Embed Size (px)

Citation preview

The ShawCor Difference

STRONGFUNDAMENTALS

FUNDAMENTALSTRENGTHS

Investor Presentation

March 2014

2

The Global Leader in Pipe Coating and Related Products/ Services

Strategic Global Locations

Proprietary Technology

Track Record of Reliable Execution

Superior Financial Performance

ShawCor at a GlanceA global leader in energy services

3

The company

The market opportunity

The strengths

The future

Agenda

4

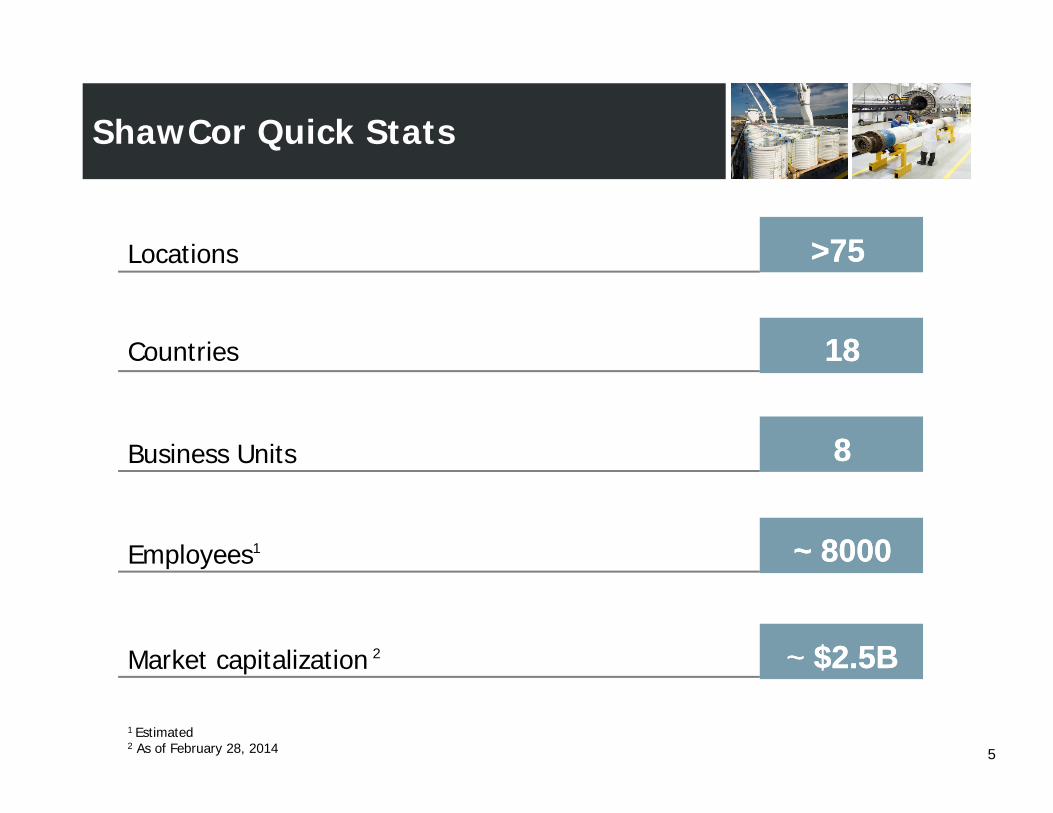

>75 >75 Locations

1818

Business Units 88

Employees1 ~ 8000~ 8000

ShawCor Quick Stats

Countries

Market capitalization 2 ~ $2.5B~ $2.5B

1 Estimated2 As of February 28, 2014 5

Bredero ShawCoatings- corrosion protection- insulation- weight / protective- internal flow efficiency

GuardianDrill pipe/tubularinspectionInventory management services

FlexpipeFlexible composite pipe for:- oil and natural gas

gathering lines- oilfield water and

fluids

PIPELINE & PIPE SERVICES

DSG-Canusa

Heat shrinktubing for sealing and protection

ShawFlex

Control, instrumentationcable

PETROCHEMICAL& INDUSTRIAL

Canusa-CPS

Weld inspection- radiographic- ultrasonic

Shaw Pipeline Services

Joint protectionPipe coating materials

Eight Business Units– All Ranked #1 or #2

SocothermCoatings- corrosion protection- weight / protective- thermal insulation

6

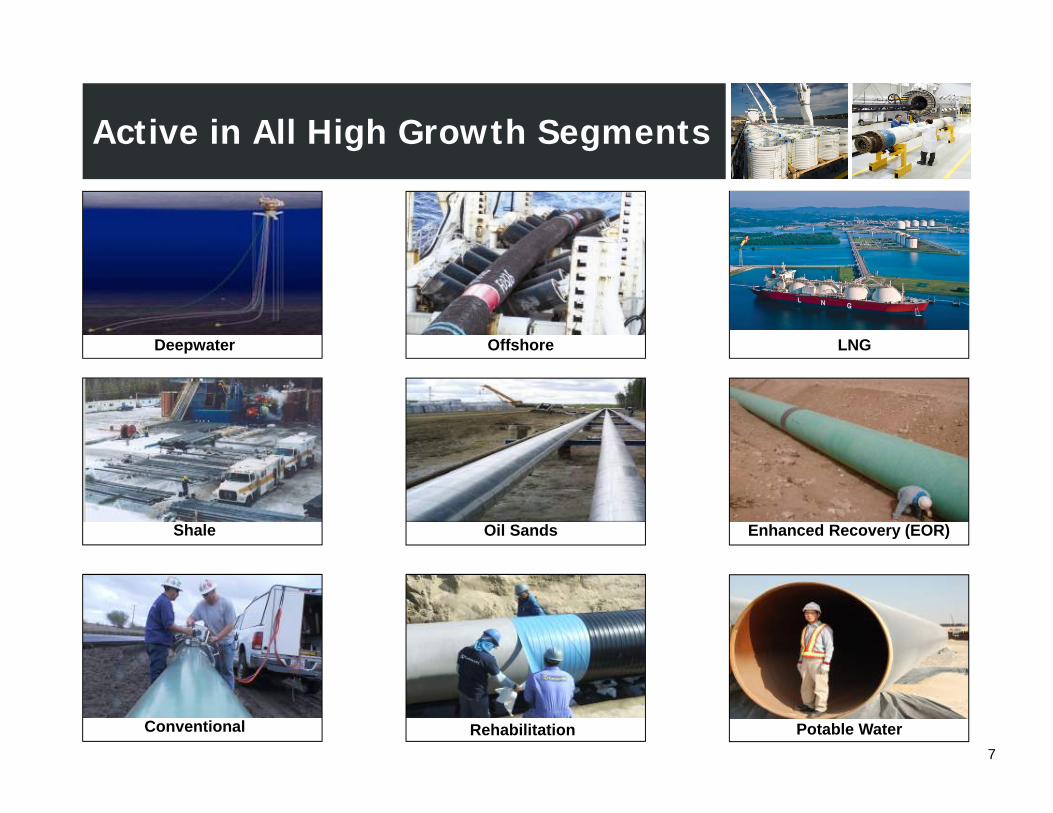

Active in All High Growth Segments

7Rehabilitation

Deepwater Offshore LNG

Shale

Conventional Potable Water

Enhanced Recovery (EOR)Oil Sands

Technology Sets Us Apart

270 Issued Patents – 57 technologies

164 Patents Pending – 51 technologies

86 Proprietary Formulations

20 Scientists at Corporate Laboratories

Subsea Test Facility

Mobile Plant Technology

8

The Need for New Technologies

HPPC

Next GenerationLand Coatings

New High Performance Powder Coating (HPPC) and SureBond coatings provide increased reliability

Shale PlaysSpoolable composite pipe offers corrosion resistance, faster installation and lower total installed cost FlexPipe Linepipe

Offshore Concrete Weight Coating provides seabed stability and pipeline protection

Thermotite® ULTRA™

DeepwaterProprietary passive insulation coating provides flow assurance for subsea pipelines and SURF (Subsea Umbilicals, Risers and Flowlines)

HeviCote®

9

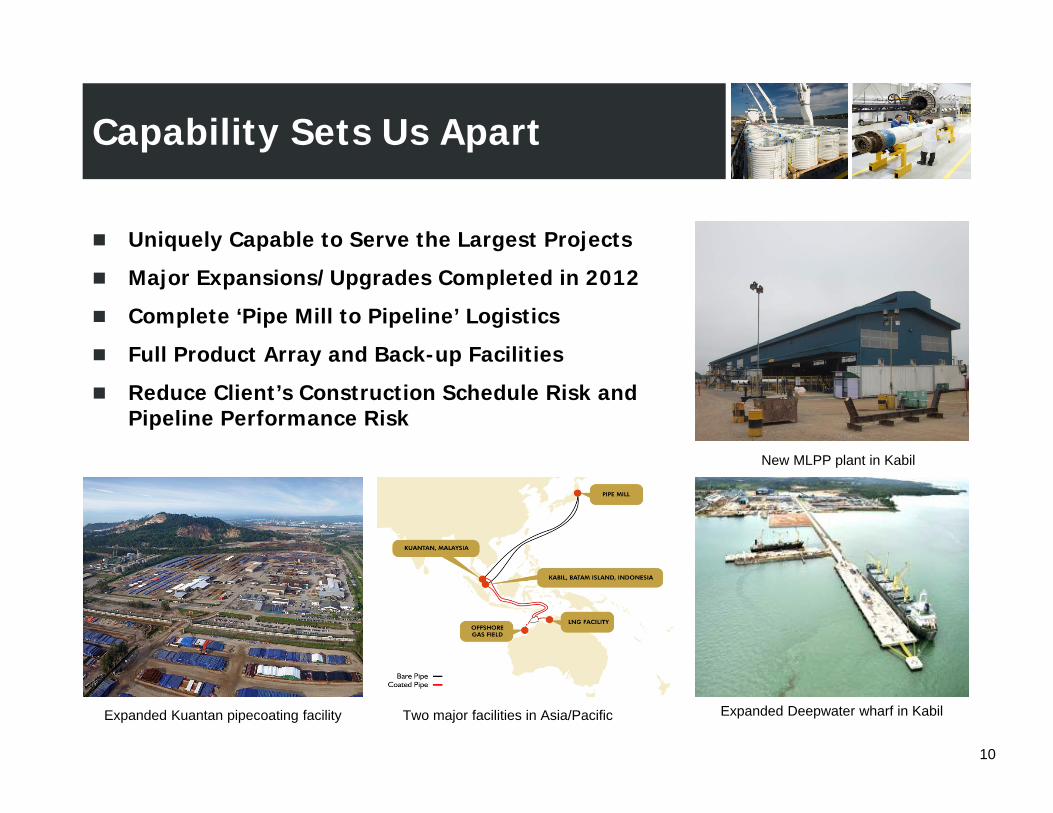

Capability Sets Us Apart

10

Uniquely Capable to Serve the Largest Projects

Major Expansions/Upgrades Completed in 2012

Complete ‘Pipe Mill to Pipeline’ Logistics

Full Product Array and Back-up Facilities

Reduce Client’s Construction Schedule Risk and Pipeline Performance Risk

New MLPP plant in Kabil

Expanded Deepwater wharf in KabilExpanded Kuantan pipecoating facility Two major facilities in Asia/Pacific

The company

The future

The market opportunity

The strengths

Agenda

11

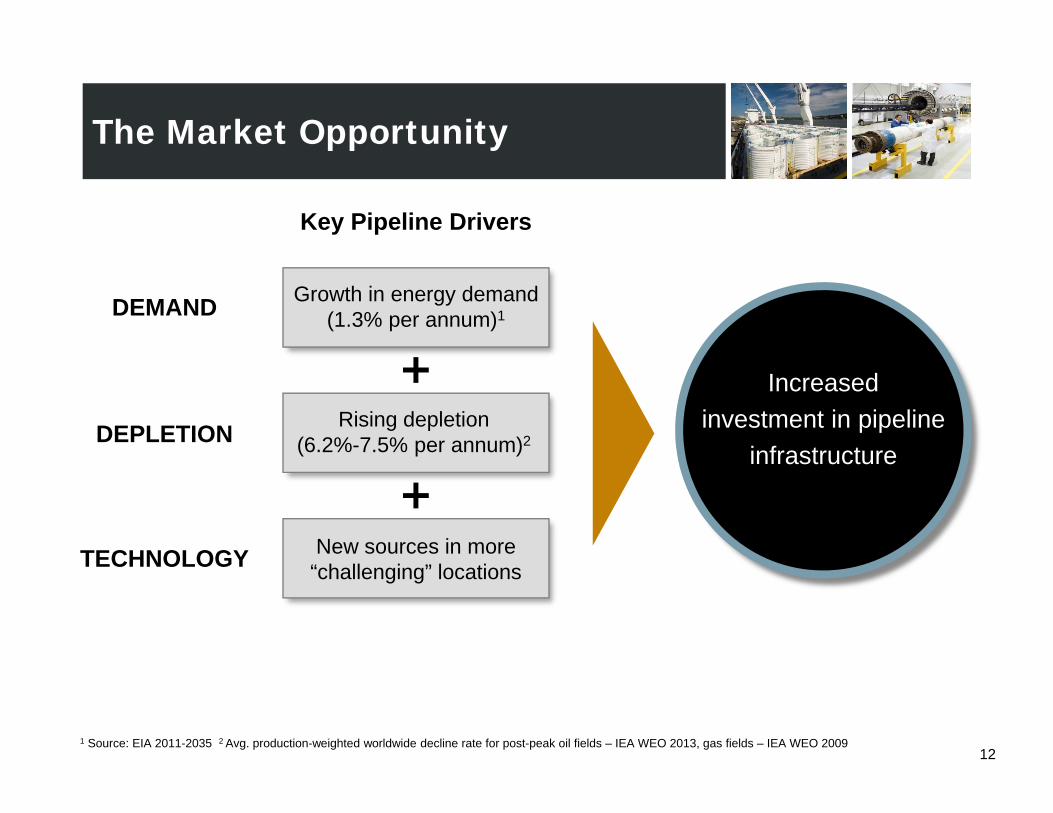

Growth in energy demand (1.3% per annum)1

Rising depletion (6.2%-7.5% per annum)2

New sources in more“challenging” locations

Increasedinvestment in pipeline

infrastructure

DEMAND

DEPLETION

TECHNOLOGY

1 Source: EIA 2011-2035 2 Avg. production-weighted worldwide decline rate for post-peak oil fields – IEA WEO 2013, gas fields – IEA WEO 2009

Key Pipeline Drivers

The Market Opportunity

12

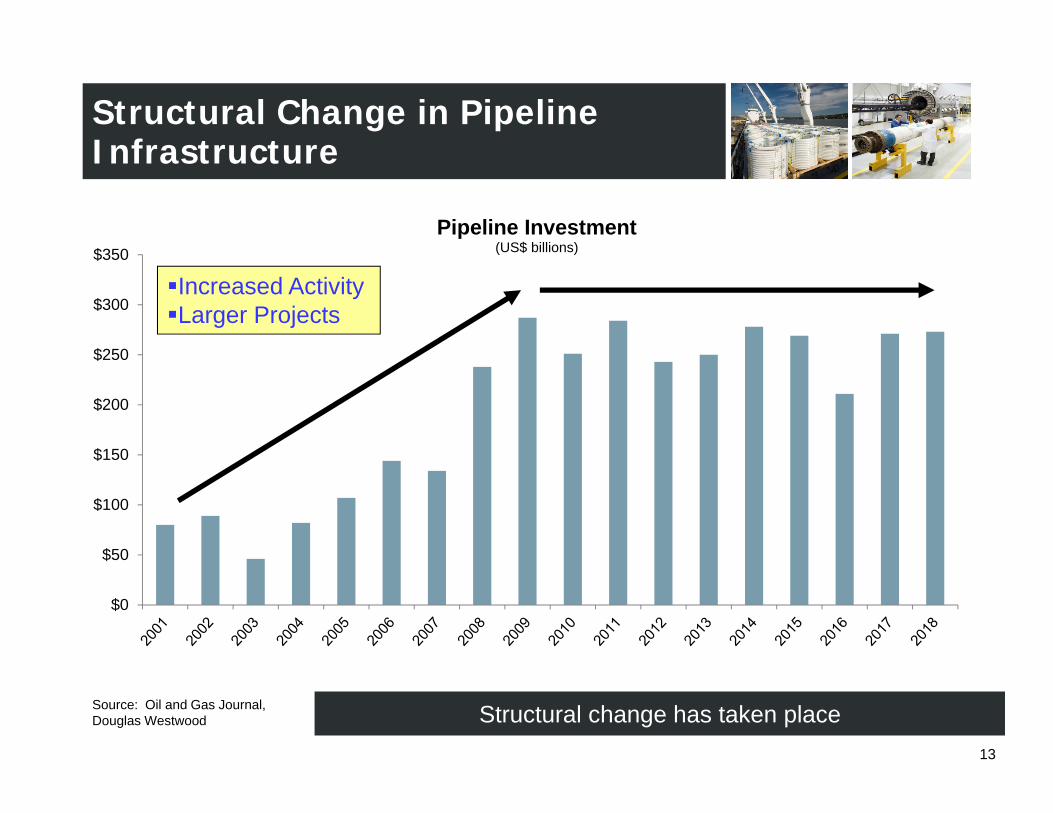

$0

$50

$100

$150

$200

$250

$300

$350Pipeline Investment

(US$ billions)

Source: Oil and Gas Journal,Douglas Westwood

Structural Change in Pipeline Infrastructure

Increased ActivityLarger Projects

Structural change has taken place13

The company

The market opportunity

The future

The strengths

Agenda

14

1. CLOSE W ITH CL I ENTSClient Relationships and Track Record

Strong relationships with all major global players

Americas EMAR Asia Pacific

* Partial list only15

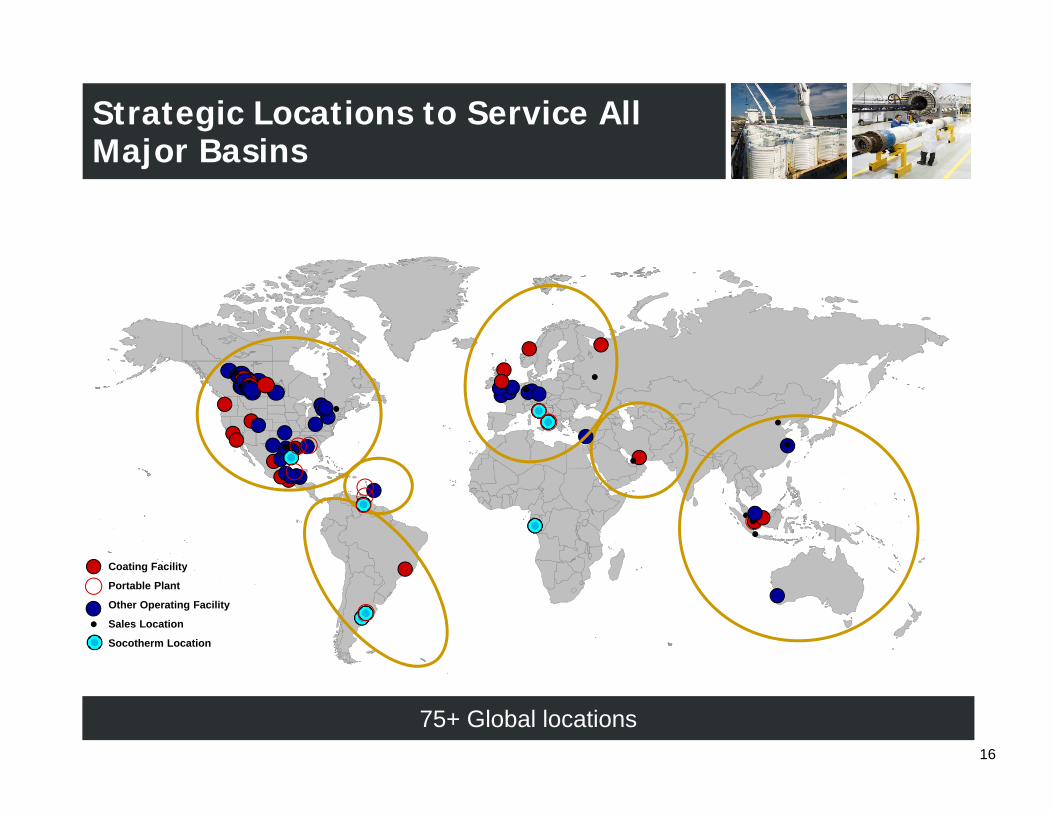

1. CLOSE W ITH CL I ENTSStrategic Locations to Service All Major Basins

Coating Facility

Portable Plant

Other Operating Facility

Sales Location

Socotherm Location

75+ Global locations16

Effective Acquisition Program

New Growth Platforms ‘Flexpipe’

Geographic Expansion ‘Brazil’

Expanded Services ‘ShawCor CSI’

Socotherm Acquisition

Brazil, October 2010 CSI, March 2011

Flexpipe, July 2008

Socotherm, Oct 2012

Socotherm LaBarge, April 201317

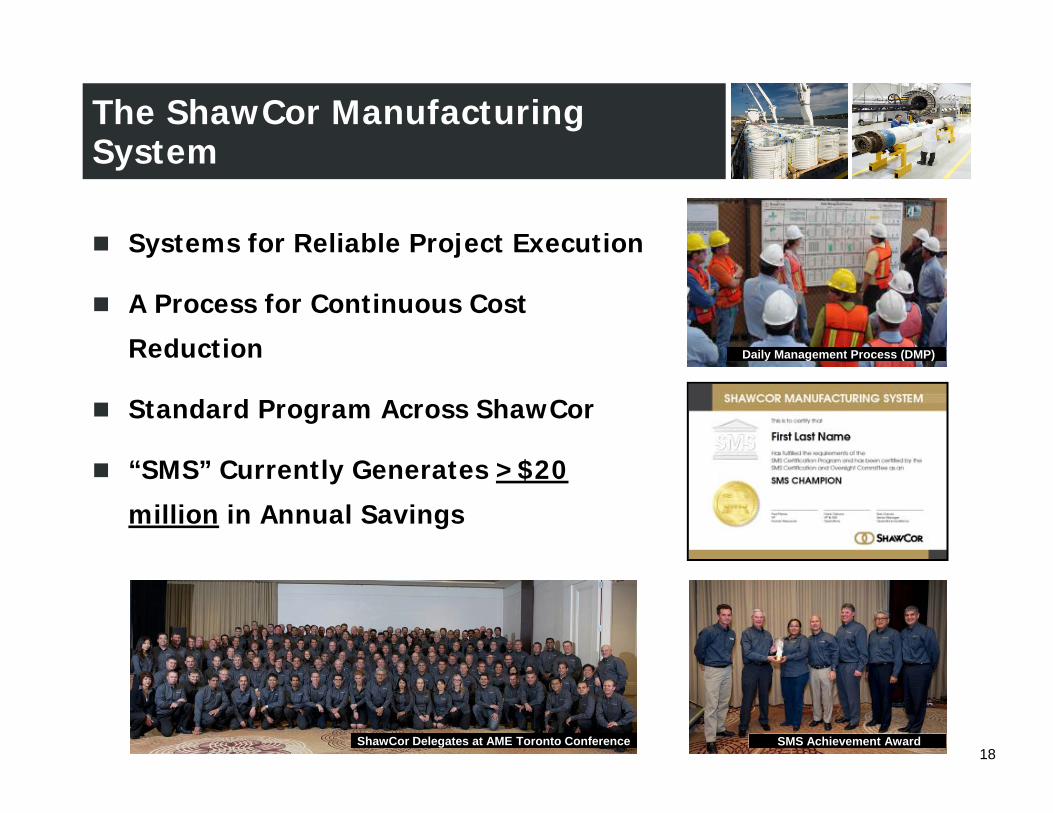

The ShawCor Manufacturing System

18

Systems for Reliable Project Execution

A Process for Continuous Cost

Reduction

Standard Program Across ShawCor

“SMS” Currently Generates >$20

million in Annual Savings

ShawCor Delegates at AME Toronto Conference SMS Achievement Award

Daily Management Process (DMP)

Cash flow > $1 Billion from operations (6 yr)

Term Debt $350 Million 10.4 years @ 3.65%

Cash Position + Available Credit Facilities to fund growth = $295 Million

Net Resources Competitive Advantage

Able to Simultaneously Execute:

The Largest ProjectsGeographic ExpansionNew TechnologiesNew Product ProgramsAcquisitions

4. F I NANC IAL STRE NGTH

Financial Strength

19

The company

The market opportunity

The strengths

The future

Agenda

20

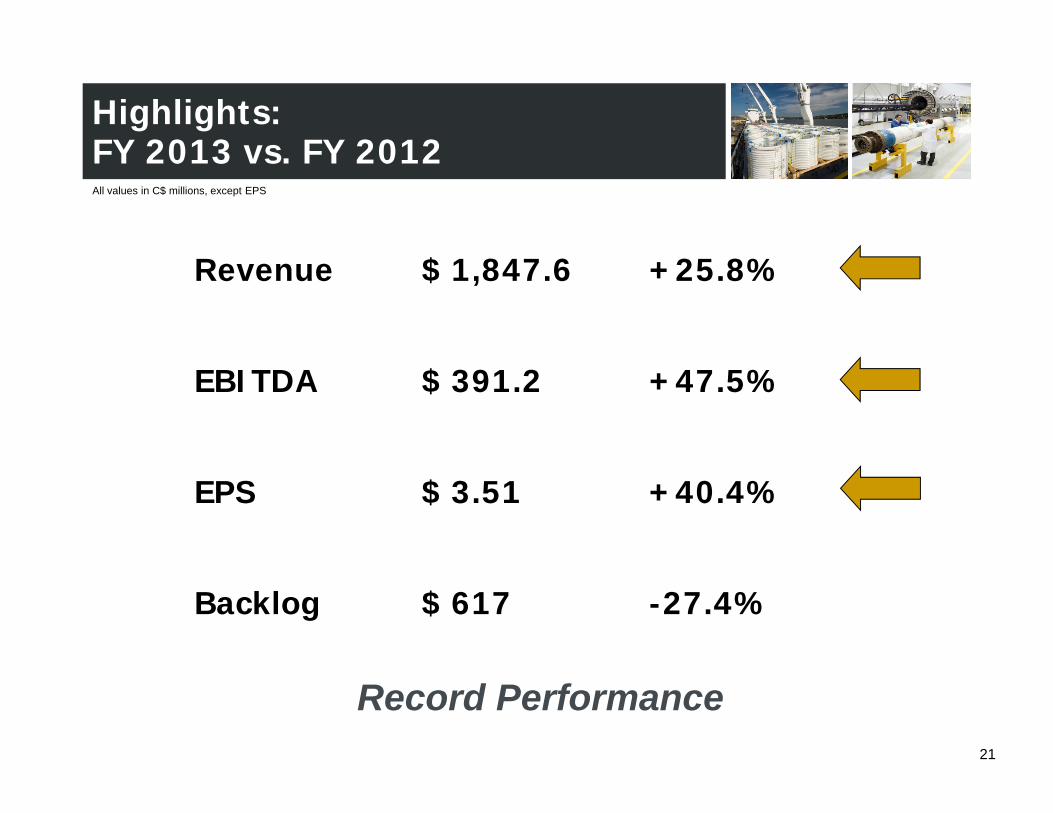

Highlights:FY 2013 vs. FY 2012

21

Revenue $ 1,847.6 +25.8%

EBITDA $ 391.2 +47.5%

EPS $ 3.51 +40.4%

Backlog $ 617 -27.4%

Record Performance

All values in C$ millions, except EPS

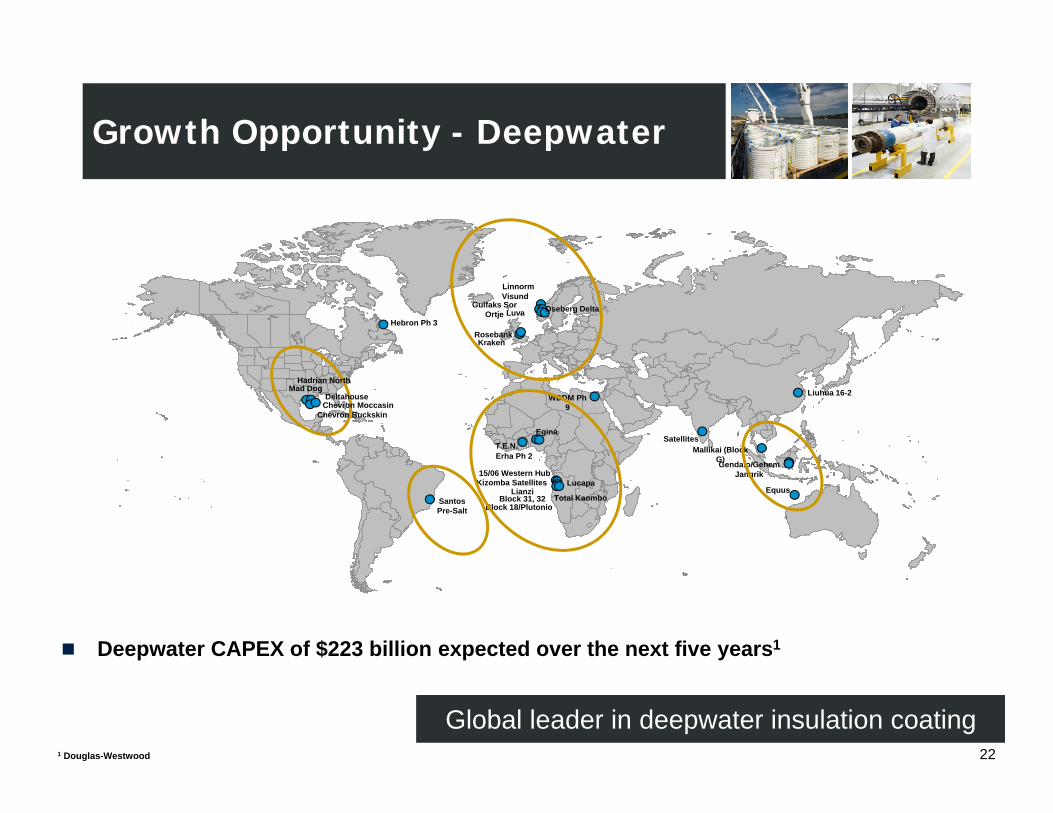

Growth Opportunity - Deepwater

Santos Pre-Salt

Gulfaks Sor Ortje

Visund

15/06 Western HubKizomba Satellites

Lianzi

WDDM Ph 9

Erha Ph 2

Mad Dog

Hebron Ph 3

Egina

Block 31, 32

Linnorm

Mallikai (Block G)

Block 18/Plutonio

Lucapa

Gendalo/Gehem

Rosebank

Luva Oseberg Delta

Liuhua 16-2

Equus

Kraken

Jangrik

T.E.N.Satellites

Hadrian North

Deepwater CAPEX of $223 billion expected over the next five years1

1 Douglas-Westwood

Global leader in deepwater insulation coating22

DeltahouseChevron Moccasin

Chevron Buckskin

Total Kaombo

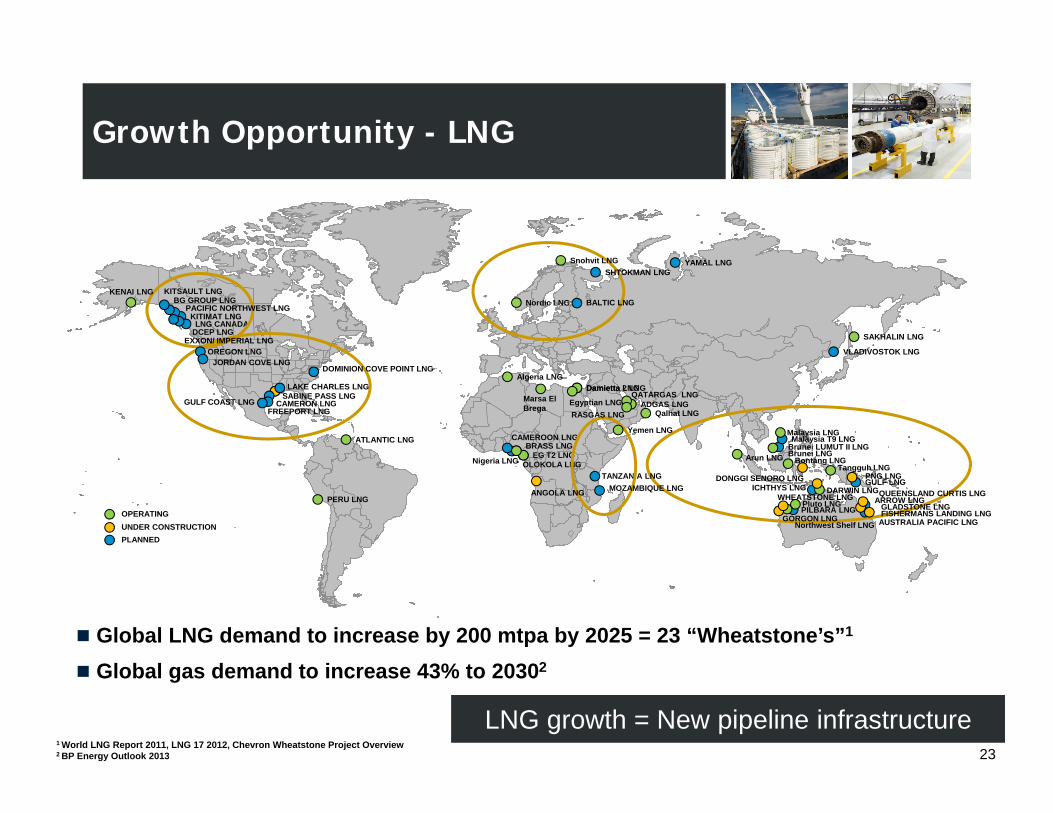

Growth Opportunity - LNG

SABINE PASS LNG

ARROW LNG

BRASS LNG

KITIMAT LNG

OLOKOLA LNG

YAMAL LNG

FISHERMANS LANDING LNG

GULF LNGDARWIN LNG

PILBARA LNG

Brunei LUMUT II LNGMalaysia T9 LNG

EG T2 LNG

CAMEROON LNG

Damietta 2 LNG

TANZANIA LNG

LNG CANADA

MOZAMBIQUE LNG

PACIFIC NORTHWEST LNGBG GROUP LNG

KITSAULT LNG

VLADIVOSTOK LNG

SHTOKMAN LNG

ADGAS LNG

Algeria LNG

Arun LNG Bontang LNG

ATLANTIC LNGBrunei LNG

Damietta LNG

Egyptian LNGQATARGAS LNG

KENAI LNG

Marsa El Brega

Malaysia LNG

Nigeria LNG

Nordic LNG

Northwest Shelf LNG

Qalhat LNG

Pluto LNGPERU LNG

RASGAS LNG

SAKHALIN LNG

Snohvit LNG

Tangguh LNG

Yemen LNG

ANGOLA LNG

AUSTRALIA PACIFIC LNG

DONGGI SENORO LNG

GLADSTONE LNGGORGON LNG

ICHTHYS LNGPNG LNG

QUEENSLAND CURTIS LNGWHEATSTONE LNG

CAMERON LNGFREEPORT LNG

LAKE CHARLES LNG

DCEP LNG

DOMINION COVE POINT LNG

GULF COAST LNG

OREGON LNG

OPERATINGUNDER CONSTRUCTIONPLANNED

Global LNG demand to increase by 200 mtpa by 2025 = 23 “Wheatstone’s”1

Global gas demand to increase 43% to 20302

1 World LNG Report 2011, LNG 17 2012, Chevron Wheatstone Project Overview2 BP Energy Outlook 2013

LNG growth = New pipeline infrastructure23

JORDAN COVE LNG

EXXON/ IMPERIAL LNG

BALTIC LNG

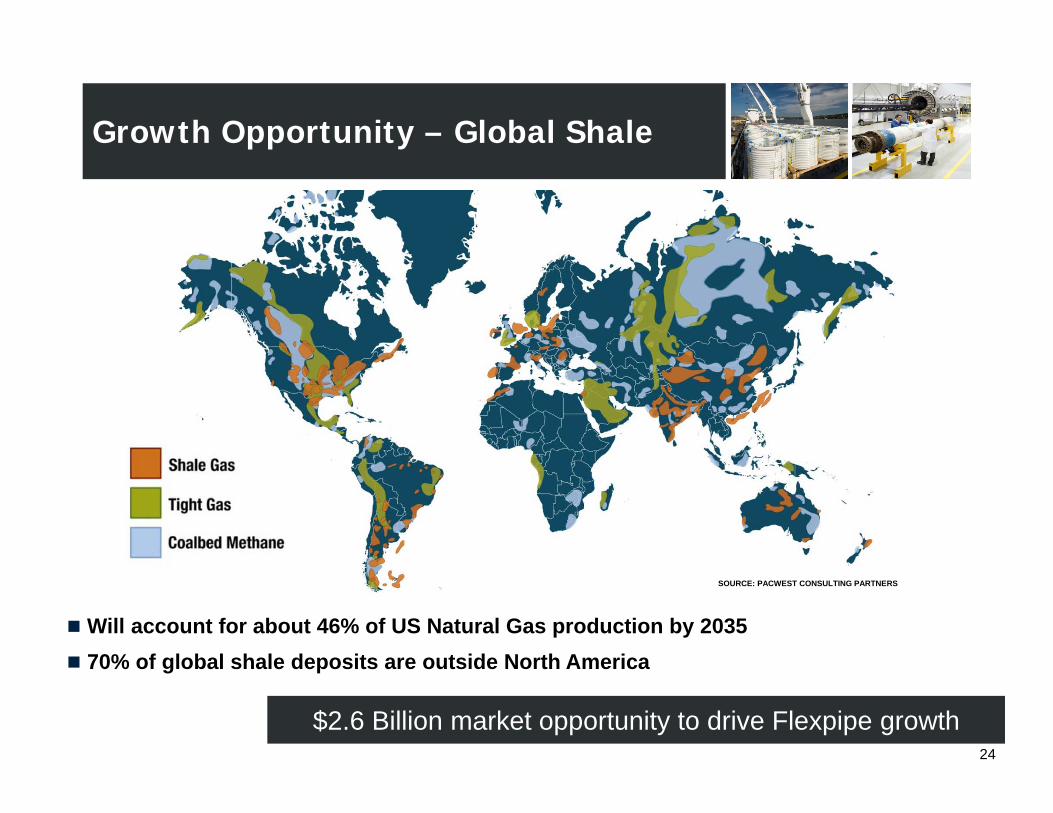

Growth Opportunity – Global Shale

SOURCE: PACWEST CONSULTING PARTNERS

Will account for about 46% of US Natural Gas production by 203570% of global shale deposits are outside North America

$2.6 Billion market opportunity to drive Flexpipe growth24

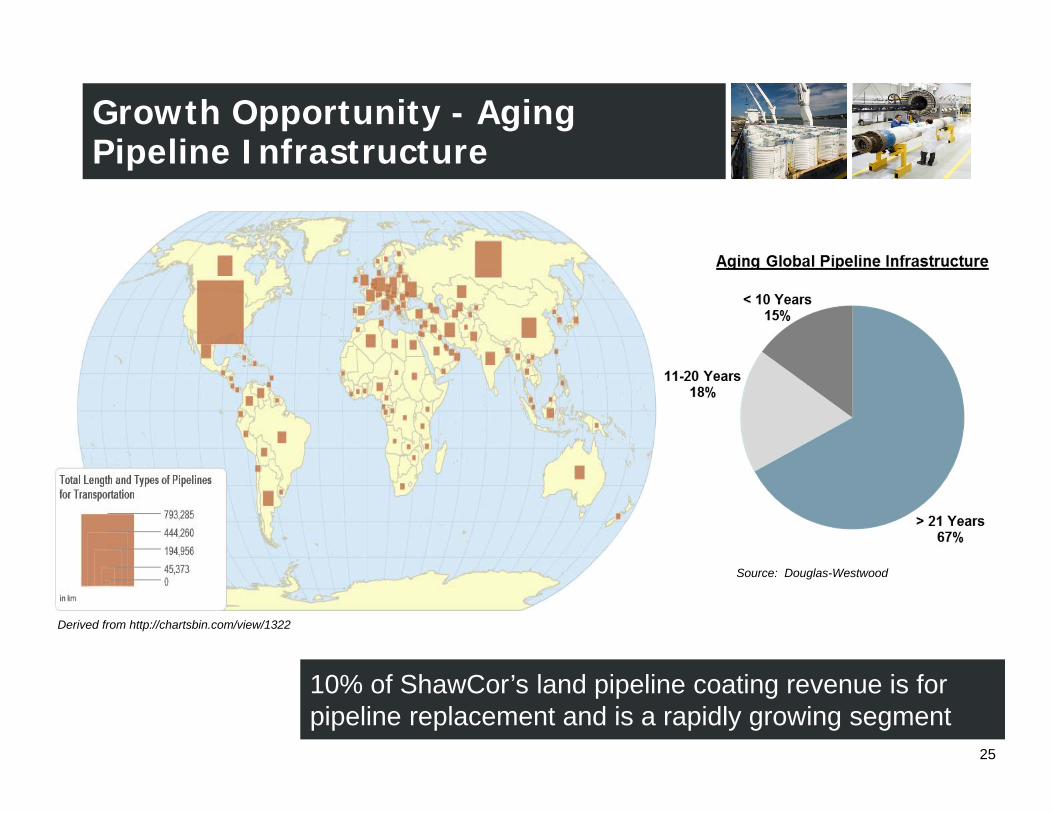

Growth Opportunity - Aging Pipeline Infrastructure

10% of ShawCor’s land pipeline coating revenue is for pipeline replacement and is a rapidly growing segment

25

Derived from http://chartsbin.com/view/1322

Source: Douglas-Westwood

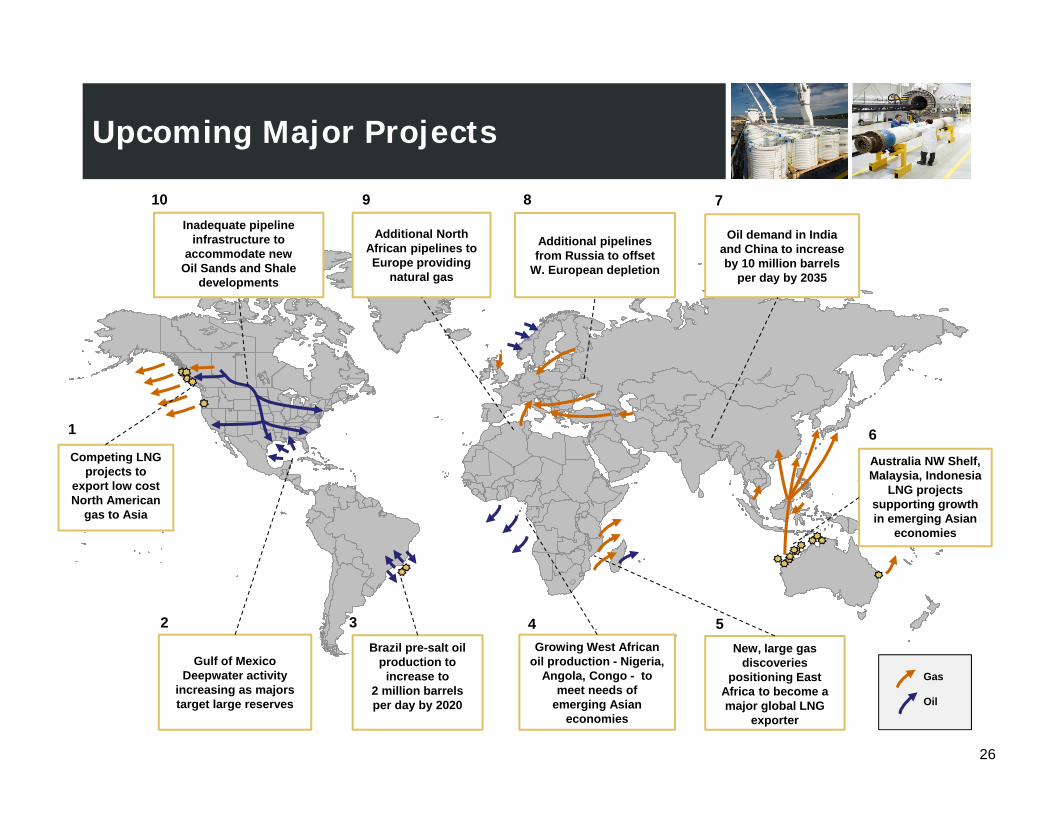

Upcoming Major Projects

26

Competing LNG projects to

export low cost North American

gas to Asia

Brazil pre-salt oil production to

increase to 2 million barrels per day by 2020

Growing West African oil production - Nigeria,

Angola, Congo - to meet needs of

emerging Asian economies

New, large gas discoveries

positioning East Africa to become a major global LNG

exporter

Australia NW Shelf, Malaysia, Indonesia

LNG projects supporting growth in emerging Asian

economies

Additional pipelines from Russia to offset

W. European depletion

Gulf of Mexico Deepwater activity

increasing as majors target large reserves

Inadequate pipeline infrastructure to

accommodate new Oil Sands and Shale

developments

Additional North African pipelines to Europe providing

natural gas

Oil demand in India and China to increase by 10 million barrels

per day by 2035

Gas

Oil

1

2 3 4 5

6

78910

Underway

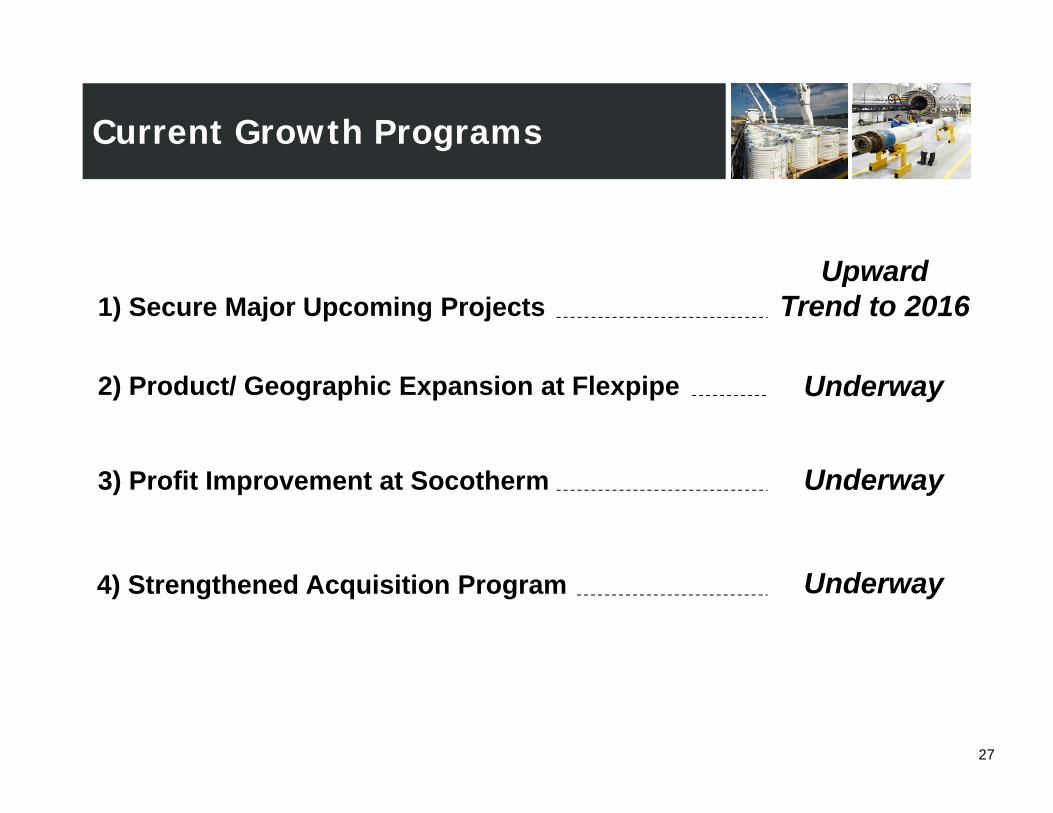

UpwardTrend to 20161) Secure Major Upcoming Projects

2) Product/ Geographic Expansion at Flexpipe

4) Strengthened Acquisition Program

Current Growth Programs

3) Profit Improvement at Socotherm

27

Underway

Underway

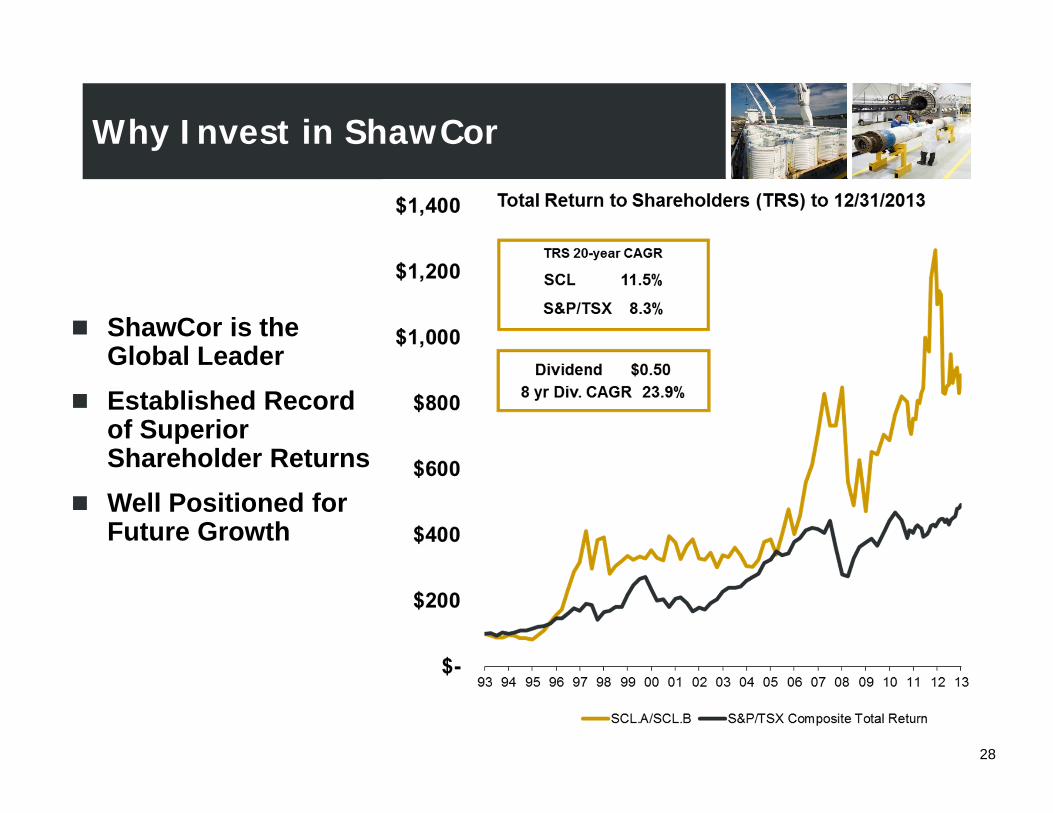

Why Invest in ShawCor

ShawCor is the Global LeaderEstablished Record of Superior Shareholder ReturnsWell Positioned for Future Growth

28

The ShawCor Difference

STRONGFUNDAMENTALS

FUNDAMENTALSTRENGTHS

Investor Presentation

March 2014