Embed Size (px)

Citation preview

Page 1 of 9

The Property Registry Land Titles Accounts: Information for Lawyers New to Filing Documents with The Property Registry (i.e. New Firms or New Practice Area) The Law Society Perspective Version 1N1 April 20, 2016 Paper prepared by: Appendices courtesy of: Kathy Levacque, CPA, CA The Property Registry Director of Audit Law Society of Manitoba Introduction The initiative of The Property Registry (“TPR”) regarding the Land Titles deposit accounts has had a significant impact on the daily accounting processes of many law firms that file documents with TPR, and the Law Society of Manitoba has a number of related requirements. The purpose of this document is to relate TPR filings and documents – in particular as it relates to the Client File Report – to Law Society requirements. New Process: Summary As explained by TPR in their October 28, 2014 announcement, the following was required when the accounting system AAMS was adopted in March, 2015: ! All law firms doing business with TPR must have a Land Titles deposit account; ! All financial transactions between TPR and law firms will flow through the Land

Titles deposit account. That is: o All funds provided for registration services at Land Titles will be deposited

to this account; o All rejections or overpayments will be refunded to this account; o Any shortfalls will be debited (charged) to this account;

! In addition to the monthly account statement, a Client File Report will be produced upon acceptance or rejection of a registration, tracing all transactions with the same client file number;

! Refunds from the deposit account will be available upon written request, with a minimum refund requirement of $100; and

! There is no requirement for a minimum balance to be maintained in the deposit account.

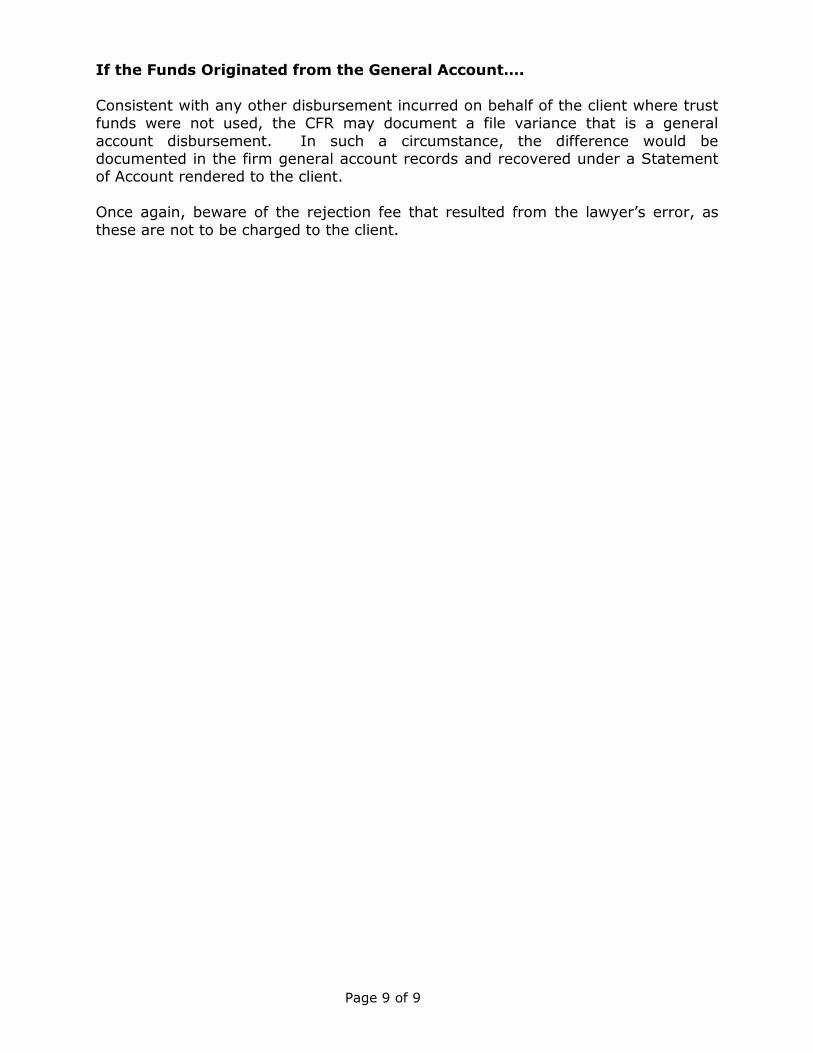

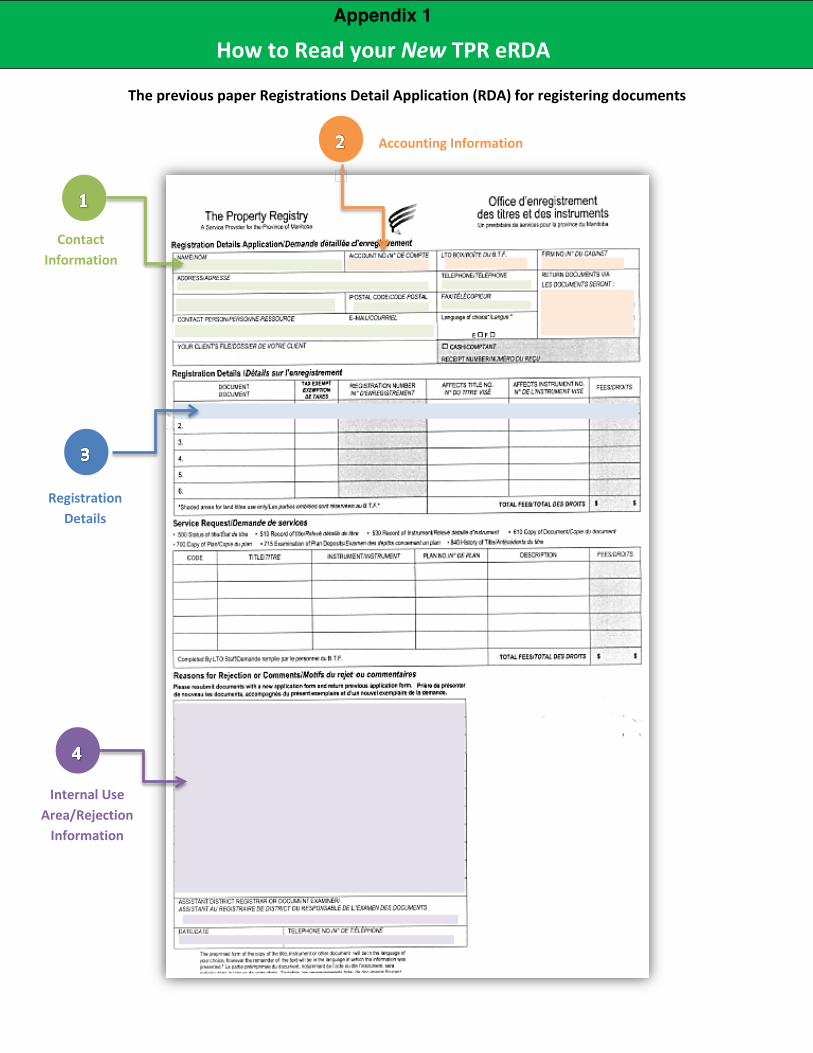

On December 7, 2015, TPR released a new electronically fillable PDF Registration Details Application (RDA) form.

1 Versions – Different versions of this document are available. ‘E’ versions are designed for firms that existed prior to the March, 2015 system conversion at The Property Registry. The ‘N’ version is designed for firms that opened subsequent to March, 2015 or are new to filing with The Property Registry. This is the first version published in the ‘N’ series.

Page 2 of 9

To facilitate understanding of the eRDA, as well as the eReceipt and Client File Report, please refer to How to Read your New TPR eRDA, How to Read your New TPR eReceipt, and How to Read your Client File Report, included as Appendix 1. TPR Land Titles Deposit Account: How does it fit with Law Society Rules for handling trust money? Many law firms had historically been hesitant to use the Land Titles deposit account with funds originating from the firm trust account, concerned that the trust funds would be comingled at TPR with other clients’ money or with funds that originated from the firm’s general account and therefore a violation of Law Society Rules. What is important to remember, though, is that the firm’s Land Titles deposit account is not the same as a firm trust or general bank account. TPR is a third party service provider, and when a firm pays TPR for a service (e.g. registration of a document), those funds paid to TPR become the property of TPR. This is not unlike any other commodity or third party service for which a law firm disburses funds, such as a sales commission to a real estate agent or final balance on a Manitoba Hydro loan. What makes TPR rather unique is that the exact amount due is sometimes adjusted after the fact. It is also unique in the possibility that documents can be rejected. Clearly the law firm will have to reconcile the TPR ‘activity’ in the Land Titles deposit account on any given file back to the firm accounting records, keeping the original identity of the funds provided (trust v. general) in focus. The “Client File Report” (“CFR”), provides timely information back to firms for use on a per client matter basis. This allows firms to make any necessary adjustments for the end result of the transaction (refunding or charging differences). So, can a law firm use a Land Titles deposit account with funds originating both from the law firm’s trust and general accounts and not be in violation of Law Society Rules? Yes, but you must follow the Law Society requirements for how the account is used. These requirements are outlined later in this paper. TPR Land Titles Deposit Account: Funds kept in the account and funds passing through the account Some of the examples of the CFR included as appendices to this paper assume the law firm periodically provides funds from the general account to TPR specifically to maintain a balance of funds in the deposit account at any given time. Many firms currently find it convenient to maintain a ‘float’ of some amount in the account. However, keep in mind that the Law Society is not requiring firms to maintain such a balance in the Land Titles deposit account and it is perfectly acceptable for a firm to have a ‘no balance’ policy. Nevertheless, even with such a policy, it is mandatory that the law firm use and manage its Land Titles deposit account, as:

Page 3 of 9

! all documents filed at Land Titles have related funds passing through the Land Titles deposit account; and

! refunds for rejections or overpayments are automatically deposited to the Land Titles deposit account.

TPR Land Titles Deposit Account: Law Society requirements for use of the account For all law firms submitting documents to the Land Titles Office, the Law Society has the following requirements:

! File number: You must provide a unique client file number for the matter. The numbering system must be reflected in your accounting records and on the file folders themselves;

! Client File Report: The Client File Report is to be used by firms to ensure all

client trust funds used in Land Titles transactions and all payments from the general account which are to be billed to the client are accounted for accurately;

! Reconciliation of Client File Report to Firm Accounting Records: When

the Land Titles transaction is complete – Accepted, Rejected or Discharged – the law firm must compare its accounting records for the matter with the Client File Report. Variances must be identified and resolved expeditiously. Refer to the below section “Process at Law Firms” for further details on how this requirement is to be met;

! Filing of CFR: When review of the CFR is concluded and all necessary action

items are identified and executed, a copy of the CFR is to be placed in the law firm’s client file for the matter.

Process at Law Firms Note that the example Client File Reports used as appendices 2, 3A & 3B to this paper were at the development stage and look slightly different now that they have been put into production. You should also note that Appendices 2 and 3B are extracted from a power point presentation and had been streamlined to accommodate the screen. Appendix 3A more closely reflects the format of what a firm will receive. A) Coordinate all Firm Lawyers If your firm has more than one lawyer submitting documents to TPR, you should consider a firm policy on how you manage your Land Titles deposit account to ensure your use of the account is consistent and coordinated.

Page 4 of 9

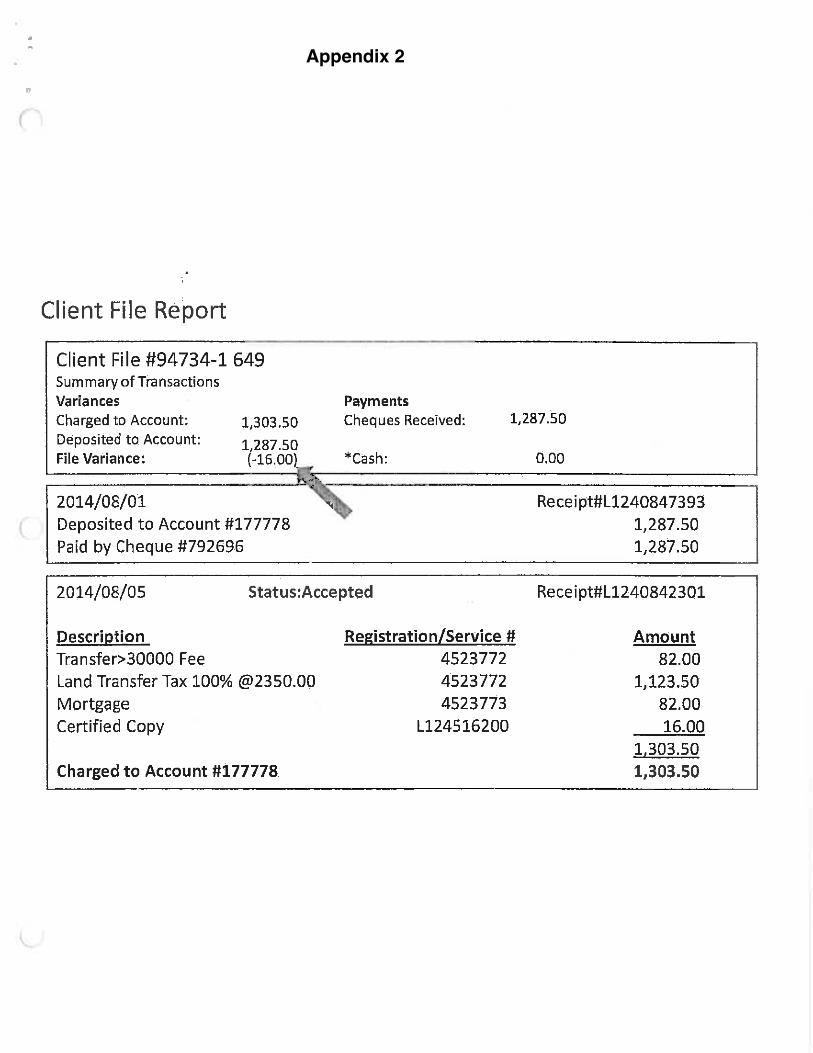

B) Example Client File Report: Scenario 1 (Appendix 2) Scenario 1: The example CFR in Appendix 2 reflects the following scenario:

! Your law firm is representing the purchaser in a real estate transaction that is closing August 1;

! Your client file number for the matter is 94734-1 649; ! You submit your PRA/RDA form with trust cheque #792696 for $1,287.50 to

pay for the transfer, mortgage, and certified copy; ! Your firm is maintaining a balance in the Land Titles deposit account; ! Your trust cheque accidentally was for not enough funds – you didn’t include

the $16 for the certified copy. Your documents are accepted, though, and you receive your certified copy since you had funds on hand in your Land Titles deposit account to pay for the copy.

CFR Review Steps: When the law firm receives the above CFR for matter 94734-1 649, it triggers the following processes in the law firm:

! Check the status shown on the CFR: Accepted, Rejected, or Discharged? ! As the status is accepted:

o Have the client trust ledger for matter 94734-1 649 handy: ! On the CFR, review the payment information in both the

“Summary of Transactions” box and the first section below the box;

! Compare the ledger and the CFR to see if they both reflect the same payment information;

! Check the CFR summary box for any variance; ! In this scenario, more funds were needed to conclude the

services on this matter than were provided by the initial trust cheque – the variance on the CFR is $16;

! Seeing the reason for the variance in the lower section of the CFR, the law firm would record a general account disbursement of $16 for the certified copy for matter 94734-1 649. As with any other general account disbursements, the $16 would be recovered under a Statement of Account rendered to the client;

! When review of the CFR is concluded and all necessary action items and identified and executed, the Law Society requires a copy of it to be placed in the law firm’s client file for matter 94734-1 649.

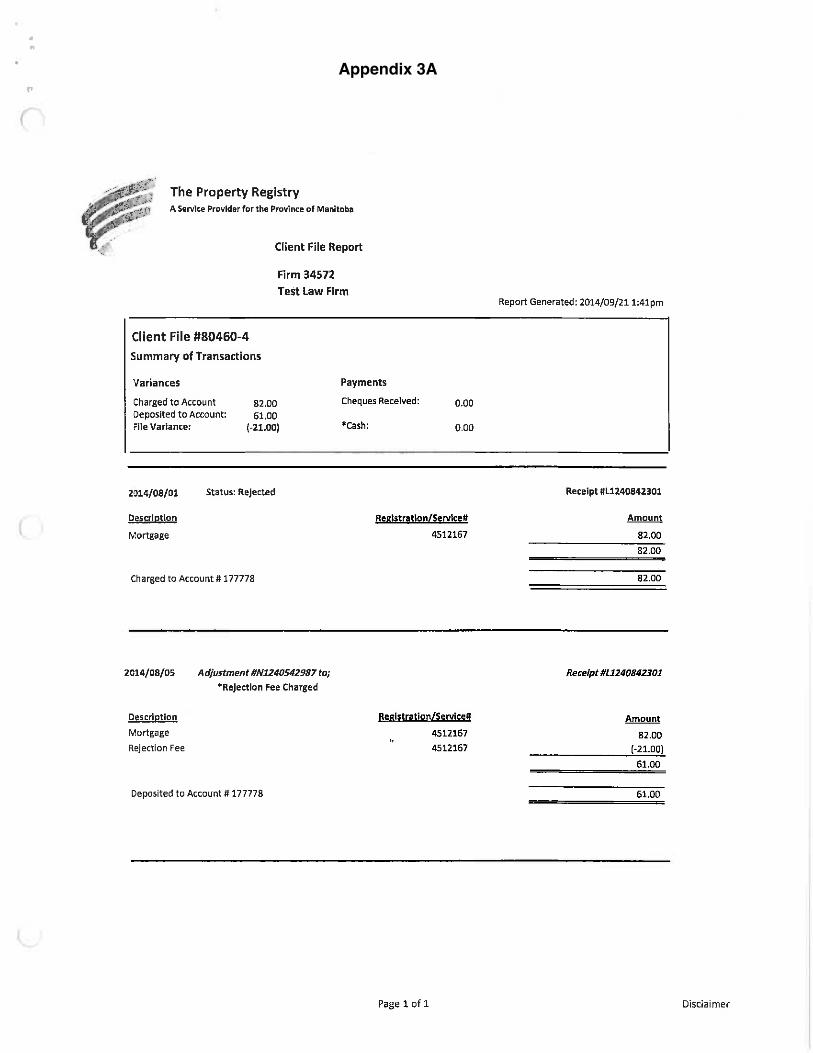

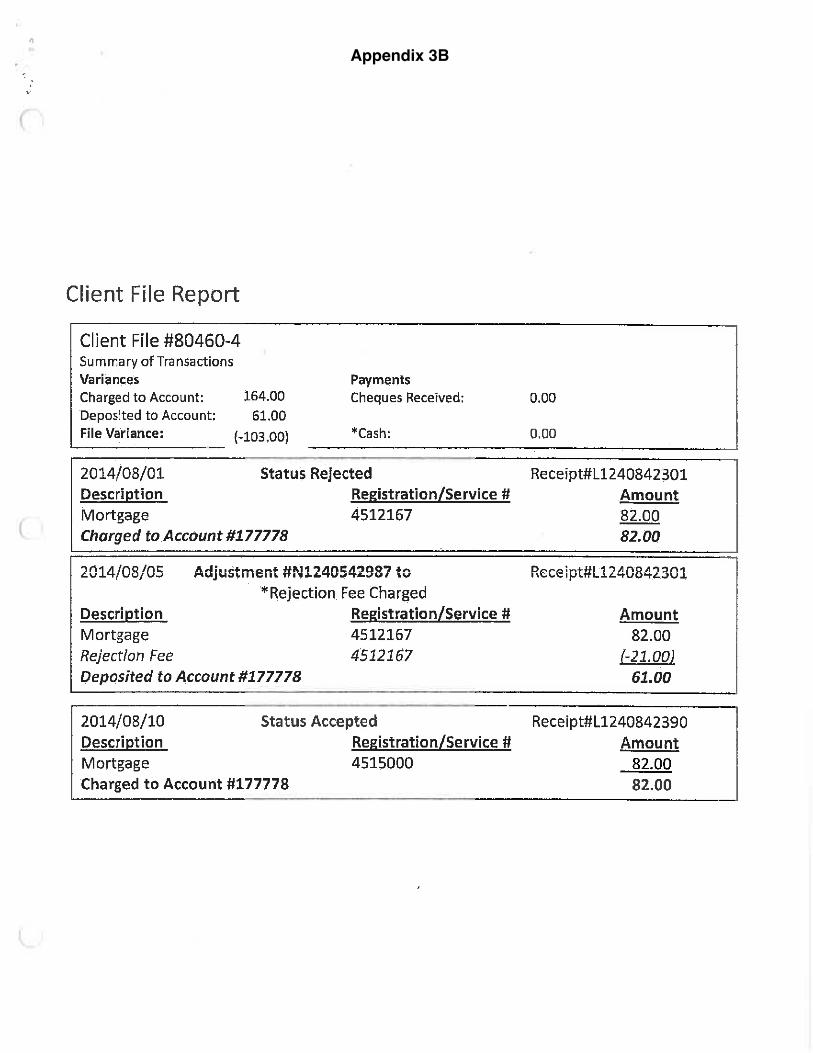

C) Example Client File Report: Scenario 2 (Appendices 3A and 3B) Scenario 2 has two parts. Since the initial mortgage registration is rejected, the Client File Report from Appendix 3A is provided to the law firm on or around August 5. After the necessary corrections are made and the document is re-filed, the mortgage gets accepted, with the CFR in Appendix 3B provided on or around August 10.

Page 5 of 9

Scenario 2 Part A - Rejection: The example CFR in Appendix 3A reflects the following scenario:

! Your law firm is representing a mortgage lender; ! Your client file number for the matter is 80460-4; ! You submit your PRA/RDA form without a cheque, requesting a mortgage to

be registered; ! Your firm is maintaining a balance in the Land Titles deposit account; ! Your request is rejected. Under the old process - if you did not use a deposit

account and had submitted a cheque with your request - the rejection fee of $21 would have been deducted from the $82 the firm had submitted with the request, and a refund cheque of $61 would have been issued to the firm. Under the new process, the $61 gets re-deposited to the Land Titles deposit account.

CFR Review Steps: When the law firm receives the CFR for matter 80460-4 (Appendix 3A), it triggers the following processes in the law firm:

! Check the status shown on the CFR: Accepted, Rejected, or Discharged? ! As the status is rejected, you will need to identify whatever reason the

document was rejected and determine whether and how quickly the document will be re-submitted to TPR.

! Have the client trust ledger for matter 80460-4 handy: ! Review the payment information in both the “Summary of

Transactions” box and the first section below the box; ! Compare the ledger and the CFR to see if they both reflect the

same payment information. While this step may seem unnecessary since the CFR shows funds from the deposit account were used for the transaction, it is possible that the firm had prepared a cheque to accompany the request and for whatever reason, it is not showing on the CFR. Any inconsistencies at this stage need to be investigated and resolved;

! Check the summary box for any variance; ! In this scenario, you see a $21 variance in the box, and see

later in the CFR that your Land Titles deposit account has been charged a $21 rejection fee;

! If the rejection was the result of the lawyer’s error, this fee is not to be passed on to the client.

! When review of the CFR is concluded and all necessary action items are identified and executed, the Law Society requires a copy of the CFR to be placed in the law firm’s file for matter 80460-4.

Scenario 2 Part B - Accepted: The example CFR in Appendix 3B reflects the following continuation of scenario 2:

! You make the necessary corrections and re-submit the documents; and ! On August 10, your registration is accepted.

A key difference between scenarios 1 and 2 is that the mortgage is initially rejected in scenario 2. This difference will impact the Client File Report. You will now be receiving more than one CFR – one on or around August 5 (“Time 1”), and one on

Page 6 of 9

or around August 10 (“Time 2”). Comparing the CFRs at the two different times, note the CFR at Time 1 will include the first three boxes, and then at Time 2 the report will include four boxes – the extra box showing what happened August 10. You should also note the difference in the summary box at the top – although this box is included on both reports, the variance information in the Summary of Transactions changed. A special word about the Time 2 variances: To interpret the variances on the CFR at Time 2, you need to remember that the mortgage has already been rejected once. From TPR’s perspective, the deposit account has had the following occur:

Charge for registration/service # 4512167 August 1 $ 82 Charge for registration/service # 4515000 August 10 $ 82

Total Charges to Account $164 For deposits to the account, after the mortgage was rejected on August 5, $61 was returned to the deposit account, representing the charge from August 1 of $82, less the rejection fee of $21. The file variance at Time 2 is therefore is composed of the following two components: Rejection fee August 5 $ 21

Charge for registration/service #4515000 August 10 $ 82 File Variance $103

CFR Review Steps at Time 2: When the law firm receives the CFR for matter 80460-4 on or about August 10, it triggers the following processes in the law firm:

! Check the status shown on the CFR: Accepted, Rejected, or Discharged? ! As the status is now accepted:

o Have the client trust ledger for matter 80460-4 and the CFR from Time 1 handy:

! Compare the CFR from Time 1 to Time 2. While this step may seem unnecessary, should there be any keying or posting errors at the firm or TPR (especially in the client file # field), these two reports may not be the same for the top three boxes of information. Further, as explained above, box 1 will be changed to reflect the additional information from box 4. Any inconsistencies at this stage need to be investigated and resolved;

! Review the payment information in both the “Summary of Transactions” box and the lower boxes;

! Compare the ledger and the CFR to see if they both reflect the same payment information. Any inconsistencies at this stage need to be investigated and resolved;

! Check the summary box for any variance; ! At Time 2 in this scenario, you see a $103 variance in the box,

and see later in the CFR that your Land Titles deposit account has been charged a $21 rejection fee and $82 for the accepted mortgage on August 10 (in the last box);

Page 7 of 9

! Again, if the rejection was the result of the lawyer’s error, this fee is not to be passed on to the client;

! Since the law firm did not provide a trust or general account cheque for the registration, the $82 mortgage registration fee as at August 10 now needs to be recorded in the firm general account records as a disbursement recovered under a later Statement of Account rendered to the client.

At the end of the process, you will now have two copies of the CFR – one each for Time 1 and Time 2. Do you need to keep both copies in the client file now? Yes. Like any time sensitive source document, they reflect information at different points in time and should both be on the client file. D) What About Overpayments or Refunds? If the Funds Originated from the Trust Account…. When the Land Titles transaction is complete (Accepted, Rejected or Discharged), any refund or overpayment of trust funds must be returned to the trust account expeditiously. This requirement may be met by applying the following processes:

(i) Rejection: Re-filing Immediately Imminent

When the lawyer becomes aware of rejection, the reasons for the rejection must be addressed immediately. The lawyer must make an assessment of whether the steps required to correct the documents are within the lawyer’s control and will be accomplished within 10 business days. If so, it is permissible to leave the refunded payment (less the rejection fee) in the deposit account pending re-submission of the documents. If not, the funds will need to be replaced into the pooled trust account using one of the methods noted in this paper. However, keep in mind that if at any later point in time it becomes apparent that the documents will not be re-submitted for registration within the 10 day period, you will need to immediately replace the funds to the pooled trust account using one of the methods noted in this paper.

(ii) Rejection: Re-filing NOT Immediately Imminent

If the corrections needed in order to re-file documents are not going to be completed within the timeline discussed above, any funds which originated from the trust account must be re-deposited to the trust account. This can be accomplished in one of two ways:

(a) A cheque can be written from the firm general account and deposited to

the trust account for the amount of funds to be returned to trust.

Page 8 of 9

Remember that if the rejection was the result of the lawyer’s error, the rejection fee charged is not to be passed on to the client. Therefore, the amount of the cheque from the general account to be deposited to trust in most cases will be the full amount of the original trust cheque written when the documents were initially filed.

(b) If TPR’s dollar amount threshold of $100 or more is met, a refund may

be requested. The request must be filed within the same or next day of receipt of the CFR. The refund cheque later received would be deposited directly to the trust account.

HOWEVER, if a refund request is planned but the firm cannot send in the request to TPR by no later than the day after the CFR is received by the firm, then method (a) above must be followed. If a refund is later requested and the funds have already been returned to the trust account, the refund can be deposited directly to the general account.

(iii) Accepted/Discharged: Negative File Variance (“Underpaid”)

As discussed at B) above regarding Scenario 1, if the trust funds submitted to conclude the transaction were insufficient (and the difference is not a rejection fee), then the firm may record a disbursement in the general account records for the difference.

(iv) Accepted/Discharged: Positive File Variance (“Overpaid”)

Any overpayment for accepted/discharged status which originated from the trust account must be re-deposited to the trust account. This can be accomplished in one of two ways:

(a) A cheque can be written from the firm general account and deposited to

the trust account for the amount of funds to be returned to trust.

Remember that if part of the overpayment has been offset by a rejection fee where the rejection was the result of the lawyer’s error, the rejection fee must be added back to ensure the client is not charged for the fee.

(b) If TPR’s dollar amount threshold of $100 or more is met, a refund may be

requested from TPR. When the refund cheque is received, the cheque must be deposited to the trust account.

HOWEVER, if a refund request is planned but the firm cannot send in the request to TPR by no later than the day after the CFR is received by the firm, then method (a) above must be followed. If a refund is later requested and the funds have already been returned to the trust account, the refund can be deposited directly to the general account.

Page 9 of 9

If the Funds Originated from the General Account…. Consistent with any other disbursement incurred on behalf of the client where trust funds were not used, the CFR may document a file variance that is a general account disbursement. In such a circumstance, the difference would be documented in the firm general account records and recovered under a Statement of Account rendered to the client. Once again, beware of the rejection fee that resulted from the lawyer’s error, as these are not to be charged to the client.

How to Read your New TPR eRDA

The previous paper Registrations Detail Application (RDA) for registering documents

Contact

Information

Accounting Information

Internal Use

Area/Rejection

Information

Registration

Details

Appendix 1

How to Read your New TPR eRDA

Contact

Information

Internal Use

Area/Rejection

Information

Here is your new eRDA for Registrations!

Registration

Details

Accounting

Information

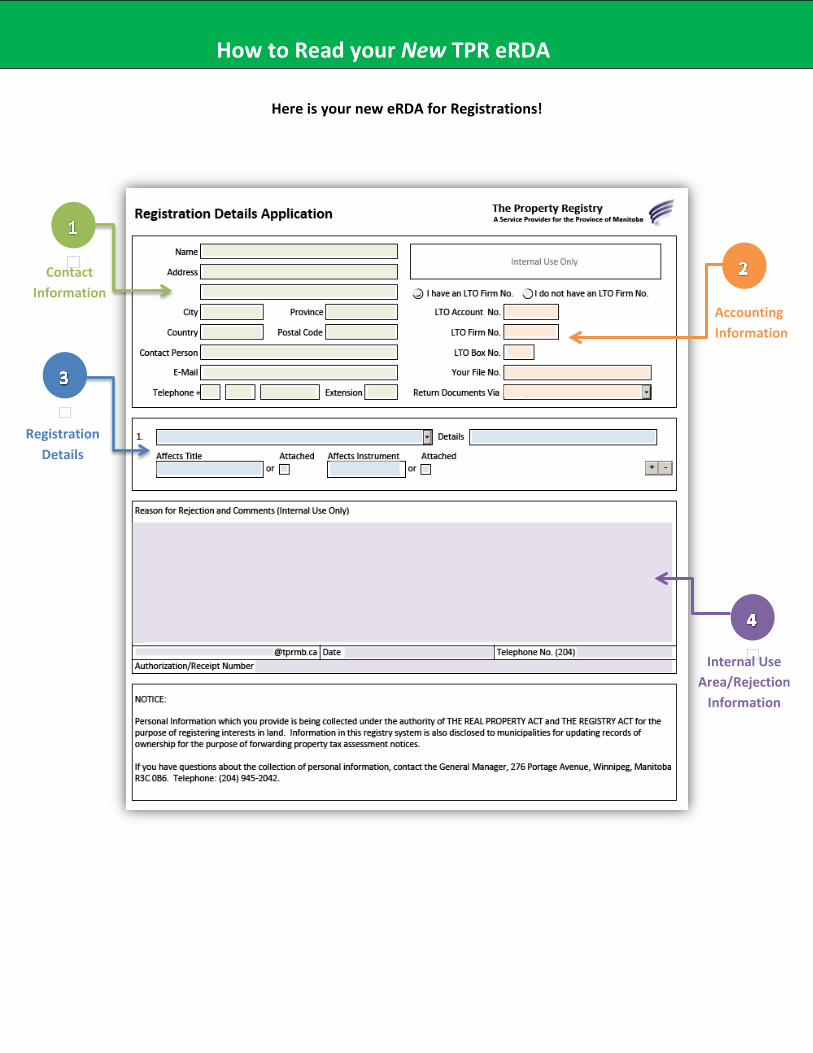

How to Read your New TPR eReceipt

Your receipt was The yellow copy of the Registrations Detail Application (RDA.)

ABC Law Inc.

125 Main Street Winnipeg, MB

9999 88888

R1R 1R1

204-123-4567

125489614478AZ

Transfer Mortgage

7654321/1 1234567/1 7654322/1 issuing

2635 85 2720-

610

Mortgage Upon acceptance 16

16

Registering

Party Details

Account Number

Firm

Number

Client File

Number

Fees

Registration

Details and

Copy upon

Completion

Requests

Payment

Details

Receipt #:R102771 Account #: 9999 Firm #: 88888

1.T1 7654321/1 $85.00 2015-08-20 12:10PM – R102771 2.LTAX 7654321/1 $2550.00 2015-08-20 12:10PM – R102771 3.M 7654322/1 $85.00 2015-08-20 12:10PM – R102771 4.610 S26932 $16.00 2015-08-20 12:10PM – R102771

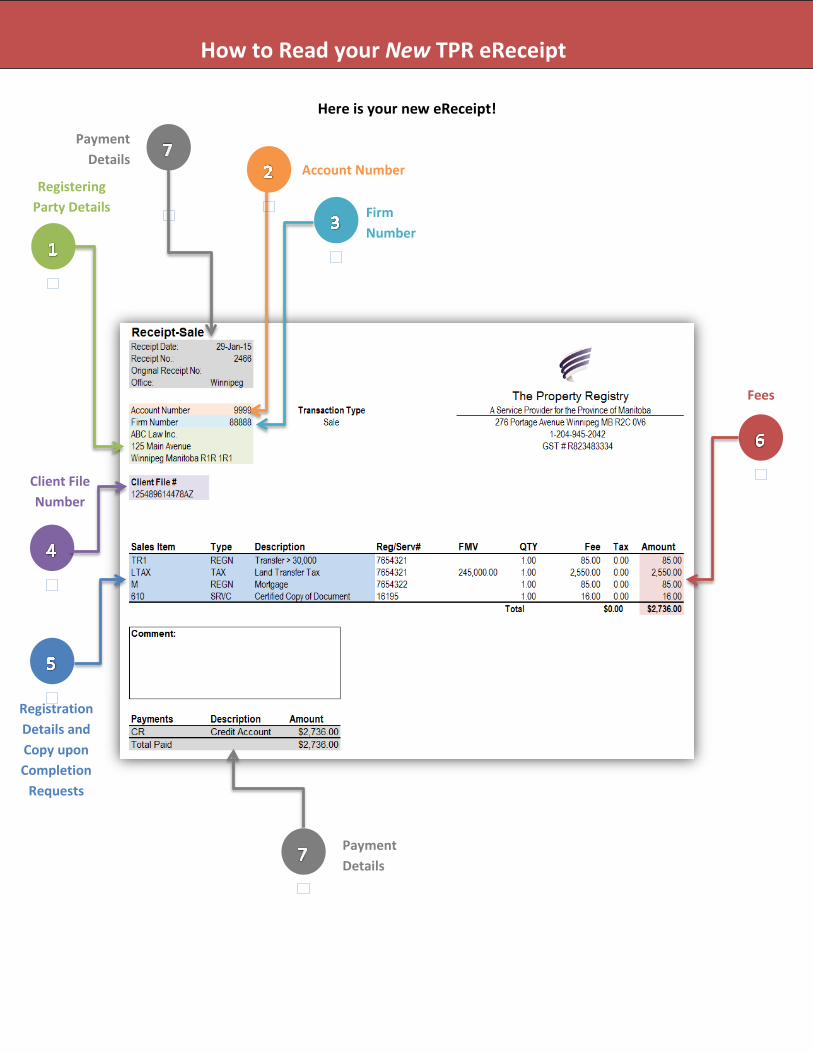

How to Read your New TPR eReceipt

Here is your new eReceipt!

Registration

Details and

Copy upon

Completion

Requests

Account Number

Firm

Number

Client File

Number

Registering

Party Details

Fees

Payment

Details

Payment

Details

How to Read your Client File Report

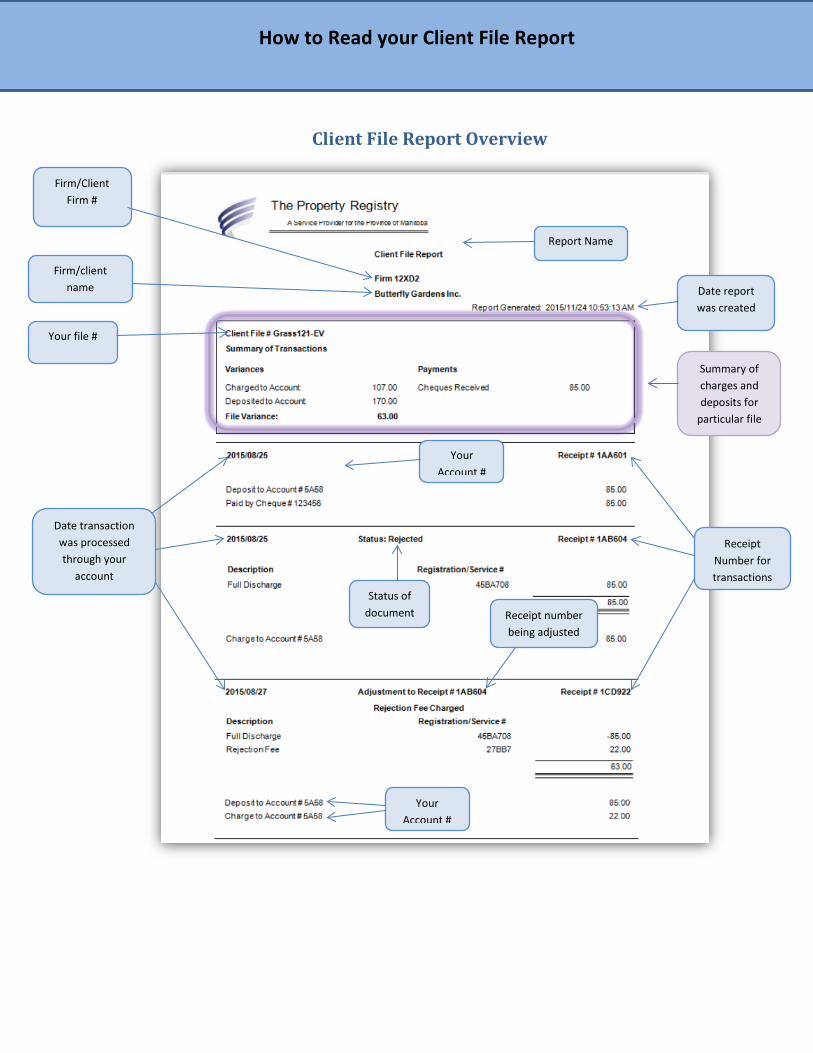

Client File Report Overview

Your file #

Report Name

Date transaction was processed through your

account

Firm/client name

Receipt Number for transactions

Date report was created

Status of document

Firm/Client Firm #

Your Account #

Receipt number being adjusted

Summary of charges and deposits for

particular file

Your Account #

How to Read your Client File Report

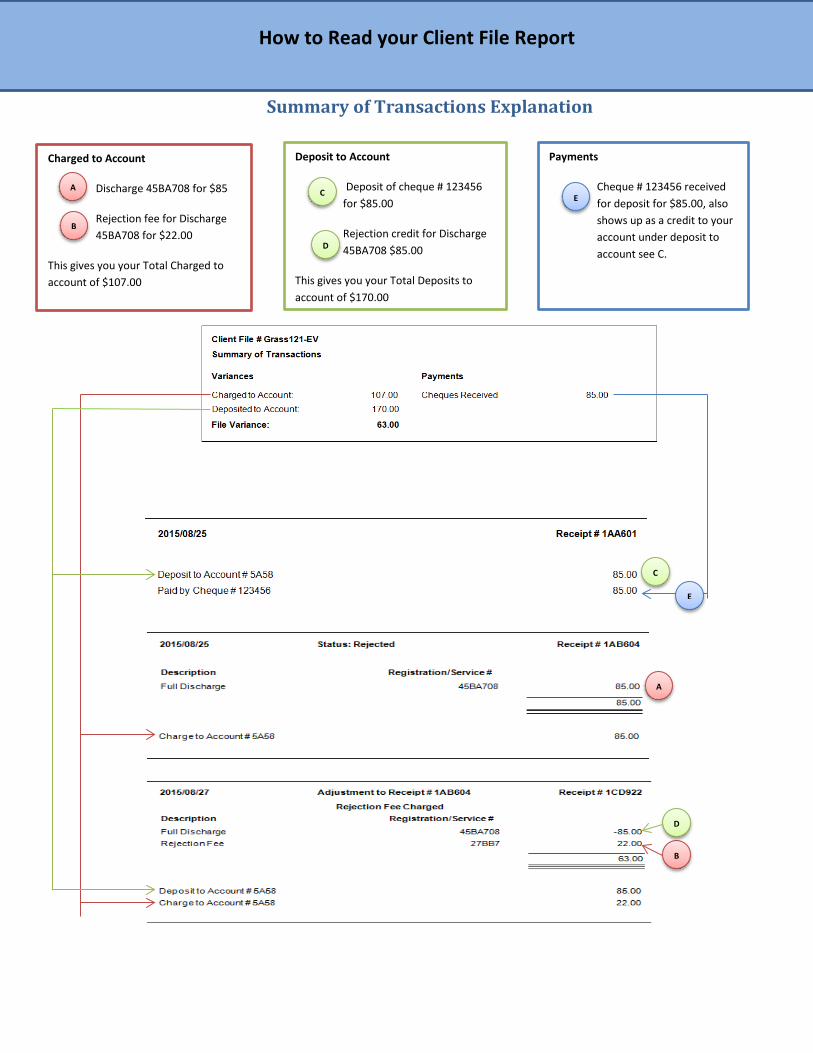

Summary of Transactions Explanation

Payments

Cheque # 123456 received for deposit for $85.00, also shows up as a credit to your account under deposit to account see C.

Charged to Account

Discharge 45BA708 for $85

Rejection fee for Discharge 45BA708 for $22.00

This gives you your Total Charged to account of $107.00

Deposit to Account

Deposit of cheque # 123456 for $85.00

Rejection credit for Discharge 45BA708 $85.00

This gives you your Total Deposits to account of $170.00

A

A

B

B

C

D

C

D

E

E

Appendix 2

Appendix 3A

Appendix 3B