyears.• Thesecomparisonsrepresentaveragesbutsuggestthatclaimsofperformanceimprovementsmay

bepremature.

Slide11LabyrinthConsultingServices,Inc. artberman.com

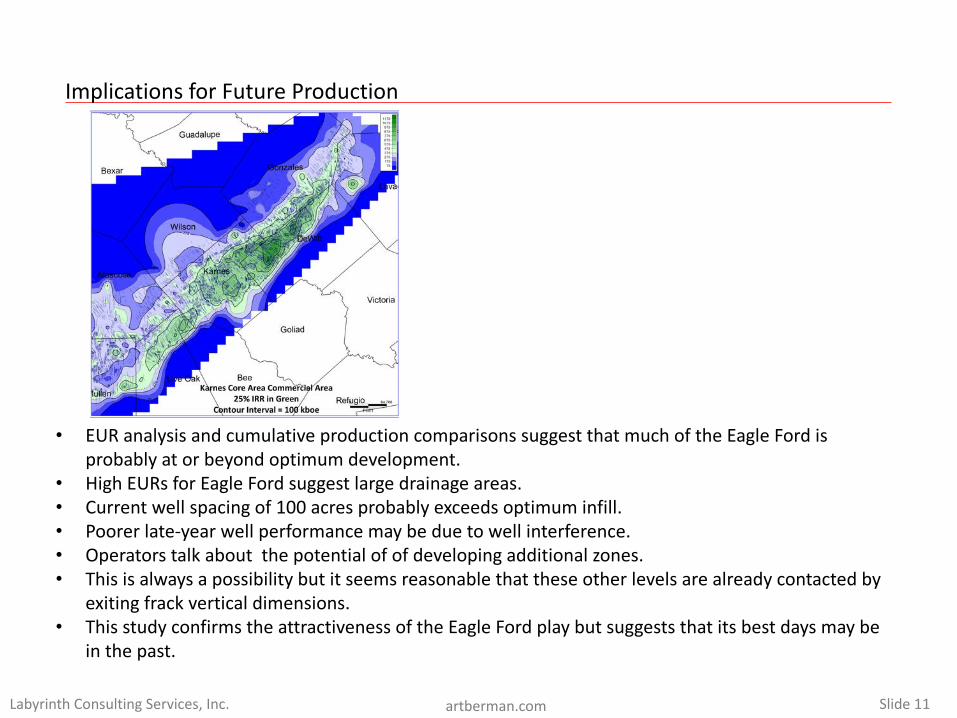

ImplicationsforFutureProduction

• EURanalysisandcumulativeproductioncomparisonssuggestthatmuchoftheEagleFordisprobablyatorbeyondoptimumdevelopment.

• HighEURsforEagleFordsuggestlargedrainageareas.• Currentwellspacingof100acresprobablyexceedsoptimuminfill.• Poorerlate-yearwellperformancemaybeduetowellinterference.• Operatorstalkaboutthepotentialofofdevelopingadditionalzones.• Thisisalwaysapossibilitybutitseemsreasonablethattheseotherlevelsarealreadycontactedby

exitingfrackverticaldimensions.• ThisstudyconfirmstheattractivenessoftheEagleFordplaybutsuggeststhatitsbestdaysmaybe

inthepast.

Slide12LabyrinthConsultingServices,Inc. artberman.com

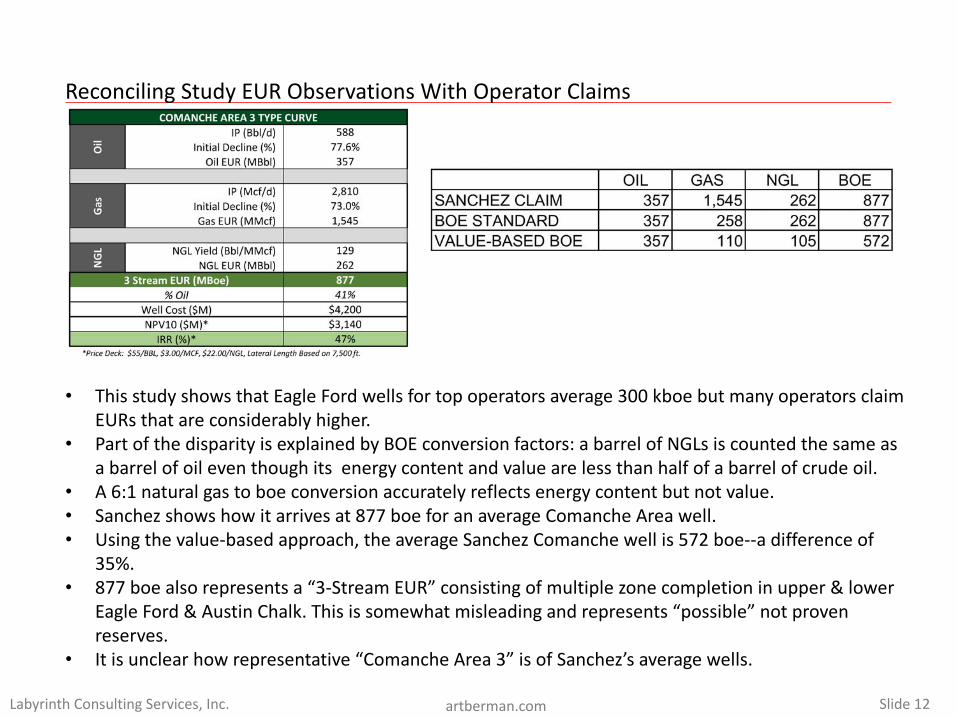

• ThisstudyshowsthatEagleFordwellsfortopoperatorsaverage300kboe butmanyoperatorsclaimEURsthatareconsiderablyhigher.

• PartofthedisparityisexplainedbyBOEconversionfactors:abarrelofNGLsiscountedthesameasabarrelofoileventhoughitsenergycontentandvaluearelessthanhalfofabarrelofcrudeoil.

• A6:1naturalgastoboe conversionaccuratelyreflectsenergycontentbutnotvalue.• Sanchezshowshowitarrivesat877boe foranaverageComancheAreawell.• Usingthevalue-basedapproach,theaverageSanchezComanchewellis572boe--adifferenceof

35%.• 877boe alsorepresentsa“3-StreamEUR”consistingofmultiplezonecompletioninupper&lower

EagleFord&AustinChalk.Thisissomewhatmisleadingandrepresents“possible”notprovenreserves.

• Itisunclearhowrepresentative“ComancheArea3”isofSanchez’saveragewells.

ReconcilingStudyEURObservationsWithOperatorClaims

Slide13LabyrinthConsultingServices,Inc. artberman.com

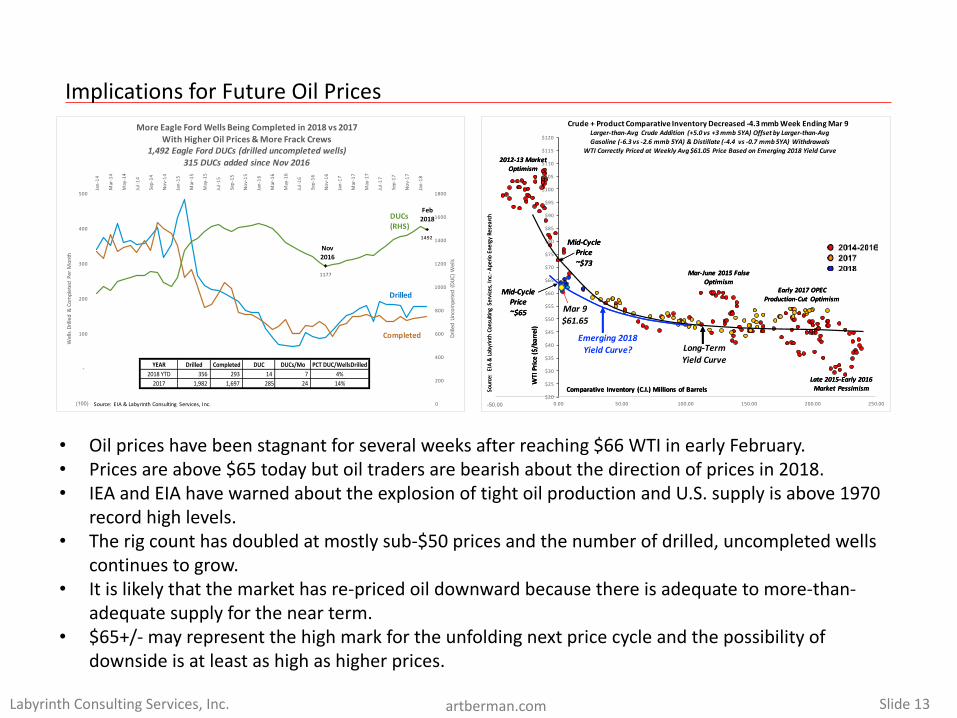

1177

1492

0

200

400

600

800

1000

1200

1400

1600

1800

(100)

-

100

200

300

400

500

Jan-14

Mar-14

May-14

Jul-1

4

Sep-14

Nov-14

Jan-15

Mar-15

May-15

Jul-1

5

Sep-15

Nov-15

Jan-16

Mar-16

May-16

Jul-1

6

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-1

7

Sep-17

Nov-17

Jan-18

DrilledUncom

peted(DUC)W

ells

WellsDrilled&Com

pletedPerM

onth

MoreEagleFordWellsBeingCompletedin2018vs2017WithHigherOilPrices&MoreFrackCrews

1,492EagleFordDUCs(drilleduncompletedwells)315DUCsaddedsinceNov2016

DUCs(RHS)

Drilled

Completed

Source:EIA&LabyrinthConsulting Services,Inc.

EAGLEFORD

YEAR Drilled Completed DUC DUCs/Mo PCTDUC/WellsDrilled2018YTD 356 293 14 7 4%2017 1,982 1,697 285 24 14%

Nov2016

Feb2018

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

$100

$105

$110

$115

$120

-50.00 0.00 50.00 100.00 150.00 200.00 250.00

Crude+ProductComparativeInventoryDecreased-4.3mmbWeekEndingMar9

Comparative Inventory (C.I.)Millionsof Barrels

WTIPrice($/barrel)

Source:EIA

&LabyrinthConsultingServices,Inc.-Aperio

EnergyResearch

Mar-June 2015FalseOptimism

Early 2017OPECProduction-Cut Optimism

2012-13MarketOptimism

Late2015-Early2016MarketPessimism

Mid-CyclePrice~$65

Mid-CyclePrice~$73

Long-TermYieldCurve

Emerging2018YieldCurve?

Comparative Inventory (C.I.)Millionsof Barrels

WTIPrice($/barrel)

Source:EIA

&LabyrinthConsultingServices,Inc.-Aperio

EnergyResearch

Mar-June 2015FalseOptimism

Early 2017OPECProduction-Cut Optimism

2012-13MarketOptimism

Late2015-Early2016MarketPessimism

Mid-CyclePrice~$65

Mid-CyclePrice~$73

Mar9$61.65

Larger-than-Avg CrudeAddition (+5.0vs+3mmb5YA)OffsetbyLarger-than-AvgGasoline(-6.3vs-2.6mmb5YA)&Distillate(-4.4vs-0.7mmb5YA)Withdrawals

WTICorrectly PricedatWeeklyAvg$61.05PriceBasedonEmerging2018YieldCurve

ImplicationsforFutureOilPrices

• Oilpriceshavebeenstagnantforseveralweeksafterreaching$66WTIinearlyFebruary.• Pricesareabove$65todaybutoiltradersarebearishaboutthedirectionofpricesin2018.• IEAandEIAhavewarnedabouttheexplosionoftightoilproductionandU.S.supplyisabove1970

recordhighlevels.• Therigcounthasdoubledatmostlysub-$50pricesandthenumberofdrilled,uncompletedwells

continuestogrow.• Itislikelythatthemarkethasre-pricedoildownwardbecausethereisadequatetomore-than-

adequatesupplyforthenearterm.• $65+/- mayrepresentthehighmarkfortheunfoldingnextpricecycleandthepossibilityof

downsideisatleastashighashigherprices.

Slide14LabyrinthConsultingServices,Inc. artberman.com

ConcludingObservations

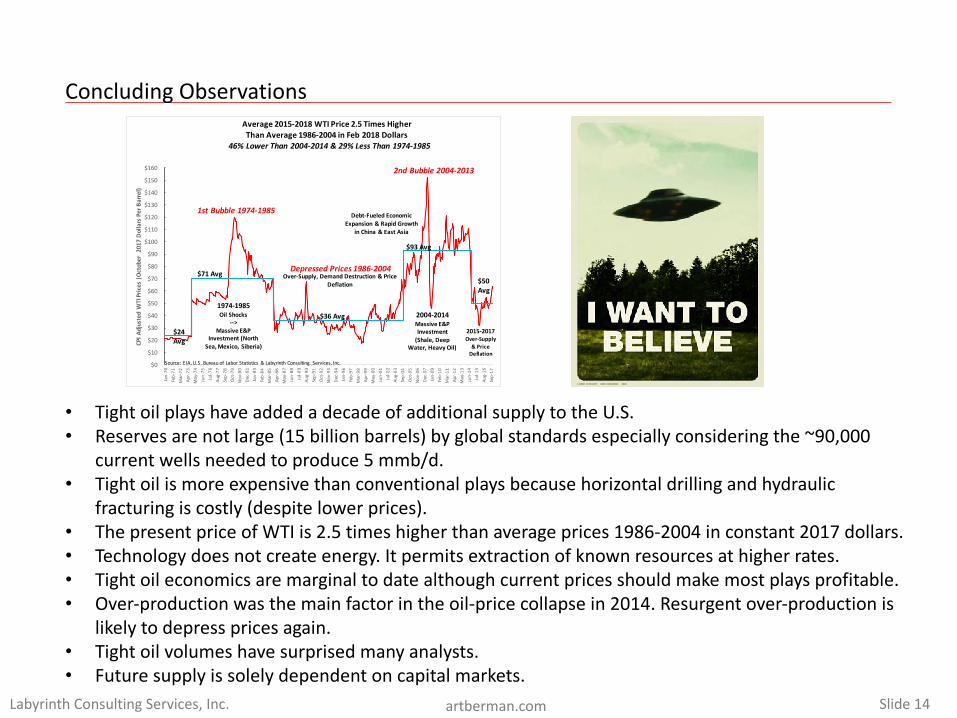

• TightoilplayshaveaddedadecadeofadditionalsupplytotheU.S.• Reservesarenotlarge(15billionbarrels)byglobalstandardsespeciallyconsideringthe~90,000

currentwellsneededtoproduce5mmb/d.• Tightoilismoreexpensivethanconventionalplaysbecausehorizontaldrillingandhydraulic

fracturingiscostly(despitelowerprices).• ThepresentpriceofWTIis2.5timeshigherthanaverageprices1986-2004inconstant2017dollars.• Technologydoesnotcreateenergy.Itpermitsextractionofknownresourcesathigherrates.• Tightoileconomicsaremarginaltodatealthoughcurrentpricesshouldmakemostplaysprofitable.• Over-productionwasthemainfactorintheoil-pricecollapsein2014.Resurgentover-productionis

likelytodepresspricesagain.• Tightoilvolumeshavesurprisedmanyanalysts.• Futuresupplyissolelydependentoncapitalmarkets.

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

$160Jan-70

Feb-71

Mar-72

Apr-73

May-74

Jun-75

Jul-7

6 Au

g-77

Sep-78

Oct-79

Nov-80

Dec-81

Jan-83

Feb-84

Mar-85

Apr-86

May-87

Jun-88

Jul-8

9 Au

g-90

Sep-91

Oct-92

Nov-93

Dec-94

Jan-96

Feb-97

Mar-98

Apr-99

May-00

Jun-01

Jul-0

2 Au

g-03

Sep-04

Oct-05

Nov-06

Dec-07

Jan-09

Feb-10

Mar-11

Apr-12

May-13

Jun-14

Jul-1

5 Au

g-16

Sep-17

CPIAdjustedW

TIPrices(October2017DollarsPerBarrel)

1974-1985OilShocks

-->

Massive E&PInvestment(North

Sea,Mexico,Siberia)

Over-Supply, DemandDestruction&Price

Deflation

Debt-FueledEconomic

Expansion&RapidGrowth

inChina&EastAsia

2004-2014MassiveE&PInvestment

(Shale, DeepWater,HeavyOil)

2015-2017Over-Supply

&Price

Deflation

Average2015-2018WTIPrice2.5TimesHigher

ThanAverage1986-2004inFeb2018Dollars

Source:EIA, U.S.Bureau ofLaborStatistics &LabyrinthConsulting Services,Inc.

$36Avg

1stBubble 1974-1985

2ndBubble2004-2013

$93Avg

$71Avg

$24

Avg

$50

Avg

DepressedPrices 1986-2004

46%LowerThan2004-2014&29%LessThan1974-1985