Embed Size (px)

Citation preview

CFA Institute

The Value Creation Potential of High-Tech MergersAuthor(s): Ninon Kohers and Theodor KohersSource: Financial Analysts Journal, Vol. 56, No. 3 (May - Jun., 2000), pp. 40-50Published by: CFA InstituteStable URL: http://www.jstor.org/stable/4480246 .

Accessed: 15/06/2014 17:48

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

CFA Institute is collaborating with JSTOR to digitize, preserve and extend access to Financial AnalystsJournal.

http://www.jstor.org

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

The Value Creation Potential of High-Tech Mergers

Ninon Kohers and Theodor Kohers

The distinctive high-growth, high-risk nature of technology-based industries raises important questions about the creation of wealth in high- tech takeovers. Do investors perceive acquisitions of high-tech targets to have strong potential for value creation? Or, given the large degree of uncertainty associated with many high-tech companies, is the market skeptical of the potential benefits of high-tech acquisitions? Our results show that acquirers of high-tech targets experience significantly positive abnormal returns, regardless of whether the merger isfinanced with cash or stock. Factors influencing bidder returns are the time period in which the merger occurs, the ownership structure of the acquirer, the high-tech affiliation of acquirers, and the ownership status of the target.

I n recent years, high-tech companies have emerged as leaders in the economy through their technological advancements, their job growth creation, and their contribution to

efficiency gains. According to a report by the Orga- nization for Economic Cooperation and Develop- ment, more than half of the total GDP in the wealthy economies of the world is based on high- tech industries, such as telecommunications, com- puters, software, and pharmaceuticals; in the United States, high-tech sectors have cut an esti- mated half percentage point off inflation because of cost savings and productivity gains.1

Relatively high rates of growth are a notable feature of companies operating in high-tech sectors. In the 1993-96 period, the growth of high-tech stocks far outpaced other sectors, and high-tech stocks provided annual returns of 35 percent, in comparison with the 20 percent annual returns of the S&P 500 Index.2 In 1998, the value of large technology companies increased more than 85 per- cent and the value of communications technology companies rose more than 100 percent.3 The high- tech sector continues to drive the U.S. economy. Since mid-1994, technology indexes have climbed twice as fast as the S&P 500.4

As might be expected, takeover activity in high-tech industries has soared as acquirers seek to capitalize on the growth potential offered by high- tech companies. For example, takeovers in infor-

mation technology and communications increased 92 percent in just the first half of 1999, and these deals accounted for $1 out of every $3 spent by acquirers worldwide.5

The high-growth nature of technology-based industries distinguishes them from other types of industries. For example, as compared with lower- growth target companies, targets from high-tech sectors may be able to provide greater shareholder wealth benefits to acquiring companies. In addition to their high-growth potential, however, another distinctive feature of high-tech industries is the inherent uncertainty associated with companies whose values rely on future outcomes or develop- ments in unproven, uncharted fields. For example, the value of a biotechnology company that is devel- oping a new drug or medical device depends heavily on the success or failure of the new product. Furthermore, some high-tech companies are not expected to generate any cash flow in the near future, which makes their valuation riskier for the bidder than in many other merger and acquisition (M&A) situations. Thus, from the perspective of bidder shareholders, the attractive growth pros- pects a high-tech target offers can come with a high price tag, especially because the prospects may never actually be realized.

In contrast to more established fields, it is the function of high-tech companies to develop and manufacture new, cutting-edge technology, and it is the inherent uncertainty of this technological innovation that produces the unique risks of these emerging areas.6 These characteristics raise some interesting questions about the creation of wealth in high-tech M&As.

Ninon Kohers is assistant professor of finance at the University of South Florida. Theodor Kohers is professor of finance and international business at Mississippi State University.

40 2 02000, Association for Investment Management and Research

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

The Value Creation Potential of High-Tech Mergers

Given the risk factors, the types of bidders that engage in these transactions would be expected to have some degree of confidence in their ability to make a success of acquisitions in high-tech areas. These acquirers would also need to instill such confidence in their investors. If acquirers are will- ing to pay high premiums for these high-risk investments, how do shareholders of acquiring companies perceive these deals? Are investors gen- erally optimistic about the potential synergies of acquiring high-tech targets? What is the overall effect of these M&As on the shareholder wealth of acquiring companies?

Previous studies examining the market reac- tion to merger announcements by acquiring com- panies found that investors tend to be skeptical about the benefits of the acquisitions.7 This market skepticism may also apply to high-tech mergers if acquiring-company investors perceive the take- overs as an expensive way for acquirers to obtain enhanced growth. But although high-tech merg- ers have received considerable attention from analysts, investors, and the financial press, the M&A literature is lacking specific examination of this distinctive type of takeover.8 Our study pro- vides evidence on the shareholder wealth implica- tions of takeovers in high-growth, high-risk fields that require the most sophisticated equipment and advanced engineering techniques and examines how these unique features influence the perceived value creation of this type of corporate combina- tion. Given the increasingly prominent role high- tech industries play in the current economy and the distinct high-growth/high-risk profile of high-tech companies, this article fills an important niche in the M&A literature.

Predictions for High-Tech Mergers The distinctive nature of mergers in high-tech industries prompted this examination of the conse- quences of these types of investments for share- holders. The first set of hypotheses described here addresses the overall effect of high-tech takeovers on acquiring-company wealth; the remaining hypotheses focus on the factors that explain cross- sectional variations in the shareholder wealth effects of acquirers.

Shareholder Wealth Effects. We consider in this section the benefits, costs, and methods of payment involved in high-tech mergers and acquisitions.

M Growth benefits versus costs. High-tech tar- gets possess desirable growth opportunities, which makes them well equipped to create value in merg- ers for bidder companies. Furthermore, given the

increasing reliance of companies on technology, the acquisition of the technology itself may increase the competitiveness of an acquiring company.

Recently, investors have demonstrated consid- erable optimism about the future growth of technology-based companies involved in emerg- ing, cutting-edge fields, such as computers, soft- ware, and communications.9 The lofty valuations of many Internet companies, which are often not expected to produce positive earnings in the near future, provide some indication of the favorable perception of companies involved in certain high- tech pursuits. One hypothesis is that acquiring these attractive growth opportunities causes posi- tive reactions from bidder-company investors, who are optimistic about the future benefits of the investment. Bidder-company shareholders are likely to believe that the growth potential high-tech targets provide is well worth the cost.

The uncertainty surrounding high-tech opera- tions, however, and the unproven nature of the industries may make acquiring-company share- holders especially wary of the future merits of the merger. Thus, a competing hypothesis is that bidder-company shareholders believe the growth potential is not worth the cost. If acquiring-company shareholders believe that the acquirer has overpaid for the growth prospects, abnormal returns for bid- ders will be negative (see Kaplan 1989).

g Acquirer qualifications. We also expected that acquirers who are willing to undertake acqui- sitions in emerging areas would have some degree of confidence in their abilities to manage the acqui- sitions. Consequently, the types of bidders that engage in these high-risk transactions should them- selves be relatively attractive performers that are better able than poor performers to convince their shareholders of their ability to create value through the takeover.

9 Financing: stock versus cash. Previous research examining method-of-payment effects in mergers has shown that in stock offers, acquiring companies often experience negative abnormal returns and in cash offers, the acquirers' abnormal returns tend to be insignificant.10 Wealth effects on targets' shareholders are generally positive in both types of offers, although the average returns are higher in cash offers. Many of the theories explain- ing these shareholder reactions are based on signal- ing or agency models.

In analyzing the factors that influence the method-of-payment choice, Martin (1995) noted that the use of stock financing in acquisitions allows greater financial flexibility for companies with attractive growth opportunities and thus provides them the mluch-needed freedom to take advantage of the investment opportunities as they arise. Such

May/June 2000 41

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

results showing a relationship between method-of- payment choice and an acquiring company's investment opportunities are consistent with evi- dence from the capital structure literature. For example, Jung, Kim, and Stulz (1996) found that companies with the most valuable investment opportunities do not experience significant nega- tive abnormal returns when they issue equity. In addition, to allow for the use of the pooling method instead of the purchase method in accounting for the acquisition, acquirers in high-tech takeovers may actually prefer stock financing to cash financ- ing so that they can avoid recording large amounts of accounting goodwill. The hypothesis we tested is that, overall, if the market perceives high-tech acquisitions as a means to increased growth oppor- tunities for the bidder, stock offers used in high-tech takeovers should be viewed positively by the mar- ket. To test this theory, we used indicator variables to distinguish between stock offers and cash offers.

Factors Influencing Shareholder Wealth Effects. The following hypotheses address fac- tors that we expected to influence cross-sectional differences in the market response to bidders' high- tech merger announcements. These predictions focus on the time period during which the takeover occurred, the growth stage of the target (proxied by public versus private ownership), the bidder's involvement in high-tech operations, and the own- ership structure of the bidder.

M Time period. To capture possible shifts in merger motivations from the 1980s to the 1990s, we controlled for the time period in which the merger occurred. For example, in the 1980s, much of the corporate restructuring focused on streamlining inefficient conglomerate companies that resulted from diversification moves made in earlier years. Many of the mergers in the 1990s, however, appear to have been motivated by the search for synergies and enhanced competitiveness through increased focus on a company's core businesses and/or acquisition of technologies. Given the dramatic increase in the role of technology in the operations of companies in recent years, we hypothesized that the market reaction to high-tech mergers would be more positive in the later time period.

M Stage of target's growth. Privately held high- tech targets tend to be smaller, younger companies and in earlier stages of growth than their publicly traded counterparts. Because their limited access to capital may be preventing them from realizing their true growth potential, these financially con- strained companies may be able to provide sub- stantial growth benefits once given access to the financial resources of the bidder. Thus, the market may perceive that the growth opportunities of pri-

vately held high-tech companies are more valuable than those of publicly traded high-tech companies. In other words, we expected the marginal benefits of access to bidders' resources to be lower for pub- licly traded companies. Consequently, we hypoth- esized that the bidders' market response would be lower in acquisitions of publicly traded high-tech companies.

X High-tech acquirers. Previous studies have found that, on average, focus-increasing transac- tions enhance shareholder wealth whereas diversi- fying takeovers decrease shareholder wealth.11 In examining high-tech industries in particular, we hypothesized that the market's reaction would be more positive for mergers between acquirers and targets when both were involved in high-tech lines of business. This expectation suggested that the bidder-company abnormal returns would be higher for takeover announcements made by acquirers also in high-tech fields than for announcements by non-high-tech acquirers.

M Ownership structure of the acquirer. A num- ber of studies have indicated that companies with managers as owners generally have fewer agency problems than companies with less or no manage- rial ownership.12 Some studies, however, have noted that high levels of insider ownership may be associated with management entrenchment and, therefore, have adverse consequences for company performance.13 Similar to studies by McConnell and Servaes, Stulz, Han (1998), and Denis, Denis, and Sarin (1997), we used an insider ownership variable and a squared insider ownership term to control for the nonlinear effects of managerial own- ership on a bidder's excess returns. Given the pre- vious evidence on insider ownership and company performance, our next hypothesis was that a mod- erate level of insider ownership would be posi- tively related to bidder returns but a high level of insider ownership would be negatively associated with bidder returns.

In addition, previous studies that examined the role of institutional ownership in affecting com- pany performance suggested that institutional investors may serve as effective monitors of com- pany managers.14 If institutional investors act to alleviate agency problems and discourage poor decisions made by entrenched managers, then a positive relationship would be expected between institutional ownership and a bidder's long-run performance. Other arguments, however, hold that institutional investors do not generally act as effec- tive monitors. For example, Pound (1988) noted that institutional investors can actually exacerbate the problem of management entrenchment through their endorsement of incumbent managers during proxy fights. Furthermore, some have

42 ?2000, Association for Investment Management and Research

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

The Value Creation Potential of High-Tech Mergers

argued that institutional investors have myopic investment objectives, which causes them to sell the stock of an underperforming company rather than actively attempt to make value-enhancing changes at the company through vigilant monitoring.15 Also, given that institutional owners tend to be sophisticated, experienced investors, they may be more deliberate and conservative than individual investors in their assessments of high-tech takeover decisions. Individual investors may be more prone to speculative optimism about high-growth com- panies involved in technological innovations and cutting-edge operations (as in "dot com fever"). In this case, one would expect to find an insignificant, or even negative, relationship between institu- tional ownership and bidder abnormal returns.

M Bidder size versus deal size. In addition, because some previous studies found that target companies that are large relative to their acquirers are able to provide greater s nergies in mergers than small targets can offer, we also tested this hypothesis on our sample.

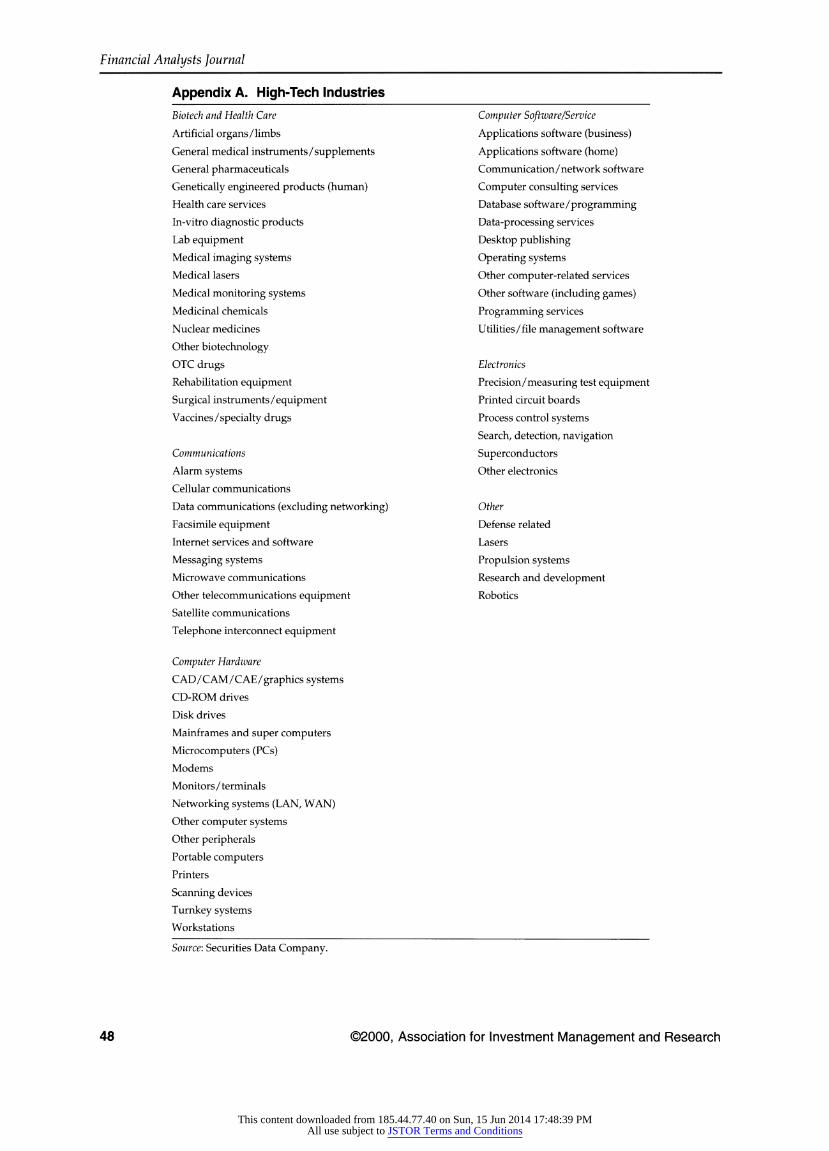

Methodology and Sample Analysis High-tech industry identifications were based on classifications made by Securities Data Company (SDC) and included areas in biotechnology, chemi- cals, computers, defense, electronics, communica- tions, medical, and pharmaceuticals, among others. Appendix A provides a list of the high-tech industry sectors. The merger announcement dates and other merger-related information came from SDC's Merg- ers and Acquisitions database, and the stock return data and other financial information came from the CRSP and Compustat databases. After we obtained the necessary return data, the sample numbered 1,634 mergers in the various high-tech areas that occurred between January 1987 and April 1996.

Abnormal returns were calculated by subtract- ing the expected return for a security from the actual return for that security. Using the standard market model, we defined the abnormal return for security i on day t to be the actual return, Ri t, minus the security's expected return, Qi + OiRmt:

Ait = Rit -

&i + f3iRmt)I

where &i and Pi were obtained from the ordinary least-squares (OLS) regression of security returns with market returns during the estimation period and Rmt is the return on the market index for day t. We used the CRSP value-weighted index as the market index proxy. Also, the estimation period used in the OLS regression spanned Day -300 to Day -51, where Day 0 denotes the event day-that is, the day on which the merger was first announced

to the public (e.g., at a news conference)-and Day 1 denotes the day on which the news item may have first appeared in the press.

The regression model used to test the hypoth- eses that predicted the factors influencing bidder- company abnormal returns was as follows (with expected relationship signs in parentheses):

CAR(Bidder) = f [ERA (+); PUB (-); TEKBID (+);

INSIDER (+); INSIDER2 (-); INSTIT (+?-); STOCK (+/-); RELSIZE (+)]

where

CAR(Bidder) = the two-day cumulative abnor- mal return for the bidder on Day 0, the announcement day, and Day 1

ERA = 1 if the takeover occurred dur- ing the 1990s; 0 if the takeover occurred during the 1980s

PUB = 1 if the target was a public company; 0 otherwise

TEKBID = 1 if the acquirer was from a high-tech industry; 0 otherwise

INSIDER = the percentage of insider own- ership in the acquirer during the year prior to the merger announcement

INSIDER2 = the squared percentage of in- sider ownership to capture nonlinearities in insider own- ership effects

INSTIT the percentage of institutional ownership in the acquirer dur- ing the year prior to the merger announcement

STOCK 1 if the merger involved stock financing; 0 otherwise

RELSIZE = the relative transaction size: Transaction value/ [(Acquirer's market value on day t - 11) + Transaction value]

We expected an examination of these factors to help explain the cross-sectional variations in market reac- tions to high-tech takeovers.

Results Summary descriptive statistics for the high-tech mergers are reported in Table 1. Panel A contains key bidder characteristics and merger deal infor- mation. The mean transaction value for the high- tech acquisitions, or the average amount paid for the high-tech targets, in the period was $125.78 million, but many of the deals involved relatively small high-tech companies, as reflected in the smaller median transaction value. Also, bidders, on average, were notably larger than their targets.

May/June 2000 43

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

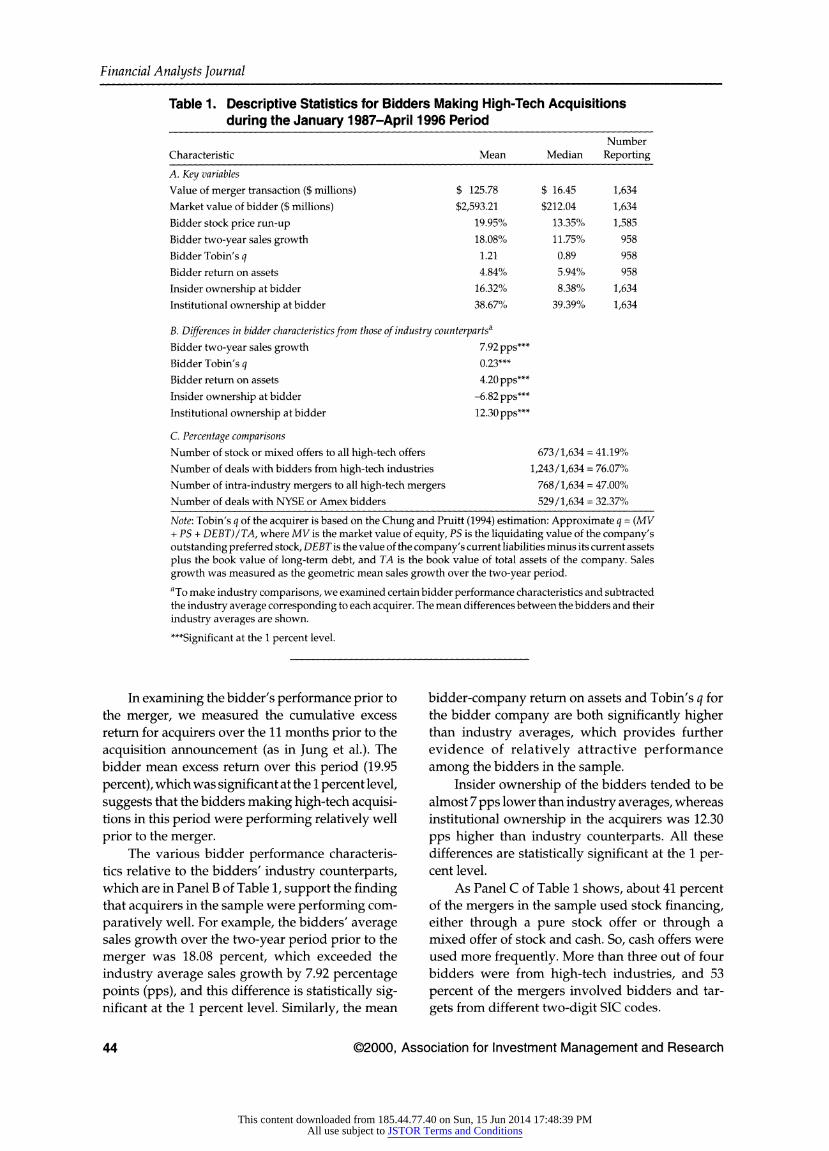

Table 1. Descriptive Statistics for Bidders Making High-Tech Acquisitions during the January 1987-April 1996 Period

Number Characteristic Mean Median Reporting

A. Key variables Value of merger transaction ($ millions) $ 125.78 $ 16.45 1,634 Market value of bidder ($ millions) $2,593.21 $212.04 1,634 Bidder stock price run-up 19.95% 13.35% 1,585 Bidder two-year sales growth 18.08% 11.75% 958 Bidder Tobin's q 1.21 0.89 958 Bidder return on assets 4.84% 5.94% 958 Insider ownership at bidder 16.32% 8.38% 1,634 Institutional ownership at bidder 38.67% 39.39% 1,634

B. Differences in bidder characteristics from those of industry counterpartsa Bidder two-year sales growth 7.92 pps*** Bidder Tobin's q 0.23*** Bidder return on assets 4.20 pps'**

Insider ownership at bidder -6.82 pps*** Institutional ownership at bidder 12.30 pps***

C. Percentage comparisons Number of stock or mixed offers to all high-tech offers 673/1,634 = 41.19% Number of deals with bidders from high-tech industries 1,243/1,634 = 76.07% Number of intra-industry mergers to all high-tech mergers 768/1,634 = 47.00% Number of deals with NYSE or Amex bidders 529/1,634 = 32.37%

Note: Tobin's q of the acquirer is based on the Chung and Pruitt (1994) estimation: Approximate q = (MV + PS + DEBT)/TA, where MV is the market value of equity, PS is the liquidating value of the company's outstanding preferred stock, DEBT is the value of the company's current liabilities minus its current assets plus the book value of long-term debt, and TA is the book value of total assets of the company. Sales growth was measured as the geometric mean sales growth over the two-year period.

'To make industry comparisons, we examined certain bidder performance characteristics and subtracted the industry average corresponding to each acquirer. The mean differences between the bidders and their industry averages are shown.

***Significant at the 1 percent level.

In examining the bidder's performance prior to the merger, we measured the cumulative excess return for acquirers over the 11 months prior to the acquisition announcement (as in Jung et al.). The bidder mean excess return over this period (19.95 percent), which was significant at the 1 percent level, suggests that the bidders making high-tech acquisi- tions in this period were performing relatively well prior to the merger.

The various bidder performance characteris- tics relative to the bidders' industry counterparts, which are in Panel B of Table 1, support the finding that acquirers in the sample were performing com- paratively well. For example, the bidders' average sales growth over the two-year period prior to the merger was 18.08 percent, which exceeded the industry average sales growth by 7.92 percentage points (pps), and this difference is statistically sig- nificant at the 1 percent level. Similarly, the mean

bidder-company return on assets and Tobin's q for the bidder company are both significantly higher than industry averages, which provides further evidence of relatively attractive performance among the bidders in the sample.

Insider ownership of the bidders tended to be almost 7 pps lower than industry averages, whereas institutional ownership in the acquirers was 12.30 pps higher than industry counterparts. All these differences are statistically significant at the 1 per- cent level.

As Panel C of Table 1 shows, about 41 percent of the mergers in the sample used stock financing, either through a pure stock offer or through a mixed offer of stock and cash. So, cash offers were used more frequently. More than three out of four bidders were from high-tech industries, and 53 percent of the mergers involved bidders and tar- gets from different two-digit SIC codes.

44 ?2000, Association for Investment Management and Research

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

The Value Creation Potential of High-Tech Mergers

Premiums for High-Tech Targets versus Non-High-Tech Targets. To examine whether high-tech targets are paid higher premiums than non-high-tech targets, we used a control sample of mergers involving non-high-tech companies. The premium information was limited because market- determined premium measures are available only for publicly traded targets. Thus, in Table 2, the one- day, one-week, and four-week premiums apply to publicly traded high-tech companies and a compar- ison sample of all publicly traded non-high-tech companies with sufficient premium information. In particular, we measured the one-day premium as the percentage difference between the amount paid for the target and its market value one day prior to the merger announcement. The one-week and four- week premiums were measured similarly over those time frames. The results show that the high- tech targets were paid significantly higher premi- ums than non-high-tech target companies over all three time intervals. The last line of Table 2 provides the ratio of the offer price-to-book value of equity (offer P/B), or the total amount paid relative to the target's book value of equity, for private as well as public targets.17 The mean offer P/B for the high- tech companies was almost twice as much as the corresponding measure for the non-high-tech com- panies. The offer P/B and the one-day, one-week, and four-week premiums for high-tech targets are significantly higher at the 1 percent significance level than the corresponding premiums for non- high-tech targets. Overall, the results presented in Table 2 suggest that high-tech targets do receive relatively attractive premiums when compared with mergers involving non-high-tech targets.

Abnormal Return Analysis. Examining the stock-price reaction to high-tech mergers tests the growth benefits versus costs hypothesis. As shown in Table 3, the acquirers of high-tech companies

Table 2. Premiums Paid in High-Tech versus Non-High-Tech Target Takeovers, January 1987-April 1996

High-Tech Non-High-Tech Mergers Mergers

One-day premium 37.89% 29.21% (n = 226) (n = 1,914)

One-week premium 37.41% 30.47% (n = 226) (n = 1,914)

Four-week premium 45.13% 33.26% (n = 226) (n = 1,914)

Offer-to-book value 6.89 3.70

(n = 409) (n = 1,589)

experienced, on average, significant positive cumu- lative abnormal return in the two-day event period, CAR0,1, of 1.26 percent. This result supports the predictions made by the high-tech growth benefits hypothesis. Thus, the market tends to assess acqui- sitions of high-tech targets as attractive investments. The relatively strong premerger performance of acquirers making high-tech acquisitions (shown in Table 1) would help instill confidence in bidder- company investors about the acquirers' ability to create value in these high-risk deals.

Table 3. Bidder Abnormal Returns in High-Tech Mergers during the January 1987- April 1996 Period by Method of Payment

Asset Bidder CAR0,1 Observations

Cash 1.37%*** 961 Stock 1.09*** 673

All 1.26*** 1,634

***Significant at the 1 percent level.

Because the method of payment used in merg- ers has been known to have significant shareholder implications, we also compared the returns of high- tech bidders using different means of payment. Table 3 shows that for high-tech bidders, the CARo, 1 is positive regardless of the payment method. This result supports the hypothesis that stock offers used to finance high-growth investments are viewed favorably by the market and is in agreement with the findings of Jung et al. and Martin.18

Analysis of Factors. In this section, we turn to the various factors that were hypothesized to influence the shareholder wealth effect of high-tech takeovers.

M Excess returns over time. In addition to the cross-sectional regression to be discussed later, we carried out a separate analysis of changes in share- holder wealth effects over time. As Table 4 shows, returns to companies that acquired high-tech tar- gets show a distinct upward trend from the first subperiod to the most recent subperiod. The differ- ence between the bidder CAR in the earliest period (0.69 percent) and the latest period (1.58 percent) is significant at the 5 percent level.

This trend differs from the commonly observed general market trend of decreasing bidder excess returns over time (Weston, Chung, and Siu 1998). Our findings suggest that the positive perception of acquiring-company investors in high-tech acquisi- tions has grown more favorable over time as new high-tech areas have emerged, existing fields have developed and evolved, and companies' reliance on technology has increased.

May/June 2000 45

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

Table 4. Bidder Abnormal Returns in High-Tech Mergers over Time

Bidder Time CARo,1 p-Value Observations

1987-89 subperiod 0.69% 0.0225 437

1990-92 subperiod 1.15 0.0013 330

1993-April 1996 subperiod 1.58 0.0001 867

Total period 1.26 0.0063 1,634

Note: Statistically significant differences from zero are indicated by the p-values.

M Cross-sectional regression model. We used the following cross-sectional regression model to test the hypotheses predicting that various factors would explain cross-sectional differences in the shareholder wealth effects of high-tech takeovers:

CAR(Bidder)i = At + f, ERAi + f2PUBi + 33TEKBIDi

+ I4INSIDERi + f3INSIDER7

+ f6INSTITi + 37STOCKi

+ f8RELSIZEi + ci,

where ? is the error term and all other variables are as previously defined.

Overall, as shown in Table 5, the regression, which used 1,634 acquisitions involving high-tech targets, is significant at the 1 percent level. First, the relationship between bidders' CARo 1 and ERA was found to be positive and significant at the 5 percent level, which supports the finding in Table 4 that investor sentiment toward acquisitions of high-tech companies has grown more positive over time. The increasing media coverage in recent years may have contributed to heightened market awareness of the enormous growth potential of high-tech companies involved in mergers.

Another factor that appears to boost investor confidence about the merits of high-tech invest- ments, as shown by the TEKBID results in Table 5, is whether the acquiring company is also from a high-tech industry. This finding is significant at the 1 percent level. In accordance with the high- tech acquirer hypothesis discussed earlier, bidder- company investors appear to be more optimistic about the high-tech acquisition decisions of com- panies that are also involved in fields dealing with emerging technology. Investors may anticipate larger growth benefits to result from the combina- tion of two high-tech companies.

In addition to the acquirer's industry affilia- tion, the target's ownership status also influences the market's perception of high-tech acquisitions. Specifically, the coefficient for PUB, the public tar- get indicator variable, was found to be negative and significant at the 1 percent level, which shows that acquisitions of public high-tech targets cause less favorable reactions from bidder-company share- holders than do acquisitions of private high-tech targets (which is consistent with Hansen and Lott 1996). In agreement with the stage of growth hypothesis, this finding suggests that the market expects greater contributions from a young, pri- vately held high-tech company whose growth can be spurred by the financial resources of the bidder than from an older, publicly held target.

An examination of the influence of the bidder's ownership structure shows that both insider owner- ship and institutional ownership have an effect on the bidder's abnormal returns at the time of the high-tech merger announcement. In particular, as indicated by the positive sign of INSIDER, which is significant at the 5 percent level, the acquirer's insider ownership has a positive effect on acquirer returns up to a certain point. These results suggest that at moderate levels of managerial ownership,

Table 5. Factors Explaining Bidder Shareholder Wealth Effects of Takeovers in High-Tech Industries during the January 1987-April 1996 Period

Independent Variable Estimate t-Statistic

Intercept 0.003 0.40 ERA (1990s versus 1980s mergers) 0.008 1.97** PUB (publicly traded target) -0.016 -4.15*** TEKBID (high-tech acquirer) 0.010 2.54*** INSIDER (insider ownership in bidder) 0.0004 2.05** INSIDER2 (insider ownership in bidder)2 -4.0 x E-6 -1.57 INSTIT (institutional ownership in bidder) -0.0002 -2.20** STOCK (stock financing) -0.005 -1.56 RELSIZE (relative transaction size) 0.037 3.62*** F-statistic 8.65***

Note: The number of observations was 1,634. The t-statistics were adjusted for heteroscedasticity using White's correction.

**Significant at the 5 percent level. ~**Significant at the 1 percent level.

46 ?2000, Association for Investment Management and Research

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

The Value Creation Potential of High-Tech Mergers

agency problems may be alleviated when managers are also owners of the company. The squared insider ownership term, INSIDER2, is negative, however, although not significant. This finding implies, con- sistent with the conclusions of Stulz, McConnell and Servaes, and Han, that excessive insider ownership may be associated with managerial entrenchment, which would not improve the market's enthusiasm for a high-tech merger. Also, the negative coefficient for INSTIT suggests that higher institutional owner- ship is associated with lower abnormal returns for bidders. This outcome could be attributable to a more reserved and discriminating assessment of the prospects of the consolidated companies by institu- tional owners than by individual investors. The average individual investor tends to be less sophis- ticated and experienced than institutional investors, which may be less likely to engage in speculative enthusiasm for high-growth companies operating in highly uncertain fields.

The method-of-payment findings for high- tech mergers, the STOCK variable, lend support to the hypothesis that offers using stock to purchase high-tech companies do not necessarily produce adverse reactions from bidder-company investors. The coefficient of STOCK is insignificant, which indicates that the market perceptions of stock- financed and cash-financed mergers do not differ notably. This result is consistent with Martin and with Jung et al., who showed that the growth opportunities of the acquiring company play an influential role in shaping the market's perception of the merits of an investment. More specifically, this result suggests that the market reaction to a merger announcement reflects investors' collective assessment of the bidder's investment decision. This investor response is not, as treated in many previous studies, a simple automatic reaction to the choice of stock financing, whereby investors assume the use of stock implies stock overvalua- tion. In addition, given that large amounts of accounting goodwill are created in cash offers, acquirers of high-tech companies may actually pre- fer to use stock financing so that they can avoid the recording of goodwill. This choice of pooling over purchase accounting could, in part, account for the relatively favorable stock-price reaction to stock offers used in high-tech acquisitions. At the same time, however, previous studies examining the relationship between the pooling method and bid- der returns did not find a significant positive rela- tionship between this accounting choice and abnormal returns of acquirers.19

Finally, our examination of the size effects of high-tech takeovers, based on the RELSIZE results in Table 5, revealed a positive relationship between bidder excess returns and the size of the transaction relative to the acquirer's size. Thus, the sharehold-

ers of acquiring companies believe, on average, that larger high-tech targets are better able than small targets to provide synergies in a merger.20

Conclusions The high-growth, high-risk nature of industries dependent on the development and use of new and emerging technologies makes these industries dis- tinct from more moderately or more slowly grow- ing areas and raises some interesting questions about the creation of wealth in high-tech mergers and acquisitions. the results of this study indicate that acquirers of high-tech targets experience sig- nificantly positive abnormal returns at the time of the merger announcement regardless of whether the merger is financed with cash or stock. This finding suggests that the market is optimistic about such mergers and expects that, on average, acqui- sitions of high-tech companies will provide future growth benefits for acquiring companies.

In considering the method-of-payment impli- cations of these mergers, investors evidently take into account the nature of the investment for which the financing is being used rather than simply react- ing to the financing decision by assuming that stock offerings necessarily signal overvaluation. We also found the average performance of the acquirers prior to the merger to be significantly higher than their industry-matched competitors, which would help to convince investors that these acquirers are capable of creating value through the acquisition. Overall, the wealth gains for bidder-company shareholders, together with the relatively high pre- miums that high-tech targets receive, indicate that high-tech takeovers provide benefits for both par- ties. Thus, these results suggest that high-tech acquisitions are value enhancing in the short run.

The factors that influenced bidder returns in the study are as follows: the time period in which the merger was announced (with higher abnormal returns in more recent acquisitions); the high-tech affiliation of the acquirer; the growth stage of the target (with takeovers of private targets generating higher bidder abnormal returns than takeovers of public targets); the bidder ownership structure (with moderate levels of insider ownership having a positive relationship and institutional ownership having a negative relationship with bidder returns); and the size of the transaction relative to the bidder (with larger transactions associated with larger bid- der returns).

An interesting area for future research would be an examination of the long-term shareholder wealth implications of high-tech takeovers. Such an investigation would shed light on whether the initial positive reaction from bidder-company shareholders is an unbiased forecast of the future long-term performance of high-tech mergers.

May/June 2000 47

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

Appendix A. High-Tech Industries

Biotech and Health Care Computer Software/Service

Artificial organs/limbs Applications software (business)

General medical instruments/supplements Applications software (home)

General pharmaceuticals Communication/network software

Genetically engineered products (human) Computer consulting services

Health care services Database software/programming

In-vitro diagnostic products Data-processing services

Lab equipment Desktop publishing

Medical imaging systems Operating systems

Medical lasers Other computer-related services

Medical monitoring systems Other software (including games)

Medicinal chemicals Programming services

Nuclear medicines Utilities/file management software

Other biotechnology

OTC drugs Electronics

Rehabilitation equipment Precision/measuring test equipment

Surgical instruments/equipment Printed circuit boards

Vaccines/specialty drugs Process control systems

Search, detection, navigation

Communications Superconductors

Alarm systems Other electronics

Cellular communications

Data communications (excluding networking) Other

Facsimile equipment Defense related

Internet services and software Lasers

Messaging systems Propulsion systems

Microwave communications Research and development

Other telecommunications equipment Robotics

Satellite communications

Telephone interconnect equipment

Computer Hardware

CAD/CAM/CAE/graphics systems

CD-ROM drives

Disk drives

Mainframes and super computers

Microcomputers (PCs)

Modems

Monitors/terminals

Networking systems (LAN, WAN)

Other computer systems

Other peripherals

Portable computers

Printers

Scanning devices

Turnkey systems

Workstations

Source: Securities Data Company.

48 ?)2000, Association for Investment Management and Research

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

The Value Creation Potential of High-Tech Mergers

Notes 1. Buisiness Week (May 25, 1998):32; Economist (September 28,

1996):543. 2. Business Week (March 31, 1997):58. 3. Wall Street Journal (January 4, 1999):R1. 4. Business Week (June 14, 1999):142. 5. USA Today (July 28, 1999):1.B. 6. Economist (January 20, 1996):73. 7. For example, Amihud, Lev, and Travlos (1990); Brown and

Ryngaert (1991); Servaes (1991); Travlos (1987). 8. One of the few studies that focus specifically on high-tech

sectors is by Bessembinder and K aufman (1998), who noted that high-tech stocks are of interest in part because of their high trading volume. In their comparison of high-tech stocks from the NYSE and Nasdaq, the authors found that the volatility and trading costs of technology stocks are lower for those trading on the NYSE.

9. See Business Week (March 31, 1997):58. 10. For example, see Wansley, Lane, and Yang (1983); Hansen

(1987); Huang and Walkling (1987); Travlos; Bradley, Desai, and Kim (1988); Murphy and Nathan (1989); Amihud, Lev, and Travlos; Berkovitch and Narayanan (1990); Brown and Ryngaert; Servaes.

11. For example, Morck, Shleifer, and Vishny (1990); Healy, Palepu, and Ruback (1992); Lang and Stulz (1994); Berger and Ofek (1995); Comment and Jarrell (1995); John and Ofek (1995).

12. Jensen and Meckling (1976); Fama and Jensen (1983); Ami- hud, Dodd, and Weinstein (1986); Morck, Shleifer, and Vishny; Denis, Denis, and Sarin (1997).

13. Stulz (1988); McConnell and Servaes (1990).

14. Jarrell and Poulsen (1987); Brickley, Lease, and Smith (1988); McConnell and Servaes; Han.

15. Jarrell, Lehn, and Marr (1985); Duggal and Millar (1999). 16. Asquith, Bruner and Mullins (1983); Bruner (1988); Song

and Walkling (1993). 17. The choice of a premium variable is severely limited for

privately held targets because these companies do not have market values, which are typically used to measure the premiums for public targets. The offer P/B is the best available premium measure that we could obtain for both private and public targets.

18. The common characteristic of high-tech industries is their focus on the development and use of emerging technology; yet, the different high-tech fields still reflect much diver- sity. To examine whether the market reaction is notably different in different technology areas, we analyzed the bidder two-day CARs broken down by high-tech industry sector. The results revealed significant positive bidder excess returns for each major high-tech group, with no significant differences between the bidder returns in the different high-tech sectors.

19. Hong, Mandelker, and Kaplan (1978); Davis (1990). 20. We also analyzed other variables, such as the bidder's q, its

book-to-market ratio, bidder size, and various bidder lever- age measures, because some studies (e.g., Lang, Stulz, and Walkling 1991; Fama and French 1992) have shown that these factors play an important role in explaining stock returns. Also, we used a dummy variable to distinguish between takeovers of targets in the same industry as the bidder and takeovers of targets in different industries. Of these variables, only bidder size was significant, at the 1 percent level, and it was negative.

References Amihud, Yakov, Peter Dodd, and Mark Weinstein. 1986. "Conglomerate Mergers, Managerial Motives, and Stockholder Wealth." Journal of Banking and Finance, vol. 10, no. 3 (October):401-410.

Amihud, Yakov, Baruch Lev, and Nickolaos G. Travlos. 1990. "Corporate Control and the Choice of Investment Financing: The Case of Corporate Acquisitions." Journal of Finance, vol. 45, no. 2 (June):603-616.

Asquith, Paul, Robert F. Bruner, and David W. Mullins, Jr. 1983. "The Gains to Bidding Firms from Merger." Journal of Financial Economics, vol. 11, no. 1 (April):121-139.

Berger, Philip G., and Eli Ofek. 1995. "Diversification's Effect on Firm Value." Jouirnal of Financial Economics, vol. 37, no. 1 (January):39-65.

Berkovitch, Elazar, and M.P. Narayanan. 1990. "Competition and the Medium of Exchange in Takeovers." Review of Financial Studies, vol. 3, no. 2 (Summer):153-174.

Bessembinder, Hendrik, and Herbert M. Kaufman. 1998. "Trading Costs and Volatility for Technology Stocks." Financial Analysts Jolurnal, vol. 54, no. 5 (September/October):64-71.

Bradley, Michael, Anand Desai, and E. Han Kim. 1988. "Synergistic Gains from Corporate Acquisitions and Their Division between the Stockholders of Target and Acquiring Firms." Jouirnal of Financial Economics, vol. 21, no. 1 (May):3-40.

Brickley, James A., Ronald C. Lease, and Clifford W. Smith, Jr. 1988. "Ownership Structure and Voting on Anti-Takeover

Amendments." Journal of Financial Economics, vol. 20, no. 1/2 (January/March):267-291.

Brown, David T., and Michael D. Ryngaert. 1991. "The Mode of Acquisition in Takeovers: Taxes and Asymmetric Information." Journal of Finance, vol. 46, no. 2 (June):653-669.

Bruner, Robert F. 1988. "The Use of Excess Cash and Debt Capacity as a Motive for Merger." Journal of Financial and Quantitative Analysis, vol. 23, no. 2 (June):199-217.

Chung, Kee H., and Stephen W. Pruitt. 1994. "A Simple Approximation of Tobin's q." Financial Management, vol. 23, no. 3 (Autumn):70-74.

Comment, Robert R., and Gregg A. Jarrell. 1995. "Corporate Focus and Stock Returns." Journal of Financial Economics, vol. 37, no. 1 (January):67-87.

Davis, Michael L. 1990. "Differential Market Reaction to Pooling and Purchase Methods." Accounting Reviezw, vol. 65, no. 3 (July):696-709.

Denis, David J., Diane K. Denis, and Atulya Sarin. 1997. "Agency Problems, Equity Ownership, and Corporate Diversification." Journal of Finance, vol. 52, no. 1 (March):135-160.

Duggal, Rakesh, and James A. Millar. 1999. "Institutional Ownership and Firm Performance: The Case of Bidder Returns." Journal of Corporate Finance, vol.5, no.2 (June):103-117.

Fama, Eugene F., and Kenneth R. French. 1992. "The Cross- Section of Expected Stock Returns." Journal of Finiance, vol. 47, no. 2 (June):427-465.

May/June 2000 49

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

Fama, Eugene F., and Michael C. Jensen. 1983. "Separation of Ownership and Control." Journal of Law & Economics, vol. 26, no. 2 (June):327-349.

Han, Ki C. 1998. "The Effect of Ownership Structure on Firm Performance: Additional Evidence." Review of Financial Economics, vol. 7, no. 2 (Spring):143-152.

Hansen, Robert G., and John R. Lott, Jr. 1996. "Externalities and Corporate Objectives in a World with Diversified Shareholders/ Consumers." Journal of Financial and QuantitativeAnalysis, vol. 30, no. 1 (March):43-68.

Hansen, Robert S. 1987. "A Theory for the Choice of Exchange Medium in Mergers and Acquisitions." Journal of Business, vol. 60, no. 1 (January):75-95.

Healy, Paul M., Krishna G. Palepu, and Richard S. Ruback. 1992. "Does Corporate Performance Improve after Mergers?" Journal of Financial Economics, vol. 31, no. 2 (April):135-175.

Hong, Hai, Gershon Mandelker, and Robert S. Kaplan. 1978. "Pooling vs. Purchase: The Effects of Accounting for Mergers on Stock Prices." Accounting Review, vol. 53, no. 1 (January):31-47.

Huang, Yeng-Sheng, and Ralph A. Walkling. 1987. "Target Abnormal Returns Associated with Acquisition Announcements: Payment Method, Acquisition Form, and Managerial Resistance." Journal of Financial Economics, vol. 19, no. 2 (December):329-350.

Jarrell, Gregg A., and Annette B. Poulsen. 1987. "Shark Repellants and Stock Prices: The Effect of Antitakeover Amendments since 1980." Journal of Financial Economics, vol. 19, no. 1 (September):127-168.

Jarrell, Gregg A., Ken Lehn, and Wayne Marr. 1985. Institutional Ownership, Tender Offers and Long-Term Investments. Washington, DC: Office of the Chief Economist, Securities and Exchange Commission.

Jensen, Michael C., and William H. Meckling. 1976. "Theory of the Firm: Managerial Behavior, Agency Costs, and Ownership Structure." Journal of Financial Economics, vol. 3, no. 4 (October):305-360.

John, Kose, and Eli Ofek. 1995. "Asset Sales and Increase in Focus." Journal of Financial Economics, vol. 37, no. 1 (January):105-126.

Jung, Kooyul, Yong-Cheol Kim, and Rene M. Stulz. 1996. "Timing, Investment Opportunities, Managerial Discretion, and the Security Issue Decision." Journal of Financial Economics, vol. 42, no. 2 (October):159-185.

Kaplan, Steven N. 1989. "Campeau's Acquisition of Federated: Value Destroyed or Value Added?" Journal of Financial Economics, vol. 25, no. 2 (December):191-212.

Lang, Larry H.P., and Rene M. Stulz. 1994. "Tobin's q, Corporate Diversification, and Firm Performance." Journal of Political Economy, vol. 102, no. 6 (December):1248-80.

Lang, Larry H.P., Rene M. Stulz, and Ralph A. Walkling. 1991. "A Test of the Free Cash Flow Hypothesis: The Case of Bidder Returns." Journal of Financial Economics, vol. 29, no. 2 (October):315-336.

Martin, Kenneth. 1995. "The Method of Payment in Corporate Acquisitions, Investment Opportunities, and Management Ownership." Journal of Finance, vol. 50, no.4 (September):1227-46.

McConnell, John J., and Henry Servaes. 1990. "Additional Evidence on Equity Ownership and Corporate Value." Journal of Financial Economics, vol. 27, no. 2 (October):595-612.

Morck, Randall, Andrei Shleifer, and Robert W. Vishny. 1990. "Do Managerial Objectives Drive Bad Acquisitions?" Journal of Finance, vol. 45, no. 1 (March):31-48.

Murphy, Austin, and Kevin Nathan. 1989. "An Analysis of Merger Financing." Financial Review, vol. 24, no. 4 (November):551-566.

Pound, John. 1988. "Proxy Contests and the Efficiency of Shareholder Oversight." Journal of Financial Economics, vol. 20, no. 1/2 (January/March):237-265.

Servaes, Henry. 1991. "Tobin's q and the Gains from Takeovers." Journal of Finance, vol. 46, no. 1 (March):409-419.

Song, Moon H., and Ralph A. Walkling. 1993. "The Impact of Managerial Ownership on Acquisition Attempts and Target Shareholder Wealth." Journal of Finanlcial and Quantitative Analysis, vol. 28, no. 4 (December):439-457.

Stulz, Rene M. 1988. "Managerial Control of Voting Rights: Financing Policies and the Market for Corporate Control." Journal of Financial Economics, vol. 20, no. 1/2 January/March):25-54.

Travlos, Nickolaos G. 1987. "Corporate Takeover Bids, Methods of Payment and Bidding Firms' Stock Returns." Journal of Finance, vol. 42, no. 4 (September):943-964.

Wansley, James W., William R. Lane, and Ho C. Yang. 1983. "Abnormal Returns to Acquired Firms by Type of Acquisition and Method of Payment." Financial Management, vol. 12, no. 3 (Autumn):16-22.

Weston, J. Fred, Kwan S. Chung, and Juan A. Siu. 1998. Takeovers, Restructuring, and Corporate Governance. 2nd ed. Upper Saddle River, NJ: Prentice Hall.

50 ?2000, Association for Investment Management and Research

This content downloaded from 185.44.77.40 on Sun, 15 Jun 2014 17:48:39 PMAll use subject to JSTOR Terms and Conditions